EMA bands + leledc + bollinger bands trend following strategy v2The basics:

In its simplest form, this strategy is a positional trend following strategy which enters long when price breaks out above "middle" EMA bands and closes or flips short when price breaks down below "middle" EMA bands. The top and bottom of the middle EMA bands are calculated from the EMA of candle highs and lows, respectively.

The idea is that entering trades on breakouts of the high EMAs and low EMAs rather than the typical EMA based on candle closes gives a bit more confirmation of trend strength and minimizes getting chopped up. To further reduce getting chopped up, the strategy defaults to close on crossing the opposite EMA band (ie. long on break above high EMA middle band and close below low EMA middle band).

This strategy works on all markets on all timeframes, but as a trend following strategy it works best on markets prone to trending such as crypto and tech stocks. On lower timeframes, longer EMAs tend to work best (I've found good results on EMA lengths even has high up to 1000), while 4H charts and above tend to work better with EMA lengths 21 and below.

As an added filter to confirm the trend, a second EMA can be used. Inputting a slower EMA filter can ensure trades are entered in accordance with longer term trends, inputting a faster EMA filter can act as confirmation of breakout strength.

Bar coloring can be enabled to quickly visually identify a trend's direction for confluence with other indicators or strategies.

The goods:

Waiting for the trend to flip before closing a trade (especially when a longer base EMA is used) often leaves money on the table. This script combines a number of ways to identify when a trend is exhausted for backtesting the best early exits.

"Delayed bars inside middle bands" - When a number of candle's in a row open and close between the middle EMA bands, it could be a sign the trend is weak, or that the breakout was not the start of a new trend. Selecting this will close out positions after a number of bars has passed

"Leledc bars" - Originally introduced by glaz, this is a price action indicator that highlights a candle after a number of bars in a row close the same direction and result in greatest high/low over a period. It often triggers when a strong trend has paused before further continuation, or it marks the end of a trend. To mitigate closing on false Leledc signals, this strategy has two options: 1. Introducing requirement for increased volume on the Leledc bars can help filter out Leledc signals that happen mid trend. 2. Closing after a number of Leledc bars appear after position opens. These two options work great in isolation but don't perform well together in my testing.

"Bollinger Bands exhaustion bars" - These bars are highlighted when price closes back inside the Bollinger Bands and RSI is within specified overbought/sold zones. The idea is that a trend is overextended when price trades beyond the Bollinger Bands. When price closes back inside the bands it's likely due for mean reversion back to the base EMA in which this strategy will ideally re-enter a position. Since the added RSI requirements often make this indicator too strict to trigger a large enough sample size to backtest, I've found it best to use "non-standard" settings for both the bands and the RSI as seen in the default settings.

"Buy/Sell zones" - Similar to the idea behind using Bollinger Bands exhaustion bars as a closing signal. Instead of calculating off of standard deviations, the Buy/Sell zones are calculated off multiples of the middle EMA bands. When trading beyond these zones and subsequently failing back inside, price may be due for mean reversion back to the base EMA. No RSI filter is used for Buy/Sell zones.

If any early close conditions are selected, it's often worth enabling trade re-entry on "middle EMA band bounce". Instead of waiting for a candle to close back inside the middle EMA bands, this feature will re-enter position on only a wick back into the middle bands as will sometimes happen when the trend is strong.

Any and all of the early close conditions can be combined. Experimenting with these, I've found can result in less net profit but higher win-rates and sharpe ratios as less time is spent in trades.

The deadly:

The trend is your friend. But wouldn't it be nice to catch the trends early? In ranging markets (or when using slower base EMAs in this strategy), waiting for confirmation of a breakout of the EMA bands at best will cause you to miss half the move, at worst will result in getting consistently chopped up. Enabling "counter-trend" trades on this strategy will allow the strategy to enter positions on the opposite side of the EMA bands on either a Leledc bar or Bollinger Bands exhaustion bar. There is a filter requiring either a high/low (for Leledc) or open (for BB bars) outside the selected inner or outer Buy/Sell zone. There are also a number of different close conditions for the counter-trend trades to experiment with and backtest.

There are two ways I've found best to use counter-trend trades

1. Mean reverting scalp trades when a trend is clearly overextended. Selecting from the first 5 counter-trend closing conditions on the dropdown list will usually close the trades out quickly, with less profit but less risk.

2. Trying to catch trends early. Selecting any of the close conditions below the first 5 can cause the strategy to behave as if it's entering into a new trend (from the wrong side).

This feature can be deadly effective in profiting from every move price makes, or deadly to the strategy's PnL if not set correctly. Since counter-trend trades open opposite the middle bands, a stop-loss is recommended to reduce risk. If stop-losses for counter-trend trades are disabled, the strategy will hold a position open often until liquidation in a trending market if th trade is offsides. Note that using a slower base EMA makes counter-trend stop-losses even more necessary as it can reduce the effectiveness of the Buy/Sell zone filter for opening the trades as price can spend a long time trending outside the zones. If faster EMAs (34 and below) are used with "Inner" Buy/Zone filter selected, the first few closing conditions will often trigger almost immediately closing the trade at a loss.

The niche:

I've added a feature to default into longs or shorts. Enabling these with other features (aside from the basic long/short on EMA middle band breakout) tends to break the strategy one way or another. Enabling default long works to simulate trying to acquire more of the asset rather than the base currency. Enabling default short can have positive results for those high FDV, high inflation coins that go down-only for months at a time. Otherwise, I use default short as a hedge for coins that I hold and stake spot. I gain the utility and APR of staking while reducing the risk of holding the underlying asset by maintaining a net neutral position *most* of the time.

Disclaimer:

This script is intended for experimenting and backtesting different strategies around EMA bands. Use this script for your live trading at your own risk. I am a rookie coder, as such there may be errors in the code that cause the strategy to behave not as intended. As far as I can tell it doesn't repaint, but I cannot guarantee that it does not. That being said if there's any question, improvements, or errors you've found, drop a comment below!

在腳本中搜尋"stop loss"

Stochastic Moving AverageHi all,

This Strategy script combines the power of EMAs along with the Stochastic Oscillator in a trend following / continuation manner, along with some cool functionalities.

I designed this script especially for trading altcoins, but it works just as good on Bitcoin itself and on some Forex pairs.

______ SIGNALS ______

The script has 4 mandatory conditions to unlock a trading signal. Find these conditions for a long trade below (works the exact other way round for shorts)

- Fast EMA must be higher than Slow EMA

- Stochastic K% line must be in oversold territory

- Stochastic K% line must cross over Stochastic D% line

- Price as to close between slow EMA and fast EMA

Once all the conditions are true, a trade will start at the opening of the next

______ SETTINGS ______

- Trade Setup:

Here you can choose to trade only longs or shorts and change your Risk:Reward.

You can also decide to adjust your volume per position according to your risk tolerance. With “% of Equity” your stop loss will always be equal to a fixed percentage of your initial capital (will “compound” overtime) and with “$ Amount” your stop loss will always be 'x' amount of the base currency (ex: USD, will not compound)

Stop Loss:

The ATR is used to create a stop loss that matches current volatility. The multiplier corresponds to how many times the ATR stop losses and take profits will be away from closing price.

- Stochastic:

Here you can find the usual K% & D% length and overbought (OB) and oversold (OS) levels.

The “Stochastic OB/OS lookback” increase the tolerance towards OB/OS territories. It allows to look 'x' bars back for a value of the Stochastic K line to be overbought or oversold when detecting an entry signal.

The “All must be OB/OS” refers to the previous “Stochastic OB/OS lookback” parameter. If this option is ticked, instead of needing only 1 OB/OS value within the lookback period to get a valid signal, now, all bars looked back must be OB/OS.

The color gradient drawn between the fast and slow EMAs is a representation of the Stochastic K% line position. With default setting colors, when fast EMA > slow EMA, gradient will become solid blue when Stochastic is oversold and when slow EMA > fast EMA, gradient will become solid blue when Stochastic is overbought

- EMAs:

Just pick your favorite ones

- Reference Market:

An additional filter to be certain to stay aligned with the current a market index trend (in our case: Bitcoin). If selected reference market (and timeframe) is trading above selected EMA, this strategy will only take long trades (vice-versa for shorts) Because, let’s face it… even if this filter isn’t bulletproof, you know for sure that when Bitcoin tanks, there won’t be many Alts going north simultaneously. Once again, this is a trend following strategy.

A few tips for increased performance: fast EMA and D% Line can be real fast… 😉

As always, my scripts evolve greatly with your ideas and suggestions, keep them coming! I will gladly incorporate more functionalities as I go.

All my script are tradable when published but remain work in progress, looking for further improvements.

Hope you like it!

Bounce Manager ATRThis is a tool to turn any line or indicator into a signaller from bounces from the source line.

The ATR version is build to specify what would be considered a worthy entry from the line using ATR multiplier values as inputs.

COMPONENTS:

- Max violation: When price moves past this the script will no longer look for entry until a new trend has been established. The line can also be used as a stop loss.

- Confirmation line: When price touches the line during a trend it

will wait to cross over this line to confirm a reaction from the line.

- Min past distance: A trend filtering system, this is a distance from

the line price has to break to confirm trend direction.

- Stop loss: This can be set to a percentage distance from the low after

bounce. Or it can be set to the max violation line

- Take profit: This can be a fixed take profit target or a risk to reward

based take profit. With risk to reward it will multiply the stop loss

distance by the input and use that to create target (green cross)

- ATR based or % based: there are 2 versions of the script, one for strict

percentage based logic and another one based on ATR values

In bounce manager v1 these stop loss and take profit targets are there only for plotting and visual backtesting purposes. Right now it can only send long and short signals.

Part of the Honest Algo service.

3 Candle Strike SPY Option StrategyImportant notes:

1. This strategy is designed for same day SPY option scalping. All profit shown in back testing report is based on Profit/Loss (P/L) estimates from trading options with approximately 7.5 weeks of data. By default, it is set to 10 option contracts. By default the initial capital is set to $5000.

2. This strategy also takes into account of extended market data, so turn it on for it to work as intended.

3. This strategy is mainly developed for SPY trading on 1 min chart, it probably will not work with other tickers without tweaking all the parameters first.

4. At the time of publish, the market is experiencing high volatility. Keep that in mind as market conditions changes constantly.

How it works:

Basic idea of this strategy is to look for 3 candle reversal pattern within trending market structure. The 3 candle reversal pattern consist of 3 consecutive bullish or bearish candles, followed by an engulfing candle in the opposite direction. This pattern usually signals a reversal of short term trend (a.k.a pullbacks). This strategy uses multiple moving averages to filter long or short entries. For example, if the 21 smoothed moving average is above the 50, only look for long (bullish) entries, and vise versa. There are settings to change these moving average periods to suit your needs. Linear Regression to determine whether the market is trending. The 3 candle pattern is more successful under trending market.

This strategy aims for approximately 1:3 risk to reward ratio. Stop losses are calculated using the closest low or high values for long or short entries, respectively, with an offset using a percentage of the daily ATR value. This allows some price fluctuation without being stopped out prematurely. Price target is calculated by multiplying the difference between the entry price and the stop loss by a factor of 3. When price target is reach, this strategy will set stop loss at the price target and wait for exit conditions to maximize potential profit.

By default, the strategy signals a trade in the opposite direction if the previous one had resulted in a loss. Often times, this opposite trade results in profit.

This strategy automatically signal to close all trades at 3:50 pm EST at the end of the day.

Enjoy~!!! Let's all make $$$

[Wantrader] Volatility Breakout Strategy V3This is the Wantrader's volatility breakthrough version 9,

which developed Larry Williams' volatility breakthrough strategy.

The following elements are included.

- Entry : Enter the market price, calculated by the volatility (TR) * ratio (K) of the previous day.

- Exit : Based on the selected time frame, closing the closing price, closing the market price,

- Stop loss: When it breaks through the entry price and buys, returns to the market price (the previous day's closing price) and changes to bear candle, stop loss.

- Long/short comparison: When short version is selected, it shows the result of short instead of long.

This strategy is a low-level strategy.

When used in practice, it can be stronger and more compliant than expected, but it is not smart.

I recommend you to develop a more hidden edge and use it as a drawing paper to create your own strategy.

Through the option settings,

I'll check if it's right for my first salary or at different times.

It will be an opportunity to think about why there is a difference in profits between Long and Short.

Also, the result shows the big difference between having and not having a loss.

I hope it will be an opportunity to break the relationship in the future.

========================================================================================

래리윌리엄스의 변동성돌파전략을 발전시킨

원트레이더 변동성돌파 버전3 입니다.

아래 요소가 포함되어있습니다.

- 진입 : 전일변동성(TR) * 비율(K) 로 계산한 진입가에, 시장가 진입

- 청산 : 선택한 타임프레임 기준으로 종가에, 시장가 청산

- 손절 : 진입가 돌파하여 매수 후, 당일 시가(전일 종가)로 돌아와서 음봉으로 바뀔때 손절

- 롱/숏 비교 : 숏버전을 선택하면 롱대신 숏으로만 처리한 결과를 보여줌

본 전략은 레벨이 낮은 전략으로

실전에서 사용 시 생각보다 강건하고 준수할 순 있으나 스마트하진 못합니다.

더 숨겨진 엣지를 개발하여 자신만의 전략을 만들기 위한 도화지 처럼 사용하시길 추천드립니다.

옵션 설정을 통해

일봉에서 잘 맞는지 다른 시간대에서 맞는지 등을 확인하고

롱과 숏의 수익의 차이는 왜 나는 것인지 고민해보는 계기가 될 것입니다.

또한 손절이 있는 것과 없는 것의 큰 차이를 결과로 확인하여

앞으로 반드시 손절을 넣게 되는 계기가 되길 기원합니다.

PeCryptoThe PeCrypto Indicator is a momentum indicator developed by tradewithpecunia. The indicator is made with 5+ robust indicators for the crypto charts. The indicator has been made with the concepts of support and resistance, ascending/ descending channel, flag, and pole pattern & rising/falling wedges with the crossover of 3+ moving averages. Different parameters (mathematical calculations for each) have been set by us for each mentioned concept above. According to the parameter set by us, the indicator detects different trends in the price using 3 different algorithms. With the help of sigma calculations and the use of 4 different slopes the indicator catches momentum at different positions, according to the parameter set, and generates signal using the conjunction of both the above-mentioned rules. We call this a Kayo cum Shelve system because utilizing the concepts it finds the signals and after satisfying the parameters it generates the final signals. This ensures that there is a momentum check and enough buy and sell signals are generated.

Using 4 parameters for upper bound/lower bounds and divergence rules the catch for median points has been done. 7+ & 7- lengths are looked at from the median points where we have put the stop loss.

Note:

If you are using this script, you acknowledge that the past performance is not necessarily the indication of future results and there are many more factors that go into being a profitable trader.

Before you proceed:

We are not SEBI Registered Analysts and shall not be culpable for any loss incurred directly or indirectly. Our indicator is no holy grail system. Investment in the stock market is subject to market risk. Trading in stocks, futures, or options is not suitable for every trader and involves a considerable risk of loss.

The market may fluctuate, and the user always has a risk of loss, thus, we won’t be liable for any losses incurred while using our indicator, our trading ideas, or our approach.

[Joy] Aladdin Long Trading Strategy 1.0.0 AlphaAladdin's Long trading strategy is to test out Aladdin for long trades only

This strategy is mainly used to test whether Aladdin is suitable for a coin/stocks/futures or for any trading. The profitability, average drawdown, average profits, etc are used by me to decide whether to use it for trading.

What is Aladdin and what does it do?

Using the volume and gradual flow of non-interrupted data (wicks and body of the candles), it tries to detect the macro condition of the market so that one may know in which direction the market is flowing.

* Bearish / Sell sign: On the candle's close, I open a short position

* Bullish sign: On the candle's close, I open a long position

* I take at least 50% profit when the indicator indicates to do so. One can configure that value as desired from the configuration depending on one's risk/money management. I might even convert some portion of the position into stable coins.

FAQ

Q: Does it use some EMA /MA/etc.? Does it use any indicator with tweaked settings?

Answer: No.

Q: What does it mostly depend on?

Answer: Volume and gradual flow of non-interrupted data. The logic depends purely on volume , price bars and the wicks.

Q: Does it work with all coins, stocks, futures, instruments?

Answer: I prefer to use the exchange with the best possible data. Then backtest out to find the best possible timeframe, stop loss and target all derived from this script data.

Q: Can you make it free or make it open source?

Answer: There is no free lunch in this world. I will never reveal or share the source code!

Q: Do you provide ongoing support for the indicator?

Answer: Yes, as long as I can, I will continue updating the indicator

Q: Are the bullish /buy & the bearish/sell markers automatic?

Answer: I have no control over the markers. It is driven purely by logic from the script.

Q: Is this financial advice?

Answer: This is not financial advice. I do not guarantee any profit or loss. I am not responsible for any of your losses or profits. My indicators do not assure profit or loss. It also does not auto-open or auto-close a trade.

Assumptions:

Only long trades are opened and closed. No short trades.

Starting Capital: $20,000

Order Size: 20% of Capital

Data used: Whatever data is available from 2011 till today on Trading view

Findings:

INDEX: BTCUSD 83% profitability using 2day tf

54 closed trades

Profit factor: 16

Sortino Ratio: 5.2

Average Winning Trade: 30%

Average Losing Trade: 9.12%

Largest Winning Trade: 1218%

Largest Losing Trade: 20.25%

Below are the profitability rate for the timeframe and the coins listed as found by running the trading strategy over the following as of today (Aug 1st 2021 12:40 pm Sydney Time).

⚜️ INDEX:BTCUSD 83% using 2day tf

⚜️INDEX:ETHUSD 80% using 1day tf

⚜️FTTUSD 81% using 2day tf

⚜️SRMUSD 71% using 1day tf

⚜️ADAUSDT 81% using 2day tf

⚜️ALGOUSD > 90% using 2day tf

⚜️ALTPERP 81% using 2day tf

⚜️AVAXUSDT 75% using 1day tf

⚜️BANDUSD > 90% using 2day tf

⚜️BCHUSD 82% using 2day tf

⚜️BNBUSD 79% using 1day tf

⚜️BNBUSD 85% using 2day tf

⚜️CHZUSD 71% using 1day tf

⚜️COMPUSD 81% using 1day tf

⚜️DOGEUSD 77% using 1day tf

⚜️EXCHPERP 83% using 1day tf

⚜️FILUSD > 90% using 1day tf

⚜️FTMUSD 70% using 2day tf

⚜️HTUSDT 75% using 2day tf

⚜️KINUSD >90% using 2day tf

⚜️LINKPERP 85% using 2day tf

⚜️LTCUSD 80% using 2day tf

⚜️MATICUSD 77% using 2day tf

⚜️NEOUSD 80% using 1day tf

⚜️NEXOUSD > 90% using 1day tf

⚜️OKBUSD 71% using 1day tf

⚜️OMGUSD 75% using 1day tf

⚜️RSRUSD 87% using 1day tf

⚜️RUNEUSD > 90% using 1day tf

⚜️SHITPERP > 90% using 1day tf

⚜️SOLUSD 84% using 1day tf

⚜️SUSHIUSD 71% using 1day tf

⚜️THETAUSD > 90% using 2day tf

⚜️UNIPERP 83% using 1day tf

⚜️VERTPERP > 90% using 1day tf

⚜️XAUUSD 63% using 2day tf

⚜️XTZUSD 83% using 2day tf

⚜️ZECUSD 72% using 2day tf

Disclaimer:

No one knows what will happen in the future. DYOR and decide on your own conditions. Do realize that neither I nor my indicator can guarantee any profit or loss. And there is no assurance that any trade will ever result in any profit. It is not financial advice.

[ADOL_]Trend Break Pro ARVIS BOTENG) Trend Break Pro Version : ARVIS BOT

It automatically draws trend lines and signals signals based on sophisticated standards.

It is an indicator that can be used as a tool for trading. from scalping

It was made as an all-round player that can even use the swing.

It contains all the signals of a breakout of the basic trend line,

By applying a new logic, signals that are faster than the breakout point of the basic trend line and

I made it to produce a better value while catching the signal of the press.

principle)

Basic trendline features:

It reflects the concepts of HH and LL.

Trendlines are created using the basic construction method, connecting highs and highs and lows and lows.

The 3 candles prior to the breakout of the trend line are the triggers to create a ready-to-prepare base signal.

What is HH? It is an abbreviation of Higher High, which means to raise the high.

What is LL? An abbreviation of Lower Low, which means to lower the low.

Features of the new core logic:

This is a quick way to find a reversal of a trend, taking into account candle patterns, volume, and moving averages.

The candle pattern that is reversed when the trading volume increases and then disappears is processed by subdividing and digitizing the pattern.

generate a signal. At the turning point of the trend, it triggers a long and short reversal signal.

For trading volume, obv was utilized. Overlaid elements allow you to find signals that are slightly faster than the trend line.

What is obv? OBV = An abbreviation of On Balance Volume. It is a secondary indicator showing the cumulative total of trading volume.

The background is a notation of the section where the trend is reversing.

option)

The degree of freedom to set options according to scalping, single stroke, swing, and bot implementation is given.

A volatility warning notification has been included. The function of TD setup is included.

You can set the range of candles as an option. The backtesting value is printed.

The backtesting value is calculated as the average of the opening and closing prices.

Volatility warnings are displayed in yellow.

TD Setup: Numbers floating on the candle, in ascending and descending order (=sequence) from 1 to 9.

The reason for writing up to 9 is based on statistics, and the more fundamental principle is the theory of the Fibonacci sequence.

The Fibonacci sequence is the number in the golden ratio that makes up nature, 1.1.2.3.5.8.13.21.34.55.89...

The sum of the nth and n+1th numbers becomes n+2th.

A note on odds of winning. Even if the win rate is 33%, if the profit-loss stop-loss ratio is 3 to 1, the profit exceeds 2, so cumulative profits are generated.

In other words, it is decided by considering both the win rate and profit/loss ratio, not just the win rate. The logic of a short stop loss and a long profit trend is reflected.

time frame)

Applicable to any timeframe.

Scalping: 1 minute, 3 minute, 5 minute / Danta: 15 minute, 1 hour / Swing: 4 hour, daily

Recommended time frame: 3, 15 minutes

alarm)

Various alert functions are available. based on the alert signal

When trading, various signals help to set specific conditions.

- Basic long and short alerts

- Volatility warning alert

- Filtered long and short alerts

- Long and short alerts occur Next peak alerts

- Uptrend line, downtrend line breakout alert

- Alerts about bot start and end when bot is running

- Filtered uptrend line, downtrend line breakout alert

- Alerts for rising and falling 1 setup and rising and falling 9 setups respectively

trading method)

1. For the trend line breakout signal, when the signal overlaps more than 3 times, the breakout probability increases.

It reflects the concept below.

One touch of support/resistance: The first touch sees longs at support and shorts at resistance.

2 touches of support/resistance line: Confirm the position once more in the stage of building support/resistance line (compacting). We see longs at support and shorts at resistance.

3 touches of the ground/resistance line: This is a section with a high possibility of both directions.

Support/resistance line 4 (over) touch: Used as a breakout reference line. When breaking through, short at support and long at resistance.

When the support/resistance line breaks through the closing price, support becomes resistance and resistance becomes support.

2. Trade support/resistance lines using the trend line breakout and signal as an important reference bar.

example)

3-1. Entry criteria/stop loss criteria (when trading hands and bots)

- entry criteria; Follow the signal.

- Stop loss criteria;

Use fixed stop loss: Set 1% fixed stop loss section from signal generation. (% is set individually)

Use Candle Stop Loss: Set a stop loss when the low or high point of the signal generating bar collapses.

Use flow stop loss: Set the stop loss considering the flow of the wave.

3-2. Entry criteria/stop loss criteria (in case of signal-based bot trading)

- Approach with a low magnification (more than 10 times is not recommended) to prevent the risk of liquidation of the largest drop,

There is an opposite signal after entering without setting stop loss separately.

4. Note

You are solely responsible for any trading decisions you make.

5. How to use

It is set to be available only to invited users. When invited,

Tap Add Indicator to Favorites at the bottom of the indicator.

If you click the indicator at the top of the chart screen and look at the left tab, there is a Favorites tab.

Add an indicator by clicking the indicator name in the Favorites tab.

KOR) Trend Break Pro버전 : ARVIS BOT ; 아비스 봇 입니다.

추세선을 자동으로 작도해주며, 정교화된 기준으로 시그널을

발생시켜 매매에 도구로써 활용가능한 지표입니다. 스캘핑부터

스윙까지 활용가능한 올라운드 플레이어로 만들어졌습니다.

기본 추세선 돌파의 시그널들을 모두 포함하고 있으며,

새로운 로직을 적용하여 기본 추세선 돌파시점보다 빠른 신호와

눌림의 신호까지 잡아내면서, 더 나은 값을 산출하도록 만들었습니다.

원리)

기본 추세선 기능 :

HH와 LL의 개념을 반영합니다.

추세선은 고점과 고점, 저점과 저점을 잇는 기본 작도 방법으로 만들어집니다.

추세선 돌파의 3개 이전 캔들부터 신호발생으로 준비를 기본 시그널을 만듭니다.

HH란 ? Higher High의 약자로 고점을 높인다는 의미입니다.

LL란? Lower Low의 약자로 저점을 낮춘다는 의미입니다.

새로운 핵심적인 로직의 기능 :

추세의 반전을 빠르게 찾기 위한 방법으로 캔들패턴, 거래량, 이평선을 고려하여 만들어졌습니다.

거래량이 증가하다가 소멸하는 시점에서 반전되는 캔들패턴을 세분화하고 수치화하여 가공된

신호를 발생시킵니다. 추세의 전환자리에서 롱과 숏의 전환 신호를 발생시키도록 합니다.

거래량에는 obv가 활용되었습니다. 중첩된 요소들을 통해 추세선보다 조금 더 빠른 신호를 찾을 수 있습니다.

obv란 ? OBV = On Blance Volume의 약자로 거래량의 누적합계를 나타내는 보조지표 입니다.

배경은 추세가 전환되는 구간의 표기입니다.

옵션)

스캘핑과 단타, 스윙, 봇의 구현에 맞게 옵션을 설정할 수 있는 자유도를 부여하였습니다.

변동성 경고 알림이 포함되었습니다. TD셋업의 기능이 포함되었습니다.

캔들의 범위를 옵션으로 설정할 수 있습니다. 백테스팅 값이 출력됩니다.

백테스팅 값은 시가와 종가의 평균값으로 산출됩니다.

변동성경고는 yellow 컬러로 표기됩니다.

TD셋업 : 캔들위에 플로팅 되는 숫자로 1~9까지의 오름차순, 내림차순 (=시퀀스)으로 구성됩니다.

9까지 쓰는 이유는 통계기반, 좀 더 근본적인 원리는 피보나치 수열의 이론이 반영되어 있습니다.

피보나치 수열이란 자연을 이루는 황금비율의 숫자로 1.1.2.3.5.8.13.21.34.55.89...

n번째와 n+1번째 숫자의 합이 n+2번째가 됩니다.

원리 예시)

승률에 관한 참고사항. 승률이 33퍼센트의 승률이어도 3대 1의 익절 손절 비율이면 이익이 2를 넘어가니까 누적수익이 발생합니다.

즉, 승률과 손익비를 모두 고려해서 결정하는 것이지, 승률만 봐서는 안됩니다.

손절은 짧게, 수익은 추세대로 길게의 로직이 반영되어 있습니다.

타임프레임)

모든 시간프레임에 적용 가능합니다.

스캘핑 : 1분봉, 3분봉, 5분봉 / 단타 : 15분봉, 1시간봉 / 스윙 : 4시간봉, 일봉

추천타임프레임 : 3, 15분봉

5분봉)

15분봉)

4시간봉)

알람)

다양한 얼러트 기능을 사용할 수 있습니다. 얼러트 신호를 기반으로

매매시 다양한 신호는 구체적 조건 설정에 도움이 됩니다.

- 기본 롱,숏 얼러트

- 변동성 경고 얼러트

- 필터링된 롱,숏 얼러트

- 롱,숏 얼러트 발생 다음봉 얼러트

- 상승추세선, 하락추세선 돌파 얼러트

- 봇구동시 봇의 시작과 종료에 관한 얼러트

- 필터링된 상승추세선, 하락추세선 돌파 얼러트

- 상승,하락1셋업과 상승,하락9셋업 각각에 대한 얼러트

매매방법)

1. 추세선 돌파신호는 신호가 3번이상 중첩될시 돌파확률이 상승합니다.

아래 개념을 반영합니다.

지지/저항선 1터치 : 첫번째 터치에는 지지선에서 롱을, 저항선에서 숏을 봅니다.

지지/저항선 2터치 : 지지/저항선 구축(다지기)의 단계로 한번 더 자리를 확인합니다. 지지선에서 롱을, 저항선에서 숏을 봅니다.

지/저항선의 3터치 : 양방향의 가능성이 높은 구간입니다.

지지/저항선4(이상)터치 : 돌파기준선으로 사용합니다. 돌파할 때, 지지선에서 숏을, 저항선에서 롱을 칩니다.

지지/저항선이 종가로 뚫리면 지지는 저항이 되고, 저항은 지지가 됩니다.

2. 추세선돌파와 시그널이 발생한 봉을 중요한 기준봉으로 활용하여 지지/저항선 매매를 합니다.

예시)

3-1. 진입기준/손절기준(손,봇 매매시)

- 진입기준; 시그널을 따릅니다.

- 손절기준;

고정손절가 이용 : 시그널 발생으로부터 1% 고정 손절가 구간을 설정합니다.(%는 개별로 설정)

캔들손절가 이용 : 시그널 발생봉의 저점이나 고점이 무너지면 손절을 설정합니다.

흐름손절가 이용 : 파동의 흐름을 고려하여 손절을 설정합니다.

3-2. 진입기준/손절기준(신호기반 봇 매매시)

- 저배율(10배이상은 권장하지 않습니다)로 접근해 최대낙폭의 청산위험을 예방하며,

손절가를 따로 설정하지 않고 진입후 반대신호가 뜰때마다 스위칭을 합니다.

4. 참고

귀하가 내리는 모든 거래 결정은 전적으로 귀하의 책임입니다.

5. 사용방법

초대된 사용자만 사용할 수 있도록 설정이 되어있습니다. 초대를 받을 경우,

지표 하단의 즐겨찾기에 인디케이터 넣기를 누릅니다.

차트화면 상단에 지표를 눌러서 왼쪽탭에 보면 즐겨찾기 탭이 있습니다.

즐겨찾기 탭에서 지표이름을 눌러서 지표를 추가합니다.

Breakout Trend Trading Strategy - V1Strategy in nutshell:

This strategy is made to be used in daily time-frames. Works better on trending instruments where volume is available. Hence, this is more suitable for trending shares rather than currencies, commodities and indexes where volume data is either not present or not reliable.

Breakout signifies the continuation of trend. Hence, trade in the direction of breakouts. Breakouts are calculated based on high volume and price movement in a day. This will be combined with few other conditions to generate buy and sell signals along with stop and compound targets. Supertrend is used for trend bias. Our buy and sell targets do not directly depend on the bias. But, entry criteria in opposite trend is made much difficult than that of trend direction. Further explanation of method and input parameters are explained below.

Backtesting parameters :

Capital and position sizing : Capital and position sizing parameters are set to test investing 2000 wholly on certain stock without compounding.

Initial Capital : 2000

Order Size : 100% of equity

Pyramiding : 1

ExitOnSignal : If unchecked exit is triggered solely on trailing stop

Trade Direction : Long, Short or All. Short condition is riskier than long conditions and often results in losses as per my observation. On most of the stocks trending up, strategy will not generate any short signals. This is achieved by comparing yearly high lows to previous two years to decide whether to allow short or long entries.

allowImmediateCompound : Applicable only if compounding/pyramiding is enabled in trade. If checked allows to place compounding orders immediately. If unchecked, it waits for stopline to cross order price before placing next compound.

Display Mode :

Targets : Whenever breakout happens, show marker for upTarget and downTarget

TargetChannel : Show up target and downtarget as a channel

Target With Stop : Along with targets, show also stop levels for breakouts

Up Channel : Channel created from UpTarget and respective stops

Down Channel : Channel created from DownTarget and respective stops

ShowTrailingStop : Shows trailing stop and compound lines when there is a trading position.

ShowTargetLevels : Shows Buy Sell target levels along with stop and compound lines. Trades are done as market orders. Hence, target levels are displayed after strategy makes the trade. Since only one order allowed per side without compounding, target, stop and compound levels are shown sometimes even without trade being made. These can be considered as entry levels if there is no existing position.

ShowPreviousLevels : Shows previous buy/sell target levels. When enabled, layout can look messy.

StopMultiplyer: To Set trailing stop loss.

BacktestYears: Number of years to include in backtest

So far my test cases are:

Positive : AAPL, AMZN, TSLA, RUN, VRT, ASX:APT

Negative Test Cases: WPL, WHC, NHC, WOW, COL, NAB (All ASX stocks)

Special test case: WDI

Negative test cases still show losses in backtesting. I have attempted including many conditions to eliminate or reduce the loss. But, further efforts has resulted in reduction in profits in positive cases as well. Still experimenting. Will update whenever I find improvements. Comments and suggestions welcome :)

Tweezer Top & Tweezer Bottom Pattern (Expo)Tweezer Top/Bottom Pattern (Expo) indicator identifies real-time Tweezer Top and Tweezer Bottom in any market and in any timeframe. This is an enhanced version of the pattern which enables higher accuracy, and noise filtering. In addition to that, Tweezer Levels can be displayed which can be used in many different ways, for instance, as a stop loss level, or to confirm the signal.

The ideal Tweezer pattern includes that the wicks should be 100% the same length. However, that rarely happens. So in this enhanced version, the user can set the maximum change that is allowed between the wicks.

To enhance the signal accuracy a Bullish engulfing and Bearish engulfing filter can be toggled on. So a signal will only be displayed if an engulfing candle is in play.

HOW TO USE

Tweezer Top/Bottom should be used together with KEY market levels or with KEY supply/demand zones.

Enter Long: if a Tweezer Bottom signal occurs at a KEY Level or on a KEY supply/demand zone.

Target: The first target should be the nearest resistance level or supply zone. The second target should be the next resistance level or supply zone, and so on.

Enter Short: if a Tweezer Top signal occurs at a KEY Level or on a KEY supply/demand zone.

Target: The first target should be the nearest support level or demand zone. The second target should be the next support level or demand zone, and so on.

Stop Loss: The Tweezer levels can be used as a stop loss.

Remember: Use the indicator together with KEY levels or KEY Supply/Demand Zones.

INDICATOR IN ACTION

4 Hour chart

I hope you find this indicator useful , and please comment or contact me if you like the script or have any questions/suggestions for future improvements. Thanks!

I will continually work on this indicator, so please share your experience and feedback as it will enable me to make even better improvements. Thanks to everyone that has already contacted me regarding my scripts. Your feedback is valuable for future developments!

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My scripts/indicators/ideas are only for educational purposes!

-----------------

ACCESS THE INDICATOR

• Contact me on TradingView or use the links below

Grid Like StrategyIt is possible to use progressive position sizing in order to recover from past losses, a well-known position sizing system being the "martingale", which consists of doubling your position size after a loss, this allows you to recover any previous losses in a losing streak + winning an extra. This system has seen a lot of attention from the trading community (mostly from beginners), and many strategies have been designed around the martingale, one of them being "grid trading strategies".

While such strategies often shows promising results on paper, they are often subjects to many frictions during live trading that makes them totally unusable and dangerous to the trader. The motivations behind posting such a strategy isn't to glorify such systems, but rather to present the problems behind them, many users come to me with their ideas and glorious ways to make money, sometimes they present strategies using the martingale, and it is important to present the flaws of this methodology rather than blindly saying "you shouldn't use it".

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the symbol you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, as such higher values will generate fewer trades.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after any wins.

The Grid

Grid strategies are commons and do not present huge problems until we use certain position sizing methods such as the martingale. A martingale is extremely sensitive to any kind of friction (frictional costs, slippage...etc), the grid strategy aims to provide a stable and simple environment where a martingale might possibly behave well.

The goal of a simple grid strategy is to go long once the price crossover a certain level, a take profit is set at the level above the current one and stop loss is placed at the level below the current one, in a winning scenario the price reach the take profit, the position is closed and a new one is opened with the same setup. In a losing scenario, the price reaches the stop loss level, the position is closed and a short one is opened, the take profit is set at the level below the current one, and a stop loss is set at the level above the current one. Note that all levels are equally spaced.

It follows from this strategy that wins and losses should be constant over time, as such our balance would evolve in a linear fashion. This is a great setup for a martingale, as we are theoretically assured to recover all the looses in a losing streak.

Martingale - Exponential Decays - Risk/Reward

By using a martingale we double our position size (exposure) each time we lose a trade, if we look at our balance when using a martingale we see significant drawdowns, with our balance peaking down significantly. The martingale sequence is subject to exponential growth, as such using a martingale makes our balance exposed to exponential decays, that's really bad, we could basically lose all the initially invested capital in a short amount of time, it follows from this that the theoretical success of a martingale is determined by what is the maximum losing streak you can endure

Now consider how a martingale affects our risk-reward ratio, assuming unity position sizing our martingale sequence can be described by 2^(x-1) , using this formula we would get the amount of shares/contracts we need to purchase at the x trade of a losing streak, we would need to purchase 256 contracts in order to recover from a losing streak of size 9, this is enormous when you take into account that your wins are way smaller, the risk-reward ratio is totally unfair.

Of course, some users might think that a losing streak of size 9 is pretty unlikely, if the probability of winning and losing are both equal to 0.5, then the probability of 9 consecutive losses is equal to 0.5^9 , there are approximately 0.2% of chance of having such large losing streak, note however that under a ranging market such case scenario could happen, but we will see later that the length of a losing streak is not the only problem.

Other Problems

Having a capital large enough to tank 9any number of consecutive losses is not the only thing one should focus on, as we have to take into account market prices and trading dynamics, that's where the ugly part start.

Our first problem is frictional costs, one example being the spread, but this is a common problem for any strategy, however here a martingale is extra sensitive to it, if the strategy does not account for it then we will still double our positions costs but we might not recover all the losses of a losing streak, instead we would be recovering only a proportion of it, under such scenario you would be certain to lose over time.

Another problem are gaps, market price might open under a stop-loss without triggering it, and this is a big no-no.

Equity of the strategy on AMD, in a desired scenario the equity at the second arrow should have been at a higher position than the equity at the first arrow.

In order for the strategy to be more effective, we would need to trade a market that does not close, such as the cryptocurrency market. Finally, we might be affected by slippage, altho only extreme values might drastically affect our balance.

The Anti Martingale

The strategy lets you use an anti-martingale, which double the position size after a win instead of a loss, the goal here is not to recover from a losing strike but instead to profit from a potential winning streak.

Here we are exposing your balance to exponential gross but you might also lose a trade at the end a winning streak, you will generally want to reinitialize your position size after a few wins instead of waiting for the end of a streak.

Alternative

You can use other-kind of progressions for position sizing, such as a linear one, increasing your position size by a constant number each time you lose. More gentle progressions will recover a proportion of your losses in a losing streak.

You can also simulate the effect of a martingale without doubling your position size by doubling your target profit, if for example you have a 10$ profit-target/stop-loss and lose a trade, you can use a 20$ profit target to recover from the lost trade + gain a profit of 10$. While this approach does not introduce exponential decay in your balance, you are betting on the market reaching your take profits, considering the fact that you are doubling their size you are expecting market volatility to increase drastically over time, as such this approach would not be extremely effective for high losing streak.

Conclusion

You will see a lot of auto-trading strategies that are based on a grid approach, they might even use a martingale. While the backtests will look appealing, you should think twice before using such kind of strategy, remember that frictional costs will be a huge challenge for the strategy, and that it assumes that the trader has an important initial capital. We have also seen that the risk/reward ratio is theoretically the worst you can have on a strategy, having a low reward and a high risk. This does not mean that progressive position sizing is bad, but it should not be pushed to the extreme.

It is nice to note that the martingale is originally a betting system designed for casino games, which unlike trading are not subject to frictional costs, but even casino players don't use it, so why would you?

Thx for reading

Two Take Profit StrategyThis script is for research purposes only. I am not a financial advisor.

Entry Condition

This strategy is based on two take profit targets and scaling out strategy. The entry rule is very simple. Whenever the EMA crossover WMA, the long trade is taken and vice versa.

Take Profit and Stop Loss

The first take profit is set at 20 pips above the long entry and the second take profit is set at 40 pips above the long entry. Meanwhile, the stop loss is set at 20 pips below the long entry.

Money Management

When the first take profit is achieved, half of the position is closed. The rest of the position is open to achieve either second take profit or stop loss.

There are three outcomes when using this strategy. Let's say you enter the trade with 200 lot size and you are risking 2% of your equity.

1. The first outcome is when the price hits stop loss, you lose the entire 2%.

2. The second outcome is when the price hits the first take profit and you close half of your position. Meaning that you have gained 1%. Then you let the trade running and eventually it hits stop loss. The total loss is 0% because the remaining lot size which is 200/2=100 times by 20pips is 1%. You have gained the earlier 1% and then loss 1%. At this point, you are at break even.

3. The third outcome is similar to the second out but instead of hiring stop loss, the trade is running to your favor and hits the second take profit.

Therefore, you gained 1% from the first take profit and you gained another 2% for the second take profit. Your total gained is 3%

Summary

The reason behind this strategy is to minimize risk. with normal strategy, you only have two outcomes which are either win or loss. With this strategy, you have three outcomes which are win, loss or break even.

Gandulfas Trading SuiteAn indicator designed to quickly and easily enter you trades, with all the information you need in just one chart!

It uses a combination of :

Price action to have a Weekly BIAS

Volatility channels to track dynamic points of support/resistance

A momentum indicator on the background to point out when the pair is in "overbought/oversold" status - adds confluence to our entries.

Volatility pivots based on the Average Daily Range, to quickly manage your entries and stop losses - more confluence!

How to use this system?

First, we use the price action lines to define a weekly bias. If the price moves above this anchor, then we are looking for buying oportunities on retracements. If the price moves below this anchor, then we look for seling oportunities on retracements.

Now that we have a Weekly BIAS, we know that for this week we are currently looking for buying oportunities. Then, we can use the Volatility Channel to look for buying oportunities. Optimal entries are found within the channels and clouds!.

We should always look for a confluence of factors before entering any trade , and for that we decided to also add to the system a momentum indicator . This also can act as an early warning, telling us a that a potential setup is coming our way.

Does it repaint? No. The system is designed this way to reduce confirmation bias and keep your emotions at bay. For example, if you see the momentum indicator , maybe it is close to your threshold but it did not crossed over or crossed under it. Maybe it's 35, when your threshold is 25. It is low indeed , but it has not crossed it. Fact is this will get you emotional, and perhaps make you trigger a trade before you should.

So for this reason we decided to add the momentum indicator just showing the triangles when indeed the threshold has been crossed, so you don't get emotional trying to enter a trade too early. For this reason, you should always wait to the candle to close, to see if indeed we have crossed that threshold.

And then we have our volatility pivots , that help us to define better entries, targets and stop losses. They are based on the Average Daily Range, and it's use is pretty much straigthforward. The notion of this system is to take entries in the weekly direction. So, what we are really trying to achieve here is to get a chunk of that weekly expansion . The fastest the better, as having a positions means having exposure to the market. To achieve this objective the daily range helps us a lot.

If we are looking for a bullish day, that means we are looking for an good expansion of the Open-High range. So the daily range helps us to see how many pips this range could be on any given day. Then we apply a correction factor , because we do not want to estimate the whole range, we are good to go if we could anticipate just a 60% of it, let's say.

And it also helps us to define our stop loss places, because the range also tell us when it is most probable that our trading idea was wrong. Because if we are looking for a bullish day, we expect a good expansion on the open-high, not on the open-low!. So it also makes sense to take a look on the level that makes our idea most probably wrong!.

Here you can see how these pivots helps us to add extra confluence to our trading idea.

Our best trades are then performed....

Wednesday on the chart is the perfect example of the best type of trade you could perform. You have price entering the volatility channel, with the momentum indicator in our oversold zone, and price just a bit above our ADR pivots!.

Where should you put your targets?

You can use the volatility channel, and or also the pivots as we just described!

Where should you put your stop loss?

Below the volatility channel, taking into account where the pivots are. Because remember, if price trades below those, it most likely means that your idea was wrong, and you should not keep the trade open.

If you want to test or use this trading system on a regular basis, please get in touch with us through the private chat!

T3 ATR [DCAUT]█ T3 ATR

📊 ORIGINALITY & INNOVATION

The T3 ATR indicator represents an important enhancement to the traditional Average True Range (ATR) indicator by incorporating the T3 (Tilson Triple Exponential Moving Average) smoothing algorithm. While standard ATR uses fixed RMA (Running Moving Average) smoothing, T3 ATR introduces a configurable volume factor parameter that allows traders to adjust the smoothing characteristics from highly responsive to heavily smoothed output.

This innovation addresses a fundamental limitation of traditional ATR: the inability to adapt smoothing behavior without changing the calculation period. With T3 ATR, traders can maintain a consistent ATR period while adjusting the responsiveness through the volume factor, making the indicator adaptable to different trading styles, market conditions, and timeframes through a single unified implementation.

The T3 algorithm's triple exponential smoothing with volume factor control provides improved signal quality by reducing noise while maintaining better responsiveness compared to traditional smoothing methods. This makes T3 ATR particularly valuable for traders who need to adapt their volatility measurement approach to varying market conditions without switching between multiple indicator configurations.

📐 MATHEMATICAL FOUNDATION

The T3 ATR calculation process involves two distinct stages:

Stage 1: True Range Calculation

The True Range (TR) is calculated using the standard formula:

TR = max(high - low, |high - close |, |low - close |)

This captures the greatest of the current bar's range, the gap from the previous close to the current high, or the gap from the previous close to the current low, providing a comprehensive measure of price movement that accounts for gaps and limit moves.

Stage 2: T3 Smoothing Application

The True Range values are then smoothed using the T3 algorithm, which applies six exponential moving averages in succession:

First Layer: e1 = EMA(TR, period), e2 = EMA(e1, period)

Second Layer: e3 = EMA(e2, period), e4 = EMA(e3, period)

Third Layer: e5 = EMA(e4, period), e6 = EMA(e5, period)

Final Calculation: T3 = c1×e6 + c2×e5 + c3×e4 + c4×e3

The coefficients (c1, c2, c3, c4) are derived from the volume factor (VF) parameter:

a = VF / 2

c1 = -a³

c2 = 3a² + 3a³

c3 = -6a² - 3a - 3a³

c4 = 1 + 3a + a³ + 3a²

The volume factor parameter (0.0 to 1.0) controls the weighting of these coefficients, directly affecting the balance between responsiveness and smoothness:

Lower VF values (approaching 0.0): Coefficients favor recent data, resulting in faster response to volatility changes with minimal lag but potentially more noise

Higher VF values (approaching 1.0): Coefficients distribute weight more evenly across the smoothing layers, producing smoother output with reduced noise but slightly increased lag

📊 COMPREHENSIVE SIGNAL ANALYSIS

Volatility Level Interpretation:

High Absolute Values: Indicate strong price movements and elevated market activity, suggesting larger position risks and wider stop-loss requirements, often associated with trending markets or significant news events

Low Absolute Values: Indicate subdued price movements and quiet market conditions, suggesting smaller position risks and tighter stop-loss opportunities, often associated with consolidation phases or low-volume periods

Rapid Increases: Sharp spikes in T3 ATR often signal the beginning of significant price moves or market regime changes, providing early warning of increased trading risk

Sustained High Levels: Extended periods of elevated T3 ATR indicate sustained trending conditions with persistent volatility, suitable for trend-following strategies

Sustained Low Levels: Extended periods of low T3 ATR indicate range-bound conditions with suppressed volatility, suitable for mean-reversion strategies

Volume Factor Impact on Signals:

Low VF Settings (0.0-0.3): Produce responsive signals that quickly capture volatility changes, suitable for short-term trading but may generate more frequent color changes during minor fluctuations

Medium VF Settings (0.4-0.7): Provide balanced signal quality with moderate responsiveness, filtering out minor noise while capturing significant volatility changes, suitable for swing trading

High VF Settings (0.8-1.0): Generate smooth, stable signals that filter out most noise and focus on major volatility trends, suitable for position trading and long-term analysis

🎯 STRATEGIC APPLICATIONS

Position Sizing Strategy:

Determine your risk per trade (e.g., 1% of account capital - adjust based on your risk tolerance and experience)

Decide your stop-loss distance multiplier (e.g., 2.0x T3 ATR - this varies by market and strategy, test different values)

Calculate stop-loss distance: Stop Distance = Multiplier × Current T3 ATR

Calculate position size: Position Size = (Account × Risk %) / Stop Distance

Example: $10,000 account, 1% risk, T3 ATR = 50 points, 2x multiplier → Position Size = ($10,000 × 0.01) / (2 × 50) = $100 / 100 points = 1 unit per point

Important: The ATR multiplier (1.5x - 3.0x) should be determined through backtesting for your specific instrument and strategy - using inappropriate multipliers may result in stops that are too tight (frequent stop-outs) or too wide (excessive losses)

Adjust the volume factor to match your trading style: lower VF for responsive stop distances in short-term trading, higher VF for stable stop distances in position trading

Dynamic Stop-Loss Placement:

Determine your risk tolerance multiplier (typically 1.5x to 3.0x T3 ATR)

For long positions: Set stop-loss at entry price minus (multiplier × current T3 ATR value)

For short positions: Set stop-loss at entry price plus (multiplier × current T3 ATR value)

Trail stop-losses by recalculating based on current T3 ATR as the trade progresses

Adjust the volume factor based on desired stop-loss stability: higher VF for less frequent adjustments, lower VF for more adaptive stops

Market Regime Identification:

Calculate a reference volatility level using a longer-period moving average of T3 ATR (e.g., 50-period SMA)

High Volatility Regime: Current T3 ATR significantly above reference (e.g., 120%+) - favor trend-following strategies, breakout trades, and wider targets

Normal Volatility Regime: Current T3 ATR near reference (e.g., 80-120%) - employ standard trading strategies appropriate for prevailing market structure

Low Volatility Regime: Current T3 ATR significantly below reference (e.g., <80%) - favor mean-reversion strategies, range trading, and prepare for potential volatility expansion

Monitor T3 ATR trend direction and compare current values to recent history to identify regime transitions early

Risk Management Implementation:

Establish your maximum portfolio heat (total risk across all positions, typically 2-6% of capital)

For each position: Calculate position size using the formula Position Size = (Account × Individual Risk %) / (ATR Multiplier × Current T3 ATR)

When T3 ATR increases: Position sizes automatically decrease (same risk %, larger stop distance = smaller position)

When T3 ATR decreases: Position sizes automatically increase (same risk %, smaller stop distance = larger position)

This approach maintains constant dollar risk per trade regardless of market volatility changes

Use consistent volume factor settings across all positions to ensure uniform risk measurement

📋 DETAILED PARAMETER CONFIGURATION

ATR Length Parameter:

Default Setting: 14 periods

This is the standard ATR calculation period established by Welles Wilder, providing balanced volatility measurement that captures both short-term fluctuations and medium-term trends across most markets and timeframes

Selection Principles:

Shorter periods increase sensitivity to recent volatility changes and respond faster to market shifts, but may produce less stable readings

Longer periods emphasize sustained volatility trends and filter out short-term noise, but respond more slowly to genuine regime changes

The optimal period depends on your holding time, trading frequency, and the typical volatility cycle of your instrument

Consider the timeframe you trade: Intraday traders typically use shorter periods, swing traders use intermediate periods, position traders use longer periods

Practical Approach:

Start with the default 14 periods and observe how well it captures volatility patterns relevant to your trading decisions

If ATR seems too reactive to minor price movements: Increase the period until volatility readings better reflect meaningful market changes

If ATR lags behind obvious volatility shifts that affect your trades: Decrease the period for faster response

Match the period roughly to your typical holding time - if you hold positions for N bars, consider ATR periods in a similar range

Test different periods using historical data for your specific instrument and strategy before committing to live trading

T3 Volume Factor Parameter:

Default Setting: 0.7

This setting provides a reasonable balance between responsiveness and smoothness for most market conditions and trading styles

Understanding the Volume Factor:

Lower values (closer to 0.0) reduce smoothing, allowing T3 ATR to respond more quickly to volatility changes but with less noise filtering

Higher values (closer to 1.0) increase smoothing, producing more stable readings that focus on sustained volatility trends but respond more slowly

The trade-off is between immediacy and stability - there is no universally optimal setting

Selection Principles:

Match to your decision speed: If you need to react quickly to volatility changes for entries/exits, use lower VF; if you're making longer-term risk assessments, use higher VF

Match to market character: Noisier, choppier markets may benefit from higher VF for clearer signals; cleaner trending markets may work well with lower VF for faster response

Match to your preference: Some traders prefer responsive indicators even with occasional false signals, others prefer stable indicators even with some delay

Practical Adjustment Guidelines:

Start with default 0.7 and observe how T3 ATR behavior aligns with your trading needs over multiple sessions

If readings seem too unstable or noisy for your decisions: Try increasing VF toward 0.9-1.0 for heavier smoothing

If the indicator lags too much behind volatility changes you care about: Try decreasing VF toward 0.3-0.5 for faster response

Make meaningful adjustments (0.2-0.3 changes) rather than small increments - subtle differences are often imperceptible in practice

Test adjustments in simulation or paper trading before applying to live positions

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Responsiveness Characteristics:

The T3 smoothing algorithm provides improved responsiveness compared to traditional RMA smoothing used in standard ATR. The triple exponential design with volume factor control allows the indicator to respond more quickly to genuine volatility changes while maintaining the ability to filter noise through appropriate VF settings. This results in earlier detection of volatility regime changes compared to standard ATR, particularly valuable for risk management and position sizing adjustments.

Signal Stability:

Unlike simple smoothing methods that may produce erratic signals during transitional periods, T3 ATR's multi-layer exponential smoothing provides more stable signal progression. The volume factor parameter allows traders to tune signal stability to their preference, with higher VF settings producing remarkably smooth volatility profiles that help avoid overreaction to temporary market fluctuations.

Comparison with Standard ATR:

Adaptability: T3 ATR allows adjustment of smoothing characteristics through the volume factor without changing the ATR period, whereas standard ATR requires changing the period length to alter responsiveness, potentially affecting the fundamental volatility measurement

Lag Reduction: At lower volume factor settings, T3 ATR responds more quickly to volatility changes than standard ATR with equivalent periods, providing earlier signals for risk management adjustments

Noise Filtering: At higher volume factor settings, T3 ATR provides superior noise filtering compared to standard ATR, producing cleaner signals for long-term analysis without sacrificing volatility measurement accuracy

Flexibility: A single T3 ATR configuration can serve multiple trading styles by adjusting only the volume factor, while standard ATR typically requires multiple instances with different periods for different trading applications

Suitable Use Cases:

T3 ATR is well-suited for the following scenarios:

Dynamic Risk Management: When position sizing and stop-loss placement need to adapt quickly to changing volatility conditions

Multi-Style Trading: When a single volatility indicator must serve different trading approaches (day trading, swing trading, position trading)

Volatile Markets: When standard ATR produces too many false volatility signals during choppy conditions

Systematic Trading: When algorithmic systems require a single, configurable volatility input that can be optimized for different instruments

Market Regime Analysis: When clear identification of volatility expansion and contraction phases is critical for strategy selection

Known Limitations:

Like all technical indicators, T3 ATR has limitations that users should understand:

Historical Nature: T3 ATR is calculated from historical price data and cannot predict future volatility with certainty

Smoothing Trade-offs: The volume factor setting involves a trade-off between responsiveness and smoothness - no single setting is optimal for all market conditions

Extreme Events: During unprecedented market events or gaps, T3 ATR may not immediately reflect the full scope of volatility until sufficient data is processed

Relative Measurement: T3 ATR values are most meaningful in relative context (compared to recent history) rather than as absolute thresholds

Market Context Required: T3 ATR measures volatility magnitude but does not indicate price direction or trend quality - it should be used in conjunction with directional analysis

Performance Expectations:

T3 ATR is designed to help traders measure and adapt to changing market volatility conditions. When properly configured and applied:

It can help reduce position risk during volatile periods through appropriate position sizing

It can help identify optimal times for more aggressive position sizing during stable periods

It can improve stop-loss placement by adapting to current market conditions

It can assist in strategy selection by identifying volatility regimes

However, volatility measurement alone does not guarantee profitable trading. T3 ATR should be integrated into a comprehensive trading approach that includes directional analysis, proper risk management, and sound trading psychology.

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. T3 ATR provides adaptive volatility measurement but has limitations and should not be used as the sole basis for trading decisions. The indicator measures historical volatility patterns, and past volatility characteristics do not guarantee future volatility behavior. Market conditions can change rapidly, and extreme events may produce volatility readings that fall outside historical norms.

Traders should combine T3 ATR with directional analysis tools, support/resistance analysis, and other technical indicators to form a complete trading strategy. Proper backtesting and forward testing with appropriate risk management is essential before applying T3 ATR-based strategies to live trading. The volume factor parameter should be optimized for specific instruments and trading styles through careful testing rather than assuming default settings are optimal for all applications.

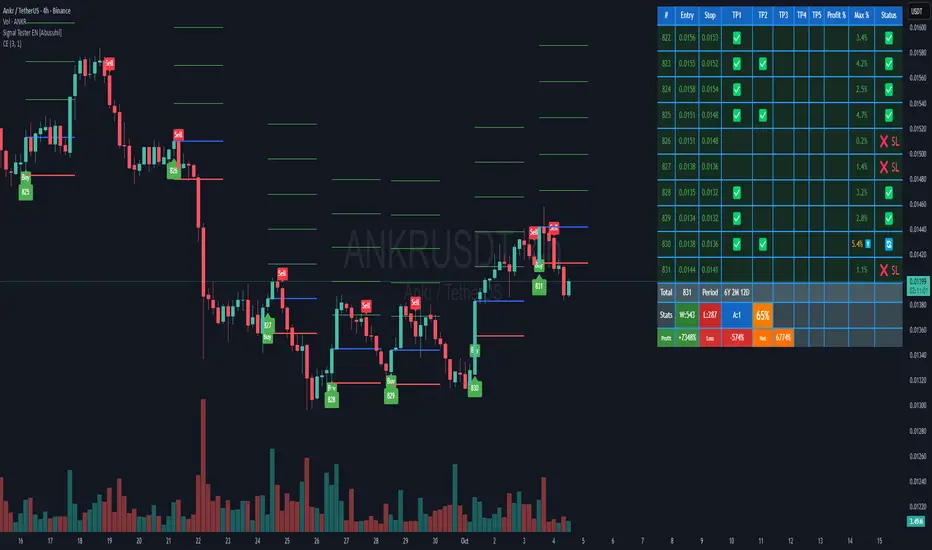

Signal Tester EN [Abusuhil]Signal Tester - Complete Description

Overview

Signal Tester is a comprehensive trading tool designed to backtest and analyze external trading signals with advanced risk management capabilities. The indicator provides seven different calculation methods for stop-loss and take-profit levels, along with detailed performance statistics and real-time tracking of active trades.

Important Disclaimer: This indicator is a tool for analysis and education purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Always conduct your own research and consider seeking advice from a qualified financial advisor before making trading decisions.

Key Features

7 Calculation Methods for customizable risk management

External Signal Integration via any oscillator or indicator

Real-time Trade Tracking with visual entry/exit points

Comprehensive Statistics Table showing win rate, profit/loss, and active trades

Date Filtering for focused backtesting periods

Custom Alerts for new buy signals

Multi-Target System with up to 5 take-profit levels

How to Use

Step 1: Connect External Signal

The indicator requires an external signal source to generate buy signals.

Add your preferred indicator to the chart (RSI, MACD, Stochastic, custom indicator, etc.)

In Signal Tester settings, locate "External Indicator" input

Click the input and select your indicator's plot line

Buy signals are generated when the external source crosses above zero

Example: If using RSI, connect the RSI line. A buy signal triggers when RSI crosses above the zero reference (if plotted as oscillator).

Step 2: Choose Your Calculation Method

Select one of seven methods under "Calculation Method":

1. Percentage %

The simplest method using fixed percentage values.

Settings:

Stop Loss %: Distance from entry to stop-loss (default: 2%)

Target 1-5 %: Distance from entry to each take-profit level

Example: Entry at $100

Stop Loss (2%): $98

Target 1 (2%): $102

Target 2 (4%): $104

Best For: Beginners, markets with consistent volatility

2. ATR Multiplier

Uses Average True Range for dynamic levels based on market volatility.

Settings:

ATR Period: Calculation period (default: 14)

Stop Multiplier: ATR multiplier for stop-loss (default: 1.5)

Target Multipliers: ATR multipliers for each take-profit

Example: Entry at $100, ATR = $2

Stop Loss (1.5x ATR): $100 - $3 = $97

Target 1 (2x ATR): $100 + $4 = $104

Best For: Volatile markets, adapting to changing conditions

3. Risk:Reward Ratio

Calculates targets based on risk-to-reward ratios.

Settings:

Stop Loss %: Initial risk percentage

Target Ratios: R:R ratio for each target (1:1.5, 1:2, 1:3, etc.)

Example: Entry at $100, Stop at $98 (2% risk = $2)

Target 1 (1:1.5): $100 + ($2 × 1.5) = $103

Target 2 (1:2): $100 + ($2 × 2) = $104

Target 3 (1:3): $100 + ($2 × 3) = $106

Best For: Traders focused on risk management and position sizing

4. Swing High/Low

Places stop-loss at recent swing low with targets as multiples of the risk.

Settings:

Swing Lookback Candles: Number of bars to find swing low (default: 5)

Stop Safety Distance %: Buffer below swing low

Target Multipliers: Risk multiples for each target

Example: Entry at $105, Swing Low at $100

Stop Loss: $100 - 0.1% = $99.90 (risk = $5.10)

Target 1 (1.5x): $105 + ($5.10 × 1.5) = $112.65

Best For: Swing traders, respecting market structure

5. Partial Take Profit

Sells portions of the position at each target level, moving stop to entry after first target.

Settings:

Stop Loss %: Initial stop distance

Target 1-5 %: Price levels for partial exits

Sell % at TP1-4: Percentage of position to close at each level

Example: 100% position, 50% sell at each target

TP1 hit: Sell 50%, remaining 50%, stop moves to entry

TP2 hit: Sell 25% (50% of remaining), remaining 25%

TP3 hit: Sell 12.5%, remaining 12.5%

Best For: Conservative traders, locking in profits gradually

6. Trailing Stop

Similar to Partial Take Profit but trails the stop-loss to each achieved target.

Settings:

Stop Loss %: Initial stop distance

Target 1-5 %: Price levels for trailing stops

Sell % at TP1-4: Percentage to close at each level

Example:

TP1 ($102) hit: Sell 50%, stop trails to $102

TP2 ($104) hit: Sell 25%, stop trails to $104

Price retraces to $104: Exit with locked profits

Best For: Trend followers, maximizing profit in strong moves

7. Smart Exit

Advanced method that moves stop to entry after first target, then exits based on technical conditions.

Settings:

Stop Loss %: Initial stop distance

First Target %: When hit, stop moves to breakeven

Exit Method: Choose from 8 exit strategies

Exit Methods:

Close < EMA 21: Exits when price closes below 21-period EMA

Close < MA 20: Exits when price closes below 20-period Moving Average

Supertrend Flip: Exits when Supertrend indicator flips bearish

ATR Trailing Stop: Dynamic trailing stop based on ATR

MACD Crossover: Exits on MACD bearish crossover

RSI < 50: Exits when RSI drops below specified level

Parabolic SAR Flip: Exits when SAR flips above price

Bollinger Bands: Exits when price closes below middle or lower band

Best For: Advanced traders, letting winners run with protection

Date Filtering

Control which trades are included in backtesting.

Filter Types:

Specific Date: Only trades after selected date

Number of Weeks: Last X weeks (default: 12)

Number of Months: Last X months (default: 3)

How to Enable:

Check "Enable Date Filter"

Select filter type

Set the date or number of weeks/months

Use Case: Test strategy performance in recent market conditions or specific periods

Understanding the Statistics Table

The table displays the last 10 trades plus comprehensive statistics:

Trade Columns:

#: Trade number

Entry: Entry price

Stop: Current stop-loss level

TP1-TP5: Checkmarks (✅) when targets are hit

Profit %: Realized profit for the trade

Max %: Maximum unrealized profit reached (⬆️ indicates active trade)

Status:

🔄 Active trade

✅ Closed winner

❌ SL - Stopped out

Summary Row:

Total: Number of trades executed

Period: Duration of trading period (Years, Months, Days)

Statistics Row:

W: Number of winning trades

L: Number of losing trades

A: Number of active (open) trades

Win Rate %: (Wins / Total Trades) × 100

Performance Row:

Profit: Total profit from all winning trades

Loss: Total loss from all losing trades

Net: Net profit/loss (Profit - Loss)

Visual Elements

When a buy signal triggers, the indicator draws:

Blue Line: Entry price

Red Line: Stop-loss level

Green Lines: Take-profit levels (up to 5)

Green Label: Trade number below the entry bar

Green Triangle: Buy signal marker

Alerts

The indicator includes customizable alerts for new buy signals.

Setting Up Alerts:

Click the "⏰" icon in TradingView

Select "Signal Tester "

Choose condition: "Buy"

Configure notification preferences (popup, email, webhook)

Click "Create"

Alert Message Format:

🚀 New Buy Signal!

Price:

Trade #:

Best Practices

Backtest First: Test each calculation method on historical data before live trading

Match Timeframe: Use the indicator on the timeframe you plan to trade

Combine with Analysis: Use alongside support/resistance, trend analysis, and other tools

Risk Management: Never risk more than 1-2% of capital per trade

Review Statistics: Regularly check win rate and profit/loss metrics

Adjust Settings: Optimize parameters based on the asset's volatility and your risk tolerance

Limitations

Requires external signal source (does not generate signals independently)

Backtesting assumes perfect entry/exit execution (real trading includes slippage)

Past performance does not guarantee future results

Should be used as one component of a complete trading strategy

Version Information

Version: 1.0

Pine Script Version: v5

Type: Overlay Indicator

Author: Abusuhil

Support and Updates

This indicator is provided as-is for educational and analytical purposes. Users are responsible for their own trading decisions and should thoroughly test any strategy before implementing it with real capital.

Risk Warning: Trading financial instruments carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk appetite. Only trade with money you can afford to lose.

Advanced Trading System - [WOLONG X DBG]Advanced Multi-Timeframe Trading System

Overview

This technical analysis indicator combines multiple established methodologies to provide traders with market insights across various timeframes. The system integrates SuperTrend analysis, moving average clouds, MACD-based candle coloring, RSI analysis, and multi-timeframe trend detection to suggest potential entry and exit opportunities for both swing and day trading approaches.

Methodology

The indicator employs a multi-layered analytical approach based on established technical analysis principles:

Core Signal Generation

SuperTrend Engine: Utilizes adaptive SuperTrend calculations with customizable sensitivity (1-20) combined with SMA confirmation filters to identify potential trend changes and continuations