Range: OHLC vs Previous OHLC - Version 2Version 1 here -

This is essentially the same as version 1 with one update. You have the freedom to independently choose OHLC for current candle and prior candle.

To elaborate further, Version 1 had 1 choice. For example, Close; you could only compare the close of prior candle to the current candle.

Version 2; you can compare close of the current candle to the low of the prior candle.

在腳本中搜尋"range"

Range & Consolidation DetectorHello friends,

I’m excited to share my latest discovery with you — the Range & Consolidation Detector. This script is built on a unique methodology I’m truly proud of. It uses no traditional indicators like ADX, RSI, or ATR — just pure statistics and mathematics under the hood. No parameters to tweak, no settings to guess — it just works, right out of the box.

🛠️ How It Works

At its core is a proprietary formula that reliably identifies ranging conditions across all tickers and timeframes. It’s simple, robust, and consistent — exactly what traders need to spot sideways markets without noise or lag.

🔥 Key Features

Pine Script v6 – Uses the latest version for maximum performance

Zero configuration – No inputs to adjust, no hidden settings — the algorithm works automatically

Optimized performance – Runs efficiently for smooth charting

Universal compatibility – Works flawlessly on any asset and timeframe, in every market condition — from euphoric peaks to choppy ranges

📸 Visual Examples

If you’d like access or have any questions, feel free to reach out to me directly via DM.

👋 Good luck and happy trading!

付費腳本

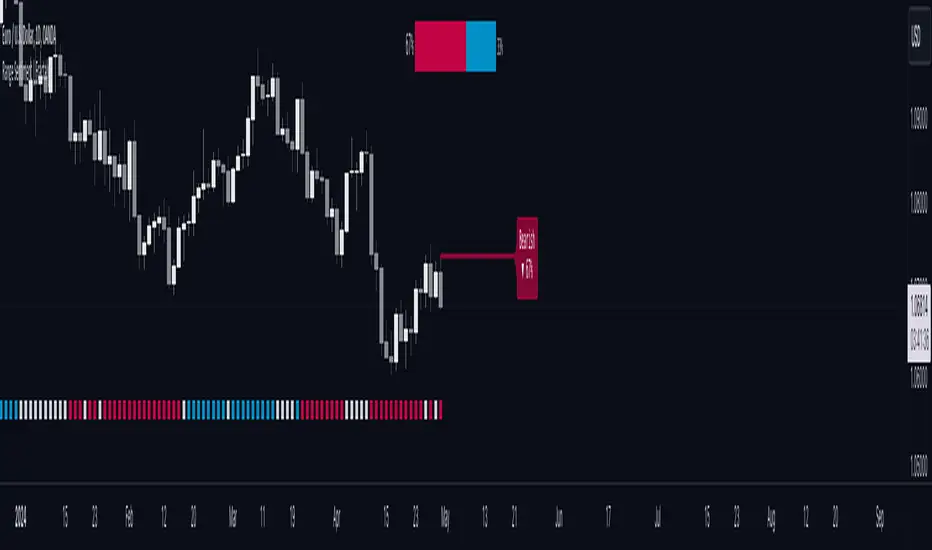

Range Sentiment | FractalystWhat’s the purpose of this indicator?

This indicator aims to calculate the percentage level of bullish or bearish fluctuations within equally divided price sections, in the latest price range.

----

How does this indicator calculate the current sentiment?

This indicator calculates the current sentiment by identifying the highest swing high and the lowest swing low, then evenly dividing the distance between them into percentage amounts. If the price is above the 50% mark, it indicates bullishness, whereas if it's below 50%, it suggests bearishness.

----

Is this sentiment the same as the ones on online websites?

No, the sentiment as discussed earlier, is based on analyzing price action on charts and calculating the current range in percentage.

----

What methods do other websites typically use to determine market sentiment?

1. Broker Data Aggregation: Compiling data from various forex brokers to assess the percentage of long and short positions taken by traders.

2. Lot Size Analysis: Considering the size of positions taken by traders, where a significant number of large positions in one direction may indicate strong bullish or bearish sentiment.

3. Order Flow Analysis: Tracking the flow of orders in the forex market, with an increase in buy orders suggesting bullish sentiment and a surge in sell orders indicating bearish sentiment.

4. Sentiment Surveys: Conducting surveys among forex traders to gather opinions about future price movements and gauge sentiment.

----

What are the options to display the current market sentiment?

1. Table - located at top centre of your charts

2. Label - indicating the 50% level of the current range mentioned above

----

How can I analyze how the sentiment worked on historical data?

There are 3 available options:

1. Shapes

2. Candles

3. Background

- White colour/transparent background denote a weak or uncertain trend, where the bullish or bearish degree is less than 60%.

- Blue colour indicates that the price is trading bullish.

- Red colour indicates that the price is trading bearish.

----

On what market and timeframe this indicator operates on?

The Range Sentiment indicator is applicable to all markets and timeframes.

When switching between timeframes, the values remain consistent because it utilizes the daily bias to determine the sentiment for the current day.

----

How can I use this indicator?

1. Add "Range Sentiment | Fractalyst" to your TradingView chart.

2. Choose the pair you want to analyze or trade intraday/during session.

3. Make sure the sentiment is showing you a bullish or a bearish degree of higher than 60%.

(To avoid potentially choppy price action)

4. Use your favourite entry model to trade in the same direction that the sentiment is showing you.

5. Determine your take profit based on the daily swing level OR previous daily high if the bullish degree is above +60% and previous daily low if the bearish degree is +60%.

6. Risk adjustment and Trade management based on your personal preferences.

Example:

----

User-input settings and customizations

----

What makes this indicator original?

1. It utilizes the daily timeframe's current range to determine the day's bias degree in percentage.

2. Apart from presenting the current sentiment in a sentimental table, it also visualizes the 50% threshold as a label, indicating where price may shift direction from a sentiment perspective.

3. It offers the feature to analyze historical data, allowing users to observe indicator performance through shapes, candles, and background colors.

4. By integrating market sentiment directly into the charts, it simplifies the trading process, removing the reliance on online websites and services for sentiment analysis, which often rely on limited brokerage data and resources.

5. Unlike most sentiment websites that primarily focus on forex pairs sentiment data, this indicator stands out by its capability to analyze sentiment across all markets. Moreover, it provides real-time updates, ensuring traders have access to the latest sentiment information regardless of the market they are trading in.

----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer.

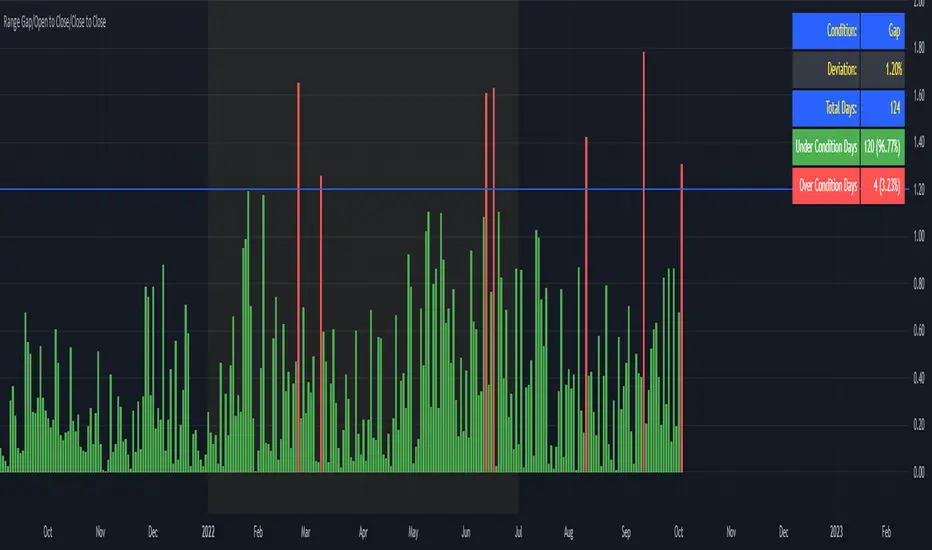

Range Gap/Open to Close/Close to CloseThis indicator shows the percentage variation of:

gap

close to close (day including gap)

open to close (without gap)

The green bars represent the days when the variation did not reach the selected range. The red bars show the days when the variation was higher than the selected range.

Best timeframe : DAY

Range support and resistanceWelcome all

==========

This script specially is for Kunal Saraogi Senani Traders and beginners.

.

With this script you can find support and resistance for input range on any time-frame chart.

You need not draw line by own. You just input your desired range and this script will do your work automatically.

You can adjust range according to your choice.

Also have an option to select range source which help you to find support and resistance on the basis of close price or high/low of input range. Default range source is close price.

.

Latest support and resistance value labels also display on the chart.

.

To use this script, add to favorite and apply on chart.

.

Feel free to comment your suggestions.

.

Thanks all

Range Identifying For cheese trade, range is a important sign.

This is the first version trying to identify the range.

Use 2 white lines to show the range's high and low.

Hope this helps, and welcome comment.

Range EstimateAs a trader I need to know what are the best ranges to get in or out

So this tool try to help a little bit .

First we have Pivot points (all forms with fib ,traditional etc)

next is percentage channel (uper=upper % from close and Lper=lower % from close) , in btc I use 3% up or low for 1 hour candles as it give me good range of lower and upper bound . This you need to change for different TF or different assets

next we have Bollinger upper and lower (Bup= Bollinger upper and Blow=Bollinger lower) it has also MTF function

last we MA =,20,50,100,200

in total the aim of this indicator is to give fast glance on the numbers that important to you as trader fast with a clean graph so you can add your indicator to it to see better how they work

The info panel you can change the font size, you can change distance by offset

and the position on the graph , you need to adjust with position -in this case since it btc I put number of 8700

let say it ETH then I put a number 5% above the close number

if it XRP = then the same trick , lets say 0.3 etc

Range Percent Histogram📌 Range Percent Histogram – Indicator Description

The Range Percent Histogram is a custom indicator that behaves like a traditional volume histogram, but instead of showing traded volume it displays the percentage range of each candle.

In other words, the height of each bar represents how much the price moved (in percentage terms) within that candle, from its low to its high.

🔧 What it shows

The indicator has two main components:

Component Description

Histogram Bars Columns plotted in red or green depending on the candle direction (green = bullish candle, red = bearish). The height of each bar = (high - low) / low * 100. That means a candle that moved, for example, 1 % from its lowest point to its highest point will show a bar with 1 % height.

Moving Average (optional) A 20-period Simple Moving Average applied directly to the bar values. It can be turned ON/OFF via a checkbox and helps you detect whether current range activity is above or below the average range of the past candles.

⚙️ How it works

Every time a new candle closes, the indicator calculates its range and converts it into a percentage.

This value is drawn as a column under the chart.

If the closing price is above the opening price → the bar is green (bullish range).

If the closing price is below the opening price → the bar is red (bearish range).

When the Show Moving Average option is enabled, a smooth line is plotted on top of the histogram representing the average percentage range of the last 20 candles.

📈 How to use it

This indicator is very helpful for detecting moments of range expansion or contraction.

One powerful way to use it is similar to a volume exhaustion / low-volume pattern:

Situation Interpretation

Consecutive bars with very low height Price is in a period of low volatility → possible accumulation or "pause" phase.

A sudden large bar after a series of small ones Indicates a strong pickup in volatility → often marks the start of a new impulse in the direction of the breakout.

Range + VWAP + Gann Levels + ZL AMA + Gann Square Num# Multi-Strategy Market Analysis Indicator

## Overview

This comprehensive indicator combines several powerful technical analysis tools to help traders identify potential price movements, market trends, and key support/resistance levels. By integrating price range prediction, volume-weighted averages, adaptive moving averages, and Gann-based mathematical levels, this indicator provides a complete toolkit for market analysis.

## Components & How They Work

### 1. Range Calculator

**What it does:** Calculates the expected price range based on current volatility, useful for predicting potential price movements during a specific time period.

**How it works:**

- Uses the current price level and VIX (Volatility Index) to estimate how far the price might move in a given number of days

- Applies the square root of time principle (volatility grows with the square root of time)

- Displays upper and lower bounds of the expected price range

- Shows the calculation details in a convenient table

**How to use it:**

- Enter the current price level, VIX value, and number of days

- red line indicates potential resistance

- green line indicates potential support

- Useful for options trading, setting stop-loss levels, or preparing for upcoming market events

### 2. Gann Square Numbers

**What it does:** Identifies mathematically significant price levels based on square numbers.

**How it works:**

- Takes the square root of the current price

- Calculates the next 5 square numbers above the current price (upper levels)

- Calculates the 5 square numbers below the current price (lower levels)

- Draws these levels as horizontal lines on the chart

**How to use it:**

- Pink lines (upper levels) show potential resistance levels

- Blue lines (lower levels) show potential support levels

- These mathematical levels often coincide with significant market reactions

- Based on W.D. Gann's theory that price tends to respect mathematical square numbers

### 3. Zero Lag Adaptive Moving Average (AMA)

Bullish Scenario

Bearish Scenario

**What it does:** Provides a dynamic moving average that adapts to changing market conditions, reducing lag during trends while filtering noise during sideways markets.

**How it works:**

- Calculates an "Efficiency Ratio" that measures the directional movement relative to volatility

- Adjusts the smoothing factor based on market efficiency

- Uses a faster smoothing factor during trending markets and slower smoothing during sideways markets

- Background color changes to indicate the trend direction (green for uptrend, red for downtrend)

**How to use it:**

- When price is above the AMA line with green background: Strong uptrend

- When price is below the AMA line with red background: Strong downtrend

- Helpful for trend identification and potential entry/exit points

### 4. Gann Stepline Levels

**What it does:** Creates dynamic support and resistance levels based on multiple SMAs (Simple Moving Averages) of different lengths.

**How it works:**

- Calculates two key dynamic levels:

- Gann 50% Level: Average of 90 and 144-period SMAs

- Gann Level: Average of six different SMAs (90, 144, 180, 216, 240, 288)

- These levels adjust automatically as the market evolves

**How to use it:**

- Blue line (Gann 50% Level) acts as dynamic support in uptrends and resistance in downtrends

- Orange line (Gann Level) serves as a longer-term trend indicator

- Price interaction with these levels often indicates potential reversal or continuation points

### 5. Anchored VWAP (Volume-Weighted Average Price)

**What it does:** Shows the average price weighted by volume starting from a specific anchor point.

**How it works:**

- Calculates the average price weighted by volume from a chosen anchor period (Session, Day, Week, Month)

- Resets calculations at the beginning of each new period

- Shows where the current price is relative to the average trading price

**How to use it:**

- Price above VWAP: Bullish bias, buyers are in control

- Price below VWAP: Bearish bias, sellers are in control

- VWAP often acts as dynamic support/resistance level

- Institutional traders often use VWAP for order execution

## Key Benefits

- **Comprehensive Analysis:** Combines volatility-based, trend-following, volume-weighted, and mathematical approaches

- **Multi-timeframe Perspective:** Different components operate on various timeframes for a complete market view

- **Visual Clarity:** Color-coded lines and background help quickly identify market conditions

- **Customizable Components:** Range Calculator, VWAP, and Gann Square Numbers can be adjusted to fit your trading style

## How to Interpret When Used Together

- **Strong Trend Confirmation:** When AMA shows a trend and price respects the Gann Dynamic levels

- **Reversal Signals:** When price reaches the expected range bounds and encounters a Gann Square Number

- **High-Probability Zones:** Areas where multiple components show support/resistance at similar levels

- **Volatility Assessment:** Compare the expected range from the Range Calculator with the actual price movement

This indicator combines statistical, trend-following, and mathematical approaches to market analysis, providing traders with a well-rounded view of market conditions and potential price movements.

Range Filter Buy and Sell 5min## **Enhanced Range Filter Strategy: A Comprehensive Overview**

### **1. Introduction**

The **Enhanced Range Filter Strategy** is a powerful technical trading system designed to identify high-probability trading opportunities while filtering out market noise. It utilizes **range-based trend filtering**, **momentum confirmation**, and **volatility-based risk management** to generate precise entry and exit signals. This strategy is particularly useful for traders who aim to capitalize on trend-following setups while avoiding choppy, ranging market conditions.

---

### **2. Key Components of the Strategy**

#### **A. Range Filter (Trend Determination)**

- The **Range Filter** smooths price fluctuations and helps identify clear trends.

- It calculates an **adjusted price range** based on a **sampling period** and a **multiplier**, ensuring a dynamic trend-following approach.

- **Uptrends:** When the current price is above the range filter and the trend is strengthening.

- **Downtrends:** When the price falls below the range filter and momentum confirms the move.

#### **B. RSI (Relative Strength Index) as Momentum Confirmation**

- RSI is used to **filter out weak trades** and prevent entries during overbought/oversold conditions.

- **Buy Signals:** RSI is above a certain threshold (e.g., 50) in an uptrend.

- **Sell Signals:** RSI is below a certain threshold (e.g., 50) in a downtrend.

#### **C. ADX (Average Directional Index) for Trend Strength Confirmation**

- ADX ensures that trades are only taken when the trend has **sufficient strength**.

- Avoids trading in low-volatility, ranging markets.

- **Threshold (e.g., 25):** Only trade when ADX is above this value, indicating a strong trend.

#### **D. ATR (Average True Range) for Risk Management**

- **Stop Loss (SL):** Placed **one ATR below** (for long trades) or **one ATR above** (for short trades).

- **Take Profit (TP):** Set at a **3:1 reward-to-risk ratio**, using ATR to determine realistic price targets.

- Ensures volatility-adjusted risk management.

---

### **3. Entry and Exit Conditions**

#### **📈 Buy (Long) Entry Conditions:**

1. **Price is above the Range Filter** → Indicates an uptrend.

2. **Upward trend strength is positive** (confirmed via trend counter).

3. **RSI is above the buy threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **📉 Sell (Short) Entry Conditions:**

1. **Price is below the Range Filter** → Indicates a downtrend.

2. **Downward trend strength is positive** (confirmed via trend counter).

3. **RSI is below the sell threshold** (e.g., 50, to confirm momentum).

4. **ADX confirms trend strength** (e.g., above 25).

5. **Volatility is supportive** (using ATR analysis).

#### **🚪 Exit Conditions:**

- **Stop Loss (SL):**

- **Long Trades:** 1 ATR below entry price.

- **Short Trades:** 1 ATR above entry price.

- **Take Profit (TP):**

- Set at **3x the risk distance** to achieve a favorable risk-reward ratio.

- **Ranging Market Exit:**

- If ADX falls below the threshold, indicating a weakening trend.

---

### **4. Visualization & Alerts**

- **Colored range filter line** changes based on trend direction.

- **Buy and Sell signals** appear as labels on the chart.

- **Stop Loss and Take Profit levels** are plotted as dashed lines.

- **Gray background highlights ranging markets** where trading is avoided.

- **Alerts trigger on Buy, Sell, and Ranging Market conditions** for automation.

---

### **5. Advantages of the Enhanced Range Filter Strategy**

✅ **Trend-Following with Noise Reduction** → Helps avoid false signals by filtering out weak trends.

✅ **Momentum Confirmation with RSI & ADX** → Ensures that only strong, valid trades are executed.

✅ **Volatility-Based Risk Management** → ATR ensures adaptive stop loss and take profit placements.

✅ **Works on Multiple Timeframes** → Effective for day trading, swing trading, and scalping.

✅ **Visually Intuitive** → Clearly displays trade signals, SL/TP levels, and trend conditions.

---

### **6. Who Should Use This Strategy?**

✔ **Trend Traders** who want to enter trades with momentum confirmation.

✔ **Swing Traders** looking for medium-term opportunities with a solid risk-reward ratio.

✔ **Scalpers** who need precise entries and exits to minimize false signals.

✔ **Algorithmic Traders** using alerts for automated execution.

---

### **7. Conclusion**

The **Enhanced Range Filter Strategy** is a powerful trading tool that combines **trend-following techniques, momentum indicators, and risk management** into a structured, rule-based system. By leveraging **Range Filters, RSI, ADX, and ATR**, traders can improve trade accuracy, manage risk effectively, and filter out unfavorable market conditions.

This strategy is **ideal for traders looking for a systematic, disciplined approach** to capturing trends while **avoiding market noise and false breakouts**. 🚀

Range Detection [No Repaint]DETECTS RANGE EARLY

Using Confirmed Data:

All calculations now use to reference the previous completed candle

Signals are only generated based on completed candles

Range state is stored and confirmed before displaying

Key Changes to Prevent Repainting:

ATR calculations use previous candle data

Bollinger Bands calculate from previous closes

Price range checks use previous highs and lows

Range state is confirmed before displaying

How to Verify No Repainting:

Signals will only appear after a candle closes

Historical signals will remain unchanged

Alerts will only trigger on confirmed changes

This means:

The indicator will be slightly delayed (one candle)

But signals will be more reliable

Historical analysis will be accurate

Backtesting results will match real-time performance

Usage Tips with No-Repaint Version:

Wait for candle close before acting on signals

Use the confirmed range state for decision making

Consider the one-candle delay in your strategy timing

Alerts will only trigger on confirmed condition changes

Would you like me to:

Add a parameter to choose between real-time and no-repaint modes?

Add visual indicators for pending vs confirmed signals?

Modify the sensitivity of the range detection?

Range Force Impulse The "Range Force Impulse" indicator combines 4 useful indicators into one, freeing up chart real-estate and giving the trader insight into trend health, bull/bear commitment, range and volatility all at a glance.

The indicator consists of the following:

Direction - True Range and Average True Range columns shown above and below 0 depending on direction of the period's price

-- TR (gray) shows the current period's trading volatility

-- ATR (Impulse colors, see below) shows an EMA of TR over a specified length

-- Can be used to determine stops and targets (Example: Stop loss at prev close - ATR, Target at 2x ATR)

Index - Alexander Elder's EMA of (change(close) * volume), shows crosses above 0 (green) and below 0 (red), and intermediate signals

-- Shows bull vs. bear interest/commitment/dominance

-- Elder recommends EMA length of 2 for daily chart buy/sell signals, and 13 for weekly chart bull/bear dominance & trend direction signals

-- Intermediate signals are shown above 0 when falling (salmon), or below 0 when rising (pale yellow)

System - Range columns are colored using Alexander Elder's censorship system (green: do not short, red: do not long, blue: is up to you)

-- Shows overall trend health (Macd histogram and EMA up/down changes)

Range Marker by Vinay SinghThis indicator marks back and forth range on given timeframes. good indicator to test range breakout.

Range EncapsulatorWhen a user selects a start date and the desired duration, the specified date range will be highlighted. High and low data lines corresponding to this range will be drawn. Additionally, quarter-point interval lines from the previous data range will be displayed between the high and low lines of the current range, provided they fall within those boundaries.

Range-scannerThis indicator shows you the range of the chart based on your specifications in minutes. For example, if you set 30 minutes, the indicator will show you the range of the last 30 minutes in real time, as well as the high and low prices for the same period.

Range TableThe Range Table indicator calculates and displays the Daily Average True Range (ATR), the current day's True Range (TR), and two customizable ATR percentage values in a clean table format. It provides values in ticks, points, and USD, helping traders set stop-loss buffers based on market volatility.

**Features:**

- Displays the Daily ATR (14-period) and current day's True Range (TR) with its percentage of the Daily ATR.

- Includes two customizable ATR percentages (default: 75% and 10%, with the second disabled by default).

- Shows values in ticks, points, and USD based on the symbol's tick size and point value.

- Customizable table position, background color, text color, and font size.

- Toggle visibility for the table and percentage rows via input settings.

**How to Use:**

1. Add the indicator to your chart.

2. Adjust the table position, colors, and font size in the input settings.

3. Enable or disable the 75% and 10% ATR rows or customize their percentages.

4. Use the displayed values to set stop-loss or take-profit levels based on volatility.

**Ideal For:**

- Day traders and swing traders looking to set volatility-based stop-losses.

- Users analyzing tick, point, and USD-based risk metrics.

**Notes:**

- Ensure your chart is set to a timeframe that aligns with the daily ATR calculations.

- USD values are approximate if `syminfo.pointvalue` is unavailable.

Developed by FlyingSeaHorse.

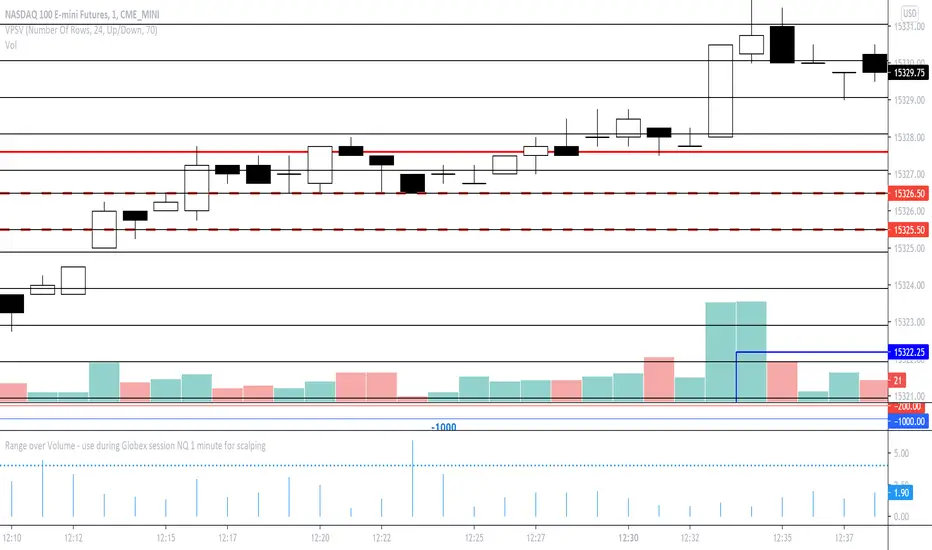

Range over Volume This is a scalping aid for NQ in the 1 minute time range for the Globex session.

Mathematically, the plot is range in ticks divided by 0.1*volume

This returns a histogram plot for RoV (range over volume)

The idea is that candles that ascribe a larger range with minimal volume does because there is unilateral aggression from the buy side, or sell side, and the subsequent behavioural outcome of this will either be an extension of that aggression unilaterally, or commonly, a counter to that aggression!

Wait for a candle to close with the RoV above 4.00. For that candle which formed the RoV above 4.00, plot the highs and lows of that candle and draw a 1.618x and -0.618x Fibonacci extension across it.

Enter short on the -0.618x and take profits at the -1.618x. Use the low of the ROV > 4 candle as a protective stop

Enter long on the 1.618 and take profits at 2.618. Use the high of the ROV > 4 candle as a protective stop

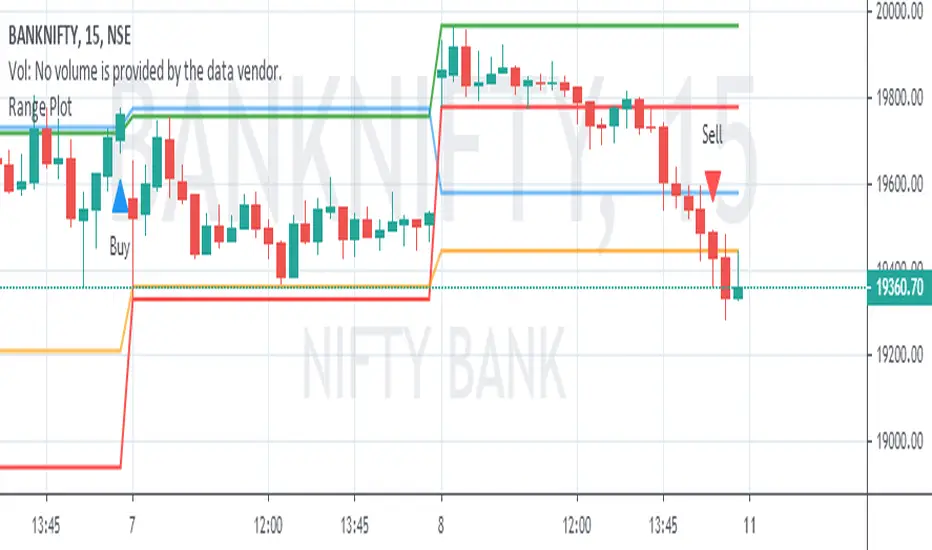

Range PlotToday's first 75 minutes candle high in darker blue color and today's first 75 minutes candle low in darker red color.

Previous trading session last 75 minutes candle high in green color and previous trading session last 75 minutes candle low in orange color.

Today's marking are in blue n red little darker and previous day's last candle marking are in orange and red.

You are likely to familiar with the opening range of 5 min, 15 min, or even of 60 min also. In the opening range, we use today's' candle only. In the range plot, we have made a little addition of previous trading session last candle also. And we got very good results.

Price doesn't know what we have plotted. we just try to make our trading decisions around this area.

Range plot give very good signal in trending scripts and it helps to keep us out from ranging stock.

Range filter v2This version give us signal by the cross of super trend and range filter . since both system try to do the same but calculated different , I was thinking why not to cross them each other by the same way we do with MA length

if you want to see the real trend just remove the // from the plot of super trend and the range finder

alerts and take profit inside

Range Trends Enhanced (eleven11)This indicator automatically draws your Range Trend lines based upon your timeframe. When you select a timeframe, in the options, those lines will be locked in, whenever you switch timeframes on the chart. This allows you to "lock in" a timeframe's trendlines and then view it on different timeframes. But if you want to view the current trendlines for a timeframe then you need to select that "lockdown" timeframe in the settings. The original code was created by eleven11

Range Channel by Atilla YurtsevenThis script creates a dynamic channel around a user-selected moving average (MA). It calculates the relative difference between price and the MA, then finds the average of the positive differences and the negative differences separately. Using these averages, it plots upper and lower bands around the MA as well as a histogram-like oscillator to show when price moves above or below the average thresholds.

How It Works

Moving Average Selection

The indicator allows you to choose among multiple MA types (SMA, EMA, WMA, Linear Regression, etc.). Depending on your preference, it calculates the chosen MA for the selected lookback period.

Relative Difference Calculation

It then computes the percentage difference between the source (typically the closing price) and the MA. (diff = (src / ma - 1) * 100)

Positive & Negative Averages

- Positive differences are averaged and represent how far the price typically moves above the MA.

- Negative differences are similarly averaged for when price moves below the MA.

Range Channel & Oscillator

- The channel is plotted around the MA using the average positive and negative differences (Upper Edge and Lower Edge).

- The “Untrended” histogram plots the difference (diff). Green bars occur when price is above the MA on average, and red bars when below. Two additional lines mark the upper and lower average thresholds on this histogram.

How to Use

Identify Overbought/Oversold Zones: The upper edge can serve as a dynamic overbought level, while the lower edge can suggest potential oversold conditions. When the histogram approaches or crosses these levels, it may signal price extremes relative to its average movement.

Trend Confirmation: Compare price action relative to the channel. If price and the histogram consistently remain above the MA and upper threshold, it could indicate a stronger bullish trend. If they remain below, it might signal a prolonged bearish trend.

Entry/Exit Timings:

- Entry: Traders can look for moments when price breaks back inside the channel from an extreme, anticipating a mean reversion.

- Exit: Watching how price interacts with these dynamic edges can help define stop-loss or take-profit points.

Because these thresholds adapt over time based on actual price behavior, they can be more responsive than fixed-percentage bands. However, like all indicators, it’s most effective when used in conjunction with other technical and fundamental tools.

Disclaimer

This script is provided for educational and informational purposes only. It does not guarantee any specific outcome or profit. Use it at your own discretion and risk.

Trade smart, stay safe.

Atilla Yurtseven

Range of body 30min avggives the average range of the past 30bars and indicates when a candle's body is greater than 150% the average.