Implied and Historical Volatility v4There is a famous option strategy📊 played on volatility📈. Where people go short on volatility, generally, this strategy is used before any significant event or earnings release. The basic phenomenon is that the Implied Volatility shoots up before the event and drops after the event, while the volatility of the security does not increase in most of the scenarios. 💹

I have tried to create an Indicator using which you

can analyse the historical change in Implied Volatility Vs Historic Volatility.

To get a basic idea of how the security moved during different events.

Notes:

a) Implied Volatility is calculated using the bisection method and Black 76 model option pricing model.

b) For the risk-free rate I have fetched the price of the “10-Year Indian Government Bond” price and calculated its yield to be used as our Risk-Free rate.

Volaility

MOVE/VXTLT CorrelationMany know of the VIX for equity trading. Yet, many are unaware that there is the same kind of volatility measure for trading bonds, called the MOVE Index.

"The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options which are weighted on the 2, 5, 10, and 30 year contracts."

With this script one can see the the correlation and divergences between bonds and its volatility measure to make educated decisions in trading or hedging.

The idea of this script comes from NicTheMajestic.

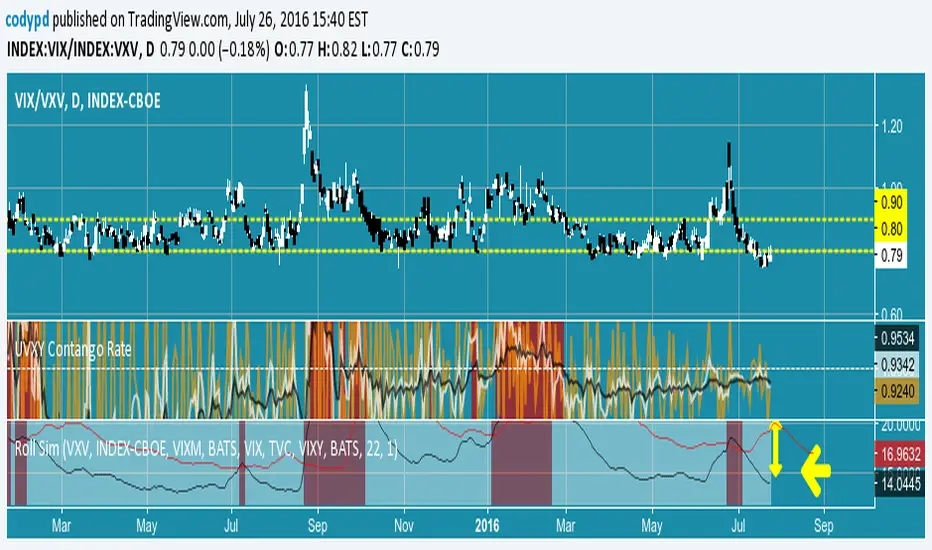

UVXY Contango Rate - my quick and dirty indicatorFeel the force ... read the source.

Give you an idea of the contango headwind / backwardation tailwind that UVXY is experiencing.

Works on Daily time frame only unless you buy the VIX feed.