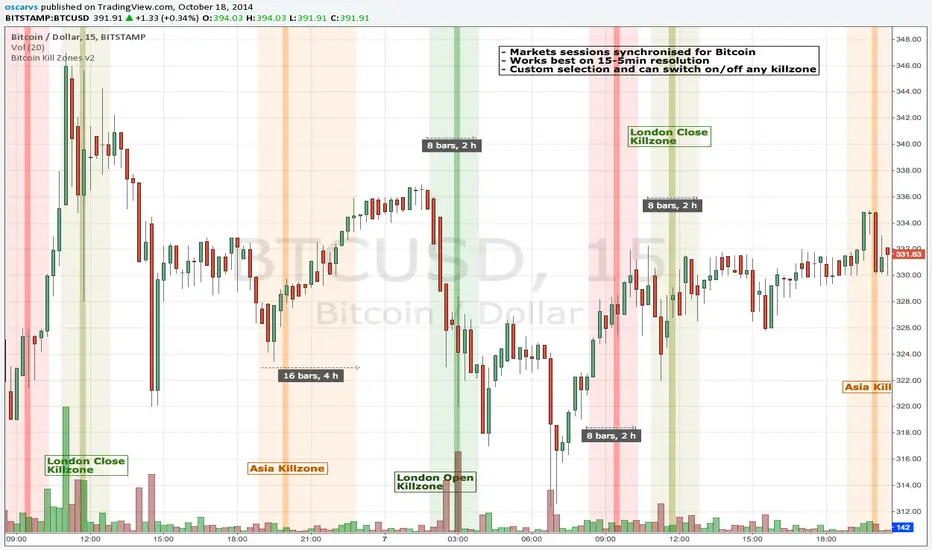

BITCOIN KILL ZONES v2Kill Zones

Kill zones are really liquidity events. Many different market participants often come together and act around these events. The activity itself may be event driven (margin calls or options exercise related activity), portfolio management driven (buy-on-close and asset allocation rebalancing orders) or institutionally driven (larger players needing liquidity to get filled in size) or a combination of any/all three. The point is, this intense cross current of activity at a very specific point in time often occurs near significant technical levels and trends established coming out of these events often persist until the next Kill Zone in approached/entered.

Specifically, there are three Kill Zones and each has its own importance/significance.

1. Asian Kill Zone (1900 - 2300 EST) Considered the "institutional" zone, this zone represents both the launch pad for new trends and also too a reloading area from the post American session. It is the start of a new day (or week) for the world and as such it makes sense this zone will often set the tone for the rest of the world's trading day. Since it is very wide (4 hours) one should pay attention to the Tokyo open (2100 EST) the Beijing open (2120 EST) and the Sydney open (0650 EST previous day).

2. London Kill Zone (0200 - 0400 EST) Considered the center of the financial universe for more than 500 years, Europe still carries a lot of influence within the banking world. Many larger players use the Euro session to establish their positions. As such, the London open often sees the most significant trend establishment activity through any given trading day. Indeed, it has been suggested 80% of all weekly trends are established through Tuesday's London Kill Zone.

3. New York Kill Zone (0830 - 1030 EST) The United States is still by far the world's largest economy and so by default New York's open carries a lot of weight and often comes with a big injection of liquidity. Indeed, most of the world's trade-able assets are priced in US dollars which gives even more significance to political and economic activity within this region. Because it comes relatively late in the globe's trading day, this Kill Zone often sees violent price swings within it's first hour leading to the time tested adage "never trust the first hour of North American trading.

Additional notes:

It has become apparent these Kill Zones are evolving over time and the course of world history. Since the end of the second world war, New York has slowly encroached on London's place as the global center for commercial banking. So much so through the later part of the 20th century New York was considered indeed, the new center of the financial universe. With the end of the cold war that leadership seems to have shifted back toward Europe and away from The United States. Additionally, Japan has slowly lost its former predominance within the global economic landscape while Beijing's has risen dramatically.

Only time will tell how these kill zones will evolve given each region's ever changing political, economic and socioeconomic influences.

Trading Notes:

If you have specific levels of interest odds are the bigger players have the same levels too. If it is indeed a solid level, look for price to trade to your level through the kill zone because the zone is a liquidity event where the bigger players can find enough size to get their big orders filled.

Try to avoid taking positions heading into Kill Zones and look for confirmation of your levels coming out of the event. For the more advanced trader, look to take positions on those level hits through the zone but understand higher time frame players often have far deeper pockets then day traders and can endure far more volatility then us little guys.

Thanks for the contribution to @CRInvestor and @ICT_MHuddleston

在腳本中搜尋"session"

Daily Session DividerThis script draws vertical lines showing the new daily sessions. These will only be displayed when it's on an intraday timeframe (lower than daily timeframe).

Settings:

Line Color: Choose the color you want and change the opacity

Line Width: If you want a thicc line. Defaults to 1 (recommended setting)

Line Style: Choose between solid (default), dashed, or dotted

ICT MacrosThis script allows traders to visualize the range of time when a macro (an automated series of instructions/trades from large fund traders, executed by an algorithm) will likely occur in the market. It does this by drawing vertical lines and labels on the chart at these specific times:

(Macro Open) - 9:50 AM EST

(Macro Close) - 10:10 AM EST

(Macro Open) - 10:50 AM EST

(Macro Close) - 11:10 AM EST

(Macro Open) - 1:10 PM EST

(Macro Close) - 1:40 PM EST

(Macro Open) - 3:15 PM EST

(Macro Close) - 3:45 PM EST

The theory behind the use of these macros - is that the market will either seek buy side or sell side liquidity, or seek to rebalance price at a point of interest in between the open and close of the macro. Traders who follow this theory can use that information to anticipate how price might behave.

When a macro occurs, the script draws a vertical line on the chart using a dotted line style with a user-defined color. Additionally, a label is placed above the line to indicate whether it is a Macro Open or Macro Close event.

To preserve space, the labels are abbreviated on chart - "Macro Open" (M.O.) and "Macro Close" (M.C.) for both the morning and afternoon trading sessions. The labels may be turned on/off by the user.

The script also includes alerts that can notify traders when a macro occurs. These alerts can be set to go off once per bar close, and the alert message indicates the specific macro type and time.

This script is entirely open-source, meaning that traders can read the code and modify it as needed. Credit to the foundation of this script goes to TradingView user @rickyzcarroll for his open source Strat Assistant Hour Flip script. Important changes include the specific time changes and alert function.

Ultimate Time Filter V1The only time filter that you will ever need.

Easily filter for:

--> Start/End Dates

--> Weekdays

--> 1 or 2 Daily Trade Sessions.

This is open source on purpose so you can enjoy ease of use on your own codes. Simply copy the code and use the variable "inTime" to filter bars that fit your time constraints.

I spent a lot more time on this than I'd like to admit but so be it. Any comments for improvements, or questions on how to use the script is appreciated. Or if you wanna chat about trading / pine script hit me up on Discord.

Cheers

Peak Trading Activity Graphs [LuxAlgo]The Peak Trading Activity Graphs displays four graphs that allow traders to see at a glance the times of the highest and lowest volume and volatility for any month, day of the month, day of the week, or hour of the day. By default, it plots the median values of the selected data for each period. Traders can enable the Median Delta feature to further highlight differences in the data. The graphs are customizable in width and height and feature gradient colors by default.

🔶 USAGE

The tool is simple yet powerful. Using the three main parameters on the settings panel, traders can display up to four different graphs and up to 16 different configurations.

There are two main types of data: volume and volatility. There are also four different time periods: months, days of the month, days of the week, and hours of the day. There is also the possibility of displaying the raw medians or the delta between them.

Understanding which time periods have the most and least volume and volatility is essential for any trader. From avoiding trading during periods of low volume to properly sizing positions during periods of high volatility, there are multiple use cases directly related to improving execution and risk management.

🔹 Months

This chart shows the monthly volume and volatility of NQ as medians at the top and as the delta of medians at the bottom.

As we can see on the left-hand chart, the volume is fairly consistent throughout the year. January, March, and October have the highest volume, and December has the lowest volume for obvious reasons. Note the bottom chart with the delta feature enabled, which clearly shows the top and bottom periods.

On the right, we have volatility, which is also evenly distributed throughout most months. October is the most volatile month, and March is the least volatile month. The differences are also very clear on the bottom chart with delta enabled.

Traders may want to compare median volatility and volume by month to size positions and favor exposure during historically high-activity months.

🔹 Days of Month

The same NQ charts are shown, but in this case, the Days of Month period has been selected. As you can see, this displays a calendar-like graph. The volume is on the left, the volatility is on the right, and the delta feature is enabled on the bottom charts. This feature allows for stronger differences in gradient.

The top charts show that the raw medians of both volume and volatility are evenly distributed. We need to enable the delta feature on the bottom charts to see where the most and least volume and volatility are.

Traders can use median activity by calendar day to anticipate liquidity expansions or contractions and adjust trade frequency.

🔹 Days of Week

In this case, we have BTC charts with the same layout as before. Notably, the difference in volume on weekends is not as pronounced from a volatility perspective on those same days.

A practical use case can be differentiate high-risk, high-participation weekdays from low-activity sessions to select trend or range-based strategies.

🔹 Hours of Day

This shows the volume and volatility of each hour of the day for gold futures. As we can see, the most volume and volatility occur during the three hours around the RTH open at 8:00, 9:00, and 10:00 a.m.

Traders may want to isolate hours with the highest median volatility and volume to concentrate execution and avoid low-liquidity periods.

🔹 Assets Comparison

This tool allows us to compare different assets over the same period. In this case, we are comparing the hours of the day for 10-year notes, the S&P 500, silver, and the yen. Each asset has a different volatility profile throughout the day.

With the Delta feature enabled, we can clearly see the differences. The 10Y Notes move from 7:00 to 9:00 and from 2:00 to 9:00. The Yen moves from 7:00 to 9:00 and from 2:00 to 9:00. Silver moves from 8:00 to 10:00. The S&P 500 moves from 8:00 to 9:00 and from 14:00 to 15:00. All times are in exchange time.

🔹 Sizing & Coloring Graphs

Traders can adjust the width and height of the graphs, as well as the text size, at will.

Traders can choose from four different color configurations in the settings panel.

🔶 SETTINGS

Data: Select the type of data to display: Volume or Volatility.

Period: Select the time period to display: Month, Day of Month, Day of Week, or Hours.

Display delta between medians. Display the difference between the medians as a percentage. The smaller median is 0 and the larger median is 100. Enabling this feature highlights the differences between values.

🔹 Graph

Graph: Select the graph location.

Size: Select the graph size.

Width: Select the graph width.

Height: Select the height of the graph.

🔹 Style

Colors: Select a color map: Viridis, Plasma, Magma, or Custom.

Custom Cold: Select a custom color for cold (low values).

Custom Lukewarm: Select a custom color for lukewarm (medium values).

Custom Hot: Select a custom color for hot (high values).

NQ 5x Daily SessionsThis indicator automatically plots horizontal lines for the Daily Open as well as four of the most significant trading milestones of the day (CET/Berlin time). It helps you instantly identify psychological price levels and institutional opening marks directly on your chart.

Features:

Key Time Stamps: Automatic lines for the daily opening price and specific session opens at 08:00 (Frankfurt/Pre-Market), 10:00, 14:00, and 15:30 (NYSE Open).

Fully Customizable:

Control line thickness, label visibility, and the extension of current intraday lines via the settings menu.

Trading Application:

These levels often act as significant Support & Resistance during intraday trading. The 08:00 and 15:30 marks, in particular, frequently represent turning points or the start of strong trends, as trading volume spikes significantly during these windows.

TOA SESSION INDICATOR PRO - MARKED WITH COLORSThis indicator is made for The Orderflow Academy community.

You can see the highs and lows of the sessions in colors.

NY Session Start & End LinesDraws a vertical line at the start and end of regular trading hours for the NY session.

Daily 5 & 20 (Session Lines)Daily 5 & 20 Moving Average Levels

This indicator plots the Daily 5-period and Daily 20-period moving averages as horizontal levels on any timeframe. Each level starts at the first bar of the trading day and extends only to the current price, keeping the chart clean and focused on the active session.

The levels update once per day using confirmed daily data and are designed to act as intraday bias, support, and resistance references. Labels are aligned on the right side for a minimal, institutional-style presentation.

Useful for:

Intraday trading on lower timeframes

Identifying daily trend bias

Mean reversion and pullback setups

Futures, stocks, ETFs, and options

No future extension, no repainting, and no unnecessary clutter.

-Golden Zone Family

Macro PO3 + Sessions + H/L LevelsMacro power of 3

Session highs lows

previous days highs and lows

previous week highs and lows

ICT Master: Type-Safe Sessions & FVGsasia, london , new york session and killzones used by ict and other top traders

Prop ES Bollinger Bands Strat during Single/Dual Trading SessionBollinger Band strategy for ES futures optimized for prop firm rules.

Choose long-only, short-only, or both directions.

Customizable BB length and multiplier.

Enter trades during one or two configurable sessions specified in New York time.

Fixed TP/SL in ticks with forced close by 4:59 PM NY time.

3 Session ORB (Opening Range Breakout) [TickDaddy]The ORB, or Opening Range Breakout indicator. will show all 3 sessions and you can adjust the times.

Prop ES EMA Cross during Single/Dual Trading SessionEMA crossover strategy for ES futures optimized for prop firm rules.

Choose long-only, short-only, or both directions.

Customizable short and long EMA lengths.

Enter trades during one or two configurable sessions specified in New York time.

Fixed TP/SL in ticks with forced close by 4:59 PM NY time.

EMA + Sessions + RSI Strategy v1.0A professional trading strategy that combines multiple technical indicators for high-probability entries. This system uses EMA crossovers, RSI zone filtering, and trend confirmation to identify optimal trading opportunities while managing risk with advanced position management tools.

Key Features:

✅ Dual Entry Signals (EMA21 + EMA100 crossover conditions)

✅ Trend Filter EMA750 (trade only with the major trend)

✅ Complete Risk Management (SL 1%, TP 3% default)

✅ Trailing Stop & Breakeven (maximize profits, protect capital)

✅ Compact Statistics Table (real-time performance metrics)

✅ RSI & Session Filters (avoid low-probability setups)

✅ Optional Pyramiding (scale into winning positions)

Perfect for swing trading and trend-following on any timeframe. Fully customizable to match your trading style.

an_dy_time_marker+killzone+sessionAn indicator where you can configure 5 different trading times. You can also view the kill zone and the entire session.

Have fun and catch the pips!

FX Sessions by m_cptForex Intraday Sessions Indicator, config time in UTC-4. Support 4 main sessions, smooth end-to-start candles mode, without gaps if your sessions has config like:

1) 19:00 - 03:00

2) 02:00 - 03:00

3) 03:00 -11:00

No excluded last candles issue on all TFs.

Working on LTF up to 1h TF since its intraday sessions indicator.

Stocks Sessions TableThe stock market open session table is a great way to keep an eye on the market's open and close. This is aimed at the UK traders working with the BST timezone

Trading Sessionsconst string TZ_TOOLTIP_TEXT = "The session's time zone, specified in either GMT notation (e.g., 'GMT-5') or as an IANA time zone database name (e.g., 'America/New_York')."

Night and Day Session Highlighter % (Valehson)- This script splits the day into night and day sessions and displays the price change in percentage.

- Этот скрипт разделяет день на вечерние и дневные сессии и показывает изменение цены в процентах.

Custom Time Session Background (Amsterdam Time, DST Safe)This indicator highlights two custom intraday time ranges with background colors on your chart. The times are set based on your local Amsterdam time and automatically adjust for Daylight Saving Time (DST).

📌 Features:

- Define two separate time ranges (Start & End) in local Amsterdam time

- Background color highlighting for each range

- Fully DST-aware using the "Europe/Amsterdam" timezone

- Works across all intraday timeframes

🎯 Use Cases:

- Highlight key market sessions (e.g., EU open, NY overlap)

- Visually segment your trading hours

- Eliminate manual DST adjustments

Developed with Pine Script v5.

Made for traders who want clarity during specific time zones, without worrying about time shifts across the year.