CryptoKillerCryptoKiller is a trend following trading system. It provides entry and exit points, a money management system and a trade management system.

The entry points (fuchsia line) are determined by CryptoKiller Oscillator (see other published script to understand how the oscillator works).

The trade management system provides the exit points in profit and in loss. This script works with multiple take profits (green lines), the initial position is liquidated little by little as the trend reaches the profit targets. Trade management also provides trailing stop exits to save the remaining profits.

Stop loss (red line) take into account the recent past of the chart to be determined, while take profits are fixed and have been calculated based on historical volatility.

The money management system is very simple, it plans to enter a position with a fixed percentage with respect to equity.

CryptoKiller, during an operation, also draws supports and resistances on the chart - determined by the oscillator (orange lines) these supports and resistances are used as a filter to understand where there is the greatest probability of trend development (some entry points provided by the oscillator will therefore not be considered by CryptoKiller as entry points, as in disagreement with the traced supports / resistances).

We know that an error appears in the backtest calculation, where the script is said to suffer from a bias, so the backtest calculation may not be accurate. Actually this happens in high times like H4 or daily, but CryptoKiller is not designed for these timeframes. it is a short-term strategy.

For more information read the author's instructions to contact us, we will send a PDF file with a more complete explanation of the strategy accompanied by screenshots.

Access to this script is granted along with access to CryptoKiller Oscillator.

在腳本中搜尋"stop loss"

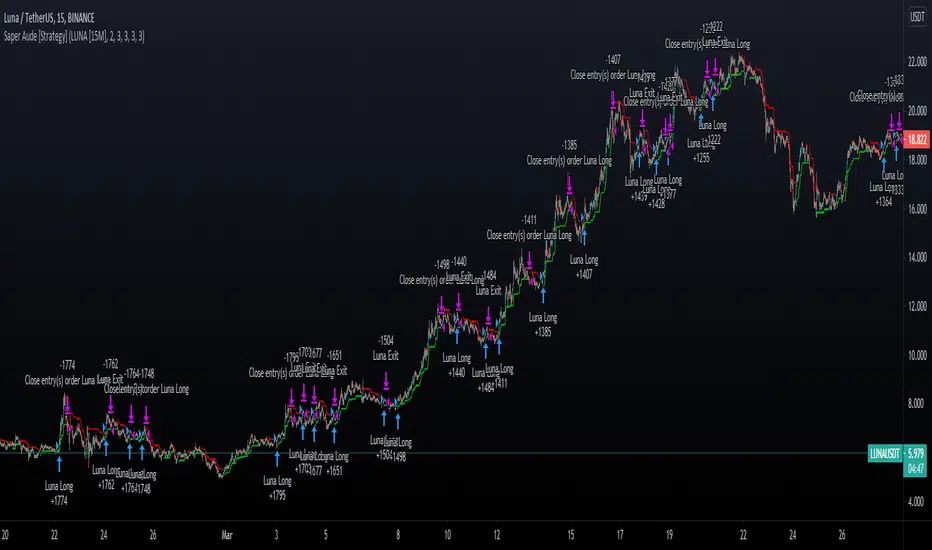

Saper Aude [Strategy]Sapere Aude Strategy

Trend based scalping strategy, to work on lower timeframes (15Minute - 1 Hour)

Calculations on ATR, strategy uses extra conditions to help filter out bad trades.

How to use the strategy?

Simple as when green line shows below, that can be either a good entry point or a signal to start building limit orders on the plot.

I use the ATR as a trailing stop loss for exit.

vica versa for entering shorts. The strategy is only set up to take long positions though.

This is a great scalping strategy for bots in Ranging or up trending markets.

This scripts has 5 variations built within it which are fitted for certain coins & their timeframes

The coins included are

BTC/USDT 1 Hour

ETH/USDT 1 Hour

ADA/USDT 30 Minutes

DOGE/USDT 15 Minutes

LUNA/USDT/15 Minutes

The Strategy backtest results includes Fess and there is NO Repaint! The script is written in Version 4

There is an option in the settings cog to choose from the 5 coins and their timeframes where they have been optimised

There is also an option to change the backtesting range

The stop Losses are also adjustable and listed under the settings

The strategy performs best on the Binance listings

Momentum Trading Strategy (Weekly Chart)The strategy will open position when there is momentum in the stock

The strategy will ride up your stop loss based on the super trend.

The strategy will close your operation when the market price crossed the stop loss.

The strategy will close operation when the line based on the volatility will crossed

Reversal with Bollinger Bands + RSI + ADX + ATR (Upgraded)Hi,

Welcome to my 4th script.

Someone asked me some questions about the Bollinger Band strategy I previously published. When I went back to my published script I couldn't help myself but simply try and make it better. Which I did.

Since I've published that script, I've gained much more knowledge about how Pinescript functions. As well as gaining more and more knowledge about how the markets are structered etc.

In this reversal script we use 4 indicators to determine good entry signals, we determine whether the market is ranging or trending and we still only want to take trades in the direction of the "trend".

Bollinger Bands are used for our entry signal. When price hits either side of the band, we wait for a reverse candlestick before we enter a position.

RSI is used to determine if we're in a trending market or in a ranging market. You can adjust the values in the inputs. You can determine the minimum RSI value and the maximum RSI value.

ADX is used the same way as RSI, you can adjust the value in the inputs. You can determine the minimum ADX value.

Last but not least we use two EMA's, a 200 EMA and 100 EMA. Both are adjustable through the inputs. I used two EMA's because I noticed when using this strategy that we'd enter a new position often after having a bad trade. Using two EMA's might clean up some signals, in my case with EUR/USD on a 15m timeframe, it didn't clean up enough signals.

All the default values are pretty decent but might require some finetuning on a certain instrument. Don't overfit the strategy though, that'll only give you bad signals in the future.

Then we are off to our exit signals.

Initially I wanted to incorporate my previous Bollinger Band exit signals as well, but it was too much of a hassle to make the script work as intended so I left it out. If you want to use those exit signals, just find my other script.

When we're in a position and price crosses the opposite band, we wait for a reverse candlestick before we exit the position.

Additionally we want our losses to be as small as possible, so we use RSI to signal us when the market is, or starts to, trend against us. This is where you use the minimum and maximum exit values. So when RSI crosses over or under that value, it'll exit the position.

Furthermore, we use the ATR indicator to set our stop loss, which is pretty basic stuff. You can adjust the ATR multiplier in the inputs. Disabling "Use Trailing Stop?" is really inadvisable unless you know this script inside out as your only exit signals will be opposite Bollinger Band Cross and RSI overbought / oversold areas.

JFRewards Indi Channel <Heikin> v4.0<>

SOP guidelines only given to JF members .

The ideas are:

1) Finding where to enter position of buying and sell.

2) Finding where is the realistic take profit target within 24 hours with maximum profits.

3) Finding Trailing STOP LOSS, Trailing Take Profit, Take Profit, STOP LOSS.

Fully tested with @Binance Exchanger with numerous of stablecoins and altcoins as well as BTC , ETH.

Performance cannot be shown due to non standard chart of Heikin Ashi.

KISS Strategy: SMA + EMA//Hello my fellow investors

//I am creating a simple non-cluttered strategy that uses 3(+1) simple means to determine: viability, entry, and exit

//1) Has a consistent trend been maintained for several days/weeks

//2) SH SMA crossover LG SMA = Bullish entry/LG SMA crossover SH SMA = Bearish entry

//3) Use the Slope factor & Weeks in Trend (WiT) to dertermine how strong of an entry signal you are comfortable with

//4) Exit position based on next SMA cross and trend reversal or stop loss%

//3+1) For added confidence in trend detection: Apply MACD check - buy--> MACD line above signal line and corssover below histogram \\ sell --> MACD line below signal line and crossover above histogram.

//*)This code also allows you to determine your desired backtesting date compliments of alanaster

The chart shown has:

Starting Capital: $10,000

Investment percent per trade: 1.5%

Stop Loss: 20%

Take Profit: 100%

Gregoire Channel StrategyAdd the strategy to the chart, and start by selecting one of four systems:

1) Trend Following

2) Trend Following - Long Only

3) Volatility Breakout

4) Volatility Breakout - Long Only

Each system is better suited to a particular type of market. Find out through back-testing which system and timeframe is best for each market.

Trend Following is good for securities that strongly trend up and down. Examples: Bitcoin, "growth" stocks.

Trend Following (Long Only) is great for stock indexes that are on a 100 year uptrend, or US-based crypto exchanges which don't allow margin trading but you want to catch the big trends (BTC, ETH).

Volatility Breakout is a defensive system designed to capture the meat of the move and protect the gains. This system is better for altcoins and mature markets like forex pairs.

Volatility Breakout (Long Only) is for US-based crypto exchanges that don't allow margin trading. Good for altcoins.

DEFAULT SETTINGS:

START DATE: 1/1/2020

FEE: 0.1% (This is the Binance.us fee per trade, tailor it to your exchange)

TAKE PROFIT GCW: 0

STOP LOSS GCW: 0

LENGTH: 20

SOURCE: HL2

The system doesn't need stop losses or take profit levels as they are built into the system, but you can add them if you want. 1 GCW = half the channel, so the distance from the top of the channel to the middle line. 2 GCW = the height of the channel.

MISC

-Make sure you calculate the fees! They make a huge difference in profitability. For example, test how Coinbase.com's fees of 0.5% compared to Binance.us's fees of 0.1%. It's huge!

-Try different sets of lengths and timeframes. For example, I like using the daily timeframe and low length for stocks and intraday timeframe with long lengths for crypto. See what tests best!

Disclaimer: past performance doesn't equal future results, this isn't financial advice, this is for entertainment purposes only, consult a professional financial advisor.

Buy the Dips (by Coinrule)Taking your first steps into automated trading may be challenging. Coinrule's mission is to make it as easy as possible, also for beginners.

Here follows the best trading strategy to get started with Coinrule. This strategy doesn't involve complex indicators, yet was proved to be effective in the long term for many coins. Results seem to be improved when trading a coin vs Bitcoin.

The strategy buys the dips of a coin to sell with a profit. A stop-loss protects every trade.

Crypto markets offer high volatility and, thus, excellent opportunities for trading. Excluding times of severe downtrend, buying the dip is a simple and effective long-term trading strategy. The buy-signal is set to a 2% drop in a 30-minutes time frame.

Each trade comes with a take profit and a stop loss. Both set at 2%.

You can adjust these percentages to the market volatility as an advanced setup. You can backtest the outcomes using the backtesting tool from Tradingview

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Simple and efficient MACD crypto strategy with risk managementToday I am glad to bring you another great creation suited for crypto markets.

MARKET

Its a simple and efficient strategy, designed for crypto markets( btcusd , btcusdt and so on), and suited for for higher time charts : like 1hour, 4hours, 1 day and so on.

Preferably to use 1h time charts.

COMPONENTS

MACD with simple moving average

ENTRY DESCRIPTION

For entries we have :

We check the direction with MACD . Depending if its an uptrend and positive level on histogram of MACD we go long, otherwise we go short.

RISK MANAGEMENT

In this strategy we use a stop loss based on our equity. For this example I choosed a 2% risk .That means if our account has 100.000 eur, it will automatically close the trade if we lose 2.000.

We dont use a take profit level.

In this example also we use a 100.000 capital account, risking 5% on each trade, but since its underleveraged, we only use 5000 of that ammount on every trade. With leveraged it can be achieved better profits and of course at the same time we will encounter bigger losses.

The comission applied is 5$ and a slippage of 5 points aswell added.

For any questions or suggestions regarding the script , please let me know.

High/low crypto strategy with MACD/PSAR/ATR/EWaveToday I am glad to bring you another great creation of mine, this time suited for crypto markets.

MARKET

Its a high and low strategy, designed for crypto markets( btcusd , btcusdt and so on), and suited for for higher time charts : like 1hour, 4hours, 1 day and so on.

Preferably to use 1h time charts.

COMPONENTS

Higher high and lower low between different candle points

MACD with simple moving average

PSAR for uptrend and downtrend

Trenddirection made of a modified moving average and ATR

And lastly elliot wave oscillator to have an even better precision for entries and exits.

ENTRY DESCRIPTION

For entries we have : when the first condition is meet(we have a succession on higher high or lower lows), then we check the macd histogram level, then we pair that with psar for the direction of the trend, then we check the trend direction based on atr levels with MA applied on it and lastly to confirm the direction we check the level of elliot wave oscillator. If they are all on the same page we have a short or a long entry.

STATS

Its a low win percentage , we usually have between 10-20% win rate, but at the same time we use a 1:30 risk reward ratio .

By this we achieve an avg profit factor between 1.5- 2.5 between different currencies.

RISK MANAGEMENT

In this example, the stop loss is 0.5% of the price fluctuation ( 10.000 -> 9950 our sl), and tp is 15% (10.000 - > 11500).

In this example also we use a 100.000 capital account, risking 5% on each trade, but since its underleveraged, we only use 5000 of that ammount on every trade. With leveraged it can be achieved better profits and of course at the same time we will encounter bigger losses.

The comission applied is 5$ and a slippage of 5 points aswell added.

For any questions or suggestions regarding the script , please let me know.

2 Candles Inside ATR2 agitated candles falling inside ATR range, awaiting possibly a big move.

Buy / Sell signals at combined high / low can be used as order with other as stop loss.

Counter trade, when this minimal stop loss is hit, is also as useful. However, wait till the SL candle closes, before opening position on the other side.

Works quite well on 15 mins chart, with settings of ATR duration 25 and multiplier 0.6. These settings are configurable, so feel free.

Intraday Trend Following Algorithm [Bitduke]Description :

Trend following strategy that constantly adjusts to volatility and avoids of most whipsaws; rapidly moves up or down according to a quickly changing market. Great strategy for high volatile markets, like crypto market.

Based on a couple of special moving averages with integrated smoother which helps to avoid whipsaws.

Backtesting

Backtested on BTCPERP ( FTX ). It shows much better results on 4h timeframe (more than 222% YTD) and relatively low drawdown which allows you to use up to x3 leverage without a fear of huge losses. I.e if we have 5% drawdown for this strategy and using x3 leverage then to be prepared to 15% drawdown maximum in this case.

Initial Capital: $1000

Capital per trade: $1000

Including fee: 0.075% (buy + sell) side, type "taker"

When we get a signal (green/red column on chart) algo opens a trade by the next candle open price.

Others:

Risk management: Stop loss/Take profit in %

Strategy doesn't repaint .

----------

To access: sign up on FTX using ref link from my signature.

Lowkey System (Strategy)View study version

A long-only strategy that aim to detect the beginning of new bullish trends and their ends.

For entering a new position this script is waiting for a moving average crossover then wait for a volume increase relative to the current volatility.

For closing a position it's simply waiting for a crossunder of whether the MA or if enabled the stop loss.

This strategy is already configured to run on BTCUSD in a 4h timeframe but you can customize the moving average and the stop loss parameters to suit your needs.

I've worked a lot to write this script so I'm not giving it for free but you can try it for 10 days.

Contact me for more details.

Have fun!

PS: I'm french so please excuse me if I've made some grammar errors ;)

PD Crypto Performer PRO (Backtest)Description:

This is the backtesting version of the PD Crypto Performer Pro (Alert) . You can choose to backtest either one of the two strategies included, a trend-identifying swing strategy and a low risk scalping strategy. Both strategies assume the same capital amount invested ($10,000) each trade. You can also see how your capital grows over time by enabling the reinvesting proceeds option. For details, please check out this tutorial .

The backtesting results could be easily improved in live trading by utilizing the “Take Profit” signals and following the recommended methods of use below.

To assist the decision-making process, the code currently references BTCUSD. As a result, it is only suitable for crypto traders. However, we are working on the stock and forex versions, and the Performer will have these compatibilities soon.

Most importantly, our signals DO NOT REPAINT !

Recommended Use:

- Time Frame: 1HR

- Asset: Large cap crypto assets.

For lower risk tolerance, we recommend using the indicator on ETHUSD. For maximizing profits, we recommend using the indicator on BCHUSD.

- Always set stop loss according to your own risk tolerance

- Take profits along the way. Check out this video tutorial for when to reenter after our take profit signals.

Recommended Use for Advanced Traders:

- Position sizing:

Larger position if the 1HR signal is in the same direction compared to the 4HR trend.

Smaller position if the 1HR signal is in the opposite direction compared to the 4HR trend.

- Better entry/exit points:

Track the 1HR signal for the asset you are trading on other exchanges along with the BTCUSD 1HR signal. Sometimes, the signals from different exchanges occur with a 1-2 hour difference. You could use these earlier signals along with a lower time frame (eg. 15min) entry confirmation from your own exchange for better entry / exit points.

- Use “Take Profit” signals for counter trend scalps. Recover at the reentering opportunities . This works best with candlestick pattern confirmations.

Never use this if you suspect a flag / inverted flag pattern is forming.

Go to www.phi-deltalytics.com and sign up for a FREE trial today!

Let us know if you have any questions or recommendations. We are here for your success!

Disclaimer:

It should not be assumed that the methods, techniques, or indicators presented will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. This is not a solicitation of any order to buy or sell.

PD Crypto Performer (Backtest)Description:

This is the backtesting version of the PD Crypto Performer (Alert) . The strategy assumes the same capital amount invested ($10,000) each trade. You can also see how your capital grows over time by enabling the reinvesting proceeds option. For details, please check out this tutorial . The backtesting results could be easily improved in live trading by following the recommended methods of use below.

To assist the decision-making process, the code currently references BTCUSD. As a result, it is only suitable for crypto traders. However, we are working on the stock and forex versions, and the Performer will have these compatibilities soon.

Most importantly, our signals DO NOT REPAINT !

Recommended Use:

- Time Frame: 1HR

- Asset: Large cap crypto assets.

For lower risk tolerance, we recommend using the indicator on ETHUSD. For maximizing profits, we recommend using the indicator on BCHUSD.

- Always set stop loss according to your own risk tolerance

- Take profits along the way.

Recommended Use for Advanced Traders:

- Position sizing:

Larger position if the 1HR signal is in the same direction compared to the 4HR trend.

Smaller position if the 1HR signal is in the opposite direction compared to the 4HR trend.

- Better entry/exit points:

Track the 1HR signal for the asset you are trading on other exchanges along with the BTCUSD 1HR signal. Sometimes, the signals from different exchanges occur with a 1-2 hour difference. You could use these earlier signals along with a lower time frame (eg. 15min) entry confirmation from your own exchange for better entry / exit points.

Go to www.phi-deltalytics.com and sign up for a FREE trial today!

Let us know if you have any questions or recommendations. We are here for your success!

Disclaimer:

It should not be assumed that the methods, techniques, or indicators presented will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. This is not a solicitation of any order to buy or sell.

Directional Momentum Flux StrategyDirectional Momentum Flux (DMF) is a compound indicator designed to surface signals of projected change in directional momentum. The primary goal is to identify possible momentum inflection points and signal them before they happen, which is reached by applying a set of well-known high-level indicators (e.g. DEMA, RSIs, CCIs and VWAP), lower-level indicators (e.g. BOP, PPO and RMOMO), and some special sauce brewed in-house by yours truly.

This strategy is invite-only. Invitations are offered for a one-time fee of $250 payable in several cryptocurrencies (ETH, BTC, DASH, XMR or ZEC). Once you've got an invitation, you will automatically receive updates forever*.

DMF was designed to work across multiple asset classes. Extensive backtesting has been performed over multiple sample series (not just during the bull runs, for example) and against a randomized pool of assets. But don't take my word for it, I've included some time-based backtesting support tools to make it easy-peasy for you to validate the results yourself!

Under the hood, DMF is powered by numerous indicators, including:

✓ Double EMA & Composite SMA;

✓ Double RSI (fast & slow, variable);

✓ Composite StochRSI & VWAP (StochRSI+, two series);

✓ Composite Commodity Channel Index (CCI+, two series);

✓ Volume-Weighted Balance of Power (BOP itself was adapted from BOP_LB, kudos to LazyBear);

✓ Percentage Price Oscillator (PPO, split, two series);

✓ Range-adjusted Momentum Oscillator (RMOMO, my fancy MOM variant);

It crunches all that data and generates signals which are issued in two ways:

✓ Vertical Bands (or VBs) - Entry/Exit windows as vertical bands that remain "lit" (e.g. the background of a series of candles is semi-opaque white) while the top-level signals are showing sufficiently strong BUY signals. These windows are the primary entry/exit targets and can be relied upon with sufficient risk mitigation (e.g. a reasonable stop-loss or other scale-out exit mechanism). A VB followed immediately by an egg is as good as gold.

✓ Eggs - Entry/Exit validation signals that confirm the condition indicated by VBs. A lit VB without an egg in the same or next candle session is considered to be valid , but not safe (see above warning). Waiting for an egg can improve performance at the risk of missing the best possible entry point. Consider your risk tolerance and act accordingly.

Basic Instructions:

✓ Configure The Settings! The defaults are pretty good, but don't be scared to try variations. For example, by default SHORT positions are disabled. You might want to enable them if your risk tolerance allows them. (IMO there's gold on both ends of the rainbow. 🌈)

✓ Pay attention to the VBs. If you see a lit band being placed in an otherwise dark area, it's a projected inflection point. This is expected to be validated and confirmed in the same or immediately following period with an egg. You can enter a LONG position at this time.

✓ Pay attention to the eggs. If you see an egg, it's a confirmation that the VB changes in the same or immediately preceding candle period is valid. If you did not enter or exit your position at the point of the VB shift, now is the time to do so.

✓ Watch for the end of a VB period and be prepared to exit your position quickly as the next egg may be accompanied by a large directional momentum inflection.

Things to Note:

📉 - DMF is designed for day trading with aggressive position TTLs (15m was the upper bound during development and strategy testing). It appears to issue valid signals for other intervals, but it was not designed for >15m and YMMV. Don't go manually opening a LONG with no exit strategy and go to sleep... it probably won't work out to your benefit. You should be prepared to exit positions at any time. (Pro tip: automation is your friend!)

💸 - DMF indicator is not free from risk. As with all investment strategies, it is crucial to exercise caution and only trade with funds you are comfortable losing. DMF does not offer any form of guarantee or warranty, implied or otherwise. If you lose money, your house, your 401K... that's on you. (Pro tip: don't risk anything you're not ready to lose, because losses are part of the game and you WILL have them.)

🤔 - By using this indicator, you understand that any and all risks are the sole and complete responsibility of the end user (yeah, that's you). Don't use it if you're not 100% clear that you know exactly what you're doing. (Pro tip: always ask questions if you're feeling confused.)

⏱ - * Forever in this context means that, where room for improvement exists, I will improve it over time and you'll get all updates until I stop making them. (Pro tip: nobody lives forever.)

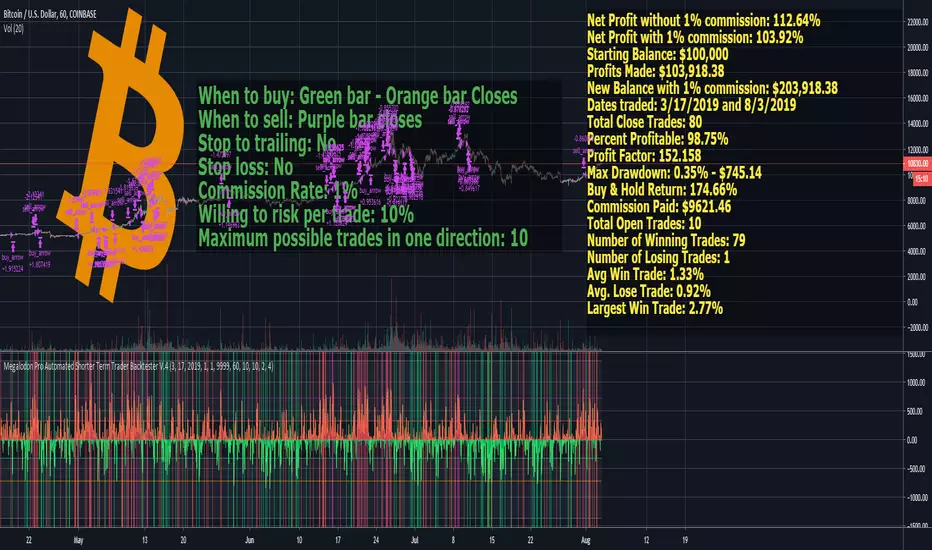

Megalodon Pro Automated Shorter Term Trader BacktesterSTRATEGY

When to buy: Green bar - Orange bar Closes

When to sell: Purple bar closes

Stop to trailing: No

Stop loss: No

Commission Rate: 1%

Willing to risk per trade: 10%

Maximum possible trades in one direction: 10

RESULTS

Net Profit without 1% commission: 112.64%

Net Profit with 1% commission: 103.92%

Starting Balance: $100,000

Profits Made: $103,918.38

New Balance with 1% commission: $203,918.38

Dates traded: 3/17/2019 and 8/3/2019

Total Close Trades: 80

Percent Profitable: 98.75%

Profit Factor: 152.158

Max Drawdown: 0.35% - $745.14

Buy & Hold Return: 174.66%

Commission Paid: $9621.46

Total Open Trades: 10

Number of Winning Trades: 79

Number of Losing Trades: 1

Avg Win Trade: 1.33%

Avg. Lose Trade: 0.92%

Largest Win Trade: 2.77%

Let me know what you guys think about the results?

Due to the tradingview's limitations on providing the shorter time frame price data, we had to provide a 60 minute time frame backtesting results.

The shorter time frames including 1 minute and 15 minutes backtesting results are way more accurate and precise than 60 minutes time frame results.

Megalodon Trading

Enlightening the Modern Investors

15MEX Momentum ScalperAlpha product project in development. Uses a combination of MACD and T3-CCI with tweaked settings to catch directional momentum and scalp a small move. Strategy is quantity of trades over quality of trades to build profits.

Use this strategy for 15-min Bitmex scalping on XBT contracts only. Recommend 100k contract size or less; backtested with 100k contracts.

Market enter, then use post-only limit exits and stop losses.

Setting is pre-optimized for 0.5% tp target and 0.5% sl of entry price. Recommend default 3 bars as basis for confirming recent MACD crossover as well as default 0.618 Fibonacci ratio as the T3-CCI basis.

Default risk level setting is approximately 2-3 trades a day. You can double the amount to 4-5 trades a day by enabling Aggressive mode. This may lead to larger profits and more entries, but with more frequent stop losses.

Future version will include trailing TPs/stops. Still undergoing optimization and refinement.

RePaNoCHa [Backtest]This is a very long script and adjusting the settings can be a bit slow so I share some settings. (these may be even better)

It has no security() and no Heikin Ashi so no repaint and Backtest is real.

It's important to adjust correctly the tics/pips correction.

All timeframes but good results at 2H

Default settings for ETHUSD (BITMEX) 2H

Alerts version coming soon...

Enjoy!!!

"Este script es la repanocha"

XBTUSD (BITMEX)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 8

T3 Volume Factor = 0.9

Range Filter+ADX == true

Sampling Period = 16

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 10

ADX Threshold = 20

Parabolic SAR == true

SAR start = 0.03

SAR inc = 0.02

SAR max = 0.3

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.2

Trailing Stop Offset % (when profit=10 %) = 1.2

Stop Loss = 3.2

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

ETHUSD (BITMEX)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 6

T3 Volume Factor = 0.7

Range Filter+ADX == true

Sampling Period = 10

Range Multiplier = 0.9

Flat Market Trades == true

ADX lenght = 11

ADX Threshold = 19

Parabolic SAR == true

SAR start = 0.06

SAR inc = 0.07

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss = 3.2

Tics/Pips Correction = 100

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

BNBUSDT (BINANCE)

Timeframe = 2H

Position Side = LONG

Source = hlc3

T3 == true

T3 Length = 6

T3 Volume Factor = 0.7

Range Filter+ADX == true

Sampling Period = 17

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 5

ADX Threshold = 18

Parabolic SAR == true

SAR start = 0.04

SAR inc = 0.03

SAR max = 0.25

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss == false

Tics/Pips Correction = 10000

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

LTCUSDT (BINANCE)

Timeframe = 2H

Position Side = LONG

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 11

Range Multiplier = 1.1

Flat Market Trades == true

ADX lenght = 6

ADX Threshold = 22

Parabolic SAR == true

SAR start = 0.07

SAR inc = 0.04

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss == false

Tics/Pips Correction = 100

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

TRXUSDT (BINANCE)

Timeframe = 2H

Position Side = LONG

Source = hlc3

T3 == true

T3 Length = 7

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 8

Range Multiplier = 1.1

Flat Market Trades == true

ADX lenght = 4

ADX Threshold = 22

Parabolic SAR == true

SAR start = 0.07

SAR inc = 0.04

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss == false

Tics/Pips Correction = 100000

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

NAS100 (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 12

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 18

ADX Threshold = 21

Parabolic SAR == true

SAR start = 0.08

SAR inc = 0.06

SAR max = 0.25

Pyramiding = 15

Trailing Stop Activation % = 0.2

Trailing Stop Offset % (when profit=0.5 %) = 0.15

Trailing Stop Offset % (when profit=10 %) = 1

Stop Loss == false

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 3 contracts

Commission value = 0.2 USD per contract

NATGAS(OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 15

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 12

ADX Threshold = 21

Parabolic SAR == true

SAR start = 0.08

SAR inc = 0.06

SAR max = 0.4

Pyramiding = 15

Trailing Stop Activation % = 0.2

Trailing Stop Offset % (when profit=0.5 %) = 0.15

Trailing Stop Offset % (when profit=10 %) = 1

Stop Loss == false

Tics/Pips Correction = 1000

Initial Capital = 1000

Quantity = 4500 contracts

Commission value = 0.002 USD per contract

SPX500 (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 4

T3 Volume Factor = 0.8

Range Filter+ADX == true

Sampling Period = 14

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 12

ADX Threshold = 17

Parabolic SAR == true

SAR start = 0.09

SAR inc = 0.04

SAR max = 0.2

Pyramiding = 15

Trailing Stop Activation % = 0.15

Trailing Stop Offset % (when profit=0.5 %) = 0.1

Trailing Stop Offset % (when profit=10 %) = 0.5

Stop Loss = 1.5

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 8 contracts

Commission value = 0.2 USD per contract

US30 (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 4

T3 Volume Factor = 0.9

Range Filter+ADX == true

Sampling Period = 11

Range Multiplier = 1.1

Flat Market Trades == true

ADX lenght = 16

ADX Threshold = 24

Parabolic SAR == true

SAR start = 0.08

SAR inc = 0.03

SAR max = 0.05

Pyramiding = 15

Trailing Stop Activation % = 0.15

Trailing Stop Offset % (when profit=0.5 %) = 0.075

Trailing Stop Offset % (when profit=10 %) = 0.5

Stop Loss = 1.5

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 1 contracts

Commission value = 1.5 USD per contract

WHEAT (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1.1

Range Filter+ADX == true

Sampling Period = 12

Range Multiplier = 0.9

Flat Market Trades == true

ADX lenght = 13

ADX Threshold = 21

Parabolic SAR == true

SAR start = 0.1

SAR inc = 0.05

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.2

Trailing Stop Offset % (when profit=0.5 %) = 0.1

Trailing Stop Offset % (when profit=10 %) = 1

Stop Loss = 2.5

Tics/Pips Correction = 1000

Initial Capital = 1000

Quantity = 2500 contracts

Commission value = 0.003 USD per contract

Bedrock Bot - BTCUSD 30m Scalper BotBedrock Bot trades on BTCUSD charts and is a high frequency scalper bot - for those that like a little more action.

The strategy was developed for use on more recent market conditions - smaller trends within larger sideways ranges. It will work in trends as well. It is made for quick take profits and tight stop losses to maximize overall profit and minimize losses (check out the win ratio and downdraw results). It does not trade on the weekends as much of the volume is now weekday based.

Backtest results look great and we have been running this bot on live markets as well in forward testing with profit results.

These live tests were done exclusively on BitMex and by using automation on Crypto Bots Hub . Monthly returns have been around 8% - you may think this doesn't sound amazing but understand compound interest and do check out the win percentage and downdraw. In these sideways markets, this can keep building your profits slow and steady with minimal risk.

The bot controls entries, stop losses, and take profits as part of the code.

Message me on information to get free access.

cryptomars 1.0 signal Concussion trend

Description:

1. In the indicator, there is an orange signal that fluctuates linearly. It is a buy signal when it goes from bottom to top. When the signal line remains in the upper position, it indicates a multi-party trend.

2. When it goes from top to bottom, it indicates a sell signal. When the signal line remains below, it indicates a sales trend.

3. Depending on the time level, when the position of the signal line changes, determine whether the current candle is completed or not according to the time level of the chart you selected to determine the signal. For example, if you select a chart level of 5 meters, then when the signal line changes, for example, it will send a sell signal from top to bottom. At this time, please do not rush to sell. You should wait for this 5 meter candlestick to complete. When the candle is over and the next candle is started, if the signal line remains in the top-down form, the sell signal is normal and you can sell it.

Because the position of the signal appears, it is the location of the sale. During the completion of the candlestick , the signal may disappear after disappearing. We only have to wait for a while to get a more stable deal.

4. The alarm setting is very simple. There are two lines in the indicator. One is the orange signal line that fluctuates up and down, and the other is the fixed zero line of “zero”.

We set it in the alarm. When the signal line passes "zero" from the top, the short signal is sent only when the candle map is completed. When the signal line passes "zero" from "up" below, the signal is sent for a long time when the candlestick is completed.

One trick, the appearance of the signal, is that the price runs in one direction for a while, so it appears at or near the bottom. Because, when we have already made a profit in the transaction, we can make a profit in advance, and we do not need to wait for the opposite signal to stop the profit and reduce the risk of profit retracement.

Because in this market, the fluctuations are very large, and the people who compete are also very fierce. What we need to do is to make every transaction as possible, and we are all profitable. If we sell and find that the price is still rising, please don't feel sorry, don't consider eating all the profits.

6. When the signal appears, in most cases, even in the impact trend, it will still run a distance in the direction of the signal, that is, you will profit, so please close the position and make a profit in time. Otherwise, when the price volatility is too small, you miss the profit point, the price starts to run in the opposite direction, and you may change from profit to loss.

BITMEX's trailing stop loss is a great feature, please use it flexibly.

7, if it is a shock trend, please try not to trade.

8. We recommend that you turn on the “cryptomars 3.0” and “cryptomars 2.0” indicators. No matter who signs the trade first, you can trade, which can help you get more profit.

9. Remember, I hope this indicator will be your powerful assistant, but please don't rely on it completely. Learning more trading knowledge and skills is even more important. Therefore, when we consider the profitable position, you can use your trading skills, MACD , KDJ, etc. to assist and profit in a more suitable position.

cryptomars signal short 2.0Description:

1. In the indicator, there is an orange signal that fluctuates linearly. It is a buy signal when it goes from bottom to top. When the signal line remains in the upper position, it indicates a multi-party trend.

2. When it goes from top to bottom, it indicates a sell signal. When the signal line remains below, it indicates a sales trend.

3. Depending on the time level, when the position of the signal line changes, determine whether the current candle is completed or not according to the time level of the chart you selected to determine the signal. For example, if you select a chart level of 5 meters, then when the signal line changes, for example, it will send a sell signal from top to bottom. At this time, please do not rush to sell. You should wait for this 5 meter candlestick to complete. When the candle is over and the next candle is started, if the signal line remains in the top-down form, the sell signal is normal and you can sell it.

Because the position of the signal appears, it is the location of the sale. During the completion of the candlestick , the signal may disappear after disappearing. We only have to wait for a while to get a more stable deal.

4. The alarm setting is very simple. There are two lines in the indicator. One is the orange signal line that fluctuates up and down, and the other is the fixed zero line of “zero”.

We set it in the alarm. When the signal line passes "zero" from the top, the short signal is sent only when the candle map is completed. When the signal line passes "zero" from "up" below, the signal is sent for a long time when the candlestick is completed.

One trick, the appearance of the signal, is that the price runs in one direction for a while, so it appears at or near the bottom. Because, when we have already made a profit in the transaction, we can make a profit in advance, and we do not need to wait for the opposite signal to stop the profit and reduce the risk of profit retracement.

Because in this market, the fluctuations are very large, and the people who compete are also very fierce. What we need to do is to make every transaction as possible, and we are all profitable. If we sell and find that the price is still rising, please don't feel sorry, don't consider eating all the profits.

6. When the signal appears, in most cases, even in the impact trend, it will still run a distance in the direction of the signal, that is, you will profit, so please close the position and make a profit in time. Otherwise, when the price volatility is too small, you miss the profit point, the price starts to run in the opposite direction, and you may change from profit to loss.

BITMEX's trailing stop loss is a great feature, please use it flexibly.

7, if it is a shock trend, please try not to trade.

8. We recommend that you turn on the “cryptomars 3.0” and “cryptomars 1.0” indicators. No matter who signs the trade first, you can trade, which can help you get more profit.

9. Remember, I hope this indicator will be your powerful assistant, but please don't rely on it completely. Learning more trading knowledge and skills is even more important. Therefore, when we consider the profitable position, you can use your trading skills, MACD , KDJ, etc. to assist and profit in a more suitable position.

cryptomars signal 3.0Description:

1. In the indicator, there is an orange signal that fluctuates linearly. It is a buy signal when it goes from bottom to top. When the signal line remains in the upper position, it indicates a multi-party trend.

2. When it goes from top to bottom, it indicates a sell signal. When the signal line remains below, it indicates a sales trend.

3. Depending on the time level, when the position of the signal line changes, determine whether the current candle is completed or not according to the time level of the chart you selected to determine the signal. For example, if you select a chart level of 5 meters, then when the signal line changes, for example, it will send a sell signal from top to bottom. At this time, please do not rush to sell. You should wait for this 5 meter candlestick to complete. When the candle is over and the next candle is started, if the signal line remains in the top-down form, the sell signal is normal and you can sell it.

Because the position of the signal appears, it is the location of the sale. During the completion of the candlestick , the signal may disappear after disappearing. We only have to wait for a while to get a more stable deal.

4. The alarm setting is very simple. There are two lines in the indicator. One is the orange signal line that fluctuates up and down, and the other is the fixed zero line of “zero”.

We set it in the alarm. When the signal line passes "zero" from the top, the short signal is sent only when the candle map is completed. When the signal line passes "zero" from "up" below, the signal is sent for a long time when the candlestick is completed.

One trick, the appearance of the signal, is that the price runs in one direction for a while, so it appears at or near the bottom. Because, when we have already made a profit in the transaction, we can make a profit in advance, and we do not need to wait for the opposite signal to stop the profit and reduce the risk of profit retracement.

Because in this market, the fluctuations are very large, and the people who compete are also very fierce. What we need to do is to make every transaction as possible, and we are all profitable. If we sell and find that the price is still rising, please don't feel sorry, don't consider eating all the profits.

6. When the signal appears, in most cases, even in the impact trend, it will still run a distance in the direction of the signal, that is, you will profit, so please close the position and make a profit in time. Otherwise, when the price volatility is too small, you miss the profit point, the price starts to run in the opposite direction, and you may change from profit to loss.

BITMEX's trailing stop loss is a great feature, please use it flexibly.

7, if it is a shock trend, please try not to trade.

8. We recommend that you turn on the “cryptomars 2.0” and “cryptomars 1.0” indicators. No matter who signs the trade first, you can trade, which can help you get more profit.

9. Remember, I hope this indicator will be your powerful assistant, but please don't rely on it completely. Learning more trading knowledge and skills is even more important. Therefore, when we consider the profitable position, you can use your trading skills, MACD , KDJ, etc. to assist and profit in a more suitable position.