Cristina - Trading Sessions and Moving AveragesCombination of Trading Sessions and Moving Averages. You can easily edit the time frame background to give you a visual presentation of your most active trading hours or customize it to represent the different forex trading session inline with your local time.

The default moving average here is the 20, 50, 100, 200 and 250 MA. The use of moving averages could be in a (1) form of cross over to find out the dominant trend, (2) use it to find value zone or (3) use it to find dynamic support levels. It greatly depends on your trading system.

With the combination of the trading sessions and the moving averages, you could isolate the trades you will be taking inline with your active hours. Thus this is a great tool to add in terms of day trading or swing trading with the lower time frames.

在腳本中搜尋"session"

Initial Balance Monitoring PanelInitial Balance Monitoring Panel

Allows you to have an instant view of 16 Crypto pairs within a monitoring panel, monitoring Initial Balance (Asia, London, New York Stock Exchanges).

The code can easily be changed to suit the crypto pairs you are trading.

The setup of my chart would also include this indicator and the " Initial Balance Markets Time Zones - Overall Highest and Lowest " (with all IBs enabled) as shown above.

Initial Balance is based on the highest and lowest price action within the first 60 minutes of trading. Reading online this can depict which way the market can trend for the session.

The indicator has been coded for Crypto (so other symbols may not work as expected).

Though Initial Balance is based off the first 60 minutes of the trading markets opening, but Crypto is 24/7, this indicator looks at how Asia, London and New York Stock Exchanges opening trading can affect Crypto price action.

As the current Market sentiment is bullish if the price action fell below all Initial balances I would be looking at completing Technical Analysis for a long trade and to see if price action can find support from the trading sessions Initial Balance:

Please see below an example of this....

IOTAUSDT signaled red (that it had dropped below all IBs) but then found support and moved on up.

Also a similar example as above for BTCUSDT....

If the signal is green do your technical analysis, but as shown below once the highest Initial Balance has been broken price can increase.

LINKLUSDT

I would like to say thanks to AnyDozer from StackOverFlow for helping me get my idea onto the charts and wugamlo for allowing me to use some of his panel code.

CM_Forex-Sessions-HighLowDay_V1Este indicador presenta las sesiones forex de Asia Londres y Nueva York junto a los altos y bajos del precio durante la jornada, se puede complementar con el indicador CM_Forex-AsiaSession-8H_V1 para ver los segmentos de 8 horas de la sesión de Asia.

This indicator presents the forex sessions of Asia London and New York along with the highs and lows of the price during the day, it can be complemented with the indicator CM_Forex-AsiaSession-8H_V1 to see the 8-hour segments of the Asian session.

Hedge Fund Session Ranges [GMT+2] - Multi-Timezone TrackingOverview

This professional-grade tool is designed for institutional-style trading, specifically focusing on the Liquidity Cycles of the global markets. It allows traders to visualize key trading windows (Asia, Europe, and US) with precision, using a fixed GMT+2 offset—ideal for traders aligned with Middle Eastern or Eastern European timezones.

Key Features

Triple Session Tracking: Includes pre-defined windows for Asia, London Morning, and NY Afternoon.

Dynamic Box Scaling: Automatically calculates and visualizes the High/Low range of each session in real-time.

GMT+2 Optimization: Built-in timezone handling to ensure your charts align perfectly with local bank hours.

Clean Visuals: Minimalist design to avoid chart clutter, allowing for clear price action analysis.

Why Trade Sessions?

Institutional volume isn't distributed evenly throughout the day. By identifying the Asian Range (01:00-06:00), the London Open (10:00-12:00), and the NY Reversal/Trend (16:30-18:30), traders can identify "Liquidity Grabs" and "Expansion Phases" more effectively.

EURCHF Pro: 1H Trend + Prob + Sessions + Timer + SwingsEURCHF – Table Explanation (Calm & Precision)

EURCHF is a slow and controlled pair.

The table focuses on patience and precision.

🔹 Market Trend (1H)

If the trend is not clear → no trade

EURCHF dislikes choppy markets

👉 The table helps you stay out of bad conditions.

🔹 Session

Best time:

London session only

👉 LOW session = stay out.

🔹 Candle Time Left

Less critical than other pairs.

Still useful for final confirmation

👉 No need to rush.

🔹 Buy / Sell Probability

Best results at 60%+

Fewer trades, higher quality

👉 One clean trade is better than many weak ones.

🔹 RSI / Volume

RSI moves slowly

Weak volume = low continuation

🟢 Result:

A precision-focused table for patient traders.

Chiefs sessions 4This is just an indicator marking the most recent asian session and london session highs and lows, and also marks off previous days high and lows in white. Blue is asian session and red is london. This indicator resets every day.

Moving Average Shift WaveTrend StrategyMoving Average Shift WaveTrend Strategy

🧭 Overview

The Moving Average Shift WaveTrend Strategy is a trend-following and momentum-based trading system designed to be overlayed on TradingView charts. It executes trades based on the confluence of multiple technical conditions—volatility, session timing, trend direction, and oscillator momentum—to deliver logical and systematic trade entries and exits.

🎯 Strategy Objectives

Enter trades aligned with the prevailing long-term trend

Exit trades on confirmed momentum reversals

Avoid false signals using session timing and volatility filters

Apply structured risk management with automatic TP, SL, and trailing stops

⚙️ Key Features

Selectable MA types: SMA, EMA, SMMA (RMA), WMA, VWMA

Dual-filter logic using a custom oscillator and moving averages

Session and volatility filters to eliminate low-quality setups

Trailing stop, configurable Take Profit / Stop Loss logic

“In-wave flag” prevents overtrading within the same trend wave

Visual clarity with color-shifting candles and entry/exit markers

📈 Trading Rules

✅ Long Entry Conditions:

Price is above the selected MA

Oscillator is positive and rising

200-period EMA indicates an uptrend

ATR exceeds its median value (sufficient volatility)

Entry occurs between 09:00–17:00 (exchange time)

Not currently in an active wave

🔻 Short Entry Conditions:

Price is below the selected MA

Oscillator is negative and falling

200-period EMA indicates a downtrend

All other long-entry conditions are inverted

❌ Exit Conditions:

Take Profit or Stop Loss is hit

Opposing signals from oscillator and MA

Trailing stop is triggered

🛡️ Risk Management Parameters

Pair: ETH/USD

Timeframe: 4H

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 2% of account equity (adjustable)

Total Trades: 224

Backtest Period: May 24, 2016 — April 7, 2025

Note: Risk parameters are fully customizable to suit your trading style and broker conditions.

🔧 Trading Parameters & Filters

Time Filter: Trades allowed only between 09:00–17:00 (exchange time)

Volatility Filter: ATR must be above its median value

Trend Filter: Long-term 200-period EMA

📊 Technical Settings

Moving Average

Type: SMA

Length: 40

Source: hl2

Oscillator

Length: 15

Threshold: 0.5

Risk Management

Take Profit: 1.5%

Stop Loss: 1.0%

Trailing Stop: 1.0%

👁️ Visual Support

MA and oscillator color changes indicate directional bias

Clear chart markers show entry and exit points

Trailing stops and risk controls are transparently managed

🚀 Strategy Improvements & Uniqueness

In-wave flag avoids repeated entries within the same trend phase

Filtering based on time, volatility, and trend ensures higher-quality trades

Dynamic high/low tracking allows precise trailing stop placement

Fully rule-based execution reduces emotional decision-making

💡 Inspirations & Attribution

This strategy is inspired by the excellent concept from:

ChartPrime – “Moving Average Shift”

It expands on the original idea with advanced trade filters and trailing logic.

Source reference:

📌 Summary

The Moving Average Shift WaveTrend Strategy offers a rule-based, reliable approach to trend trading. By combining trend and momentum filters with robust risk controls, it provides a consistent framework suitable for various market conditions and trading styles.

⚠️ Disclaimer

This script is for educational purposes only. Trading involves risk. Always use proper backtesting and risk evaluation before applying in live markets.

All Forex Sessions (SAST Accurate) + LabelsFor traders in South Africa

Uses timestamp("Africa/Johannesburg", ...) — this locks the session window to true SAST time

The session now perfectly aligns from 14:00 to 18:00 local time no matter what time zone your TradingView chart is in

Also shows start and end vertical lines only when the session opens and closes

TimeFilterLibrary "TimeFilter"

provides utilities for dates and times

inSession(session, timezone, period)

Parameters:

session (simple string)

timezone (simple string)

period (simple string)

Returns: bool inSession Whether the current time is within the defined time session

inDateRange(startDate, endDate)

Parameters:

startDate (int)

endDate (int)

Returns: bool inRange Whether the current time is within the defined date range

isWeekDay(weekDay, timezone)

Parameters:

weekDay (int)

timezone (simple string)

Returns: bool isWeekDay Whether the provided day is the current day of the week

inWeek(useMon, useTue, useWed, useThu, useFri, useSat, useSun, timezone)

Parameters:

useMon (bool)

useTue (bool)

useWed (bool)

useThu (bool)

useFri (bool)

useSat (bool)

useSun (bool)

timezone (simple string)

Returns: bool inWeek Whether the current time is one of the defined days

filter(useRange, useSession, useWeek, inRange, inSession, inWeek)

Parameters:

useRange (bool)

useSession (bool)

useWeek (bool)

inRange (bool)

inSession (bool)

inWeek (bool)

Returns: bool filter Whether the filter matches or not

VWAP Suite, Session Cloud RevOverview

The VWAP Suite with Standard Deviation Strategy is a comprehensive indicator designed to help traders make informed trading decisions based on the Volume Weighted Average Price (VWAP) and its associated standard deviation bands. This indicator provides multiple VWAP calculations for different timeframes (Session, Day, Week, Month) and incorporates standard deviation bands to identify potential trade entry and exit points.

Components

VWAP Calculation:

Session VWAP: VWAP calculated based on the current trading session.

Day VWAP: VWAP calculated for the daily timeframe.

Week VWAP: VWAP calculated for the weekly timeframe.

Month VWAP: VWAP calculated for the monthly timeframe.

Standard Deviation Bands:

The indicator includes three standard deviation bands (StDev 1, StDev 2, and StDev 3) around the VWAP. These bands help identify the dispersion of price from the VWAP, providing insight into potential overbought or oversold conditions.

Additional VWAP Lines:

VWAP 2: An additional VWAP line with a customizable timeframe (Day, Week, Month).

VWAP 3: Another VWAP line for further analysis with a customizable timeframe (Day, Week, Month).

Strategy Description

The primary strategy implemented in this indicator revolves around the second standard deviation band (StDev 2). The key aspects of this strategy include:

Entry Points:

Long Entry: Consider entering a long position when the price moves below the lower StDev 2 band and then starts to revert back towards the VWAP. This indicates a potential oversold condition.

Short Entry: Consider entering a short position when the price moves above the upper StDev 2 band and then starts to revert back towards the VWAP. This indicates a potential overbought condition.

Exit Points:

Long Exit: Exit the long position when the price moves back up to the VWAP or the upper StDev 1 band, indicating a normalization of the price.

Short Exit: Exit the short position when the price moves back down to the VWAP or the lower StDev 1 band, indicating a normalization of the price.

Risk Management:

Set stop-loss levels slightly beyond the StDev 3 bands to protect against significant adverse price movements.

Use trailing stops to lock in profits as the price moves favorably.

Customization

The VWAP Suite allows for extensive customization, enabling traders to adjust the following settings:

VWAP Mode: Select the timeframe for the primary VWAP calculation (Session, Day, Week, Month).

Line Widths and Colors: Customize the line widths and colors for VWAP and standard deviation bands.

Fill Opacity: Adjust the opacity of the fill between standard deviation bands for better visual clarity.

Additional VWAPs: Enable and customize additional VWAP lines (VWAP 2 and VWAP 3) for further analysis.

CME Gap Detector [CryptoSea]The CME Gap Indicator , is a tool designed to identify and visualize potential price gaps in the cryptocurrency market, particularly focusing on gaps that occur during the weekend trading sessions. By highlighting these gaps, traders can gain insights into potential market movements and anticipate price behavior.

Key Features

Gap Identification: The indicator identifies gaps in price between the Friday close and the subsequent opening price on Monday. It plots these gaps on the chart, allowing traders to easily visualize and analyze their significance.

Weekend Price Comparison: It compares the closing price on Friday with the opening price on Monday to determine whether a gap exists and its magnitude.

Customizable Visualization: Traders have the option to customize the visualization of the gaps, including the color scheme for better clarity and visibility on the chart.

Neutral Candle Color Option: Users can choose to display neutral candle colors, enhancing the readability of the chart and reducing visual clutter.

How it Works

Data Fetching and Calculation: The indicator fetches the daily close price and calculates whether a gap exists between the Friday close and the subsequent Monday opening price.

Plotting: It plots the current price and the previous Friday's close on the chart, making it easy for traders to compare and analyze.

Gradient Fill: The indicator incorporates a gradient fill feature to visually represent the magnitude of the gap, providing additional insights into market sentiment.

Weekend Line Logic: It includes logic to identify Sunday bars and mark them on the chart, aiding traders in distinguishing weekend trading sessions.

Application

Gap Trading Strategy: Traders can use the identified gaps as potential entry or exit points in their trading strategies, considering the tendency of price to fill gaps over time.

Market Sentiment Analysis: Analyzing the presence and size of weekend gaps can provide valuable insights into market sentiment and participant behavior.

Risk Management: Understanding the existence and significance of gaps can help traders manage their risk exposure and make informed decisions.

The CME Gap indicator offers traders a valuable tool for analyzing weekend price gaps in the cryptocurrency market, empowering them to make informed trading decisions and capitalize on market opportunities.

Intraday trading period indicatorI have created this indicator because I was in a need of simple indication of personal session time for my backtesting while practicing intraday Futures trading.

How it works:

1. Define your timezone.

2. Set Trading session start/end time.

3. Choose the colour you want to see your intraday session in.

Actual result: Your selected session is displayed with selected colour and within selected time period. Your are good to go.

It is not perfect for sure but it does what it needs to do and I think it is awesome.

Hope it will be useful for you and let the Profit be with you!

The Only EURUSD Trading Strategy You Need - KaspricciThe Only EURUSD Trading Strategy You Need

I got the idea to this strategy from a youtube video uploaded by Trade Beta. It is designed to capture the early market move of major forex pair EURUSD at beginning of New York Stock Exchange (13:30 GMT). Trade Beta tested his strategy on the 5 minute chart. I have set all parameters to same values as shown in the video.

The strategy creates two pending orders at the recent swing high and low. Once the first pending order entered, the remaining one is cancelled. Latest at the end of market session all pending orders are cancelled and all open trade are closed as well.

In rare case that price at session opening is above swing high, only a pending sell stop order is created at swing high price. And in case price is below swing low, a pending buy stop order is created.

Settings

Trading Time - default: New York Stock Exchange opening hours. Pending orders are created at the close of the first candle within the session.

Swing High Source / Bars - default: High / 5 bars. Used to find the latest swing high within a range of 5 bars left and right. Price is used for buy stop order.

Swing Low Source / Bars - default: Low / 5 bars. Used to find the latest swing low within a range of 5 bars left and right. Price is used for sell stop order.

Stop Loss Type - default: ATR. You can switch between stop loss calculation based on Average True Range value or fixed value.

ATR Length / Factor / TP Ratio - default: 14 / 2.0 / 2.0. Used to calculate the Stop Loss as ATR * Factor and Take Profit as Stop Loss * TP Ratio.

FIX Stop Loss / Take Profit - default: 10 pips / 20 pips. In case you select Stop Loss Type = FIX, these value swill be used.

This strategy is for educational purposes only! It is not meant to be a financial advice.

[FriZz]Watermark -- Watermark by FriZz | FrizLabz --

Lets you Customize a watermark how ever you would like

There are 4 Textboxes in the settings window 2 for your inputs

There's 1 with instructions/examples and 1 with Special Characters (there are tons more online)

-- The options you can type into Textbox 1 and 2 --

- Volume

- Open

- Close

- High

- Low

- Ticker [ Chart ticker ]

- Ticker2 [ Optional 2nd ticker that can be set in the settings will also display close ]

- TF

- Day

- Date

- Time

- Session

- SessionTime

-- Important --

These options need to be spelled and Case matched correctly or it will simply just display the word

You can add anything around a word or between two words you would like

If you want a new line simply press [ ENTER/RETURN ] and continue

-- Tooltip --

Tooltip appears when you mouse over the watermark

There are options to change the session times if you need too

The Sessions will be listed on the tooltip with Session times

I think that pretty much covers most of it if you have any questions or suggestions on this or anything else I've made

or if I missed a bug.. feel free to comment or DM me

Enjoy! - FriZz

MILK (My Intraday Lazy Kit)I made this script to group information considered useful in forex day trading, of course it can be used on crypto or other markets.

First of all, feel free to suggest any improvement/new feature you would consider interesting for such an use. This is not especially a final version and I'm sure other relevant information can be added in this tool.

Current features are the following

An international clock showing time and session status (open/closed) for 5 different cities. You can modify it in parameters.

Drawings of previous days/weeks open/high/low/close prices, which will be often used as supports and resistances zones.

The Clock shows

City

Time (with a bgcolor corresponding to the "period" of the day (Morning, Afternoon, Evening, Night)

Session status (Cyan when the corresponding session is open, blue when it's closed)

Price levels names are

YTD-H : Yesterday's high

YTD-L : Yesterday's low

YTD-C : Yesterday's close

YTD-O : Yesterday's open

PWH : Previous week high

PWL : Previous week low

PWO : Previous week open

PWC : Previous week close

Levels width and colors can be modified.

You can also enable/disable the clock, and daily or weekly levels in the options panel.

Nothing more to say for now, I mainly integrated information I like to have, but I'll probably add new features in it if I get some.

Triple VWAP for FOREX SessionsThis script runs on my previous script Masterwork VWAP .

►It uses regular built-in VWAP improved to avoid weird connecting of the line with its yesterday's value.

►It starts a new VWAP when London session opens . You can select to end it next morning or when the session is about to close.

►It starts a new VWAP when New York session opens . You can select to end it next morning or when the session is about to close.

►You can select intelligent_enabler function to plot the VWAPs on your chart when viewing low timeframe charts (1m, 5m, 15m, 30m)

Kill ZonesThe Indicator is supposed to mark the first two hours of the:

Open session of Tokyo stocks market

Open session of the London stocks market

Open session of the NY stocks market

Go to the indicator's settings and set the open hours for your timezone.

Use on 1H timeframe.

Trading Sessions with 15 minute ORBA working copy of the original Tradingview trading sessions indicator with the addition of horizontal lines marking the 15 minute opening range for your ORB strategy. The lines reset with each session start.

Monks - SessionsScript that shows the sessions of the market by coloring the candles of each market session as defined by the user. It also shows inside bars, a timer on the left of the screen, it shows if the previous high time frame candle has been gained (1D,1W or 1M). It also shows the days of the week as vertical lines

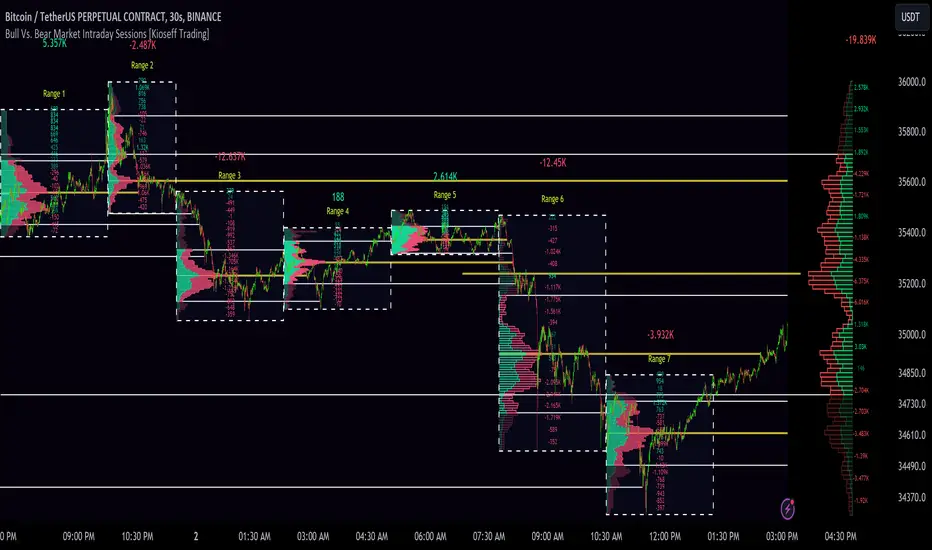

10x Bull Vs. Bear VP Intraday Sessions [Kioseff Trading]Hello!

This script "10x Bull Vs. Bear VP Intraday Sessions" lets the user configure up to 10 session ranges for Bull Vs. Bear volume profiles!

Features

Up To 10 Fixed Ranges!

Volume Profile Anchored to Fixed Range

Delta Ladder Anchored to Range

Bull vs Bear Profiles!

Standard Poc and Value Area Lines, in Addition to Separated POCs and Value Area Lines for Bull Profiles and Bear Profiles

Configurable Value Area Target

Up to 2000 Profile Rows per Visible Range

Stylistic Options for Profiles

This script generates Bull vs. Bear volume profiles for up to 10 fixed ranges!

Up to 2000 volume profile levels (price levels) Can be calculated for each profile, thanks to the new polyline feature, allowing for less aggregation / more precision of volume at price and volume delta.

Bull vs Bear Profiles

The image above shows primary functionality!

Green profiles = buying volume

Red profiles = selling volume

All colors are configurable.

Bullish & bearish POC + value areas for each fixed range are displayable!

That’s about it :D

This indicator is part of a series titled “Bull vs. Bear”.

If you have any suggestions please feel free to share!

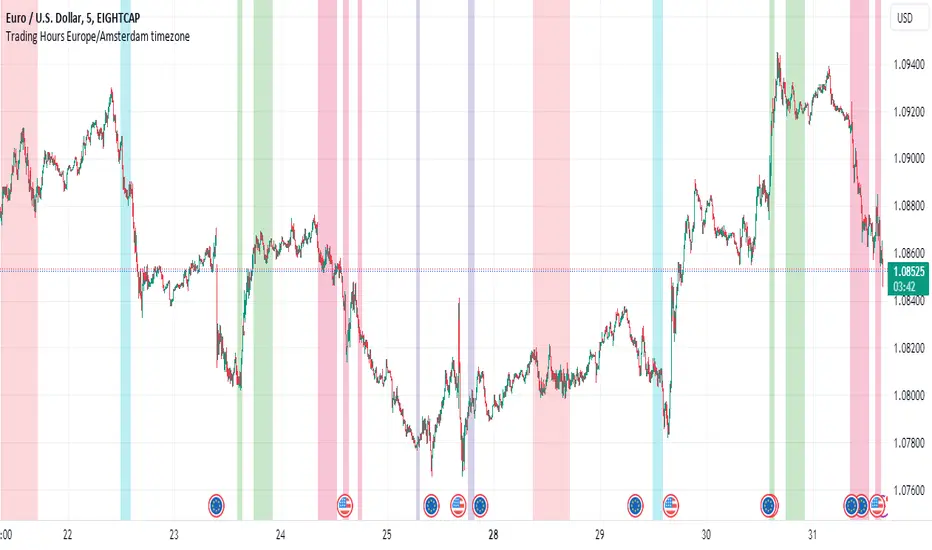

Personal Trading Hours (timezone Europe/Amsterdam)This Personal Trading Hours indicator is intended to specify the times you can trade and make them visible on the chart. Multiple sessions can be specified per specific day of the week and you can give each day its own color if you want.

This can be used perfectly if you are backtesting your strategy manually. You can indicate exactly when you have time to look at the charts and therefore only perform your backtest at those times. Making mistakes that you open en close trades during your sleeptime or worktime in your backtest are gone.

But this indicator is also suitable for live trading.

Filter out the times when you don't want to trade, for example during lunchtime, during opening hours of the exchanges or when you know that big news events will take place during your tradingweek. All the timesessions you do want to trade you can make visible on you chart.

The timezone that is used for this indicator is the timezone: Europe/Amsterdam and therefor only usable for traders in this timezone.

You can use this indicator for timeframes lower then the Daily timeframe with the normal settings. If you want to use this indicator on the Daily timeframe, all the settings in the upper part of the settingsmenu must be unchecked and only the part at the bottom of the settingsmenu can then be used.

This indicator doesn't work on timeframes higher than the Daily timeframe.

If you do not use all the tradingsessions on each day, you have to make sure that all the boxes are filled. So unused session boxes must have the same timeperiodes as the used boxes, otherwise the whole day will be highlighted on the chart.

Igor Sessions Average Candle RangeCalculated Average Candle Range for Igor Sessions. Resets average at these time UTC: 00:00, 06:00, 12:00, 20:00.