Comprehensive Market AnalyzerVERSION 2.0:

Notice to users: To better reflect its extensive features, this indicator has been renamed from "Tsūrubokkusu (Toolbox) 🧰" to "Comprehensive Market Analyzer". Thank you for your understanding and adaptation to this change.

Purpose and Usage:

The Comprehensive Market Analyzer is designed to provide traders with a holistic view of market conditions by integrating various technical indicators into a single,

cohesive tool. Each indicator has been carefully selected and improved to work together, offering enhanced customization and advanced market insights.

This combination allows for more comprehensive market analysis, improved decision-making, and efficient trading strategies.

📘 Machine Learning Integration

Purpose : Utilizes machine learning algorithms to analyze past market data and provides predictive insights based on historical data.

Usage : Activate machine learning features, set lookback windows, influence weighting, and start bar for improved trend predictions.

Activate Machine Learning :

Description : Enables advanced machine learning features that analyze past market data.

Details : This feature allows the algorithm to use historical data to forecast market movements, providing traders with enhanced predictive insights on historical data.

Kernel Lookback Window :

Description : Sets the number of previous bars that the algorithm will analyze.

Details : A higher number provides a broader view of market trends, while a lower number makes the model more sensitive to recent changes.

Kernel Influence Weighting :

Description : Adjusts the emphasis on recent versus older data.

Details : Increasing this value gives more importance to recent data, potentially making predictions more responsive to new trends.

Kernel Calculation Start Bar :

Description : Specifies the bar number from which to start the machine learning calculations.

Details : Avoids early data which may contain excessive noise and less reliable market signals.

Kernel Functions :

Gaussian Kernel :

Description : Uses a Gaussian distribution to weight historical data, focusing on more recent data points for trend analysis.

Details : Calculates weights based on the Gaussian distribution, emphasizing data points closer to the present.

Laplacian Kernel :

Description : Applies Laplacian distribution, emphasizing data points closer to the current time more heavily.

Details : Uses the Laplacian function to provide a different perspective on data weighting.

RBF Kernel :

Description : Utilizes a Radial Basis Function for smoothing and analyzing data, providing a different approach to trend prediction.

Details : Applies the RBF function to smooth data and enhance the accuracy of trend predictions.

Wavelet Kernel :

Description : Applies wavelet transform for analyzing frequency components, helping to detect patterns in the price movements.

Details : Uses wavelet-based calculations to focus on specific frequency components within the data, aiding in pattern recognition.

📘 Enhanced Ichimoku Kinkō Hyō Integration

Purpose : Provides a comprehensive overview of market trends and momentum using the Ichimoku Kinkō Hyō indicator.

Usage : Display various components of the Ichimoku Kinkō Hyō, customize their appearance, provides additional calculations for trend analysis.

Display Ichimoku Kinkō Hyō :

Description : Toggle to show or hide the Ichimoku Kinkō hyō indicator.

Details : This indicator helps traders see support and resistance levels, trend direction, and potential future movements.

Activate Heikin-Ashi Source :

Description : Switches between regular price data and Heikin-Ashi candles for analysis.

Details : Heikin-Ashi candles smooth price data, making trends easier to spot.

Display Tenkan-Sen Line :

Description : Shows the Tenkan-Sen line, a key short-term trend indicator.

Color Customization : Set the color of the Tenkan-Sen line for better visibility.

Minimum Length : Determine the shortest period for calculating the Tenkan-Sen line.

Maximum Length : Determine the longest period for calculating the Tenkan-Sen line.

Dynamic Length Adjustment : Automatically adjusts the length of the Tenkan-Sen based on market conditions.

Display Kijun-Sen Line :

Description : Shows the Kijun-Sen line, a key medium-term trend indicator.

Color Customization : Set the color of the Kijun-Sen line for better visibility.

Minimum Length : Determine the shortest period for calculating the Kijun-Sen line.

Maximum Length : Determine the longest period for calculating the Kijun-Sen line.

Dynamic Length Adjustment : Automatically adjusts the length of the Kijun-Sen based on market conditions.

Kijun-Sen Divider Tool : Adjust the sensitivity of the Kijun-Sen calculation.

Display Chikou Span :

Description : Shows the Chikou Span, which lags behind the current price to help confirm trends.

Bear Phase Color : Set the color for bearish periods.

Bull Phase Color : Set the color for bullish periods.

Consolidation Color : Set the color for consolidation periods.

Minimum Length : Determine the shortest lag period for the Chikou Span.

Maximum Length : Determine the longest lag period for the Chikou Span.

Dynamic Length Adjustment : Automatically adjusts the length of the Chikou Span based on market conditions.

Display Senkou Span A and B :

Description : Shows the Senkou Span A and B, which form the Ichimoku Cloud indicating future support and resistance levels.

Bear Color : Set the color for bearish clouds.

Bull Color : Set the color for bullish clouds.

Neutral Color : Set the color for neutral periods.

Minimum Length : Determine the shortest period for calculating the Senkou Span.

Maximum Length : Determine the longest period for calculating the Senkou Span.

Dynamic Length Adjustment : Automatically adjusts the length of the Senkou Span based on market conditions.

Projection Offset : Set how far ahead the Senkou Span is projected.

Kumo Cloud Settings :

Enable Kumo Cloud Fill : Toggle to fill the space between Senkou Span A and B with color.

Cloud Fill Transparency : Adjust the transparency of the cloud fill.

Apply WMA Smoothing :

Description : Smooths the indicator lines using a Weighted Moving Average to clarify trends.

Bar Coloring Based on Ichimoku Signals :

Description : Colors the bars based on Ichimoku signals to provide a quick visual indication of market sentiment.

Bearish Signal Bar Color : Set the color for bars during bearish signals.

Bullish Signal Bar Color : Set the color for bars during bullish signals.

Consolidation Signal Bar Color : Set the color for bars during consolidation periods.

Neutral Bar Color : Set the color for bars during neutral conditions.

Enhanced Calculations :

Heikin Ashi Values : Smooths price movements to make trends more visible.

Alternative Source Calculation : Uses a different method for calculating the indicator based on user settings.

Volume Calculations : Enhanced functions for calculating volume based on different candlestick patterns.

Dynamic Length Adjustment : Automatically adjusts the length of Ichimoku components based on market volatility.

Gaussian Kernel Calculations : Uses advanced calculations for smoother and more accurate trend analysis.

Chikou Span Adaptation : Improved calculation for the Chikou Span using dynamic lengths and advanced methods.

Visual Enhancements : Adds color gradients to the Senkou Span and dynamic coloring for the Chikou Span to improve trend visibility.

Plotting Ichimoku Components :

Tenkan-Sen : Plots the Tenkan-Sen line with dynamic adjustments.

Kijun-Sen : Plots the Kijun-Sen line with dynamic adjustments.

Senkou Span A and B : Plots these lines with dynamic projections and advanced smoothing.

Chikou Span : Plots the Chikou Span with dynamic offsets and coloring.

📘 Enhanced Candlestick Patterns Integration

Purpose : Identifies and displays various candlestick patterns to help traders spot key market movements and potential reversals.

Usage : Toggle the display of patterns, select specific pattern types, and customize pattern labels for improved visual analysis.

Display Patterns :

Description : Toggle to enable or disable the display of all candlestick patterns.

Details : When enabled, all selected candlestick patterns will be displayed on the chart, aiding traders in identifying key market movements and potential reversals.

Select Pattern Type :

Description : Select the type of candlestick patterns to detect.

Details : Options include Bullish (indicating potential upward trends), Bearish (indicating potential downward trends), or Both.

Trend Filter Method :

Description : Select the method to filter trends.

Details : Options include True Range (based on price range), Fractals, Volume, Combined, or None (no filtering).

Pattern Label Colors :

Bullish Pattern Color : Choose the color for labeling Bullish patterns, indicating potential upward trends.

Bearish Pattern Color : Choose the color for labeling Bearish patterns, indicating potential downward trends.

Indecision Pattern Color : Choose the color for labeling Indecision patterns, indicating no clear trend direction.

Base Line and Patterns Display Options :

Show Base Line in Place of Labels : Toggle to display a base line instead of labels for detected patterns. This helps visualize the general trend.

Show Counterattack Lines : Toggle to display Counterattack Lines patterns, indicating potential reversal points.

Show Dark Cloud Cover : Toggle to display Dark Cloud Cover patterns, a bearish pattern suggesting a potential reversal from an uptrend to a downtrend.

Show Engulfing Patterns : Toggle to display Engulfing patterns. Bullish Engulfing patterns suggest a potential upward reversal, while Bearish Engulfing patterns suggest a potential downward reversal.

Show Hammer Patterns : Toggle to display Hammer patterns, a bullish pattern indicating a potential reversal from a downtrend to an uptrend.

Show Hanging Man Patterns : Toggle to display Hanging Man patterns, a bearish pattern indicating a potential reversal from an uptrend to a downtrend.

Show Harami Patterns : Toggle to display Harami patterns. Bullish Harami patterns suggest a potential upward reversal, while Bearish Harami patterns suggest a potential downward reversal.

Show In-Neck Patterns : Toggle to display In-Neck patterns, indicating a potential continuation of the current trend.

Show On-Neck Patterns : Toggle to display On-Neck patterns, indicating a potential continuation of the current trend.

Show Piercing Patterns : Toggle to display Piercing patterns, a bullish pattern suggesting a potential reversal from a downtrend to an uptrend.

Show Three Black Crows : Toggle to display Three Black Crows patterns, a bearish pattern suggesting a potential reversal from an uptrend to a downtrend.

Show Thrusting Patterns : Toggle to display Thrusting patterns, a bearish pattern suggesting a potential continuation of the downtrend.

Show Upside Gap Two Crows : Toggle to display Upside Gap Two Crows patterns, a bearish pattern suggesting a potential downward reversal after an upward gap.

Show Evening Star : Toggle to display Evening Star patterns, a bearish pattern suggesting a potential reversal from an uptrend to a downtrend.

Show Inverted Hammer : Toggle to display Inverted Hammer patterns, a bullish pattern suggesting a potential reversal from a downtrend to an uptrend.

Show Morning Star : Toggle to display Morning Star patterns, a bullish pattern suggesting a potential reversal from a downtrend to an uptrend.

Show Shooting Star : Toggle to display Shooting Star patterns, a bearish pattern suggesting a potential reversal from an uptrend to a downtrend.

Show Doji Patterns : Toggle to display Doji patterns, indicating market indecision and potential reversals.

Show Dragonfly Doji : Toggle to display Dragonfly Doji patterns, a bullish pattern suggesting a potential reversal from a downtrend to an uptrend.

Show Evening Doji Star : Toggle to display Evening Doji Star patterns, a bearish pattern suggesting a potential reversal from an uptrend to a downtrend.

Show Gravestone Doji : Toggle to display Gravestone Doji patterns, a bearish pattern suggesting a potential reversal from an uptrend to a downtrend.

Show Long-Legged Doji : Toggle to display Long-Legged Doji patterns, indicating high market indecision and potential reversals.

Show Morning Doji Star : Toggle to display Morning Doji Star patterns, a bullish pattern suggesting a potential reversal from a downtrend to an uptrend.

Show Rising Three Methods : Toggle to display Rising Three Methods patterns, a bullish pattern suggesting a continuation of the uptrend.

Show Falling Three Methods : Toggle to display Falling Three Methods patterns, a bearish pattern suggesting a continuation of the downtrend.

Show Tasuki Patterns : Toggle to display Tasuki patterns, indicating potential trend continuation after a gap.

Show Marubozo : Toggle to display Marubozo patterns, indicating strong trend continuation, either bullish or bearish.

Show Long Lower Shadow : Toggle to display Long Lower Shadow patterns, indicating strong buying pressure and potential upward movement.

Show Long Upper Shadow : Toggle to display Long Upper Shadow patterns, indicating strong selling pressure and potential downward movement.

Show Three Inside Up/Down : Toggle to display Three Inside Up/Down patterns, indicating potential bullish or bearish reversals.

Show Kicker Pattern : Toggle to display Kicker patterns, indicating significant potential reversals.

Show Tweezer Tops/Bottoms : Toggle to display Tweezer Tops/Bottoms patterns, indicating potential reversals at the tops or bottoms.

Show Mat Hold Pattern : Toggle to display Mat Hold patterns, a bullish pattern suggesting a continuation of the uptrend.

Candle Body/Shadow Comparison Options :

Candle Body/Shadow Comparison : Choose the criteria to compare candle sizes: Shadows (larger shadows), Body (larger body), Both (larger shadows and body), Either (larger shadows or body), or None (no comparison).

Look-back Period for Candle Comparison : Specify the number of periods to look back when comparing the current candle size to determine if it is significant.

Period for Body Length Average : Specify the period for calculating the average body length of candles to help identify significant patterns.

Period for Candle Length Average : Specify the period for calculating the average length of candles to help identify significant patterns.

Specific Pattern Thresholds :

Doji Body Percentage Threshold : Set the percentage threshold for identifying Doji patterns based on the candle body size compared to its range.

Upper Shadow Percentage Limit : Set the maximum allowed upper shadow percentage of the candle’s range for identifying specific Doji patterns.

Lower Shadow Percentage Limit : Set the maximum allowed lower shadow percentage of the candle’s range for identifying specific Doji patterns.

Price Deviation Tolerance : Specify the price deviation tolerance for pattern recognition, which helps in identifying patterns within a certain price range.

Thrusting Neck Percentage : Set the percentage threshold for identifying Thrusting Neck patterns, indicating a potential continuation of the current trend.

Base Line Settings :

Base Line EMA Length : Specify the length of the EMA for the Base Line, helping to visualize the general trend.

Enhanced Calculations :

Wavelet Transform : If machine learning is enabled, calculates the wavelet transform for smoother and more accurate pattern detection.

Candle Body and Shadows Calculation : Detailed calculations for candle body and shadow lengths to improve pattern detection.

Average Calculations : Calculate averages for body and candle sizes to help identify significant patterns.

Fractals Calculation : Identify fractal highs and lows to aid in trend detection.

Trend Filters : Apply user-selected trend filters based on True Range, Fractals, Volume, or a combination.

Pattern Detection and Labeling : Detects and labels various candlestick patterns, including Doji, Engulfing, Hammer, and more, with options for displaying labels or base lines.

Alerts and Notifications : Set alerts for detected patterns and base line colors to notify traders of significant market events.

Plotting Candlestick Patterns :

Pattern Detection : Automatically detects and labels various candlestick patterns based on user settings.

Label Customization : Customize the labels for different patterns, including color and text.

Base Line Plotting : Option to plot a base line instead of labels for detected patterns, enhancing trend visualization.

Alerts for Patterns : Set alerts for detected patterns to keep traders informed of significant market changes.

📘 Enhanced Fibonacci Retracement Integration

Purpose : Provides a tool for identifying potential support and resistance levels using Fibonacci retracement.

Usage : Toggle the display of Fibonacci levels, adjust the lookback period, and customize the appearance of Fibonacci levels for better market analysis.

Auto Mode :

Description : Toggle to enable or disable automatic detection of price points.

Details : When enabled, the highest and lowest price points within a specified period will be automatically detected to set Fibonacci levels. Disable to manually set the top and bottom prices.

Period :

Description : Set the lookback period for detecting price points.

Details : Defines the number of bars to look back when detecting the highest and lowest prices in Auto Mode, used for calculating Fibonacci levels.

Manual Top :

Description : Manually set the top price level.

Details : Adjust this setting to reflect the peak price of interest when Auto Mode is disabled.

Manual Bottom :

Description : Manually set the bottom price level.

Details : Adjust this setting to reflect the low price of interest when Auto Mode is disabled.

Display Fibonacci :

Description : Toggle to show or hide Fibonacci retracement levels.

Details : When enabled, the calculated Fibonacci levels will be displayed on the chart, overlaying the price data.

Baseline Levels :

Description : Select Fibonacci levels to highlight as baselines.

Details : Choose specific levels to be visually distinct, emphasizing their significance in the analysis.

Fibonacci Levels Colors :

Upper Levels Color : Set the color for Fibonacci levels above the baseline, indicating potential resistance levels.

Lower Levels Color : Set the color for Fibonacci levels below the baseline, indicating potential support levels.

Baseline Levels Color : Set the color for highlighted baseline Fibonacci levels, making them stand out from other levels.

Display Individual Fibonacci Levels :

Show Level : Toggle to enable or disable the display of specific Fibonacci levels.

Level Value : Set the multiplier used to calculate each specific Fibonacci level relative to the price range.

Reverse Levels :

Description : Toggle to switch the calculation direction of Fibonacci levels.

Details : When enabled, levels are calculated in reverse, useful for analyzing downtrends.

Line Extension :

Description : Choose how Fibonacci level lines are extended on the chart.

Details : Options include extending lines to the left, right, or both, affecting their visual presentation.

Text Size :

Description : Adjust the font size of the labels for Fibonacci levels.

Details : Options range from large to tiny, allowing for readability adjustments according to user preference.

Line Style :

Description : Select the line style for Fibonacci levels.

Details : Options include solid, dotted, and dashed, providing visual distinction.

Line Width :

Description : Set the thickness of the Fibonacci level lines.

Details : A higher value makes the lines more prominent on the chart.

Baseline Line Style :

Description : Choose the line style specifically for the baseline levels.

Details : This can differ from other Fibonacci levels to emphasize their importance.

Baseline Line Width :

Description : Adjust the thickness of the baseline level lines.

Details : Can be set differently from other levels for visual emphasis.

Enhanced Calculations :

Automatic and Manual Top/Bottom Setup : Detect or manually set the highest and lowest price points.

Price Range Calculation : Determine the range between the highest and lowest prices.

Fibonacci Level Values : Calculate the values for each Fibonacci level.

Visual and Label Configuration : Configure visual aspects and labels for each level.

Plotting and Labeling :

Level Plotting :

Description : Plot each Fibonacci level on the chart.

Details : Draw lines representing each calculated level.

Label Customization :

Description : Customize the labels for Fibonacci levels.

Details : Include text, colors, and positioning for clarity.

📘 Supports and Resistances Integration

Purpose : Identifies key support and resistance levels to aid in market analysis.

Usage : Toggle the display of support and resistance lines, customize their appearance, and use Bollinger Bands for additional insights.

Display Supports and Resistances :

Description : Toggle to enable or disable the display of support and resistance lines.

Details : When enabled, support and resistance lines will be shown on the chart, providing key levels for market analysis.

Swing Period :

Description : Set the retrospective period for identifying swing points.

Details : A longer period captures more significant trends but may reduce sensitivity. The default value is 10.

Support Line Color :

Description : Set the color for support lines.

Details : Choose a color that enhances chart readability. Default is green.

Resistance Line Color :

Description : Set the color for resistance lines.

Details : Choose a color that makes resistance lines easily distinguishable. Default is red.

Trend-Based Line Color :

Description : Toggle to enable dynamic coloring based on trend direction.

Details : When enabled, the color of the lines will change according to the trend, aiding visual analysis.

Line Thickness :

Description : Adjust the thickness of the support and resistance lines.

Details : Choose a thickness value between 1 and 5 for better visibility.

Line Style :

Description : Select the style of the lines.

Details : Options include Solid, Dotted, or Dashed lines for visual distinction.

Number of Lines to Display :

Description : Set the maximum number of support/resistance lines to display.

Details : Adjust the number of lines to avoid clutter or to show more levels.

Display Bollinger Bands :

Description : Toggle to show or hide Bollinger Bands on the chart.

Details : Bollinger Bands provide a visual representation of volatility and potential price ranges.

Bollinger Bands Integration :

Description : Enable the integration of Bollinger Bands for S/R calculation.

Details : This feature adjusts the placement of S/R lines based on the market volatility captured by the Bollinger Bands.

Bollinger Bands Color Settings :

Description : Set colors for different Bollinger Band conditions.

Details :

Green: Prices above the median but below the upper band (potential overbought area).

Dark green: Prices above the upper band (strong upward momentum).

Light red: Prices below the median but above the lower band (potential oversold area).

Dark red: Prices below the lower band (strong downward momentum).

Fill Opacity Adjustment :

Description : Adjust the fill opacity between Bollinger Bands.

Details : Set the opacity level to balance visibility with other chart elements.

BB Sensitivity Level :

Description : Adjust the sensitivity for determining S/R levels near Bollinger Bands.

Details : A higher value increases the consideration of levels near the bands.

Band Width Multiplier :

Description : Control the width of the Bollinger Bands.

Details : Adjust the multiplier to expand or contract the bands based on market volatility.

Uniform BB Coloring :

Description : Apply a consistent color to Bollinger Bands.

Details : Simplify visual interpretation with a uniform color.

Plotting and Alerts :

Plotting Bollinger Bands :

Description : Plot the Bollinger Bands on the chart.

Details : The bands are colored based on the conditions set for market volatility and price ranges.

Alerts and Notifications :

Description : Set alerts for support/resistance breaks and Bollinger Band breakouts.

Details : Notify traders of significant market events related to these levels.

📘 Enhanced Trend Lines Integration

Purpose : Identifies and plots trend lines based on market structure to help traders understand market direction and potential buy/sell points.

Usage : Toggle the display of trend lines, customize their appearance, and use enhanced calculations for trend analysis.

Display Trend Lines :

Description : Enable or disable the display of trend lines on the chart.

Details : These trend lines are calculated based on market structure, specifically through the detection of Breaks of Structure (BOS). If enabled, the trend lines will help in identifying the market overall trend and potential buy and sell points.

Trend Line Colors :

Upper Line Color : Set the color for the upper trend lines to enhance visual distinction.

Lower Line Color : Set the color for the lower trend lines, aiding in easy identification of support levels.

Pivot Labels :

Show Pivots Labels : Control the display of pivot labels on the chart.

Pivot Label Size : Select the size of the pivot labels displayed on the chart. Options include Tiny, Small, Normal, Large, and Huge.

Trend Line Calculations :

Pivot Depth : Adjust the depth for pivot calculation based on the selected timeframe to capture significant price movements.

Pivot Deviation : Set the deviation for pivot calculation to identify key turning points.

Pivot Backstep : Define the backstep for pivot calculation to ensure accurate detection of pivot points.

Enhanced Calculations :

Market Structure Detection : Utilize advanced algorithms to identify key market structures, improving trend line accuracy.

Adaptive Parameters : Automatically adjust pivot depth, deviation, and backstep based on the selected timeframe for better relevance.

Zigzag Calculation : Implement zigzag patterns to dynamically adjust trend lines, ensuring they reflect current market conditions.

Slope and Intercept Calculation : Compute the slope and intercept for trend lines to enhance precision in trend detection.

Dynamic Updates : Continuously update trend lines as new data becomes available, ensuring real-time accuracy.

Alerts and Notifications : Set alerts for new high and low pivots, as well as for when the price crosses upper or lower trend lines, keeping traders informed of significant market changes.

Plotting Trend Lines :

Trend Line Plotting : Automatically draw trend lines based on detected BOS, helping traders visualize the market trend.

Diagonal Support/Resistance Lines : Plot diagonal lines to indicate support and resistance levels, enhancing the understanding of market dynamics.

Pivot Label Customization : Customize pivot labels for clear identification of high and low points in the trend.

Alerts for Trend Lines : Set alerts for when price crosses trend lines, ensuring timely notifications of potential trading opportunities.

📘 Enhanced Linear Regression Integration

Purpose : Uses linear regression to analyze price movements and identify trends.

Usage : Display the linear regression projection line, customize its appearance, and use enhanced calculations for better trend analysis.

Display Projection Line :

Description : Toggle to display or hide the linear regression projection line on the chart.

Details : This line represents the best fit line that predicts future prices based on historical data.

Data Source :

Description : Select the data source for the linear regression projection.

Details : This is typically the closing price but can be any price point such as open, high, or low. The selected source will be used to calculate the linear regression projection line.

Trend-Based Line Color :

Enable Trend-Based Line Color : Toggle to automatically color the projection line based on the trend direction. When enabled, the line will be red for a downward trend and green for an upward trend, providing a visual indication of market direction.

Uptrend Line Color : Select the color for the projection line when the trend is upward. This color will be used when "Enable Trend-Based Line Color" is active.

Downtrend Line Color : Select the color for the projection line when the trend is downward. This color will be used when "Enable Trend-Based Line Color" is active.

Enhanced Calculations :

Standard Deviation Calculation : Calculate the standard deviation for a given length to understand the volatility around the linear regression line.

Pearson's Correlation Calculation : Compute Pearson's R to measure the strength of the linear relationship between the price points and the linear regression line.

Slope and Intercept Calculation : Calculate the slope and intercept for the regression line, providing the basis for the projection.

Kernel Application : Optionally apply the RBF Kernel to the selected source data for smoothing and enhancing the regression calculations.

Dynamic Length Selection : Automatically select the optimal regression period based on the highest Pearson's R value, ensuring the most accurate trend representation.

Real-Time Updates : Continuously update the regression line and related calculations as new data becomes available, maintaining accuracy in real-time.

Alerts and Notifications : Set alerts for when the price crosses the linear regression projection line, notifying traders of significant market events.

Plotting Linear Regression Components :

Projection Line Plotting : Automatically draw the linear regression projection line based on historical data and the selected data source.

Label Customization : Customize the label for the projection line, including color and text, for clear identification on the chart.

Alerts for Projection Line : Set alerts for when the price crosses the projection line, ensuring timely notifications of potential trading opportunities.

📘 POC Analysis Integration

Purpose : Identifies the Point of Control (POC) to highlight price levels with the highest trading volume.

Usage : Toggle the display of the POC, customize its appearance, and use enhanced calculations for better market analysis.

Display POC :

Description : Toggle to display or hide the Point of Control (POC) on the chart.

Details : The POC is the price level at which the highest volume of trading occurred, indicating a focal point of market activity.

Data Source :

Description : Select the price source for POC analysis.

Details : This is typically the closing price but can be any price point such as open, high, or low. The selected source will be used to calculate the POC.

POC Line Colors :

Color Above POC : Set the line color when the closing price is above the POC.

Color Below POC : Set the line color when the closing price is below the POC.

Width Multiplier :

Description : Adjust the width around the price for POC analysis.

Details : A higher value broadens the calculation range.

POC Calculation and Visualization :

Price Level Initialization : Calculate the initial spacing between price levels based on the first candlestick and user settings.

Volume Data Accumulation : Accumulate volume data at specified price levels for each candlestick to determine the POC.

Dynamic Array Expansion : Expand price levels array to accommodate new price data outside the current range.

POC Determination : Determine and visualize the POC at the last candlestick if enabled by the user.

Alerts and Notifications : Set alerts for when the price crosses the POC, notifying traders of significant market events.

Plotting POC Components :

POC Line Plotting : Automatically draw the POC line based on historical data and the selected data source.

Label Customization : Customize the label for the POC line, including color and text, for clear identification on the chart.

Alerts for POC : Set alerts for when the price crosses the POC, ensuring timely notifications of potential trading opportunities.

📘 Enhanced Divergences Integration

Purpose : Detects and displays divergences between price movements and indicators to identify potential reversal points.

Usage : Toggle the display of divergences, select data sources, customize divergence colors, and use enhanced calculations for better trend analysis.

Display Divergences :

Description : Toggle to display or hide the detected divergences on the chart.

Details : Divergences occur when the price movement of an asset and a related indicator (e.g., volume or momentum) move in opposite directions. They are used to identify potential reversal points in the market. Regular divergences signal possible reversals, while hidden divergences can indicate continuation.

Data Source :

Description : Defines the timeframe from which to fetch data for analysis.

Details : Typically lower than the chart current timeframe for multi-timeframe analysis.

Divergence Colors :

Bearish Divergence Color : Sets the color for bearish divergence lines. Bearish divergences typically suggest potential downward price movement.

Bullish Divergence Color : Sets the color for bullish divergence lines. Bullish divergences typically indicate potential upward price movement.

Pivot Bars :

Left Bars : Number of bars to the left of the pivot point to consider. Helps in identifying the pivot high or low by looking back these many bars.

Right Bars : Number of bars to the right of the pivot point to consider. Assists in confirming a pivot point by ensuring no higher high or lower low is present within this range.

Display Hidden Divergences :

Description : When enabled, this setting reveals hidden divergences on the chart.

Details : Hidden divergences are a subtler form of divergence that often signal continuation rather than reversal. A hidden bullish divergence occurs when price makes a higher low while the indicator makes a lower low, suggesting the continuation of an uptrend. Conversely, a hidden bearish divergence occurs when price makes a lower high while the indicator makes a higher high, indicating the continuation of a downtrend. These divergences are particularly useful for identifying the strength of the current trend.

Dynamic Line Width Based on Divergence Count :

Description : When enabled, adjusts the width of the divergence line dynamically based on the count of divergences detected.

Details : This provides visual emphasis on stronger signals.

Enhanced Calculations :

Standard Deviation Calculation : Calculate the standard deviation for a given length to understand the volatility around the linear regression line.

Pearson's Correlation Calculation : Compute Pearson's R to measure the strength of the linear relationship between the price points and the linear regression line.

Slope and Intercept Calculation : Calculate the slope and intercept for the regression line, providing the basis for the projection.

Kernel Application : Optionally apply the RBF Kernel to the selected source data for smoothing and enhancing the regression calculations.

Dynamic Length Selection : Automatically select the optimal regression period based on the highest Pearson's R value, ensuring the most accurate trend representation.

Real-Time Updates : Continuously update the regression line and related calculations as new data becomes available, maintaining accuracy in real-time.

Alerts and Notifications : Set alerts for when the price crosses the linear regression projection line, notifying traders of significant market events.

Plotting Divergence Components :

Divergence Line Plotting : Automatically draw divergence lines based on historical data and the selected data source.

Label Customization : Customize the label for the divergence lines, including color and text, for clear identification on the chart.

Alerts for Divergences : Set alerts for when a divergence is detected, ensuring timely notifications of potential trading opportunities.

📘 Enhanced Average True Range Integration

Purpose : Measures market volatility using the Average True Range (ATR) to assist in identifying potential buy and sell points.

Usage : Set the ATR period, minimum tick filter, upper and lower coefficients, and customize ATR colors for better market analysis.

Show Labels :

Description : Enable or disable the display of labels for the Average True Range (ATR) indicator.

Details : This option controls whether the ATR signals (buy and sell) are shown on the chart with respective labels.

ATR Period :

Description : Sets the period for calculating the Average True Range (ATR).

Details : The ATR measures market volatility by calculating the average range of price movement over a specified period. A shorter period makes the ATR more sensitive to recent price movements, while a longer period smooths out short-term volatility.

Minimum Tick Filter :

Description : Sets the minimum tick filter for buy and sell signals.

Details : This filter ensures that the price movement is significant enough to be considered a valid signal. For example, a value of 20 means that the price must move at least 20 ticks from the open to the close to generate a signal.

Upper Coefficient :

Description : Sets the upper coefficient for band calculation.

Details : This value adjusts the sensitivity of the upper band used to detect high points. A higher coefficient makes the band wider, capturing more significant price movements, while a lower coefficient makes the band narrower, making it more sensitive to smaller price changes.

Lower Coefficient :

Description : Sets the lower coefficient for band calculation.

Details : This value adjusts the sensitivity of the lower band used to detect low points. A higher coefficient makes the band wider, capturing more significant price movements, while a lower coefficient makes the band narrower, making it more sensitive to smaller price changes.

ATR Colors :

Bullish Color : Sets the color for the bullish signal, helping to visually distinguish bullish trends.

Bearish Color : Sets the color for the bearish signal, helping to visually distinguish bearish trends.

Enhanced Calculations :

Dynamic Coefficient Calculation : Calculates dynamic coefficients based on market volatility, adjusting the sensitivity of ATR bands accordingly.

Band Calculation : Computes high and low bands using dynamic coefficients to detect significant price movements.

High/Low Point Detection : Identifies potential high and low points based on ATR band calculations and price thresholds.

Real-Time Updates : Continuously updates ATR calculations and signals as new data becomes available, ensuring accuracy in real-time.

Plotting ATR Components :

Signal Plotting : Plots bullish and bearish ATR signals on the chart based on calculated conditions.

Label Customization : Customize the labels for ATR signals, including color and text, for clear identification on the chart.

Alerts for Signals : Set alerts for detected bullish and bearish signals, ensuring timely notifications of potential trading opportunities.

📘 Enhanced ATR Visualization Parameters

Purpose : Provides a visual representation of market volatility using the ATR Strength Meter.

Usage : Toggle the display of the ATR Strength Meter, set thresholds, and customize its appearance for better market analysis.

Display ATR Strength Meter :

Description : Toggle to display or hide the ATR Strength Meter, a visual representation of market volatility.

Details : The meter is based on the Average True Range (ATR) and helps identify volatility trends.

High ATR Threshold :

Description : Set the threshold for high volatility.

Details : ATR values above this threshold indicate increased market volatility.

Low ATR Threshold :

Description : Set the threshold for low volatility.

Details : ATR values below this threshold indicate decreased market volatility.

Progression Bar Position :

Description : Select the position of the ATR Strength Meter on the chart.

Details : Options are "Top" or "Bottom", affecting where the volatility meter is displayed relative to price action.

Progress Bar Length :

Description : Set the horizontal length of the ATR Strength progression bar.

Details : Adjust to increase or decrease the bar's width, accommodating different chart sizes and user preferences.

Enhanced Calculations :

ATR Strength Calculation : Calculate the ATR strength to measure market volatility.

Dynamic Coefficients : Use dynamic coefficients based on volatility for more accurate calculations.

Progress Bar Calculation : Determine the position and color of the progression bar based on ATR strength.

Label Positioning : Dynamically position labels for minimum and maximum values to avoid overlap.

Plotting ATR Strength Meter :

Progression Bar Plotting : Plot the progression bar to represent the ATR strength.

Label Customization : Customize labels for the ATR strength, minimum, and maximum values.

📘 Enhanced Relative Strength Index Integration

(A special thanks to RumpyPumpyDumpy for allowing the private reuse of his script.)

Purpose : Measures market momentum using the Relative Strength Index (RSI) and Stochastic RSI to assist in identifying potential buy and sell points.

Usage : Set the RSI and StochRSI parameters, toggle the display of the RSI Meter, and customize its appearance for better market analysis.

RSI Calculation Parameters :

RSI Length : Defines the length of the RSI calculation.

Details : A longer period captures more data points but may reduce sensitivity.

RSI Overbought Level : Sets the overbought level for RSI.

Details : Values above this level indicate overbought conditions.

RSI Oversold Level : Sets the oversold level for RSI.

Details : Values below this level indicate oversold conditions.

StochRSI Length : Defines the length of the StochRSI calculation.

Details : A longer period captures more data points but may reduce sensitivity.

StochRSI %K Length : Defines the length of the %K line of the StochRSI.

StochRSI %D Length : Defines the length of the %D line (SMA of %K) of the StochRSI.

RSI Visualization Parameters :

Display RSI Meter : Toggle the display of the RSI Meter on the chart.

RSI Meter Size : Adjust the size of the RSI Meter displayed on the chart.

Details : Measured as the diameter of the meter. Increase the value for larger display size, enhancing visibility and making it easier to read the RSI trend at a glance.

Horizontal Offset : Move the RSI Meter horizontally across the chart.

Details : Positive values shift the meter to the left, allowing for placement adjustments relative to the chart's current view or specific visual preferences.

RSI Meter Components :

Sectors and Ticks : Draw sector arcs and tick marks around the RSI Meter to represent different RSI levels and thresholds.

Needle : Draw the needle on the RSI Meter to indicate the current RSI value.

Sector Labels : Label each sector of the RSI Meter to indicate market conditions like "Strong Buy," "Buy," "Neutral," "Sell," and "Strong Sell."

Title Label : Draw the title label for the RSI Meter displaying the RSI value and its period.

Enhanced Calculations :

RSI Calculation : Calculate the RSI using the built-in function with the specified length and source.

StochRSI Calculation : Calculate StochRSI values using the specified lengths for RSI, %K, and %D.

Dynamic Line Management : Efficiently manage and update dynamically created line objects to prevent potential memory leaks.

Optimized Sector and Needle Drawing : Enhanced the drawing functions for sectors, needles, and ticks to improve visual clarity and performance.

Plotting RSI Meter :

Sector Plotting : Draw the sectors on the RSI Meter using specified colors and widths to represent different RSI levels and thresholds.

Needle Plotting : Plot the needle on the RSI Meter based on the calculated RSI value to visually indicate the current RSI level.

Tick Plotting : Plot tick marks around the RSI Meter to denote key RSI levels and thresholds for better readability.

Label Plotting : Draw sector labels and a title label on the RSI Meter to provide context and information about the RSI levels and their corresponding market conditions.

📘 Market Sentiment Integration

Purpose : Analyzes market sentiment using various indicators to provide an overall sentiment score.

Usage : Enable or disable individual sentiment indicators, set account type, and customize sentiment calculations for better market analysis.

Volatility Index (IV) :

Description : Enable or disable the use of the Volatility Index in sentiment calculation.

Details : When enabled, the Volatility Index (IV) provides insight into market sentiment by measuring market volatility. The selected Volatility Index varies based on your TradingView account type.

Account Type :

Description : Select your TradingView account type.

Details : Free accounts use SPX, while Premium accounts use VIX.

Put/Call Ratio (PCR) :

Description : Enable or disable the use of the Put/Call ratio in sentiment calculation.

Details : The Put/Call ratio is a sentiment indicator that measures the volume of put options traded relative to call options, indicating market sentiment towards bearish or bullish expectations.

Fear and Greed Index :

Description : Enable or disable the use of the Fear and Greed Index in sentiment calculation.

Details : The Fear and Greed Index gauges the prevailing emotions in the market, indicating whether investors are inclined towards fear (bearish sentiment) or greed (bullish sentiment).

Momentum Indicators :

Description : Enable or disable the use of momentum indicators like MACD and RoC in sentiment calculation.

Details : Momentum indicators help identify the strength and direction of price movements, assisting in sentiment analysis.

Adaptive Periods for Shorter Timeframes :

Description : Toggle this option to use shorter periods for sentiment indicators when analyzing lower timeframes.

Details : Enabling this option allows for more responsive and sensitive analysis when working with shorter timeframes.

Calculation Details :

Normalization Function : Normalize the values of the indicators over a 252-period range.

Set Periods Function : Set periods based on user preference for faster or slower periods, adjusting the analysis sensitivity.

IV Calculation : Calculate the IV value based on the selected Volatility Index (SPX for Free accounts, VIX for Premium accounts).

Put/Call Ratio Calculation : Calculate the Put/Call ratio using volume data, where put volume is proportional to the trading range, and call volume is proportional to the price change.

RoC Calculation : Calculate the Rate of Change (RoC) as a momentum indicator, measuring the percentage change in closing prices over a specified period.

Dynamic Thresholds : Define dynamic thresholds based on historical data, calculating mean and standard deviation to determine upper and lower thresholds for IV, PCR, and RoC.

📘 Enhanced Market Trend Dashboard Integration

Purpose : Provides a summary of key market indicators and signals in a single dashboard for quick and easy reference.

Usage : Customize the dashboard settings to display relevant market information, including Ichimoku components, Linear Regression, Support/Resistance levels, MACD, RSI, and Market Sentiment.

Market Trend Dashboard Parameters :

Display Market Trend Dashboard : Toggle to show or hide the market trend dashboard, providing a summary of key indicators and signals.

Panel Position : Select the position of the dashboard on the chart for optimal viewing.

Panel Text Size : Choose the text size for the information displayed in the dashboard, ensuring readability.

Panel Background Color : Set the background color of the market trend dashboard, enhancing contrast with the chart.

Ichimoku Dashboard Parameters :

Display Ichimoku Dashboard : Toggle to show or hide the Ichimoku section in the dashboard.

Display Tenkan-Sen Price Cross : Indicate when the price crosses the Tenkan-Sen line, signaling potential trade opportunities.

Display Kijun-Sen Price Cross : Indicate when the price crosses the Kijun-Sen line, often considered a stronger signal than Tenkan-Sen crosses.

Display Chikou Span Price Cross : Indicate Chikou Span price crosses, providing insight into potential trend reversals.

Display Kumo Breakout : Indicate Kumo (cloud) breakouts, which can signify major trend shifts.

Display Kumo Twist : Indicate Kumo twists, suggesting changing market dynamics and potential reversals.

Linear Regression Projection Dashboard Parameters :

Display LR Projection Dashboard : Toggle to show or hide the Linear Regression Projection section in the dashboard.

Display Linear Regression Period : Indicate the period used for Linear Regression Projection analysis.

Display Pearson R Details : Show the Pearson R value in the dashboard, indicating the strength and direction of the correlation in the Linear Regression Projection.

Supports and Resistances Dashboard Parameters :

Display S/R Dashboard : Toggle to show or hide the Support and Resistance section in the dashboard.

Display S/R Break Prices : Show the latest break prices of support and resistance levels in the dashboard.

MACD Dashboard Parameters :

Display MACD Dashboard : Toggle to show or hide the MACD section in the dashboard.

RSI Dashboard Parameters :

Display RSI Dashboard : Toggle to show or hide the Relative Strength Index section in the dashboard.

Display RSI Details : Show the RSI value and status in the dashboard.

Display StochRSI Details : Show the StochRSI %K, %D values and status in the dashboard.

Market Sentiment Dashboard Parameters :

Display Market Sentiment Dashboard : Enable or disable the display of the Market Sentiment Dashboard, which summarizes key market sentiment indicators like Implied Volatility, Put/Call Ratio, and Fear and Greed Index.

Display Implied Volatility Details : Show or hide the Implied Volatility details in the Market Sentiment Dashboard.

Display Put/Call Ratio Details : Show or hide the Put/Call Ratio details in the Market Sentiment Dashboard.

Display Fear and Greed Index Details : Show or hide the Fear and Greed Index details in the Market Sentiment Dashboard.

Enhanced Calculations :

Ichimoku Cloud Trend Calculation : Calculates trend based on the relationship between Ichimoku Cloud components, identifying bullish or bearish trends.

Support and Resistance Break Detection : Detects breaks in support and resistance levels and updates the dashboard accordingly.

Linear Regression Projection Calculation : Calculates Linear Regression Projection and Pearson R value for trend analysis.

MACD Signal Calculation : Determines MACD status based on histogram values.

RSI and StochRSI Calculation : Calculates RSI and StochRSI values and updates their statuses in the dashboard.

Market Sentiment Score Calculation : Calculates overall market sentiment score based on individual sentiment indicators.

Dynamic Alert Management : Manages alerts for various dashboard signals to prevent repeated alerts.

Real-Time Data Integration : Continuously updates the dashboard with real-time data for accurate and current trend analysis.

Plotting Market Trend Dashboard Components :

Ichimoku Components Plotting : Plots Tenkan-Sen, Kijun-Sen, Chikou Span, and Kumo cloud with dynamic adjustments.

Support and Resistance Levels Plotting : Plots support and resistance levels and updates them dynamically based on market data.

Linear Regression Projection Plotting : Plots the Linear Regression Projection line and labels with trend-based colors.

MACD and RSI Plotting : Plots MACD and RSI signals on the dashboard, including status updates.

Market Sentiment Indicators Plotting : Plots Market Sentiment indicators like IV, PCR, and Fear and Greed Index with dynamic updates.

Alert Notifications Plotting : Plots alert notifications for significant market changes based on dashboard signals.

Summary

This comprehensive market analyzer integrates multiple technical indicators, including machine learning, Ichimoku Kinkō Hyō, candlestick patterns, Fibonacci retracement, support and resistance levels, trend lines, linear regression, POC analysis, divergences, ATR, RSI, and market sentiment. Each section includes detailed descriptions and usage instructions to help traders understand how to effectively utilize the indicator in their trading strategies.

在腳本中搜尋"relative strength"

Average True Ranges with IBD RSAdvanced ATR Analysis with IBD Relative Strength

This comprehensive indicator combines Average True Range (ATR) analysis with IBD (Investor's Business Daily) Relative Strength calculation, providing both volatility measurement and momentum analysis in one powerful tool.

Key Features:

ATR Analysis:

Standard ATR: Customizable period (default 14) with multiple smoothing options

1.5x ATR: Extended range for wider stop-loss and target calculations

Smoothing Options: Choose between RMA, SMA, EMA, or WMA for ATR calculation

Customizable Colors: Distinct colors for easy visual identification

IBD Relative Strength:

Professional RS Formula: Uses the same calculation method as Investor's Business Daily

Multi-Timeframe Analysis: Compares current price to 3, 6, 9, and 12-month performance

Weighted Calculation: 40% weight on 3-month, 20% each on 6, 9, and 12-month performance

Zero-Based Scale: Values above 0 indicate outperformance, below 0 indicate underperformance

Trading Applications:

Volatility-Based Stops: Use ATR and 1.5x ATR for dynamic stop-loss placement

Position Sizing: ATR helps determine appropriate position size based on volatility

Relative Strength Analysis: IBD RS identifies stocks with superior momentum

Market Timing: High RS values often precede strong price moves

Risk Management: Combine volatility (ATR) with momentum (RS) for comprehensive analysis

Technical Details:

ATR Calculation: True Range smoothed over selected period with chosen method

IBD RS Formula: (40% × 3M) + (20% × 6M) + (20% × 9M) + (20% × 12M) - 100

Display: Separate pane indicator with customizable colors for each component

How to Interpret:

High ATR: Increased volatility, wider stops needed

Low ATR: Reduced volatility, tighter stops possible

Positive IBD RS: Stock outperforming market over measured periods

Negative IBD RS: Stock underperforming market over measured periods

Customizable Parameters:

ATR calculation length

Smoothing method for ATR

Individual colors for ATR, 1.5x ATR, and IBD RS lines

Perfect for swing traders and position traders who want to combine volatility analysis with relative strength momentum in their decision-making process. Particularly useful for stock selection and risk management.

Dual Custom Index with SpreadDual Custom Index with Spread

Create powerful custom indices from any instruments and analyze their relative strength dynamics

Overview

This advanced indicator allows you to build two completely customizable indices from your choice of instruments and analyze their spread relationship. Perfect for inter-market analysis, sector rotation strategies, currency strength comparisons, and sophisticated relative performance studies.

Key Features

🔧 Fully Customizable Index Construction

Build each index from up to 6 instruments with individual weightings

Enable/disable instruments on the fly without losing settings

Automatic weight validation ensures mathematically accurate calculations

Invert functionality for instruments that move opposite to index strength

📊 Advanced ADX-Based Methodology

Uses sophisticated ADX +DI/-DI directional bias calculations

Normalized bias calculation for consistent scaling across different instruments

Optimized default settings for intraday trading with full customization options

Professional-grade smoothing and filtering options

📈 Dual Analysis Modes

Difference Mode: Shows absolute strength difference (Index1 - Index2)

Ratio Mode: Shows relative performance ratio (Index1 / Index2)

Additional spread smoothing for cleaner signals

🎨 Professional Display Options

Custom labels with full color, size, and positioning control

Dynamic "Follow Line" labels that move with your data

Static corner positioning for reference displays

Clean error messaging and validation feedback

Use Cases

Gold Trading: Create gold strength vs USD strength indices for precise market timing

Sector Analysis: Compare technology vs financial sector strength for rotation strategies

Currency Strength: Build custom currency baskets for advanced forex analysis

Commodity Spreads: Analyze relative strength between different commodity groups

Regional Markets: Compare strength between different geographical market indices

Crypto Analysis: Track relative performance between different cryptocurrency sectors

Technical Specifications

Instruments per Index: Up to 6 with individual enable/disable

Weight Validation: Automatic 100% total weight enforcement

Calculation Method: ADX-based directional bias with trend strength weighting

Smoothing Options: Multiple levels of customizable smoothing

Error Handling: Professional validation with clear user feedback

Optimization Tips

Intraday Trading: Use DI Length 3-7 for faster response

Daily Analysis: Use DI Length 10-14 for smoother signals

Noisy Markets: Increase Final Smoothing for cleaner signals

Trending Markets: Lower smoothing values for faster reaction

Perfect for traders who need sophisticated inter-market analysis tools beyond standard indicators. Whether you're analyzing gold vs dollar dynamics, sector rotation opportunities, or custom currency strength relationships, this indicator provides institutional-grade analysis capabilities with complete customization flexibility.

VIV 1.0 // AN IDEA BY Sunil SethiVIV (Very Important Volume) is a custom-built TradingView indicator designed to decode the psychology behind price and volume behavior — whether you are a breakout trader, reversal trader, or use your own discretionary logic. VIV reveals where institutional activity is likely taking place, highlights trend stages, uncovers volume footprints, and identifies high-probability trading zones — all with zero lag & 100% price-action-based logic.

Key Features (Expanded Concepts)

01. Trend-Based Analysis with Stages and Background Colors

VIV breaks down the market into three color-coded stages based on trend confirmation:

Stage 3: Uptrend (Short-Term Trend Confirmation)

Marks early accumulation or consolidation.

Shows possible reversal zones.

Short-term traders use this to spot opportunities before a breakout.

Stage 2: Uptrend (Medium-Term Trend Confirmation)

Highlights the start of a strong directional move.

Confidence zone for position building and breakout-following strategies.

Stage 1: Uptrend (Long-Term Trend Confirmation)

Indicates long term strength.

These trend stages reflect the emotional phases of market participants and the shifting balance of power between buyers and sellers. You can toggle trend backgrounds for intraday, daily, weekly, and monthly trends and change their background colors.

Note : If the % difference in Stage 3 exceeds 10%, the stock is considered extended. Such setups should be evaluated with caution before making any trade decisions.

02. . Volume Footprints (➕ Signs)

VIV intelligently identifies past candles with high-volume activity (accumulation/distribution).

These are not typical breakout volumes, but subtle footprints of smart money.

Help spot reversal points, liquidity zones, and retest levels.

Valuable for both breakout and reversal traders to confirm zone strength.

You can enable or disable these lines, adjust color, style, and width via VIV Line Settings.

03. VIV || H, VIV || L and VIV || C Zones

Automatically plots horizontal levels from high-volume, high-activity candles—revealing the footprints of smart money.

VIV || H (High) = Top of important bar.

VIV || L (Low) = Bottom of important bar.

VIV || C (Close) = Close price of important bar.

Key levels used by traders for:

Entries

Stop-loss placement

Targets

These zones show where price historically reacted due to strong institutional presence. They come with customizable label colors and backgrounds.

04. Price Tightness Detection

Detects when two or more candles compress within the range of a larger parent candle.

Represents indecision, contraction, or coiling behavior before major price moves.

Ideal for both:

Breakout traders looking for base formations.

Reversal traders watching for exhaustion.

Color-coded markers indicate such tight price zones — disabled by default but can be enabled.

05. Technical Stats Panel (Important Data Table)

An insightful dashboard providing:

ADR% – Volatility-based movement expectations (change period via input).

ATR – Real volatility indicator.

Average Volume / Price Volume – Customizable average period and currency unit (INR/USD).

Trend Data:

10/20/200 SMAs

10-week & 20-week trend stages (custom SMA period/timeframe supported)

Relative Strength vs Benchmark

RS grade: GREAT, GOOD, FAIR, UNCERTAIN, UNDER PERFORMER, LAGGARD, POOR

When RS is comparing: BOTH STRONG, BOTH WEEK

You can also display the benchmark symbol name and change the symbol for relative strength comparison.

06. Relative Strength Grade Change Alerts

VIV tracks relative strength changes against a chosen benchmark (e.g., Nifty MidSmallCap).

The above tells us that if the stock is stronger or weaker than the benchmark.

Detects when relative strength shifts from:

Strong → Weak (e.g., EXCELLENT → GOOD → FAIR)

Weak → Strong (e.g., LAGGARD → POOR → FAIR → GOOD)

Sudden transitions (e.g., WORST → FAIR, BOTH WEAK → GOOD, BOTH GOOD → POOR)

BOTH WEAK → GOOD or BOTH GOOD → POOR means stock's strength is better/poor than the benchmark

and more.

These alerts can help in:

Early trend following

Exiting when RS degrades

Adding positions when RS improves

07. Smart Alerts (Built-in Conditions)

You can set alerts for (any timeframe)

Positive Trend

Negative Trend

Rise in Volume

Relative Strength Changed

Set your preferred interval and trigger type in TradingView to stay updated without chart-watching.

08. Pivot Points

VIV allows visualizing pivot highs and lows using a dynamic window (left/right lookback).

Customizable label text and background color.

Helpful in identifying support or resistance zones and breakout points.

09. Customization Options

Toggle modules like trend background, labels, stats, and volume zones.

Customize colors for:

Labels

Zones

Trend backgrounds

Table text, borders, and alignment

Adjust visibility per timeframe (inputs tab)

How to Use VIV Effectively

Use trend background colors to identify phase (base, uptrend, top).

Look for stage 1, stage 2 and stage 3 for short, medium and long term trend.

Watch for old high-volume candles (➕ marks) to plan entries/exits.

Trade around ➕ marks, VIV || H and VIV || L levels.

Use tight price zones to anticipate explosive moves.

Monitor table for ATR/ADR, RS grade, and moving averages.

Use alerts to automate monitoring of trend, volume, or RS shifts.

Best Suited For:

Reversal traders (demand/supply based)

Breakout traders using base-building logic

Systematic or discretionary traders

Anyone who values price-volume behavior over lagging indicators

MB - Currency Strength ROCCurrency Strength ROC Enhanced is a technical indicator designed to measure and visualize the relative strength of different currencies in the foreign exchange market. Using a Rate of Change (ROC) approach and moving averages, this indicator provides valuable insights into the dynamics of currency strengths.

Key Features:

Relative Strength Measurement:

Calculates the strength of each currency relative to others, allowing you to identify which currencies are appreciating or depreciating.

Strength Histogram:

Presents normalized strength in a histogram format, making it easy to quickly see areas of positive (green) and negative (red) strength

Moving Averages:

Includes moving averages of normalized strength and trend, providing a clear view of the overall direction of strength over time.

Overbought and Oversold Zones:

Highlights critical levels of strength through horizontal lines, allowing traders to identify potential trend reversals.

MTF RSI+CMO PROThis RSI+CMO script combines the Relative Strength Index (RSI) and Chande Momentum Oscillator (CMO), providing a powerful tool to help traders analyze price momentum and spot potential turning points in the market. Unlike using RSI alone, the CMO (especially with a 14-period length) moves faster and accentuates price pops and dips in the histogram, making price shifts more apparent.

Indicator Features:

➡️RSI and CMO Combined: This indicator allows traders to track both RSI and CMO values simultaneously, highlighting differences in their movement. RSI and CMO values are both plotted on the histogram, while CMO values are also drawn as a line moving through the histogram, giving a visual representation of their relationship. The often faster-moving CMO accentuates short-term price movements, helping traders spot subtle shifts in momentum that the RSI might smooth out.

➡️Multi-Time Frame Table: A real-time, multi-time frame table displays RSI and CMO values across various timeframes. This gives traders an overview of momentum across different intervals, making it easier to spot trends and divergences across short and long-term time frames.

➡️Momentum Chart Label: A chart label compares the current RSI and CMO values with values from 1 and 2 bars back, providing an additional metric to gauge momentum. This feature allows traders to easily see if momentum is increasing or decreasing in real-time.

➡️RSI/CMO Bullish and Bearish Signals: Colored arrow plot shapes (above the histogram) indicate when RSI and CMO values are signaling bullish or bearish conditions. For example, green arrows appear when RSI is above 65, while purple arrows show when RSI is below 30 and CMO is below -40, indicating strong bearish momentum.

➡️Divergences in Histogram: The histogram can make it easier for traders to spot divergences between price and momentum. For instance, if the price is making new highs but the RSI or CMO is not, a bearish divergence may be forming. Similarly, bullish divergences can be spotted when prices are making lower lows while RSI or CMO is rising.

➡️Alert System: Alerts are built into the indicator and will trigger when specific conditions are met, allowing traders to stay informed of potential entry or exit points based on RSI and CMO levels without constantly monitoring the chart. These are set manually. Look for the 3 dots in the indicator name.

How Traders Can Use the Indicator:

💥Identifying Momentum Shifts: The RSI+CMO combination is ideal for spotting momentum shifts in the market. Traders can monitor the histogram and the CMO line to determine if the market is gaining or losing strength.

💥Confirming Trade Entries/Exits: Use the real-time RSI and CMO values across multiple time frames to confirm trades. For instance, if the 1-hour RSI is above 70 but the 1-minute RSI is turning down, it could indicate short-term overbought conditions, signaling a potential exit or reversal.

💥Spotting Divergences: Divergences are critical for predicting potential reversals. The histogram can be used to spot divergences when RSI and CMO values deviate from price action, offering an early signal of market exhaustion.

💥Tracking Multi-Time Frame Trends: The multi-time frame table provides insight into the market’s overall trend across several timeframes, helping traders ensure their decisions align with both short and long-term trends.

RSI vs. CMO: Why Use Both?

While both RSI and CMO measure momentum, the CMO often moves faster with a value of 14 for example, reacting to price changes more quickly. This makes it particularly effective for detecting sharp price movements, while RSI helps smooth out price action. By using both, traders get a clearer picture of the market's momentum, particularly during volatile periods.

Confluence and Price Fluidity:

One of the powerful ways to enhance the effectiveness of this indicator is by using it in conjunction with other technical analysis tools to create confluence. Confluence occurs when multiple indicators or price action signals align, providing stronger confirmation for a trade decision. For example:

🎯Support and Resistance Levels: Traders can use RSI+CMO in combination with key support and resistance zones. If the price is nearing a support level and RSI+CMO values start to signal a bullish reversal, this alignment strengthens the case for entering a long position.

🎯Moving Averages: When the RSI+CMO signals a potential trend reversal and this is confirmed by a crossover in moving averages (such as a 50-day and 200-day moving average), traders gain additional confidence in the trade direction.

🎯Momentum Indicators: Traders can also look for momentum indicators like the MACD to confirm the strength of a trend or potential reversal. For instance, if the RSI+CMO values start to decrease rapidly while both the RSI+CMO also shows overbought conditions, this could provide stronger confirmation to exit a long trade or enter a short position.

🎯Candlestick Patterns: Price fluidity can be monitored using candlestick formations. For example, a bearish engulfing pattern with decreasing RSI+CMo values offers confluence, adding confidence to the signal to close or short the trade.

By combining the MTF RSI+CMO PRO with other tools, traders ensure that they are not relying on a single indicator. This layered approach can reduce the likelihood of false signals and improve overall trading accuracy.

Gaussian RSI For Loop [TrendX_]The Gaussian RSI For Loop indicator is a sophisticated tool designed for trend-following traders seeking to identify strong uptrends in the market. By integrating a Gaussian and Weighted-MA (GWMA) with the Relative Strength Index (RSI), this indicator employs a loop-based scoring system to provide clear signals for potential trading opportunities. The combination of Gaussian smoothing techniques and overbought/oversold filtering enhances the indicator's ability to capture significant price movements while reducing noise, making it an optimal choice for traders aiming to capitalize on robust upward trends.

💎 KEY FEATURES

Gaussian Weighted Moving Average (GWMA): Smooths price data to reduce noise and enhance responsiveness to significant price changes.

Filtered RSI: Applies the RSI to Gaussian-filtered data, allowing for more accurate momentum readings.

Wavetrend Analysis: Calculates the difference between the Filtered RSI and its short-term moving average, providing additional insights into momentum shifts.

Loop-Based Scoring System: Evaluates the strength and direction of uptrends through a systematic analysis of the Filtered RSI against defined thresholds.

⚙️ USAGES

Identifying Strong Uptrends: Traders can use this indicator to pinpoint periods of strong upward momentum, helping them make informed decisions about entering long positions and its exits.

Trend and Signal Confirmation: The Score confirms Long and Exit signals which traders can see through the Dots on the Gaussian RSI.

🔎 BREAKDOWN

Gaussian-Filtered Data:

The first component of the Gaussian RSI For Loop is the application of a GWMA to the sourced price data. This smoothing technique uses weighted averages based on a Gaussian distribution, which emphasizes more recent prices while diminishing the impact of older prices. This GWMA effectively reduces market noise, allowing traders to focus on significant price movements. By adjusting weights using sigma parameters, traders can fine-tune the sensitivity of the indicator, making it more responsive to genuine market trends while filtering out minor fluctuations that could lead to misleading signals.

Filtered RSI:

Next, the RSI is applied to the Gaussian-filtered data. The RSI measures the speed and change of price movements, providing insights into overbought or oversold conditions. By applying the RSI to smoothed price data, traders obtain a clearer view of momentum without the distortion caused by sudden price spikes or drops. This results in more reliable readings that help identify potential trend reversals or continuations.

Wavetrend Analysis:

The Wavetrend component calculates the difference between the Filtered RSI and its short-term moving average (MA). This difference serves as an additional momentum indicator. When the Filtered RSI is above its short-term MA, it suggests that upward momentum is strengthening; conversely, when it falls below, it indicates weakening momentum. This analysis helps traders confirm whether an uptrend is gaining strength or losing traction.

Loop-Based Scoring System:

Range Analysis: The system evaluates the Filtered RSI by comparing its current value against overbought (OB) and oversold (OS) thresholds over a defined range. This systematic approach ensures that each value within this range contributes to understanding overall trend strength.

Score Calculation: As the loop iterates through values within the defined range, it adjusts a score based on whether the current Filtered RSI and its previous values are higher or lower than established OB and OS levels. This scoring mechanism quantifies trend strength and direction.

Strong Uptrend Trigger: A strong uptrend signal is generated when the score exceeds a predefined Score Threshold (Long). This indicates that bullish momentum is robust enough to warrant entry into long positions.

None Trend: Conversely, if the score falls below the Score Threshold (Short), it suggests that upward momentum has weakened significantly, signaling potential exit points and it can be consolidated or downtrend.

DISCLAIMER

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur. Therefore, one should always exercise caution and judgment when making decisions based on past performance.

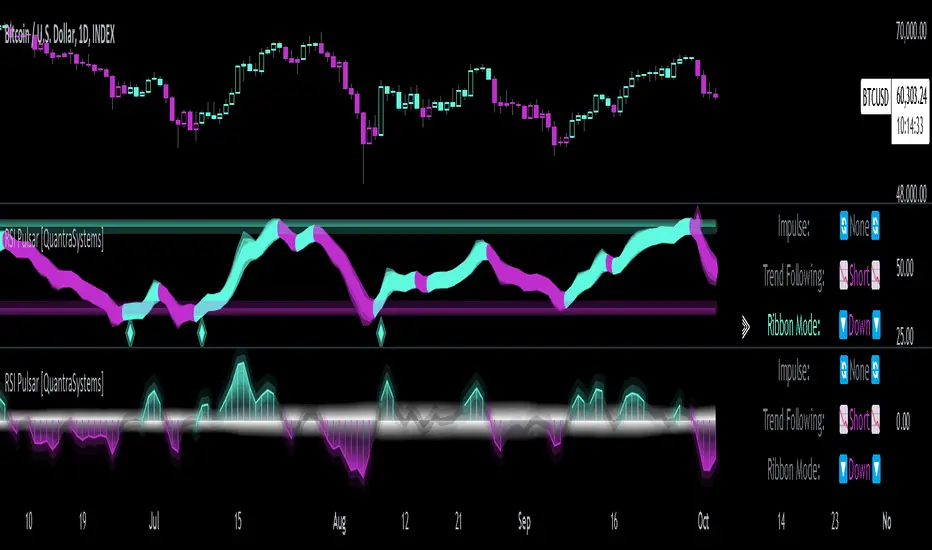

RSI Pulsar [QuantraSystems]RSI Pulsar

Introduction

The RSI Pulsar is an advanced and multifaceted tool designed to cater to the varying needs of traders, from long-term swing traders to higher-frequency day traders. This indicator takes the Relative Strength Index (RSI) to new heights by combining several unique methodologies to provide clear, actionable signals across different market conditions. With its ability to analyze impulsive trend strength, volatility, and binary market direction, the RSI Pulsar offers a holistic view of the market that assists traders in identifying robust signals and rotational opportunities within a volatile market.

The integration of dynamic color coding further aids in quick visual assessments, allowing traders to adapt swiftly to changing market conditions, making the RSI Pulsar an essential component in the arsenal of modern traders aiming for precision and adaptability in their trading endeavors.

Legend

The RSI Pulsar encapsulates various modes tailored to diverse trading strategies. The different modes are the:

Impulse Mode:

Focuses on strong outperformance, ideal for capturing movements in highly dynamic tokens.

Trend Following Mode:

A classical perpetual trend-following approach and provides binary long and short signal classifications ideal for medium term swing trading.

Ribbon Mode: