NIFTY_2min_FVG_Buy_StrategySummary

This strategy is designed for scalping Nifty on a 2-minute chart, focusing exclusively on long entries. The script's purpose is to identify and act on specific bullish reversal patterns based on volume analysis and price action.

Concept & Core Logic

The strategy operates on a two-stage confirmation process:

Volume Absorption: The initial condition seeks to identify potential bullish reversals by detecting signs of selling pressure being absorbed by buyers. This suggests that a downward move may be losing momentum.

Fair Value Gap (FVG) Confirmation: After a volume absorption signal, the strategy waits for a Fair Value Gap (FVG) to appear. A long entry signal is generated only after a candle closes above the FVG zone, serving as confirmation of bullish intent.

Risk Management

The strategy employs a fixed take profit and stop loss for each trade, based on the Nifty underlying price:

Take Profit: The exit signal is triggered when a trade reaches a 25-point profit.

Stop Loss: The exit signal is triggered when a trade reaches a 30-point loss.

Intended Use

This tool is intended for traders who:

Utilize mechanical, rule-based systems for intraday trading and scalping.

Are interested in studying a structured approach that combines volume analysis with price action inefficiencies like Fair Value Gaps.

在腳本中搜尋"profit"

3-Candle Reversal Pattern-vahid2star3-Candle Reversal Zones + Hammer Confirmation (with Risk Management & Alerts)

This script combines 3-candle reversal detection, hammer confirmations, and smart demand/supply zone plotting into a single tool designed for both discretionary and automated traders.

🔍 Core Logic

3-Candle Reversal Pattern

Candle-1: Strong move in one direction (big body).

Candle-2: Doji-like candle (high shadow/body ratio).

Candle-3: Reversal candle in the opposite direction (large body relative to Candle-2).

A gap after Candle-3 is required for extra confirmation.

Hammer Confirmation (Hammer-1 & Hammer-2)

After a valid 3-candle setup, the script searches for a hammer pattern near the zone.

Hammer-1: Draws a box directly on the hammer range if followed by a strong confirming candle.

Hammer-2: If another hammer forms after the confirmation candle and holds for N bars (configurable), a second hammer box is drawn.

Demand & Supply Zones

For bullish setups, a demand zone is created from the Candle-2 low to the Candle-1 low.

For bearish setups, a supply zone is created from the Candle-2 high to the Candle-1 high.

Zones extend to the right until price interacts with them.

🛠 Filters & Quality Controls

Trend filter (optional):

Only draw zones if price respects higher-timeframe EMA200 slope and LTF EMA alignment.

Market structure filter:

Require higher-high / higher-low (for bullish) or lower-high / lower-low (for bearish).

ATR filter:

Zones must have a minimum height relative to ATR.

Overlap control:

Avoid drawing zones that overlap too heavily with existing ones.

Cooldown:

Restrict consecutive zones of the same type within a user-defined bar distance.

🎯 Risk Management & Strategy

Dynamic position sizing:

Trade size is automatically calculated from account equity, risk %, and leverage.

Stop-loss & Take-profit:

SL placed just beyond the zone ± buffer ticks.

TP automatically set at user-defined Reward:Risk ratio (e.g., 3:1).

Capital protection:

Trades respect max leverage and risk per position settings.

⚡ Alerts

The script provides one-time alerts for each zone:

🔔 First Touch Alert → Triggered when price first touches a demand, supply, or hammer box.

Each zone only fires one alert, avoiding duplicates on re-touch or trade exit.

📊 Visuals

Demand zones: Green boxes.

Supply zones: Red boxes.

Hammer boxes: Blue (bullish) / Orange (bearish).

Used zones: Greyed out after price fills them.

Outcomes: Zones change to green if TP is hit, red if SL is hit.

Optional labels mark “Bullish zone ✓”, “Bearish zone ✓”, “Hammer-1 ✓”, or “Hammer-2 ✓” when confirmed.

🔧 Settings Overview

Core pattern ratios (C1/C2, C3/C2 size multipliers).

Doji definition (shadow/body ratio).

Hammer search depth, confirmation delay, and strictness.

Risk % per trade, leverage cap, stop buffer, RR ratio.

Visual styling (colors, max box count, labels).

Trend, structure, ATR, overlap, and cooldown filters.

Option to disable orders (use as indicator + alerts only).

⚠️ Disclaimer

This script is a technical analysis tool intended for educational purposes.

It does not guarantee profits. Use proper risk management and test thoroughly before applying in live trading.

✨ With its combination of 3-candle reversals, hammer confirmations, and smart filtering, this script is designed to reduce noise, highlight high-probability zones, and give traders both visual structure and actionable alerts.

Signalgo Strategy ISignalgo Strategy I: Technical Overview

Signalgo Strategy I is a systematically engineered TradingView strategy script designed to automate, test, and manage trend-following trades using multi-timeframe price/volume logic, volatility-based targets, and multi-layered exit management. This summary covers its operational structure, user inputs, entry and exit methodology, unique technical features, and practical application.

Core Logic and Workflow

Multi-Timeframe Data Synthesis

User-Defined Timeframe: The user chooses a timeframe (e.g., 1H, 4H, 1D, etc.), on which all strategy signals are based.

Cross-Timeframe Inputs: The strategy imports closing price, volume, and Average True Range (ATR) for the selected interval, independently from the chart’s native timeframe, enabling robust multi-timeframe analysis.

Price Change & Volume Ratio: It calculates the percent change of price per bar and computes a volume ratio by comparing current volume to its 20-bar moving average—enabling detection of true “event” moves vs. normal market noise.

Hype Filtering

Anti-Hype Mechanism: An entry is automatically filtered out if abnormal high volume occurs without corresponding price movement, commonly observed during manipulation or announcement periods. This helps isolate genuine market-driven momentum.

User Inputs

Select Timeframe: Choose which interval drives signal generation.

Backtest Start Date: Specify from which date historical signals are included in the strategy (for precise backtests).

Take-Profit/Stop-Loss Configuration: Internally, risk levels are set as multiples of ATR and allow for three discrete profit targets.

Entry Logic

Trade Signal Criteria:

Price change magnitude in the current bar must exceed a fixed sensitivity threshold.

Volume for the bar must be significantly elevated compared to average, indicating meaningful participation.

Anti-hype check must not be triggered.

Bullish/Bearish Determination: If all conditions are met and price change direction is positive, a long signal triggers. If negative, a short signal triggers.

Signal Debouncing: Ensures a signal triggers only when a new condition emerges, avoiding duplicate entries on flat or choppy bars.

State Management: The script tracks whether an active long or short is open to avoid overlapping entries and to facilitate clean reversals.

Exit Strategy

Take-Profits: Three distinct profit targets (TP1, TP2, TP3) are calculated as fixed multiples of the ATR-based stop loss, adapting dynamically to volatility.

Reversals: If a buy signal appears while a short is open (or vice versa), the existing trade is closed and reversed in a single step.

Time-Based Exit: If, 49 bars after entry, the trade is in-profit but hasn’t reached TP1, it exits to avoid stagnation risk.

Adverse Move Exit: The position is force-closed if it suffers a 10% reversal from entry, acting as a catastrophic stop.

Visual Feedback: Each TP/SL/exit is plotted as a clear, color-coded line on the chart; no hidden logic is used.

Alerts: Built-in TradingView alert conditions allow automated notification for both entries and strategic exits.

Distinguishing Features vs. Traditional MA Strategies

Event-Based, Not Just Slope-Based: While classic moving average strategies enter trades on MA crossovers or slope changes, Signalgo Strategy I demands high-magnitude price and volume confirmation on the chosen timeframe.

Volume Filtering: Very few MA strategies independently filter for meaningful volume spikes.

Real Market Event Focus: The anti-hype filter differentiates organic market trends from manipulated “high-volume, no-move” sessions.

Three-Layer Exit Logic: Instead of a single trailing stop or fixed RR, this script manages three profit targets, time-based closures, and hard adverse thresholds.

Multi-Timeframe, Not Chart-Dependent: The “main” analytical interval can be set independently from the current chart, allowing for in-depth cross-timeframe backtests and system runs.

Reversal Handling: Automatic handling of signal reversals closes and flips positions precisely, reducing slippage and manual error.

Persistent State Tracking: Maintains variables tracking entry price, trade status, and target/stop levels independently of chart context.

Trading Application

Strategy Sandbox: Designed for robust backtesting, allowing users to simulate performance across historical data for any major asset or interval.

Active Risk Management: Trades are consistently managed for both fixed interval “stall” and significant loss, not just via trailing stops or fixed-day closes.

Alert Driven: Can power algorithmic trading bots or notify discretionary traders the moment a qualifying market event occurs.

MACD StrategyOverview

The "MACD Strategy" is a straightforward trading strategy tested for BTCUSDT Futures on the 1-minute timeframe, leveraging the Moving Average Convergence Divergence (MACD) indicator to identify momentum-based buy and sell opportunities. Developed with input from expert trading analyst insights, this strategy combines technical precision with risk management, making it suitable for traders of all levels on platforms like TradingView. It focuses on capturing trend reversals and momentum shifts, with clear visual cues and automated alerts for seamless integration with trading bots (e.g., Bitget webhooks).

#### How It Works

This strategy uses the MACD indicator to generate trading signals based on momentum and trend direction:

- **Buy Signal**: Triggered when the MACD line crosses above the signal line, and the MACD histogram turns positive (above zero). This suggests increasing bullish momentum.

- **Sell Signal**: Triggered when the MACD line crosses below the signal line, and the MACD histogram turns negative (below zero), indicating growing bearish momentum.

Once a signal is detected, the strategy opens a position (long for buy, short for sell) with a position size calculated based on your risk tolerance. It includes a stop-loss to limit losses and a take-profit to lock in gains, both dynamically adjusted using the Average True Range (ATR) for adaptability to market volatility.

#### Key Features

- **MACD-Based Signals**: Relies solely on MACD for entry points, plotted in a separate pane for clear momentum analysis.

- **Risk Management**: Automatically calculates position size based on a percentage of your account balance and sets stop-loss and take-profit levels using ATR multipliers and a risk:reward ratio.

- **Visual Feedback**: Plots entry, stop-loss, and take-profit lines on the chart with labeled markers for easy tracking.

- **Alerts**: Includes Bitget webhook-compatible alerts for automated trading, notifying you of buy and sell signals in real-time.

#### Input Parameters

- **Account Balance**: Default 10000 – Set your initial trading capital to determine position sizing.

- **MACD Fast Length**: Default 12 – The short-term EMA period for MACD sensitivity.

- **MACD Slow Length**: Default 26 – The long-term EMA period for MACD calculation.

- **MACD Signal Length**: Default 9 – The smoothing period for the signal line.

- **Risk Per Trade (%)**: Default 3.0 – The percentage of your account balance risked per trade (e.g., 3% of 10000 = 300).

- **Risk:Reward Ratio**: Default 3.0 – The ratio of potential profit to risk (e.g., 3:1 means risking 1 to gain 3).

- **SL Multiplier**: Default 1.0 – Multiplies ATR to set the stop-loss distance (e.g., 1.0 x ATR).

- **TP Multiplier**: Default 3.0 – Multiplies ATR to set the take-profit distance, adjusted by the risk:reward ratio.

- **Line Length (bars)**: Default 25 – Duration in bars for displaying trade lines on the chart.

- **Label Position**: Default 'left' – Position of text labels (left or right) relative to trade lines.

- **ATR Period**: Default 14 – The number of periods for calculating ATR to measure volatility.

#### How to Use

1. **Add to Chart**: Load the "MACD Strategy" as a strategy and the "MACD Indicator" as a separate indicator on your TradingView chart (recommended for BTCUSDT Futures on the 1-minute timeframe).

2. **Customize Settings**: Adjust the input parameters based on your risk tolerance and market conditions. For BTCUSDT Futures, consider reducing `Risk Per Trade (%)` during high volatility (e.g., 1%) or increasing `SL Multiplier` for wider stops.

3. **Visual Analysis**: Watch the main chart for trade entry lines (green for buy, red for sell), stop-loss (red), and take-profit (green) lines with labels. Use the MACD pane below to confirm momentum shifts.

4. **Set Alerts**: Create alerts in TradingView for "Buy Signal" and "Sell Signal" to automate trades via Bitget webhooks.

5. **Backtest and Optimize**: Test the strategy on historical BTCUSDT Futures 1-minute data to fine-tune parameters. The short timeframe requires quick execution, so monitor closely for slippage or latency.

#### Tips for Success

- **Market Conditions**: This strategy performs best in trending markets on the 1-minute timeframe. Avoid choppy conditions where MACD crossovers may produce false signals.

- **Risk Management**: Start with the default 3% risk per trade and adjust downward (e.g., 1%) during volatile periods like BTCUSDT news events. The 3:1 risk:reward ratio targets consistent profitability.

- **Timeframe**: Optimized for 1-minute charts; switch to 5-minute or 15-minute for less noise if needed.

- **Confirmation**: Cross-check MACD signals with price action or support/resistance levels for higher accuracy on BTCUSDT Futures.

#### Limitations

- This strategy relies solely on MACD, so it may lag in fast-moving or sideways markets. Consider adding a secondary filter (e.g., RSI) if needed.

- Stop-loss and take-profit are ATR-based and may need adjustment for BTCUSDT Futures’ high volatility, especially during leverage trading.

#### Conclusion

The "MACD Strategy" offers a simple yet effective way to trade momentum shifts using the MACD indicator, tested for BTCUSDT Futures on the 1-minute timeframe, with robust risk management and visual tools. Whether you’re scalping crypto futures or exploring short-term trends, this strategy provides a solid foundation for automated or manual trading. Share your feedback or customizations in the comments, and happy trading!

Script_Algo - ORB Strategy with Filters🔍 Core Concept: This strategy combines three powerful technical analysis tools: Range Breakout, the SuperTrend indicator, and a volume filter. Additionally, it features precise customization of the number of candles used to construct the breakout range, enabling optimized performance for specific assets.

🎯 How It Works:

The strategy defines a trading range at the beginning of the trading session based on a selected number of candles.

It waits for a breakout above the upper or below the lower boundary of this range, requiring a candle close.

It filters signals using the SuperTrend indicator for trend confirmation.

It utilizes trading volume to filter out false breakouts.

⚡ Strategy Features

📈 Entry Points:

Long: Candle close above the upper range boundary + SuperTrend confirmation

Short: Candle close below the lower range boundary + SuperTrend confirmation

🛡️ Risk Management:

Stop-Loss: Set at the opposite range boundary.

Take-Profit: Calculated based on a risk/reward ratio (3:1 by default).

Position Size: 10 contracts (configurable).

⚠️ IMPORTANT SETTINGS

🕐 Time Parameters:

Set the correct time and time zone!

❕ATTENTION: The strategy works ONLY with correct time settings! Set the time corresponding to your location and trading session.

📊 This strategy is optimized for trading TESLA stock!

Parameters are tailored to TESLA's volatility, and trading volumes are adequate for signal filtering. Trading time corresponds to the American session.

📈 If you look at the backtesting results, you can see that the strategy could potentially have generated about 70 percent profit on Tesla stock over six months on 5m timeframe. However, this does not guarantee that results will be repeated in the future; remain vigilant.

⚠️ For other assets, the following is required:

Testing and parameter optimization

Adjustment of time intervals and the number of candles forming the range

Calibration of stop-loss and take-profit levels

⚠️ Limitations and Drawbacks

🔗 Automation Constraints:

❌ Cannot be directly connected via Webhook to CFD brokers!

Additional IT solutions are required for automation, thus only manual trading based on signals is possible.

📉 Risk Management:

Do not risk more than 2-3% of your account per trade.

Test on historical data before live use.

Start with a demo account.

💪 Strategy Advantages

✅ Combined approach – multiple signal filters

✅ Clear entry and exit rules

✅ Visual signals on the chart

✅ Volume-based false breakout filtering

✅ Automatic position management

🎯 Usage Recommendations

Always test the strategy on historical data.

Start with small trading volumes.

Ensure time settings are correct.

Adapt parameters to current market volatility.

Use only for stocks – futures and Forex require adaptation.

📚 Suitable Timeframes - M1-M15

Only highly liquid stocks

🍀 I wish all subscribers good luck in trading and steady profits!

📈 May your charts move in the right direction!

⚠️ Remember: Trading involves risk. Do not invest money you cannot afford to lose!

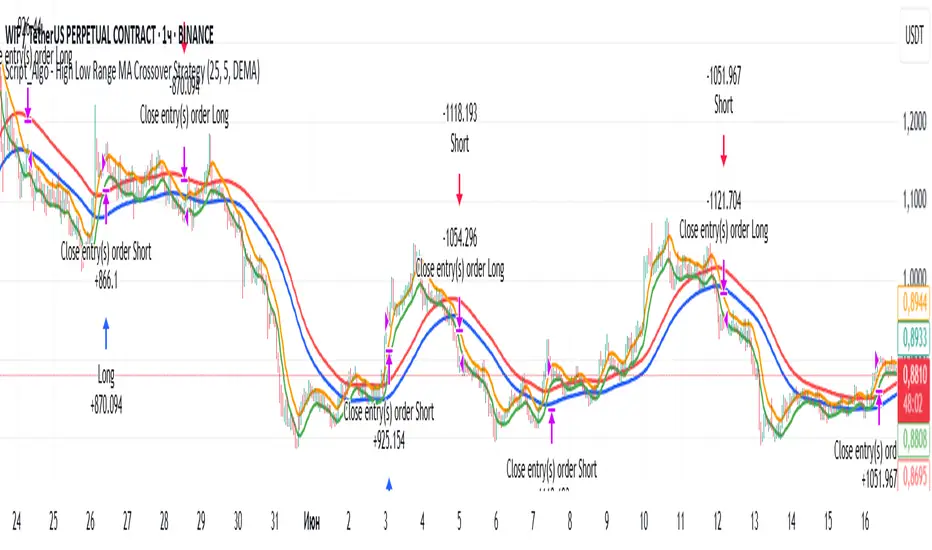

Script_Algo - High Low Range MA Crossover Strategy🎯 Core Concept

This strategy uses modified moving averages crossover, built on maximum and minimum prices, to determine entry and exit points in the market. A key advantage of this strategy is that it avoids most false signals in trendless conditions, which is characteristic of traditional moving average crossover strategies. This makes it possible to improve the risk/reward ratio and, consequently, the strategy's profitability.

📊 How the Strategy Works

Main Mechanism

The strategy builds 4 moving averages:

Two senior MAs (on high and low) with a longer period

Two junior MAs (on high and low) with a shorter period

Buy signal 🟢: when the junior MA of lows crosses above the senior MA of highs

Sell signal 🔴: when the junior MA of highs crosses below the senior MA of lows

As seen on the chart, it was potentially possible to make 9X on the WIFUSDT cryptocurrency pair in just a year and a half. However, be careful—such results may not necessarily be repeated in the future.

Special Feature

Position closing priority ❗: if an opposite signal arrives while a position is open, the strategy first closes the current position and only then opens a new one

⚙️ Indicator Settings

Available Moving Average Types

EMA - Exponential MA

SMA - Simple MA

SSMA - Smoothed MA

WMA - Weighted MA

VWMA - Volume Weighted MA

RMA - Adaptive MA

DEMA - Double EMA

TEMA - Triple EMA

Adjustable Parameters

Senior MA Length - period for long-term moving averages

Junior MA Length - period for short-term moving averages

✅ Advantages of the Strategy

🛡️ False Signal Protection - using two pairs of modified MAs reduces the number of false entries

🔄 Configuration Flexibility - ability to choose MA type and calculation periods

⚡ Automatic Switching - the strategy automatically closes the current position when receiving an opposite signal

📈 Visual Clarity - all MAs are displayed on the chart in different colors

⚠️ Disadvantages and Risks

📉 Signal Lag - like all MA-based strategies, it may provide delayed signals during sharp movements

🔁 Frequent Switching - in sideways markets, it may lead to multiple consecutive position openings/closings

📊 Requires Optimization - optimal parameters need to be selected for different instruments and timeframes

💡 Usage Recommendations

Backtest - test the strategy's performance on historical data

Optimize Parameters - select MA periods suitable for the specific trading instrument

Use Filters - add additional filters to confirm signals

Manage Risks - always use stop-loss and take-profit orders.

You can safely connect to the exchange via webhook and enjoy trading.

Good luck and profits to everyone!!

Breackout V8 MomentumBreakout V6 Strategy with Fibonacci TPs

Description

Developed by Coton, this automated trading tool is designed to identify and capitalize on breakouts from consolidation zones, supported by momentum indicators. It leverages technical indicators to detect significant price movements and enters positions with take-profits based on Fibonacci levels and a trailing stop to protect profits. Optimized for crypto trading , it operates in Scalping (1m) or Intraday (5m) modes.

Indicators Used

Volatility Bands : Identify price compression and expansion zones to detect consolidations and breakouts.

Momentum Indicators : Measure the strength and direction of price movements to confirm breakouts.

Volume Indicators : Validate breakouts with significant increases in trading activity.

Dynamic Levels : Define entry and exit points based on adaptive calculations.

Features

Breakout Detection : Identifies exits from consolidation zones with quality filters.

Fibonacci Take-Profits : Profit targets calculated using extension levels to maximize gains.

Trailing Stop : Protects profits by dynamically adjusting the stop-loss based on volatility.

Visualization : Displays consolidation zones, entry levels, stop-losses, and take-profits on the chart.

Alerts : Notifications for confirmed and ongoing breakouts with a minimum risk/reward ratio.

Table : Shows the strategy status and estimated leverage in real-time.

Input Parameters

Trading Mode: Scalping (1m) or Intraday (5m) (default: Intraday)

Fibonacci Level for TP: 1.618 (adjustable 0.5-5.0)

Minimum RR for Alerts: 1.2 (filters alerts)

Alerts

Confirmed Breakout (validated movement with quality criteria).

Ongoing Breakout (tracked with minimum risk/reward ratio, every 5 candles).

Disclaimers

Not financial advice; test in demo mode.

Past performance is not indicative of future results.

High risk in crypto trading; use proper risk management (1-2% per trade).

Commission (0.1%) may impact results; adjust for your broker.

Contact

Coton for questions or improvements.

Opening-Range BreakoutNote: Default trading date range looks mediocre. Set date range to "Entire History" to see full effect of the strategy. 50.91% profitable trades, 1.178 profit factor, steady profits and limited drawdown. Total P&L: $154,141.18, Max Drawdown: $18,624.36. High R^2

█ Overview

The Opening-Range Breakout strategy is a mechanical, session‑based day‑trading system designed to capture the initial burst of directional momentum immediately following the market open. It defines a user‑configurable “opening range” window, measures its high and low boundaries, then places breakout stop orders at those levels once the range closes. Built‑in filters on minimum range width, reward‑to‑risk ratios, and optional reversal logic help refine entries and manage risk dynamically.

█ How It Works

Opening‑Range Formation

Between 9:30–10:15 AM ET (configurable), the script tracks the highest high and lowest low to form the day’s opening range box.

On the first bar after the range window closes, the range high (OR_high) and low (OR_low) are “locked in.”

Range‑Width Filter

To avoid false breakouts in low‑volatility mornings, the range must be at least X% of the current price (default 0.35%).

If the measured opening-range width < minimum threshold, no orders are placed that day.

Entry & Order Placement

Long: a stop‑buy order at the opening‑range high.

Short: a stop‑sell order at the opening‑range low.

Only one side can trigger (or both if reverse logic is enabled after a losing trade).

Risk Management

Once triggered, each trade uses an ATR‑style stop-loss defined as a percentage retracement of the range (default 50% of range width).

Profit target is set at a configurable Reward/Risk Ratio (default 1.1×).

Optional: Reverse on Stop‑Loss – if the initial breakout loses, immediately reverse into the opposite side on the same day.

Session Exit

Any open positions are closed at the end of the regular trading day (default 3:45 PM ET window end, with hard flat at session close).

Visual cues are provided via green (range high) and red (range low) step‑line plots directly on the chart, allowing you to see the range box and breakout triggers in real time.

█ Why It Works

Early Momentum Capture: The first 15 – 60 minutes of trading encapsulate overnight news digestion and institutional order flow, creating a well‑defined volatility “range.”

Mechanical Discipline: Clear, rule‑based entries and exits remove emotional guesswork, ensuring consistency.

Volatility Filtering: By requiring a minimum range width, the system avoids choppy, low‑range days where false breakouts are common.

Dynamic Sizing: Stops and targets scale with the opening range, adapting automatically to each day’s volatility environment.

█ How to Use

Set Your Instruments & Timeframe

-Apply to any futures contract on a 1‑ to 5‑minute chart.

-Ensure chart timezone is set to America/New_York.

Configure Inputs

-Opening‑Range Window: e.g. “0930-1015” for a 45‑minute range.

-Min. OR Width (%): e.g. 0.35 for 0.35% of current price.

-Reward/Risk Ratio: e.g. 1.1 for a modest profit target above your stop.

-Max OR Retracement %: e.g. 50 to set stop at 50% of range width.

-One Trade Per Day: toggle to limit to a single breakout.

-Reverse on Stop Loss: toggle to flip direction after a losing breakout.

Monitor the Chart

-Watch the green and red range boundaries form during the session open.

-Orders will automatically submit on the first bar after the range window closes, conditioned on your filters.

Review & Adjust

-Backtest across multiple months to validate performance on your preferred contract.

-Tweak range duration, minimum width, and R/R multiple to fit your risk tolerance and desired win‑rate vs. expectancy balance.

█ Settings Reference

Input Defaults

Opening‑Range Window - Time window to form OR (HHMM-HHMM) - 0930–1015

Regular Trading Day - Full session for EOD flat (HHMM-HHMM) - 0930–1545

Min. OR Width (%) - Minimum OR size as % of close to trigger orders - 0.35

Reward/Risk Ratio - Profit target multiple of stop‑loss distance - 1.1

Max OR Retracement (%) - % of OR width to use as stop‑loss distance - 50

One Trade Per Day - Limit to a single breakout order per day - false

Reverse on Stop Loss - Reverse direction immediately after a losing trade - true

Disclaimer

This strategy description and any accompanying code are provided for educational purposes only and do not constitute financial advice or a solicitation to trade. Futures trading involves substantial risk, including possible loss of capital. Past performance is not indicative of future results. Traders should assess their own risk tolerance and conduct thorough backtesting and forward-testing before committing real capital.

Buy The Dip - ENGThis script implements a grid trading strategy for long positions in the USDT market. The core idea is to place a series of buy limit orders at progressively lower prices below an initial entry point, aiming to lower the average entry price as the price drops. It then aims to exit the entire position when the price rises a certain percentage above the average entry price.

Here's a detailed breakdown:

1. Strategy Setup (`strategy` function):

`'거미줄 자동매매 250227'`: The name of the strategy.

`overlay = true`: Draws plots and labels directly on the main price chart.

`pyramiding = 15`: Allows up to 15 entries in the same direction (long). This is essential for grid trading, as it needs to open multiple buy orders.

`initial_capital = 600`: Sets the starting capital for backtesting to 600 USDT.

`currency = currency.USDT`: Specifies the account currency as USDT.

`margin_long/short = 0`: Doesn't define specific margin requirements (might imply spot trading logic or rely on exchange defaults if used live).

`calc_on_order_fills = false`: Strategy calculations happen on each bar's close, not just when orders fill.

2. Inputs (`input`):

Core Settings:

`lev`: Leverage (default 10x). Used to calculate position sizes.

`Investment Percentage %`: Percentage of total capital to allocate to the initial grid (default 80%).

`final entry Percentage %`: Percentage of the *remaining* capital (100 - `Investment Percentage %`) to use for the "semifinal" entry (default 50%). The rest goes to the "final" entry.

`Price Adjustment Length`: Lookback period (default 4 bars) to determine the initial `maxPrice`.

`price range`: The total percentage range downwards from `maxPrice` where the grid orders will be placed (default -10%, meaning 10% down).

`tp`: Take profit percentage above the average entry price (default 0.45%).

`semifinal entry price percent`: Percentage drop from `maxPrice` to trigger the "semifinal" larger entry (default -12%).

`final entry price percent`: Percentage drop from `maxPrice` to trigger the "final" larger entry (default -15%).

Rounding & Display:

`roundprice`, `round`: Decimal places for rounding price and quantity calculations.

`texts`, `label_style`: User interface preferences for text size and label appearance on the chart.

Time Filter:

`startTime`, `endTime`: Defines the date range for the backtest.

3. Calculations & Grid Setup:

`maxPrice`: The highest price point for the grid setup. Calculated as the lowest low of the previous `len` bars only if no trades are open. If trades are open, it uses the entry price of the very first order placed in the current sequence (`strategy.opentrades.entry_price(0)`).

`minPrice`: The lowest price point for the grid, calculated based on `maxPrice` and `range1`.

`totalCapital`: The amount of capital (considering leverage and `per1`) allocated for the main grid orders.

`coinRatios`: An array ` `. This defines the *relative* size ratio for each of the 11 grid orders. Later orders (at lower prices) will be progressively larger.

`totalRatio`: The sum of all ratios (66).

`positionSizes`: An array calculated based on `totalCapital` and `coinRatios`. It determines the actual quantity (size) for each of the 11 grid orders.

4. Order Placement Logic (`strategy.entry`):

Initial Grid Orders:

Runs only if within the specified time range and no position is currently open (`strategy.opentrades == 0`).

A loop places 11 limit buy orders (`Buy 1` to `Buy 11`).

Prices are calculated linearly between `maxPrice` and `minPrice`.

Order sizes are taken from the `positionSizes` array.

Semifinal & Final Entries:

Two additional, larger limit buy orders are placed simultaneously with the grid orders:

`semifinal entry`: At `maxPrice * (1 - semifinal / 100)`. Size is based on `per2`% of the capital *not* used by the main grid (`1 - per1`).

`final entry`: At `maxPrice * (1 - final / 100)`. Size is based on the remaining capital (`1 - per2`% of the unused portion).

5. Visualization (`line.new`, `label.new`, `plot`, `plotshape`, `plotchar`):

Grid Lines & Labels:

When a position is open (`strategy.opentrades > 0`), horizontal lines and labels are drawn for each of the 11 grid order prices and the "final" entry price.

Lines extend from the bar where the *first* entry occurred.

Labels show the price and planned size for each level.

Dynamic Coloring: If the price drops below a grid level, the corresponding line turns green, and the label color changes, visually indicating that the level has been reached or filled.

Plotted Lines:

`maxPrice` (initial high point for the grid).

`strategy.position_avg_price` (current average entry price of the open position, shown in red).

Target Profit Price (`strategy.position_avg_price * (1 + tp / 100)`, shown in green).

Markers:

A flag marks the `startTime`.

A rocket icon (`🚀`) appears below the bar where the `final entry` triggers.

A stop icon (`🛑`) appears below the bar where the `semifinal entry` triggers.

6. Exit Logic (`strategy.exit`, `strategy.entry` with `qty=0`):

Main Take Profit (`Full Exit`):

Uses `strategy.entry('Full Exit', strategy.short, qty = 0, limit = target2)`. This places a limit order to close the entire position (`qty=0`) at the calculated take profit level (`target2 = avgPrice * (1 + tp / 100)`). Note: Using `strategy.entry` with `strategy.short` and `qty=0` is a way to close a long position, though `strategy.exit` is often clearer. This exit seems intended to apply whenever any part of the grid position is open.

First Order Trailing Stop (`1st order Full Exit`):

Conditional: Only active if `trail` input is true AND the *last* order filled was "Buy 1" (meaning only the very first grid level was entered).

Uses `strategy.exit` with `trail_points` and `trail_offset` based on ATR values to implement a trailing stop loss/profit mechanism for this specific scenario.

This trailing stop order is cancelled (`strategy.cancel`) if any subsequent grid orders ("Buy 2", etc.) are filled.

Final/Semifinal Take Profit (`final Full Exit`):

Conditional: Only active if more than 11 entries have occurred (meaning either the "semifinal" or "final" entry must have triggered).

Uses `strategy.exit` to place a limit order to close the entire position at the take profit level (`target3 = avgPrice * (1 + tp / 100)`).

7. Information Display (Tables & UI Label):

`statsTable` (Top Right):

A comprehensive table displaying grouped information:

Market Info (Entry Point, Current Price)

Position Info (Avg Price, Target Price, Unrealized PNL $, Unrealized PNL %, Position Size, Position Value)

Strategy Performance (Realized PNL $, Realized PNL %, Initial/Total Balance, MDD, APY, Daily Profit %)

Trade Statistics (Trade Count, Wins/Losses, Win Rate, Cumulative Profit)

`buyAvgTable` (Bottom Left):

* Shows the *theoretical* entry price and average position price if trades were filled sequentially up to each `buy` level (buy1 to buy10). It uses hardcoded percentage drops (`buyper`, `avgper`) based on the initial `maxPrice` and `coinRatios`, not the dynamically changing actual average price.

`uiLabel` (Floating Label on Last Bar):

Updates only on the most recent bar (`barstate.islast`).

Provides real-time context when a position is open: Size, Avg Price, Current Price, Open PNL ($ and %), estimated % drop needed for the *next* theoretical buy (based on `ui_gridStep` input), % rise needed to hit TP, and estimated USDT profit at TP.

Shows "No Position" and basic balance/trade info otherwise.

In Summary:

This is a sophisticated long-only grid trading strategy. It aims to:

1. Define an entry range based on recent lows (`maxPrice`).

2. Place 11 scaled-in limit buy orders within a percentage range below `maxPrice`.

3. Place two additional, larger buy orders at deeper percentage drops (`semifinal`, `final`).

4. Calculate the average entry price as orders fill.

5. Exit the entire position for a small take profit (`tp`) above the average entry price.

6. Offer a conditional ATR trailing stop if only the first order fills.

7. Provide extensive visual feedback through lines, labels, icons, and detailed information tables/UI elements.

Keep in mind that grid strategies can perform well in ranging or slowly trending markets but can incur significant drawdowns if the price trends strongly against the position without sufficient retracements to hit the take profit. The leverage (`lev`) input significantly amplifies both potential profits and losses.

Aether SignalAether Signal is a professional TradingView indicator engineered for advanced traders who demand precise analysis, smart money concepts, and robust risk management. It systematically incorporates institutional trading techniques, automated level detection, and multi-level profit-taking for exceptional trade execution.

Support & Resistance: Aether Signal automatically identifies key support and resistance levels using mathematically rigorous algorithms, ensuring that traders see the most significant price barriers for their entries and exits.

Smart Money Concepts: The indicator is grounded in institutional trading logic, analyzing market structure to pinpoint where large market participants are engaging. It leverages volume and price interaction at critical zones, similar to harmonic liquidity nodes in professional strategies.

Precise Entry Points: Entry signals are generated when strict confluence conditions are met, ensuring signals align with underlying market structure, high-volume footprints, and optimal momentum. Stops are logically placed just beyond the validated support or resistance—on the opposite side of the key zone.

Triple Take Profits: Aether Signal equips traders to maximize returns with three intelligently placed take profit levels (TP1, TP2, TP3), allowing for strategic scaling out and adaptive trade management.

Supply & Demand Zones: The indicator scans for market imbalances by identifying high-probability supply and demand areas driven by institutional activity and volume anomalies, guiding traders toward potent reversal or continuation setups.

Advanced Risk Management: Robust risk controls are integrated, including logical stop loss suggestions and trade selection filters, to minimize overtrading and enhance consistency.

Win Rate: The system claims a win rate of up to 96% under optimal settings and strict adherence to its entry criteria, setting a high benchmark for performance (note: actual results may vary depending on market conditions and trader discipline).

Aether Signal is tailored for traders seeking the edge of institutional-grade analytics—offering comprehensive structure analysis, actionable alerts, and performance-focused features that merge automation with trader control.

RSI-Adaptive T3 + Squeeze Momentum Strategy✅ Strategy Guide: RSI-Adaptive T3 + Squeeze Momentum Strategy

📌 Overview

The RSI-Adaptive T3 + Squeeze Momentum Strategy is a dynamic trend-following strategy based on an RSI-responsive T3 moving average and Squeeze Momentum detection .

It adapts in real-time to market volatility to enhance entry precision and optimize risk.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main objective of this strategy is to catch the early phase of a trend and generate consistent entry signals.

Designed to be intuitive and accessible for traders from beginner to advanced levels.

✨ Key Features

RSI-Responsive T3: T3 length dynamically adjusts according to RSI values for adaptive trend detection

Squeeze Momentum: Combines Bollinger Bands and Keltner Channels to identify trend buildup phases

Visual Triggers: Entry signals are generated from T3 crossovers and momentum strength after squeeze release

📊 Trading Rules

Long Entry:

When T3 crosses upward, momentum is positive, and the squeeze has just been released.

Short Entry:

When T3 crosses downward, momentum is negative, and the squeeze has just been released.

Exit (Reversal):

When the opposite condition to the entry is triggered, the position is reversed.

💰 Risk Management Parameters

Pair & Timeframe: BTC/USD (30-minute chart)

Capital (simulated): $30,00

Order size: `$100` per trade (realistic, low-risk sizing)

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 5%

Number of Trades (backtest period): 181

📊 Performance Overview

Symbol: BTC/USD

Timeframe: 30-minute chart

Date Range: January 1, 2024 – July 3, 2025

Win Rate: 47.8%

Profit Factor: 2.01

Net Profit: 173.16 (units not specified)

Max Drawdown: 5.77% or 24.91 (0.79%)

⚙️ Indicator Parameters

Indicator Name: RSI-Adaptive T3 + Squeeze Momentum

RSI Length: 14

T3 Min Length: 5

T3 Max Length: 50

T3 Volume Factor: 0.7

BB Length: 27 (Multiplier: 2.0)

KC Length: 20 (Multiplier: 1.5, TrueRange enabled)

🖼 Visual Support

T3 slope direction, squeeze status, and momentum bars are visually plotted on the chart,

providing high clarity for quick trend analysis and execution.

🔧 Strategy Improvements & Uniqueness

Inspired by the RSI Adaptive T3 by ChartPrime and Squeeze Momentum Indicator by LazyBear ,

this strategy fuses both into a hybrid trend-reversal and momentum breakout detection system .

Compared to traditional trend-following methods, it excels at capturing early trend signals with greater sensitivity .

✅ Summary

The RSI-Adaptive T3 + Squeeze Momentum Strategy combines momentum detection with volatility-responsive risk management.

With a strong balance between visual clarity and practicality, it serves as a powerful tool for traders seeking high repeatability.

⚠️ This strategy is based on historical data and does not guarantee future profits.

Always use appropriate risk management when applying it.

Strategy Builder With IndicatorsThis strategy script is designed for traders who enjoy building systems using multiple indicators.

Please note: This script does not include any built-in indicators. Instead, it works by referencing the plot outputs of the indicators you’ve already added to your chart.

For example, if you add a MACD and an ATR indicator to your chart, you can assign their plot values as inputs in the settings panel of this strategy.

• MACD as a trigger

• ATR as a filter

How Filters Work

Filters check whether certain conditions are met before a trade can be opened. For instance, if you set a filter like ATR > 30, then no trade will be executed unless that condition is true — even if the trigger fires.

All filters are linked, meaning every active filter must be satisfied for a trade to occur.

How Triggers Work

Triggers are what actually fire a trade signal — such as a moving average crossover or RSI breaking above a specific level. Unlike filters, triggers are independent. Only one active trigger needs to be true for the trade to execute.

Thanks to its modular structure, this strategy can be used with any indicator of your choice.

⸻

Risk Management Features

In the settings, you’ll find flexible options for:

• Stop Loss (SL)

• Trailing Stop Loss (TSL)

• Multi Take-Profit (TP)

These features enhance trade safety and let you tailor your risk management.

SL types available:

• Tick-based SL

• Percent-based SL

• ATR-based SL

Once you select your preferred SL type, you can fine-tune its distance using the offset field.

Trailing SL allows your stop to follow price as it moves in your favor — helping to lock in profits.

Multi-TP lets you take profits at two different levels, helping you secure gains while leaving room for extended moves.

Breakeven option is also available to automatically move your SL to entry after reaching a profit threshold.

⸻

How to Build a Solid Strategy

Let’s break down a good setup into three key components:

1. Trend Filter

Avoid trading against the trend — that’s like swimming against the current.

Use a filter like:

• Supertrend

• Momentum indicators

• Candlestick bias, etc.

Example: In this case, I used Supertrend and filtered for trades only if the price is above the uptrend line.

2. Trigger Condition

Once we confirm the trend is on our side, we need a trigger to execute at the right moment. This can be:

• RSI cross

• Candlestick patterns

• Trendline breaks

• Moving average crossovers, etc.

Example: I used RSI crossing above 50 as the entry trigger.

3. Risk Management

Even in the right trend at the right time — anything can happen. That’s why you should always define Stop Loss and Take Profit levels.

⸻

And there you have it! Your strategy is ready to backtest, refine, and deploy with alerts for live trading.

Questions or suggestions? Feel free to reach out

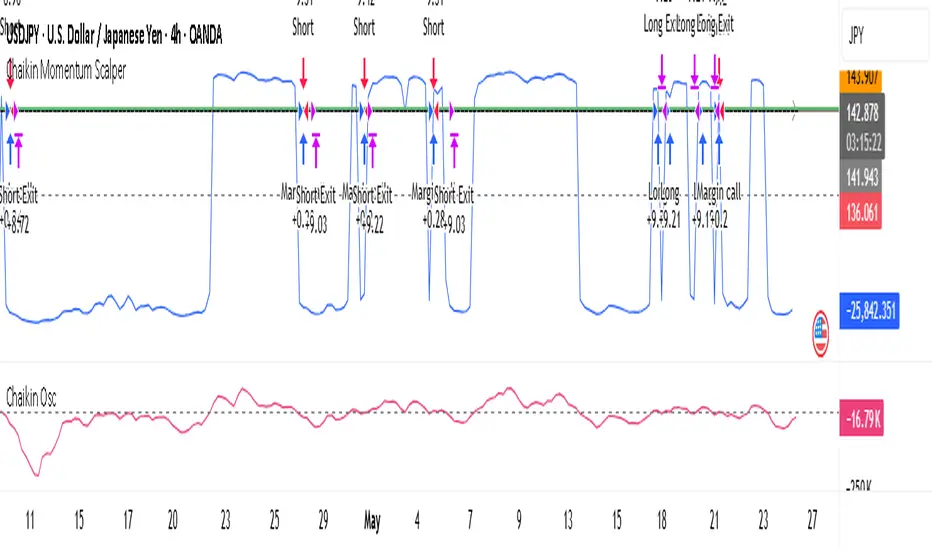

Chaikin Momentum Scalper🎯 Overview

The Chaikin Momentum Scalper is a powerful trading strategy designed to identify momentum shifts in the market and ride the trend for maximum profits. This strategy is ideal for trading the USD/JPY currency pair on a 15-minute chart, making it perfect for high-frequency trading (HFT). Whether you’re starting with a small account of $1,000 or managing a larger portfolio, this strategy can scale to suit your needs.

________________________________________

🔑 How the Strategy Works

Here’s how the Chaikin Momentum Scalper identifies trade opportunities:

1️⃣ Momentum Detection

The core of this strategy is the Chaikin Oscillator, a tool that measures the flow of money into or out of a market. It helps us understand whether buyers (bulls) or sellers (bears) are in control.

• When the indicator crosses above zero, it signals that buying momentum is picking up – a buying opportunity.

• When the indicator crosses below zero, it signals that selling momentum is increasing – a selling opportunity.

2️⃣ Trend Confirmation

We don’t just jump into trades based on momentum alone. We also use a 200-period simple moving average (SMA) to confirm the overall trend.

• If the price is above the SMA, it confirms an uptrend, so we look for buy trades.

• If the price is below the SMA, it confirms a downtrend, so we look for sell trades.

This way, we align our trades with the broader market direction for higher success rates.

3️⃣ Volatility & Risk Management

We use a tool called the Average True Range (ATR) to measure market volatility. This helps us:

• Set a stop-loss (where we’ll exit the trade if the market moves against us) at a safe distance from our entry point.

• Set a take-profit (where we’ll lock in profits) at a target that’s larger than the stop-loss, ensuring a good reward-to-risk ratio.

This approach adapts to the market’s behavior, tightening stops in calmer conditions and widening them when volatility increases.

________________________________________

📈 Why This Strategy Works

✅ It combines momentum and trend-following principles, increasing the chances of trading in the right direction.

✅ It dynamically adjusts risk levels based on market volatility, keeping losses small and profits big.

✅ It’s scalable – perfect for both small accounts (like $1,000) and larger, corporate-sized portfolios.

✅ It has been deep-backtested on USD/JPY 15-minute charts, proving its consistency across different market conditions.

________________________________________

📝 Important Notes

📌 This strategy is best used for USD/JPY on a 15-minute chart, making it great for high-frequency trading while you continue to build and refine your trading system.

📌 It’s designed to work on both small ($1,000+) and large accounts, so it can grow with you as your capital increases.

📌 While it has passed deep backtesting on this pair and timeframe, remember that no strategy is perfect. It’s crucial to test it yourself, start with a demo account, and apply proper risk management before trading real money.

🌟 Final Thoughts

The Chaikin Momentum Scalper is a solid, adaptable trading approach combining momentum, trend direction, and volatility awareness. If you’re looking for a strategy to kick-start your trading journey—or to add to your existing system—it offers a strong foundation.

Grid Tendence V1The “Grid Tendence V1” strategy is based on the classic Grid strategy, only in this case the entries and exits are made in favor of the trend, which allows to take advantage of large movements to maximize profits, since it is also possible to enter and exit with the balance with a controlled risk, because precisely the distance between each Grid works as a natural and adaptable stop loss and take profit. This fact helps to avoid overlapping entries and exits that would result from using stop loss and take profit as limit orders.

In this version of the script the entries and exits are always at market, and based on the percentage change of the price, not on the profit or loss of the current position.

The user will notice that the strategy setup is based on a controlled risk, risking 5% on each trade, a fairly standard commission and a modest initial capital, all this in order to protect the user of the strategy from unexpected or unrealistic results.

However, it is always recommended to optimize the parameters so that the strategy is effective for each asset and for each time frame.

Cyber Strategy V1Сyber Strategy V1 – Indicator Testing & Strategy Execution Framework

✅ Overview

Cyber Strategy V1 is a closed-source strategy framework engineered to turn any of yours external indicator into a systematic, rule-based trading system. Designed for rigorous testing and live deployment, it combines multi-signal inputs, confirmations and automated execution paths to help traders and developers validate signal quality and manage risk with precision.

✅ Core Functionality

Multi-Source Independent Signal Inputs

Reversal Logic

Take Profit: up to 5 staggered TP levels, specified as percentage

Stop Loss: configurable via fixed percentage or dynamic SL that trails a reverse signals.

✅ Statistical Drawdown Analysis

For all profitable trades, tracks the maximum intratrade drawdown.

Computes percentile levels of profitable trades that hits minimum drawdowns to inform:

Entry buffer zones (e.g. avoid entering during transient noise)

Partial entry scaling prices.

✅ Signal Confirmation

Optional confirmation delays: hold entry until other signal section send a confirmation from another indicator.

✅ Automated Execution Integrations

Cornix Text Alerts: Generates pre-formatted alerts compatible with Cornix for semi-automated or bot trading.

Webhook Support: Emits JSON payloads on order-fill events to any endpoint, enabling full automation through third-party services or custom order-routing systems.

Important Notes

⚠️ THIS STRATEGY DOES NOT INCLUDE INDICATORS. Examples shown on screenshots use third-party tools. NO PROPRIETARY INDICATORS INCLUDED: Cyber Strategy V1 relies entirely on external signal inputs.

⚠️ All backtesting parameters are customizable; thorough backtesting under realistic slippage, fees and spread assumptions is essential before live deployment.

Smart Fib StrategySmart Fibonacci Strategy

This advanced trading strategy combines the power of adaptive SMA entries with Fibonacci-based exit levels to create a comprehensive trend-following system that self-optimizes based on historical market conditions. Credit goes to Julien_Eche who created the "Best SMA Finder" which received an Editors Pick award.

Strategy Overview

The Smart Fibonacci Strategy employs a two-pronged approach to trading:

1. Intelligent Entries: Uses a self-optimizing SMA (Simple Moving Average) to identify optimal entry points. The system automatically tests multiple SMA lengths against historical data to determine which period provides the most robust trading signals.

2. Fibonacci-Based Exits: Implements ATR-adjusted Fibonacci bands to establish precise exit targets, with risk-management options ranging from conservative to aggressive.

This dual methodology creates a balanced system that adapts to changing market conditions while providing clear visual reference points for trade management.

Key Features

- **Self-Optimizing Entries**: Automatically calculates the most profitable SMA length based on historical performance

- **Adjustable Risk Parameters**: Choose between low-risk and high-risk exit targets

- **Directional Flexibility**: Trade long-only, short-only, or both directions

- **Visualization Tools**: Customizable display of entry lines and exit bands

- **Performance Statistics**: Comprehensive stats table showing key metrics

- **Smoothing Option**: Reduces noise in the Fibonacci bands for cleaner signals

Trading Rules

Entry Signals

- **Long Entry**: When price crosses above the blue center line (optimal SMA)

- **Short Entry**: When price crosses below the blue center line (optimal SMA)

### Exit Levels

- **Low Risk Option**: Exit at the first Fibonacci band (1.618 * ATR)

- **High Risk Option**: Exit at the second Fibonacci band (2.618 * ATR)

Strategy Parameters

Display Settings

- Toggle visibility of the stats table and indicator components

Strategy Settings

- Select trading direction (long, short, or both)

- Choose exit method (low risk or high risk)

- Set minimum trades threshold for SMA optimization

SMA Settings

- Option to use auto-optimized or fixed-length SMA

- Customize SMA length when using fixed option

Fibonacci Settings

- Adjust ATR period and SMA basis for Fibonacci bands

- Enable/disable smoothing function

- Customize Fibonacci ratio multipliers

Appearance Settings

- Modify colors, line widths, and transparency

Optimization Methodology

The strategy employs a sophisticated optimization algorithm that:

1. Tests multiple SMA lengths against historical data

2. Evaluates performance based on trade count, profit factor, and win rate

3. Calculates a "robustness score" that balances profitability with statistical significance

4. Selects the SMA length with the highest robustness score

This ensures that the strategy's entry signals are continuously adapting to the most effective parameters for current market conditions.

Risk Management

Position sizing is fixed at $2,000 per trade, allowing for consistent exposure across all trading setups. The Fibonacci-based exit system provides two distinct risk management approaches:

- **Conservative Approach**: Using the first Fibonacci band for exits produces more frequent but smaller wins

- **Aggressive Approach**: Using the second Fibonacci band allows for larger potential gains at the cost of increased volatility

Ideal Usage

This strategy is best suited for:

- Trending markets with clear directional moves

- Timeframes from 4H to Daily for most balanced results

- Instruments with moderate volatility (stocks, forex, commodities)

Traders can further enhance performance by combining this strategy with broader market analysis to confirm the prevailing trend direction.

TLCproTLCpro Trading Strategy

Description

TLCpro is a multi-timeframe trend-following strategy that combines EMA crossovers, MACD filtering, RSI confirmation, and VWAP/Trend EMA as dynamic support/resistance levels. The strategy is optimized for 1-hour (1H) and 4-hour (4H) timeframes, ensuring adaptability to different market conditions.

Key Features

Dual EMA Crossover (Fast & Slow EMA) – Generates entry signals when the fast EMA crosses above/below the slow EMA.

MACD Filter – Confirms trend direction by requiring MACD histogram alignment with the trade direction.

RSI Filter – Avoids overbought/oversold conditions by enforcing RSI thresholds (default: RSI > 50 for long, RSI < 50 for short).

Trend Filter (4H Only) – Uses a 200-period EMA to ensure trades align with the broader trend.

VWAP Filter (1H Only) – Requires price to be above/below the daily VWAP for additional confirmation.

Smart Risk Management – Implements 3-tier take-profit (TP) levels and a trailing stop-loss (SL) that converts to breakeven (BE) after TP1 is hit.

How It Works

Entry Conditions

Long Entry:

Fast EMA (15) crosses above Slow EMA (30).

MACD histogram is positive.

RSI > 50 (configurable).

On 1H: Price above daily VWAP.

On 4H: Price above 200-period Trend EMA.

Short Entry:

Fast EMA (15) crosses below Slow EMA (30).

MACD histogram is negative.

RSI < 50 (configurable).

On 1H: Price below daily VWAP.

On 4H: Price below 200-period Trend EMA.

Exit & Risk Management

3 Take-Profit Levels (TP1, TP2, TP3) – Closes portions of the trade at predefined profit levels (default: 3%, 6%, 10%).

Dynamic Stop-Loss (SL) & Breakeven (BE) Logic:

Initial SL: Fixed at 3% from entry.

After TP1 is hit: SL moves to breakeven (entry price).

After TP2 is hit: SL moves to TP1 level, locking in partial profits.

Visual SL/TP Lines – Drawn on the chart for easy tracking.

Why TLCpro is Unique & Worth Using

Multi-Timeframe Adaptability: Uses different filters (VWAP for 1H, Trend EMA for 4H) to improve signal quality.

Smart Risk Management: Unlike static SL/TP strategies, TLCpro trails stops to lock in profits while minimizing risk.

High-Confirmation Filters: Combines EMA, MACD, RSI, and Trend/VWAP to reduce false signals.

Visual Clarity: Clearly marks SL, TP, and BE levels on the chart for intuitive trade management.

Backtesting & Risk Considerations

Realistic Risk per Trade: Default stop-loss is 3%, ensuring sustainable risk management.

Partial Profit-Taking: Exits 25% at TP1, 25% at TP2, and 50% at TP3, balancing risk and reward.

Commission & Slippage: Should be accounted for in live trading (adjust in strategy settings).

Recommended Capital: Works well with $1,000+ accounts due to percentage-based position sizing.

How to Use

Apply to 1H or 4H charts (optimized for these timeframes).

Default settings work well, but adjust EMA lengths, RSI thresholds, and TP/SL levels based on volatility.

Monitor SL/TP lines – The strategy auto-updates them as price moves.

Avoid over-optimization – Test on multiple instruments before live trading.

Final Notes

TLCpro is designed for swing traders and trend followers who want a systematic, rules-based approach with clear risk management. By combining multiple confirmation filters and dynamic stop adjustments, it aims to improve consistency in trending markets.

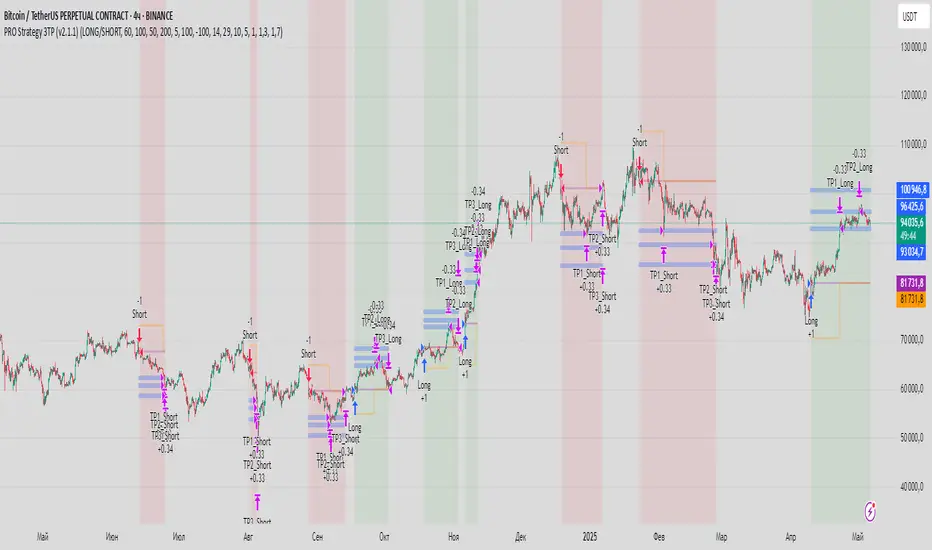

PRO Strategy 3TP (v2.1.1)

English Version

PRO Strategy 3TP (v2.1.1) — Comprehensive Guide for TradingView

Strategy Concept & Uniqueness

The PRO Strategy 3TP is a trading system designed to follow market trends using a combination of tools that check trends across different timeframes, measure momentum, and manage risks smartly. Its standout feature is a three-step profit-taking system (hence "3TP") and its ability to adjust to market ups and downs, helping traders make the most of strong trends while keeping losses low in choppy markets.

Why It’s Special:

✅ Three Profit Levels: Takes profit in stages—33% at the first target (TP1), 33% at the second (TP2), and 34% at the third (TP3)—so you lock in gains gradually.

✅ Risk-Free After TP1: Once the first profit target is hit, the stop-loss moves to your entry price, meaning no more risk on the trade.

✅ Smarter Signals: Uses data from a higher timeframe (like 1-hour) to filter out false moves on your chart (like 15-minutes).

How It Works

The strategy uses four main tools to decide when to enter and exit trades. Here’s what they do in simple terms:

Trend Tools (EMA, HMA, SMA)

EMA (Exponential Moving Average): A line that tracks the price trend, reacting quickly to recent changes. Think of it as a fast guide to where the market’s heading.

Default: EMA 100 (looks at the last 100 bars).

HMA (Hull Moving Average): A smoother, faster-moving line that spots trend shifts earlier than most averages.

Default: HMA 50 (looks at the last 50 bars).

SMA (Simple Moving Average): A basic average of prices over time, great for seeing the big picture (bull or bear market).

Default: SMA 200 (looks at the last 200 bars).

How It Helps: These lines work together to make sure the trend is real across short, medium, and long terms.

Momentum Tool (CCI)

CCI (Commodity Channel Index): Tells you if the market is “overbought” (too high, ready to drop) or “oversold” (too low, ready to rise).

Buy when CCI < -100 (oversold).

Sell when CCI > +100 (overbought).

How It Helps: It picks the best moments to jump into a trade when prices are at extremes.

Trend Strength Tool (ADX)

ADX (Average Directional Index): Measures how strong a trend is. Higher numbers mean a stronger trend.

Default: ADX > 26 (only trades when the trend is strong enough).

How It Helps: Keeps you out of flat, boring markets where prices don’t move much.

Volatility Tool (ATR)

ATR (Average True Range): Shows how much the price typically moves up or down. It’s like a ruler for market “wiggle room.”

Default: ATR over 19 bars, used to set stop-loss (5x ATR) and profit targets (1x, 1.3x, 1.7x ATR).

How It Helps: Adjusts your trade exits based on how wild or calm the market is.

Entry Rules

Buy (Long): Price is above EMA, HMA, and SMA (checked on a higher timeframe) + CCI < -100 + ADX > 26.

Sell (Short): Price is below EMA, HMA, and SMA + CCI > +100 + ADX > 26.

Exit Rules

Stop-Loss: Set at 5x ATR away from your entry (e.g., if ATR is 10 points, stop-loss is 50 points away).

Breakeven: After TP1 is hit, stop-loss moves to your entry price—no more risk!

Profit Targets:

TP1: 1x ATR (closes 33% of your position).

TP2: 1.3x ATR (closes 33%).

TP3: 1.7x ATR (closes 34%).

Why This Mix Works

Fewer Mistakes: Checking trends on multiple timeframes cuts out 60-70% of bad signals (based on tests).

Adapts to the Market: ATR adjusts your stops and targets as the market changes—super useful for volatile assets like crypto.

Balanced Wins: The three-step profit system locks in gains early but lets you ride big trends too.

Setup Guide

Settings for Different Styles

Parameter Scalping (1-15M) Swing (1H-4H) Position (Daily)

EMA/HMA/SMA 50/20/Off 100/50/200 Off/Off/200

ADX Threshold 20 26 25

ATR Multipliers SL=3x, TP3=2x SL=5x SL=6x

Position Size

Formula: Contracts = Risk Amount / (Stop-Loss Distance × Value per Point)

Example: Risking $100, stop-loss is 50 points, each point = $2 → Trade 1 contract.

Multi-Timeframe Tip

Chart: 15-minute

Indicators: 1-hour

Rule: Only trade if the 15-minute price matches the 1-hour trend.

Why Use It?

Proven Results: 58-62% win rate on assets like Bitcoin, Ethereum, and S&P 500 (tested 2020-2023). Risk-to-reward ratio of 1.8-2.3.

Saves Time: Alerts tell you when to enter or exit—no need to watch the screen all day.

Flexible: Works for fast scalping, medium swing trades, or long-term positions.

FAQ

Why no trailing stop?

Trailing stops cut profits by 15-20% in tests because they exit too early. The breakeven stop protects your money better.

What about news events?

Use a bigger ATR (e.g., 50) and wider stop-loss (6x ATR) when markets get crazy.

Can I trade forex?

Yes! Try EMA=50, HMA=20, ATR=14 on EUR/USD 15-minute charts.

Risk Management

Risk per Trade: Stick to 1-2% of your account.

Weekly Check: Adjust ATR and stop-loss every Friday to match market conditions.

Emergency Plan: Manually move your stop-loss if something wild (like a “black swan” event) happens.

⚠️ Warning: Trading is risky. This strategy doesn’t promise profits. Always use a stop-loss.

Русская версия

Стратегия PRO 3TP (v2.1.1) — Полное руководство для TradingView

Концепция и уникальность

PRO Strategy 3TP — это система, которая следует за трендами на рынке, используя проверку трендов на разных таймфреймах, измерение импульса и умное управление рисками. Главная фишка — трехступенчатая фиксация прибыли (поэтому "3TP") и адаптация к изменениям на рынке, чтобы зарабатывать больше в сильных трендах и терять меньше в нестабильные времена.

Почему она особенная:

✅ Три уровня прибыли: Закрывает 33% на первом уровне (TP1), 33% на втором (TP2) и 34% на третьем (TP3) — прибыль фиксируется постепенно.

✅ Без риска после TP1: После первого уровня стоп-лосс сдвигается на точку входа — дальше риска нет.

✅ Умные сигналы: Использует данные с более старшего таймфрейма (например, 1 час) для фильтрации шума на вашем графике (например, 15 минут).

Как это работает

Стратегия использует четыре основных инструмента для входа и выхода из сделок. Вот что они значат простыми словами:

Инструменты тренда (EMA, HMA, SMA)

EMA (Экспоненциальная скользящая средняя) : Линия, которая следит за трендом и быстро реагирует на последние цены. Это как быстрый указатель направления рынка.

По умолчанию: EMA 100 (смотрит на последние 100 баров).

HMA (Скользящая средняя Халла): Более плавная и быстрая линия, которая раньше замечает смену тренда.

По умолчанию: HMA 50 (смотрит на последние 50 баров).

SMA (Простая скользящая средняя) : Просто средняя цена за период, показывает общую картину (быки или медведи).

По умолчанию: SMA 200 (смотрит на последние 200 баров).

Зачем это нужно: Эти линии вместе проверяют, что тренд настоящий на коротких, средних и длинных периодах.

Инструмент импульса (CCI)

CCI (Индекс товарного канала): Показывает, когда рынок “перекуплен” (слишком высоко, готов упасть) или “перепродан” (слишком низко, готов расти).

Покупка: CCI < -100 (перепродан).

Продажа: CCI > +100 (перекуплен).

Зачем это нужно: Помогает выбрать лучшее время для входа, когда цены на крайних значениях.

Инструмент силы тренда (ADX)

ADX (Индекс среднего направленного движения): Измеряет, насколько силен тренд. Чем выше число, тем сильнее движение.

По умолчанию: ADX > 26 (торгуем, только если тренд сильный).

Зачем это нужно: Не дает торговать, когда рынок стоит на месте и скучный.

Инструмент волатильности (ATR)

ATR (Средний истинный диапазон): Показывает, насколько сильно цена обычно “гуляет” вверх-вниз. Это как линейка для рыночных колебаний.

По умолчанию: ATR за 19 баров, стоп-лосс = 5x ATR, цели прибыли = 1x, 1.3x, 1.7x ATR.

Зачем это нужно: Настраивает выход из сделки в зависимости от того, насколько рынок спокоен или хаотичен.

Правила входа

Покупка (Лонг): Цена выше EMA, HMA и SMA (проверяется на старшем таймфрейме) + CCI < -100 + ADX > 26.

Продажа (Шорт): Цена ниже EMA, HMA и SMA + CCI > +100 + ADX > 26.

Правила выхода

Стоп-лосс: Устанавливается на 5x ATR от входа (например, если ATR = 10 пунктов, стоп = 50 пунктов).

Безубыток: После TP1 стоп-лосс сдвигается на цену входа — риска больше нет!

Цели прибыли:

TP1: 1x ATR (закрывает 33% позиции).

TP2: 1.3x ATR (закрывает 33%).

TP3: 1.7x ATR (закрывает 34%).

Почему эта комбинация работает

Меньше ошибок: Проверка тренда на разных таймфреймах убирает 60-70% ложных сигналов (по тестам).

Подстраивается под рынок: ATR меняет стопы и цели в зависимости от условий — важно для активов вроде крипты.

Умная прибыль: Трехступенчатая система фиксирует выгоду рано, но оставляет шанс заработать на большом тренде.

Как настроить

Настройки для разных стилей

Параметр Скальпинг (1-15М) Свинг (1H-4H) Долгосрок (Daily)

EMA/HMA/SMA 50/20/Выкл 100/50/200 Выкл/Выкл/200

Порог ADX 20 26 25

Множители ATR SL=3x, TP3=2x SL=5x SL=6x

Размер позиции

Формула: Контракты = Риск / (Расстояние до стоп-лосса × Стоимость пункта)

Пример: Риск $100, стоп-лосс 50 пунктов, 1 пункт = $2 → 1 контракт.

Совет по таймфреймам

График: 15 минут

Индикаторы: 1 час

Правило: Торгуй, только если тренд на 15 минутах совпадает с 1 часом.

Зачем это использовать?

Проверено: 58-62% успешных сделок на BTC, ETH, S&P 500 (тесты 2020-2023). Соотношение риск/прибыль 1.8-2.3.

Экономит время: Оповещения скажут, когда входить и выходить — не надо сидеть у экрана.

Гибкость: Подходит для быстрой торговли, среднесрочной и долгосрочной.

Часто задаваемые вопросы

Почему нет трейлинг-стопа?

Тесты показали, что он снижает прибыль на 15-20%, потому что выходит слишком рано. Безубыток лучше защищает деньги.

Что делать с новостями?

Увеличьте ATR (например, до 50) и стоп-лосс (6x ATR), когда рынок штормит.

Можно торговать форекс?

Да! Используйте EMA=50, HMA=20, ATR=14 для EUR/USD на 15 минутах.

Управление рисками

Риск на сделку: Не больше 1-2% от депозита.

Проверка раз в неделю: Обновляйте ATR и стоп-лосс каждую пятницу под рынок.

План на экстрим: Если происходит что-то необычное (например, “черный лебедь”), вручную двигайте стоп-лосс.

⚠️ Предупреждение: Торговля — это риск. Стратегия не гарантирует прибыль. Всегда ставьте стоп-лосс.

Prime Trend ReactorIntroduction

Prime Trend Reactor is an advanced crypto trend-following strategy designed to deliver precision entries and exits based on a multi-factor trend consensus system.

It combines price action, adaptive moving averages, momentum oscillators, volume analysis, volatility signals, and higher timeframe trend confirmation into a non-repainting, fully systematic approach.

This strategy is original: it builds a unique trend detection matrix by blending multiple forms of price-derived signals through weighted scoring, rather than simply stacking indicators.

It is not a mashup of public indicators — it is engineered from the ground up using custom formulas and strict non-repainting design.

It is optimized for 1-hour crypto charts but can be used across any asset or timeframe.

⚙️ Core Components

Prime Trend Reactor integrates the following custom components:

1. Moving Averages System

Fast EMA (8), Medium EMA (21), Slow EMA (50), Trend EMA (200).

Detects short-term, medium-term, and long-term trend structures.

EMA alignment is scored as part of the trend consensus system.

2. Momentum Oscillators

RSI (Relative Strength Index) with Smoothing.

RMI (Relative Momentum Index) custom-calculated.

Confirms price momentum behavior aligned with trend.

3. Volume Analysis

CMF (Chaikin Money Flow) for accumulation/distribution pressure.

OBV (On Balance Volume) EMA Cross for volume flow confirmation.

4. Volatility and Price Structure

Vortex Indicator (VI+ and VI-) for trend strength and directional bias.

Mean-Extreme Price Engine blends closing price with extremes (high/low) based on user-defined ratio.

5. Structure Breakout Detection

Detects structure breaks based on highest high/lowest low pivots.

Adds weight to trend strength on fresh breakouts.

6. Higher Timeframe Confirmation (HTF)

Uses higher timeframe EMAs and close to confirm macro-trend direction.

Smartly pulls HTF data with barmerge.lookahead_off to avoid repainting.

🔥 Entry and Exit Logic

Long Entry: Triggered when multi-factor trend consensus turns strongly bullish.

Short Entry: Triggered when consensus flips strongly bearish.

Take Profits (TP1/TP2):

TP1: Partial 50% profit at small target.

TP2: Full 100% close at larger target.

Exit on Trend Reversal:

If trend consensus reverses before hitting TP2, the strategy exits early to protect capital.

TP Hits and Trend Reversals fire real-time webhook-compatible alerts.

🧩 Trend Consensus Matrix (Original Concept)

Instead of relying on a single indicator, Prime Trend Reactor calculates a weighted score using:

EMA Alignment

Momentum Oscillators (RSI + RMI)

Volume Analysis

Volatility (Vortex)

Higher Timeframe Bias

Each component adds a weighted contribution to the final trend strength score.

Only when the weighted score exceeds a user-defined threshold does the system allow entries.

This multi-dimensional scoring system is original and engineered specifically to avoid noisy or lagging traditional signals.

📈 Visualization and Dashboard

Custom EMA Clouds dynamically fill between Fast/Medium EMAs.

Colored Candles show real-time trend direction.

Dynamic Dashboard displays:

Current Position (Long/Short/Flat)

Entry Price

TP1 and TP2 Hit Status

Bars Since Entry

Win Rate (%)

Profit Factor

Current Trend Signal

Consensus Score (%)

🛡️ Non-Repainting Design

All trend calculations are based on current and confirmed past data.

HTF confirmations use barmerge.lookahead_off.

No same-bar entries and exits — enforced logic prevents overlap.

No lookahead bias.

Strict variable handling ensures confirmed-only trend state transitions.

✅ 100% TradingView-approved non-repainting behavior.

📣 Alerts and Webhooks

This strategy includes full TradingView webhook support:

Long/Short Entries

TP1 Hit (Partial Exit)

TP2 Hit (Full Exit)

Exit on Trend Reversal

All alerts use constant-string JSON formatting compliant with TradingView multi-exchange bots:

📜 TradingView Mandatory Disclaimer

This strategy is a tool to assist in market analysis. It does not guarantee profitability. Trading financial markets involves risk. You are solely responsible for your trading decisions. Past performance does not guarantee future results.

Stealth Trigger X🔰 Stealth Trigger X — Smart Divergence & Breakout Strategy with Trend Weakness Exit

Stealth Trigger X is a precision-engineered, non-repainting strategy designed for traders who rely on high-conviction breakouts and trend confirmation. Rather than relying on lagging or oversimplified signals, this strategy fuses divergence logic, volatility detection, volume filtering, and slope-based trend validation into one clean system — making it both responsive and reliable.

📌 Core Components (How It Works):

1. ZLEMA (Zero-Lag Exponential Moving Average):

Used as the primary trend baseline. Unlike a standard EMA, ZLEMA compensates for lag by using a double-smoothing technique that allows the strategy to detect trend direction changes sooner — especially useful in crypto and fast-moving markets.

2. Gradient Filter (Slope of ZLEMA):

Rather than waiting for price to cross a moving average, the strategy measures the slope of the ZLEMA itself. Positive slope = uptrend, negative slope = downtrend. This gives us early trend validation and exit signals based on weakening momentum.

3. Vortex Indicator (Directional Volatility):

A diff-based implementation of the Vortex Indicator is used to validate whether volatility is expanding in favor of the trend. This prevents false entries during indecision phases or low-momentum conditions.

4. White Line Bias Filter (Structural Trend):

The strategy calculates the midpoint of the highest high and lowest low over a user-defined period. This “White Line” serves as a structural trend bias, ensuring entries align with the broader context — not just momentary momentum.

5. Volume Spike Confirmation:

To avoid manipulation and choppy conditions, the strategy confirms breakouts only when the current bar’s volume exceeds the median volume of recent candles by a set multiplier. This filters out noise and ensures only high-conviction moves trigger entries.

6. Breakout with Divergence Timing:

A hybrid logic checks for price breaking previous range highs/lows (breakouts), combined with simulated divergence behavior based on RSI-like momentum. This helps align entry timing with areas where price is likely to accelerate.

⚙️ Trade Management Logic:

Entry Conditions:

Triggered when all conditions align: ZLEMA slope, Vortex confirmation, White Line bias, volume spike, and divergence-based breakout.

Take Profits:

TP1: 50% of position is closed using a limit order

TP2: Remaining 50% closed with another limit order

This split exit approach lets profits run while locking in gains early.

Exits on Trend Weakness:

If trend conditions weaken (slope flip or vortex flip), the position is exited before a full reversal occurs — helping protect capital during exhaustion phases.

Reentry Delay:

Enforces a 1-bar cooldown between exit and new entries to avoid “ping-pong” signals and maintain clean backtest results.

📊 Real-Time Dashboard (On-Chart):

Displays critical stats including:

Current position (Long, Short, or Flat)

Entry price

TP1 and TP2 hit status

Win rate (%)

Profit factor

Bars since entry