Industry Indices ComparisonA dynamic industry sector performance comparison indicator that helps traders and investors track relative strength across different market sectors in real-time.

- Compares up to 5 industry sector ETFs against a benchmark index (default: SPY)

- Displays key metrics including:

* Performance % over selected timeframe

* Relative performance vs benchmark

* Trend direction (▲ up, ▼ down, − neutral)

* Volume in millions (M) of shares traded

- Configurable timeframes: 1D, 1W, 1M, and 3M comparisons

- Color-coded performance indicators (green for outperformance, red for underperformance)

- Customizable table position and text size for optimal chart placement

The indicator helps identify:

1. Sector rotation patterns through relative performance

2. Leading and lagging sectors vs the broader market

3. Volume trends across different sectors

For traders, if you are considering two equally good setups, then choosing the setup belonging to a currently strong sector could be beneficial.

在腳本中搜尋"神户胜利+VS+磐田喜悦"

SMT Divergence [TakingProphets]The SMT (Smart Money Technique) Divergence indicator identifies potential market manipulation and smart money footprints by comparing price action between correlated instruments. It uses a dual-detection system to catch both frequent local SMTs and larger structural SMTs:

• Primary detection uses a shorter lookback period (default 5) to identify common SMT patterns

• Secondary detection uses a longer lookback period (default 8) to catch larger structural SMTs

• Automatically filters significant moves to prevent noise

• Labels are placed clearly outside of price action for better visibility

• Toggle between showing all SMTs or only significant liquidity sweeps

Compare any two instruments to spot divergences in their price action. Particularly useful for:

- Futures vs Spot markets

- Related currency pairs

- Index vs its components

- Any correlated instruments

Default settings are optimized for intraday trading but can be adjusted for different timeframes.

Note: This indicator works best when comparing closely correlated instruments and should be used alongside other technical analysis tools.

EMA Study Script for Price Action Traders, v2JR_EMA Research Tool Documentation

Version 2 Enhancements

Version 2 of the JR_EMA Research Tool introduces several powerful features that make it particularly valuable for studying price action around Exponential Moving Averages (EMAs). The key improvements focus on tracking and analyzing price-EMA interactions:

1. Cross Detection and Counting

- Implements flags for crossing bars that instantly identify when price crosses above or below the EMA

- Maintains running counts of closes above and below the EMA

- This feature helps students understand the persistence of trends and the frequency of EMA interactions

2. Bar Number Tracking

- Records the specific bar number when EMA crosses occur

- Stores the previous crossing bar number for reference

- Enables precise measurement of time between crosses, helping identify typical trend durations

3. Variable Reset Management

- Implements sophisticated reset logic for all counting variables

- Ensures accuracy when analyzing multiple trading sessions

- Critical for maintaining clean data when studying patterns across different timeframes

4. Cross Direction Tracking

- Monitors the direction of the last EMA cross

- Helps students identify the current trend context

- Essential for understanding trend continuation vs reversal scenarios

Educational Applications

Price-EMA Relationship Studies

The tool provides multiple ways to study how price interacts with EMAs:

1. Visual Analysis

- Customizable EMA bands show typical price deviation ranges

- Color-coded fills help identify "normal" vs "extreme" price movements

- Three different band calculation methods offer varying perspectives on price volatility

2. Quantitative Analysis

- Real-time tracking of closes above/below EMA

- Running totals help identify persistent trends

- Cross counting helps understand typical trend duration

Research Configurations

EMA Configuration

- Adjustable EMA period for studying different trend timeframes

- Customizable EMA color for visual clarity

- Ideal for comparing different EMA periods' effectiveness

Bands Configuration

Three distinct calculation methods:

1. Full Average Bar Range (ABR)

- Uses the entire range of price movement

- Best for studying overall volatility

2. Body Average Bar Range

- Focuses on the body of the candle

- Excellent for studying conviction in price moves

3. Standard Deviation

- Traditional statistical approach

- Useful for comparing to other technical studies

Signal Configuration

- Optional signal plotting for entry/exit studies

- Helps identify potential trading opportunities

- Useful for backtesting strategy ideas

Using the Tool for Study

Basic Analysis Steps

1. Start with the default 20-period EMA

2. Observe how price interacts with the EMA line

3. Monitor the data window for quantitative insights

4. Use band settings to understand normal price behavior

Advanced Analysis

1. Pattern Recognition

- Use the cross counting system to identify typical pattern lengths

- Study the relationship between cross frequency and trend strength

- Compare different timeframes for fractal analysis

2. Volatility Studies

- Compare different band calculation methods

- Identify market regimes through band width changes

- Study the relationship between volatility and trend persistence

3. Trend Analysis

- Use the closing price count system to measure trend strength

- Study the relationship between trend duration and subsequent reversals

- Compare different EMA periods for optimal trend following

Best Practices for Research

1. Systematic Approach

- Start with longer timeframes and work down

- Document observations about price behavior in different market conditions

- Compare results across multiple symbols and timeframes

2. Data Collection

- Use the data window to record significant events

- Track the number of bars between crosses

- Note market conditions when signals appear

3. Optimization Studies

- Test different EMA periods for your market

- Compare band calculation methods for your trading style

- Document which settings work best in different market conditions

Technical Implementation Notes

This tool is particularly valuable for educational purposes because it combines visual and quantitative analysis in a single interface, allowing students to develop both intuitive and analytical understanding of price-EMA relationships.

3 Drive Harmonic Pattern [TradingFinder] Three Drive Reversal🔵 Introduction

The Three Drive harmonic pattern closely resembles other price structures such as Wedge Pattern and Three Push Pattern, yet it stands out due to its precise use of Fibonacci ratios and symmetrical price movements.

This pattern comprises three consecutive and symmetrical price drives, each validated by key Fibonacci ratios (1.27 and 1.618), which help identify critical Potential Reversal Zones (PRZ).

Unlike the Wedge, which relies on converging trend lines and can indicate either continuation or reversal, and the Three Push, which lacks defined Fibonacci ratios and symmetry, the Three Drive pattern defines PRZ with greater accuracy, providing traders with high-probability trading opportunities.

This pattern appears in both bullish and bearish trends. After the completion of the third drive (Drive 3), it signals the market's readiness to reverse direction. The PRZ in this pattern serves as a crucial zone where price is highly likely to reverse, offering a strategic point for entering or exiting trades. Professional traders utilize the Three Drive pattern and PRZ as essential tools for analyzing and capitalizing on potential market reversals.

Bullish Pattern :

Bearish Pattern :

🔵 How to Use

The Three Drive harmonic pattern is an effective tool for identifying potential reversal points in the market. By utilizing Fibonacci extension levels (1.27 and 1.618) and focusing on the pattern’s symmetry, traders can pinpoint Potential Reversal Zones (PRZ) where the price is likely to change direction. This pattern works in both bearish and bullish scenarios, each with distinct characteristics and trading opportunities.

🟣 Bullish Three Drive Pattern

The bullish Three Drive pattern develops during a downtrend, indicating a potential reversal to the upside. Similar to its bearish counterpart, this pattern features three consecutive downward price movements (drives) with retracements in between. The third drive concludes within the PRZ, which serves as a strong support zone where the price is expected to reverse upwards.

The first drive begins with a downward movement, followed by a retracement to the 0.618 Fibonacci level. The second drive continues downward to reach a 1.27 or 1.618 Fibonacci extension of the retracement. Finally, the third drive aligns with the PRZ, where a confluence of Fibonacci levels creates a high-probability support zone.

In the PRZ, traders look for bullish confirmation signals such as bullish candlestick patterns (e.g., bullish engulfing or pin bars) or increasing trading volume. Once confirmation is observed, the PRZ becomes an ideal entry point for a buy position. Stop-loss orders are placed slightly below the PRZ to minimize risk, while take-profit targets are set at key resistance levels or Fibonacci retracement levels.

🟣 Bearish Three Drive Pattern

The bearish Three Drive pattern forms during an uptrend, signaling a potential reversal to the downside. This pattern consists of three consecutive upward price movements (drives) and intermediate retracements. Each drive aligns with Fibonacci extension levels, and the third drive ends within the PRZ, indicating a high probability of a bearish reversal.

In the first drive, the price moves upward and then retraces to approximately the 0.618 Fibonacci retracement level, forming the base for the second drive. The second drive then extends upward to the 1.27 or 1.618 Fibonacci extension of the preceding retracement. This process repeats for the third drive, which reaches the PRZ, typically defined by the convergence of Fibonacci levels from previous drives.

Once the PRZ is identified, traders look for confirmation signals such as bearish candlestick patterns (e.g., bearish engulfing or pin bars) or declining trading volume. If confirmation is present, the PRZ becomes an optimal zone for entering a sell position. Stop-loss levels are typically placed slightly above the PRZ to protect against pattern failure, and take-profit targets are set at key support levels or Fibonacci retracement levels of the overall structure.

🟣 Three Drive Vs Wedge Pattern Vs 3 Push pattern

The Three Drive, Wedge, and Three Push patterns are all used to identify potential price reversal points, but they differ significantly in structure and application. The Three Drive pattern is based on three consecutive and symmetrical price movements, validated by precise Fibonacci ratios (1.27 and 1.618), to define Potential Reversal Zones (PRZ).

In contrast, the Wedge pattern relies on converging trend lines and does not require Fibonacci ratios; it can act as either a reversal or continuation pattern. Meanwhile, the Three Push pattern shares similarities with Three Drive but lacks precise symmetry and Fibonacci-based validation.

Instead of a PRZ, Three Push focuses on identifying areas of support and resistance, often signaling weakening momentum in the current trend. Among these, the Three Drive pattern is more reliable for pinpointing high-probability reversal zones due to its strict Fibonacci-based and symmetrical structure.

🔵 Setting

🟣 Logical Setting

ZigZag Pivot Period : You can adjust the period so that the harmonic patterns are adjusted according to the pivot period you want. This factor is the most important parameter in pattern recognition.

Show Valid Format : If this parameter is on "On" mode, only patterns will be displayed that they have exact format and no noise can be seen in them. If "Off" is, the patterns displayed that maybe are noisy and do not exactly correspond to the original pattern.

Show Formation Last Pivot Confirm : if Turned on, you can see this ability of patterns when their last pivot is formed. If this feature is off, it will see the patterns as soon as they are formed. The advantage of this option being clear is less formation of fielded patterns, and it is accompanied by the latest pattern seeing and a sharp reduction in reward to risk.

Period of Formation Last Pivot : Using this parameter you can determine that the last pivot is based on Pivot period.

🟣 Genaral Setting

Show : Enter "On" to display the template and "Off" to not display the template.

Color : Enter the desired color to draw the pattern in this parameter.

LineWidth : You can enter the number 1 or numbers higher than one to adjust the thickness of the drawing lines. This number must be an integer and increases with increasing thickness.

LabelSize : You can adjust the size of the labels by using the "size.auto", "size.tiny", "size.smal", "size.normal", "size.large" or "size.huge" entries.

🟣 Alert Setting

Alert : On / Off

Message Frequency : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone : The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

🔵 Conclusion

The Three Drive pattern is a highly effective harmonic tool for identifying potential reversal points in the market. By leveraging its symmetrical structure and precise Fibonacci ratios (1.27 and 1.618), this pattern provides traders with clear entry and exit signals, enhancing the accuracy of their trades.

Whether in bullish or bearish scenarios, the identification of the Potential Reversal Zone (PRZ) serves as a critical aspect of this pattern, enabling traders to anticipate price movements with greater confidence.

Compared to similar patterns like Wedge and Three Push, the Three Drive pattern stands out for its stringent reliance on Fibonacci levels and symmetrical price movements, making it a more robust choice for forecasting reversals. However, as with any technical analysis tool, its effectiveness increases when combined with confirmation signals, such as candlestick patterns, volume analysis, and broader market context.

Mastering the Three Drive pattern requires practice and attention to detail, especially in accurately defining the PRZ and ensuring the pattern adheres to its criteria. Traders who consistently apply this pattern as part of a comprehensive trading strategy can capitalize on high-probability opportunities and improve their overall performance in the market.

52 Week High/Low Tracking TableThis Indicator helps the User to Quickly view Current Closing Price Compared to the Mentioned Period High and Low.

"Bars Back" indicate the period you need to look back. In case of Daily charts 260 Bars Back usually indicate 52 Weeks/1 year. This is set a default. But you can change it as well.

The Indicator will show the data for below:-

1) High - Highest Close price for the Mentioned Period

2) % from High - The Percentage difference between the Current Close Price Vs Highest Close price for the Mentioned Period. (-) indicate that the current close price is lesser then then High Price.

3) Low - Lowest Close price for the Mentioned Period

4) % from Low - The Percentage difference between the Current Close Price Vs Highest Close price for the Mentioned Period. (-) indicate that the current close price is lesser then then High Price.

You can add this indicator to Quickly Scan multiple stocks to see were they stand.

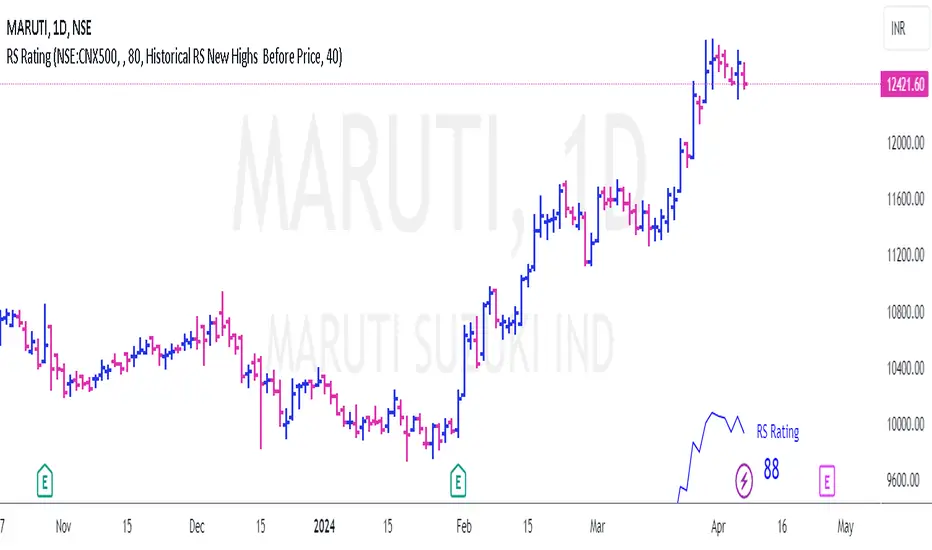

RS Rating for Indian MarketRS Rating for Trading View

This Trading View script calculates the Relative Price Strength (RS) Rating for a given stock. It's a measure of a stock's price performance over the last twelve months, compared to all stocks in a selected Index. The rating scale ranges from 1 (lowest) to 99 (highest).

Features

- Adaptation for Indian Market

- Option to choose the index to compare to (NSE:NIFTY, NSE:CNX500, NSE:NIFTYSMLCAP250, NSE:CNXSMALLCAP)

- Option to compare to a different index

- Option to hide the RS rating

- Option to plot RS new highs

- Option to adjust the offset of the line for display purposes

- Option to change the color of the RS Line & Rating

- Option to change the color of the dots for RS new highs

- Option to choose which new high to plot (RS New Highs, RS New Highs Before Price, Historical RS New Highs, Historical RS New Highs Before Price)

- Option to adjust the recent high look-back count

Please note that the script is designed to work best in the daily timeframe. Results may not be accurate in other timeframes.

This script uses three methods to calculate the RS Rating:

1. A method that calculates how the stock behaves vs SMA.

2. A classic performance method that calculates the performance of the stock's closing price vs the closing price 3 months back.

3. A method that measures how the stock performs against the comparative Symbol.

The final RS Rating is a combination of the results from these three methods. The script also includes some adjustments based on observations to improve the accuracy of the rating.

CVD Divergence Strategy.1.mmThis is the matching Strategy version of Indicator of the same name.

As a member of the K1m6a Lions discussion community we often use versions of the Cumulative Volume Delta indicator

as one of our primary tools along with RSI, RSI Divergences, Open interest, Volume Profile, TPO and Fibonacci levels.

We also discuss visual interpretations of CVD Divergences across multiple time frames much like RSI divergences.

RSI Divergences can be identified as possible Bullish reversal areas when the RSI is making higher low points while

the price is making lower low points.

RSI Divergences can be identified as possible Bearish reversal areas when the RSI is making lower high points while

the price is making higher high points.

CVD Divergences can also be identified the same way on any timeframe as possible reversal signals. As with RSI, these Divergences

often occur as a trend's momentum is giving way to lower volume and areas when profits are being taken signaling a possible reversal

of the current trending price movement.

Hidden Divergences are identified as calculations that may be signaling a continuation of the current trend.

Having not found any public domain versions of a CVD Divergence indicator I have combined some public code to create this

indicator and matching strategy. The calculations for the Cumulative Volume Delta keep a running total for the differences between

the positive changes in volume in relation to the negative changes in volume. A relative upward spike in CVD is created when

there is a large increase in buying vs a low amount of selling. A relative downward spike in CVD is created when

there is a large increase in selling vs a low amount of buying.

In the settings menu, the is a drop down to be used to view the results in alternate timeframes while the chart remains on current timeframe. The Lookback settings can be adjusted so that the divs show on a more local, spontaneous level if set at 1,1,60,1. For a deeper, wider view of the divs, they can be set higher like 7,7,60,7. Adjust them all to suit your view of the divs.

To create this indicator/strategy I used a portion of the code from "Cumulative Volume Delta" by @ contrerae which calculates

the CVD from aggregate volume of many top exchanges and plots the continuous changes on a non-overlay indicator.

For the identification and plotting of the Divergences, I used similar code from the Tradingview Technical "RSI Divergence Indicator"

This indicator should not be used as a stand-alone but as an additional tool to help identify Bullish and Bearish Divergences and

also Bullish and Bearish Hidden Divergences which, as opposed to regular divergences, may indicate a continuation.

CVD Divergence Indicator.1.mmAs a member of the K1m6a Lions discussion community we often use versions of the Cumulative Volume Delta indicator

as one of our primary tools along with RSI, RSI Divergences, Open interest, Volume Profile, TPO and Fibonacci levels.

We also discuss visual interpretations of CVD Divergences across multiple time frames much like RSI divergences.

RSI Divergences can be identified as possible Bullish reversal areas when the RSI is making higher low points while

the price is making lower low points.

RSI Divergences can be identified as possible Bearish reversal areas when the RSI is making lower high points while

the price is making higher high points.

CVD Divergences can also be identified the same way on any timeframe as possible reversal signals. As with RSI, these Divergences

often occur as a trend's momentum is giving way to lower volume and areas when profits are being taken signaling a possible reversal

of the current trending price movement.

Hidden Divergences are identified as calculations that may be signaling a continuation of the current trend.

Having not found any public domain versions of a CVD Divergence indicator I have combined some public code to create this

indicator and matching strategy. The calculations for the Cumulative Volume Delta keep a running total for the differences between

the positive changes in volume in relation to the negative changes in volume. A relative upward spike in CVD is created when

there is a large increase in buying vs a low amount of selling. A relative downward spike in CVD is created when

there is a large increase in selling vs a low amount of buying.

In the settings menu, the is a drop down to be used to view the results in alternate timeframes while the chart remains on current timeframe. The Lookback settings can be adjusted so that the divs show on a more local, spontaneous level if set at 1,1,60,1. For a deeper, wider view of the divs, they can be set higher like 7,7,60,7. Adjust them all to suit your view of the divs.

To create this indicator/strategy I used a portion of the code from "Cumulative Volume Delta" by @ contrerae which calculates

the CVD from aggregate volume of many top exchanges and plots the continuous changes on a non-overlay indicator.

For the identification and plotting of the Divergences, I used similar code from the Tradingview Technical "RSI Divergence Indicator"

This indicator should not be used as a stand-alone but as an additional tool to help identify Bullish and Bearish Divergences and

also Bullish and Bearish Hidden Divergences which, as opposed to regular divergences, may indicate a continuation.

RSI-Divergence Goggles [Trendoscope®]🎲 Introducing the RSI-Divergence Goggle

🎯 Revolutionizing Divergence Analysis in Trading

While the concept of divergence plays a crucial role in technical analysis, existing indicators in the community library have faced limitations, particularly in simultaneously displaying divergence lines on both price and oscillator graphs. This challenge stems from the fact that RSI and other oscillators are typically plotted in a separate pane from the price chart. Traditional Pine Script® indicators are confined to a single pane, thus restricting comprehensive divergence analysis.

🎯 Our Innovative Solution: RSI on the Price Pane

The RSI-Divergence Goggle breaks through these limitations. Our innovative approach involves plotting the RSI directly onto the price pane within a movable and resizable widget. This groundbreaking feature allows for the simultaneous drawing of zigzag patterns on both price and the oscillator, enabling the effective calculation and visualization of divergence lines on both.

🎯 The Foundation: Our Divergence Research and Rules

Our journey into divergence research began three years ago with the launch of the "Zigzag Trend Divergence Detector." The foundational rules established with this script remain pertinent and form the basis of all our subsequent divergence-based indicators.

🎯 Understanding Divergence: Key Concepts

Divergence Varieties : We identify two main types - Bullish Divergence (and its hidden counterpart) occurs at pivot lows, while Bearish Divergence (and its hidden version) appears at pivot highs.

Contextual Occurrence : Bullish divergence is a phenomenon of downtrends, whereas bearish divergence is unique to uptrend. Conversely, hidden bullish divergence arises in uptrends, and hidden bearish divergence in downtrends.

Oscillator Behavior : In standard divergence scenarios, the oscillator lags behind price, signaling potential reversals. In hidden divergence cases, the oscillator leads, suggesting trend continuation.

🎯 Visual Insights: Divergence and Hidden Divergence

For a clearer understanding, refer to our visual guides:

🎯 A Word of Caution

While divergence is a powerful tool, it's not a standalone guarantee of trend reversals or continuations. We recommend using these patterns in conjunction with support and resistance levels, as demonstrated in our "Divergence Based Support Resistance" implementation.

🎯 Using the RSI-Divergence Goggles

Upon applying the indicator to your chart, you'll be prompted to select two corner points, defining the widget's placement and size. This widget is the stage for your RSI plotting and divergence calculations. Choose these points carefully to ensure they encompass your area of interest without overlapping important price bars.

An example as below.

🎯 Innovative Features:

Plotting RSI: RSI values are scaled from 0 to 100 within the widget. This unique plotting may not align with individual bar values, but pivot labels and tooltips provide detailed RSI and retracement ratio information.

Zigzag and Pivots: Our adjusted RSI plots determine the zigzag pivot highs and lows, which may not always correspond with visible price pivots. However, calculations based on close prices ensure minimal deviation.

Divergence Display: Divergence types are identified following our established rules, with a simple moving average employed to discern the prevailing trend.

🎯 Trend Detection Mechanism

A simple moving average is used as base for determining the trend. If the difference between moving averages of the alternate pivots is positive, then the sentiment is considered to be uptrend. Else, we consider the sentiment to be in downtrend.

This is a simple method to identify trend, implemented via this indicator. The indicator does not provide alternative methods to identify trend. This is something that we can explore in the future.

🎯 Interactive and Customizable

The RSI-Divergence Goggle isn't just a static tool; it's an interactive feature on your chart. You can move or resize the widget, allowing for dynamic analysis and focused study on different chart segments.

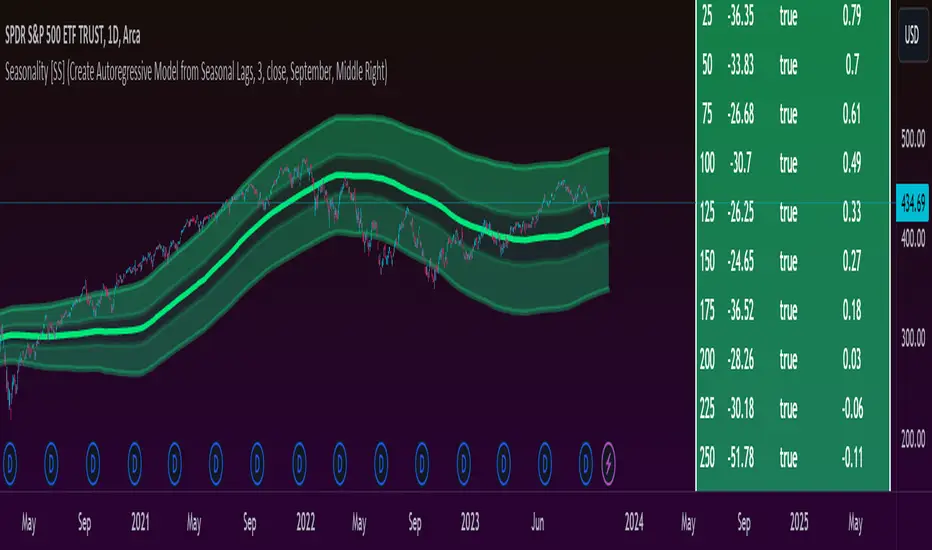

Ultimate Seasonality Indicator [SS]Hello everyone,

This is my seasonality indicator. I have been working on it for like 2 months, so hope you like it!

What it does?

The Ultimate Seasonality indicator is designed to provide you, the trader, an in-depth look at seasonality. The indicator gives you the ability to do the following functions:

View the most bearish and bullish months over a user defined amount of years back.

View the average daily change for each respective months over a user defined amount of years back.

See the most closely correlated month to the current month to give potential insights of likely trend.

Plot out areas of High and Low Seasonality.

Create a manual seasonal forecast model by selecting the desired month you would like to model the current month data after.

Have the indicator develop an autoregressive seasonal model based on seasonally lagged variables, using principles of machine learning.

I will go over these functions 1 by 1, its a whopper of an indicator so I will try to be as clear and concise as possible.

Viewing Bullish vs Bearish Months, Average Daily Change & Correlation to Current Month

The indicator will break down the average change, as well as the number of bullish and bearish days by month. See the image below as an example:

In the table to the right, you will see a breakdown of each month over the past 3 years.

In the first column, you will see the average daily change. A negative value, means it was a particularly bearish month, a positive value means it was a particularly bullish month.

The next column over shows the correlation to the current dataset. How this works is the indicator takes the size of the monthly data for each month, and compares it to the last X number of days up until the last trading day. It will then perform a correlation assessment to see how closely similar the past X number of trading days are to the various monthly data.

The last 2 columns break down the number of Bullish and Bearish days, so you can see how many red vs green candles happened in each respective month over your set timeframe. In the example above, it is over the pats 3 years.

Plot areas of High and Low Seasonality

In the chart above, you will see red and green highlighted zones.

Red represents areas of HIGH Seasonality .

Green represents areas of LOW Seasonality .

For this function, seasonality is measured by the autocorrelation function at various lags (12 lags). When there is an average autocorrelation of greater than 0.85 across all seasonal lags, it is considered likely the result of high seasonality/trend.

If the lag is less than or equal to 0.05, it is indicative of very low seasonality, as there is no predominate trend that can be found by the autocorrelation functions over the seasonally lagged variables.

Create Manual Seasonal Forecasts

If you find a month that has a particularly high correlation to the current month, you can have the indicator create a seasonal model from this month, and fit it onto the current dataset (past X days of trading).

If we look at the example below:

We can see that the most similar month to the current data is September. So, we can ask the indicator to create a seasonal forecast model from only September data and fit it to our current month. This is the result:

You will see, using September data, our most likely close price for this month is 450 and our model is y= 1.4305x + -171.67.

We can accept the 450 value but we can use the equation to model the data ourselves manually.

For example, say we have a target price on the month of 455 based on our own analysis. We can calculate the likely close price, should this target be reached, by substituting this target for x. So y = 1.4305x + -171.67 becomes

y = 1.4305(455) +- 171.67

y = 479.20

So the likely close price would be 479.20. No likely, and thus its not likely we are to see 455.

HOWEVER, in this current example, the model is far too statistically insignificant to be used. We can see the correlation is only 0.21 and the R squared is 0.04. Not a model you would want to use!

You want to see a correlation of at least 0.5 or higher and an R2 of 0.5 or higher.

We can improve the accuracy by reducing the number of years we look back. This is what happens when we reduce the lookback years to 1:

You can see reducing to 1 year gives December as the most similar month. However, our R2 value is still far too low to really rely on this data whole-heartedly. But it is a good reference point.

Automatic Autoregressive Model

So this is my first attempt at using some machine learning principles to guide statistical analysis.

In the main chart above, you will see the indicator making an autoregressive model of seasonally lagged variables. It does this in steps. The steps include:

1) Differencing the data over 12, seasonally lagged variables.

2) Determining stationarity using DF test.

3) Determining the highest, autocorrelated lags that fall within a significant stationary result.

4) Creating a quadratic model of the two identified lags that best represents a stationary model with a high autocorrelation.

What are seasonally lagged variables?

Seasonally lagged variables are variables that represent trading months. So a lag of 25 would be 1 month, 50, 2 months, 75, 3 months, etc.

When it displays this model, it will show us what the results of the t-statistic are for the DF test, whether the data is stationary, and the result of the autocorrelation assessment.

It will then display the model detail in the tip table, which includes the equation, the current lags being used, the R2 and the correlation value.

Concluding Remarks

That's the indicator in a nutshell!

Hope you like it!

One final thing, you MUST have your chart set to daily, otherwise you will get a runtime error. This can ONLY be used on the daily timeframe!

Feel free to leave your questions, comments and suggestions below.

Note:

My "ultimate" indicators are made to give the functionality of multiple indicators in one. If you like this one, you may like some of my others:

Ultimate P&L Indicator

Ultimate Customizable EMA/SMA

Thanks for checking out the indicator!

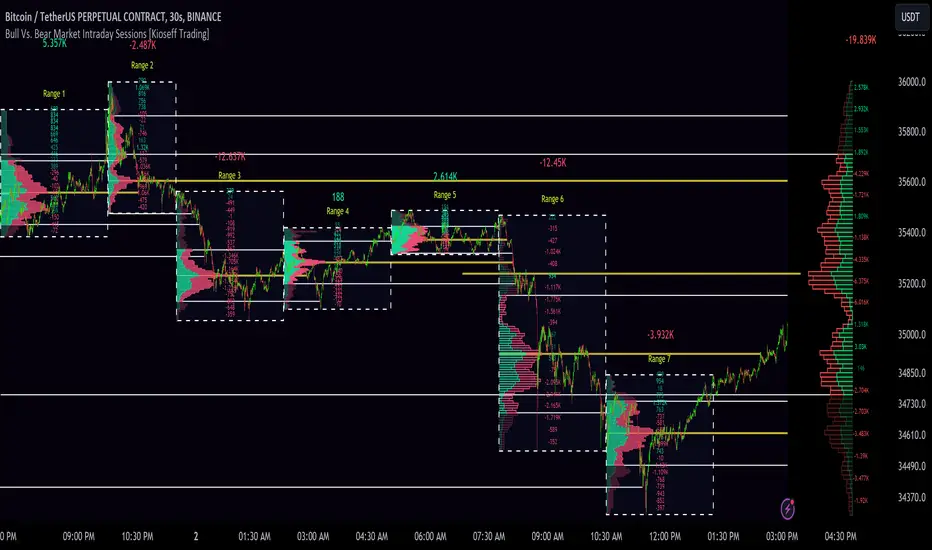

10x Bull Vs. Bear VP Intraday Sessions [Kioseff Trading]Hello!

This script "10x Bull Vs. Bear VP Intraday Sessions" lets the user configure up to 10 session ranges for Bull Vs. Bear volume profiles!

Features

Up To 10 Fixed Ranges!

Volume Profile Anchored to Fixed Range

Delta Ladder Anchored to Range

Bull vs Bear Profiles!

Standard Poc and Value Area Lines, in Addition to Separated POCs and Value Area Lines for Bull Profiles and Bear Profiles

Configurable Value Area Target

Up to 2000 Profile Rows per Visible Range

Stylistic Options for Profiles

This script generates Bull vs. Bear volume profiles for up to 10 fixed ranges!

Up to 2000 volume profile levels (price levels) Can be calculated for each profile, thanks to the new polyline feature, allowing for less aggregation / more precision of volume at price and volume delta.

Bull vs Bear Profiles

The image above shows primary functionality!

Green profiles = buying volume

Red profiles = selling volume

All colors are configurable.

Bullish & bearish POC + value areas for each fixed range are displayable!

That’s about it :D

This indicator is part of a series titled “Bull vs. Bear”.

If you have any suggestions please feel free to share!

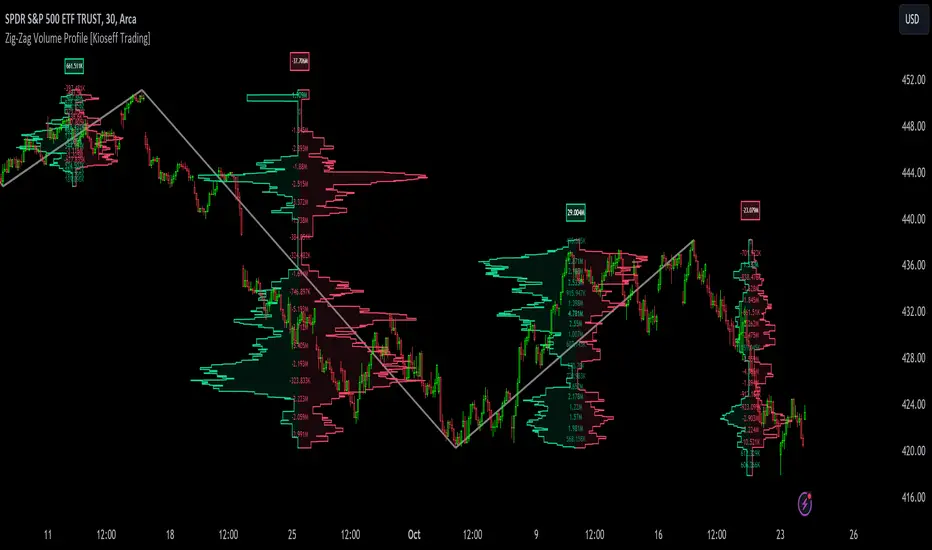

Zig-Zag Volume Profile (Bull vs. Bear) [Kioseff Trading]Hello!

Thank you @Pinecoders and @TradingView for putting polylines in production and making this viable!!

This script "Zig Zag Volume Profile" implements the polyline feature for Pine Script!

Features

Volume Profile anchored to zig zag trends

Bull vs Bear profiles!

Delta x price level

Standard POC and value area lines, in addition to separated POCs and value area lines for bull profiles and bear profiles

Up to 9999 profile rows per zigzag trend

Stylistic options for profiles

Configurable zig zag - profiles generated for small to large trends

Polylines!

This script generates Bull vs. Bear volume profiles for zig zag trends!

The zigzag indicator is configurable as normal; minor and major trend volume profiles are calculable. This indicator can be thought of as "Volume Profile/Delta for Trends''.

Up to 9999 volume profile levels (price levels) can be calculated for each profile, thanks to the new polyline feature, allowing for less aggregation / more precision of volume at price and volume delta.

Zig Zag Bull Vs Bear Profiles

The image above shows primary functionality!

Green profiles = buying volume

Red profiles = selling volume

Profiles are generated for each trend identified by the zigzag indicator.

The image above shows the indicator calculating volume delta for specific price blocks on the profile. Aggregate volume delta for the identified trend is displayed over the profile!

The image above shows Bull Profile POC lines and value area lines. Bear Profile POC lines and value area lines are also shown!

All colors and transparencies are configurable to the user's liking :D

Additionally, you can select to have the profiles drawn on contrasting sides. Bull Profile on left and Bear Profile on right.

For a more traditional look - you can select to draw the Bull & Bear profiles on the same x-point.

The indicator is robust enough to calculate on "long zig zags" and "short zig zags"; curved profiles can also be used!

The image above exemplifies usage of the indicator!

Bull & Bear volume profiles are calculated for trends on the 30-second timeframe.

The image above shows a more "utilitarian" presentation of the profiles. Once more, line and linefill colors/transparencies are all customizable; the indicator can look however you would like it to!

The image above shows key levels, the Bull vs. Bear profile, and volume delta for the current trend!

That's about it :D

This indicator is part of a series titled "Bull vs. Bear" - a suite of profile-like indicators I will be releasing over coming days. Thanks for checking this out!

Of course, a big thank you to @RicardoSantos for his MathOperator library that I use in every script.

If you have any suggestions please feel free to share!

Frequency Distribution Overlay [SS]Hello all,

This is the frequency distribution indicator. It does as the name suggests,

It breaks down the frequency distribution of any stock over a user defined lookback period and shows where the accumulations rest by percantage.

This is a function that I used to have to export to Excel or SPSS to do, but now its possible in Pinescript!

Essentially, it breaks down the areas a stock has closed in over a defined period and gives you the accumulation for each area.

What it is used for:

It is used to see where the higher areas of price accumulation rest. This helps us to identify potentially likely retracement areas and pullback areas.

It colour coordinates based on distribution and lists the composition of each zone in a label in each box.

The zones are divided by standard deviation, which means that the top and bottom of each range act as substantial areas of support/resistance (as it falls outside the normal variance of a stock).

Customizability:

The indicator is pretty straight forward, you select your desired lookback period and it will adjust accordingly.

Additionally, you can adjust for close, high, low, etc. if you want to see the accumulation and distribution of hights vs, lows vs closes.

You can toggle off the text labels if you don't want them.

The green boxes represent the areas of highest accumulation, the red box the areas of lower accumulation.

You can use it on any timeframe you wish. Above is an example of the daily, but you can also use it on the smaller TFs as well:

TSLA on the 5 minute:

And that is the indicator!

Let me know if you have questions or suggestions.

Safe trades everyone!

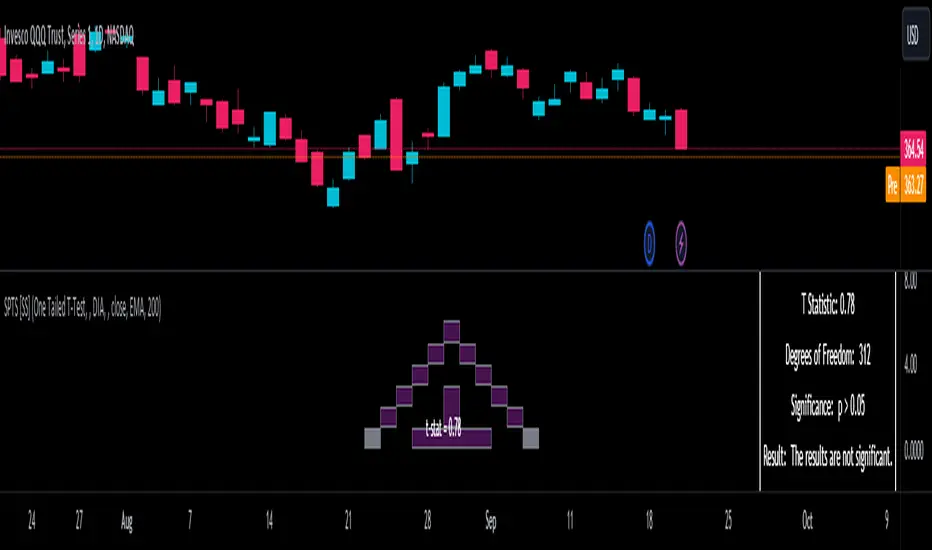

Statistical Package for the Trading Sciences [SS]

This is SPTS.

It stands for Statistical Package for the Trading Sciences.

Its a play on SPSS (Statistical Package for the Social Sciences) by IBM (software that, prior to Pinescript, I would use on a daily basis for trading).

Let's preface this indicator first:

This isn't so much an indicator as it is a project. A passion project really.

This has been in the works for months and I still feel like its incomplete. But the plan here is to continue to add functionality to it and actually have the Pinecoding and Tradingview community contribute to it.

As a math based trader, I relied on Excel, SPSS and R constantly to plan my trades. Since learning a functional amount of Pinescript and coding a lot of what I do and what I relied on SPSS, Excel and R for, I use it perhaps maybe a few times a week.

This indicator, or package, has some of the key things I used Excel and SPSS for on a daily and weekly basis. This also adds a lot of, I would say, fairly complex math functionality to Pinescript. Because this is adding functionality not necessarily native to Pinescript, I have placed most, if not all, of the functionality into actual exportable functions. I have also set it up as a kind of library, with explanations and tips on how other coders can take these functions and implement them into other scripts.

The hope here is that other coders will take it, build upon it, improve it and hopefully share additional functionality that can be added into this package. Hence why I call it a project. Okay, let's get into an overview:

Current Functions of SPTS:

SPTS currently has the following functionality (further explanations will be offered below):

Ability to Perform a One-Tailed, Two-Tailed and Paired Sample T-Test, with corresponding P value.

Standard Pearson Correlation (with functionality to be able to calculate the Pearson Correlation between 2 arrays).

Quadratic (or Curvlinear) correlation assessments.

R squared Assessments.

Standard Linear Regression.

Multiple Regression of 2 independent variables.

Tests of Normality (with Kurtosis and Skewness) and recognition of up to 7 Different Distributions.

ARIMA Modeller (Sort of, more details below)

Okay, so let's go over each of them!

T-Tests

So traditionally, most correlation assessments on Pinescript are done with a generic Pearson Correlation using the "ta.correlation" argument. However, this is not always the best test to be used for correlations and determine effects. One approach to correlation assessments used frequently in economics is the T-Test assessment.

The t-test is a statistical hypothesis test used to determine if there is a significant difference between the means of two groups. It assesses whether the sample means are likely to have come from populations with the same mean. The test produces a t-statistic, which is then compared to a critical value from the t-distribution to determine statistical significance. Lower p-values indicate stronger evidence against the null hypothesis of equal means.

A significant t-test result, indicating the rejection of the null hypothesis, suggests that there is statistical evidence to support that there is a significant difference between the means of the two groups being compared. In practical terms, it means that the observed difference in sample means is unlikely to have occurred by random chance alone. Researchers typically interpret this as evidence that there is a real, meaningful difference between the groups being studied.

Some uses of the T-Test in finance include:

Risk Assessment: The t-test can be used to compare the risk profiles of different financial assets or portfolios. It helps investors assess whether the differences in returns or volatility are statistically significant.

Pairs Trading: Traders often apply the t-test when engaging in pairs trading, a strategy that involves trading two correlated securities. It helps determine when the price spread between the two assets is statistically significant and may revert to the mean.

Volatility Analysis: Traders and risk managers use t-tests to compare the volatility of different assets or portfolios, assessing whether one is significantly more or less volatile than another.

Market Efficiency Tests: Financial researchers use t-tests to test the Efficient Market Hypothesis by assessing whether stock price movements follow a random walk or if there are statistically significant deviations from it.

Value at Risk (VaR) Calculation: Risk managers use t-tests to calculate VaR, a measure of potential losses in a portfolio. It helps assess whether a portfolio's value is likely to fall below a certain threshold.

There are many other applications, but these are a few of the highlights. SPTS permits 3 different types of T-Test analyses, these being the One Tailed T-Test (if you want to test a single direction), two tailed T-Test (if you are unsure of which direction is significant) and a paired sample t-test.

Which T is the Right T?

Generally, a one-tailed t-test is used to determine if a sample mean is significantly greater than or less than a specified population mean, whereas a two-tailed t-test assesses if the sample mean is significantly different (either greater or less) from the population mean. In contrast, a paired sample t-test compares two sets of paired observations (e.g., before and after treatment) to assess if there's a significant difference in their means, typically used when the data points in each pair are related or dependent.

So which do you use? Well, it depends on what you want to know. As a general rule a one tailed t-test is sufficient and will help you pinpoint directionality of the relationship (that one ticker or economic indicator has a significant affect on another in a linear way).

A two tailed is more broad and looks for significance in either direction.

A paired sample t-test usually looks at identical groups to see if one group has a statistically different outcome. This is usually used in clinical trials to compare treatment interventions in identical groups. It's use in finance is somewhat limited, but it is invaluable when you want to compare equities that track the same thing (for example SPX vs SPY vs ES1!) or you want to test a hypothesis about an index and a leveraged share (for example, the relationship between FNGU and, say, MSFT or NVDA).

Statistical Significance

In general, with a t-test you would need to reference a T-Table to determine the statistical significance of the degree of Freedom and the T-Statistic.

However, because I wanted Pinescript to full fledge replace SPSS and Excel, I went ahead and threw the T-Table into an array, so that Pinescript can make the determination itself of the actual P value for a t-test, no cross referencing required :-).

Left tail (Significant):

Both tails (Significant):

Distributed throughout (insignificant):

As you can see in the images above, the t-test will also display a bell-curve analysis of where the significance falls (left tail, both tails or insignificant, distributed throughout).

That said, I have not included this function for the paired sample t-test because that is a bit more nuanced. But for the one and two tailed assessments, the indicator will provide you the P value.

Pearson Correlation Assessment

I don't think I need to go into too much detail on this one.

I have put in functionality to quickly calculate the Pearson Correlation of two array's, which is not currently possible with the "ta.correlation" function.

Quadratic (Curvlinear) Correlation

Not everything in life is linear, sometimes things are curved!

The Pearson Correlation is great for linear assessments, but tends to under-estimate the degree of the relationship in curved relationships. There currently is no native function to t-test for quadratic/curvlinear relationships, so I went ahead and created one.

You can see an example of how Quadratic and Pearson Correlations vary when you look at CME_MINI:ES1! against AMEX:DIA for the past 10 ish months:

Pearson Correlation:

Quadratic Correlation:

One or the other is not always the best, so it is important to check both!

R-Squared Assessments:

The R-squared value, or the square of the Pearson correlation coefficient (r), is used to measure the proportion of variance in one variable that can be explained by the linear relationship with another variable. It represents the goodness-of-fit of a linear regression model with a single predictor variable.

R-Squared is offered in 3 separate forms within this indicator. First, there is the generic R squared which is taking the square root of a Pearson Correlation assessment to assess the variance.

The next is the R-Squared which is calculated from an actual linear regression model done within the indicator.

The first is the R-Squared which is calculated from a multiple regression model done within the indicator.

Regardless of which R-Squared value you are using, the meaning is the same. R-Square assesses the variance between the variables under assessment and can offer an insight into the goodness of fit and the ability of the model to account for the degree of variance.

Here is the R Squared assessment of the SPX against the US Money Supply:

Standard Linear Regression

The indicator contains the ability to do a standard linear regression model. You can convert one ticker or economic indicator into a stock, ticker or other economic indicator. The indicator will provide you with all of the expected information from a linear regression model, including the coefficients, intercept, error assessments, correlation and R2 value.

Here is AAPL and MSFT as an example:

Multiple Regression

Oh man, this was something I really wanted in Pinescript, and now we have it!

I have created a function for multiple regression, which, if you export the function, will permit you to perform multiple regression on any variables available in Pinescript!

Using this functionality in the indicator, you will need to select 2, dependent variables and a single independent variable.

Here is an example of multiple regression for NASDAQ:AAPL using NASDAQ:MSFT and NASDAQ:NVDA :

And an example of SPX using the US Money Supply (M2) and AMEX:GLD :

Tests of Normality:

Many indicators perform a lot of functions on the assumption of normality, yet there are no indicators that actually test that assumption!

So, I have inputted a function to assess for normality. It uses the Kurtosis and Skewness to determine up to 7 different distribution types and it will explain the implication of the distribution. Here is an example of SP:SPX on the Monthly Perspective since 2010:

And NYSE:BA since the 60s:

And NVDA since 2015:

ARIMA Modeller

Okay, so let me disclose, this isn't a full fledge ARIMA modeller. I took some shortcuts.

True ARIMA modelling would involve decomposing the seasonality from the trend. I omitted this step for simplicity sake. Instead, you can select between using an EMA or SMA based approach, and it will perform an autogressive type analysis on the EMA or SMA.

I have tested it on lookback with results provided by SPSS and this actually works better than SPSS' ARIMA function. So I am actually kind of impressed.

You will need to input your parameters for the ARIMA model, I usually would do a 14, 21 and 50 day EMA of the close price, and it will forecast out that range over the length of the EMA.

So for example, if you select the EMA 50 on the daily, it will plot out the forecast for the next 50 days based on an autoregressive model created on the EMA 50. Here is how it looks on AMEX:SPY :

You can also elect to plot the upper and lower confidence bands:

Closing Remarks

So that is the indicator/package.

I do hope to continue expanding its functionality, but as of now, it does already have quite a lot of functionality.

I really hope you enjoy it and find it helpful. This. Has. Taken. AGES! No joke. Between referencing my old statistics textbooks, trying to remember how to calculate some of these things, and wanting to throw my computer against the wall because of errors in the code, this was a task, that's for sure. So I really hope you find some usefulness in it all and enjoy the ability to be able to do functions that previously could really only be done in external software.

As always, leave your comments, suggestions and feedback below!

Take care!

SPDR TrackerMonitor all SPDR Index Funds in one location! The purpose of this indicator is to review which sectors are trend up vs down to better manage risk against SPY, other funds and/or individual stocks.

With this indicator it may become more apparent which sectors to begin investment in that are at lows compared to others, or use it to determine which stocks may be undervalued or overvalued against SPY.

There is a small table at the bottom where each fund symbol is presented along with it's mode value, last period change as well as last period volume - there's a tooltip that shows the description for each symbol for a quick reminder.

Review the configuration pane where:

Individual funds can have their visibility toggled

Change funds colors

Adjust display mode for each fund (SMA, EMA, VWMA, BBW, Change, ATR, VWAP - many more!)

Some presentation modes may look better on some timeframes vs others, adjust lengths and use anchor point for VWAP.

Future updates may bring about new features, I have some code organization and refactoring to do but wanted to share the idea anyways.

Feel free to drop any suggestions for feature enhancement and I hope it brings success to many, enjoy.

High/Low of week: Stats & Day of Week tendencies// Purpose:

-To show High of Week (HoW) day and Low of week (LoW) day frequencies/percentages for an asset.

-To further analyze Day of Week (DoW) tendencies based on averaged data from all various custom weeks. Giving a more reliable measure of DoW tendencies ('Meta Averages').

-To backtest day-of-week tendencies: across all asset history or across custom user input periods (i.e. consolidation vs trending periods).

-Education: to see how how data from a 'hard-defined-week' may be misleading when seeking statistical evidence of DoW tendencies.

// Notes & Tips:

-Only designed for use on DAILY timeframe.

-Verification table is to make sure HoW / LoW DAY (referencing previous finished week) is printing correctly and therefore the stats table is populating correctly.

-Generally, leaving Timezone input set to "America/New_York" is best, regardless of your asset or your chart timezone. But if misaligned by 1 day =>> tweak this timezone input to correct

-If you want to use manual backtesting period (e.g. for testing consolidation periods vs trending periods): toggle these settings on, then click the indicator display line three dots >> 'Reset Points' to quickly set start & end dates.

// On custom week start days:

-For assets like BTC which trade 7 days a week, this is quite simple. Pick custom start day, use verification table to check all is well. See the start week day & time in said verification table.

-For traditional assets like S&P which trade only 5 days a week and suffer from occasional Holidays, this is a bit more complicated. If the custom start day input is a bank holiday, its custom 'week' will be discounted from the data set. E.g.1: if you choose 'use custom start day' and set it to Monday, then bank holiday Monday weeks will be discounted from the data set. E.g.2: If you choose 'use custom start day' and set it to Thursday, then the Holiday Thursday custom week (e.g Thanksgiving Thursday >> following Weds) would be discounted from the data set.

// On 'Meta Averages':

-The idea is to try and mitigate out the 'continuation bias' that comes from having a fixed week start/end time: i.e. sometimes a market is trending through the week start/end time, so the start/end day stats are over-weighted if one is trying to tease out typical weekly profile tendencies or typical DoW tendencies. You'll notice this if you compare the stats with various custom start days ('bookend' start/end days are always more heavily weighted). I wanted to try to mitigate out this 'bias' by cycling through all the possible new week start/end days and taking an average of the results. i.e. on BTC/USD the 'meta average' for Tuesday would be the average of the Tuesday HoW frequencies from the set of all 7 possible custom weeks(Mon-Sun, Tues-Mon, Weds-Tues, etc etc).

// User Inputs:

~Week Start:

-use custom week start day (default toggled OFF); Choose custom week start day

-show Meta Averages (default toggled ON)

~Verification Table:

-show table, show new week lines, number of new week lines to show

-table formatting options (position, color, size)

-timezone (only for tweaking if printed DoW is misaligned by 1 day)

~Statistics Table:

-show table, table formatting options (position, color, size)

~Manual Backtesting:

-Use start date (default toggled OFF), choose start date, choose vline color

-Use end date (defautl toggled OFF), choose end date, choose vline color

// Demo charts:

NQ1! (Nasdaq), Full History, Traditional week (Mon>>Friday) stats. And Meta Averages. Annotations in purple:

NQ1! (Nasdaq), Full History, Custom week (custom start day = Wednesday). And Meta Averages. Annotations in purple:

Support and Resistance Backtester [SS]Hey everyone,

Excited to release this indicator I have been working on.

I conceptualized it as an idea a while ago and had to nail down the execution part of it. I think I got it to where I am happy with it, so let me tell you about it!

What it does?

This provides the user with the ability to quantify support and resistance levels. There are plenty of back-test strategies for RSI, stochastics, MFI, any type of technical based indicator. However, in terms of day traders and many swing traders, many of the day traders I know personally do not use or rely on things like RSI, stochastics or MFI. They actually just play the support and resistance levels without attention to anything else. However, there are no tools available to these people who want to, in a way, objectively test their identified support and resistance levels.

For me personally, I use support and resistance levels that are mathematically calculated and I am always curious to see which levels:

a) Have the most touches,

b) Have provided the most support,

c) Have provided the most resistance; and,

d) Are most effective as support/resistance.

And, well, this indicator answers all four of those questions for you! It also attempts to provide some way to support and resistance traders to quantify their levels and back-test the reliability and efficacy of those levels.

How to use:

So this indicator provides a lot of functionality and I think its important to break it down part by part. We can do this as we go over the explanation of how to use it. Here is the step by step guide of how to use it, which will also provide you an opportunity to see the options and functionality.

Step 1: Input your support and resistance levels:

When we open up the settings menu, we will see the section called "Support and Resistance Levels". Here, you have the ability to input up to 5 support and resistance levels. If you have less, no problem, simply leave the S/R level as 0 and the indicator will automatically omit this from the chart and data inclusion.

Step 2: Identify your threshold value:

The threshold parameter extends the range of your support and resistance level by a desired amount. The value you input here should be the value in which you would likely stop out of your position. So, if you are willing to let the stock travel $1 past your support and resistance level, input $1 into this variable. This will extend the range for the assessment and permit the stock to travel +/- your threshold amount before it counts it as a fail or pass.

Step 3: Select your source:

The source will tell the indicator what you want to assess. If you want to assess close, it will look at where the ticker closes in relation to your support and resistance levels. If you want to see how the highs and lows behave around the S/R levels, then change the source to High or Low.

It is recommended to leave at close for optimal results and reliability however.

Step 4: Determine your lookback length:

The lookback length will be the number of candles you want the indicator to lookback to assess the support and resistance level. This is key to get your backtest results.

The recommendation is on timeframes 1 hour or less, to look back 300 candles.

On the daily, 500 candles is recommended.

Step 5: Plot your levels

You will see you have various plot settings available to you. The default settings are to plot your support and resistance levels with labels. This will look as follows:

This will plot your basic support and resistance levels for you, so you do not have to manually plot them.

However, if you want to extend the plotted support and resistance level to visually match your threshold values, you can select the "Plot Threshold Limits" option. This will extend your support and resistance areas to match the designated threshold limits.

In this case on MSFT, I have the threshold limit set at $1. When I select "Plot Threshold Limits", this is the result:

Plotting Passes and Fails:

You will notice at the bottom of the settings menu is an option to plot passes and plot fails. This will identify, via a label overlaid on the chart, where the support and resistance failures and passes resulted. I recommend only selecting one at a time as the screen can get kind of crowded with both on. here is an example on the MSFT chart:

And on the larger timeframe:

The chart

The chart displays all of the results and counts of your support and resistance results. Some things to pay attention to use the chart are:

a) The general success rate as support vs resistance

Rationale: Support levels may act as resistance more often than they do support or vice versa. Let's take a look at MSFT as an example:

The chart above shows the 334.07 level has acted as very strong support. It has been successful as support almost 82% of the time. However, as resistance, it has only been successful 33% of the time. So we could say that 334 is a strong key support level and an area we would be comfortable longing at.

b) The number of touches:

Above you will see the number of touches pointed out by the blue arrow.

Rationale: The number of touches differs from support and resistance. It counts how many times and how frequently a ticker approaches your support and/or resistance area and the duration of time spent in that area. Whereas support and resistance is determined by a candle being either above or below a s/r area, then approaching that area and then either failing or bouncing up/down, the number of touches simply assesses the time spent (in candles) around a support or resistance level. This is key to help you identify if a level has frequent touches/consolidation vs other levels and can help you filter out s/r levels that may not have a lot of touches or are infrequently touched.

Closing comments:

So this is pretty much the indicator in a nutshell. Hopefully you find it helpful and useful and enjoy it.

As always let me know your questions/comments and suggestions below.

As always I appreciate all of you who check out, try out and read about my indicators and ideas. I wish you all the safest trades and good luck!

High of Day Low of Day hourly timings: Statistics. Time of day %High of Day (HoD) & Low of Day (LoD) hourly timings: Statistics. Time of day % likelihood for high and low.

//Purpose:

To collect stats on the hourly occurrences of HoD and LoD in an asset, to see which times of day price is more likely to form its highest and lowest prices.

//How it works:

Each day, HoD and LoD are calculated and placed in hourly 'buckets' from 0-23. Frequencies and Percentages are then calculated and printed/tabulated based on the full asset history available.

//User Inputs:

-Timezone (default is New York); important to make sure this matches your chart's timezone

-Day start time: (default is Tradingview's standard). Toggle Custom input box to input your own custom day start time.

-Show/hide day-start vertical lines; show/hide previous day's 'HoD hour' label (default toggled on). To be used as visual aid for setting up & verifying timezone settings are correct and table is populating correctly).

-Use historical start date (default toggled off): Use this along with bar-replay to backtest specific periods in price (i.e. consolidated vs trending, dull vs volatile).

-Standard formatting options (text color/size, table position, etc).

-Option to show ONLY on hourly chart (default toggled off): since this indicator is of most use by far on the hourly chart (most history, max precision).

// Notes & Tips:

-Make sure Timezone settings match (input setting & chart timezone).

-Play around with custom input day start time. Choose a 'dead' time (overnight) so as to ensure stats are their most meaningful (if you set a day start time when price is likely to be volatile or trending, you may get a biased / misleadingly high readout for the start-of-day/ end-of-day hour, due to price's tendency for continuation through that time.

-If you find a time of day with significantly higher % and it falls either side of your day start time. Try adjusting day start time to 'isolate' this reading and thereby filter out potential 'continuation bias' from the stats.

-Custom input start hour may not match to your chart at first, but this is not a concern: simply increment/decrement your input until you get the desired start time line on the chart; assuming your timezone settings for chart and indicator are matching, all will then work properly as designed.

-Use the the lines and labels along with bar-replay to verify HoD/LoD hours are printing correctly and table is populating correctly.

-Hour 'buckets' represent the start of said hour. i.e. hour 14 would be populated if HoD or LoD formed between 14:00 and 15:00.

-Combined % is simply the average of HoD % and LoD %. So it is the % likelihood of 'extreme of day' occurring in that hour.

-Best results from using this on Hourly charts (sub-hourly => less history; above hourly => less precision).

-Note that lower tier Tradingview subscriptions will get less data history. Premium acounts get 20k bars history => circa 900 days history on hourly chart for ES1!

-Works nicely on Btc/Usd too: any 24hr assets this will give meaningful data (whereas some commodities, such as Lean Hogs which only trade 5hrs in a day, will yield less meaningful data).

Example usage on S&P (ES1! 1hr chart): manual day start time of 11pm; New York timezone; Visual aid lines and labels toggled on. HoD LoD hour timings with 920 days history:

Directional Volume EStimate from Price Action (RedK D_VESPA)The "Directional Volume EStimate from Price Action (RedK D_VESPA)" is another weapon for the VPA (Volume Price Analysis) enthusiasts and traders who like to include volume-based insights & signals to their trading. The basic concept is to estimate the sell and buy split of the traded volume by extrapolating the price action represented by the shape of the associated price bar. We then create and plot an average of these "estimated buy & sell volumes" - the estimated average Net Volume is the balance between these 2 averages.

D_VESPA uses clear visualizations to represent the outcomes in a less distracting and more actionable way.

How does D_VESPA work?

-------------------------------------

The key assumption is that when price moves up, this is caused by "buy" volume (or increasing demand), and when the price moves down, this is due to "selling" volume (or increasing supply). Important to note that we are making our Buy/sell volume estimates here based on the shape of the price bar, and not looking into lower time frame volume data - This is a different approach and is still aligned to the key concepts of VPA.

Originally this work started as an improvement to my Supply/Demand Volume Viewer (V.Viewer) , I ended up re-writing the whole thing after some more research and work on VPA, to improve the estimation, visualization and usability / tradability.

Think of D_VESPA as the "Pro" version of V.Viewer -- and please go back and review the details of V.Viewer as the root concepts are the same so I won't repeat them here (as it comes to exploring Balance Zone and finding Price Convergence/Divergence)

Main Features of D_VESPA

--------------------------------------

- Update Supply/Demand calculation to include 2-bar gaps (improved algo)

- Add multiple options for the moving average (MA type) for the calculation - my preference is to use WMA

- Add option to show Net Volume as 3-color bars

- Visual simplification and improvements to be less distracting & more actionable

- added options to display/hide main visuals while maintaining the status line consistency (Avg Supply, Avg Demand, Avg Net)

- add alerts for NetVol moving into Buy (crosses 0 up) or Sell (crosses 0 down) modes - or swing from one mode to the other

(there are actually 2 sets of alerts, one set for the main NetVol plot, and the other for the secondary TF NetVol - give user more options on how to utilize D_VESPA)

Quick techie piece, how does the estimated buy/sell volume algo work ?

------------------------------------------------------------------------------------------

* per our assumption, buy volume is associated with price up-moves, sell volume is associated with price down-moves

* so each of the bulls and bears will get the equivalent of the top & bottom wicks,

* for up bars, bulls get the value of the "body", else the bears get the "body"

* open gaps are allocated to bulls or bears depending on the gap direction

The below sketch explains how D_VESPA estimates the Buy/Sell Volume split based on the bar shape (including gap) - the example shows a bullish bar with an opening gap up - but the concept is the same for a down-bar or a down-gap.

I kept both the "Volume Weighted" and "2-bar Gap Impact" as options in the indicator settings - these 2 options should be always kept selected. They are there for those who would like to experiment with the difference these changes have on the buy/sell estimation. The indicator will handle cases where there is no volume data for the selected symbol, and in that case, it will simply reflect Average Estimated Bull/Bear ratio of the price bar

The Secondary TF Est Average Net Volume:

---------------------------------------------------------

I added the ability to plot the Estimate Average Net Volume for a secondary timeframe - options 1W, 1D, 1H, or Same as Chart.

- this feature provides traders the confidence to trade the lower timeframes in the same direction as the prevailing "market mode"

- this also adds more MTF support beyond the existing TradingView's built-in MTF support capability - experiment with various settings between exposing the indicator's secondary TF plot, and changing the TF option in the indicator settings.

Note on the secondary TF NetVol plot:

- the secondary TF needs to be set to same as or higher TF than the chart's TF - if not, a warning sign would show and the plot will not be enabled. for example, a day trader may set the secondary TF to 1Hr or 1Day, while looking at 5min or 15min chart. A swing/trend trader who frequently uses the daily chart may set the secondary TF to weekly, and so on..

- the secondary TF NetVol plot is hidden by default and needs to be exposed thru the indicator settings.

the below chart shows D_VESPA on a the same (daily) chart, but with secondary TF plot for the weekly TF enabled

Final Thoughts

-------------------

* RedK D_VESPA is a volume indicator, that estimates buy/sell and net volume averages based on the price action reflected by the shape of the price bars - this can provide more insight on volume compared to the classic volume/VolAverage indicator and assist traders in exploring the market mode (buyers/sellers - bullish/bearish) and align trades to it.

* Because D_VESPA is a volume indicator, it can't be used alone to generate a trading signal - and needs to be combined with other indicators that analysis price value (range), momentum and trend. I recommend to at least combine D_VESPA with a variant of MACD and RSI to get a full view of the price action relative to the prevailing market and the broader trend.

* I found it very useful to take note and "read" how the Est Buy vs Est Sell lines move .. they sort of "tell a story" - experiment with this on your various chart and note the levels of estimate avg demand vs estimate avg supply that this indicator exposes for some very valuable insight about how the chart action is progressing. Please feel free to share feedback below.

Volume DashboardReleasing Volume Dashboard indicator.

What it does:

The volume dashboard indicator pulls volume from the current session. The current session is defaulted to NYSE trading hours (9:30 - 1600).

It cumulates buying and selling volume.

Buying volume is defined as volume associated with a green candle.

Selling volume is defined as volume associated with a red candle.

It also pulls Put to Call Ratio data from the Ticker PCC (Total equity put to call ratios).

With this data, the indicator displays the current Buy Volume and the Current Sell Volume.

It then uses this to calculate a "Buyer to Seller Ratio". The Buy to Sell ratio is calculated by Buy Volume divided by Sell Volume.

This gives a ratio value and this value will be discussed below.

The Indicator also displays the current Put to Call Ratio from PCC, as well as displays the SMA.

Buy to Sell Ratio:

The hallmark of this indicator is its calculation of the buy to sell ratio.

A buy to sell ratio of 1 or greater means that buyers are generally surpassing sellers.

However, a buy to sell ratio below 1 generally means that sellers are outpacing buyers (0 buyers to 0.xyx sellers).

The SMA is also displayed for buy to sell ratio. Generally speaking, a buy to sell SMA of greater than or equal to 1 means that there are consistent buyers showing up. Below this, means there is inconsistent buying.

Change Analysis:

The indicator also displays the current change of Volume and Put to Call.

Put to Call Change:

A negative change in Put to Call is considered positive, as puts are declining (i.e. sentiment is bullish).

A positive change in Put to Call is considered negative, as puts are increasing (i.e. sentiment is bearish).

The Put to Call change is also displayed in an SMA to see if the negative or positive change is consistent.

Volume Change :

A negative volume change is negative, as buyers are leaving (i.e. sentiment is bearish).

A positive volume change is positive, as buyers are coming in (i.e. sentiment is bullish).

The volume change is also displayed as an SMA to see if the negative or positive change is consistent.

Indicator breakdown:

The indicator displays the total cumulative Buy vs Sell volume at the top.

From there, it displays the Ratio and various other variables it tracks.

The colour scheme will change to signal bearish vs bullish variables. If a box is red, the indicator is assessing it as a bearish indicator.

If it is green, it is considered a bullish indicator.

The indicator will also plot a green up arrow when buying volume surpasses selling volume and a red down arrow when selling volume surpasses buying volume:

Customization:

The indicator is defaulted to regular market hours of the NYSE. If you are using this for trading Futures, or trading pre-market, you will need to manually adjust the session time to include these time periods.

The indicator is defaulted to read volume data on the 1 minute timeframe. My suggestion is to leave it as such, even if you are viewing this on the 5 minute timeframe.

The volume data is best accumulated over the 1 minute timeframe. This permits more reliable reading of volume data.

However, you do have the ability to manually modify this if you wish.

As well, the user can toggle on or off the SMA assessments. If you do not wish to view the SMAs, simply toggle off "Show SMAs" in the settings menu.

The user can also choose what time period the SMA is using. It is defaulted to a 14 candle lookback, but you can modify this to your liking, simply input the desired lookback time in the SMA lookback input box on the settings menu. Please note, the SMA Length setting will apply to ALL of the SMAs.

That is the bulk of the indicator!

As always, let me know your questions or feedback on the indicator below.

Thank you for taking the time to check it out and safe trades!

RSI and Stochastic Probability Based Price Target IndicatorHello,

Releasing this beta indicator. It is somewhat experimental but I have had some good success with it so I figured I would share it!

What is it?

This is an indicator that combines RSI and Stochastics with probability levels.

How it works?

This works by applying a regression based analysis on both Stochastics and RSI to attempt to predict a likely close price of the stock.

It also assess the normal distribution range the stock is trading in. With this information it does the following:

2 lines are plotted: