BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

在腳本中搜尋"stop loss"

Optimized ADX DI CCI Strategy### Key Features:

- Combines ADX, DI+/-, CCI, and RSI for signal generation.

- Supports customizable timeframes for indicators.

- Offers multiple exit conditions (Moving Average cross, ADX change, performance-based stop-loss).

- Tracks and displays trade statistics (e.g., win rate, capital growth, profit factor).

- Visualizes trades with labels and optional background coloring.

- Allows countertrading (opening an opposite trade after closing one).

1. **Indicator Calculation**:

- **ADX and DI+/-**: Calculated using the `ta.dmi` function with user-defined lengths for DI and ADX smoothing.

- **CCI**: Computed using the `ta.cci` function with a configurable source (default: `hlc3`) and length.

- **RSI (optional)**: Calculated using the `ta.rsi` function to filter overbought/oversold conditions.

- **Moving Averages**: Used for CCI signal smoothing and trade exits, with support for SMA, EMA, SMMA (RMA), WMA, and VWMA.

2. **Signal Generation**:

- **Buy Signal**: Triggered when DI+ > DI- (or DI+ crosses over DI-), CCI > MA (or CCI crosses over MA), and optional ADX/RSI filters are satisfied.

- **Sell Signal**: Triggered when DI+ < DI- (or DI- crosses over DI+), CCI < MA (or CCI crosses under MA), and optional ADX/RSI filters are satisfied.

3. **Trade Execution**:

- **Entry**: Long or short trades are opened using `strategy.entry` when signals are detected, provided trading is allowed (`allow_long`/`allow_short`) and equity is positive.

- **Exit**: Trades can be closed based on:

- Opposite signal (if no other exit conditions are used).

- MA cross (price crossing below/above the exit MA for long/short trades).

- ADX percentage change exceeding a threshold.

- Performance-based stop-loss (trade loss exceeding a percentage).

- **Countertrading**: If enabled, closing a trade triggers an opposite trade (e.g., closing a long opens a short).

4. **Visualization**:

- Labels are plotted at trade entries/exits (e.g., "BUY," "SELL," arrows).

- Optional background coloring highlights open trades (green for long, red for short).

- A statistics table displays real-time metrics (e.g., capital, win rates).

5. **Trade Tracking**:

- Tracks the number of long/short trades, wins, and overall performance.

- Monitors equity to prevent trading if it falls to zero.

### 2.3 Key Components

- **Indicator Calculations**: Uses `request.security` to fetch indicator data for the specified timeframe.

- **MA Function**: A custom `ma_func` handles different MA types for CCI and exit conditions.

- **Signal Logic**: Combines crossover/under checks with recent bar windows for flexibility.

- **Exit Conditions**: Multiple configurable exit strategies for risk management.

- **Statistics Table**: Updates dynamically with trade and capital metrics.

## 3. Configuration Options

The script provides extensive customization through input parameters, grouped for clarity in the TradingView settings panel. Below is a detailed breakdown of each setting and its impact.

### 3.1 Strategy Settings (Global)

- **Initial Capital**: Default `10000`. Sets the starting capital for backtesting.

- **Effect**: Determines the base equity for calculating position sizes and performance metrics.

- **Default Quantity Type**: `strategy.percent_of_equity` (50% of equity).

- **Effect**: Controls the size of each trade as a percentage of available equity.

- **Pyramiding**: Default `2`. Allows up to 2 simultaneous trades in the same direction.

- **Effect**: Enables multiple entries if conditions are met, increasing exposure.

- **Commission**: 0.2% per trade.

- **Effect**: Simulates trading fees, reducing net profit in backtesting.

- **Margin**: 100% for long and short trades.

- **Effect**: Assumes no leverage; adjust for margin trading simulations.

- **Calc on Every Tick**: `true`.

- **Effect**: Ensures real-time signal updates for precise execution.

### 3.2 Indicator Settings

- **Indicator Timeframe** (`indicator_timeframe`):

- **Options**: `""` (chart timeframe), `1`, `5`, `15`, `30`, `60`, `240`, `D`, `W`.

- **Default**: `""` (uses chart timeframe).

- **Effect**: Determines the timeframe for ADX, DI, CCI, and RSI calculations. A higher timeframe reduces noise but may delay signals.

### 3.3 ADX & DI Settings

- **DI Length** (`adx_di_len`):

- **Default**: `30`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for calculating DI+ and DI-. Longer periods smooth trends but reduce sensitivity.

- **ADX Smoothing Length** (`adx_smooth_len`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Smooths the ADX calculation. Longer periods produce smoother ADX values.

- **Use ADX Filter** (`use_adx_filter`):

- **Default**: `false`.

- **Effect**: If `true`, requires ADX to exceed the threshold for signals to be valid, filtering out weak trends.

- **ADX Threshold** (`adx_threshold`):

- **Default**: `25`.

- **Range**: Minimum `0`.

- **Effect**: Sets the minimum ADX value for valid signals when the filter is enabled. Higher values restrict trades to stronger trends.

### 3.4 CCI Settings

- **CCI Length** (`cci_length`):

- **Default**: `20`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for CCI calculation. Longer periods reduce noise but may lag.

- **CCI Source** (`cci_src`):

- **Default**: `hlc3` (average of high, low, close).

- **Effect**: Defines the price data for CCI. `hlc3` is standard, but users can choose other sources (e.g., `close`).

- **CCI MA Type** (`ma_type`):

- **Options**: `SMA`, `EMA`, `SMMA (RMA)`, `WMA`, `VWMA`.

- **Default**: `SMA`.

- **Effect**: Determines the moving average type for CCI signal smoothing. EMA is more responsive; VWMA weights by volume.

- **CCI MA Length** (`ma_length`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for the CCI MA. Longer periods smooth the MA but may delay signals.

### 3.5 RSI Filter Settings

- **Use RSI Filter** (`use_rsi_filter`):

- **Default**: `false`.

- **Effect**: If `true`, applies RSI-based overbought/oversold filters to signals.

- **RSI Length** (`rsi_length`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for RSI calculation. Longer periods reduce sensitivity.

- **RSI Lower Limit** (`rsi_lower_limit`):

- **Default**: `30`.

- **Range**: `0` to `100`.

- **Effect**: Defines the oversold threshold for buy signals. Lower values allow trades in more extreme conditions.

- **RSI Upper Limit** (`rsi_upper_limit`):

- **Default**: `70`.

- **Range**: `0` to `100`.

- **Effect**: Defines the overbought threshold for sell signals. Higher values allow trades in more extreme conditions.

### 3.6 Signal Settings

- **Cross Window** (`cross_window`):

- **Default**: `0`.

- **Range**: `0` to `5` bars.

- **Effect**: Specifies the lookback period for detecting DI+/- or CCI crosses. `0` requires crosses on the current bar; higher values allow recent crosses, increasing signal frequency.

- **Allow Long Trades** (`allow_long`):

- **Default**: `true`.

- **Effect**: Enables/disables new long trades. If `false`, only closing existing longs is allowed.

- **Allow Short Trades** (`allow_short`):

- **Default**: `true`.

- **Effect**: Enables/disables new short trades. If `false`, only closing existing shorts is allowed.

- **Require DI+/DI- Cross for Buy** (`buy_di_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a DI+ crossover DI- for buy signals; if `false`, DI+ > DI- is sufficient.

- **Require CCI Cross for Buy** (`buy_cci_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a CCI crossover MA for buy signals; if `false`, CCI > MA is sufficient.

- **Require DI+/DI- Cross for Sell** (`sell_di_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a DI- crossover DI+ for sell signals; if `false`, DI+ < DI- is sufficient.

- **Require CCI Cross for Sell** (`sell_cci_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a CCI crossunder MA for sell signals; if `false`, CCI < MA is sufficient.

- **Countertrade** (`countertrade`):

- **Default**: `true`.

- **Effect**: If `true`, closing a trade triggers an opposite trade (e.g., close long, open short) if allowed.

- **Color Background for Open Trades** (`color_background`):

- **Default**: `true`.

- **Effect**: If `true`, colors the chart background green for long trades and red for short trades.

### 3.7 Exit Settings

- **Use MA Cross for Exit** (`use_ma_exit`):

- **Default**: `true`.

- **Effect**: If `true`, closes trades when the price crosses the exit MA (below for long, above for short).

- **MA Length for Exit** (`ma_exit_length`):

- **Default**: `20`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for the exit MA. Longer periods delay exits.

- **MA Type for Exit** (`ma_exit_type`):

- **Options**: `SMA`, `EMA`, `SMMA (RMA)`, `WMA`, `VWMA`.

- **Default**: `SMA`.

- **Effect**: Determines the MA type for exit signals. EMA is more responsive; VWMA weights by volume.

- **Use ADX Change Stop-Loss** (`use_adx_stop`):

- **Default**: `false`.

- **Effect**: If `true`, closes trades when the ADX changes by a specified percentage.

- **ADX % Change for Stop-Loss** (`adx_change_percent`):

- **Default**: `5.0`.

- **Range**: Minimum `0.0`, step `0.1`.

- **Effect**: Specifies the percentage change in ADX (vs. previous bar) that triggers a stop-loss. Higher values reduce premature exits.

- **Use Performance Stop-Loss** (`use_perf_stop`):

- **Default**: `false`.

- **Effect**: If `true`, closes trades when the loss exceeds a percentage threshold.

- **Performance Stop-Loss (%)** (`perf_stop_percent`):

- **Default**: `-10.0`.

- **Range**: `-100.0` to `0.0`, step `0.1`.

- **Effect**: Specifies the loss percentage that triggers a stop-loss. More negative values allow larger losses before exiting.

## 4. Visual and Statistical Output

- **Labels**: Displayed at trade entries/exits with arrows (↑ for buy, ↓ for sell) and text ("BUY," "SELL"). A "No Equity" label appears if equity is zero.

- **Background Coloring**: Optionally colors the chart background (green for long, red for short) to indicate open trades.

- **Statistics Table**: Displayed at the top center of the chart, updated on timeframe changes or trade events. Includes:

- **Capital Metrics**: Initial capital, current capital, capital growth (%).

- **Trade Metrics**: Total trades, long/short trades, win rate, long/short win rates, profit factor.

- **Open Trade Status**: Indicates if a long, short, or no trade is open.

## 5. Alerts

- **Buy Signal Alert**: Triggered when `buy_signal` is true ("Cross Buy Signal").

- **Sell Signal Alert**: Triggered when `sell_signal` is true ("Cross Sell Signal").

- **Usage**: Users can set up TradingView alerts to receive notifications for trade signals.

VoVix DEVMA🌌 VoVix DEVMA: A Deep Dive into Second-Order Volatility Dynamics

Welcome to VoVix+, a sophisticated trading framework that transcends traditional price analysis. This is not merely another indicator; it is a complete system designed to dissect and interpret the very fabric of market volatility. VoVix+ operates on the principle that the most powerful signals are not found in price alone, but in the behavior of volatility itself. It analyzes the rate of change, the momentum, and the structure of market volatility to identify periods of expansion and contraction, providing a unique edge in anticipating major market moves.

This document will serve as your comprehensive guide, breaking down every mathematical component, every user input, and every visual element to empower you with a profound understanding of how to harness its capabilities.

🔬 THEORETICAL FOUNDATION: THE MATHEMATICS OF MARKET DYNAMICS

VoVix+ is built upon a multi-layered mathematical engine designed to measure what we call "second-order volatility." While standard indicators analyze price, and first-order volatility indicators (like ATR) analyze the range of price, VoVix+ analyzes the dynamics of the volatility itself. This provides insight into the market's underlying state of stability or chaos.

1. The VoVix Score: Measuring Volatility Thrust

The core of the system begins with the VoVix Score. This is a normalized measure of volatility acceleration or deceleration.

Mathematical Formula:

VoVix Score = (ATR(fast) - ATR(slow)) / (StDev(ATR(fast)) + ε)

Where:

ATR(fast) is the Average True Range over a short period, representing current, immediate volatility.

ATR(slow) is the Average True Range over a longer period, representing the baseline or established volatility.

StDev(ATR(fast)) is the Standard Deviation of the fast ATR, which measures the "noisiness" or consistency of recent volatility.

ε (epsilon) is a very small number to prevent division by zero.

Market Implementation:

Positive Score (Expansion): When the fast ATR is significantly higher than the slow ATR, it indicates a rapid increase in volatility. The market is "stretching" or expanding.

Negative Score (Contraction): When the fast ATR falls below the slow ATR, it indicates a decrease in volatility. The market is "coiling" or contracting.

Normalization: By dividing by the standard deviation, we normalize the score. This turns it into a standardized measure, allowing us to compare volatility thrust across different market conditions and timeframes. A score of 2.0 in a quiet market means the same, relatively, as a score of 2.0 in a volatile market.

2. Deviation Analysis (DEV): Gauging Volatility's Own Volatility

The script then takes the analysis a step further. It calculates the standard deviation of the VoVix Score itself.

Mathematical Formula:

DEV = StDev(VoVix Score, lookback_period)

Market Implementation:

This DEV value represents the magnitude of chaos or stability in the market's volatility dynamics. A high DEV value means the volatility thrust is erratic and unpredictable. A low DEV value suggests the change in volatility is smooth and directional.

3. The DEVMA Crossover: Identifying Regime Shifts

This is the primary signal generator. We take two moving averages of the DEV value.

Mathematical Formula:

fastDEVMA = SMA(DEV, fast_period)

slowDEVMA = SMA(DEV, slow_period)

The Core Signal:

The strategy triggers on the crossover and crossunder of these two DEVMA lines. This is a profound concept: we are not looking at a moving average of price or even of volatility, but a moving average of the standard deviation of the normalized rate of change of volatility.

Bullish Crossover (fastDEVMA > slowDEVMA): This signals that the short-term measure of volatility's chaos is increasing relative to the long-term measure. This often precedes a significant market expansion and is interpreted as a bullish volatility regime.

Bearish Crossunder (fastDEVMA < slowDEVMA): This signals that the short-term measure of volatility's chaos is decreasing. The market is settling down or contracting, often leading to trending moves or range consolidation.

⚙️ INPUTS MENU: CONFIGURING YOUR ANALYSIS ENGINE

Every input has been meticulously designed to give you full control over the strategy's behavior. Understanding these settings is key to adapting VoVix+ to your specific instrument, timeframe, and trading style.

🌀 VoVix DEVMA Configuration

🧬 Deviation Lookback: This sets the lookback period for calculating the DEV value. It defines the window for measuring the stability of the VoVix Score. A shorter value makes the system highly reactive to recent changes in volatility's character, ideal for scalping. A longer value provides a smoother, more stable reading, better for identifying major, long-term regime shifts.

⚡ Fast VoVix Length: This is the lookback period for the fastDEVMA. It represents the short-term trend of volatility's chaos. A smaller number will result in a faster, more sensitive signal line that reacts quickly to market shifts.

🐌 Slow VoVix Length: This is the lookback period for the slowDEVMA. It represents the long-term, baseline trend of volatility's chaos. A larger number creates a more stable, slower-moving anchor against which the fast line is compared.

How to Optimize: The relationship between the Fast and Slow lengths is crucial. A wider gap (e.g., 20 and 60) will result in fewer, but potentially more significant, signals. A narrower gap (e.g., 25 and 40) will generate more frequent signals, suitable for more active trading styles.

🧠 Adaptive Intelligence

🧠 Enable Adaptive Features: When enabled, this activates the strategy's performance tracking module. The script will analyze the outcome of its last 50 trades to calculate a dynamic win rate.

⏰ Adaptive Time-Based Exit: If Enable Adaptive Features is on, this allows the strategy to adjust its Maximum Bars in Trade setting based on performance. It learns from the average duration of winning trades. If winning trades tend to be short, it may shorten the time exit to lock in profits. If winners tend to run, it will extend the time exit, allowing trades more room to develop. This helps prevent the strategy from cutting winning trades short or holding losing trades for too long.

⚡ Intelligent Execution

📊 Trade Quantity: A straightforward input that defines the number of contracts or shares for each trade. This is a fixed value for consistent position sizing.

🛡️ Smart Stop Loss: Enables the dynamic stop-loss mechanism.

🎯 Stop Loss ATR Multiplier: Determines the distance of the stop loss from the entry price, calculated as a multiple of the current 14-period ATR. A higher multiplier gives the trade more room to breathe but increases risk per trade. A lower multiplier creates a tighter stop, reducing risk but increasing the chance of being stopped out by normal market noise.

💰 Take Profit ATR Multiplier: Sets the take profit target, also as a multiple of the ATR. A common practice is to set this higher than the Stop Loss multiplier (e.g., a 2:1 or 3:1 reward-to-risk ratio).

🏃 Use Trailing Stop: This is a powerful feature for trend-following. When enabled, instead of a fixed stop loss, the stop will trail behind the price as the trade moves into profit, helping to lock in gains while letting winners run.

🎯 Trail Points & 📏 Trail Offset ATR Multipliers: These control the trailing stop's behavior. Trail Points defines how much profit is needed before the trail activates. Trail Offset defines how far the stop will trail behind the current price. Both are based on ATR, making them fully adaptive to market volatility.

⏰ Maximum Bars in Trade: This is a time-based stop. It forces an exit if a trade has been open for a specified number of bars, preventing positions from being held indefinitely in stagnant markets.

⏰ Session Management

These inputs allow you to confine the strategy's trading activity to specific market hours, which is crucial for day trading instruments that have defined high-volume sessions (e.g., stock market open).

🎨 Visual Effects & Dashboard

These toggles give you complete control over the on-chart visuals and the dashboard. You can disable any element to declutter your chart or focus only on the information that matters most to you.

📊 THE DASHBOARD: YOUR AT-A-GLANCE COMMAND CENTER

The dashboard centralizes all critical information into one compact, easy-to-read panel. It provides a real-time summary of the market state and strategy performance.

🎯 VOVIX ANALYSIS

Fast & Slow: Displays the current numerical values of the fastDEVMA and slowDEVMA. The color indicates their direction: green for rising, red for falling. This lets you see the underlying momentum of each line.

Regime: This is your most important environmental cue. It tells you the market's current state based on the DEVMA relationship. 🚀 EXPANSION (Green) signifies a bullish volatility regime where explosive moves are more likely. ⚛️ CONTRACTION (Purple) signifies a bearish volatility regime, where the market may be consolidating or entering a smoother trend.

Quality: Measures the strength of the last signal based on the magnitude of the DEVMA difference. An ELITE or STRONG signal indicates a high-conviction setup where the crossover had significant force.

PERFORMANCE

Win Rate & Trades: Displays the historical win rate of the strategy from the backtest, along with the total number of closed trades. This provides immediate feedback on the strategy's historical effectiveness on the current chart.

EXECUTION

Trade Qty: Shows your configured position size per trade.

Session: Indicates whether trading is currently OPEN (allowed) or CLOSED based on your session management settings.

POSITION

Position & PnL: Displays your current position (LONG, SHORT, or FLAT) and the real-time Profit or Loss of the open trade.

🧠 ADAPTIVE STATUS

Stop/Profit Mult: In this simplified version, these are placeholders. The primary adaptive feature currently modifies the time-based exit, which is reflected in how long trades are held on the chart.

🎨 THE VISUAL UNIVERSE: DECIPHERING MARKET GEOMETRY

The visuals are not mere decorations; they are geometric representations of the underlying mathematical concepts, designed to give you an intuitive feel for the market's state.

The Core Lines:

FastDEVMA (Green/Maroon Line): The primary signal line. Green when rising, indicating an increase in short-term volatility chaos. Maroon when falling.

SlowDEVMA (Aqua/Orange Line): The baseline. Aqua when rising, indicating a long-term increase in volatility chaos. Orange when falling.

🌊 Morphism Flow (Flowing Lines with Circles):

What it represents: This visualizes the momentum and strength of the fastDEVMA. The width and intensity of the "beam" are proportional to the signal strength.

Interpretation: A thick, steep, and vibrant flow indicates powerful, committed momentum in the current volatility regime. The floating '●' particles represent kinetic energy; more particles suggest stronger underlying force.

📐 Homotopy Paths (Layered Transparent Boxes):

What it represents: These layered boxes are centered between the two DEVMA lines. Their height is determined by the DEV value.

Interpretation: This visualizes the overall "volatility of volatility." Wider boxes indicate a chaotic, unpredictable market. Narrower boxes suggest a more stable, predictable environment.

🧠 Consciousness Field (The Grid):

What it represents: This grid provides a historical lookback at the DEV range.

Interpretation: It maps the recent "consciousness" or character of the market's volatility. A consistently wide grid suggests a prolonged period of chaos, while a narrowing grid can signal a transition to a more stable state.

📏 Functorial Levels (Projected Horizontal Lines):

What it represents: These lines extend from the current fastDEVMA and slowDEVMA values into the future.

Interpretation: Think of these as dynamic support and resistance levels for the volatility structure itself. A crossover becomes more significant if it breaks cleanly through a prior established level.

🌊 Flow Boxes (Spaced Out Boxes):

What it represents: These are compact visual footprints of the current regime, colored green for Expansion and red for Contraction.

Interpretation: They provide a quick, at-a-glance confirmation of the dominant volatility flow, reinforcing the background color.

Background Color:

This provides an immediate, unmistakable indication of the current volatility regime. Light Green for Expansion and Light Aqua/Blue for Contraction, allowing you to assess the market environment in a split second.

📊 BACKTESTING PERFORMANCE REVIEW & ANALYSIS

The following is a factual, transparent review of a backtest conducted using the strategy's default settings on a specific instrument and timeframe. This information is presented for educational purposes to demonstrate how the strategy's mechanics performed over a historical period. It is crucial to understand that these results are historical, apply only to the specific conditions of this test, and are not a guarantee or promise of future performance. Market conditions are dynamic and constantly change.

Test Parameters & Conditions

To ensure the backtest reflects a degree of real-world conditions, the following parameters were used. The goal is to provide a transparent baseline, not an over-optimized or unrealistic scenario.

Instrument: CME E-mini Nasdaq 100 Futures (NQ1!)

Timeframe: 5-Minute Chart

Backtesting Range: March 24, 2024, to July 09, 2024

Initial Capital: $100,000

Commission: $0.62 per contract (A realistic cost for futures trading).

Slippage: 3 ticks per trade (A conservative setting to account for potential price discrepancies between order placement and execution).

Trade Size: 1 contract per trade.

Performance Overview (Historical Data)

The test period generated 465 total trades , providing a statistically significant sample size for analysis, which is well above the recommended minimum of 100 trades for a strategy evaluation.

Profit Factor: The historical Profit Factor was 2.663 . This metric represents the gross profit divided by the gross loss. In this test, it indicates that for every dollar lost, $2.663 was gained.

Percent Profitable: Across all 465 trades, the strategy had a historical win rate of 84.09% . While a high figure, this is a historical artifact of this specific data set and settings, and should not be the sole basis for future expectations.

Risk & Trade Characteristics

Beyond the headline numbers, the following metrics provide deeper insight into the strategy's historical behavior.

Sortino Ratio (Downside Risk): The Sortino Ratio was 6.828 . Unlike the Sharpe Ratio, this metric only measures the volatility of negative returns. A higher value, such as this one, suggests that during this test period, the strategy was highly efficient at managing downside volatility and large losing trades relative to the profits it generated.

Average Trade Duration: A critical characteristic to understand is the strategy's holding period. With an average of only 2 bars per trade , this configuration operates as a very short-term, or scalping-style, system. Winning trades averaged 2 bars, while losing trades averaged 4 bars. This indicates the strategy's logic is designed to capture quick, high-probability moves and exit rapidly, either at a profit target or a stop loss.

Conclusion and Final Disclaimer

This backtest demonstrates one specific application of the VoVix+ framework. It highlights the strategy's behavior as a short-term system that, in this historical test on NQ1!, exhibited a high win rate and effective management of downside risk. Users are strongly encouraged to conduct their own backtests on different instruments, timeframes, and date ranges to understand how the strategy adapts to varying market structures. Past performance is not indicative of future results, and all trading involves significant risk.

🔧 THE DEVELOPMENT PHILOSOPHY: FROM VOLATILITY TO CLARITY

The journey to create VoVix+ began with a simple question: "What drives major market moves?" The answer is often not a change in price direction, but a fundamental shift in market volatility. Standard indicators are reactive to price. We wanted to create a system that was predictive of market state. VoVix+ was designed to go one level deeper—to analyze the behavior, character, and momentum of volatility itself.

The challenge was twofold. First, to create a robust mathematical model to quantify these abstract concepts. This led to the multi-layered analysis of ATR differentials and standard deviations. Second, to make this complex data intuitive and actionable. This drove the creation of the "Visual Universe," where abstract mathematical values are translated into geometric shapes, flows, and fields. The adaptive system was intentionally kept simple and transparent, focusing on a single, impactful parameter (time-based exits) to provide performance feedback without becoming an inscrutable "black box." The result is a tool that is both profoundly deep in its analysis and remarkably clear in its presentation.

⚠️ RISK DISCLAIMER AND BEST PRACTICES

VoVix+ is an advanced analytical tool, not a guarantee of future profits. All financial markets carry inherent risk. The backtesting results shown by the strategy are historical and do not guarantee future performance. This strategy incorporates realistic commission and slippage settings by default, but market conditions can vary. Always practice sound risk management, use position sizes appropriate for your account equity, and never risk more than you can afford to lose. It is recommended to use this strategy as part of a comprehensive trading plan. This was developed specifically for Futures

"The prevailing wisdom is that markets are always right. I take the opposite view. I assume that markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis."

— George Soros

— Dskyz, Trade with insight. Trade with anticipation.

Mogwai Method with RSI and EMA - BTCUSD 15mThis is a custom TradingView indicator designed for trading Bitcoin (BTCUSD) on a 15-minute timeframe. It’s based on the Mogwai Method—a mean-reversion strategy—enhanced with the Relative Strength Index (RSI) for momentum confirmation. The indicator generates buy and sell signals, visualized as green and red triangle arrows on the chart, to help identify potential entry and exit points in the volatile cryptocurrency market.

Components

Bollinger Bands (BB):

Purpose: Identifies overextended price movements, signaling potential reversions to the mean.

Parameters:

Length: 20 periods (standard for mean-reversion).

Multiplier: 2.2 (slightly wider than the default 2.0 to suit BTCUSD’s volatility).

Role:

Buy signal when price drops below the lower band (oversold).

Sell signal when price rises above the upper band (overbought).

Relative Strength Index (RSI):

Purpose: Confirms momentum to filter out false signals from Bollinger Bands.

Parameters:

Length: 14 periods (classic setting, effective for crypto).

Overbought Level: 70 (price may be overextended upward).

Oversold Level: 30 (price may be overextended downward).

Role:

Buy signal requires RSI < 30 (oversold).

Sell signal requires RSI > 70 (overbought).

Exponential Moving Averages (EMAs) (Plotted but not currently in signal logic):

Purpose: Provides trend context (included in the script for visualization, optional for signal filtering).

Parameters:

Fast EMA: 9 periods (short-term trend).

Slow EMA: 50 periods (longer-term trend).

Role: Can be re-added to filter signals (e.g., buy only when Fast EMA > Slow EMA).

Signals (Triangles):

Buy Signal: Green upward triangle below the bar when price is below the lower Bollinger Band and RSI is below 30.

Sell Signal: Red downward triangle above the bar when price is above the upper Bollinger Band and RSI is above 70.

How It Works

The indicator combines Bollinger Bands and RSI to spot mean-reversion opportunities:

Buy Condition: Price breaks below the lower Bollinger Band (indicating oversold conditions), and RSI confirms this with a reading below 30.

Sell Condition: Price breaks above the upper Bollinger Band (indicating overbought conditions), and RSI confirms this with a reading above 70.

The strategy assumes that extreme price movements in BTCUSD will often revert to the mean, especially in choppy or ranging markets.

Visual Elements

Green Upward Triangles: Appear below the candlestick to indicate a buy signal.

Red Downward Triangles: Appear above the candlestick to indicate a sell signal.

Bollinger Bands: Gray lines (upper, middle, lower) plotted for reference.

EMAs: Blue (Fast) and Orange (Slow) lines for trend visualization.

How to Use the Indicator

Setup

Open TradingView:

Log into TradingView and select a BTCUSD chart from a supported exchange (e.g., Binance, Coinbase, Bitfinex).

Set Timeframe:

Switch the chart to a 15-minute timeframe (15m).

Add the Indicator:

Open the Pine Editor (bottom panel in TradingView).

Copy and paste the script provided.

Click “Add to Chart” to apply it.

Verify Display:

You should see Bollinger Bands (gray), Fast EMA (blue), Slow EMA (orange), and buy/sell triangles when conditions are met.

Trading Guidelines

Buy Signal (Green Triangle Below Bar):

What It Means: Price is oversold, potentially ready to bounce back toward the Bollinger Band middle line.

Action:

Enter a long position (buy BTCUSD).

Set a take-profit near the middle Bollinger Band (bb_middle) or a resistance level.

Place a stop-loss 1-2% below the entry (or based on ATR, e.g., ta.atr(14) * 2).

Best Context: Works well in ranging markets; avoid during strong downtrends.

Sell Signal (Red Triangle Above Bar):

What It Means: Price is overbought, potentially ready to drop back toward the middle line.

Action:

Enter a short position (sell BTCUSD) or exit a long position.

Set a take-profit near the middle Bollinger Band or a support level.

Place a stop-loss 1-2% above the entry.

Best Context: Effective in ranging markets; avoid during strong uptrends.

Trend Filter (Optional):

To reduce false signals in trending markets, you can modify the script:

Add and ema_fast > ema_slow to the buy condition (only buy in uptrends).

Add and ema_fast < ema_slow to the sell condition (only sell in downtrends).

Check the Fast EMA (blue) vs. Slow EMA (orange) alignment visually.

Tips for BTCUSD on 15-Minute Charts

Volatility: BTCUSD can be erratic. If signals are too frequent, increase bb_mult (e.g., to 2.5) or adjust RSI levels (e.g., 75/25).

Confirmation: Use volume spikes or candlestick patterns (e.g., doji, engulfing) to confirm signals.

Time of Day: Mean-reversion works best during low-volume periods (e.g., Asian session in crypto).

Backtesting: Use TradingView’s Strategy Tester (convert to a strategy by adding entry/exit logic) to evaluate performance with historical BTCUSD data up to March 13, 2025.

Risk Management

Position Size: Risk no more than 1-2% of your account per trade.

Stop Losses: Always use stops to protect against BTCUSD’s sudden moves.

Avoid Overtrading: Wait for clear signals; don’t force trades in choppy or unclear conditions.

Example Scenario

Chart: BTCUSD, 15-minute timeframe.

Buy Signal: Price drops to $58,000, below the lower Bollinger Band, RSI at 28. A green triangle appears.

Action: Buy at $58,000, target $59,000 (middle BB), stop at $57,500.

Sell Signal: Price rises to $60,500, above the upper Bollinger Band, RSI at 72. A red triangle appears.

Action: Sell at $60,500, target $59,500 (middle BB), stop at $61,000.

This indicator is tailored for mean-reversion trading on BTCUSD. Let me know if you’d like to tweak it further (e.g., add filters, alerts, or alternative indicators)!

Breaks and Retests - Free990Strategy Description: "Breaks and Retests - Free990"

The "Breaks and Retests - Free990" strategy is based on identifying breakout and retest opportunities for potential entries in both long and short trades. The idea is to detect price breakouts above resistance levels or below support levels, and subsequently identify retests that confirm the breakout levels. The strategy offers an automated approach to enter trades after a breakout followed by a retest, which serves as a confirmation of trend continuation.

Key Components:

Support and Resistance Detection:

The strategy calculates pivot levels based on historical price movements to define support and resistance areas. A lookback range is used to determine these key levels.

Breakouts and Retests:

The system identifies when a breakout occurs above a resistance level or below a support level.

It then waits for a retest of the previously broken level as confirmation, which is often a better entry opportunity.

Trade Direction Selection:

Users can choose between "Long Only," "Short Only," or "Both" directions for trading based on their market view.

Stop Loss and Trailing Stop:

An initial stop loss is placed at a defined percentage away from the entry.

The trailing stop loss is activated after the position gains a specified percentage in profit.

Long Entry:

A long entry is triggered if the price breaks above a resistance level and subsequently retests that level successfully.

The entry condition checks if the breakout was confirmed and if a retest was valid.

The long entry is only executed if the user-selected direction is either "Long Only" or "Both."

Short Entry:

A short entry is triggered if the price breaks below a support level and subsequently retests that level.

The short entry is only executed if the user-selected direction is either "Short Only" or "Both."

sell_condition checks whether the support has been broken and whether the retest condition is valid.

An initial stop loss is placed when the trade is opened to limit the risk if the trade moves against the position.

The stop loss is calculated based on a user-defined percentage (stop_loss_percent) of the entry price.

pinescript

Copy code

stop_loss_price := strategy.position_avg_price * (1 - stop_loss_percent / 100)

For long positions, the stop loss is placed below the entry price.

For short positions, the stop loss is placed above the entry price.

Trailing Stop:

When a position achieves a certain profit threshold (profit_threshold_percent), the trailing stop mechanism is activated.

For long positions, the trailing stop follows the highest price reached, ensuring that some profit is locked in if the price reverses.

For short positions, the trailing stop follows the lowest price reached.

Code Logic for Trailing Stop:

Exit Execution:

The strategy exits the position when the price hits the calculated stop loss level.

This includes both the initial stop loss and the trailing stop that adjusts as the trade progresses.

Code Logic for Exit:

Summary:

Breaks and Retests - Free990 uses support and resistance levels to identify breakouts, followed by retests for confirmation.

Entry Points: Triggered when a breakout is confirmed and a retest occurs, for both long and short trades.

Exit Points:

Initial Stop Loss: Limits risk for both long and short trades.

Trailing Stop Loss: Locks in profits as the price moves in favor of the position.

This strategy aims to capture the momentum after breakouts and minimize losses through effective use of stop loss and trailing stops. It gives the flexibility of selecting trade direction and ensures trades are taken with confirmation through the retest, which helps to reduce false breakouts.

Original Code by @HoanGhetti

Crypto Volatility Bitcoin Correlation Strategy Description:

The Crypto Volatility Bitcoin Correlation Strategy is designed to leverage market volatility specifically in Bitcoin (BTC) using a combination of volatility indicators and trend-following techniques. This strategy utilizes the VIXFix (a volatility indicator adapted for crypto markets) and the BVOL7D (Bitcoin 7-Day Volatility Index from BitMEX) to identify periods of high volatility, while confirming trends with the Exponential Moving Average (EMA). These components work together to offer a comprehensive system that traders can use to enter positions when volatility and trends are aligned in their favor.

Key Features:

VIXFix (Volatility Index for Crypto Markets): This indicator measures the highest price of Bitcoin over a set period and compares it with the current low price to gauge market volatility. A rise in VIXFix indicates increasing market volatility, signaling that large price movements could occur.

BVOL7D (Bitcoin 7-Day Volatility Index): This volatility index, provided by BitMEX, measures the volatility of Bitcoin over the past 7 days. It helps traders monitor the recent volatility trend in the market, particularly useful when making short-term trading decisions.

Exponential Moving Average (EMA): The 50-period EMA acts as a trend indicator. When the price is above the EMA, it suggests the market is in an uptrend, and when the price is below the EMA, it suggests a downtrend.

How It Works:

Long Entry: A long position is triggered when both the VIXFix and BVOL7D indicators are rising, signaling increased volatility, and the price is above the 50-period EMA, confirming that the market is trending upward.

Exit: The strategy exits the position when the price crosses below the 50-period EMA, which signals a potential weakening of the uptrend and a decrease in volatility.

This strategy ensures that traders only enter positions when the volatility aligns with a clear trend, minimizing the risk of entering trades during periods of market uncertainty.

Testing and Timeframe:

This strategy has been tested on Bitcoin using the daily timeframe, which provides a longer-term perspective on market trends and volatility. However, users can adjust the timeframe according to their trading preferences. It is crucial to note that this strategy does not include comprehensive risk management, aside from the exit condition when the price crosses below the EMA. Users are strongly advised to implement their own risk management techniques, such as setting appropriate stop-loss levels, to safeguard their positions during high volatility periods.

Utility:

The Crypto Volatility Bitcoin Correlation Strategy is particularly well-suited for traders who aim to capitalize on the high volatility often seen in the Bitcoin market. By combining volatility measurements (VIXFix and BVOL7D) with a trend-following mechanism (EMA), this strategy helps identify optimal moments for entering and exiting trades. This approach ensures that traders participate in potentially profitable market moves while minimizing exposure during times of uncertainty.

Use Cases:

Volatility-Based Entries: Traders looking to take advantage of market volatility spikes will find this strategy useful for timing entry points during market swings.

Trend Confirmation: By using the EMA as a confirmation tool, traders can avoid entering trades that go against the trend, which can result in significant losses during volatile market conditions.

Risk Management: While the strategy exits when price falls below the EMA, it is important to recognize that this is not a full risk management system. Traders should use caution and integrate additional risk measures, such as stop-losses and position sizing, to better manage potential losses.

How to Use:

Step 1: Monitor the VIXFix and BVOL7D indicators. When both are rising and the Bitcoin price is above the EMA, the strategy will trigger a long entry, indicating that the market is experiencing increased volatility with a confirmed uptrend.

Step 2: Exit the position when the price drops below the 50-period EMA, signaling that the trend may be reversing or weakening, reducing the likelihood of continued upward price movement.

This strategy is open-source and is intended to help traders navigate volatile market conditions, particularly in Bitcoin, using proven indicators for volatility and trend confirmation.

Risk Disclaimer:

This strategy has been tested on the daily timeframe of Bitcoin, but users should be aware that it does not include built-in risk management except for the below-EMA exit condition. Users should be extremely cautious when using this strategy and are encouraged to implement their own risk management, such as using stop-losses, position sizing, and setting appropriate limits. Trading involves significant risk, and this strategy does not guarantee profits or prevent losses. Past performance is not indicative of future results. Always test any strategy in a demo environment before applying it to live markets.

Position Size Calculator for ContractDescription:

Position Size Calculator is a versatile Pine Script tool designed to help traders manage their risk and position sizing effectively. This script calculates essential trading metrics and visualizes them directly on your chart, helping you make informed trading decisions.

Features:

- Account Size & Risk Management:

- Account Size: Input your total account balance to calculate position sizes.

- Maximum Risk: Define how much of your account you are willing to risk per trade in dollars.

- Pip Value: Set the value of a single pip for one contract, which is crucial for calculating risk

and position size.

Trade Setup Visualization:

- Entry Price: Specify the price at which you plan to enter the trade.

- Stop Loss: Define your stop loss level to manage your risk.

- Take Profit: Set your target profit level for the trade.

- Visualize the Entry, Stop Loss, and Take Profit levels on your chart with customizable line

colors and text sizes.

- View the distance in pips between the Entry, Stop Loss, and Take Profit levels.

Position Size Calculation:

- Calculates the number of contracts to open based on your risk tolerance and the pip value.

- Displays the maximum number of contracts you can open given your risk parameters.

Customizable Table Display:

- Table Position: Choose the position of the summary table on the chart (Top-Left, Top-Right,

Bottom-Left, Bottom-Right, etc.).

- Table Text Size: Adjust the text size for the summary table.

- Table Background Color: Set the background color for the summary table.

- Table Border Color: Customize the border color of the summary table.

How to Use:

1- Input your Account Size: Enter your current account balance.

2- Set Maximum Risk and Pip Value: Define how much you're willing to risk per trade and the

pip value for your contract.

3- Define Trade Levels: Input your desired Entry Price, Stop Loss, and Take Profit levels.

4- Customize Visuals: Adjust the line styles and table settings to fit your preferences.

5- View Calculations: The script will display the distance in pips and the calculated position

size directly on your chart.

Example Usage:

Example to calculate the value of 1 pips with 1 contract:

Inputs:

Account Size: Your total trading account balance.

Maximum Risk: Risk amount per trade in dollars.

Pip Value: Value of one pip for a single contract.

Entry Price: The price at which you plan to enter the trade.

Stop Loss: The level at which you will exit the trade to cut losses.

Take Profit: The target price to lock in profits.

Line Text Size: Size of the text for the Entry, Stop Loss, and Take Profit lines.

Line Extend: Option to extend the lines for visual clarity.

Table Position: Position of the summary table on the chart.

Table Text Size: Size of the text in the summary table.

Table Background Color: Background color of the summary table.

Table Border Color: Border color of the summary table.

Visuals:

Entry Price, Stop Loss, and Take Profit levels are clearly marked on the chart.

Summary Table with important trade metrics displayed.

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Range Average Retest Model [LuxAlgo]The Range Average Retest Model tool highlights setups from the range average retest entry model, a model using the retest of the average between two opposite swing points as an entry.

This tool uses long-term volatility coupled with user-defined multipliers to filter out swing areas and set take profit and stop loss levels for all trades.

Key features include:

Draw up to 165 swing areas and their associated trades

Filter out swing areas using Pivot Length , Selection Mode and Threshold parameters

Filter out trades with Maximum Distance and Minimum Distance parameters

Enable or disable swing areas and select default colors

Enable or disable overlapping trades and change the default colors for Take Profit and Stop Loss zones

🔶 USAGE

The "Range Average Retest Model" is an entry model that enters a position when the price retests the average made between two swing points. Users can determine the period of the detected swing points from the "Pivot Length" setting.

The conditions for long or short trades, regardless of whether the swing area is bullish or bearish, are as follows:

Long positions: the current bar close is below the swing area average and the last bar close was above it.

Short positions: the current bar close is above the swing area average price and the last bar close was below it.

Each trade is displayed on the chart with a line connecting it to its swing area highlighting the range average, a green area for the take profit, and a red area for the stop loss.

Both the Take Profit and Stop Loss levels are calculated by applying your own multiplier in the settings panel to the long-term volatility measure, in this case, the average true range over the last 200 bars.

Trades will remain open until they reach either the Stop Loss or Take Profit price levels.

🔹 Filtering Swing Areas

The daily chart of the Nasdaq-100 futures (NQ) with pivot length 2 and bullish selection mode: it only detects bullish swing areas, but they are smaller and more numerous.

Traders can manipulate the behavior of the swing areas from the settings panel.

The Selection mode will filter areas by bias: it will detect bullish areas, bearish areas, or both.

The Threshold parameter is applied to the long-term volatility to filter out areas where the average prices are too close together; the higher the value, the greater the difference between the average prices must be.

🔹 Trades

3-minute chart of the Nasdaq-100 futures (NQ) with pivot length 5, bearish selection mode maximum distance 4, and stop loss 2: many trades detected with very asymmetric risk/reward.

The behavior of the trades is also manipulated from the settings panel.

The maximum and minimum distance parameters specify the number of bars a trade must be away from a swing area.

The Take Profit and Stop Loss parameters are applied to the long-term volatility to obtain their respective price levels.

🔹 Overlapping Trades

Same chart as before, but with overlapping trades: messy, right?

By default the tool does not show overlapping trades, this allows for a cleaner chart.

In the settings panel traders can enable overlapping mode, in which case the tool will show all available trades.

Traders must be aware that the chart can be very crowded.

🔶 SETTINGS

🔹 Swings

Pivot Length: How many bars are used to confirm a swing point. The larger this parameter is, the larger and fewer swing areas will be detected.

Selection Mode: Swing area detection mode, detect only bullish swings, only bearish swings, or both.

Threshold: Swing area comparator. This threshold is multiplied by a measure of volatility (average true range over the last 200 bars), for a new swing area to be detected it must have an average level that is sufficiently distant from the average level of any untouched swing area, this parameter controls that distance.

🔹 Trades

Maximum distance: Maximum distance allowed between a swing area and a trade.

Minimum distance: Minimum distance allowed between a swing area and a trade.

Take profit: The size of the take profit - this threshold is multiplied by a measure of volatility (the average true range over the last 200 bars).

Stop loss: The size of the stop-loss: this threshold is multiplied by a measure of volatility (the average true range over the last 200 bars).

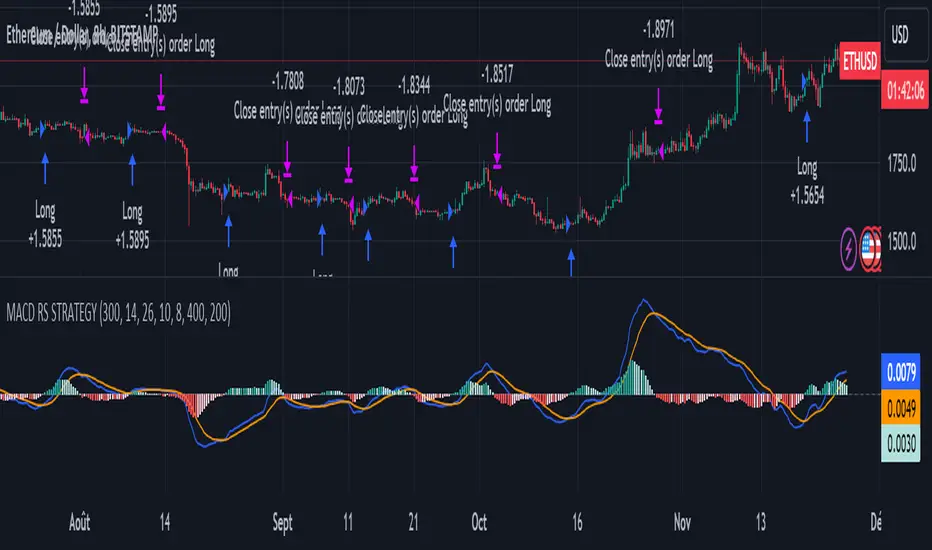

MACD of Relative Strenght StrategyMACD Relative Strenght Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators: MACD and Relative Strenght (RS). By coupling them, we obtain powerful buy signals. In fact, the special feature of this strategy is that it creates an indicator from an indicator. Thus, we construct a MACD whose source is the value of the RS. The strategy only takes buy signals, ignoring SHORT signals as they are mostly losers. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RELATIVE STRENGHT :

RS is an indicator that measures the anomaly between momentum and the assumption of market efficiency. It is used by professionals and is one of the most robust indicators. The idea is to own assets that do better than average, based on their past performance. We calculate RS using this formula :

RS = close/highest_high(RS_Length)

Where highest_high(RS_Length) = highest value of the high over a user-defined time period (which is the RS_Length).

We can thus situate the current price in relation to its highest price over this user-defined period.

MACD (Moving Average Convergence - Divergence) :

This is one of the best-known indicators, measuring the distance between two exponential moving averages : one fast and one slower. A wide distance indicates fast momentum and vice versa. We'll plot the value of this distance and call this line macdline. The MACD uses a third moving average with a lower period than the first two. This last moving average will give a signal when it crosses the macdline. It is therefore constructed using the values of the macdline as its source.

It's important to note that the first two MAs are constructed using RS values as their source. So we've just built an indicator of an indicator. This kind of method is very powerful because it is rarely used and brings value to the strategy.

PARAMETERS :

RS Length : Relative Strength length i.e. the number of candles back to find the highest high and compare the current price with this high. Default is 300.

MACD Fast Length : Relative Strength fast EMA length used to plot the MACD. Default is 14.

MACD Slow Length : Relative Strength slow EMA length used to plot the MACD. Default is 26.

MACD Signal Smoothing : Macdline SMA length used to plot the MACD. Default is 10.

Max risk per trade (in %) : The maximum loss a trade can incur (in percentage of the trade value). Default is 8%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD in 8h timeframe with the parameters set by default.

ENTER RULES :

The entry rules are very simple : we open a long position when the MACD value turns positive. You are therefore LONG when the MACD is green.

EXIT RULES :

We exit a position (whether losing or winning) when the MACD becomes negative, i.e. turns red.

RISK MANAGEMENT :

This strategy can incur losses, so it's important to manage our risks well. If the position is losing and has incurred a loss of -8%, our stop loss is activated to limit losses.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

Portfolio Backtester Engine█ OVERVIEW

Portfolio Backtester Engine (PBTE). This tool will allow you to backtest strategies across multiple securities at once. Allowing you to easier understand if your strategy is robust. If you are familiar with the PineCoders backtesting engine , then you will find this indicator pleasant to work with as it is an adaptation based on that work. Much of the functionality has been kept the same, or enhanced, with some minor adjustments I made on the account of creating a more subjectively intuitive tool.

█ HISTORY

The original purpose of the backtesting engine (`BTE`) was to bridge the gap between strategies and studies . Previously, strategies did not contain the ability to send alerts, but were necessary for backtesting. Studies on the other hand were necessary for sending alerts, but could not provide backtesting results . Often, traders would have to manage two separate Pine scripts to take advantage of each feature, this was less than ideal.

The `BTE` published by PineCoders offered a solution to this issue by generating backtesting results under the context of a study(). This allowed traders to backtest their strategy and simultaneously generate alerts for automated trading, thus eliminating the need for a separate strategy() script (though, even converting the engine to a strategy was made simple by the PineCoders!).

Fast forward a couple years and PineScript evolved beyond these issues and alerts were introduced into strategies. The BTE was not quite as necessary anymore, but is still extremely useful as it contains extra features and data not found under the strategy() context. Below is an excerpt of features contained by the BTE:

"""

More than `40` built-in strategies,

Customizable components,

Coupling with your own external indicator,

Simple conversion from Study to Strategy modes,

Post-Exit analysis to search for alternate trade outcomes,

Use of the Data Window to show detailed bar by bar trade information and global statistics, including some not provided by TV backtesting,

Plotting of reminders and generation of alerts on in-trade events.

"""

Before I go any further, I want to be clear that the BTE is STILL a good tool and it is STILL very useful. The Portfolio Backtesting Engine I am introducing is only a tangental advancement and not to be confused as a replacement, this tool would not have been possible without the `BTE`.

█ THE PROBLEM

Most strategies built in Pine are limited by one thing. Data. Backtesting should be a rigorous process and researchers should examine the performance of their strategy across all market regimes; that includes, bullish and bearish markets, ranging markets, low volatility and high volatility. Depending on your TV subscription The Pine Engine is limited to 5k-20k historical bars available for backtesting, which can often leave the strategy results wanting. As a general rule of thumb, strategies should be tested across a quantity of historical bars which will allow for at least 100 trades. In many cases, the lack of historical bars available for backtesting and frequency of the strategy signals produces less than 100 trades, rendering your strategy results inconclusive.

█ THE SOLUTION

In order to be confident that we have a robust strategy we must test it across all market regimes and we must have over 100 trades. To do this effectively, researchers can use the Portfolio Backtesting Engine (PBTE).

By testing a strategy across a carefully selected portfolio of securities, researchers can now gather 5k-20k historical bars per security! Currently, the PTBE allows up to 5 securities, which amounts to 25k-100k historical bars.

█ HOW TO USE

1 — Add the indicator to your chart.

• Confirm inputs. These will be the most important initial values which you can change later by clicking the gear icon ⚙ and opening up the settings of the indicator.

2 — Select a portfolio.

• You will want to spend some time carefully selecting a portfolio of securities.

• Each security should be uncorrelated.

• The entire portfolio should contain a mix of different market regimes.

You should understand that strategies generally take advantage of one particular type of market regime. (trending, ranging, low/high volatility)

For example, the default RSI strategy is typically advantageous during ranging markets, whereas a typical moving average crossover strategy is advantageous in trending markets.

If you were to use the standard RSI strategy during a trending market, you might be selling when you should be buying.

Similarily, if you use an SMA crossover during a ranging market, you will find that the MA's may produce many false signals.

Even if you build a strategy that is designed to be used only in a trending market, it is still best to select a portfolio of all market regimes

as you will be able to test how your strategy will perform when the market does something unexpected.

3 — Test a built-in strategy or add your own.

• Navigate to gear icon ⚙ (settings) of strategy.

• Choose your options.

• Select a Main Entry Strat and Alternate Entry Strat .