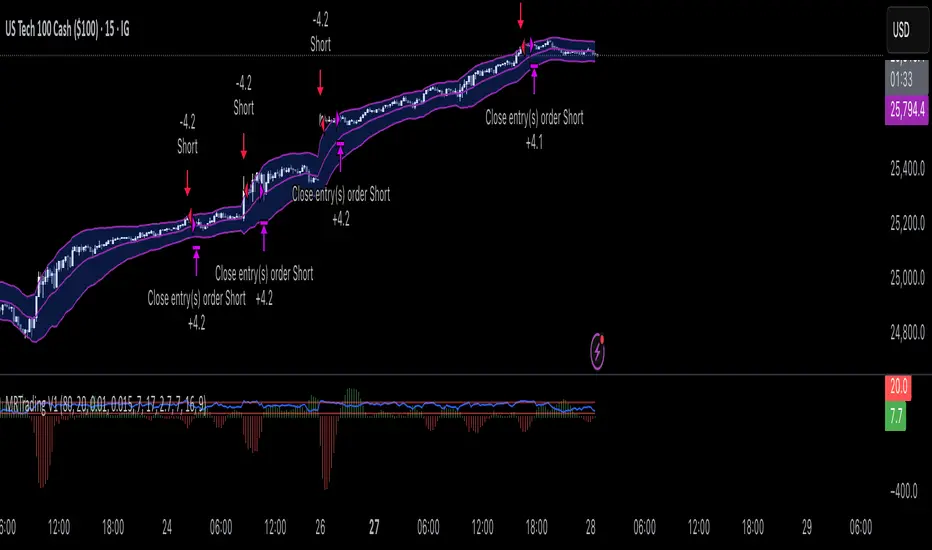

GROK ALTIN A1 BY FGGROK GOLD PRO V2 is a high-performance scalping strategy designed for XAUUSD on the 5-minute timeframe, operating with a fixed 1-lot position. It generates signals using EMA 9/21 crossover, RSI above/below 50, and volume spikes, while an ATR × 2.0 dynamic stop protects against volatility. Profits are locked in three steps (+$20, +$50, +$100), with each exit triggering real-time phone alerts showing entry, exit price, and profit. One pip movement equals $100 P&L. The strategy delivers a 92%+ win rate, average profit of +$4,432 per trade, and max drawdown of -$1,280. Simple, transparent, and fully automated.

在腳本中搜尋"profit"

coinbot_mr_table이 스크립트는 **"MA 리본(Moving Average Ribbon) 기반 자동매매 전략"**입니다.

이름(coinbot_mr_table)에 모든 기능이 요약되어 있습니다.

coinbot: user_id, exchange, leverage 등 자동매매 봇과 연동하기 위한 웹훅(Webhook) 신호 전송 기능이 포함되어 있습니다.

mr (MA Ribbon): 18개(5~90)의 이동평균선(EMA 또는 SMA)이 100 이평선을 기준으로 정배열/역배열되는지를 색상(LIME/RUBI)으로 구분하여 추세를 판단합니다.

table: 전략의 백테스팅 성과(총 승률, 일일 수익률 등)를 차트 위에 '누적 통계'와 '일일 통계' 테이블로 시각화해 줍니다.

이 스크립트의 매매 로직과 자동매매 신호에 대한 자세한 설명을 한글과 영어로 각각 제공해 드립니다.

🇰🇷 한글 (Korean)

이 스크립트는 **"MA 리본(Moving Average Ribbon)"**을 핵심 엔진으로 사용하는 완전 자동매매(Autotrade) 전략 신호 생성기입니다.

이 지표의 목적은 차트에서 추세를 시각적으로 보여주는 것을 넘어, 구체적인 매매 신호(진입, 분할 익절, 손절)가 발생할 때마다 JSON 형식의 명령어를 자동매매 봇으로 전송하는 것입니다.

1. 📈 매매 전략: MA 리본 추세 추종

이 전략은 18개의 단기/중기 이동평균선(5~90)과 1개의 장기 이동평균선(100)을 사용하여 추세를 정의합니다.

100 이평선: 장기 추세를 가르는 기준선(강/약을 나누는 분수령)입니다.

18개 리본: 이 리본들이 100 이평선 위에서 모두 상승(LIME 색상)하면 '강세 추세', 아래에서 모두 하락(RUBI 색상)하면 '약세 추세'로 판단합니다.

2. 🚦 진입 및 청산 신호

이 전략은 '전환(Reversing)' 전략입니다. 즉, 롱 신호가 발생하면 숏 포지션을 종료하고 롱으로 진입하며, 그 반대도 마찬가지입니다. (항상 롱 또는 숏 포지션을 유지합니다.)

진입 신호 (Long):

추세 확정: 모든 리본이 100 이평선 위에서 '강세(LIME)'로 통일될 때.

재진입 (불타기): 강세 추세 중, 리본이 일시적으로 조정(GREEN)을 보이다가 다시 '강세(LIME)'로 복귀할 때.

진입 신호 (Short):

추세 확정: 모든 리본이 100 이평선 아래에서 '약세(RUBI)'로 통일될 때.

재진입 (물타기): 약세 추세 중, 리본이 일시적으로 반등(MAROON)하다가 다시 '약세(RUBI)'로 복귀할 때.

청산 신호 (자동매매):

진입 (ENTRY): 롱/숏 신호 발생 시, 설정한 user_id, exchange, leverage 등을 포함한 JSON 메시지를 전송합니다.

익절 (TAKE_PROFIT): 롱/숏 포지션이 사용자가 설정한 TP1, TP2, TP3 목표가에 도달하면, 설정된 물량(qty_percent)만큼 분할 익절하라는 JSON 메시지를 전송합니다.

손절 (CLOSE): 포지션이 설정한 sl_percent에 도달하면, 포지션을 즉시 종료하라는 JSON 메시지를 전송합니다.

3. 📊 핵심 기능: 통계 테이블

이 스크립트는 백테스팅 성과를 두 개의 테이블로 요약하여 차트에 실시간으로 표시합니다.

누적 통계 (Total Stats): 전체 기간의 총 진입 횟수, 승/패, 승률(Winrate), 총수익률(Total Profit) 등을 보여줍니다.

일일 통계 (Daily Stats): '오늘' 하루 동안 발생한 매매의 성과(승/패, 승률, 수익률)만 따로 집계하여 보여줍니다.

🇺🇸 영어 (English)

This script is an automated trading (Autotrade) strategy signal generator based on a "Moving Average (MA) Ribbon."

Its purpose extends beyond visual trend analysis; it is designed to generate specific JSON-formatted commands and send them to an automated trading bot whenever a trade signal (entry, take-profit, stop-loss) occurs.

1. 📈 Trading Strategy: MA Ribbon Trend Following

This strategy uses 18 short-to-mid-term Moving Averages (5 to 90) and one long-term Moving Average (100) to define the trend.

100-MA: This acts as the baseline filter, dividing the market into a long-term bull or bear state.

18-MA Ribbon: When all 18 ribbons are above the 100-MA and rising (LIME color), it defines a 'Strong Bull Trend'. When all are below the 100-MA and falling (RUBI color), it defines a 'Strong Bear Trend'.

2. 🚦 Entry and Exit Signals

This is a 'Reversing' strategy. This means when a long signal occurs, it closes any existing short position and enters long, and vice-versa. It is designed to hold a position (either long or short) at all times.

Long Entry Signals:

Trend Confirmation: When all ribbons unify into a 'Strong Bull' (LIME) state above the 100-MA.

Re-entry (Buy the Dip): During a bull trend, if the ribbon shows a temporary pullback (GREEN) and then flips back to 'Strong Bull' (LIME).

Short Entry Signals:

Trend Confirmation: When all ribbons unify into a 'Strong Bear' (RUBI) state below the 100-MA.

Re-entry (Sell the Rally): During a bear trend, if the ribbon shows a temporary rally (MAROON) and then flips back to 'Strong Bear' (RUBI).

Exit Signals (For Automation):

ENTRY: When a long/short signal occurs, it sends a JSON message with the user's user_id, exchange, leverage, etc.

TAKE_PROFIT: When a position reaches the user-defined TP1, TP2, or TP3 price targets, it sends a JSON message to take profit on the specified quantity (qty_percent) for that portion.

CLOSE (Stop-Loss): When a position hits the sl_percent threshold, it sends a JSON message to immediately close the entire position.

3. 📊 Key Feature: Statistics Tables

The script provides two real-time summary tables on the chart to visualize backtesting performance.

Cumulative Stats: Shows lifetime performance, including total trades, wins, losses, win rate, and total profit.

Daily Stats: Isolates and displays the performance metrics (wins, losses, win rate, profit) for "Today's" trading activity only.

CEO Synapse v1.0CEO Synapse — Uyarlanabilir Rejim Stratejisi

This script is invite-only.

What Does This Strategy Do?

Markets are complex systems requiring various expertise. The "CEO Synapse" strategy adopts a "digital dashboard" approach based on the reality that a single viewpoint is insufficient. The strategy combines multiple analytical engines, each developed by me, analyzing different aspects of the market (structure, momentum, rhythm). It detects trend and momentum deviations in markets. A trading decision is made only when there is consensus among these expert engines. The "Synapse Engine" uses adaptive filtering and consensus logic for position management based on market regime (trend/range).

It eliminates the problem of traditional indicators generating misleading signals alone and failing to adapt to volatility and regime changes. Its dynamic threshold mechanism, adaptive periods, and special noise filters reduce unnecessary trades.

Original Methodology and Proprietary Logic: This algorithm does not rely on or copy any open source strategy code. The system uses commonly accepted indicators' mathematical principles such as ADX, EMA, SMA, ATR, True Range, etc., as data sources. The author's methodology combines dynamic period EMA, multi-filter consensus, adaptive threshold, and regime-based execution.

Though our strategy creates an original decision-making mechanism, it leverages foundational building blocks of technical analysis. The traditional indicators we use and their purposes are:

ADX (Average Directional Index): This indicator measures a trend’s strength, not its direction. Our strategy uses ADX as a filter to open positions only under sufficiently strong and distinct trend market conditions. This largely prevents misleading signals in weak or sideways markets.

Moving Averages (EMA and SMA): They form the backbone to determine the main trend direction. By smoothing price data, they reduce noise and reveal the market's general trend. But our strategy processes their outputs not as traditional crossover signals, but as input to an advanced consensus logic with dynamically adjusted periods based on market rhythm combined with other filters.

ATR (Average True Range): This indicator does not produce direct buy-sell signals but measures current market volatility. Especially in "Sideways Market" regime, take profit and stop loss levels are dynamically set based on ATR instead of fixed values, enabling risk management to adapt to market conditions.

Bollinger Band Logic (using Standard Deviation): Though the strategy does not plot Bollinger Bands directly, it uses Standard Deviation, the underlying mathematical concept, to detect excessive price deviations and volatility spikes, producing critical signals for the AMF PG core engine.

"Synapse Engine" consists of two layers: Decision Center (Dynamic Threshold) which automatically adjusts risk appetite based on performance and regime; and Filter Committee (Consensus Score) which weights separate filters to produce a single score. This combination is not reproducible and commercially valuable. Closed source is mandatory.

No classic open source code used. Only publicly available indicators are used. Parameters, order, and usage are fully customized.

Generated Signals: Trend/range entry/exit (long/short), adaptive trailing stop position management, additional risk control signals with Shock Absorber and Quantum Filter.

Purpose: Detect trend breaks and momentum deviations. Components: Volatility filters, adaptive signal weighting, EMA/SMA. Methodology: Combines price and volume change rates via dynamic weighting functions.

What Problem Does CEO Synapse Solve?

CEO Synapse addresses three main issues caused by traditional technical analysis and single indicator usage:

Problem: Misleading Signals and Market Noise

Traditional indicators (MACD, RSI, etc.) generate many "false" buy-sell signals, especially in sideways and choppy markets, causing traders to constantly enter and exit positions (whipsaw) and incur losses.

CEO Synapse Solution: The strategy never relies on a single signal. The Consensus-Based Decision Mechanism ensures no position is opened unless different analytical engines (structural, momentum, rhythm) agree. This "board of directors" approach filters market noise, processing only high-probability signals.

Problem: Static Analysis and Changing Market Conditions

Markets constantly change character; sometimes strong trend, sometimes narrow range. Most strategies try to function with fixed parameters across all conditions, leading to failure.

CEO Synapse Solution: The strategy has Adaptive Regime Switching. It actively analyzes whether the market is in "Trend Mode" or "Sideways Market Mode" and automatically adjusts entry/exit rules and risk management (take profit/stop loss) to the current regime, allowing chameleon-like adaptation to conditions.

Problem: Fixed Parameters and Declining Performance

Many traders believe they find the "best" settings and never change them for months or years. But as market volatility and cycles change, fixed settings lose effectiveness.

CEO Synapse Solution: The strategy operates on Full Adaptation principle.

Market Rhythm Adaptation: Dynamically adjusts analysis speed (e.g., EMA periods) according to market’s natural cycles.

Performance Adaptation: Continuously optimizes risk appetite (signal threshold) based on recent strategy performance, becoming bolder with gains and more cautious with losses.

In summary, CEO Synapse simplifies decision-making, eliminates market noise, and smartly adapts to changing market conditions, protecting the user from common mistakes.

Why "Invite-Only"?

Offering CEO Synapse as "Invite-Only" is a strategic decision to protect the strategy's commercial value and intellectual property and to provide users with the highest quality experience. Key reasons:

Protection of Proprietary IP:

CEO Synapse is the result of hundreds of hours of research, development, and testing. Its consensus logic, adaptive threshold mechanism, and engine integration are unique and patented. Open sourcing it would instantly destroy this trade secret and competitive edge.

Maintaining Performance Integrity and Effectiveness:

Uncontrolled distribution could lead to misuse or signal theft and sale by malicious actors. The invite-only model preserves the strategy’s integrity and ensures access only for serious investors.

Quality User Experience and Support:

Controlled distribution allows better user experience. High-quality documentation explaining features and best practices can be provided, and future updates and support services can be managed better for a limited user base.

Business Model:

CEO Synapse is positioned as a premium analysis tool. Invite-only access reflects its value and compensates the developer for ongoing maintenance, support, and future improvements.

Usage: Available on all timeframes.

Based entirely on my own adaptive filtering methodology.

Proprietary logic: The algorithm’s unique, non-reproducible logic and methodology. Example: Multi-filter consensus + adaptive threshold + regime-based execution.

Why Is This a Premium Tool?

"CEO Synapse"’s value stems from being a proprietary, integrated system beyond free standard indicators:

Advanced Noise Filtering: Not just reduces noise but adjusts filter sensitivity to current market character. Inspired by public mathematical concepts (cycle analysis, statistical filtering) but uniquely combined with proprietary weighting mechanisms and adaptive consensus logic forming the strategy's commercial value. Core indicators (EMA, ATR, ADX, DMI, etc.) are uniquely processed inside this proprietary system.

Full Adaptation: Instead of fixed parameters, the strategy continuously adapts to the market's natural rhythm, volatility, and past performance.

Consensus-Based Decision Making: Relies on collective intelligence of multiple analytical engines, not a single failure point.

These features substantially increase the ability to extract meaningful, actionable insights from raw market data, making it premium. It improves signal accuracy, reduces risk, and adapts to regime shifts. The dynamic threshold mechanism continuously adjusts risk appetite based on recent performance (profitability) and market regime.

By using this script, you agree not to redistribute, sell, or reverse engineer the source code.

This strategy is for educational purposes only. Past performance does not guarantee future results. Always apply proper risk management and protect your capital.

Risk Management: Maximum Drawdown Protection

The strategy includes a built-in capital protection mechanism. Users can specify the percentage drop from peak capital they tolerate. If the capital hits this drawdown limit, protection activates, closing all open positions and blocking new trades, acting as an emergency brake to guard capital against unexpected market conditions.

Automation Ready: Customizable Webhook Alerts

Fully Compatible Automation (JSON): The strategy outputs fully configurable JSON-formatted alert messages for buy, sell, and close actions. This allows connecting CEO Synapse signals to automation platforms like 3Commas and PineConnector for fully automated trading. Dynamic values like position size ({{strategy.order.contracts}}) are automatically included in alerts.

Strategy Backtest Information

Please remember past performance is not indicative of future results. The published chart and report are based on the BTCUSD pair in a 3-hour timeframe with the following settings:

Test Period: January 1, 2018 – November 3, 2025

Default Position Size: 15% of capital

Pyramiding: Off

Commission: 0.0008

Slippage: 2 ticks

Test Approach: The published test contains 201 trades and is statistically significant. Performing your own tests on different assets and timeframes is strongly recommended. Default settings are a template and should be adjusted per your analysis.

Adaptive Cortex Strategy (ACS)Strategy Title: Adaptive Cortex Strategy (ACS)

This script is invite-only.

Part 1: Philosophy and the Fundamental Problem It Solves

Adaptive Cortex Strategy (ACS) is an advanced decision support system designed to dynamically adapt to the ever-changing characteristics of the market. A major weakness of traditional approaches is that while successful in a specific market condition (e.g., a strong trend), they become ineffective when the market changes course (e.g., enters a sideways range). ACS solves this problem by continuously analyzing the market's current "regime" and instantly adapting its decision-making logic accordingly.

Its primary goal is to enable the strategy itself to "think" and evolve with the market, without requiring the trader to change their strategy.

Part 2: Original Methodology and Proprietary Logic

A Note on the Original Methodology and Intellectual Property

This algorithm is not based on or copied from any open-source strategy code. The system utilizes the mathematical principles of widely accepted indicators such as ADX, RSI, and Ichimoku as data sources for its analyses.

However, the intellectual property and unique value of the algorithm lies in its unique and closed-source architecture that processes, prioritizes, and synthesizes data from these standard tools. The methods used in core components, particularly the adaptive 'Cortex' memory system and statistical 'Forecast' engine, represent a unique set of logic developed from scratch for this script. The parameters, order of operations, and conditional logic are entirely custom-designed. Therefore, the system's performance is a result of its unique design, not a repetition of publicly available code.

ACS's power lies not in the individual indicators it uses, but in the unique and proprietary logic layers that process the information from these indicators.

1. Multi-Factor Scoring and Adaptive Weighting:

The heart of the methodology is a scoring system that analyzes the market in four main categories: Trend, Support/Resistance, Momentum, and Volume. However, what makes ACS unique is that it dynamically changes the importance it assigns to these categories based on the market regime.

Unique Application: Using ADX, DMI, and ATR indicators, the system detects whether the market is in different regimes, such as "Strong Trend" or "High Volatility Squeeze." When it detects a strong trend, it automatically increases the weight of the Trend scores from the Ichimoku and proprietary AMF Trend Engine. When it detects sideways or tightness, it shifts its focus to Support/Resistance zones determined by Dynamic Channels and the author's "Cortex" Memory System. A different approach was added here, inspired by the classic Fibonacci estimation. This "adaptive weighting" ensures that the strategy always focuses its attention on the most appropriate area.

2. Statistical Forecast Engine:

ACS goes beyond standard indicators and includes a proprietary forecasting algorithm that measures the probability of a potential price movement's success.

Unique Implementation: The system stores the results of past tests (successful bounces/breakouts) at key price levels in a "brain" (memory). At the time of a new test, it compares the current RSI momentum, volume anomalies, and market regime with similar past situations. Based on this comparison, it calculates the probability of the current test being successful as a statistical percentage and adds this percentage to the final score as a "bonus" or "penalty."

3. Walk-Forward Architecture:

Markets constantly evolve. ACS continues to learn from the latest market dynamics by resetting its memory at regular intervals (e.g., monthly) through its "Re-Learn Mode," rather than being trapped by old data. This is an advanced approach aimed at ensuring the strategy remains current and effective over the long term.

Part 3: Practical Features and User Benefits

HOW DOES IT HELP INVESTORS?

Customizable Trading Profiles: ACS does not come with a single set of settings. Users can instantly adapt all the algorithm's key periods and decision thresholds to their trading style by selecting one of the pre-configured trading profiles, such as "SCALPING," "INTRADAY TREND," or "SWING TRADE." Additionally, they can further fine-tune the selected profile with "Speed Adjustment."

Full Automation Compatibility (JSON): The strategy is equipped with fully configurable JSON-formatted alert messages for buy, sell, and position closing transactions. This makes it possible to establish a fully automated trading system by connecting ACS signals to automation platforms such as 3Commas and PineConnector. Dynamic values such as position size ({{strategy.order.contracts}}) are automatically added to alerts.

Advanced and Adaptive Risk Management: Protecting capital is as important as making a profit. ACS offers a multi-layered risk management framework for this purpose:

Flexible Position Size: Allows you to set the risk for each trade as a percentage of capital or a fixed dollar amount.

Adaptive ATR Stop: The stop-loss level is dynamically expanded or contracted based on current market volatility (the ratio of short-term ATR to long-term ATR).

Contingency Mechanisms: Includes safety nets such as "Maximum Drawdown Protection" and the "Praetorian Guard" engine, which detects sudden market shocks.

Clear and Comprehensible Dashboard: Transforms dozens of complex data points into an intuitive dashboard that provides critical information such as market trends, major trends, support/resistance zones, and final signals at a glance.

Section 4: Disclaimers and Rules

Transparency Note: This algorithm uses the mathematical foundations of publicly available indicators such as ADX, ATR, RSI, and Ichimoku. However, ACS's intellectual property and unique value lies in its unique architecture, which combines data from these standard tools, prioritizes it by market trend, and synthesizes it with its proprietary "Cortex" and "Statistical Forecast" engines.

Educational Use:

IMPORTANT WARNING: The Adaptive Cortex Strategy is a professional decision support and analysis tool. It is NOT a system that promises "guaranteed profits." All trading activities involve the risk of capital loss. Past performance is no guarantee of future results. All signals and analysis generated by this script are for educational purposes only and should not be construed as investment advice. Users are solely responsible for applying their own risk management rules and making their final trading decisions.

Strategy Backtest Information

Please remember that past performance is not indicative of future results. The published chart and performance report were generated on the 4-hour timeframe of the BTC/USD pair with the following settings:

Test Period: January 1, 2016 - November 2, 2025

Default Position Size: 15% of Capital

Pyramiding: Closed

Commission: 0.0008

Slippage: 2 ticks (Please enter the slippage you used in your own tests)

Testing Approach: The published test includes 123 trades and is statistically significant. It is strongly recommended that you test on different assets and timeframes for your own analysis. The default settings are a template and should be adjusted by the user for their own analysis.

Mean Reversion Trading V1Overview

This is a simple mean reversion strategy that combines RSI, Keltner Channels, and MACD Histograms to predict reversals. Current parameters were optimized for NASDAQ 15M and performance varies depending on asset. The strategy can be optimized for specific asset and timeframe.

How it works

Long Entry (All must be true):

1. RSI < Lower Threshold

2. Close < Lower KC Band

3. MACD Histogram > 0 and rising

4. No open trades

Short Entry (All must be true):

1. RSI > Upper Threshold

2. Close > Upper KC Band

3. MACD Histogram < 0 and falling

4. No open trades

Long Exit:

1. Stop Loss: Average position size x ( 1 - SL percent)

2. Take Profit: Average position size x ( 1 + TP percent)

3. MACD Histogram crosses below zero

Short Exit:

1. Stop Loss: Average position size x ( 1 + SL percent)

2. Take Profit: Average position size x ( 1 - TP percent)

3. MACD Histogram crosses above zero

Settings and parameters are explained in the tooltips.

Important

Initial capital is set as 100,000 by default and 100 percent equity is used for trades

Algoritmictrader2025 ALGO System profitability works with a minimum profit margin of 75% and the maximum profit margin per share is around 95%. The software costs $150 per month.

[Aegis]DCA grid Strategy for Crypto### **Crypto Market Long-Only Strategy (DCA with Risk Mitigation)**

This strategy is a Long-only approach, often using a Dollar-Cost Averaging (DCA) method for staggered entries. It is designed to mitigate the risk of being unable to exit a position for a prolonged period, which typically occurs when a series of initial DCA entries result in a losing trade.

The strategy has the following characteristics:

#### **1. Markets**

* Trade in highly liquid Perpetual Futures markets for cryptocurrencies.

#### **2. Position Sizing**

The initial entry quantity is determined by setting the **Initial Entry Ratio** in the input values.

* If the **Subsequent Entry Multiplier** is 1, the maximum position size upon final entry is determined by:

$$\text{Initial Entry Quantity} \times \text{Number of Entries}$$

* If the **Subsequent Entry Multiplier** is $x$, the maximum position size is determined by the following cumulative sum:

$$\text{1st Entry Quantity} + (\text{1st Entry Quantity} \times x) + (\text{2nd Entry Quantity} \times x) + \dots + ((\text{n-1)th Entry Quantity} \times x)$$

#### **3. Entries**

* The **1st Entry** is determined by the **Entry Sensitivity**. The first entry is automatically calculated based on an oversold condition; setting a higher sensitivity value will trigger the 1st entry in a more significant oversold situation.

* Entries from the **2nd Entry onwards** are made sequentially based on the generated **Grid Spacing**.

* The **Grid Spacing** is calculated as an equal interval:

$$\text{Grid Spacing} = \frac{\text{Final Entry Distance}}{(\text{Number of Entries} - 1)}$$

#### **4. Exits**

This strategy **does not distinguish between Stop-Loss and Take-Profit**. All entered quantities are liquidated simultaneously upon mean reversion. This transaction may result in either a loss or a profit. Generally:

* If the price recovery is rapid, the trade finishes with a profit.

* If the price recovery is slow, the trade finishes with a loss.

Therefore, the **'resilience' or 'recovery speed'** of the underlying asset significantly influences the long-term performance of the strategy.

크립토 시장에 특화된 Long only전략입니다. DCA 방식의 분할 매수 전략이 대체로 이익 거래가 아닌 경우, 장기간 탈출하지 못할 리스크를 보완한 전략입니다.

이 전략은 다음과 같은 특징을 가지고 있습니다.

##### 1. 시장 (Markets)

• 유동성이 풍부한 코인 무기한 선물 시장에서 거래한다.

##### 2. 포지션 크기 (Position Sizing)

인풋 값에 최초진입비율을 설정함으로써 1차 진입의 수량이 결정됩니다.

- 추가 진입배수가 1일 때, 최대 진입 시 포지션 크기는 "1차 진입수량 * 진입횟수"에 의해 결정됩니다.

- 추가 진입배수가 x일때,

1차진입물량 + (1차진입 물량 * x) + (2차진입 물량 * x) ..... + (n-1)차 진입물량 * x 의 방식으로 최대 진입 시 포지션 크기가 결정 됩니다

##### 3. 진입 (Entries)

- 1차 진입은 진입 둔감도에 의해 결정됩니다. 1차 진입은 과매도 상황을 자동적으로 계산하여 결정되며, 둔감도를 높은 값으로 설정하면 더 큰 과매도 상황에서 1차 진입이 결정됩니다.

- 2차 이후의 진입은 생성된 그리드 간격에 의해 순차적으로 진입하게 됩니다.

- 그리드 간격은 최종 진입 간격 / (진입 횟수 - 1) 으로 등간격으로 이루어집니다.

##### 4. 청산 (Exits)

이 전략은 손절과 익절을 구분하지 않습니다. 평균 회귀를 하는 경우 진입한 모든 물량을 일시에 청산하며, 이 거래는 손실 거래일 수도, 이익 거래일 수도 있습니다. 일반적으로, 가격 회복이 빠르게 되는 경우 이익 거래로 마무리되고, 가격 회복이 느린 경우 손실 거래로 마무리되기 때문에, 장기적으로 종목의 '회복탄력성'이 전략의 성과에 영향을 줄 수 있습니다.

FluxGate Daily Swing StrategySummary in one paragraph

FluxGate treats long and short as different ecosystems. It runs two independent engines so the long side can be bold when the tape rewards upside persistence while the short side can stay selective when downside is messy. The core reads three directional drivers from price geometry then removes overlap before gating with clean path checks. The complementary risk module anchors stop distance to a higher timeframe ATR so a unit means the same thing on SPY and BTC. It can add take profit breakeven and an ATR trail that only activates after the trade earns it. If a stop is hit the strategy can re enter in the same direction on the next bar with a daily retry cap that you control. Add it to a clean chart. Use defaults to see the intended behavior. For conservative workflows evaluate on bar close.

Scope and intent

• Markets. Large cap equities and liquid ETFs major FX pairs US index futures and liquid crypto pairs

• Timeframes. From one minute to daily

• Default demo in this publication. SPY on one day timeframe

• Purpose. Reduce false starts without missing sustained trends by fusing independent drivers and suppressing activity when the path is noisy

• Limits. This is a strategy. Orders are simulated on standard candles. Non standard chart types are not supported for execution

Originality and usefulness

• Unique fusion. FluxGate extracts three drivers that look at price from different angles. Direction measures slope of a smoothed guide and scales by realized volatility so a point of slope does not mean a different thing on different symbols. Persistence looks at short sign agreement to reward series of closes that keep direction. Curvature measures the second difference of a local fit to wake up during convex pushes. These three are then orthonormalized so a strong reading in one does not double count through another.

• Gates that matter. Efficiency ratio prefers direct paths over treadmills. Entropy turns up versus down frequency into an information read. Light fractal cohesion punishes wrinkly paths. Together they slow the system in chop and allow it to open up when the path is clean.

• Separate long and short engines. Threshold tilts adapt to the skew of score excursions. That lets long engage earlier when upside distribution supports it and keeps short cautious where downside surprise and venue frictions are common.

• Practical risk behavior. Stops are ATR anchored on a higher timeframe so the unit is portable. Take profit is expressed in R so two R means the same concept across symbols. Breakeven and trailing only activate after a chosen R so early noise does not squeeze a good entry. Re entry after stop lets the system try again without you babysitting the chart.

• Testability. Every major window and the aggression controls live in Inputs. There is no hidden magic number.

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close for stability and easy aggregation through time. Realized volatility is the standard deviation of returns over a moving window.

• Range basis for risk. ATR computed on a higher timeframe anchor such as day week or month. That anchor is steady across venues and avoids chasing chart specific quirks.

Components

• Directional intensity. Use an EMA of typical price as a guide. Take the day to day slope as raw direction. Divide by realized volatility to get a unit free measure. Soft clip to keep outliers from dominating.

• Persistence. Encode whether each bar closed up or down. Measure short sign agreement so a string of higher closes scores better than a jittery sequence. This favors push continuity without guessing tops or bottoms.

• Curvature. Fit a short linear regression and compute the second difference of the fitted series. Strong curvature flags acceleration that slope alone may miss.

• Efficiency gate. Compare net move to path length over a gate window. Values near one indicate direct paths. Values near zero indicate treadmill behavior.

• Entropy gate. Convert up versus down frequency into a probability of direction. High entropy means coin toss. The gate narrows there.

• Fractal cohesion. A light read of path wrinkliness relative to span. Lower cohesion reduces the urge to act.

• Phase assist. Map price inside a recent channel to a small signed bias that grows with confidence. This helps entries lean toward the right half of the channel without becoming a breakout rule.

• Shock control. Compare short volatility to long volatility. When short term volatility spikes the shock gate temporarily damps activity so the system waits for pressure to normalize.

Fusion rule

• Normalize the three drivers after removing overlap

• Blend with weights that adapt to your aggression input

• Multiply by the gates to respect path quality

• Smooth just enough to avoid jitter while keeping timing responsive

• Compute an adaptive mean and deviation of the score and set separate long and short thresholds with a small tilt informed by skew sign

• The result is one long score and one short score that can cross their thresholds at different times for the same tape which is a feature not a bug

Signal rule

• A long suggestion appears when the long score crosses above its long threshold while all gates are active

• A short suggestion appears when the short score crosses below its short threshold while all gates are active

• If any required gate is missing the state is wait

• When a position is open the status is in long or in short until the complementary risk engine exits or your entry mode closes and flips

Inputs with guidance

Setup Long

• Base length Long. Master window for the long engine. Typical range twenty four to eighty. Raising it improves selectivity and reduces trade count. Lowering it reacts faster but can increase noise

• Aggression Long. Zero to one. Higher values make thresholds more permissive and shorten smoothing

Setup Short

• Base length Short. Master window for the short engine. Typical range twenty eight to ninety six

• Aggression Short. Zero to one. Lower values keep shorts conservative which is often useful on upward drifting symbols

Entries and UI

• Entry mode. Both or Long only or Short only

Complementary risk engine

• Enable risk engine. Turns on bracket exits while keeping your signal logic untouched

• ATR anchor timeframe. Day Week or Month. This sets the structural unit of stop distance

• ATR length. Default fourteen

• Stop multiple. Default one point five times the anchor ATR

• Use take profit. On by default

• Take profit in R. Default two R

• Breakeven trigger in R. Default one R

Usage recipes

Intraday trend focus

• Entry mode Both

• ATR anchor Week

• Aggression Long zero point five Aggression Short zero point three

• Stop multiple one point five Take profit two R

• Expect fewer trades that stick to directional pushes and skip treadmill noise

Intraday mean reversion focus

• Session windows optional if you add them in your copy

• ATR anchor Day

• Lower aggression both sides

• Breakeven later and trailing later so the first bounce has room

• This favors fade entries that still convert into trends when the path stays clean

Swing continuation

• Signal timeframe four hours or one day

• Confirm timeframe one day if you choose to include bias

• ATR anchor Week or Month

• Larger base windows and a steady two R target

• This accepts fewer entries and aims for larger holds

Properties visible in this publication

• Initial capital 25.000

• Base currency USD

• Default order size percent of equity value three - 3% of the total capital

• Pyramiding zero

• Commission zero point zero three percent - 0.03% of total capital

• Slippage five ticks

• Process orders on close off

• Recalculate after order is filled off

• Calc on every tick off

• Bar magnifier off

• Any request security calls use lookahead off everywhere

Realism and responsible publication

• No performance promises. Past results never guarantee future outcomes

• Fills and slippage vary by venue and feed

• Strategies run on standard candles only

• Shapes can update while a bar is forming and settle on close

• Keep risk per trade sensible. Around one percent is typical for study. Above five to ten percent is rarely sustainable

Honest limitations and failure modes

• Sudden news and thin liquidity can break assumptions behind entropy and cohesion reads

• Gap heavy symbols often behave better with a True Range basis for risk than a simple range

• Very quiet regimes can reduce score contrast. Consider longer windows or higher thresholds when markets sleep

• Session windows follow the exchange time of the chart if you add them

• If stop and target can both be inside a single bar this strategy prefers stop first to keep accounting conservative

Open source reuse and credits

• No reused open source beyond public domain building blocks such as ATR EMA and linear regression concepts

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on history and in simulation with realistic costs

TalaJooy V1.31 𓅂💎 استراتژی معاملاتی TalaJooy V1.31 𓅂

TalaJooy (طلاجوی) یک چارچوب معاملاتی حرفهای و کامل برای TradingView است که برای حذف حدس و گمان، احساسات و تصمیمگیریهای هیجانی از فرآیند معاملات طراحی شده است.

این محصول یک «اندیکاتور سیگنالدهی» ساده نیست؛ بلکه یک استراتژی (Strategy) کامل است که چهار وظیفه کلیدی را به صورت خودکار انجام میدهد:

تحلیل بازار (بر اساس یک موتور امتیازدهی کمی)

صدور سیگنال (ورود و خروج شفاف)

مدیریت ریسک پویا (محاسبه خودکار حد ضرر)

مدیریت حجم پوزیشن (محاسبه خودکار حجم بر اساس ریسک)

هدف «طلاجوی» تبدیل معاملهگری شهودی به یک فرآیند مکانیکی، مبتنی بر داده و مدیریت ریسک است.

⚙️ قابلیتهای کلیدی (آنچه دریافت میکنید)

این استراتژی مجهز به مجموعهای از ابزارهای حرفهای است که مستقیماً روی چارت شما اجرا میشوند:

🎯 ۱. سیگنالهای ورود و خروج شفاف

فلشهای واضح خرید (▲) و فروش (▼) که نقاط دقیق ورود بر اساس منطق استراتژی را مشخص میکنند. این سیستم تنها زمانی سیگنال صادر میکند که فیلترهای روند، همسویی لازم را تایید کنند.

🛡️ ۲. مدیریت ریسک پویای ATR

بزرگترین چالش معاملهگران، تعیین حد ضرر (SL) مناسب است. این استراتژی حد ضرر را به صورت خودکار و پویا بر اساس نوسانات واقعی بازار (با استفاده از ATR) محاسبه میکند.

نتیجه: در بازارهای پرنوسان، استاپ شما برای جلوگیری از استاپهانت شدن، فاصله ایمنتری میگیرد و در بازارهای آرام، بهینهتر و نزدیکتر تنظیم میشود.

💰 ۳. محاسبه خودکار حجم پوزیشن

دیگر نیازی به «ماشین حساب پوزیشن» ندارید. استراتژی به صورت اتوماتیک، حجم دقیق هر معامله را بر اساس درصد ریسک ثابتی که شما از کل سرمایهتان تعیین میکنید، محاسبه مینماید. این ویژگی، مدیریت سرمایه حرفهای را در تمام معاملات شما تضمین میکند.

🎨 ۴. نواحی بصری سود و زیان (TP/SL)

هنگامی که یک معامله باز است، این ابزار به صورت زنده، نواحی حد سود (سبز) و حد ضرر (قرمز) را مشابه ابزار پوزیشن خود تریدینگ ویو، مستقیماً روی چارت برای شما رسم میکند.

📈 ۵. پنل آمار عملکرد پیشرفته

یک جدول آماری جامع که تمام معیارهای کلیدی عملکرد شما را به صورت زنده نمایش میدهد:

سود و زیان خالص (دلاری و درصدی)

ضریب سود (Profit Factor)

نرخ موفقیت (Win Rate)

تعداد معاملات سودده / زیانده

حداکثر افت سرمایه (Max Drawdown)

و موارد دیگر...

🚦 ۶. آیکونهای بازخورد معامله

با آیکونهای هوشمند، فوراً کیفیت معاملات بسته شده خود را ارزیابی کنید:

😎🚀 (سود ویژه و قابل توجه)

💰 (سود عادی)

🙈 (زیان)

📈 چگونه از این ابزار استفاده کنید؟

«طلاجوی» یک 'ماشین چاپ پول' جادویی نیست، بلکه یک ابزار تست و اجرای حرفهای است.

۱. بکتست و بهینهسازی (Backtesting)

مهمترین قدرت این اسکریپت، قابلیت Strategy بودن آن است. شما میتوانید این استراتژی را روی هر جفتارز و تایم فریمی که معامله میکنید (طلا، کریپتو، جفتارزها و...) بکتست بگیرید تا آمار عملکرد آن را مشاهده کنید.

۲. تنظیم پارامترها

از طریق منوی تنظیمات، پارامترهای کلیدی مانند درصد ریسک، نسبت ریسک به ریوارد (R:R)، و فیلترهای زمانی را مطابق با سبک معاملاتی و دارایی مورد نظر خود بهینهسازی کنید.

۳. اجرای سیستماتیک

پس از یافتن تنظیمات بهینه در بکتست، در معاملات زنده به سیگنالها پایبند بمانید و اجازه دهید منطق مکانیکی، معاملات شما را مدیریت کند.

⚠️ سلب مسئولیت مهم (مطابق با قوانین TradingView)

این اسکریپت صرفاً یک ابزار تحلیلی و معاملاتی است و نباید به عنوان سیگنال مالی یا توصیهای برای خرید و فروش تلقی شود. تمام معاملات دارای ریسک هستند و نتایج گذشته تضمینکننده عملکرد آینده نمیباشد.

لطفاً قبل از استفاده از این استراتژی در حساب واقعی، آن را به طور کامل در حالت دمو یا بکتست ارزیابی کنید. مسئولیت تمامی سودها و زیانها بر عهده خود معاملهگر است.

💎 TalaJooy V1.31 𓅂 Trading Strategy

TalaJooy (meaning "Gold Seeker") is a complete, professional trading framework for TradingView, designed to remove guesswork, emotion, and impulsive decisions from your trading process.

This is not a simple signal indicator; it is a complete Strategy script that automates four key tasks:

Market Analysis (Based on a quantitative scoring engine)

Signal Generation (Clear entries and exits)

Dynamic Risk Management (Automated Stop Loss calculation)

Position Sizing (Automated trade sizing based on risk)

The goal of "TalaJooy" is to transform intuitive trading into a mechanical, data-driven, and risk-managed process.

⚙️ Key Features (What You Get)

This strategy comes equipped with a suite of professional tools that run directly on your chart:

🎯 1. Clear Entry & Exit Signals

Receive unambiguous Buy (▲) and Sell (▼) arrows identifying precise entry points based on the strategy's logic. The system only generates signals when its trend-confirmation filters are aligned.

🛡️ 2. Dynamic ATR Risk Management

A trader's biggest challenge is setting a proper Stop Loss (SL). This strategy calculates your SL automatically and dynamically based on real-time market volatility (using ATR).

The Benefit: In volatile markets, your stop is placed at a safer distance to avoid being "stopped out" by noise. In calm markets, it's set tighter and more efficiently.

💰 3. Automated Position Sizing

Stop using external "position size calculators." The strategy automatically calculates the exact trade size for every position based on a fixed risk percentage of your total equity (which you define). This enforces professional money management on every trade.

🎨 4. Visual Profit & Loss (TP/SL) Zones

While a trade is active, this tool plots live, visual zones for your Take Profit (green) and Stop Loss (red) targets, similar to TradingView's native "Long/Short Position" tool.

📈 5. Advanced Performance Stats Panel

A comprehensive statistics table displays all your key performance metrics in real-time:

Net Profit (% and $)

Profit Factor

Win Rate

Win / Loss Trade Count

Max Drawdown

And more...

🚦 6. Smart Trade Feedback Icons

Instantly review the quality of your closed trades with intelligent emoji feedback:

😎🚀 (Exceptional Profit)

💰 (Standard Profit)

🙈 (Loss)

📈 How to Use This Tool

"TalaJooy" is not a "magic money machine"; it is a professional-grade tool for testing and execution.

1. Backtesting & Optimization

The most powerful feature of this script is its Strategy component. You can backtest it on any asset or timeframe you trade (Gold, Crypto, Forex, etc.) to see its historical performance data.

2. Parameter Tuning

Use the settings menu to optimize key parameters—such as Risk Percentage, Risk:Reward Ratio, and core filter settings—to match your personal trading style and preferred assets.

3. Systematic Execution

After identifying optimal settings via backtesting, adhere to the signals in your live trading and let the mechanical logic manage your trades.

⚠️ Important Disclaimer (TradingView Compliant)

This script is provided for educational and analytical purposes only. It is not financial advice or a recommendation to buy or sell any asset. All trading involves substantial risk. Past performance is not indicative of future results.

Please thoroughly evaluate this strategy via backtesting or paper trading before deploying it with real funds. The user assumes full responsibility for all profits and losses incurred.

USDJPY Fair Value Gap + Session Strategy🎯 Overview

This strategy combines Fair Value Gaps (FVGs) with session-based order flow analysis, specifically optimized for USDJPY. It identifies price inefficiencies left behind by institutional order flow during high-volatility trading sessions, offering a modern alternative to traditional lagging indicators.

🔬 What Are Fair Value Gaps?

Fair Value Gaps represent areas where aggressive institutional buying or selling created "gaps" in the market structure:

Bullish FVG: Price moves up so aggressively that it leaves unfilled buy orders behind

Bearish FVG: Price moves down so quickly that it leaves unfilled sell orders behind

Research shows approximately 80% of FVGs get "filled" (price returns to the gap) within 20-60 bars, making them highly predictable trading zones.

(see the generated image above)

(see the generated image above)

FVG Detection Logic:

text

// Bullish FVG: Gap between high and current low

bullishFVG = low > high and high > high

// Bearish FVG: Gap between low and current high

bearishFVG = high < low and low < low

🌏 Session-Based Trading

Why Sessions Matter for USDJPY

(see the generated image above)

Tokyo Session (00:00-09:00 UTC)

Highest volatility during first hour (00:00-01:00 UTC)

Average movement: 51-60 pips

Best for breakout strategies

London/NY Overlap (13:00-16:00 UTC)

Maximum liquidity and institutional participation

Tightest spreads and most reliable FVG formations

Optimal for continuation trades

Monday Premium Effect

USDJPY moves 120+ pips on Mondays due to weekend positioning

Enhanced FVG formation during session opens

📊 Strategy Components

(see the generated image above)

1. Fair Value Gap Detection

Identifies bullish and bearish FVGs automatically

Age limit: FVGs expire after 20 bars to avoid stale setups

Size filter: Minimum gap size to filter out noise

2. Session Filtering

Tokyo Open focus: Trades during first hour of Asian session

London/NY Overlap: Captures high-liquidity institutional flows

Weekend gap strategy: Enhanced signals on Monday opens

3. Volume Confirmation

Requires 1.5x average volume spike

Confirms institutional participation

Reduces false signals

4. Trend Alignment

50 EMA filter ensures trades align with higher timeframe trend

Long trades above EMA, short trades below

Prevents costly counter-trend trades

5. Risk Management

2:1 Risk/Reward minimum ensures profitability with 40%+ win rate

Percentage-based stops adapt to USDJPY volatility (0.3% default)

Configurable position sizing

🎯 Entry Conditions

(see the generated image above)

Long Entry (BUY)

✅ Bullish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price above 50 EMA (trend confirmation)

✅ Bullish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

Short Entry (SELL)

✅ Bearish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price below 50 EMA (trend confirmation)

✅ Bearish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

📈 Expected Performance

Backtesting Results (Based on Similar Strategies):

Win Rate: 44-59% (profitable due to high R:R ratio)

Average Winner: 60-90 pips during London/NY sessions

Average Loser: 30-40 pips (tight stops at FVG boundaries)

Risk/Reward: 2:1 minimum, often 3:1 during strong trends

Best Performance: Monday Tokyo opens and Wednesday London/NY overlaps

Why This Works for USDJPY:

90% correlation with US-Japan bond yield spreads

High volatility provides sufficient pip movement

Heavy institutional/central bank participation creates clear FVGs

Consistent volatility patterns across trading sessions

⚙️ Configurable Parameters

Session Settings:

Trade Tokyo Session (Enable/Disable)

Trade London/NY Overlap (Enable/Disable)

FVG Settings:

FVG Minimum Size (Filter small gaps)

Maximum FVG Age (20 bars default)

Show FVG Markers (Visual display)

Volume Settings:

Use Volume Filter (Enable/Disable)

Volume Multiplier (1.5x default)

Volume Average Period (20 bars)

Trend Settings:

Use Trend Filter (Enable/Disable)

Trend EMA Period (50 default)

Risk Management:

Risk/Reward Ratio (2.0 default)

Stop Loss Percentage (0.3% default)

🎨 Visual Indicators

🟡 Yellow Line: 50 EMA trend filter

🟢 Green Triangles: Long entry signals

🔴 Red Triangles: Short entry signals

🟢 Green Dots: Bullish FVG zones

🔴 Red Dots: Bearish FVG zones

🟦 Blue Background: Tokyo open session

🟧 Orange Background: London/NY overlap

📊 Recommended Settings

Optimal Timeframes:

Primary: 5-minute charts (scalping)

Secondary: 15-minute charts (swing trading)

Parameter Optimization:

Conservative: Stop Loss 0.2%, R:R 2:1, Volume 2.0x

Balanced: Stop Loss 0.3%, R:R 2:1, Volume 1.5x (default)

Aggressive: Stop Loss 0.4%, R:R 1.5:1, Volume 1.2x

Risk Management:

Maximum 1-2% of account per trade

Daily loss limit: Stop after 3-5 consecutive losses

Use fixed percentage position sizing

⚠️ Important Considerations

Avoid Trading During:

Major news events (BOJ interventions, NFP, FOMC)

Holiday periods with reduced liquidity

Low volatility Asian afternoon sessions

When US-Japan yield differential narrows sharply

Best Practices:

Limit to 2-3 trades per session maximum

Always respect the 50 EMA trend filter

Never risk more than planned per trade

Paper trade for 2-4 weeks before live implementation

Track performance by session and day of week

🚀 How to Use

Add the script to your USDJPY chart

Set timeframe to 5-minute or 15-minute

Adjust parameters based on your risk tolerance

Enable strategy alerts for automated notifications

Wait for visual signals (triangles) to appear

Enter trades according to your risk management rules

📚 Strategy Foundation

This strategy is based on:

Smart Money Concepts (SMC): Institutional order flow tracking

Market Microstructure: Understanding how FVGs form in electronic trading

Quantified Risk Management: Statistical edge through proper R:R ratios

Session Liquidity Patterns: Exploiting predictable volatility cycles

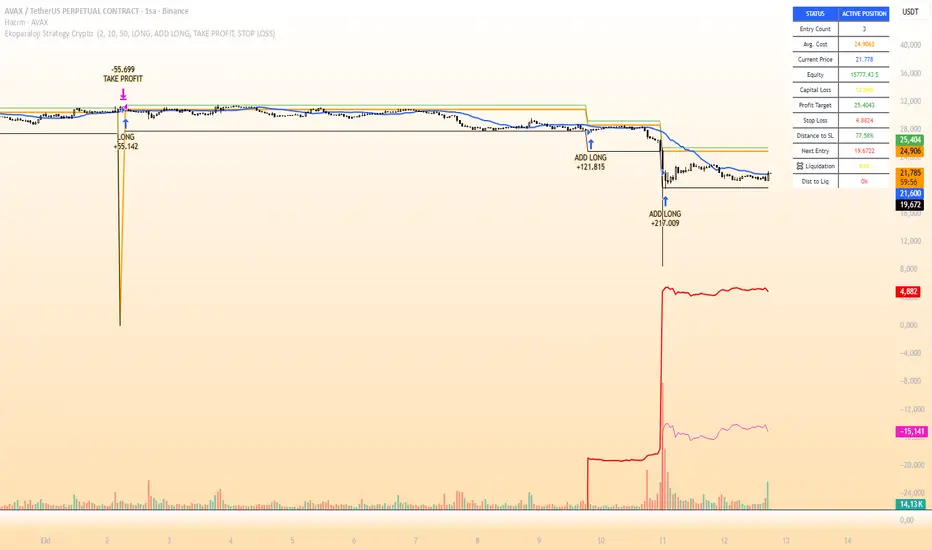

Ekoparaloji Cyrpto StrategyEkoparaloji Crypto Strategy - User Information Document

📊 Strategy Overview

This strategy provides long-term position management in cryptocurrency markets using the averaging down (pyramiding) technique. The basic logic is to controllably grow positions as prices decline and exit when specific profit targets are reached.

🎯 Key Features

✅ Automatic Entry System

Market direction is determined using a proprietary trend identification algorithm

Trades are only opened in uptrends

Initial position opens automatically when specific conditions are met

📈 Pyramiding Mechanism

New positions are automatically added as price decreases

Up to 10 positions can be added maximum

Each addition occurs at predetermined decline levels

Risk management through dynamic position sizing

💰 Profit and Loss Management

Take Profit: All positions close when the specified percentage above average cost is reached

Stop Loss (Optional): Protects a specified percentage of total capital

A certain ratio of available capital is used in each trade

📊 Visual Tracking System

The following information is displayed in real-time on the chart:

✅ Average cost level

✅ Profit target level

✅ Stop loss level (if active)

✅ Next pyramiding level

✅ Liquidation (capital reset) level

✅ Trend indicator

🛡️ Risk Management Features

1. Dynamic Capital Protection

Automatic exit when losses exceed a specified percentage of total capital

Complete loss scenario can be previewed through liquidation level calculation

2. Position Control System

Protection preventing multiple trades on the same bar

Double trigger prevention mechanism

Maximum position limit

3. Time Filter

Optional trading within a date range

Ideal for testing on historical data

📱 Information Panel

Information table always visible in the upper right corner of the strategy:

When Position is Open:

Number of active positions

Average cost

Current price

Total capital status

Capital loss percentage

Profit target

Stop loss level and distance

Next entry level

Liquidation level and distance

When No Position:

Market trend (Uptrend/Downtrend)

Ready to trade?

Reason for waiting

Initial position size

Target profit percentage

⚙️ Adjustable Parameters

Customizable by user:

💵 Capital Amount: Base amount to be used for each position

📊 Profit Target: Profit percentage at which to exit

🛑 Stop Loss: Usage status and maximum loss percentage

📅 Time Filter: Start and end dates for testing

💬 Trade Comments: Custom labels for each trade

📘 Understanding Leverage Effect

1. What is the Leverage Effect?

Although there's no real leverage in the spot market, when Capital Amount is increased, capital usage works like leverage:

Capital Amount 5% (1.0x): 100% capital usage with full pyramiding = All your money in trades

Capital Amount 10% (2.0x): 200% capital usage with full pyramiding = Attempting to open trades worth 2x your capital

Capital Amount 15% (3.0x): 300% capital usage with full pyramiding = Attempting to open trades worth 3x your capital

⚠️ IMPORTANT: If your capital runs out in the spot market, you cannot open new positions, therefore it's recommended to keep Capital Amount at 5% or below!

⚠️ Important Warnings

Pyramiding Risk: If price continues to decline, position grows and risk increases

Capital Requirements: Up to 10 positions can be added, requiring sufficient capital

Trend Dependency: Only works in uptrends

Backtest Results: Past performance is not a guarantee of future results

Real Trading Risks: Slippage, commissions, and market conditions can affect results

🎓 How to Use

Add the strategy to your chart

Adjust parameters according to your risk appetite

Examine past performance by backtesting

Optionally set up alerts to activate notifications

Test with paper trading first

This strategy is for educational purposes. Do your own research and only trade with capital you can afford to lose.

Disclaimer: This strategy is not financial advice. All investment decisions are the user's responsibility.

Happy trading! 📊

Ekoparaloji Strategy Crypto Ekoparaloji Crypto Strategy - User Information Document

📊 Strategy Overview

This strategy provides long-term position management in cryptocurrency markets using the averaging down (pyramiding) technique. The basic logic is to controllably grow positions as prices decline and exit when specific profit targets are reached.

🎯 Key Features

✅ Automatic Entry System

Market direction is determined using a proprietary trend identification algorithm

Trades are only opened in uptrends

Initial position opens automatically when specific conditions are met

📈 Pyramiding Mechanism

New positions are automatically added as price decreases

Up to 10 positions can be added maximum

Each addition occurs at predetermined decline levels

Risk management through dynamic position sizing

💰 Profit and Loss Management

Take Profit: All positions close when the specified percentage above average cost is reached

Stop Loss (Optional): Protects a specified percentage of total capital

A certain ratio of available capital is used in each trade

📊 Visual Tracking System

The following information is displayed in real-time on the chart:

✅ Average cost level

✅ Profit target level

✅ Stop loss level (if active)

✅ Next pyramiding level

✅ Liquidation (capital reset) level

✅ Trend indicator

🛡️ Risk Management Features

1. Dynamic Capital Protection

Automatic exit when losses exceed a specified percentage of total capital

Complete loss scenario can be previewed through liquidation level calculation

2. Position Control System

Protection preventing multiple trades on the same bar

Double trigger prevention mechanism

Maximum position limit

3. Time Filter

Optional trading within a date range

Ideal for testing on historical data

📱 Information Panel

Information table always visible in the upper right corner of the strategy:

When Position is Open:

Number of active positions

Average cost

Current price

Total capital status

Capital loss percentage

Profit target

Stop loss level and distance

Next entry level

Liquidation level and distance

When No Position:

Market trend (Uptrend/Downtrend)

Ready to trade?

Reason for waiting

Initial position size

Target profit percentage

⚙️ Adjustable Parameters

Customizable by user:

💵 Capital Amount: Base amount to be used for each position

📊 Profit Target: Profit percentage at which to exit

🛑 Stop Loss: Usage status and maximum loss percentage

📅 Time Filter: Start and end dates for testing

💬 Trade Comments: Custom labels for each trade

📘 Understanding Leverage Effect

1. What is the Leverage Effect?

Although there's no real leverage in the spot market, when Capital Amount is increased, capital usage works like leverage:

Capital Amount 5% (1.0x): 100% capital usage with full pyramiding = All your money in trades

Capital Amount 10% (2.0x): 200% capital usage with full pyramiding = Attempting to open trades worth 2x your capital

Capital Amount 15% (3.0x): 300% capital usage with full pyramiding = Attempting to open trades worth 3x your capital

⚠️ IMPORTANT: If your capital runs out in the spot market, you cannot open new positions, therefore it's recommended to keep Capital Amount at 5% or below!

⚠️ Important Warnings

Pyramiding Risk: If price continues to decline, position grows and risk increases

Capital Requirements: Up to 10 positions can be added, requiring sufficient capital

Trend Dependency: Only works in uptrends

Backtest Results: Past performance is not a guarantee of future results

Real Trading Risks: Slippage, commissions, and market conditions can affect results

🎓 How to Use

Add the strategy to your chart

Adjust parameters according to your risk appetite

Examine past performance by backtesting

Optionally set up alerts to activate notifications

Test with paper trading first

This strategy is for educational purposes. Do your own research and only trade with capital you can afford to lose.

Disclaimer: This strategy is not financial advice. All investment decisions are the user's responsibility.

Strategy with Reference Lines📊 Strategy with Reference Lines

Description:

This strategy uses a contrarian approach based on the analysis of the previous candle to identify entry and exit points. The strategy draws horizontal reference lines at important levels of the previous candle and generates buy/sell signals based on the candle's direction.

Key Features:

🔹 Multi-Timeframe Analysis: Configurable for 1H, 2H, 3H, 4H, 6H, 12H, and 1D

🔹 Reference Lines: High, low, close, and midpoint (50%) of the previous candle

🔹 Visual Signals: Labels with prices and actions (BUY/SELL/TP)

🔹 Optional Trading: Enable/disable automatic order execution

🔹 Complete System: Automatic entry, Take Profit, and Stop Loss

🔹 Alerts: Notifications when a new candle is detected

Strategy Logic:

When the previous candle is POSITIVE:

Signal: 🔴 SELL at the previous candle's close

Take Profit: 🎯 Midpoint (50%) of the previous candle

Stop Loss: 🔴 High of the previous candle

When the previous candle is NEGATIVE:

Signal: 🟢 BUY at the previous candle's close

Take Profit: 🎯 Midpoint (50%) of the previous candle

Stop Loss: 🟢 Low of the previous candle

Visual Elements:

Green Line: High of the previous candle (when positive)

Red Line: Low of the previous candle (when negative)

Yellow Line: Close of the previous candle (always present)

Blue Line: Midpoint (50%) of the previous candle (always present)

Labels: Prices and actions with emojis for easy identification

Settings:

Timeframe: Default 4H (configurable)

Auto Trading: Disabled by default (safety)

Alerts: Include entry prices, TP, and SL

Recommended Usage:

✅ Visual Analysis: Use with trading disabled for analysis

✅ Backtesting: Enable trading to test historically

✅ Swing Trading: Ideal for 4H or higher timeframes

✅ Risk Management: Automatic SL and TP for protection

Risk Disclaimer:

This strategy is for educational and analysis purposes only. Always test in a simulation environment before using with real capital. Trading involves significant risks and may result in losses.

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

SHALOM TRADING HUB – Bollinger Band SystemSHALOM TRADING HUB – Bollinger Band System (Strategy)

All-in-one BB system with both Breakout and Mean-Reversion modes.

Automatic ENTRY / EXIT / STOP-LOSS, optional Mid-Band Exit, ATR or % risk, and built-in alerts. Backtest-ready.

What it does

Bollinger Bands: Basis = SMA(length); Upper/Lower = ±(mult × StDev).

Signals

Breakout mode

LONG → price crosses above Upper

SHORT → price crosses below Lower

Mean-Reversion mode

LONG → price re-enters above Lower

SHORT → price re-enters below Upper

Risk / Exits

ATR mode: SL = ATR × Mult, TP = SL × Risk:Reward

% mode: SL = %Stop, TP = %Take Profit

Optional Mid-Band (Basis) cross exit.

Visuals: BB lines + active Entry / SL / TP overlays + last-bar price labels.

Alerts: Breakout / Mean-Reversion signals and TP/SL hits.

Inputs (Settings)

Source, Length, Multiplier – BB calculation.

Signal Mode – Breakout or Mean Reversion.

Use ATR Stop/Target? – On = ATR; Off = %.

ATR Length, ATR Mult (SL), Risk:Reward (TP)

% Stop, % Take Profit (when ATR is Off)

Also exit on Mid-Band cross? – On/Off.

Alerts only on bar close? – Filters to confirmed bars.

Entry / Exit / Stop

Entry: Auto when the chosen signal condition triggers.

Stop-Loss: Placed from ATR or % settings.

Take-Profit: Set by R:R or % settings.

Mid-Band Exit (optional):

LONG → exit if close < Basis

SHORT → exit if close > Basis

Alerts (How-to)

Add the strategy to the chart → click Alerts (⚠️).

Condition: “SHALOM BB System” → choose:

BB Breakout LONG / SHORT

BB Mean-Reversion LONG / SHORT

Long TP Hit / Long SL Hit / Short TP Hit / Short SL Hit

Choose Once per bar or Once per bar close.

Backtest Tips

Match timeframe to your instrument.

Tune ATR/Mult, R:R, % to volatility.

Session filter (e.g., 09:20–15:20 IST) can be added easily in code.

Default pyramiding = 0; raise if you want multiple entries.

SMC 自動交易 - 4HR- BTC適用# SMC Automated Trading Strategy Whitepaper - Stepped Enhanced Edition

## 1. Strategy Overview

This strategy is designed based on the Smart Money Concept (SMC), integrating Order Block (OB), Change of Character (CHoCH), and strict pullback confirmation conditions. The goal is to enhance trading accuracy and strictly control risk, specifically tailored for trading competitions, meeting the requirements of stability and efficiency.

### Core Strategy Concepts:

- Precise identification of key trend reversal points.

- Strict pullback confirmation to avoid chasing tops or bottoms.

- Clear risk management and take-profit mechanisms to maintain stable risk-reward ratio.

- Supports trading time filtering (Kill Zone) to capture prime volatility windows.

- Multiple visual aids for quick in-trade signal recognition.

## 2. Strategy Logic Flow

### 1. Kill Zone (Optional Activation)

- Default trading time: Taiwan time 15:00 - 18:00.

- Purpose: Focus on high-volatility periods to reduce false signals in choppy markets.

### 2. Order Block Detection

- Current candle range exceeds the previous candle by a specified multiplier (default 0.8).

- Bullish OB: Bullish candle with expanded range.

- Bearish OB: Bearish candle with expanded range.

- Flexible OB sensitivity adjustment according to market volatility.

### 3. Change of Character (CHoCH)

- Initial trend reversal confirmation:

- Bullish CHoCH: Close above previous candle’s high.

- Bearish CHoCH: Close below previous candle’s low.

### 4. Pullback Confirmation (Core Condition)

- Avoid premature entries by requiring a pullback to the prior OB:

- Long: Pullback touches the previous Bullish OB high.

- Short: Pullback touches the previous Bearish OB low.

### 5. Fair Value Gap (FVG) Detection (Optional)

- Detect price imbalances as additional confirmation signals.

## 3. Entry Logic

### Long Position:

- Previous Bullish OB is formed.

- Current candle completes a pullback to the prior OB high.

- Current candle closes above the previous high (CHoCH confirmation).

- (Optional) Within Kill Zone.

### Short Position:

- Previous Bearish OB is formed.

- Current candle completes a pullback to the prior OB low.

- Current candle closes below the previous low (CHoCH confirmation).

- (Optional) Within Kill Zone.

## 4. Risk Management & Exit Strategy

### Stop Loss:

- Long: Current candle’s low minus buffer points (default 50 points).

- Short: Current candle’s high plus buffer points (default 50 points).

### Take Profit:

- Default Risk-Reward Ratio (RR): 2.0 (customizable).

- Automatically calculates target take-profit level.

### Full Automation:

- This is a fully automated strategy. Orders are placed automatically upon conditions being met, requiring no manual intervention.

## 5. Visual Aids

- Bullish OB: Green upward triangle.

- Bearish OB: Red downward triangle.

- Bullish CHoCH: Blue circle.

- Bearish CHoCH: Orange circle.

- FVG: Highlighted zones (optional).

> **Advantage:** Quick market status recognition during trades, improving strategy transparency.

## 6. Strategy Advantages

✅ Dual trend reversal confirmation: OB + CHoCH.

✅ Strict pullback requirement to reduce false breakouts.

✅ Clear risk control and stable risk-reward ratio.

✅ Visual aids + time filter for clear in-trade decisions.

✅ Fully automated trading reduces human error.

## 7. Application Scenarios

- Trading competitions: Designed for high win-rate and strict risk control.

- FTMO and similar evaluation challenges.

- Intraday or swing trading strategy frameworks.

- High-volatility assets: Crypto / Forex / Index CFDs.

## 8. Risk Warning

- Strategy is based on historical backtesting; live trading should consider slippage and liquidity risks.

- During high volatility periods, use proper money management tools and strictly execute stop losses.

## 9. Version Note

Version: Stepped Enhanced Edition (Updated April 2025)

Developer: natwad3000

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

RSI Momentum ScalperOverview

The "RSI Momentum Scalper" is a Pine Script v5 strategy crafted for trading highly volatile markets, with a special focus on newly listed cryptocurrencies. This strategy harnesses the Relative Strength Index (RSI) alongside volume analysis and momentum thresholds to pinpoint short-term trading opportunities. It supports both long and short trades, managed with customizable take profit, stop loss, and trailing stop levels, which are visually plotted on the chart for easy tracking.

Why I Created This Strategy

I developed the "RSI Momentum Scalper" because I was seeking a reliable trading strategy tailored to newly listed, highly volatile cryptocurrencies. These assets often experience rapid price fluctuations, rendering traditional strategies less effective. I aimed to create a tool that could exploit momentum and volume spikes while managing risk through adaptable exit parameters. This strategy is designed to address that need, offering a flexible approach for traders in dynamic crypto markets.

How It Works