RSI Overbought/Oversold + Divergence IndicatorDESCRIPTION:

This script combines the Relative Strength Index ( RSI ), Moving Average and Divergence indicator to make a better decision when to enter or exit a trade.

- The Moving Average line (MA) has been made hidden by default but enhanced with an RSIMA cloud.

- When the RSI is above the selected MA it turns into green and when the RSI is below the select MA it turns into red.

- When the RSI is moving into the Overbought or Oversold area, some highlighted areas will appear.

- When some divergences or hidden divergences are detected an extra indication will be highlighted.

- When the divergence appear in the Overbought or Oversold area the more weight it give to make a decision.

- The same color pallet has been used as the default candlestick colors so it looks familiar.

HOW TO USE:

The prerequisite is that we have some knowledge about the Elliot Wave Theory, the Fibonacci Retracement and the Fibonacci Extension tools.

Wave 1

(1) When we receive some buy signals we wait until we receive some extra indications.

(2) On the RSI Overbought/Oversold + Divergence Indicator we can see a Bullish Divergence and our RSI is changing from red to green ( RSI is higher then the MA).

(3) If we are getting here into the trade then we need to use a stop loss. We put our stop loss 1 a 2 pips just below the lowest wick. We also invest maximum 50% of the total amount we want to invest.

Wave 2

(4) Now we wait until we see a clear reversal and here we starting to use the Fibonacci Retracement tool. We draw a line from the lowest point of wave(1) till the highest point of wave (1). When we are retraced till the 0.618 fib also called the golden ratio we check again the RSI Overbought/Oversold + Divergence Indicator. When we see a reversal we do our second buy. We set again a stop loss just below the lowest wick (this is the yellow line on the chart). We also move the stop loss we have set in step (3) to this level.

Wave 3

(5) To identify how far the uptrend can go we need to use the Fibonacci Extension tool. We draw a line from the lowest point of wave(1) till the highest point of wave (1) and draw it back to the lowest point of wave (2). Wave (3) is most of the time the longest wave and can go till it has reached the 1.618 or 2.618 fib. On the 1.618 we can take some profit. If we don't want to sell we move our stop loss to the 1 fib line (yellow line on the chart).

(6) We wait until we see a clear reversal on the Overbought/Oversold + Divergence Indicator and sell 33% to 50% of our investment.

Wave 4

(7) Now we wait again until we see a clear reversal and here we starting to use the Fibonacci Retracement tool. We draw a line from the lowest point of wave(2) till the highest point of wave (3). When we are retraced till the 0.618 fib also called the golden ratio we check again the RSI Overbought/Oversold + Divergence Indicator. When we see a reversal we buy again. We set again a stop loss just below the lowest wick (this is the yellow line on the chart).

(8) If we bought at the first reversal ours stop los was triggered (9) and we got out of the trade.

(9) If we did not bought at step (7) because our candle did not hit the 0.618 fib or we got stopped out of the trade we buy again at the reversal.

Wave 5

(10) To identify how far the uptrend can go we need to use the Fibonacci Extension tool. We draw a line from the lowest point of wave(2) till the highest point of wave (3) and draw it back to the lowest point of wave (4). Most of the time wave 5 goes up till it has reached the 1 fib. And that is the point where we got out of the trade with all of our investment. In this trade we got out of the trade a bit earlier. We received the sell signals and got a reversal on the Overbought/Oversold + Divergence Indicator.

We are hoping you learned something so you can make better decisions when to get into or out of a trade.

If you have any question just drop it into the comments below.

FEATURES:

• You can show/hide the RSI .

• You can show/hide the MA.

• You can show/hide the lRSIMA cloud.

• You can show/hide the Stoch RSI cloud.

• You can show/hide and adjust the Overbought and Oversold zones.

• You can show/hide and adjust the Overbought Extended and Oversold Extended zones.

• You can show/hide the Overbought and Oversold highlighted zones.

• Etc...

HOW TO GET ACCESS TO THE SCRIPT:

• Favorite the script and add it to your chart.

REMARKS:

• This advice is NOT financial advice.

• We do not provide personal investment advice and we are not a qualified licensed investment advisor.

• All information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, expressed or implied herein, are for informational, entertainment or educational purposes only and should not be construed as personal investment advice.

• We will not and cannot be held liable for any actions you take as a result of anything you read here.

• We only provide this information to help you make a better decision.

• While the information provided is believed to be accurate, it may include errors or inaccuracies.

Good Luck and have fun,

The CryptoSignalScanner Team

在腳本中搜尋"wave"

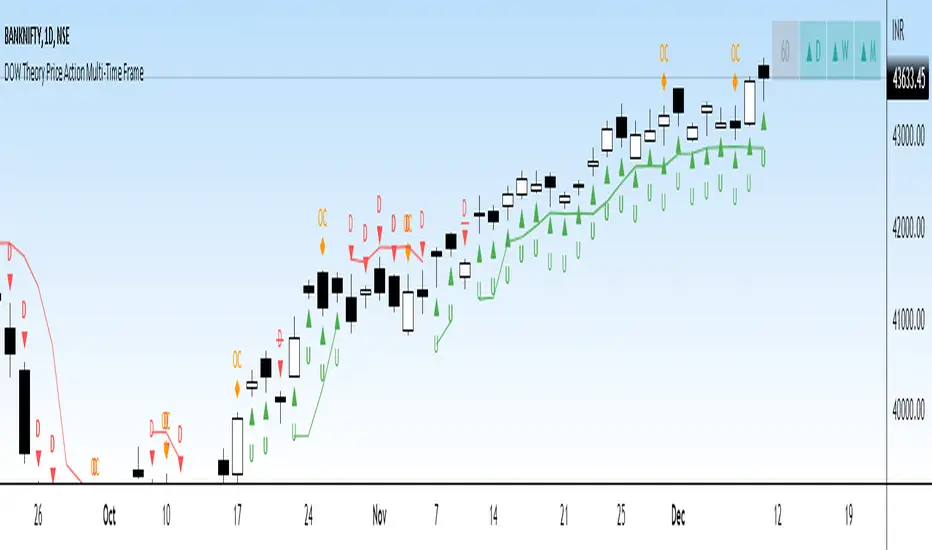

DOW Theory Price Action Multi-Time FrameThis indicator gives a visual representation of Dow Theory Price action based trend analysis and provides trader a table with 4 different timeframe to align with the trend.

It will help traders identify if it is an ongoing Impulse Wave or a Corrective Wave.

3 rules for Bullish Price Action setup (Uptrend or continuation of existing UpTrend): Denoted by 'U' below the candlestic

HH - Higher High

HL - Higher Low

CAH - Close above prior High

3 rules for Bearish Price Action setup (Downtrend or continuation of existing DownTrend): Denoted by 'D' below the candlestic

LH - Lower High

HL - LowerLow

CAH - Close below prior Low

Exception - Outside Candle: Denoted by 'OC' above the candlestic

Outside reversal is a two-day price pattern that shows when a candle or bar on a candlestick or bar chart falls “outside” of the previous day's candle or bar.

The table posistion can be set be user from the input settings as per his screen setting / resolution.

The trailing line can is also customizable from inputs, recomended value is 3-4.

Ideation Credits: Mr. Vineet Jain

SeongMo_MA_V3(Elliot_helper)Made to make it easier to count Elliott waves.

If you renew your new high price, you'll continue your new high price

When the new low is renewed, the new low is continued.

If you are within the range of the previous candle, use the ratio of the difference between the median value of the previous candle and the closing price of the current candle to determine whether to continue the high or low price.

If a can with a tail that updates a new high price and a new low price at the same time comes out, the phrase "Check_candle!" appears to mean that you should check it with a lower time zone candle.

Musashi_Katana=== Musashi-Katana ===

This tool was designed to fit my particular trading style and personal theories about the "Alchemy of the markets" and ''Harmonic Structure'.

Context

When following a Technical approach to to surf the markets, there are teachings that must be understood before reaching a confort-zone, this usually happen the possible worst way by constant experimentation, it hurts.

Here few technical hints:

- Align High timeframes with lower timeframes:

This simple concept relax a lot complexity of finding of a trend bias. Musashi-Katana allows you to use technical indicator corresponding to specific timeframes, like daily weekly or yearly. They wont change when you change the chart's timeframe, its very useful as you know where you're standing in the long term, Its quite relaxing.

- Use volume:

The constant usage of volume will allow you to sync with the market's breathing. This shows you the mass of money flowing into and out of the market, is key if you want to understand momentum. This tool can help here, as it have multi-period vwaps. You can use yearly, monthly for swing trading, and even weekly if you enjoy scalping.

Useful stuff:

- You have access to baselines, AMA and Kijun-sen with the possibility of adding ATR bands.

- AMAs come as two lines strategies for different approaches, fast medium or slow.

- You can experiment with normal and multi timeframe moving averages and other trend tools.

Final Note

If used correctly Musashi-Katana is a very powerful tool, which makes no sense as there is no correct usage. Don't add everything at the same time, experiment, combine stuff, every market is different.

Backtest every possible strategy before using it, see what works and doesn't. This gives you a lot of peace, specially while you're at the tip of the spear surfing the markets

--> I personally use this in combination with 'Musashi_Slasher (Mometum+Volatility)', as it gives me volatility and momentum in a very precise way.

[blackcat] L2 Handicap Volume for StocksLevel 2

Background

Handicap volume is a way to understand market logic.

Function

I have studied many classic trading textbooks about volume. Most textbooks tell me that the most authentic indicator in the world is the trading volume, because other things can be faked, but the trading volume is real, and the real money is there, so it cannot be faked! But now, almost everyone knows that if you place an order there, and then eat it yourself, and the volume comes out, it does not reflect the real long-short will of the market.

So why is volume still considered the most important technical indicator by many successful traders in the stock market? Here is to distinguish from the duration and intensity of the trading volume, the actions of the main whales. It's like in the sea, small fish and shrimp can only create ripples, while whales can set off huge waves. When you need to fish, you must go to the sea with both ripples and huge waves. If the volume of a stock or a currency can fluctuate evenly or pulse ECG, the price will move unnaturally, and it will also be small fluctuations or ECG. This corresponds to a group of small fish and shrimp retail investors gathering, or stocks or altcoins with high control of whales, these two cannot participate. Otherwise, either your money will be wasted there, or you will be taken over by the unscrupulous project party with high control area.

This technical indicator is the handicap trading volume and turnover rate indicators. You can see clearly the type of funds operating on this target in a suitable time period, and thus determine whether this target is in line with your trading style and whether you want to participate Among them and so on.

My technical indicator is mainly to clearly see whether there are main whales participating in the stock by distinguishing the trading volume and the enlarged turnover rate. Its main purpose is to judge the character of the stock, that is, the nature of the stock. And in the yellow and purple positions with high turnover rates, it prompts the behavior of the main whales. This is just a reminder. As for whether the main whale will attack or retreat, you need to conduct an in-depth analysis based on market logic. This analysis data has gone beyond the scope of ordinary candle chart analysis, and requires additional dimensions of information to assist judgment.

Remarks

Feedbacks are appreciated.

Bearish Market Indicator V2Definition

Have you ever wonder whether if the stock/index/market is "bearish" ? A Bearish Market Indicator (B.M.I) is not a new concept, the definition is simply 20% lower from the recent (term: short-term, recent: usually within a year, a.k.a 1 year) highs (closing price with in the recent period or within in a year or simply a 52-Week High). It is called “bearish” by definition when the closing price is below 20% from the highest price within the year (52-Week high: Green Line). To visualize the “20%” below the recent highs, there is a plot (line: light yellow color in the middle) called a Bearish Market By Definition Value. For example, the SPX 500 has been in a bearish market which is why there is a purple color highlight over the 52-Week High (green line) since September 21, 2022 because the closing price is below the Bearish Market By Definition Value (light yellow color) or “20% below the recent highs”. Finally, there is a red line under in the graph and it is the lowest price within a year. So when you hear, “this ticker is at a 52-Week Low”, you know what it means.

Line Summary:

Green Color Line = 52-Week High

Yellow Color Line = 20% away from the 52-Week High or Bearish Market By Definition Value

Red Color Line = 52-Week Low

Color Summary:

Red Color = Bad

Saturated Red Color = Very Bad

Purple Color = Bearish (It may look pink: red + purple)

White Color = Less Bad (That’s because there is no certainty only probability)

Green Color = Not too Bad (That’s because there is no certainty only probability)

Now to more complicated Metrics

>> If you do not like the technical indicators, go to the indicator settings, uncheck the tables. Otherwise, please continue reading. <<

Pre-requisites

+ Understand that the indicators are lagging indicators.

+ Using it under “D” or “Day” interval

+ Already Understand: Moving Averages, Stochastic-RSI, RSI, Super Trend and MACD.

+ Please be aware that this might not be compatible with traders!

Indicators

This B.M.I is fused (comprised, combined) with multiple indicators:

- Moving Averages

I would not rely just on the Moving Averages (MA) since it is a lagging indicator. The values are derived by finding the differences with respect to the MAs (between the closing price and with the respect MA).

- Stochastic-RSI

Stochastic and RSI combo with RSI-Color coating. The first value is the rsi-stochastic-k followed by the rsi-stochastic-d both are compartmentalized with “|”.

Parameter:

Numbers > 80 Not Good

Numbers < 20 Is it time? (You can manually verify the lines (k, d) or the values from them)

- Relative Strength Index (RSI)

The first value is the rsi followed by the rsi-ma both are compartmentalized with “|”. It is also coated with RSI-color.

Parameter:

Numbers > 70 Overbought | Color Red

If the RSI > RSI’s MA = Green

If the RSI < RSI’s MA = Red

Numbers < 30 Oversold | Color Red

- Moving Averages Convergence Divergence (MACD)

The first value is the MACD-line followed by the signal-line both are compartmentalized with “|”.

Macd-line > signal line = green

Macd-line < signal line = red

- Supertrend (please look up from the documentation; i can not embed the link)

Think of this way, you’re riding a wave. If the wave is climbing, expect the price to follow.

Direction < 0 = Green

Direction > 0 = Red

- Other Trend similar to supertrend

This is similar to the Super Trend according the some. Imagine you’re drawing a trend line manually within 6 months.

Within the period, the line gets smoothed over and over til the n=9.

> If the closing is less than the 9th value, it implies the trend is slowing down.

Usage

Adjustments

+ Since there are different holidays from different countries, you can change the BMI-Period from the indicator settings “BMI-4khansolo”.

+ You can hide Technical Indicator Tables, it is also under the settings (see above).

> This will show red over the 52-Week high if it tests for positive .

Purpose

Do you like eating the same food over and over? No! I love different food! I also love a variety of indicators. Especially, I love having MULTIPLE indicators presented in one canvas at the same time (personalized).

After spending a lot of time, I want to share my “FOOD” which is made of different ingredients (indicators) with someone who appreciates food! This Makes me a chef isn't it? Yes! Chef!

Questions?

If you have questions or spotted errors, please comment them below so that I can improve.

Sources

All the materials (i.e., functions like ta.rsi, etc...) used in here are available in the platform.

All the references or sources materials are commented with the code since the I am not allowed to put them here.

Unified Composite Index [UCI] [KuraiBlu] [LazyBear]The purpose of this indicator is to combine the four basic types of indicators (Trend, Volatility, Momentum and Volume) to create a singular, composite index in order to provide a more holistic means of observing potential changes within the market, known as the Unified Composite Index . The indicators used in this index are as follows:

Trend - Trend Composite Index

Volatility - Bollinger Bands %b

Momentum - Relative Strength Index

Volume - Money Flow Index

The average price source can’t be altered as I’ve made it an average between ((open + close) / 2) and ((high + low) / 2).

The best way to use this is by observing several of the indicators at once in conjunction with the average, rather than simply using the average produced to determine the right moment to enter, or exit a trade by itself. I've found when one indicator goes way out of bounds relative to the other three (and subsequently, the average array), then it presents a good buying, or selling opportunity.

Some adjustments were made to several of the indicators in order to standardize them on a scale of 1-100 so that they could better accommodate the average array that was finally produced. Thanks to LazyBear for letting me strip down the WaveTrend Oscillator.

Possible RSI [Loxx]Possible RSI is a normalized, variety second-pass normalized, Variety RSI with Dynamic Zones and optionl High-Pass IIR digital filtering of source price input. This indicator includes 7 types of RSI.

High-Pass Fitler (optional)

The Ehlers Highpass Filter is a technical analysis tool developed by John F. Ehlers. Based on aerospace analog filters, this filter aims at reducing noise from price data. Ehlers Highpass Filter eliminates wave components with periods longer than a certain value. This reduces lag and makes the oscialltor zero mean. This turns the RSI output into something more similar to Stochasitc RSI where it repsonds to price very quickly.

First Normalization Pass

RSI (Relative Strength Index) is already normalized. Hence, making a normalized RSI seems like a nonsense... if it was not for the "flattening" property of RSI. RSI tends to be flatter and flatter as we increase the calculating period--to the extent that it becomes unusable for levels trading if we increase calculating periods anywhere over the broadly recommended period 8 for RSI. In order to make that (calculating period) have less impact to significant levels usage of RSI trading style in this version a sort of a "raw stochastic" (min/max) normalization is applied.

Second-Pass Variety Normalization Pass

There are three options to choose from:

1. Gaussian (Fisher Transform), this is the default: The Fisher Transform is a function created by John F. Ehlers that converts prices into a Gaussian normal distribution. The normaliztion helps highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

2. Softmax: The softmax function, also known as softargmax: or normalized exponential function, converts a vector of K real numbers into a probability distribution of K possible outcomes. It is a generalization of the logistic function to multiple dimensions, and used in multinomial logistic regression. The softmax function is often used as the last activation function of a neural network to normalize the output of a network to a probability distribution over predicted output classes, based on Luce's choice axiom.

3. Regular Normalization (devaitions about the mean): Converts a vector of K real numbers into a probability distribution of K possible outcomes without using log sigmoidal transformation as is done with Softmax. This is basically Softmax without the last step.

Dynamic Zones

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

7 Types of RSI

See here to understand which RSI types are included:

Included:

Bar coloring

4 signal types

Alerts

Loxx's Expanded Source Types

Loxx's Variety RSI

Loxx's Dynamic Zones

Mark StructureMark Structure is building the market swing structure, minor and sub structure and marks all possible insignificant pivots

Building such structure is really complex task to do, that has a lot of obstacles and challenges. I'm doing my best to develop this indicator behaving in absolutely expectable and right way. Fill free to leave any comments or bug reports.

it supports:

- Marking all pivots with labels or join them continuously with trend lines.

- Marking minor and sub structured swings with labels or join them continuously with trend lines. Marking BOS or SMS BOS, which are mbos. Minor and substructure are structures inside swing structure and it can differ from the structure of lower timeframe

- Marking swings of swing structure with labels or join them continuously with trend lines. Marking BOS or SMS BOS of swing structure

- Changing bullish and bearish colors of each kind of structures

- Changing pivot labelings

- Changing colors of BOSs

Remarks:

- As I told you guys before, it has a lot of challenging cases. eg we have swing low and high on the same candle and in order to decide which pivot goes first I take lower time frame data to figure out what pivot is the first, but it happens that on lower time frame the same issue takes place, due to limitation of TradingView I can't go infinitely to lower timeframes to solve this issue, so I mark those cases with labels

- Another issue is very beginning of the trend its hard to detect swing structure there due to missing historical data. so skip a few waves in the very beginning

- Don't expect to have minor and sub structure in each swing waves, its totally fine when you don't have them at all

- Swing structure is the most significant structure and shows real price direction. Trend change is confirmed when for bull->bear the last HLbull LH>HH and HH-HL-HH are confirmed. You can change labelling for unconfirmed swing trend in the settings. By default its already done

Cumulative ATR Distance Oscillator// A Price/ATR oscillator with cumulative waves.

// Based on Cumulative Volume Delta, but using price movement alone.

// Public Domain

// By Jolly Wizard

Abraham Trend [Loxx]Indicator based on "Trading the Trend" article by Andrew Abraham published in TASC.

There has been a lot of "reincarnations" and renamed versions of this system, but since the indicator is quite good, it seemed useful to create the original version.

What is the Abraham Trend?

New traders quickly become familiar with two adages: "The trend is your friend," and "Let your profits run and cut your losses." Many of us, however, have learned the hard way that these things are easier said than done. Why is that? One reason is lack of recognition, since the trend itself is rarely clarified and defined, let alone where it starts and ends. So we need a clear explication of what a trend is as well as where its beginning and its end are.

SIMPLE ENOUGH

Simply, if the trend is considered up, then the trend of prices are composed of upwaves and the downwaves are countertrend movements. Downward trends are the opposite, seen as downwaves with countertrend upwaves. Using several tools and functions, we can design a quantifiable approach to defining these waves. My favorite is the volatility indicator, which is a formula that measures the market volatility by plotting a smoothed average of the true range. The true range indicator originates from the work of J. Welles Wilder Jr. from his New Concepts in Technical Trading Systems. The definition of the true range is defined as the largest of the following:

The difference between today's high and today's low

The difference between today's high and yesterday's close, or

The difference between today's low and yesterday's close.

The calculation uses a 21-period weighted average of the true range, giving higher weight to the true range of the most recent bar. The final value is then multiplied by 3.

The volatility indicator is used as a stop-and-reverse method. Let's say the market has been rising, then the volatility indicator is calculated each day and subtracted from the highest close during the rising market. The highest close is always used, even if there has been a series of lower closes since the highest close. If the market closes below the volatility indicator, then for the next day, the current reading of the volatility indicator is added to the lowest close. This step is followed each day until the market closes above the trailing volatility indicator.

We now have a definition of the trend. An upward trend exists as long as the volatility indicator is below the market and a downtrend is in force if the volatility indicator is above the market.

even_better_sinewave_mod

Description:

Even better sinewave was an indicator developed by John F. Ehlers (see Cycle Analytics for Trader, pg. 159), in which improvement to cycle measurements completely relies on strong normalization of the waveform. The indicator aims to create an artificially predictive indicator by transferring the cyclic data swings into a sine wave. In this indicator, the modified is on the weighted moving average as a smoothing function, instead of using the super smoother, aim to be more adaptive, and the default length is set to 55 bars.

Sinewave

smoothing = (7*hp + 6*hp_1 + 5*hp_2+ 4*hp_3 + 3*hp_4 + 2*hp5 + hp_6) /28

normalize = wave/sqrt(power)

Notes:

sinewave indicator crossing over -0.9 is considered to beginning of the cycle while crossing under 0.9 is considered as an end of the cycle

line color turns to green considered as a confirmation of an uptrend, while turns red as a confirmation of a downtrend

confidence of using indicator will be much in confirmation paired with another indicator such dynamic trendline e.g. moving average

as cited within Ehlers book Cycle Analytic for Traders, the indicator will be useful if the satisfied market cycle mode and the period of the dominant cycle must be estimated with reasonable accuracy

Other Example

Jurik Filtered, Composite Fractal Behavior (CFB) Channels [Loxx]Double Jurik-Filtered Composite Fractal Behavior (CFB) Channels is a channel indicator that acts as both a baseline, similar to Donchian, and as support and resistance levels. This indicator is price time adaptive meaning it flexes to price volatility waves. The indicators adaptive nature is calculated using the Composite Fractal Behavior (CFB) algorithm. The result of this adaptive calculation is then smoothed using Jurik Filtering, and then it's normalized to conform to a range of values. This helps better identify trends.

What is Composite Fractal Behavior (CFB)?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

Bollinger but BetterA better Bollinger Band with an average of 20 EMAs as pivot price, which makes its standard deviation way more sensitive compared to traditional Bollinger Band.

-- My Tips --

Long flat convergence suggests a big potential price movement.

Short quick convergence of short supportive ema(default: 10days) and upper band suggests a safe middle entry point.

Recommended auxiliary indicator: Wavetrend by Lazybear, which points out entry and exit points quite accurately in bull market.

-- PS --

This system is a hybrid of EMA Ribbons and Bollinger Band.

[blackcat] L2 Ehlers LoopsLevel 2

Background

John Ehlers’ articles in the June issues on 2022,“Ehlers Loops, Part 1”

Function

In his article in this issue, “Ehlers Loops,” John Ehlers presents some concepts of price and volume relationship to determine if any predictive value can be obtained by the analysis. In the analysis, both price and volume are filtered using high-pass and low-pass filters with the result delivering the desired data wavelengths. The author suggests that the resulting Ehlers Loops are a way to discretionarily predict bullish and bearish moves that are based on the curvature and direction of rotation of motion in the price-volume chart.

Remarks

Feedbacks are appreciated.

MA ClustersBackground :

This study allows to define ranges for contraction and expansion of a defined set of MA to analyse the the momentum at those specific situations.

In general all functions used are very basic but allows the user to set alerts when a cluster of MA enters a defined range within or outside the MAX and MIN of a selected MA cluster. The predefined length of the EMAs were put together by HurstHorns within a trading learning discord group and are designed for 1M timeframe to read the momentum for scalping entries - Thanks again for sharing.

Functions :

currently the following MA are available:

- ema

- sma

- smma

- wma

- vwma

- vma

the variable moving average is based on the calculation from lazybear.

- RSI Stoch Filter

- Wavetrend OB/OS filter

Currently only alerts for contraction are enabled to not overload the study but in case expansion would be from interest this can be added quickly.

Outlook:

Additional filters were added to see if they can add value in. the decision making or by simply filtering out noise. This is still quite experimental. Please share any useful observation I should add as additional filter option to find good setups. in relation to contractions or expansions.

Next version will get Bollinger bands for 1 selectable MA from the list for additional study options.

In case you are interested in more options such as more MA types or vwap.. just let me know. for VMA I need to do more research to add useful function for laddering or things like that.

In general The script itself can be easily extended by additional functions. As this is one of my first scripts the code itself might not be optimal or there are more elegant ways to come to the same goal. However please use for study purposes only and report bugs or enhancement requests.

good luck and happy trading!

TASC 2022.06 Ehlers Loops█ OVERVIEW

TASC's June 2022 edition Traders' Tips includes an article by John Ehlers titled "Ehlers Loops. Part 1". This is the code implementing the price-volume Ehlers Loops he introduced in the publication.

█ CONCEPTS

John Ehlers developed Ehlers loops as a tool to visualize the performance of one data stream versus another, both filtered and scaled. In this article, the author applies his concept to exploit and/or dispel the dogmatic principles of reliable price-volume relationships.

The script offers two different ways to visualize Ehlers Loops:

Oscillators (default option)

In this implementation, filtered and scaled volume is plotted along with filtered and scaled price as zero-mean oscillators. Observation of the relative direction of volume and price oscillators can be discretionarily used to interpret and predict market conditions. For example, it is generally assumed that an increase in volume and an increase in price define a bullish condition. Similarly, decreasing volume and increasing price are generally considered bearish. A decrease in volume and a decrease in price is considered a bullish condition. The increase in volume and decrease in price is often thought to be bearish.

Scatterplot

This Crocker-style visualization displays filtered and scaled price against filtered and scaled volume for the selected timespan. Fluctuations in volume are plotted along the x -axis, while price changes along the y -axis. This way of visualizing the Ehlers Loop allows you to analyze the curvature and directional path of the price in relation to volume, offering a different comparative perspective. The boundaries of the price and volume scale on the Ehlers Loop Crocker-chart are presented in standard deviations. Deviations can be used to predict possible future price or volume fluctuations. The expected probability of potential reversals is 68%, 95% and 99.7% at one, two and three standard deviations, respectively.

█ CALCULATIONS

The following steps are used to build an Ehlers Loop:

• Both price and volume are filtered to be band-limited signals. This is done by applying the high-pass Butterworth filter in combination with the low-pass SuperSmooth filter.

The cutoff wavelengths of the high-pass and low-pass filters are defined by the input parameters HPPeriod and LPPeriod , respectively.

These values change the appearance of the Ehlers Loops and can be customized to your trading style.

• The filtered price and volume time series are then scaled in terms of standard deviation by dividing each by their root-mean-square values.

• The resultant price and volume data are plotted as zero-mean oscillators or as a scatterplot.

Too Many Cooks trend indicatorToo many Cooks in The Kitchen

You have probably heard the adage "Too many cooks spoils the broth" before. The meaning behind it is obviously that when to many people are trying to work on the same task at once it simply devolves into a fight for control and creates a mess of the situation. But is this true for indicators is the question I had and thus I made this indicator, a simple combination of 8 random trend finding indicators I assembled (A list of these indicators and their authors will be available at the bottom of this page) . Is it any good though ? In short yes, it is a decent trend finding indicator and could likely be used in your strategy in the place of your current trend finding indicator if you so wish. However much of the versatility of the individual indicators IS lost and would not be possible to get back in this big mess of a broth, so this indicator will not be the be all end all of trend indicators nor will it be a free money machine like you may be expecting looking at the list of included indicators so the adage was correct to a degree.

List of Authors and their included indicators

Trading View defaults:

MACD (Modified by me)

Stochastic RSI (Modified by me)

Lazy Bear:

Wavetrend Oscilator (Modified by me)

Traders Dynamic Index (Modified by me)

HACOLT (Modified by me)

Algokid

AK Trend

Racer8

Average Force

KivancOzbilgic

Average Sentiment Osclilator

Moving Avareges CrossIn this script I have combined 3 indicators Ichimoku, Heiken Ashi and Moving Average Exponential.

In this strategy, you should first look for the current market trend in low time frames.

Then look at the higher time frames to decide if you are in the right place to enter the trade.

For example, in 1 minute time frame, we first look at whether the two averages 21 and 233 had a cross or not.

If the moving average of 21 crosses the moving average of 233 from the bottom up and the end of the line moves the moving average of 233 upwards, it can be concluded

The market trend in time frame has changed for 1 minute and is up.

Then we refer to the time frames of 3, 5 and 15 minutes and check the same conditions there.

If 3 of the 4 time frames have the same conditions, we use Heiken Ashi to check the strength of the wave that is formed.

And also by looking at Ichimoku we will see where this Kumo cloud formed this wave.

If these conditions are met, a serious decision can be made to enter the position.

Higher time frames such as 30 minutes or 1 hour and 4 hours can also be used to find important resistance and support pivots.

In this way, the average of 233 and 21 and the formation of the current candlestick give us an acceptable range for fluctuation.

FARAZ.MATI20vA personal indicator.

This indicator has the following features :

Thanks to the managers and administrators of TradingView site for the appropriate space with wide facilities for optimal use. All (indicators) were available on the site and I only defined certain settings for them.

FARAZ.MATI20v

EMA: 5

SMA : 20

SMA : 50

Collision and interruption of Moving 20 by Moving 5 can be the beginning of an upward trend. Provided that the Moving 5 is placed under the candles. (The best signal for the Moving 5 is to collide with the Moving 20 under the candles). Also, the collision of the Moing 5 with the Moing 20 on top of the candles can be a sign of falling. Especially if this collision occurs above the candles.The cut of the Moving 20 and the Moving 50 indicate the intensity of the wave. If Moving 20 is above Moving 50 in this collision, it shows the intensity of the uptrend and if it is below Moving 50, it shows the intensity of the downtrend.

SMA : 100

SMA : 200

Both (resistance and support) are very strong, which is very effective in larger timeframes (such as 1 day).

HMA : 20

To determine the entry point. In such a way that whenever the seeds (HMA) are below the candlesticks. 3 seeds are in ascending position. The body of the candle and the shadow should not touch them. It can be a good signal to enter. Also if the seeds are placed on top of the candlesticks. Show the descending direction of 3 seeds. Provided that the body of the candle and the shadow have not hit them. It is a signal for the short position.

SAR : With the applied settings, it is a kind (trending view) that can evaluate the volume of input to any currency much sooner and determine the probability of rising or falling. If our wave lines (stairs) are at the bottom of the candles, it means an upward trend, and if they are at the top of the candles, it means a downward trend. As the volume of inputs increases, the trend increases, and as the volume of inputs decreases, the trend will also decrease.

Ichimoku Cloud : To determine the lines (support and resistance) the peaks formed by the cloud can represent a resistance area. Price To cross the area marked by the Ichimoku cloud must have a strong candle. This can be very effective in determining the point of entry and purchase.

zig zag : For better diagnosis of the process. Using it to determine areas of support and resistance can be useful. Determining the points of the Fibonacci table is also very effective.

TradingGroundhog - Strategy & Fractal V1#-- Public Strategy - No Repaint - Fractals -- Short term

Here I come with another script, more simple than Wavetrend V1. You will love it.

#-- Synopsis --

Another simple idea, on a small time frame (15 min) we buy when the opening price goes below a Bottom fractals and sell when it goes over a Top fractals, but as this script do not use Wavetrends. You should stop by your self to use the script during long lasting downtrends.

I developed the strategy using BTC /EUR 3 MIN BINANCE but it can be applied to many other cryptos, I don't know for forex or others. You can use it for short term (to a month of uptrend) and automated trading.

#-- Graph reading --

And now, how to read it ?

Fractals:

Yellow Flags occur when the opening price goes below a Bottom fractal , it means Buy.

White Flags appear when the opening price goes over a Top fractal , it means Sell.

#-- Parameters --

*** Parameters have been intensively optimized using 10 cryptocurrency markets in order to have potent efficiency for each of them. I would recommend to only change the Can Be touch parameter. For the others, I don't recommend any modifications. The idea behind the script is to be able to switch between markets without having to optimize parameters, less work, easy to target active crypto and therefor limit the risks. ***

Can be touch :

'Filter fractals' : Activate or Disable the filtering fractal operation. If Enable, buy during less risky periods. (Activate is often better)

Can be touch but not necessary :

'VolumeMA' : The Volume corrector used by the fractals

'Extreme window' : The number of price individuals to look for if we want to remove extreme fractals.

Not to touch :

'Long Sop Loss (%)' : The minimal difference of price between a Fractal bottom and the opening price to buy.

#-- Time frame --

Should be used with the following time frames depending on the necessity:

1 MIN

3 MIN (Preferred with the parameters set)

5 MIN

#-- Last words --

The script can be set up to send Tradingview signals to 3comma just by adding comment = " " in strategy.close_all() and strategy.entry().

Good trades !

Disclaimer (As it should always be one to any script)

***

This script is intended for and only to be used for personal purposes only. No such information provided by it constitutes advice or a recommendation for any investment or trading strategy for any specific person. There is no guarantee presented or implied as to the accuracy of specific forecasts, projections, or predictive statements offered by the script. Users of the script agree that its original developer does not take responsibility for any of your investment decisions. Please seek professional advice before trading.

***

# Here are the results from the 20rst of September 2021 with 100% of equity on the BTC /EUR 3 Min and with a capital of 10 000 EUR. So almost, one month.

# As I saw, it goes from +30% to more than +160% (the great SHIB) depending on the selected crypto. It may be negative if you spot a downtrend.

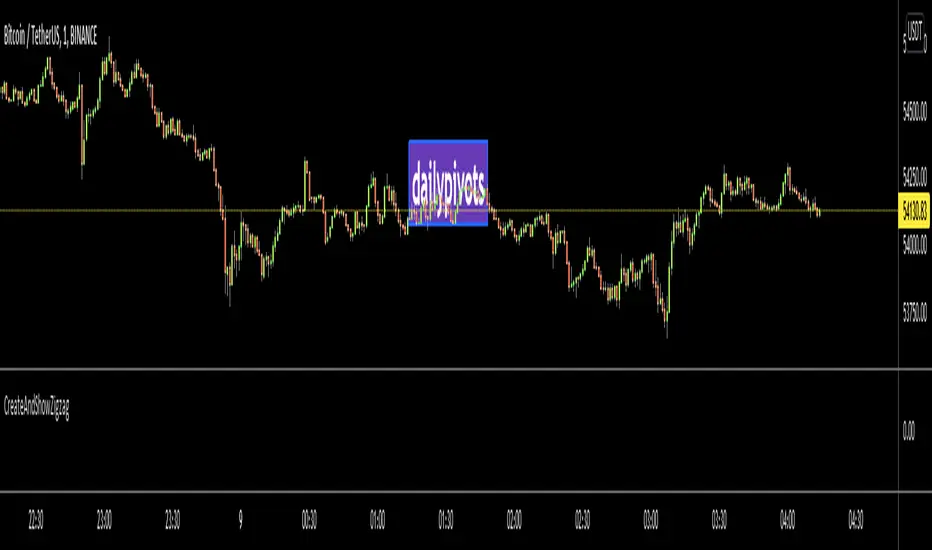

CreateAndShowZigzagLibrary "CreateAndShowZigzag"

Functions in this library creates/updates zigzag array and shows the zigzag

getZigzag(zigzag, prd, max_array_size) calculates zigzag using period

Parameters:

zigzag : is the float array for the zigzag (should be defined like "var zigzag = array.new_float(0)"). each zigzag points contains 2 element: 1. price level of the zz point 2. bar_index of the zz point

prd : is the length to calculate zigzag waves by highest(prd)/lowest(prd)

max_array_size : is the maximum number of elements in zigzag, keep in mind each zigzag point contains 2 elements, so for example if it's 10 then zigzag has 10/2 => 5 zigzag points

Returns: dir that is the current direction of the zigzag

showZigzag(zigzag, oldzigzag, dir, upcol, dncol) this function shows zigzag

Parameters:

zigzag : is the float array for the zigzag (should be defined like "var zigzag = array.new_float(0)"). each zigzag points contains 2 element: 1. price level of the zz point 2. bar_index of the zz point

oldzigzag : is the float array for the zigzag, you get copy the zigzag array to oldzigzag by "oldzigzag = array.copy(zigzay)" before calling get_zigzag() function

dir : is the direction of the zigzag wave

upcol : is the color of the line if zigzag direction is up

dncol : is the color of the line if zigzag direction is down

Returns: null

ArrayGenerateLibrary "ArrayGenerate"

Functions to generate arrays.

sequence_int(start, end, step) returns a sequence of int numbers.

Parameters:

start : int, begining of sequence range.

end : int, end of sequence range.

step : int, step, default=1 .

Returns: int , array.

sequence_float(start, end, step) returns a sequence of float numbers.

Parameters:

start : float, begining of sequence range.

end : float, end of sequence range.

step : float, step, default=1.0 .

Returns: float , array.

sequence_from_series(src, length, shift, direction_forward) Creates a array from a series sample range.

Parameters:

src : series, any kind.

length : int, window period in bars to sample series.

shift : int, window period in bars to shift backwards the data sample, default=0.

direction_forward : bool, sample from start to end or end to start order, default=true.

Returns: float array

normal_distribution(size, mean, dev) Generate normal distribution random sample.

Parameters:

size : int, size of array

mean : float, mean of the sample, (default=0.0).

dev : float, deviation of the sample from the mean, (default=1.0).

Returns: float array.

log_spaced(length, start_exp, stop_exp) Generate a base 10 logarithmically spaced sample sequence.

Parameters:

length : int, length of the sequence.

start_exp : float, start exponent.

stop_exp : float, stop exponent.

Returns: float array.

linear_range(stop, start) Generate a linearly spaced sample vector within the inclusive interval (start, stop) and step 1.

Parameters:

stop : float, stop value.

start : float, start value, (default=0.0).

Returns: float array.

periodic_wave(length, sampling_rate, frequency, amplitude, phase, delay) Create a periodic wave.

Parameters:

length : int, the number of samples to generate.

sampling_rate : float, samples per time unit (Hz). Must be larger than twice the frequency to satisfy the Nyquist criterion.

frequency : float, frequency in periods per time unit (Hz).

amplitude : float, the length of the period when sampled at one sample per time unit. This is the interval of the periodic domain, a typical value is 1.0, or 2*Pi for angular functions.

phase : float, optional phase offset.

delay : int, optional delay, relative to the phase.

Returns: float array.

sinusoidal(length, sampling_rate, frequency, amplitude, mean, phase, delay) Create a Sine wave.

Parameters:

length : int, The number of samples to generate.

sampling_rate : float, Samples per time unit (Hz). Must be larger than twice the frequency to satisfy the Nyquist criterion.

frequency : float, Frequency in periods per time unit (Hz).

amplitude : float, The maximal reached peak.

mean : float, The mean, or DC part, of the signal.

phase : float, Optional phase offset.

delay : int, Optional delay, relative to the phase.

Returns: float array.

periodic_impulse(length, period, amplitude, delay) Create a periodic Kronecker Delta impulse sample array.

Parameters:

length : int, The number of samples to generate.

period : int, impulse sequence period.

amplitude : float, The maximal reached peak.

delay : int, Offset to the time axis. Zero or positive.

Returns: float array.