Asian Range IndicatorIndicator Name:

Asian Range Indicator

Description:

This TradingView indicator is designed to accurately detect the price range during the Asian session, based on our trading strategy. This range is crucial for planning trades in the European and American sessions. Using advanced algorithms, the indicator automatically identifies and plots the highs and lows within the Asian session period, highlighting them on the chart with shaded areas for clear visualization. This helps traders anticipate breakouts and set more precise entry and exit levels.

How to Use the Indicator:

Add the indicator to your TradingView chart.

Observe the shaded areas representing the Asian range.

Use these levels to plan your trades during the European and American sessions.

Combine with other technical indicators to confirm your trading decisions.

Chart:

The chart published with this script is clean and easy to understand, clearly showing the Asian range highlighted with shaded areas. No other scripts are included, ensuring the indicator's output is easily identifiable. The shaded areas contribute to the visual understanding of the Asian range, helping traders effectively use the script.

在腳本中搜尋"range"

KillZones & Sessions [TradingFinder] Volume | Asia, London & NY🔵 Introduction

🟣 Session

The forex market operates 24 hours a day, 5 days a week, with only Saturdays and Sundays being off; traders often focus on one of the forex trading sessions instead of trying to trade in all markets 24 hours a day.

Trading sessions are time intervals during which a specific financial market is active and trades are conducted. The Asia, London, and New York sessions are the most important trading sessions throughout the 24-hour period, during which a significant amount of money and liquidity enters the market.

🟣 Kill Zone

Traders in financial markets profit from the difference between the price at which they buy or sell and the current market price. Traders have different time horizons for trading.

Among these, some traders engage in daily or even hourly trading and must operate during times when the market has desirable trading volumes and significant price movements.

Kill zones are segments of a session with higher trading volumes and price fluctuations compared to the rest of the session.

🔵 How to Use

🟣 Session Time

The "Asia Session" consists of two sessions: "Sydney" and "Tokyo." The beginning of this session, according to the "UTC" time zone, is at 23:00 and ends at 06:00. Similarly, the beginning of the "Asia KillZone," according to the "UTC" time zone, is at 23:00, and it ends at 03:55.

The "London Session" consists of two sessions: "Frankfurt" and "London." The beginning of this session, according to the "UTC" time zone, is at 07:00, and it ends at 14:25. Similarly, the beginning of the "London KillZone," according to the "UTC" time zone, is at 07:00, and it ends at 09:55.

The beginning of the "New York am" session, according to the "UTC" time zone, is at 14:30, and it ends at 19:25. Similarly, the beginning of the "New York am KillZone," according to the "UTC" time zone, is at 14:30, and it ends at 16:55.

The beginning of the "New York pm" session, according to the "UTC" time zone, is at 19:30, and it ends at 22:55. Similarly, the beginning of the "New York pm KillZone," according to the "UTC" time zone, is at 19:30, and it ends at 20:55.

Important : To prevent session overlap, the working hours of each session have slightly changed.

🔵 Features

🟣 Simultaneous Session and Kill Zone

With this indicator, you can simultaneously view the kill zone and session. High and low lines are used to indicate sessions, while filled areas with color represent kill zones. If you do not want to see kill zones, you can turn off the display settings.

🟣 Candle, Time, and Volume

Using the "More Info" feature, you can see the number of candles, elapsed time, and traded volume within the colored filled area.

🔵 Settings

•Show More Info: To display "More Info," you need to turn on this feature and turn it off whenever you don't need it.

• You can also customize these settings for each session separately :

o Display or hide session.

o Choose session color.

o Set session time range.

o Display or hide kill zone.

o Set kill zone time range.

10 Minute Futures Session Open RangeInspired by SamRecio's 30sec OR script.

The 10 minute Opening Range (OR) dynamically identifies and visualizes the opening range of a trading session within the first 10 minutes after the market opens at 9:30 AM EST, concluding at 4:00 PM EST, reflecting the typical trading hours for U.S. stock exchanges. This indicator is particularly useful for strategies that rely on the initial market momentum and direction established during the early moments of the trading session.

Upon activation, the indicator calculates the highest (orHigh) and lowest (orLow) price levels reached during the first 10 minutes of the trading session, marking these levels with green (for the high) and red (for the low) lines directly on the chart overlay. Additionally, it computes and plots a midpoint (midPoint) between these high and low levels, displayed as a blue line, offering a visual reference for the median of the opening range.

The calculations are reset daily to ensure the indicator accurately reflects the opening range for each new trading session. By doing so, it avoids carrying over data from previous days, maintaining relevance and precision for day traders and those utilizing short-term trading strategies. The indicator also incorporates timezone adjustments to align with the America/New_York timezone, ensuring that the opening range is accurately captured regardless of the user's local timezone.

This tool is invaluable for traders looking to capitalize on breakout or reversion strategies around the opening range, providing clear visual cues for significant price levels established at the start of the trading session. By focusing on the first 10 minutes of trading, it caters to a specific segment of the market that believes the initial movements can set the tone for the rest of the day's trading activity.

HL range by durgaThe script we've been working on is an indicator designed to display the high-low range of the last candlestick on a TradingView chart. It does so by plotting two lines: one for the high and another for the low of the last completed candlestick.

Additionally, the script includes a label that shows the numerical value of the high-low range. This label is positioned between the plotted lines, showing the difference between the high and low prices of the last candlestick.

The script operates in real-time, updating dynamically as new candlesticks form. Furthermore, it automatically removes the label after the close of the candlestick, maintaining a clean and clutter-free chart.

This indicator can help traders quickly visualize and assess the range of the last completed candlestick, aiding in their analysis of price action.

Average True Range Level█ Overview

The indicator uses color-coded columns to represent different levels of normalized ATR, helping traders identify periods of high or low volatility.

█ Calculations

The normalization process involves dividing the current True Range by the Average True Range. The formula for normalized ATR in the code is:

nAtr = nz(barRange/atr)

█ How To Use

Level < 1

During periods when the normalized ATR is less than 1, suggesting a lower level of volatility, traders may explore inside bar strategies. These strategies focus on trading within the range of the previous bar, aiming to capitalize on potential breakout opportunities.

Level between 1 and 3

In instances where the normalized ATR falls between 1 and 3, indicating moderate volatility, a pullback strategy may be considered. Traders look for temporary corrections against the prevailing trend, entering positions in anticipation of the trend's resumption

Level between 2 and 3

Within the range of normalized ATR between 2 and 3, signifying a balanced level of volatility, traders might explore breakout strategies. These strategies involve identifying potential breakout levels using support and resistance or other indicators and entering trades in the direction of the breakout.

Level > 3

When the normalized ATR exceeds 3, signaling high volatility, traders should approach with caution. While not ideal for typical mean reversion strategies, this condition may indicate that the price has become overextended. Traders might wait for subsequent candles, observing a normalized ATR between 2 and 3, to consider mean reversion opportunities after potential overpricing during the high volatility period.

* Note: These strategies are suggestions and may not be suitable for all trading scenarios. Traders should exercise discretion, conduct their own analysis, and adapt strategies based on individual preferences and risk tolerance.

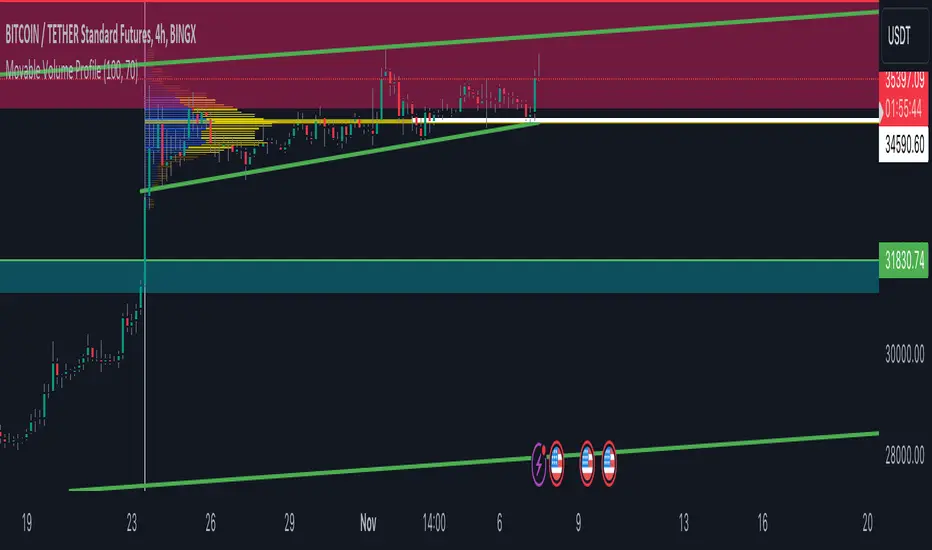

Volume Profile Movable RangeA movable range volume profile indicator is an advanced technical analysis tool that offers traders the flexibility to customize the start date from which the indicator's calculation begins. This feature is particularly valuable for investors who wish to focus on specific time periods and gain a more detailed understanding of price and volume movements within those intervals.

The primary advantage of this indicator lies in its intuitive movable bar, which allows users to easily adjust the start date on the chart. By dragging this bar forward or backward along the time axis, the volume profile calculation is automatically updated to reflect the newly selected date range. This provides traders with a unique ability to adapt to changing market conditions and adjust their analysis in real-time.

By customizing the start date, investors can explore patterns, trends, and support/resistance levels within specific timeframes more accurately and timely. Furthermore, this indicator offers a detailed interpretation of trading volume, aiding traders in assessing the strength or weakness of trends, identifying potential entry and exit points, and making informed decisions in their trading strategies.

In summary, a movable range volume profile indicator is an essential tool for traders seeking more adaptable and precise technical analysis. The ability to easily select and adjust the start date through a movable bar on the chart provides a significant advantage when making data-driven, personalized decisions in financial markets.

Breakout Sideway Range [5ema]This indicator can find the breakout of sideway range. The range create by the bars inside the highest bar.

Compared to my previous script name Breaking Bar , this one is different in important point:

The Highest bar can be found at higher timeframe.

No have opening candles of each session.

-----

How to calculate?

Find the bar have full body or full bar is highest on number left bars.

The sideway range are bars inside highest bar.

Find the bar breakout highest bar are reversal candle patterns.

The highest bar can set up on higher timeframe.

-----

How to set up?

Change the input value of left bar to find the highest bar.

Change the input value of right bar to find the inside bar of highest.

Select the time frame to find the highest bar. Set "chart" if want to follow chart.

Select the way find highest bar, by price high and low or open and close.

-----

How to use?

Choose the signal buy or sell or all.

Change the color or range if want.

Hidden, display, change color background of signal bar.

Make the alert when signal appear.

Refer the signal appear on chart:

- Signal Sell:

- Signal Buy:

-----

This indicator is for reference only, you need your own method and strategy.

If you have any questions, please let me know in the comments.

Trend-Range-Indicator - 3hrThe Trend and Range Indicator is a tool based on median calculation and volatility analysis. It helps identify trends and ranges in price charts. This indicator highlights consolidation areas.

Only work in 3 hours timeframe

Bar Magnified Volume Profile/Fixed Range [ChartPrime]This indicator draws a volume profile by utilizing data from the lower timeframe to get a more accurate representation of where volume occurred on a bar to bar basis. The indicator creates a price range, and then splits that price range into 100 grids by default. The indicator then drops down to the lower timeframe, approximately 16 times lower than the current timeframe being viewed on the chart, and then parses through all of the lower timeframe bars, and attributes the lower timeframe bar volume to all grids that it is touching. The volume is dispersed proportionally to the grids which it is touching by whatever percent of the candle is inside each grid. For example, if one of the lower timeframe bars is interacting with "2" of the grids in the profile, and 60% of the candle is inside of the top grid, 60% of the volume from said candle will be attributed to the grid.

To make all of this magic happen, this script utilizes a quadratic time complexity algorithm while parsing and attributing the volume to all of the grids. Due to this type of algorithm being used in the script, many of the user inputs have been limited to allow for simplicity, but also to prevent possible errors when executing loops. For the most part, all of the settings have been thoroughly tested and configured with the right amount of limitations to prevent these errors, but also still give the user a broad range of flexibility to adjust the script to their liking.

📗 SETTINGS

Lookback Period: The lookback period determines how many bars back the script will search for the "highest high" and the "lowest low" which will then be used to generate the grids in-between

Number Of Levels: This setting determines how many grids there will be within the volume profile/fixed range. This is personal preference, however it is capped at 100 to prevent time complexity issues

Profile Length: This setting allows you to stretch or thin the volume profile. A higher number will stretch it more, vise versa a smaller number will thin it further. This does not change the volume profiles results or values, only its visual appearance.

Profile Offset: This setting allows you to offset the profile to the left or right, in the event the user does not appreciate the positioning of the default location of the profile. A higher number will shift it to the right, vise versa a lower number will shift it to the left. This is personal preference and does not affect the results or values of the profile.

🧰 UTILITY

The volume profile/fixed range can be used in many ways. One of the most popular methods is to identify high volume areas on the chart to be used as trade entries or exits in the event of the price revisiting the high volume areas. Take this picture as an example. The image clearly demonstrates how the 2 highest areas of volume within this magnified volume profile also line up to great areas of support and resistance in the market.

Here are some other useful methods of using the volume profile/fixed range

Identify Key Support and Resistance Levels for Setups

Determine Logical Take Profits and Stop Losses

Calculate Initial R Multiplier

Identify Balanced vs Imbalanced Markets

Determine Strength of Trends

RAhul RAJ Out of Range Trade IndicatorThis indicator is for intraday with the basic logic that any script will always trade in its range.

So , if any script moves away from its range, it will try to come back to its normal range movement.

Suppose average movement of any share is 100 points, and share has moved more than 150 points there is high probability that it will move in opposite direction in order to have average movement of price of 100.

For Stocks please use average period as 15 days for index 30 days.

If share price(YELLOW LINE) moves away from higher or lower blue line, then with the help of volume confirmation a trade can be initiated in opposite direction.

Please note direction needs to be opposite of what has happened in the day.

for eg. upper blue line could be broken , in both situation i.e.. share price is rising or falling,

so if share price is rising and upper blue line is broken:

Bearsish trade can be initiated with the help of price action n volume .

if share price has falledn and upper blue is broken:

Bullish trade can be initiated with the help of volume n price action confirmation.

Release Notes:

Remove dead code

update average period m fib level

True Range Adjusted Exponential Moving Average [CC]The True Range Adjusted Exponential Moving Average was created by Vitali Apirine (Stocks and Commodities Jan 2023 pgs 22-27) and this is the latest indicator in his EMA variation series. He has been tweaking the traditional EMA formula using various methods and this indicator of course uses the True Range indicator. The way that this indicator works is that it uses a stochastic of the True Range vs its highest and lowest values over a fixed length to create a multiple which increases as the True Range rises to its highest level and decreases as the True Range falls. This in turn will adjust the Ema to rise or fall depending on the underlying True Range. As with all of my indicators, I have color coded it to turn green when it detects a buy signal or turn red when it detects a sell signal. Darker colors mean it is a very strong signal and let me know if you find any settings that work well overall vs the default settings.

Let me know if you would like me to publish any other scripts that you recommend!

Visual Range Quarter Points [dasanc]Introduction

This tool can be used in multiple ways:

explore a Symbol's historical volatility for DCA and Grid trading strategies.

combine with Order Blocks as confluence before entering trades

intra-trade management - partial exits and moving SL into profits

Features

Draw Quarter Point levels on chart based on the visible range. Interval between levels is automatically calculated by default to have ~10 levels on chart.

As you scroll through the chart or change timeframes, the interval and levels are updated.

Change the color, width of levels as a percentage of the interval, and draw additional levels as needed.

Choose to display a dashboard with relevant information on levels:

Price range - High and Low on visible range

Interval - display as Currency or PIPs for Forex pairs

Number of Levels drawn

-Cheers, DasanC

True Range ScoreTrue Range Score:

This study transforms the price similar to how z-score works. Instead of using the standard deviation to divide the difference of the source and the mean to determine the sources deviation from the mean we use the true range. This results in a score that directly relates to what multiplier you would be using with the Keltner Channel. This is useful for many applications.

One is the fact that it shows you the momentum of the price and how strong the price movement is. This is also a great metric of volatility. With this you can make a smart Keltner channel by multiplying the mean by the average true range 75th percentile of this score. I in fact do this in my automatic Keltner channel script. I hope this script is useful for you. Thank you for checking this out.

(Source - Mean)/True Range instead of (Source - Mean)/Standard Deviation

super SSL [ALZ]This script is designed and optimized for MULTI TIME

by Ali Zebardast (ALZ)

1.in part of ssl

Original Version credits to Mihkel00

Actual Version i just set alerts and change the parameters for BTCUSDT 1min Chart.

He designed for daily time. I tried to optimize 1 min time-frame .

And fix the errors with OTT

"This script has a SSL / Baseline (you can choose between the SSL or MA), a secondary SSL for continiuation trades and a third SSL for exit trades.

Alerts added for Baseline entries, SSL2 continuations, Exits.

Baseline has a Keltner Channel setting for "in zone" Gray Candles

Added "Candle Size > 1 ATR" Diamonds from my old script with the criteria of being within Baseline ATR range."

2.in part of Range

two Filter Buy and Sell for 3min

Wait For Bar close

ssl2 :Be under the candle for buy

and The bar color must confirm the order of purchase (Blue)

3.in part of OTT

when candles close over HOTT, means an UPTREND SIGNAL

and to Fuchia when candles begin closing under LOTT line to indicate a DOWNTREND SIGNAL.

FLAT ZONE is highlighted also to have the maximum concentration on sideways market conditions.

There are three quantitative parameters in this indicator:

The first parameter in the OTT indicator set by the two parameters is the period/length.

OTT lines will be much sensitive to trend movements if it is smaller.

And vice versa, will be less sensitive when it is longer.

As the period increases it will become less sensitive to little trends and price actions.

In this way, your choice of period, will be closely related to which of the sort of trends you are interested in.

The OTT percent parameter in OTT is an optimization coefficient. Just like in the period

small values are better at capturing short term fluctuations, while large values

will be more suitable for long-term trends.

The final adjustable quantitative parameter is HIGHEST and LOWEST length which is the source of calculations.

Credits go to:

SSL Hybrid www.tradingview.com

HIGH and LOW OTT : www.tradingview.com

Range Filter www.tradingview.com

Volume Profile - Custom Range, Interactive by DGTVolume Profile - Custom Range aims to display trading activity at specific price levels over user defined Custom Range of trading. Start and End Time is Interactive , they can be adjusted simply by clicking on the chart and drag the lines to specify the desired custom range. Same as is with the drawing tools available in TV

Please note, while switching between timeframes or switching to different instruments with different exchange timezones you may need to adjust the locations in case the plotting is not displied

Volume Profile - Custom Range is plotted as two horizontal histograms on the finacial isntrumnet's chart that highlights the trader's common interest at specific price levels as well as aims to reveal dominant party of who is in control, bulls or bears

You are also invated to galnce at Volume-Profile-and-Volume-Indicator , Anchored-Volume-Profile , and Price Action-Support-Resistance for different perspective of Volume Profiles

Special thanks to everyone who commented and presented their valuable suggestions

Disclaimer: Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

Central Pivot Range 2xBased on a modified Hancock Pivot Range.

Displays the Central Pivot Range for 2 customisable Timeframes Along with Targets which are based on Classic Pivot Point Extensions.

The Pivot Point Extensions are Extended to the right of the price chart which helps eliminate unnecessary clutter

TF1 Displays Right Extensions R3 to S3 + the pivot point

TF2 Displays only Right Extensions R2 to S2

I would have liked to have provided more Right Extensions plus Labels however that would have exceeded Tradingviews memory limits, having said that R3 to S3 for both timeframes can still be displayed as historical levels

Central Pivot Range High Low and Mid Levels + the Targets work great as Support and Resistance and help with analysing the trend

A Thick Central Pivot Range generally indicates consolidation whereas a Thin Central Pivot Range generally indicates a trending market

Average Daily Range TableThis is the last script to complete Vladimir Poltoratskiy's setup found in his books.

Poltoratskiy argues that you should not take any fractal corridors higher than 50% of the Average Daily Range. To be honest, even 40% is a lot, because then, your target will be 160% ADR away from your entry and one "fracture" just can't be enough to predict moves this big.

I chose a table to visually represent the indicator because it doesn't change its value during the day. It takes far less room on the chart.

There are also two simple moving averages. You may use the as an indicator if the relative volatility as of late is extremely low and in that case, perhaps, expect an increase in the coming days. They are applied to the Average Daily Range, not one day range!

LKK - Extended Range Candles GapOANDA:EURUSD

The indicator will highlight the Extended Range Candles (ERC) price gap.

Extended Range is the price excessively moving in one direction, it can be one or more candles.

ERC Gap is the range of price that doesn’t have any resistant.

To classified as ERC I use the range (highest price minus lowest price) of the candle before the ERC and divide with ERC range. If result less than given percentage (ERC %) then confirm it is ERC.

Average Weekly Ranger PlusThis is an updated version of the average weekly ranger which now includes ATR and TR values for the period, as well as the /3 divisor used by scalerz. Just swinging from the trees here. Enjoy. Tarzan.

Digital Nivesh Out of Range Trade IndicatorThis indicator is for intraday with the basic logic that any script will always trade in its range.

So , if any script moves away from its range, it will try to come back to its normal range movement.

Suppose average movement of any share is 100 points, and share has moved more than 150 points there is high probability that it will move in opposite direction in order to have average movement of price of 100.

For Stocks please use average period as 15 days for index 30 days.

If share price(YELLOW LINE) moves away from higher or lower blue line, then with the help of volume confirmation a trade can be initiated in opposite direction.

Please note direction needs to be opposite of what has happened in the day.

for eg. upper blue line could be broken , in both situation i.e.. share price is rising or falling,

so if share price is rising and upper blue line is broken:

Bearsish trade can be initiated with the help of price action n volume.

if share price has falledn and upper blue is broken:

Bullish trade can be initiated with the help of volume n price action confirmation.

Volume using Candle RangeAnother way of finding out a rough estimate of the volume or how much bulls or bears were in control using only the range of the candlesticks in relation to the closing price. If the close is in the higher range zone then the volume is said to have been positive, if the close is in the lower range zone then the volume is said to have been negative. The close is compared to the midpoint of the candle to see how far from the midpoint the close was.

The columns bars show how far each candlestick's close price is to the midpoint of its high and low. It's possible for the column bar to be a different color than the candlestick itself if the close was above or below the midpoint. An average line is shown that takes the average of a given length amount of column bars. There is an option to show the absolute value only of the columns and the average line.

This is based on an idea I found about candlestick range bars implying volume. This is an attempt to put that theory into practice and to see if there's any truth to it. It's not exactly volume and may not always look like it, and it does not show how many trades took place but instead tries to use price in relation to the high and low range.

Decomposed Average True RangeThis simple script decomposes the value of the Average True Range into a bullish component and a bearish component .

The script supports two plotting methods; Mirrored and Two Lines . If Mirrored is chosen, the indicator plots the bullish component as a positive number, and the bearish component as a negative number. If Two Lines is chosen, the indicator plots two lines, both of positive values. It is the same data, just visualized differently.

Side note: This is very similar to how the strength (average gain) part in the Relative Strength Index calculation works. However, the RSI uses the realized range (close - previous close) rather than true range. If we were to use the bullish component of the ATR as the average bullish gain part in the RSI calculation, and the bearish component of the ATR as the average bearish gain part in the RSI calculation, we would get very similar (but not equal) results to the standard RSI. This shows how the ATR and the RSI are related to each other.

Average Ranges - MMFxThis is a script that has Average Daily Ranges, as well as Weekly, Monthly, and Yearly Ranges

Users can edit:

ADR display limit - Set the number of historical ADR to display.

AWR display limit - Set the number of historical AWR to display.

AMR display limit - Set the number of historical AMR to display.

AYR display limit - Set the number of historical AYR to display.

ADR Length parameter - Set the length parameter of ADR.

WDR Length parameter - Set the length parameter of AWR.

MDR Length parameter - Set the length parameter of AMR.

YDR Length parameter - Set the length parameter of AYR.

Ranges are to be used with price action, and Market Maker Method knowledge to catch reversals and stop hunt points

Kendall Garro 2021

MasterMind FX