VPTbollfib & Camarilla (Danarilla)I do not own the original indicators. This is just a combination of the two because of their nature to work in a similar way.

Camarilla Pivots run on the basis of intraday range trading. Usually after daily open you look the fade whatever move happened before. by shorting R3/H3 levels or longing R3/L3. Targeting the other side of the range. This is the infamous PivotBoss level calculations and you would want to activate camarilla and turn off the normal pivots. They use the previous days volatility to plot the next days levels.

But what about some confirmation?

Well RafaelIzoni (who made it open source for improvement) threw together this VPTbollfib. It is volume price trend crossing down a fib line using bollinger bands as price envelope. The beauty of this is that It will signal usually counter to current price action based on selling into uptrends or vise versa. Meaning you get signals to counter price. Which is what you might be looking for on range day trade scalps for camarilla. A wick reversal or engulfing + volume based signal is a very happy pairing together. And those signals are usually suitable for the target of the range you are day trading. Hourly time frame works quite well for both. And camarilla should also be on daily settings.

Special Thanks to Nanda (who published the pivotboss indicator AND) Helped to merge the scripts together.

This indicator alone is an entire trade system. Camarilla already is. If you know the rules. it can be used for entries, exits, risk management to trade the range on TREND, COUNTER TREND, and BREAKOUT plays. The bollinger band fibs add confirmation to the trends levels. And the VPT adds a secondary confirmation to take a camarilla trade.

Try it out. I think you will find both the levels on camarilla and the VPT signals quite suprising.

在腳本中搜尋"reversal"

Higher Highs & Lower Lows Stochastics - Vitali ApirineThis is my modified "Higher Highs & Lower Lows Stochastics" employing PSv4.0, originally formulated by Vitali Apirine for TASC - February 2016 Traders Tips. Reading through a TASC magazine of mine, behold, I found a little known indicator that I can't find anywhere on all of Tradingview. That was a tragedy I felt I had to resolve... This indicator is best described as a dual momentum indicator, being helpful with anticipating reversals, spotting emerging trends, and defining correction periods. I felt it worthy of justice to unveil this for all TV members to utilize and also learn from. It's uniqueness is beyond past due for the honor it deserves on Tradingview.

As always, I have included advanced Pine programming techniques that conform to proper "Pine Etiquette". For those of you who are newcomers to Pine Script, this code release may also help you comprehend the "Power of Pine" by employing advanced programming techniques while exhibiting code utilization in a most effective manner. This script's uniqueness displays that we can now override built-in Pine functions. Firstly, you may have noticed that I replaced ema(), sma(), highest(), and lowest(). If you weren't aware of this Pine capability, well, here is a prime example... Now you know! Just heed caution when doing so to ensure your replacement algorithms are 100% sound. Lastly, I also added an additional "Median" line where the companion stochastics seemingly appear to gravitate within a central zone.

NOTICE: You may have observed, there is highest(), lowest(), ema(), and sma() custom functions overwriting Pine built-ins, some of which are audaciously used in ternary. "IF" you are planning to use Pine Script v4.0 functions in ternary, be forewarned, they WILL NOT operate as expected in most scenarios. The reason why I legitimately used them here in ternary is because they are ONLY manually controlled by an input(). If these were dynamically controlled with bar-to-bar dynamic conditional logic, you would most certainly run into serious unexpected programming issues, potentially resulting in hours of frustrations and guaranteed loss of hair. That's my lesson for this release, so never ever forget this when utilizing the full potential of the "Power of Pine". For more information concerning these potential dilemmas, please consult "Execution of Pine functions and historical context inside function blocks" in the "Pine Script v4 User Manual".

Features List Includes:

Dark Background - Easily disabled in indicator Settings->Style for "Light" charts or with Pine commenting

AND much, much more... You have the source!

The comments section below is solely just for commenting and other remarks, ideas, compliments, etc... regarding only this indicator, not others. When available time provides itself, I will consider your inquiries, thoughts, and concepts presented below in the comments section, should you have any questions or comments regarding this indicator. When my indicators achieve more prevalent use by TV members, I may implement more ideas when they present themselves as worthy additions. As always, "Like" it if you simply just like it with a proper thumbs up, and also return to my scripts list occasionally for additional postings. Have a profitable future everyone!

Engulfing Candles DetectorHello traders

Credit to HPotter for that script

I took his script and added alerts to it. 2 lines lol

But anyway, useful to detect reversals by coloring bullish/bearish engulfing candles :)

Enjoy

David

RSI+ with Bollinger BandsRelative Strenght Index + SMA on RSI + Bollinger Bands on it - very good solution to see reversals and see lows and highs.

Use different timeframe.

StdDev is 2.17 by default to get 97% probability.

RSI + SMA с наложенными Bollinger Bands - прекрасное решение для поиска разворотных точек и аномального поведения цены.

Используйте разные таймфреймы одновременно.

StdDev = 2.17 по умолчанию для обеспечения попадания в диапазон в 97% случаев.

B3 Donchian CloudsThis is the Donchian Channel expressed with a percentage cloud. Default 12.5% of the range will be filled at each edge, this helps to show reversal possibilities as price returns to the area between the clouds. This offers a usage to essentially fade the turtle trader system. That system is loosely based on the playing of the breakouts of the the channel... as you can see the that last turtle trade long in YM1! was and is off the charts awesome. I will look for the fall out of the cloud to short the market.

B3 ECOBlau's Ergodic Candlestick Oscillator = a decent trend finder, however slightly lagged. It can help you to see a reversal entry if you are looking for one. I find the one line ECO hard to use, so I have created this histogram version with a signal line. The colors help to show you whats going on with the ECO and its bias. This indicator shows up in a couple books by people other than Blau, and namely by Krausz. You can also see divergences, for example in pic above the lower or second of the two green humps showing that the general uptrend might be weakened as this run contained less momentum. Tighten up the signal line to see a faster change in its color. These settings are the B3 input settings for default, meaning the ones I use in trading. They are not however the default values you might read about other places.

Adaptive Nadaraya-Watson (Non Repainting) [Metrify]To understand this implementation of the Nadaraya-Watson estimator, we have to look at the core equation governing non-parametric regression. This script aren't trying to average prices; we are trying to find the probability density of where price should be relative to its recent history.

1. The Kernel Physics (Bandwidth Modulation)

In standard kernel regression, you have a bandwidth parameter (h). This controls the "smoothness" of the curve. If h is too low, the curve jitters with every tick of noise. If h is too high, it acts like a sluggish SMA.

A static h fails because market volatility is dynamic. When the market explodes (high volatility), a tight bandwidth generates false signals. When the market sleeps, a wide bandwidth misses the micro-trends.

It try solving this by making h a function of the Asset's volatility ratio:

heff=h×max(0.5,min(SMA(ATR20,100)ATR20,2.0))

If the current ATR(20) is double the long-term average (100), the bandwidth doubles. This forces the estimator to "zoom out" during chaos, effectively ignoring noise that would otherwise look like a reversal.

vol_ratio = use_vol ? vol_raw / (vol_base == 0 ? 1 : vol_base) : 1.0

vol_mod = math.max(0.5, math.min(vol_ratio, 2.0))

h_eff = h_val * vol_mod

2. The Gaussian Loop (Endpoint Estimation)

Standard Nadaraya-Watson scripts repaint because they calculate the regression over a full window centered on the bar. To make this usable for live trading, we must calculate the Endpoint Estimate.

We iterate backward from the current bar (i=0) to the lookback limit. For every historical price Xi, we calculate a weight wi based on how far away it is in time (distance).

The weight is derived from the Gaussian Kernel function:

wi=exp(−2heff2i2)

Price data closer to the current bar (i=0) gets a weight near 1.0. Data further away (i=50) decays exponentially toward 0.

for i = 0 to lookback by 1

float dist = float(i)

float w = math.exp(-math.pow(dist, 2) / (2 * math.pow(h_eff, 2)))

num := num + w * src

den := den + w

3. Statistical Deviation (MAE vs. StDev)

Most Bollinger Band-style indicators use Standard Deviation (Root Mean Square). The problem with StDev is that it squares the errors, which heavily penalizes large outliers. In crypto or volatile forex pairs, one wick can blow out the bands for 20 bars.

This one use Mean Absolute Error (MAE) instead.

MAE=N1∑∣Price−y^∣

MAE is linear. It measures the average distance price strays from the kernel estimate without squaring the penalty. This creates "tighter" bands that adhere closer to price action during normal trend behavior but don't expand ridiculously during a flash crash.

Pine Script

float error = math.abs(src - y_hat)

float mae = ta.sma(error, lookback)

We project two sets of bands:

Inner Band (Balanced): The "Noise Zone". Price inside here is considered random walk.

Outer Band (Precision): The "Exhaustion Zone". Price reaching here is statistically unlikely (2.8x MAE).

Input & Visual Summary

Kernel Physics:

h_val: The base smoothness. Lower (e.g., 6) = faster, noisier. Higher (e.g., 10) = slower, smoother.

use_vol: Keep this TRUE. It prevents the bands from being too tight during news events.

Envelope Statistics:

mult_in / mult_out: These are your risk settings. 1.5/2.8 is a standard deviation-like setting suited for MAE.

Hooke's Law: Market ElasticityHooke's Law: Market Elasticity is a physics-based mean reversion system that models price action using the principles of Classical Mechanics.

Most technical indicators treat the market as a purely statistical entity. This script takes a different approach, treating the market as a physical object with Mass (Volume) and Stiffness (Volatility) . By adapting Hooke’s Law of Elasticity (𝐹=−𝑘𝑋), it visualizes the "Tensile Stress" between price and its equilibrium, identifying the exact moment when a trend becomes unsustainable and must "snap back."

The Physics of Trading

In physics, Hooke's Law states that the force needed to extend a spring is proportional to the distance it is stretched. We map this to financial markets using four key components:

Equilibrium (𝑋=0): The "Resting State" of the market, calculated using a Volume-Weighted Moving Average (VWMA) . This represents the fair value where buyers and sellers agree.

2. Displacement (𝑋): The distance price travels away from this equilibrium.

3. Spring Constant (𝑘): We use Volatility (Standard Deviation) to measure the market's "stiffness."

• Low Volatility: The spring is loose; price can wander far without snapping.

• High Volatility: The spring is stiff; even small deviations create massive tension.

4. Force (𝐹): The calculation is weighted by Relative Volume . A price spike on low volume has low force (easy to reverse), while a spike on high volume carries high momentum (harder to reverse).

Visual Guide & Signals

The indicator uses a hierarchy of visuals to guide you through the trade lifecycle:

1. The Elastic Ribbon (Heatmap)

Connects Price to the Baseline. As the ribbon turns Solid White , the market has reached its Elastic Limit (Critical Zone). This is your warning that a move is overextended.

2. The "Golden" Labels (LONG / SHORT)

These are your Entry Signals . They appear only when the physics "snap" is confirmed by an internal momentum filter and price action.

3. The Small Circles (Minor Reversions)

These dots represent "Minor Snaps." They occur when the elastic tension releases, but the momentum filter hasn't fully confirmed a major reversal.

• Usage: These are excellent Early Warning signs or Scale-In points for aggressive traders.

Strategy: Entries, Exits & Take Profits

This script is designed as a complete system. Here is how to manage the trade using the visual cues:

• Entry: Wait for a LONG or SHORT label to appear.

• Stop Loss: Use the Solid White Line that appears automatically with the signal. If price touches this line, the physics setup has failed—exit immediately.

• Take Profit 1 (The Equilibrium): The Gray Baseline represents the market's center of gravity. In mean reversion trading, price tends to snap back to this line. This is the statistically highest-probability target.

• Take Profit 2 (The Circles): If you are in a trade and a Circle appears in the opposite direction, it indicates the market is experiencing counter-tension. This is an ideal place to secure partial profits or trail your stop.

Settings & Configuration

• Baseline Length (Default: 34): The lookback period for the Center of Gravity.

• Elasticity Limit (Default: 2.618): The Golden Ratio is used as the standard deviation threshold for the "Critical Zone."

• Volume Weighting (Default: True): Recommended. Adds the "Mass" component to the physics calculation.

• Stop Loss Buffer (Default: 0.5): The distance (in Sigma) for the Stop Loss placement.

Risk Disclaimer

Not Financial Advice: This indicator is designed for educational and analytical purposes only. It visualizes market data based on mathematical formulas (Hooke's Law and Statistical Deviation) and does not guarantee future performance or profits.

Market Risks: Financial trading involves significant risk. The "Critical Zones" and "Signals" generated by this script identify statistical extremes, but markets can remain irrational or overextended for long periods ("Plastic Deformation").

Usage: Do not trade blindly based on these signals. Always use this tool in conjunction with your own analysis, risk management, and stop-losses. The author assumes no responsibility for any trading losses incurred while using this script.

Market Reversal Time HighlightsThis indicator marks the times when the market has an inflection or reversal.

This script is customizable and free to use

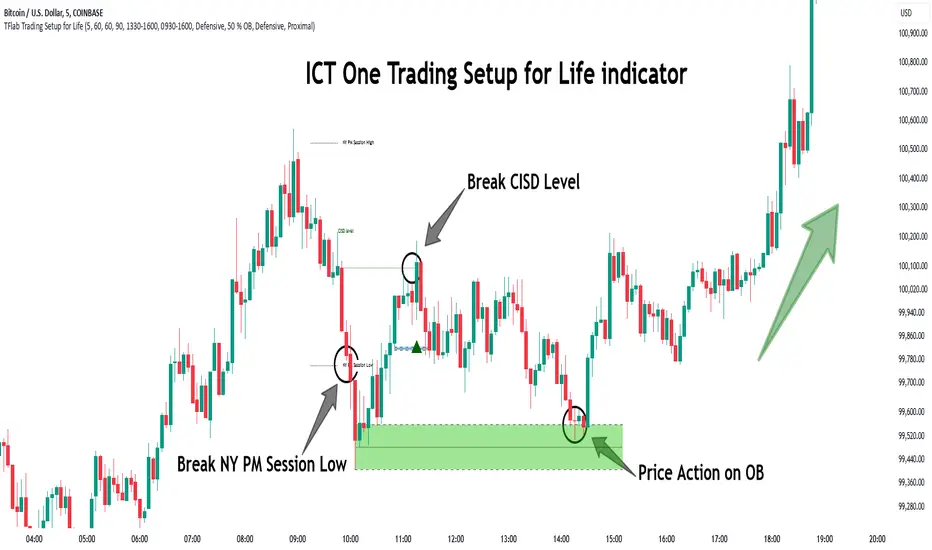

One Trading Setup for Life ICT [TradingFinder] Sweep Session FVG🔵 Introduction

ICT One Trading Setup for Life is a trading strategy based on liquidity and market structure shifts, utilizing the PM Session Sweep to determine price direction. In this strategy, the market first forms a price range during the PM Session (from 13:30 to 16:00 EST), which includes the highest high (PM Session High) and lowest low (PM Session Low).

In the next session, the price first touches one of these levels to trigger a Liquidity Hunt before confirming its trend by breaking the Change in State of Delivery (CISD) Level. After this confirmation, the price retraces toward a Fair Value Gap (FVG) or Order Block (OB), which serve as the best entry points in alignment with liquidity.

In financial markets, liquidity is the primary driver of price movement, and major market participants such as institutional investors and banks are constantly seeking liquidity at key levels. This process, known as Liquidity Hunt or Liquidity Sweep, occurs when the price reaches an area with a high concentration of orders, absorbs liquidity, and then reverses direction.

In this setup, the PM Session range acts as a trading framework, where its highs and lows function as key liquidity zones that influence the next session’s price movement. After the New York market opens at 9:30 EST, the price initially breaks one of these levels to capture liquidity.

However, for a trend shift to be confirmed, the CISD Level must be broken.

Once the CISD Level is breached, the price retraces toward an FVG or OB, which serve as optimal trade entry points.

Bullish Setup :

Bearish Setup :

🔵 How to Use

In this strategy, the PM Session range is first identified, which includes the highest high (PM Session High) and lowest low (PM Session Low) between 13:30 and 16:00 EST. In the following session, the price touches one of these levels for a Liquidity Hunt, followed by a break of the Change in State of Delivery (CISD) Level. The price then retraces toward a Fair Value Gap (FVG) or Order Block (OB), creating a trading opportunity.

This process can occur in two scenarios : bearish and bullish setups.

🟣 Bullish Setup

In a bullish scenario, the PM Session High and PM Session Low are identified. In the following session, the price first breaks the PM Session Low, absorbing liquidity. This process results in a Fake Breakout to the downside, misleading retail traders into taking short positions.

After the Liquidity Hunt, the CISD Level is broken, confirming a trend reversal. The price then retraces toward an FVG or OB, offering an optimal long entry opportunity.

The initial take-profit target is the PM Session High, but if higher timeframe liquidity levels exist, extended targets can be set.

The stop-loss should be placed below the Fake Breakout low or the first candle of the FVG.

🟣 Bearish Setup

In a bearish scenario, the market first defines its PM Session High and PM Session Low. In the next session, the price initially breaks the PM Session High, triggering a Liquidity Hunt. This movement often causes a Fake Breakout, misleading retail traders into taking incorrect positions.

After absorbing liquidity, the CISD Level breaks, indicating a shift in market structure. The price then retraces toward an FVG or OB, offering the best short entry opportunity.

The initial take-profit target is the PM Session Low, but if additional liquidity exists on higher timeframes, lower targets can be considered.

The stop-loss should be placed above the Fake Breakout high or the first candle of the FVG.

🔵 Setting

CISD Bar Back Check : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

Order Block Validity : The number of candles that determine the validity of an Order Block.

FVG Validity : The duration for which a Fair Value Gap remains valid.

CISD Level Validity : The duration for which a CISD Level remains valid after being broken.

New York PM Session : Defines the PM Session range from 13:30 to 16:00 EST.

New York AM Session : Defines the AM Session range from 9:30 to 16:00 EST.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

Demand Order Block : Enables or disables bullish Order Block.

Supply Order Block : Enables or disables bearish Order Blocks.

Demand FVG : Enables or disables bullish FVG.

Supply FVG : Enables or disables bearish FVGs.

Show All CISD : Enables or disables the display of all CISD Levels.

Show High CISD : Enables or disables high CISD levels.

Show Low CISD : Enables or disables low CISD levels.

🔵 Conclusion

The ICT One Trading Setup for Life is a liquidity-based strategy that leverages market structure shifts and precise entry points to identify high-probability trade opportunities. By focusing on PM Session High and PM Session Low, this setup first captures liquidity at these levels and then confirms trend shifts with a break of the Change in State of Delivery (CISD) Level.

Entering a trade after a retracement to an FVG or OB allows traders to position themselves at optimal liquidity levels, ensuring high reward-to-risk trades. When used in conjunction with higher timeframe bias, order flow, and liquidity analysis, this strategy can become one of the most effective trading methods within the ICT Concept framework.

Successful execution of this setup requires risk management, patience, and a deep understanding of liquidity dynamics. Traders can enhance their confidence in this strategy by conducting extensive backtesting and analyzing past market data to optimize their approach for different assets.

Three-Bar Reversal SignalThis indicator is a simple setup of Three Bar Reversal. Logic of the code is as below.

Rules :

Long Setup

Bar 1 closes down

Low of Bar 2 is below the low of Bar 1 (and Bar 3)

Bar 3 closes above the high of both Bar 1 and Bar 2

Buy at the close of Bar 3

Short Setup

Bar 1 closes up

High of Bar 2 is above the high of Bar 1 (and Bar 3)

Bar 3 closes below the low of both Bar 1 and Bar 2

Sell at the close of Bar 3

Volume ReversalsThe "Volume Reversals" indicator is a trading tool designed to identify potential buy and sell signals based on volume patterns.

Features

Filter Signals : Traders can enable or disable additional filtering of signals, which refines the conditions under which buy and sell labels are displayed.

Buy and Sell Labels: The indicator dynamically places labels on the chart to signify buy ("▲+") and sell ("▼+") opportunities. Buy labels appear at low points of bars with a green upward-pointing arrow, while sell labels appear at high points with a red downward-pointing arrow.

Customizable Alerts: Users can set alerts for buy and sell signals, receiving notifications when conditions match predefined patterns.

Logic Explained

Volume Comparison: The script examines a sequence of the last five volume bars to detect increasing or decreasing trends.

Price Action Analysis: Each volume bar is paired with a corresponding price action (bullish or bearish) from the same period.

Signal Conditions: A signal is generated under two scenarios:

Normal Conditions: Sequential increase/decrease in volume over three bars accompanied by bearish/bullish price action, followed by a dip in volume with a bullish/bearish bar.

Filtered Conditions (if filter is active): Requires all last four bars to be bearish/bullish, the most recent bar's volume to be less than the immediate previous, and then exceeds the volume two bars prior, closing bullish/bearish.

This indicator is suited for various assets and timeframes, especially in markets where volume plays a significant role in price dynamics.

Crypto Realized Profits/Losses Extremes [AlgoAlpha]🌟🚀 Introducing the Crypto Realized Profits/Losses Extremes Indicator by AlgoAlpha 🚀🌟

Unlock the potential of cryptocurrency markets with our cutting-edge On-Chain Pine Script™ indicator, designed to highlight extreme realized profit and loss zones! 🎯📈

Key Features:

✨ Realized Profits/Losses Calculation: Uses real-time data from the blockchain to monitor profit and loss realization events.

📊 Multi-Crypto Compatibility: The Indicator is compatible on other Crypto tickers besides Bitcoin.

⚙️ Customizable Sensitivity: Adjust the look-back period, normalization period, and deviation thresholds to tailor the indicator to your trading style.

🎨 Visual Enhancements: Choose from a variety of colors for up and down trends, and toggle extreme profit/loss overlay for easy viewing.

🔔 Integrated Alerts: Set up alerts for high and extreme profit or loss conditions, helping you stay ahead of significant market movements.

🔍 How to Use:

🛠 Add the Indicator: Add the indicator to favorites. Customize settings like period lengths and deviation thresholds according to your needs.

📊 Market Analysis: Monitor the main oscillator and the bands to understand current profit and loss extremes in the market. When the oscillator is at the upper band, this means that the market is doing really well and traders/investors will be likely to take profit and cause a reversal. The opposite is true when the oscillator reaches the lower band. The main oscillator can also be used for trend analysis.

🔔 Set Alerts: Configure alerts to notify you when the market enters a zone of high profit or loss, or during trend changes, enabling timely decisions without constant monitoring.

How It Works:

The indicator calculates a normalized area under the RSI curve applied on on-chain data regarding the number of wallets in profit. It employs a custom "src" variable that aggregates data from the blockchain about profit and loss addresses, adapting to intraday or longer timeframes as needed. The main oscillator plots this normalized area, while the upper and lower bands are plotted based on a deviation metric to identify extreme conditions. Colored fills between these bands visually denote these zones. For interaction, the indicator plots bubbles for extreme profits or losses and provides optional bar coloring to reflect the current market trend.

🚀💹 Enjoy a comprehensive, customizable, and visually engaging tool that helps you stay ahead in the fast-paced crypto market!

Catching Trend Reversals by shorting tops and buying bottomsHOLP (High of the low period) and LOHP (Low of the high period)

Catching Trend Reversals by shorting tops and buying bottoms

using this Swing High/Low Indicator

Trading Strategy comes from Mastering the Trade, by John Carter pg 300.

Trading Rules for Sells, Buys are reversed

1. Identifying a trending market, where today's price is making a 20-day high (17-18 day highs are also fine)

Note this is configurable by setting the trending period variable (defaults to 20)

For example if price is making a 20 period high or 20 period low, it will show a triangle up/down above the candle.

2. Identify the high bar in the uptrend

3. Go short once the price action closes below the low of this high bar

4. The initial stop is the high of the high bar.

5. If you are in the trade on the third day or period, use a 2 bar trailing stop.

You can check 2-bar trailing stop to draw the line, defaults to off.

Stop is indicated by the white dot.

Code Converted from TradeStation EasyLanguage

I can't find the original source anymore for the swing high/low plots, but if someone knows,

let me know and I'll credit here.

Fibonacci Ranges (Real-Time) [LuxAlgo]The "Fibonacci Ranges" indicator combines Fibonacci ratio-derived ranges (channels), together with a Fibonacci pattern of the latest swing high/low.

🔶 USAGE

The indicator draws real-time ranges based on Fibonacci ratios as well as retracements. Breakouts from a Fibonacci Channel are also indicated by labels, indicating a potential reversal.

Each range extremity/area can also be used as support/resistance.

🔶 CONCEPTS

Fibonacci Channels

Latest Fibonacci

Both, Latest Fibonacci and Fibonacci Channels , display different Fibonacci levels (labels not included in the code):

However, the 2 react in a totally different way.

🔹 Fibonacci Channels

2 conditions must be fulfilled until a Fibonacci Channel is displayed:

New swing high/low

close has to be between chosen limits/levels ( Break level )

As visual guidance, chosen Break levels are accentuated by 2 small gray blocks:

Once the channel is displayed, it will remain visible until x consecutive bars break out of the chosen Break level at closing time.

• x consecutive bars is set by Break count .

The amount of breaks is counted in the code. When the price, without breaking the user-set limit, closes back between the 2 levels, the count is reset to 0.

By enabling Channels and Shadows you can see previous channels (" Shadows ", which is always delayed with 1 bar)

Previous channels can be helpful in finding potential support/resistance areas, especially from large channel blocks

The more narrow Break levels are set the less chance the price closes between these 2 levels, and the quicker close breaks out.

In other words, narrow levels give fewer & smaller channels, broader levels give more & larger channels.

Note:

• swing settings: L & R

• Break count (x consecutive bars that close outside chosen levels to invalidate the Fibonacci Channel )

will also be of influence in displaying the channels.

• Show breaks enable you to visualize signals when there is a break:

• Alerts can also be set ( Break Down / Break Up )

🔹 Latest Fibonacci

This displays the Fibonacci levels between the latest swing high and swing low, independently from the Fibonacci Channel .

The Lastest Fibonacci can be helpful in detecting the current trend against the larger Fibonacci Channel .

🔶 SETTINGS

🔹 Swing Settings

L: set left of pivothigh / pivotlow

R: set right of pivothigh / pivotlow

🔹 Fibonacci Channels

Channel : Channel / Channels + Shadows / None

Break level

-0.382 - 1.382

0.000 - 1.000

0.236 - 0.764

0.382 - 0.618

Break count

🔹 Fibonacci

Toggle

Colours: [ -0.382 - 0 ], [ 0.236 - 0.382 ], [ 0.5 ], [ 0.618 - 0.764 ], [ 1 - 1.382 ]

MTF ATR Levels by makuchakuKnowing how big a range one is operating in (from a higher time frame perspective) is very important to understand where the reversals could potentially come from.

This indicator uses the closing price of previous HTF candle and plots its ATR range - and several levels on top of it.

+/- 75%

+/- 100%

+/- 150%

+/- 200%

+/- 300%

Adjustable MA & Alternating Extremities [LuxAlgo]Returns a moving average allowing the user to control the amount of lag as well as the amplitude of its overshoots thanks to a parametric kernel. The indicator displays alternating extremities and aims to provide potential points where price might reverse.

Due to user requests, we added the option to display the moving average as candles instead of a solid line.

Settings

Length: MA period, refers to the number of most recent data points to use for its calculation.

Mult: Multiplicative factor for each extremity.

As Smoothed Candles: Allows the user to show the MA as a series of candles instead of a solid line.

Show Alternating Extremities : Determines whether to display the alternating extremities or not.

Lag: Controls the amount of lag of the MA, with higher values returning a MA with more lag.

Overshoot: Controls the amplitude of the overshoots returned by the MA, with higher values increasing the amplitude of the overshoots.

Usage

Moving averages using parametric kernels allows users to have more control over characteristics such as lag or smoothness; this can greatly benefit the analyst. A moving average with reduced lag can be used as a leading moving average in a MA crossover system, while lag will benefit moving averages used as slow MA in a crossover system.

Increasing 'Lag' will increase smoothness while increasing 'overshoot' will reduce lag.

The following indicator puts more emphasis on its alternating extremities, an upper extremity will be shown once the high price crosses the upper extremity, while a low extremity will be shown once the low price crosses the lower extremity. These can be interpreted like extremities of a band indicator.

The MA using a length value of 200 with a multiplicative factor of 1.

In general, extremities will effectively return points where price might potentially bounce in ranging markets while closing prices under trending markets will often be found above an upper extremity and under a lower extremity.

Reducing the lag of the moving average allows the user to obtain a more timely estimate of the underlying trend in the price, with a better fit overall. This allows the user to obtain potentially pertinent extremities where price might reverse upon a break, even under trending markets.

In the above chart, the price initially breaks the upper extremity, however, we can observe that the upper extremity eventually reaches back the price, goes above it, provides a resistance, and effectively indicates a reversal.

Users can plot candles from the moving average, these are fairly similar to heikin-ashi candles in the sense that CandleOpen(t) ≠ CandleClose(t-1) , each point of the candle is calculated as follows for our indicator:

Open = Average between MA(t-1) and MA(t-2)

High = MA using the high price as input

Low = MA using the low price as input

Close = MA using the closing price as input

Details

Lag is defined as the effect of moving averages to reflect past price variations instead of new ones, lag can be observed by the user and is the main cause of false signals. Lag is proportional to the degree of filtering returned by the moving average.

Overshooting is a common effect encountered in non-lagging moving averages, and is defined as the tendency of a moving average to exceed a maximum level (or minimum level, which can be defined as undershooting )

MA and rolling maximum/minimum, both using a length of 50 bars. While we can think of lag as a cost of smoothness, we can think of overshooting as a cost for reduced lag on some occasions.

Explaining the kernel design behind our moving average requires understanding of the logic behind lag reduction in moving averages. This can prove to be complex for non informed users, but let's just focus on the simpler part; moving averages can be defined as a weighted sum between past prices and a set of coefficients (kernel).

MA(t) = b(0)C(t) + b(1)C(t-1) + b(2)C(t-2) + ... + b(n-1)C(t-n-1)

Where n is the period of the moving average. Lag is (non optimally) reduced by "underweighting" past prices - that is multiplying them by negative numbers.

The kernel used in our moving average is based on a modified sinewave. A weighted sum making use of a sinewave as a kernel would return an oscillator centered at 0. We can divide this sinewave by an increasing linear function in order to obtain a kernel allowing us to obtain a low lag moving average instead of a centered oscillator. This is the main idea in the design of the kernel used by our moving average.

The kernel equation of our moving average is:

sin(2πx^α)(1 - x^β)

With 1>x>0 , and where α controls the lag, while β controls the overshoot amplitude.

Using this equation we can obtain the following kernels:

Here only α is changed, while β is equal to 1. Values to the left would represent the coefficients for the most recent prices. Notice how the most significant coefficients are given to the oldest prices in the case where α increases.

Higher overshoot would require more negative values, this is controlled by β

Here only β is changed, while α is equal to 1. Notice how higher values return lower negative coefficients. This effectively increases the overshoots amplitude in our moving average. We can decrease α in order for these negative coefficients to underweight more recent values.

Using α = 0 allows us to simplify the kernel equation to:

1 - x^β

Using this kernel we can obtain more classical moving averages, this can be seen from the following results:

Using β = 1 allows us to obtain a linearly decreasing kernel (the one of a WMA), while increasing allows the kernel to converge toward a rectangular kernel (the one of SMA).

Golden Cross Optimised For Reversal (by Coinrule)A moving average crossing is a common and widely adopted trading strategy. A short-term MA crossing above a long-term one provides the buy-signal. The opposite generates a sell-signal for the strategy.

Although very popular, this strategy has some limitations that lead to frequent "false signals" and only a few very profitable trades. If the strategy provides two many trades, that generates

the risk for more potential losses

more transaction fees paid

capital allocated to the strategy, thus the impossibility of catching other potential opportunities.

Applying an additional filter to the strategy, consisting of the crossing happening below a longer-term moving average, allows increasing the chances of catching the first crossing signaling a reversal.

The indicator is set to work with three moving averages.

Buy signal: The MA(9) to cross above the MA(50), which must be below the MA(100)

Sell Signal: The MA(9) to cross below the MA(50)

This indicator works significantly better on lower time frames, where it can reduce the noise of getting too many non-profitable signals from a conventional crossing strategy.

The indicator has been backtested mostly on cryptocurrencies.

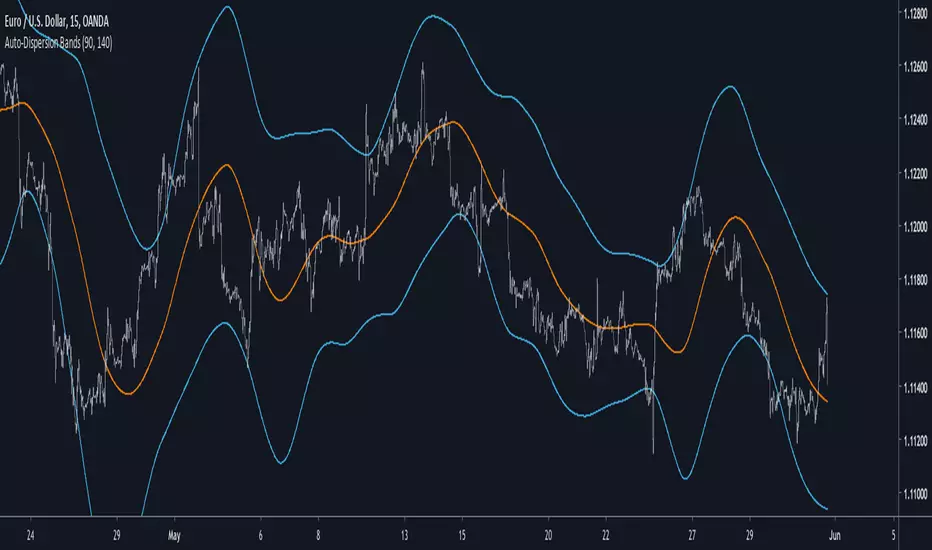

Auto-Dispersion BandsIntroduction

A really old indicator as well, thus i have no much ideas of what is going on with it, but i know that those bands returns good reversals points. The indicator don't use standard deviation, instead its a simple differencing of the price and the price length bars back who will provide a dispersion measurement, thus the name auto-dispersion.

The Indicator

The smooth parameter allow the band to cross the price, if smooth is low the chance of crosses are lower.

smooth = 3

PivotBoss Doji Reversal SetupPATTERN SUMMARY

1. The open and close price of the doji should fall within 10 percent of each other, as measured by the total range

of the candlestick.

2. For a bullish doji, the high of the doji candlestick should be below the ten-period simple moving average (H <

SMA(lO)).

3. For a bearish doji, the low of the doji candlestick should be above the ten-period simple moving average (L >

SMA(lO)).

4. For a bearish doji, one of the two bars following the doji must close beneath the low of the doji (C < L or C <

L ).

5. For a bullish doji setup, one of the two bars following the doji must close above the high of the doji (C > H )

or C > H )

PATTERN PSYCHOLOGY

The doji candlestick is the epitome of indecision. The pattern illustrates a virtual stalemate between buyers

and sellers, which means the existing trend may be on the verge of a reversal. If buyers have been controlling a

bullish advance over a period of time, you will typically see full-bodied candlesticks that personify the bullish

nature of the move. However, if a doji candlestick suddenly appears, the indication is that buyers are suddenly

not as confident in upside price potential as they once were. This is clearly a point of indecision, as buyers are no

longer pushing price to higher valuation, and have allowed sellers to battle them to a draw-at least for this one

candlestick. This leads to profit taking, as buyers begin to sell their profitable long positions, which is heightened

by responsive sellers entering the market due to perceived overvaluation. This "double whammy" of selling

pressure essentially pushes price lower, as responsive sellers take control of the market and push price back

toward fair value.

PivotBoss Outside Reversal SetupPATTERN SUMMARY

1. The engulfing bar of a bullish outside reversal setup has a low that is below the prior bar's low (L < L ) and a

close that is above the prior bar's high (C > H ).

2. The engulfing bar of a bearish outside reversal setup has a high that is above the prior bar's high (H > H )

and a close that is below the prior bar's low (C < L ).

3. The engulfing bar is usually 5 to 25 percent larger than the size of the average bar in the lookback period.

PATTERN PSYCHOLOGY

The power behind this pattern lies in the psychology behind the traders involved in this setup. If you have

ever participated in a breakout at support or resistance only to have the market reverse sharply against you, then

you are familiar with the market dynamics of this setup. What exactly is going on at these levels? To understand

this concept is to understand the outside reversal pattern. Basically, market participants are testing the waters

above resistance or below support to make sure there is no new business to be done at these levels. When no

initiative buyers or sellers participate in range extension, responsive participants have all the information they

need to reverse price back toward a new area of perceived value.

As you look at a bullish outside reversal pattern, you will notice that the current bar's low is lower than the

prior bar's low. Essentially, the market is testing the waters below recently established lows to see if a downside

follow-through will occur. When no additional selling pressure enters the market, the result is a flood of buying

pressure that causes a springboard effect, thereby shooting price above the prior bar's highs and creating the

beginning of a bullish advance.

If you recall the child on the trampoline for a moment, you'll realize that the child had to force the bounce

mat down before he could spring into the air. Also, remember Jennifer the cake baker? She initially pushed price

to $20 per cake, which sent a flood of orders into her shop. The flood of buying pressure eventually sent the price

of her cakes to $35 apiece. Basically, price had to test the $20 level before it could rise to $35.

Let's analyze the outside reversal setup in a different light for a moment. One of the reasons I like this setup

is because the two-bar pattern reduces into the wick reversal setup, which we covered earlier in the chapter. If

you are not familiar with candlestick reduction, the idea is simple. You are taking the price data over two or more

candlesticks and combining them to create a single candlestick. Therefore, you will be taking the open, high, low,

and close prices of the bars in question to create a single composite candlestick.

Take a look at Figure 2.13, which illustrates the candlestick reduction of the outside reversal setup.

Essentially, taking the highest high and the lowest low over the two-bar period gives you the range of the

composite candlestick. Then, taking the opening price of the first candle and the closing price of the last candle

will finish off the composite candlestick. Depending on the structure of the bars of the outside reversal setup, the

result of the candlestick reduction will usually be the transformation into a wick reversal setup, which we know to

be quite powerful. Therefore, in many cases the physiology of the outside reversal pattern basically demonstrates

the inherent psychological traits of the wick reversal pattern. This is just another level of analysis that reinforces

my belief in the outside reversal setup.

_mr_beach Liquidity Sweep + VWAP ReversalLiquidity Sweep + VWAP Reversal (Trend Filter, Session, 1 Trade per Day)

Overview

This strategy models a common institutional market behavior: liquidity is taken above the previous day’s high or below the previous day’s low, followed by a return toward fair value (VWAP) and a reversal in the direction of the prevailing trend.

Designed as a TradingView strategy for structured backtesting in the Strategy Tester.

Core Components

Liquidity Levels: Previous Day High / Previous Day Low

Fair Value Reference: VWAP

Trend Filter: EMA (default: 200)

Volatility-Based Risk: ATR

Trading Rules

Trend Filter

Long only when price closes above EMA

Short only when price closes below EMA

Liquidity Sweep

Bullish sweep: Low < Previous Day Low

Bearish sweep: High > Previous Day High

Entry Confirmation

Long: After a sweep below the Previous Day Low, price closes back above the level and above VWAP

Short: After a sweep above the Previous Day High, price closes back below the level and below VWAP

Risk Management

Stop Loss: ATR-based (slATR)

Take Profit: ATR-based (tpATR)

Automatically adapts to changing market volatility

Session & Trade Frequency

Optional session filter (default: 09:30–16:00 exchange time)

Optional one trade per day limit to reduce overtrading

Chart Elements

EMA (trend direction)

VWAP (fair value)

Previous Day High / Low (liquidity zones)

Alerts

Long setup: Liquidity sweep + VWAP reversal

Short setup: Liquidity sweep + VWAP reversal

Recommended Usage

Markets: Indices, liquid stocks, Forex majors, crypto

Timeframes: 5m, 15m

Note: Parameters such as ATR multipliers and session settings should be optimized per market

Disclaimer

This is a backtesting strategy, not financial advice.

Results depend on market conditions, timeframe, fees, and slippage.

Tags: Liquidity, VWAP, EMA, Reversal, Sweep, Smart Money, ICT, ATR, Strategy

Smart Money Flow Signals [QuantAlgo]🟢 Overview

The Smart Money Flow Signals indicator synthesizes significant volume-price dynamics through multi-component analysis to identify potential accumulation and distribution phases driven by substantial market participants. It combines Money Flow Index momentum, Chaikin Money Flow accumulation patterns, volume-weighted price momentum, and buying/selling pressure metrics into a unified composite oscillator that quantifies periods of concentrated capital movement, helping traders and investors identify conditions where significant volume participants may be actively positioning across multiple market conditions and timeframes.

🟢 How It Works

The indicator's core methodology lies in its weighted composite approach, where multiple volume-price components are calculated sequentially and then integrated to create a comprehensive significant flow activity signal.

First, the Money Flow Index (MFI) is calculated to measure buying and selling pressure by incorporating volume into price momentum analysis:

raw_money_flow = source * volume

positive_flow = source >= source ? raw_money_flow : 0

negative_flow = source < source ? raw_money_flow : 0

positive_money_flow = math.sum(positive_flow, mfi_period)

negative_money_flow = math.sum(negative_flow, mfi_period)

money_flow_index = 100 - 100 / (1 + positive_money_flow / negative_money_flow)

This creates an RSI-style momentum indicator that tracks whether money (price × volume) is flowing into or out of the asset, with values ranging from 0 to 100 where readings above 50 suggest buying pressure dominance.

Then, Chaikin Money Flow (CMF) is computed to evaluate accumulation and distribution by analyzing where prices close within each bar's range, weighted by volume:

money_flow_multiplier = high != low ? (close - low - (high - close)) / (high - low) : 0

money_flow_volume = money_flow_multiplier * volume

volume_sma = ta.sma(volume, trend_period)

chaikin_money_flow = volume_sma != 0 ? ta.sma(money_flow_volume, trend_period) / volume_sma : 0

Positive CMF values indicate accumulation (closes near the high of the range), while negative values indicate distribution (closes near the low of the range), with volume weighting emphasizing periods of significant participation.

Next, Volume Analysis is performed to quantify current volume intensity relative to historical averages:

volume_average = ta.sma(volume, trend_period)

volume_strength = volume_average != 0 ? volume / volume_average : 1

volume_weight = math.log(volume_strength + 1)

The logarithmic transformation creates a volume weight that amplifies signals during high-volume periods while preventing extreme volume spikes from overwhelming the composite calculation.

Following this, Buy/Sell Pressure is quantified by comparing cumulative volume during bullish versus bearish candles:

buying_pressure = math.sum(volume * (close >= open ? 1 : 0), trend_period)

selling_pressure = math.sum(volume * (close < open ? 1 : 0), trend_period)

pressure_ratio = (buying_pressure - selling_pressure) / (buying_pressure + selling_pressure) * 100

This creates a directional pressure ratio that reveals whether significant participants are predominantly buying or selling, expressed as a percentage between -100 (all selling) and +100 (all buying).

Then, Volume-Weighted Momentum is calculated through an exponential smoothing channel that adjusts price deviation based on volume intensity:

exponential_smooth_average = ta.ema(source, momentum_channel_period)

deviation = ta.ema(math.abs(source - exponential_smooth_average), momentum_channel_period)

channel_index = deviation != 0 ? (source - exponential_smooth_average) / (0.015 * deviation) * (1 + volume_weight * 0.5) : 0

This channel index measures how far price has deviated from its exponential average relative to typical deviation, with the volume weight multiplier (1 + volume_weight * 0.5) amplifying the signal when significant volume accompanies the price movement.

Finally, the Composite Wave is constructed by combining all components with specific weighting to create the final oscillator:

momentum_wave = ta.ema(channel_index, trend_period)

money_flow_wave = (money_flow_index - 50) * 1.2

chaikin_flow_wave = chaikin_money_flow * 100

composite_wave = momentum_wave * 0.5 + chaikin_flow_wave * 0.3 + money_flow_wave * 0.2

smoothed_wave = ta.sma(composite_wave, signal_smoothing)

This creates a multi-dimensional volume flow oscillator that combines price-volume momentum, accumulation-distribution patterns, and buying-selling pressure into a single signal, providing traders with probabilistic insights into periods of concentrated market activity and directional bias based on weighted component convergence.

🟢 Signal Interpretation

▶ Positive Values (Above Zero, Green): Composite money flow above equilibrium indicating net accumulation pressure, positive buying volume dominance, and bullish volume-price alignment = Favorable conditions for long positions, significant capital flowing into the asset = Buy/hold opportunities

▶ Negative Values (Below Zero, Red): Composite money flow below equilibrium indicating net distribution pressure, negative selling volume dominance, and bearish volume-price alignment = Unfavorable conditions for long positions, significant capital flowing out of the asset = Sell/short opportunities

▶ Extreme Overbought Zone: Excessive bullish money flow indicating potential accumulation exhaustion, where buying pressure may have reached unsustainable levels with elevated reversal risk = Caution on new longs, potential distribution phase beginning, profit-taking zone for existing positions

▶ Extreme Oversold Zone: Excessive bearish money flow indicating potential distribution exhaustion, where selling pressure may have reached unsustainable levels with elevated reversal risk = Caution on new shorts, potential accumulation phase beginning, buying opportunity zone for contrarian entries

▶ Smoothed Trend Line (White) Alignment: When the smoothed trend line confirms the composite wave direction, it validates the underlying volume-price trend and filters false signals caused by short-term noise

▶ Volume Intensity Correlation: Gradient intensity (color saturation) reflects combined wave strength, volume participation, and directional alignment, where darker/more saturated colors indicate stronger concentrated activity and higher-probability directional moves

🟢 Features

▶ Preconfigured Presets: Three optimized parameter configurations accommodate different trading styles, timeframes, and market analysis approaches.

1. "Default" provides balanced volume flow measurement suitable for swing trading on 4-hour and daily charts, offering moderate responsiveness to money flow shifts with standard RSI-equivalent MFI period and moderate smoothing for most market conditions.

2. "Fast Response" delivers heightened sensitivity optimized for active intraday trading and scalping on 1-minute to 1-hour charts, using compressed calculation periods across all components and minimal smoothing to capture rapid volume flow changes and quick trend shifts as they develop, ideal for early entry/exit opportunities with acceptance of increased signal frequency during consolidation.

3. "Smooth Trend" offers conservative extreme identification ideal for position trading and long-term analysis on daily to weekly charts, employing extended periods across all money flow components with substantial smoothing to filter short-term noise and isolate only strong, sustained accumulation and distribution phases driven by significant volume participants.

▶ Built-in Alerts: Seven alert conditions enable comprehensive automated monitoring of significant money flow transitions and extreme market states.

1. "Bullish Flow" triggers when the composite wave crosses above zero, signaling the shift from distribution to accumulation and concentrated buying activity beginning.

2. "Bearish Flow" activates when the composite wave crosses below zero, signaling the shift from accumulation to distribution and concentrated selling activity starting.

3. "Any Flow Direction Change" provides a combined notification for either bullish or bearish crossover regardless of direction, useful for general money flow momentum shifts.

4. "Extreme Overbought" alerts when the composite wave reaches or exceeds the overbought threshold (default +60), indicating excessive buying pressure and potential exhaustion.

5. "Extreme Oversold" notifies when the composite wave reaches or falls below the oversold threshold (default -60), indicating excessive selling pressure and potential capitulation.

6. "Overbought Reversal" triggers specifically when the wave crosses back down through the overbought level after being extended, signaling the beginning of distribution from extreme levels.

7. "Oversold Reversal" activates when the wave crosses back up through the oversold level after being extended, signaling the beginning of accumulation from extreme levels.

▶ Color Customization: Six visual themes (Classic, Aqua, Cosmic, Ember, Neon, plus Custom) accommodate different chart backgrounds and visual preferences, ensuring optimal contrast and immediate identification of bullish versus bearish volume flow conditions across various devices and screen sizes. Optional bar coloring provides instant visual context of current significant volume activity intensity and direction without switching between the price pane and indicator pane, enabling traders and investors to immediately assess volume-price positioning dynamics while analyzing price action.