DCA StrategyIntroducing the DCA Strategy, a powerful tool for identifying long entry and exit opportunities in uptrending assets like cryptocurrencies, stocks, and gold. This strategy leverages the Heikin Ashi candlestick pattern and the RSI indicator to navigate potential price swings.

Core Functionality:

Buy Signal : A buy signal is generated when a bullish (green) Heikin Ashi candle appears after a bearish (red) one, indicating a potential reversal in a downtrend. Additionally, the RSI must be below a user-defined threshold (default: 85) to prevent buying overbought assets.

Sell Signal : The strategy exits the trade when the RSI surpasses the user-defined exit level (default: 85), suggesting the asset might be overbought.

Backtesting Flexibility : Users can customize the backtesting period by specifying the start and end years.

Key Advantages:

Trend-Following: Designed specifically for uptrending assets, aiming to capture profitable price movements.

Dynamic RSI Integration: The RSI indicator helps refine entry signals by avoiding overbought situations.

User-Defined Parameters: Allows customization of exit thresholds and backtesting periods to suit individual trading preferences.

Commission and Slippage: The script factors in realistic commission fees (0.1%) and slippage (2%) for a more accurate backtesting experience.

Beats Buy-and-Hold: Backtesting suggests this strategy outperforms a simple buy-and-hold approach in uptrending markets.

Overall, the DCA Strategy offers a valuable approach for traders seeking to capitalize on long opportunities in trending markets with the help of Heikin Ashi candles and RSI confirmation.

在腳本中搜尋"rsi"

CULTURATRADING STRATEGYThe "CULTURATRADING STRATEGY" is designed to capitalize on market trends by incorporating a combination of technical indicators that signal potential entry and exit points for trades on various assets. This strategy is not just a mere collection of indicators but a well-thought-out approach that synergizes different market signals to optimize trade decisions.

The script uses the MACD (Moving Average Convergence Divergence) to gauge momentum and trend direction, with the slope of the MACD line serving as a trigger for market entries. A positive slope suggests an upward trend and potential long entry, while a negative slope indicates a downward trend and a possible short entry.

In tandem with the MACD, the ADX (Average Directional Index) is utilized to measure the strength of the trend. An ADX value above 25 signifies a strong trend, which, when aligned with MACD signals, can validate the trade entries.

The RSI (Relative Strength Index) is another critical component, identifying overbought and oversold conditions. This strategy looks for crossovers above and below key levels (60 for overbought, 40 for oversold) to determine high-probability turning points in the market. The inclusion of a 20-period SMA (Simple Moving Average) of the RSI adds a layer to filter the signals further, allowing for the refinement of entry and exit points.

The script employs a dynamic stop-loss system, set at the lowest low of the past 20 bars for long positions and the highest high for shorts, to manage risk effectively. The strategy is configured for a $10,000 account, risking a reasonable portion of capital per trade, with a pyramid effect to allow for diversified entries from various signals. The backtesting results are based on a 5% capital allocation per trade and include a 0.08% commission. To ensure accurate backtesting, the script includes an additional percentage to account for slippage within the commission.

To provide a comprehensive understanding, the script also outputs a "volatility histogram" based on the ADX, offering insights into market volatility and helping to time the trades better.

This strategy has been backtested across different timeframes and assets, showing resilience in various market conditions. It is essential to check the 'recalculate after order filled' option due to the dynamic nature of stop-loss orders.

This script is paired with the "CULTURATRADING INDICATOR" for enhanced signal clarity, providing a holistic view of the strategy's performance. Please note that this script is for educational purposes and should not be taken as financial advice.

The "CULTURATRADING INDICATOR" is an essential tool that works in conjunction with the "CULTURATRADING STRATEGY" to provide traders with a clear visualization of the market's conditions. It enhances the strategy by offering visual cues that help interpret complex market data more intuitively.

The indicator displays key RSI levels, such as 60 for overbought conditions and 40 for oversold conditions, with a mid-level at 55 to indicate when a trend may be weakening. The colors on the RSI line change to reflect these conditions, offering a quick reference for traders: a blue color signifies an RSI above 60, indicating overbought conditions; a red color shows an RSI below 40, pointing to oversold conditions; and white represents values in between, suggesting a neutral state.

Moreover, the volatility histogram, which is part of the "CULTURATRADING INDICATOR," provides a visual representation of market volatility. The histogram changes colors based on the ADX value and the slope of the MACD line. For instance, a green histogram suggests a positive MACD slope during a strong trend, indicating potential bullish momentum. Conversely, a red histogram implies a negative MACD slope during strong trends, hinting at bearish momentum. A grey color might be used to represent periods when the trend is weak or the market is less volatile.

Together, these visual elements of the "CULTURATRADING INDICATOR" complement the strategy's signals, providing traders with an at-a-glance summary of the current market scenario, which can be particularly useful when managing multiple trades or assessing opportunities quickly.

Please remember, this script and its associated indicator are designed to serve as educational tools to assist in understanding market dynamics and are not intended as financial advice. Always conduct your own research and consider consulting a financial advisor for personalized guidance.

Alex trading stragedyOverview

This script, named "ALEX TRADING STRATEGY", is a technical trading strategy designed for new investing groups. It uses a combination of various technical indicators to identify potential buying and selling opportunities in the market. The script includes the Relative Strength Index (RSI), Simple Moving Averages (SMA), Exponential Moving Averages (EMA), and Higher High Lower Low (HHLL) strategies to create a complete trading solution.

The user can change the position from long to short in the Input Settings. The script uses bar colors to indicate the current trading position. The script also has exit strategies to help manage the open trades. The user can also set the period for the various indicators used in the strategy.

The script provides various technical indicators and entry/exit signals to make the trading decision easier for the user. It also includes pivot lines, resistance and support levels to help the user make a more informed decision.

This Pine script implements a multi-indicator trading strategy that combines several technical analysis techniques for making trading decisions. The script uses the Relative Strength Index (RSI) to determine overbought and oversold conditions in the market and plots the RSI values on the chart. The RSI values above 70 are considered overbought and plotted as red upward triangles, while the RSI values below 30 are considered oversold and plotted as green downward triangles.

The script also calculates Simple Moving Averages (SMAs) with the user-defined period and plots them along with the Exponential Moving Averages (EMAs) of 20, 50, and 100 periods. Based on the crossover of the close price and the moving averages, the script enters long or short trades. The script sets the trade exit conditions as the low or high crossing the lower or upper band, respectively.

In addition to the moving average crossover, the script uses the highest high and lowest low over a user-defined period to determine long and short entries. The script plots the long and short conditions on the chart as green upward and red downward triangles, respectively. The script allows the user to switch between long and short trades by changing the input settings.

Finally, the script changes the bar colors based on the trade direction, with green bars indicating a long trade, red bars indicating a short trade, and blue bars indicating no trade. Overall, this Pine script provides a comprehensive trading strategy that combines several technical analysis techniques to make informed trading decisions.

HOW TO USE

Input Settings: In the Input Settings section, you can change the long to short position. You can also change the period value (default is 10) used to calculate the Simple Moving Average (SMA) for the Keltner channel.

Indicators: The script uses RSI (Relative Strength Index) with 14 periods as well as multiple EMAs (Exponential Moving Averages) with periods 20, 50, and 100 to help in making trading decisions.

Entry Signals: The script uses two main entry signals: (1) Keltner Channel and (2) HHLL (High-Low). When the closing price crosses above the upper band of the Keltner channel, the script generates a long signal, and when the closing price crosses below the lower band of the Keltner channel, the script generates a short signal. The HHLL strategy generates a long signal when the current high crosses above the highest high of the last "nPeriod" bars, and generates a short signal when the current low crosses below the lowest low of the last "nPeriod" bars.

Exit Signals: The script uses two exit signals: (1) Stop Loss based on Keltner channel and (2) Profit Target based on Keltner channel. The script exits the long position when the closing price crosses below the lower band of the Keltner channel, and the script exits the short position when the closing price crosses above the upper band of the Keltner channel.

To use this script, you will need to have access to a trading platform that supports PineScript, such as TradingView, and attach the script to a chart. The script will then automatically generate entry and exit signals based on the rules described above. It's important to note that this script is just a tool and not a guarantee of profit. As with any trading strategy, it's important to thoroughly test and understand the script before using it for live trading.

MATIC/USD 1H Bot for 3commas (works w/o 3commas too)This is a MATIC/USD or USDT specific implementation of my BNB/USD 1 hour bot. It should work out of the gate correctly for MATIC, at least based on what has been happening with it for the past seven weeks. You can fiddle with the following settings using the gear icon:

Fast and slow MACD length

The decision to use RSI thresholds as requirements for buys and/or sells, as well as the chart timeframe to use for that (make sure you use the same timeframe as your chart or a higher timeframe. You don't want to use a 1m RSI on a one hour chart but you can use a 4 hour RSI on a 1 hour chart with no issues.)

Buy and/or sell RSI threshold limits

Trailing stop loss %

Start date (for backtesting, I usually leave mine with 1-2 months trailing as those are usually better indicators than how they would have performed over the past few years)

Stress levels

Moving Average length and type

Linear regression amount

The gist of this bot is that it will use a smoothed EMA to make informed buys and sells. The smoothing prevents most noise from affecting your orders. It also allows you to set a trailing stop loss. If you don't want to use this feature set the value to 100 and it will effectively disable it.

Finally, you can disable RSI threshold point visibility. This won't affect bot operation, it just makes it cleaner to look at on your chart. Disabling RSI buys or sells will also disable visibility.

This bot takes a shotgun strategy to buys and sells. It makes a lot of buys and the majority of them are closed with little to no movement up or down. However, the ones that are profitable make a LOT as you will see once you start testing.

I make the full version of these bots available (though the script is protected) so users can test them, however if you want to use it with 3commas you will need access to the full script. Message me if you want the code and we can figure something out.

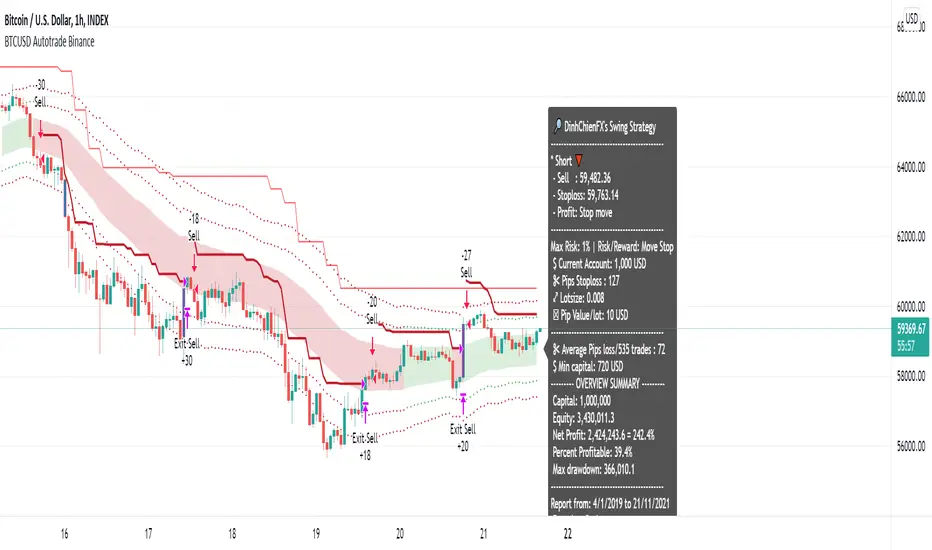

[BTCUSD] Multi Entries Autotrade BinanceCommission = 4 USD per order >>> check in the Performance Summary

Slippage = 2 ticks

- I see from Kodify (tradingview.com/pine-wizards)

Risk: 1% per trade >>> check at the "List of trades"

* Auto trade BINANCE FUTURE by Webhook + Pro, Pro+, Premium Tradingview user.

Binance future quantity setting:

- Fixed Quantity = 0 => Auto quantity (Balance, risk, pips loss)

- Fixed Quantity > 0 (0.001, 0.002, 0.01,...) => send signal with Fixed Quantity

H4 timeframe is main trend: Supertrend indicator.

- Uptrend when closes candle is below the red line

- Downtrend when closes candle is above the green line

H1 timeframe: Keltner Color count & RSI indicator:

- Keltner Color Count input:

- Length = 50

- Multi1 = 1

- Multi2 = 2

- Multi3 = 3

- Source = Close

- Lookback = 25

- RSI input: Length: 14, Source: Close

I. Entry 1: BASIS KELTNER CHANNEL

- BUY when previous OHLC4 candle crossover Basis line AND Supertrend H4 uptrend AND Keltner channels uptrend. Not repaint.

- SELL when previous OHLC4 candle crossunder Basis line AND Supertrend H4 downtrend AND Keltner channels downtrend. Not repaint.

II. Entry 2: UPPER 2/LOWER 1 KELTNER CHANNEL

- BUY when previous OHLC4 candle crossunder Upper 1 AND Supertrend H4 uptrend AND Keltner channels uptrend AND rsi uptrend. Not repaint.

- SELL when previous OHLC4 candle crossover Lower 1 AND Supertrend H4 downtrend AND Keltner channels downtrend AND rsi downtrend. Not repaint.

III. Entry 3: SELL UPPER 2/ BUY LOWER 1 KELTNER CHANNEL

- BUY when previous OHLC4 candle crossover Lower 1 AND Supertrend H4 uptrend AND Keltner channels uptrend AND rsi uptrend. Not repaint.

- SELL when previous OHLC4 candle crossunder Upper 1 AND Supertrend H4 downtrend AND Keltner channels downtrend AND rsi downtrend. Not repaint.

IV. Report all history BTCUSD (H1 timeframe)

- 01/01/2019 - 20/11/2021

- 01/01/2018 - 01/01/2021

- 01/01/2017 - 01/01/2020

- 01/01/2016 - 01/01/2019

- 01/01/2015 - 01/01/2018

- 01/01/2014 - 01/01/2017

- 01/01/2013 - 01/01/2016

- 01/01/2012 - 01/01/2015

TripleEMA + StochasticRSI + ATR Scalping Strategy by TradeSmartCOINBASE:BTCUSD Hello everyone and welcome to our second script release!

This script is one of many upcoming scripts. This one is a test for us, how it works, how you guys like this kind of stuff, and for feedback what we should change/improve at.

So feel free to comment any suggestions you have.

SCRIPT IS OPTIMIZED FOR:

BTC/USD (Coinbase) 15 minute timeframe

(Keep in mind default settings does not include trading fees, you can set it at the properties)

I recommend using this script on a trading exchange where the fees are extremely low or on an exchange where you get paid to place limit orders.

(I am not a financial avdvisor and none of this is financial advice.)

Now you can modify the following:

Stochastic RSI

3 different EMA

Length of ATR (for stop loss and take profit)

Stop Loss and Take Profit Risk to Reward ratio

Choice between Capital Risk on each trade or Risk of % of Capital

Allowing Short/Long entries only

Limit between dates

Trading days 1-7

We will update the script with more and more features taking in consideration your requests.

Hope you like it! Don't forget to let us know what we should change or improve. Thanks, and have a great day!

STRATEGY ENTRY RULES

LONG

When EMAs are lining up (meaning for ex. 400 < 13 < 7), and the Stochastic RSI crosses upwards (meaning blue line crosses orange upwards), then go long.

SHORT

When EMAs are lining down (meaning for ex. 7 < 13 < 400), and the Stochastic RSI crosses downwards (meaning blue line crosses orange downwards), then go short.

TAKE PROFIT

When price hits the exit price (calculated from stop loss with the risk ratio)

STOP LOSS

When price hits stop loss then exit the position.

QUANTITY TO BUY (Risk per Trade % or Capital %)

Risk Per Trade % attribute: we can set how much money we want to risk on one trade. Meaning that if we lose that particular position, then a Risk Per Trade % value of our equity will be lost.

Example: if you set the Risk Per Trade % to 1 % and you have a 100$ account balance, then if you loose the trade you will loose 1$ max.

Capital % we can set with how big % of our capital we want to enter into a position. Meaning that we enter with a set % of our capital.

Example: if you set the Capital % to 1 % and you have a 100$ account balance, then you will enter the position with 1$.

First Release Settings: (2021-10-25) for BTC/USD (Coinbase) 15 minute timeframe

Stochastic RSI settings: (Not displayed in the script. If you want to see it you have to add it separately.)

K: 3

D: 2

RSI Length: 6

Stochastic Length: 16

RSI Source: hlc3

EMA 1: 5

Source One: Close

EMA 2: 12

Source Two: Close

EMA 3: 215

Source Three: Close

Length of ATR: 16

Stop Loss Multiplier (risk): 3.6

Exit Price Multiplier (reward): 1

Risk Percentage: 3

Allow Long Entries: yes

Allow Short Entries: yes

Valid Trading Days: 1234567

The valid trading days of the Limit Trading Time feature. Numbers represent the days: Sunday (1), Monday (2), Tuesday (3), …, Saturday (7)

If you like this one, follow for more scripts! Thank you for your support!

[Advanced] Hilega-Milega IndicatorThis Indicator Name is Hilega Milega, and the original Idea given by Nitish Kumar, I just coded it and add some signals for backtesting.

it works on RSI + WMA and EMA plotted.

Default Values Used :

RSI = 9

WMA = 21

EMA = 3

But i added some extra, now everyone can change the Type of WMA and EMA, also SMA for trend confirmation,

How it works ??

Buy : When RSI crossover WMA or any Type of Moving Average you choose,

Sell : When RSI crossunder WMA or any Type of Moving Average you choose,

also:

Buy : When EMA crossover WMA or any Type of Moving Average you choose,

Sell : When EMA crossunder WMA or any Type of Moving Average you choose,

also:

Buy : When RSI + EMA crossover WMA or any Type of Moving Average you choose at the Same time,

Sell : When RSI + EMA crossunder WMA or any Type of Moving Average you choose at the Same time,

and Much More...! hope so you like it,

HYE Combo Market [Strategy] (Vwap Mean Reversion + Trend Hunter)In this strategy, I used a combination of trend hunter and vwap mean reversion strategies that I published before.

Trend Hunter Strategy:

Mean Reversion Vwap Strategy:

The results are quite impressive, especially for bitcoin.

While the hodl return for bitcoin was 13419%, the strategy's return in the same period was about 5 times (65000%) of this.

s3.tradingview.com

In this combo strategy, I made some changes to the original settings of the strategies used together and added some more new features.

Trend Hunter Strategy Settings: (Original / Combo)

- Slow Tenkansen Period : 9 / 9

- Slow Kijunsen Period : 26 / 13

- Fast Tenkansen Period : 5 / 3

- Fast Kijunsen Period : 13 / 7

- BB Length : 20 / 20

- BB Stdev : 2 / 2

- TSV Length : 13 / 20

- TSV Ema Length : 7 / 7

* I also added a "vidya moving average" to be used as a confirmation tool to open a long position. (Candle close must be above the vidya line.)

Vwap Mean Reversion Strategy Settings: (Original / Combo)

- Small Vwap : 2 / 8

- Big Vwap : 5 / 10

- Percent Below to Buy : 3 / 2

- RSI Period : 2 / 2

- RSI Ema Period : 5 / 5

- Maximum RSI Level for Buy : 30

* I also added a "mean vwap line" to be used for exits in this part of the strategy. In the original version, when small vwap crossovers big vwap, we close the position, but in this strategy we will wait for the close above the mean vwap.

TIPS AND WARNINGS

1-) The standard settings of this combo strategy is designed and tested with daily timeframe. For lower timeframes, you should change the strategy settings and find the best value for yourself.

2-) Only the mean vwap line is displayed on the graph. For a detailed view, you can delete the "//" marks from the plot codes in the strategy code.

3-) This is a strategy for educational and experimental purposes. It cannot be considered as investment advice. You should be careful and make your own risk assessment when opening real market trades using this strategy.

________________________________________________________

Bu stratejide, daha önce yayınladığım trend avcısı ve vwap ortalamaya geri dönüş stratejilerinin bir kombinasyonunu kullandım.

Sonuçlar özellikle bitcoin için oldukça etkileyici.

Bitcoin için hodl getirisi %13419 iken, stratejinin aynı dönemdeki getirisi bunun yaklaşık 5 katı (%65000) idi.

Bu kombo stratejide, birlikte kullanılan stratejilerin orijinal ayarlarında bazı değişiklikler yaptım ve bazı yeni özellikler ekledim.

Trend Avcısı Strateji Ayarları: (Orijinal / Combo)

- Yavaş Tenkansen Periyodu : 9 / 9

- Yavaş Kijunsen Periyodu : 26 / 13

- Hızlı Tenkansen Periyodu : 5 / 3

- Hızlı Kijunsen Periyodu : 13 / 7

- BB Uzunluğu : 20 / 20

- BB Standart Sapması : 2 / 2

- TSV Uzunluğu : 13 / 20

- TSV Ema Uzunluğu : 7 / 7

* Ayrıca long pozisyon açmak için onay aracı olarak kullanılmak üzere "vidya hareketli ortalama" ekledim. (Mum kapanışı vidya çizgisinin üzerinde olmalıdır.)

Vwap Ortalamaya Dönüş Stratejisi Ayarları: (Orijinal / Combo)

- Küçük Vwap : 2 / 8

- Büyük Vwap : 5 / 10

- Alış İçin Gerekli Fark Oranı : 3 / 2

- RSI Periyodu : 2 / 2

- RSI Ema Periyodu: 5 / 5

- Alış için gerekli maksimum RSI seviyesi : 30

* Stratejinin bu bölümünde pozisyondan çıkışlar için kullanılacak bir "ortalama vwap çizgisi" de ekledim. Orijinal versiyonda, küçük vwap, büyük vwap'ı yukarı kestiğinde pozisyonu kapatıyoruz, ancak bu stratejide, ortalama vwap'ın üzerindeki kapanışı bekleyeceğiz.

İPUÇLARI VE UYARILAR

1-) Bu birleşik stratejinin standart ayarları, günlük zaman dilimi ile tasarlanmış ve test edilmiştir. Daha düşük zaman dilimleri için strateji ayarlarını değiştirmeli ve kendiniz için en iyi değeri bulmalısınız.

2-) Grafikte sadece ortalama vwap çizgisi görüntülenir. Ayrıntılı bir görünüm için strateji kodundaki "plot" ile başlayan satırlarda grafikte görünmesini istediğiniz özelliğin önündeki "//" işaretlerini silebilirsiniz.

3-) Eğitim ve deneysel amaçlı bir stratejidir. Yatırım tavsiyesi olarak değerlendirilemez. Bu stratejiyi kullanarak gerçek piyasa işlem açarken dikkatli olmalı ve kendi risk değerlendirmenizi yapmalısınız.

72s Strat: Backtesting Adaptive HMA+ pt.1This is a follow up to my previous publication of Adaptive HMA+ few months ago, as a mean to provide some kind of initial backtesting tools. Which can be use to explore many possible strategies, optimise its settings to better conform user's pair/tf, and hopefully able to help tweaking your general strategy.

If you haven't read the study or use the indicator, kindly go here first to get the overall idea.

The first strategy introduce in this backtest is one most basic already described in the study; buy/sell is when movement is there and everything is on the right side; When RSI has turned to other side, we can use it as exit point (if in profit of course, else just let it hit our TP/SL, why would we exit before profit). Also, base on RSI when we make entry, we can further differentiate type of signals. --Please check all comments in code directly where the signals , entries , and exits section are.

Second additional strategy to check; is when we also use second faster Adaptive HMA+ for exit. So this is like a double orders on a signal but with different exit-rule (/more on this on snapshots below). Alternatively, you can also work the code so to only use this type of exit.

There's also an additional feature which you can enable its visuals, the Distance Zone , is to help measuring price distance to our xHMA+. It's just a simple atr based envelope really, I already put the sample code in study's comment section, but better gonna update it there directly for non-coder too, after this.

In this sample I use Lot for order quantity size just because that's what I use on my broker. Also what few friends use while we forward-testing it since the study is published, so we also checked/compared each profit/loss report by real number. To use default or other unit of measurement, change the entry code accordingly.

If you change your order size, you should also change the commission in Properties Tab. My broker commission is 5 USD per order/lot, so in there with example order size 0.1 lot I put commission 0.5$ per order (I'll put 2.5$ for 0.5 lot, 10$ for 2 lot, and so on). Crypto usually has higher charge. --It is important that you should fill it base on your broker.

SETTINGS

I'm trying to keep it short. Please explore it further again. (Beginner should also first get acquaintance with terms use here.)

ORDERS:

Base Minimum Profit Before Exit:

The number is multiplier of ongoing ATR. Means that when basic exit condition is met, algo will check whether you're already in minimum profit or not, if not, let it still run to TP or SL, or until it meets subsequent exit condition, then it will check again.

Default Target Profit:

Multiplier of ATR at signal. If reached before any eligible exit condition is met, exit TP.

Base StopLoss Point:

You can change directly in code to use other like ATR Trailing SL, fix percent SL, or whatever. In the sample, 4 options provided.

Maximum StopLoss:

This is like a safety-net, that if at some point your chosen SL point from input above happens to be exceeding this maximum input that you can tolerate, then this max point is the one will be use as SL.

Activate 2nd order...:

The additional doubling of certain buy/sell with different exits as described above. If enable, you should also set pyramiding to at least: 2. If not, it does nothing.

ADAPTIVE HMA+ PERIOD

Many users already have their own settings for these. So in here I only sample the default as first presented in the study. Make it to your adaptive.

MARKET MOVEMENT

(1) Now you can check in realtime how much slope degree is best to define your specific pair/tf is out of congestion (yellow) area. And (2) also able to check directly what ATR lengths are more suitable defining your pair's volatility.

DISTANCE ZONE

Distance Multiplier. Each pair/tf has its own best distance zone (in xHMA+ perspective). The zone also determine whether a signal should appear or not. (Or what type of signal, if you wanna go more detail in constructing your strategy)

USAGE

(Provided you already have your own comfortable settings for minimum-maximum period of Adaptive HMA+. Best if you already have backtested it manually too and/or apply as an add-on to your working strategy)

1. In our experiences, first most important to define is both elements in the Market Movement Settings . These also tend to be persistent for whole season since it's kinda describing that pair/tf overall behaviour. Don't worry if you still get a low Profit Factor here, but by tweaking you should start to see positive changes in one of Max Drawdown and Net Profit, or Percent Profitable.

2. Afterwards, find your pair/tf Distance Zone . When optimising this, what we seek is just a "not to bad" equity curves to start forming. At least Max Drawdown should lessen more. Doesn't have to be great already, but should be better, no red in Net Profit.

3. Then go manage the "Trailing Minimum Profit", TP, SL, and max SL.

4. Repeat 1,2,3. 👻

5. Manage order size, commission, and/or enable double-order (need pyramiding) if you like. Check if your equity can handle max drawdown before margin call.

6. After getting an acceptable backtest result, go to List of Trades tab and find the biggest loss or when many sequencing loss in a row happened. Click on it to go to exact point on chart, observe why the signal failed and get at least general idea how it can be prevented . The rest is yours, you should know your pair/tf more than other.

You can also re-explore your minimum-maximum period for both Major and minor xHMA+.

Keep in mind that all numbers in Setting are conceptually in a form of range . You don't want to get superb equity curves but actually a "fragile" , means one can easily turn it to disaster just by changing only a fraction in one/two of the setting.

---

If you just wanna test the strength of the indicator alone, you can disable "Use StopLoss" temporarily while optimising settings.

Using no SL might be tempting in overall result data in some cases, but NOTE: It is not recommended to not using SL, don't forget that we deliberately enter when it's in high volatility. If want to add flexibility or trading for long-term, just maximise your SL. ie.: chose SL Point>ATR only and set it maximum. (Check your max drawdown after this).

I think this is quite important specially for beginners, so here's an example; Hypothetically in below scenario, because of some settings, the buy order after the loss sell signal didn't appear. Let's say if our initial capital only 1000$ using leverage and order size 0,5 lot (risky position sizing already), moreover if this happens at the beginning of your trading season, that's half of account gone already in one trade . Your max SL should've made you exit after that pumping bar.

The Trailing Minimum Profit is actually look like this. Search in the code if you want to plot it. I just don't like too many lines on chart.

To maximise profit we can try enabling double-order. The only added rule coded is: RSI should rising when buy and falling when sell. 2nd signal will appears above or below default buy/sell signal. (Of course it's also prone to double-loss, re-check your max drawdown after. Profit factor play its part in here for a long run). Snapshot in comparison:

Two default sell signals on left closed at RSI exit, the additional sell signal closed later on when price crossover minor xHMA+. On buy side, price haven't met our minimum profit when first crossunder minor xHMA+. If later on we hit SL on this "+buy" signal, at least we already profited from default buy signal. You can also consider/treat this as multiple TP points.

For longer-term trading, what you need to maximise is the Minimum Profit , so it won't exit whenever an exit condition happened, it can happen several times before reaching minimum profit. Hopefully this snapshot can explain:

Notice in comparison default sell and buy signal now close in average after 3 days. What's best is when we also have confirmation from higher TF. It's like targeting higher TF by entering from smaller TF.

As also mention in the study, we can still experiment via original HMA by putting same value for minimum-maximum period setting. This is experimental EU 1H with Major xHMA+: 144-144, Flat market 13, Distance multiplier 3.6, with 2nd order activated.

Kiwi was a bit surprising for me. It's flat market is effectively below 6, with quite far distance zone of 3.5. Probably because I'm using big numbers in adaptive period.

---

The result you see in strategy tester report below for EURUSD 15m is using just default settings you see in code, as follow:

0,1 lot for each order (which is the smallest allowed by my broker).

No pyramiding. Commission: 0.5 usd per order. Slippage: 3

Opening position is only using basic strategy #1 (RSI exit). Additional exit not activated.

Minimum Profit: 1. TP: 3.

SL use: Half-distance zone. Max SL: 4.5.

Major xHMA+: 172-233. minor xHMA+: 89-121

Distance Zone Multiplier: 2.7

RSI: Standard 14.

(From our forward-testing, the difference we get from net profit is because of the spread, our entry isn't exactly at the close/open price. Not so much though, but not the same. If somebody can direct me to any example where we can code our entry via current bid/ask price, that would be awesome!)

It's already a long post (sorry), think I'm gonna pause here. Check out the code :)

---

DISCLAIMER: Past performance is no guarantee of future results , and so on.. you know the drill ;)

Please read whole description first before using, don't take 1-2 paragraph and claim it's the whole logic, you are responsible of your own actions and understanding.

MACD Strategy KMACK Rev 1.1Hull smoothed 45/10 macd

Please note that the macd/rsi values do not print unless the current day is Monday-Friday and the market will be open.

14 period hull smoothed rsi marks the rsi value at each macd reversal and will not signal a long position above 70 or a short position below 30

Macd and rsi will only display on the current day and will only display the last 2 hours

Lit candles occur after 0920 nyse time

Alerts or entries will only fire after 0931 nyse time

Entry signal will confirm with the 5 minute candle.

Long entry requires the current 5 minute candle to close>=hlc3

Short entry requires the current 5 minute candle to close<=hlc3

Buy/sell alerts will only fire in the last 10 seconds of the realtime (current) bar

Options:

Select bias

Modify macd lookback period(s)

Alerts:

Buy

Sell

Rsi crossing into the power region (60)

Rsi crossing into the weakness region (40)

Current strategy exits position upon signal opposite to selected bias, this is for simplicity.

There are currently no add-on strat signals but the alerts/lit candles will fire

Successful trades average >55% with an average profit factor of 3%

Net profit averages 3%

Max drawdown averages below 0.25%

Added order size input

Added show/hide strat signals. Still lights the bars green/red. Make sure your bar color setting in tv is set to a transparent color so you can see the bright reds and greens.

Added a couple lines of code that fire the alert/strat if macd reverses and the corresponding 5min candle does not agree and the following candle does agree. Added an average of 1.5% winning trades.

Message me for free trial access

BTC Daily Strategy BFStrategy based on code by @CredibleHulk so thanks for that.

This is a strategy for the Daily Bitcoin chart which uses the MACD, RSI, Stochastic RSI and a moving average.

The conditions for long or short signals depend on the indicators above crossing user-defined thresholds.

Long signal = (Stochastic RSI k value is below Stochastic Sell Threshold) AND EITHER (MACD delta crosses above MACD Threshold OR RSI crosses above RSI Threshold)

Short signal = (MACD delta crosses below 0) AND EITHER (Close Price - an SMA of the ohlc4 values crosses below the DMA threshold OR Stochastic RSI k value is above Stochastic Sell Threshold)

INSTRUCTIONS

Green background = go long

Red background = go short

You can adjust stop loss values for long or short signals in settings as well as all parameters for the indicators.

fm_surfing_1This script is a realisation of a strategy that I used to know from FOREX-forums as Surfing. I wrote it first as MQL-Strategy back in 2014. Today it was remastered in pinescript. This strategy is recomended for TF 15M and above.

Below is a short description of rules

Buy Stop: close of a candel is above slow green EMA (20), RSI is greater than 55 and the rolling mean of RSI with period 10 is under RSI itself.

Sell Stop: vice-versa, slow red EMA(20) is used for the signal, as RSI lower band is used 45 value.

Exit rules: rolling mean of RSI crosses the RSI itself.Trailing stop is used as well as take profit.

What is not decripted are to fast EMA(10) which had to be used as the basis for calculating trailing stop, what is currently a task for the future optimization.

Trend Scalping Strategy - ForexHi all,

I have created the attached strategy for my own use primarily but thought I would share it as my experience to date is that it is profitable in particular circumstances, so thought I would open this out to the community to see if it can be successfully applied on any other pairs and timeframes.

I have protected the source code at this time - mainly because it needs massive tidying up! If I ever get time to do this then I will

The concept of the strategy is based upon the slingshot method - the strategy fundamentally does the following:

- Tests each candle for a new short term trend based upon EMAs

- If there is a new trend, check the RSI and ensure it isnt above the upper RSI threshold (for long positions) and below the lower RSI threshold (for short positions)

- If it passes the RSI check, entry is valid and draws a bar on the chart to show the opening entry position, stop loss position, take profit 1 and take profit 2 positions.

I have backtested this across 28 pairs on the M15 timeframe, comprising of a total of 140,000 candles (35,000 hours of trading). Across this period, 18 of the 28 pairs I looked at were profitable, with overall significant profit if live traded across the 28.

I have live tested 5 pairs on the same timeframe:

- GBPJPY

- GBPUSD

- GBPEUR

- CADJPY

- EURJPY

These pairs have to date given a rough ROR (Return on Risk) position of approx 60% average per trade.

All of the above has been done with the following inputs:

- RSI Upper - 68

- RSI Lower - 32

- Stop Loss - 0.0015

- TP1 - 0.002

- TP2 - 0.004

The SL and TPs are based on a decimal entry of a percentage movement - i.e. the Stop loss above reflects a 0.15% movement, etc etc. Obviously if this were to be tested on longer time frames it is likely that these would need to be larger figures.

I have also tested this live with great success on the S&P 500 and the FTSE, with the following settings:

Indicator Timeframe TP1 TP2 SL Upper Lower

FTSE M5 0.0015 0.004 0.001 70 30

SPX M5 0.0015 0.004 0.001 75 35

Three key notes on trading this below - THESE ARE VERY IMPORTANT!

- This is NOT a high strike rate strategy. Strike rate on profitable pairs is between approx 45 and 55% (although I have seen as low as 35% and still seen significant profit). This has two natural conclusions - risk management is VITAL (I risk 0.5% on each trade, but this may in fact be high for this strategy), and be prepared for potentially significant drawdowns. I have seen certainly drawdowns of 20 consecutive losing trades (counting TP1 and TP2 as 2 trades) and probably longer, which obviously means drawdowns of 10% or greater. The other thing to bear in mind is that with this kind of strike rate, you shouldnt be setting TP1 at a 1:1 risk reward or lower.

- Take Profit 1 is easy - straight Stop and Limit orders. Take Profit 2 is a trailing stop with a start point of the limit for TP1, with then a trailing stop of this distance. This means that should you win on TP1, TP2 is a risk free trade but also trails in for profit if TP2 isnt reached (which it normally isnt). DO NOT set TP2 as a standard stop and limit, this rapidly makes this strategy unprofitable. The point here is that if you reach TP1 you are in some form of trend where you want to capture as much profit as you can.

- Do not enter a trade mid candle. The strategy is based upon the close of the trending candle not the "live" price during this candle, so no need to rush into a trade. If you enter mid candle you will find more often than not that the indicator wasnt for a valid trade by the candle close.

Also, standard disclaimer - past performance is no guarantee of future performance, and if you choose to use this strategy/indicator you do so 100% at your own risk. As a minimum, pick your pairs carefully - I have found particular unprofitability with this strategy with the AUD and NZD pairs so I have ruled these out completely at present, although with different timeframes and inputs these may of course be profitable.

I hope this is helpful for someone...I'd welcome any feedback or other setups where this is profitable.

Moving forward, I want to do some more work on this strategy to rule out some of the more negative trades, and I primarily intend to do this using pivots - however this will be an as and when I get chance.

SB_CM_RSI_2_Strategy_Version 2.0(New: Profit booking present which is not present in the previous indicator)

The strategy is based on the indicator posted by @ChrisMoody "CM RSI-2 Strategy Lower Indicator" which is based on "Larry Connors RSI-2 Strategy - Lower RSI"

In this strategy, the longs are placed when a green color is encountered in the rsi in the previous candle and short when the red color is encountered in the rsi.

Although the profits are booked when the rsi crossover the 10 level mark or crossunder the 90 level mark.

Just message in the script if you have any different idea regarding this indicator.

For the original indicator you can refer to :

For Tips to continue :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Trio Strategy w EMA Timing Gate, Early Flip, Clouds and Cross AlMomentum Trio Strategy w EMA Timing Gate, Early Flip, Clouds and Cross Alerts

Short title: Trio EMA Strategy

Concept and Originality

This strategy merges three momentum systems – StochRSI, RSI EMA, and MACD – into one coordinated Trio.

It triggers possible entries only (no exits) when all three align within user-defined windows, with an EMA timing gate for precision and an optional early flip feature if the EMA crosses first.

Optional cooldown and filters reduce false signals.

It also shows green and purple markers when all three momentum indicators cross together, and provides alert notifications on every individual and trio crossover event.

StochRSI-based clouds highlight overbought and oversold areas for quick visual context.

Each part has a defined role:

Trio alignment ensures multi-indicator confirmation.

EMA gate refines timing and enables early trend flips.

Cooldown reduces overtrading.

Filters check price, trend, and volume quality.

Clouds visualize momentum extremes.

Markers show where the Trio crosses.

Alerts notify on all key momentum events.

How It Works

Trio confirmation (core):

StochRSI – percent K and D cross within stochGroupWindow.

RSI – RSI crossing its EMA.

MACD – line crossing signal within macdGroupWindow.

When all three cross up, a green marker appears.

When all three cross down, a purple marker appears.

These mark potential entry points only. Exits are not included.

EMA timing gate:

EMA(5) and EMA(9) define short-term trend.

Longs: EMA(5) greater than EMA(9).

Shorts: EMA(5) less than EMA(9).

Early Flip: when EMA crosses before the trio, a one-time flip can trigger after the chosen cooldown.

Cooldown prevents multiple entries in choppy markets.

Filters include:

Price Filter – restricts entries relative to EMA.

Trend Filter – aligns trades with a longer EMA.

Volume Filter – checks for rising volume.

Overbought and Oversold Clouds:

Red cloud when StochRSI is greater or equal to 80 (overbought).

Green cloud when StochRSI is less or equal to 20 (oversold).

Clouds are for context only, not trade signals.

Alerts trigger on every Trio signal and each individual crossover for StochRSI, RSI, and MACD.

Inputs You Can Tune

RSI, StochRSI, and MACD periods and windows.

EMA gate lengths.

Early-flip toggle and cooldown.

Trio cooldowns.

Filters for price, trend, and volume.

Marker visibility (green and purple).

Overbought or oversold cloud display.

Alert toggles for all cross types.

How To Use

1. Apply to any liquid market such as stocks, crypto, or forex.

2. Choose timeframe.

3. Keep default settings first, then fine-tune windows or cooldowns.

4. Use clouds and markers for entry guidance only. Exits are manual or from another strategy.

5. Enable alerts for real-time notifications of indicator and Trio crosses.

Default Properties Used for Publication (Backtest Transparency)

Initial capital: 100,000 USD – necessary for stock testing so one percent sizing produces realistic order size.

Order size: one percent of equity per trade to keep risk small.

Commission: 0.10 percent per side, realistic for brokers and exchanges.

Slippage: 0.05 percent, equal to roughly one to two ticks on stocks.

Pyramiding: 0.

Execution: on close.

Sample dataset: at least 100 trades across multiple timeframes and markets.

The higher initial capital ensures valid fills for stock testing, while risk stays proportional since position size is percentage based.

Why These Components Work Together

Trio confluence confirms momentum alignment.

EMA gate refines entry timing and allows early reversals.

Cooldown and filters reduce false triggers.

Markers confirm when all three indicators cross together.

Clouds and alerts improve awareness and reaction speed.

The result is a robust entry-only framework that adapts to many markets.

Notes and Limitations

Focused on entry detection only. Exits are manual or external.

For educational use only, not financial advice.

Always test with realistic slippage, fees, and several symbols.

Past results do not guarantee future performance.

Attribution

All logic and structure are original to this publication.

Common Pine functions follow official Pine documentation.

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

XqKtPvRwSd-StrategyTradingView Pine Script Suite (v4.0) — General Overview

Purpose

A modular indicator and strategy suite designed for crypto markets, focusing on trend detection, momentum, range visualization, and signal generation. The suite supports popular symbols (BTC, ETH, BNB, SOL, DOGE) and offers flexible visualization and alert options.

Main Components

- v4.0-indicator: Multi-signal display for monitoring market conditions and trend bias.

- v4.0-watch-15m: Watchlist-style indicator with symbol-aware auto-tuning and optional chart timeframe adaptation.

- v4.0-strategy: Backtestable strategy using a unified, SuperTrend-based trend determination for entries/exits.

- v4.0-range: Range and structure visualization with dynamic lines, zones, and basic breakout cues.

- Two Poles.pinescript and fengzi/Two Poles Trend: Low-lag trend and smoothing filters for stability.

- supertrend.pinescript: SuperTrend variations used across the suite for direction and stops.

- fengzi utilities:

- Hann Window FIR Filter: Denoising and smoothing to reduce noise without excessive lag.

- Heatmap + Hann Resonance: Visual heat/energy mapping for momentum and resonance cues.

- Heatmap Trailing Stop with Breakouts: Trailing stop framework with breakout detection.

- Additional modules: super Z, AI JX, v3.2, and 4.0.pinescript (combined or experimental entries).

Key Features

- Unified Trend Logic: Strategy and visual components rely on a consistent SuperTrend-based direction model, improving clarity and consistency.

- Adaptive Timeframe: Option to use the chart’s timeframe; parameters scale from a 15m baseline to maintain relative behavior.

- Symbol Auto-Tuning: Default parameter sets are tailored for common crypto symbols; manual overrides are available.

- RSI Top/Bottom Hints: Optional dynamic cues for potential peaks in uptrends and troughs in downtrends; can contribute to scoring and alerts.

- Visual Customization: Configurable markers (arrows, dots, crosses), colors, line widths, and subtle background highlighting.

- Scoring and Clustering: Combines checks into a simplified score and clusters signals to reduce noise.

- Alerts: Supports TradingView alerts for entries, exits, and RSI hints.

- Compatibility: Designed to compile across common Pine versions and avoid local-scope plotting issues.

Basic Usage

- Add the indicator or strategy to your chart depending on your goal (monitoring vs. backtesting).

- Choose to follow the chart’s timeframe or set a working timeframe manually.

- Keep symbol auto-tuning enabled for a balanced default, or adjust parameters to match your preferences.

- Toggle optional modules (RSI hints, scoring contribution, visualization) based on your needs.

- For strategies, run backtests across your target period and review performance metrics (win rate, drawdown, and trade frequency).

Configuration Guidelines

- For earlier entries: lower SuperTrend period or multiplier; relax RSI thresholds.

- For more conservative behavior: increase SuperTrend period or multiplier; tighten thresholds; use stricter RSI logic.

- For cleaner signals: rely on the unified trend and consider limiting trades during extreme volatility or illiquid sessions.

Outputs

- Trend markers and lines indicating bullish/bearish bias and reversals.

- Range drawings with dynamic line coordinates, zones, and visual cues for consolidations and breakouts.

- Optional multi-timeframe dashboard-style summaries where applicable.

Extensibility

- Parameters and defaults can be extended for additional symbols and styles.

- Optional weighting or neutrality rules can be added to trend logic if you prefer stricter confirmation.

- Additional filters (volatility, session, volume) can be integrated to refine entries and exits.

Notes

- Not financial advice; backtest thoroughly before using any strategy live.

- Performance and signal quality vary by symbol, timeframe, and market conditions; adjust parameters as needed.

- Pine version differences may require minor adjustments; keep your environment up to date.

Hilly's Advanced Crypto Scalping Strategy - 5 Min ChartTo determine the "best" input parameters for the Advanced Crypto Scalping Strategy on a 5-minute chart, we need to consider the goals of optimizing for profitability, minimizing false signals, and adapting to the volatile nature of cryptocurrencies. The default parameters in the script are a starting point, but the optimal values depend on the specific cryptocurrency pair, market conditions, and your risk tolerance. Below, I'll provide recommended input values based on common practices in crypto scalping, along with reasoning for each parameter. I’ll also suggest how to fine-tune them using TradingView’s backtesting and optimization tools.

Recommended Input Parameters

These values are tailored for a 5-minute chart for liquid cryptocurrencies like BTC/USD or ETH/USD on exchanges like Binance or Coinbase. They aim to balance signal frequency and accuracy for day trading.

Fast EMA Length (emaFastLen): 9

Reasoning: A 9-period EMA is commonly used in scalping to capture short-term price movements while remaining sensitive to recent price action. It reacts faster than the default 10, aligning with the 5-minute timeframe.

Slow EMA Length (emaSlowLen): 21

Reasoning: A 21-period EMA provides a good balance for identifying the broader trend on a 5-minute chart. It’s slightly longer than the default 20 to reduce noise while confirming the trend direction.

RSI Length (rsiLen): 14

Reasoning: The default 14-period RSI is a standard choice for momentum analysis. It works well for detecting overbought/oversold conditions without being too sensitive on short timeframes.

RSI Overbought (rsiOverbought): 75

Reasoning: Raising the overbought threshold to 75 (from 70) reduces false sell signals in strong bullish trends, which are common in crypto markets.

RSI Oversold (rsiOversold): 25

Reasoning: Lowering the oversold threshold to 25 (from 30) filters out weaker buy signals, ensuring entries occur during stronger reversals.

MACD Fast Length (macdFast): 12

Reasoning: The default 12-period fast EMA for MACD is effective for capturing short-term momentum shifts in crypto, aligning with scalping goals.

MACD Slow Length (macdSlow): 26

Reasoning: The default 26-period slow EMA is a standard setting that works well for confirming momentum trends without lagging too much.

MACD Signal Smoothing (macdSignal): 9

Reasoning: The default 9-period signal line is widely used and provides a good balance for smoothing MACD crossovers on a 5-minute chart.

Bollinger Bands Length (bbLen): 20

Reasoning: The default 20-period Bollinger Bands are effective for identifying volatility breakouts, which are key for scalping in crypto markets.

Bollinger Bands Multiplier (bbMult): 2.0

Reasoning: A 2.0 multiplier is standard and captures most price action within the bands. Increasing it to 2.5 could reduce signals but improve accuracy in highly volatile markets.

Stop Loss % (slPerc): 0.8%

Reasoning: A tighter stop loss of 0.8% (from 1.0%) suits the high volatility of crypto, helping to limit losses on false breakouts while keeping risk manageable.

Take Profit % (tpPerc): 1.5%

Reasoning: A 1.5% take-profit target (from 2.0%) aligns with scalping’s goal of capturing small, frequent gains. Crypto markets often see quick reversals, so a smaller target increases the likelihood of hitting profits.

Use Candlestick Patterns (useCandlePatterns): True

Reasoning: Enabling candlestick patterns (e.g., engulfing, hammer) adds confirmation to signals, reducing false entries in choppy markets.

Use Volume Filter (useVolumeFilter): True

Reasoning: The volume filter ensures signals occur during high-volume breakouts, which are more likely to sustain in crypto markets.

Signal Arrow Size (signalSize): 2.0

Reasoning: Increasing the arrow size to 2.0 (from 1.5) makes buy/sell signals more visible on the chart, especially on smaller screens or volatile price action.

Background Highlight Transparency (bgTransparency): 85

Reasoning: A slightly higher transparency (85 from 80) keeps the background highlights subtle but visible, avoiding chart clutter.

How to Apply These Parameters

Copy the Script: Use the Pine Script provided in the previous response.

Paste in TradingView: Open TradingView, go to the Pine Editor, paste the code, and click "Add to Chart."

Set Parameters: In the strategy settings, manually input the recommended values above or adjust them via the input fields.

Test on a 5-Minute Chart: Apply the strategy to a liquid crypto pair (e.g., BTC/USDT, ETH/USDT) on a 5-minute chart.

Fine-Tuning for Optimal Performance

To find the absolute best parameters for your specific trading pair and market conditions, use TradingView’s Strategy Tester and optimization features:

Backtesting:

Run the strategy on historical data for your chosen pair (e.g., BTC/USDT on Binance).

Check metrics like Net Profit, Profit Factor, Win Rate, and Max Drawdown in the Strategy Tester.

Focus on a sample period of at least 1–3 months to capture various market conditions (bull, bear, sideways).

Parameter Optimization:

In the Strategy Tester, click the settings gear next to the strategy name.

Enable optimization for key inputs like emaFastLen (test range: 7–12), emaSlowLen (15–25), slPerc (0.5–1.5), and tpPerc (1.0–3.0).

Run the optimization to find the combination with the highest net profit or best Sharpe ratio, but avoid over-optimization (curve-fitting) by testing on out-of-sample data.

Market-Specific Adjustments:

Volatile Pairs (e.g., DOGE/USDT): Use tighter stop losses (e.g., 0.5–0.7%) and smaller take-profit targets (e.g., 1.0–1.2%) to account for rapid price swings.

Stable Pairs (e.g., BTC/USDT): Slightly wider stop losses (e.g., 1.0–1.2%) and take-profit targets (e.g., 1.8–2.5%) may work better.

Trending Markets: Increase emaSlowLen (e.g., to 25–30) to follow stronger trends.

Choppy Markets: Tighten bbMult (e.g., to 1.8) and lower rsiOverbought/rsiOversold (e.g., to 70/30) to filter noise.

Forward Testing:

After backtesting, run the strategy in real-time on a demo account for 1–2 weeks to validate performance under current market conditions.

Important Notes

No Universal "Best" Numbers: Optimal parameters vary by crypto pair, exchange, and market conditions (e.g., bull vs. bear market). The suggested values are a starting point based on common scalping practices.

Risk Management: Never risk more than 1–2% of your account per trade. Adjust position sizing in TradingView’s strategy settings to align with your risk tolerance.

Market Volatility: Crypto markets are highly volatile. Test the strategy on your specific pair and adjust parameters if signals are too frequent or too rare.

Not Financial Advice: This is an educational tool. Backtest thoroughly and use a demo account before trading with real funds.

If you want me to generate a chart showing backtest performance for specific parameters or to tweak the script further (e.g., adding more indicators or adjusting signal logic), let me know!can you add clear buy ans sell signs above the candles in this codeTo add clear buy and sell signals above the candles in the provided Pine Script, I'll modify the existing code to include prominent text labels directly above (for sell signals) and below (for buy signals) the candles. These labels will be larger, color-coded, and positioned to avoid clutter, ensuring they are easily visible on the chart. The core strategy logic (EMA, RSI, MACD, Bollinger Bands, candlestick patterns, and volume filter) will remain unchanged, and I'll reuse the same artifact_id since this is an update to the previous script.AdvancedCryptoScalpingStrategy.pinex-pine

Strategy Designer

**Strategy Designer**

This script is a highly modular, multi-indicator strategy framework that allows users to enable or disable a wide range of signals for precision trading control. Key components include:

* **AlphaTrend**: A dynamic trailing filter built using ATR volatility combined with directional input from RSI or MFI. It helps define bullish or bearish regimes more responsively than fixed moving averages.

* **Inverse Fisher Transformed Indicators**: The script normalizes and transforms traditional oscillators (CCI, RSI, Stochastic, MFI) using the inverse Fisher transform. This boosts signal clarity by compressing values between -1 and +1, making crossovers and trend thresholds more defined.

* **Composite Indicators**: RSI + MFI and CCI + Stoch are averaged to produce smoother, noise-reduced momentum signals. These are ideal for filtering or confirming entries across multiple timeframes or asset types.

* **Volatility & Trend Filters**:

* **ATR Trend Filter**: Confirms trades only when short-term ATR exceeds its smoothed average, indicating rising volatility or breakout conditions.

* **ADX Filter**: Includes two types of filters—ADX vs its MA and ADX vs threshold—to ensure trade entries only happen during clear trend strength.

* **Moving Averages**: Multiple MA types (SMA, EMA, HMA, WMA, DEMA, TEMA, T3, VWMA) are available for crossover and trend conditions. The structure supports general trend, long-trend, and short-trend configurations independently.

* **Volume Filter**: An optional condition to confirm that volume exceeds a moving average, helping avoid trades in low-liquidity periods.

---

**Exit Logic & Risk Management**

This strategy offers powerful and flexible exit controls to suit various risk profiles:

* **Fixed TP/SL**: You can activate classic percentage-based take profit and stop loss levels.

* **ATR-Based Floating Stop**: Dynamically calculates trailing stops based on recent volatility using a smoothed ATR, offering better adaptability in trending environments.

* **Signal-Based Exits**: Includes the ability to exit trades when the original entry conditions reverse (e.g. AlphaTrend flips, Fisher crosses back, MA cross reverses, etc.).

* **Modular Exit Triggers**: Each indicator (CCI, RSI, MFI, Stoch, AlphaTrend, Composite Indicators) can independently trigger an exit based on reversal signals or loss of trend strength.

* **Multi-Layered Protection**: Combine multiple exits (e.g. ATR + AlphaTrend + RSI reversal) to minimize drawdowns and prevent false breakouts.

---

This tool is designed for advanced traders and strategy developers who want granular control over both entries and exits. Every module is toggleable, allowing for endless backtest scenarios and tailored setups to match different market conditions or asset classes. Whether you're trend-following or counter-trading reversals, this strategy adapts.

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :

- The script first calculates the ATR-based grid levels and ensures price action has sufficient volatility before allowing trades.

- An additional RSI filter is used to ensure trades are taken at ideal market conditions.

- Once a trade is executed, the script implements a trailing stop and predefined take profit to maximize gains while reducing risks.

---

Disclaimer :

Risk Warning :

This strategy is provided for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Users are advised to conduct their own due diligence and risk management before using this strategy in live trading.

The developer and publisher of this script are not responsible for any financial losses incurred by the use of this strategy. Market conditions, slippage, and execution quality can affect real-world trading outcomes.

Use this script at your own discretion and always trade responsibly.

ATM Option Selling StrategyATM Option Selling Strategy – Explained

This strategy is designed for intraday option selling based on the 9/15 EMA crossover, 50/80 MA trend filter, and RSI 50 level. It ensures that all trades are exited before market close (3:24 PM IST).

. Indicators Used:

9 EMA & 15 EMA → For short-term trend identification.

50 MA & 80 MA → To determine the overall trend.

RSI (14) → To confirm momentum (above or below 50 level).

2. Entry Conditions:

🔴 Sell ATM Call (CE) when:

Price is below 50 & 80 MA (Bearish trend).

9 EMA crosses below 15 EMA (Short-term trend turns bearish).

RSI is below 50 (Momentum confirms weakness).

🟢 Sell ATM Put (PE) when:

Price is above 50 & 80 MA (Bullish trend).

9 EMA crosses above 15 EMA (Short-term trend turns bullish).

RSI is above 50 (Momentum confirms strength).

3. Position Sizing & Risk Management:

Sell 375 quantity per trade (Lot size).

50-Point Stop Loss → If option premium moves against us by 50 points, exit.

50-Point Take Profit → If option premium moves in our favor by 50 points, book profit.

Exit all trades at 3:24 PM IST → No overnight positions.

4. Exit Conditions:

✅ Stop Loss or Take Profit Hits → Automatically exits based on a 50-point move.

✅ Time-Based Exit at 3:24 PM → Ensures no open positions at market close.

Why This Works?

✔ Trend Confirmation → 50/80 MA ensures we only sell options in the direction of the market trend.

✔ Momentum Confirmation → RSI prevents entering weak trades.

✔ Controlled Risk → SL and TP protect against large losses.

✔ No Overnight Risk → All trades close before market close.

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

FlexATRFlexATR: A Dynamic Multi-Timeframe Trading Strategy

Overview: FlexATR is a versatile trading strategy that dynamically adapts its key parameters based on the timeframe being used. It combines technical signals from exponential moving averages (EMAs) and the Relative Strength Index (RSI) with volatility-based risk management via the Average True Range (ATR). This approach helps filter out false signals while adjusting to varying market conditions — whether you’re trading on a daily chart, intraday charts (30m, 60m, or 5m), or even on higher timeframes like the 4-hour or weekly charts.

How It Works:

Multi-Timeframe Parameter Adaptation: FlexATR is designed to automatically adjust its indicator settings depending on the timeframe:

Daily and Weekly: On higher timeframes, the strategy uses longer periods for the fast and slow EMAs and standard periods for RSI and ATR to capture more meaningful trend confirmations while minimizing noise.

Intraday (e.g., 30m, 60m, 5m, 4h): The parameters are converted from “days” into the corresponding number of bars. For instance, on a 30-minute chart, a “day” might equal 48 bars. The preset values for a 30-minute chart have been slightly reduced (e.g., a fast EMA is set at 0.35 days instead of 0.4) to improve reactivity while maintaining robust filtering.

Signal Generation:

Entry Signals: The strategy enters long positions when the fast EMA crosses above the slow EMA and the RSI is above 50, and it enters short positions when the fast EMA crosses below the slow EMA with the RSI below 50. This dual confirmation helps ensure that signals are reliable.

Risk Management: The ATR is used to compute dynamic levels for stop loss and profit target:

Stop Loss: For a long position, the stop loss is placed at Price - (ATR × Stop Loss Multiplier). For a short position, it is at Price + (ATR × Stop Loss Multiplier).

Profit Target: The profit target is similarly set using the ATR multiplied by a designated profit multiplier.