ST_EMA+VWAP_V0.0Scalping strategy using relative position of price, intraday VWAP and EMAs

ex of timeframes for scalping 3 and 5 min chart

*** Default settings

- EMA 8 / 20

- Intraday VWAP

*** For bull conditions:

- Price must close twice above all lines above

- EMA 8 must be above EMA20

- should have a recent crossover between EMA8 and EMA20

成交量加權平均 Volume Weighted Average Price (VWAP)

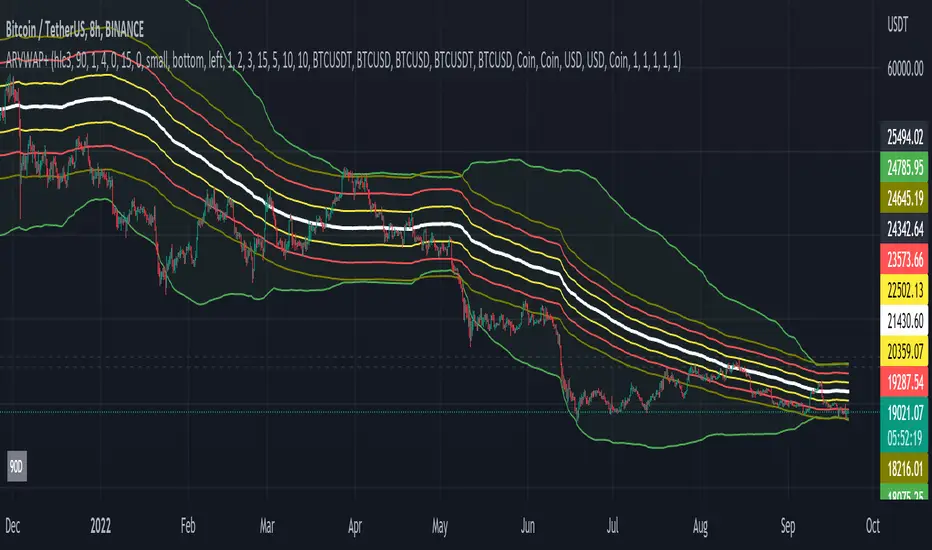

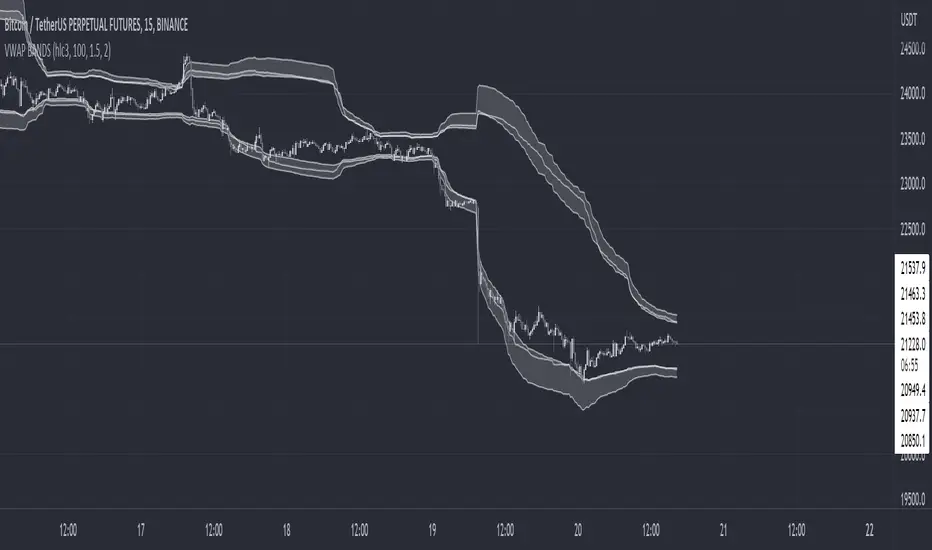

Volume Weighted Reversal BandsThis is a vwap & vwma hybrid with upper & lower deviation bands that provide excellent price channels and reversal areas. It can be used on lower & higher timeframes, just increase the deviation % for higher timeframes. Try out the 1 minute timeframe with .5% deviation for great scalping levels.

Here is the calculation used for the main line.

(VWMA100 + VWMA500 + VWMA1000 + VWAP) / 4

So it combines 3 VWMAs with the VWAP and divides that number by 4 to give us a moving average. Then we add new levels above and below that moving average to get our channels. The channels are separated by the % deviation you choose in the settings. For tighter bands, lower the percentage deviation and for wider bands, increase the percentage deviation.

The fattest line in the middle is the main moving average and you can expect price to regularly return to this level. The thick lines are the main moving average plus or minus the percentage deviation you have set. There are 10 levels in each direction from the main moving average. The is also a thin short term moving average as well with a custom calculation. It takes 4 different length moving averages that are weighted and 4 more that are volume weighted and divides the total by 8.The lines will be green when price is above the line and red when price is below the line. The thin white line is the VWAP on its own.

These lines will act as dynamic support and resistance so you can scalp them back and forth. These levels work so well because they are volume weighted and the algos hedge their positions back and forth constantly.

For best results, use this indicator on tickers with the highest volume and trading action as the price will stick to these levels better when the big money players are hedging. Some great tickers for this indicator are APPL, SPY, BTC, ETH.

All colors and linewidths can be customized in the settings easily as well as turning off the VWAP or short moving average and adjusting the percentage deviation for the channels.

***MARKETS***

This indicator can be used on all markets, including stocks, crypto, futures and forex.

***TIMEFRAMES***

This indicator can be used on all timeframes.

***TIPS***

Try using numerous indicators of ours on your chart for extra confirmation. Our favorites to pair with these bands are the Scalper Ribbon and Trend Friend Signals. The 3 combined give you a lot of extra confirmation on whether the market is going to reverse at these levels.

VWAP Bollinger BandsWhat makes this different from vwap bands / bollinger bands?

This indicator takes a bit of inspiration from bollinger but instead of utilizing built in pine script std dev that uses simple moving average internally, this version replaces that with vwap.

Also instead of traditional bollinger band basis of 20 period simple moving average, the basis here for the bands is the vwap.

How to use it?

Usage is similar to vwap itself, though the standard deviation bands will expand and contract like normal bollinger bands instead of vwap bands that just widen as the market movement continues. The bands tell a slightly different story from bollinger bands as the underlying data utilized is the vwap itself.

Which markets is this meant for?

Any market.

What conditions?

This aids in finding conditions of entry standard to vwap, but the bands could give key areas of focus for entries and exits better than standard bollinger bands or vwap bands.

VWAP Anchored Date with multiplierA modified version from the default VWAP indicator with 2 major enhancements:

1- Start date: instead of being limited to applying the indicator on the entire chart, this script allows you to select the start time to show the VWAP. You can also use this option to show VWAP on an instrument starting from a specific time, all time high for example.

2- Multiplier: You can choose a period multiplier for VWAP, like 2 days, 4 month, 3 years and so on

Aggregated Rolling VWAP +Edit of TradingView's original Rolling VWAP

Edit log:

Added Volume Aggregation Capabilities to the Script

- Price Action is impacted by volume executed in all exchanges. Even though a single exchange RVWAP can be useful, using aggregated data makes it more accurate and saves time in symbol switching.

- Aggregation is preset to be done for Bitcoin Spot Pairs. However this can be changed to Aggregate Volume from any other symbol at the bottom of the setup menu.

Added Symmetrical Deviations to the Script

- Symmetrical deviations create range of "tolerance" around the RVWAP at a fixed % distance. This helps in situations when price does not respect the exact RVWAP level and goes slightly above/under.

- Adding multiple Symmetrical Deviations at different percentage values can give relevant levels for scalping, entries and range trading.

Switched default option to manual TF instead of automatic TF

Added TF Presets for quick switching between different settings. (Feature intended for mobile charting)

Added ON/OFF Switch to all individual deviations to make it easier, faster and cleaner to display different data. (Feature intended for mobile charting)

Multiple Non-Anchored VWAPA lot of VWAP scripts are anchored and only allow single VWAP additions. This script allows up to 5 simultaneous VWAPs, for example monthly, quarterly, yearly, 3 years, etc. Can also be used on smaller timeframes. The non-anchored part of the script allows it to be constantly rolling, with no resets.

I do not endorse this script, it was created at my request :)

Average Daily Range Lines + VWAP by TenozenOANDA:EURUSD

Hello! I created an indicator called ADRL (Average Daily Range Lines). This is my first original work, and I hope it's helpful to you guys.

1. Let me explain a bit of how it works...

So first of I need the ADR value, as by default length I use 19 for it. I want this indicator to calculate every start of the new day and break if another new day starts, so if the target level isn't reached, then the value would start to go back to 0 and get the new target level of the day. The target level is based on the first ADR multiplied by how much "percent" we want for the target level to hit, based on the first ADR value of the day. When the new day starts, the algo would start to add up the ADR value. If the added ADR hits the target level, it starts to plot a line by the candlestick by its high, low, and mid-level; it would create a new line if there is a new target being hit. So that's it.

About the VWAP, I took Tradingview's VWAP. I added the anchored part so I can plot a line if there is a new target level being hit. I hope that's okay.

2. How to use it...

- Using this indicator is pretty easy. When a new box is being plotted, that means that's the time when you should trade, as the box is still fresh. The VWAP helps if the market is trending or not.

- You can treat this indicator just like an S&R, as the price tends to respect the box. So best to use it as a pullback trade.

- We can assume if the price above the box, is a buy; vice versa.

3. Best Market to use...

- I suggest a trade in a nonvolatile market. The more volatile the market is, the harder the box is to be respected by the price. But if you really want to trade in that market, I suggest adjusting the inputs by how the box is being respected.

4. Suggestions...

- Use this indicator in 5 minutes chart if you day trade.

- Try using 30 minutes and setting the percent input from 100 to 80 and changing the ADR length from 19 to 14, this is much more suitable if you tend to hold trades.

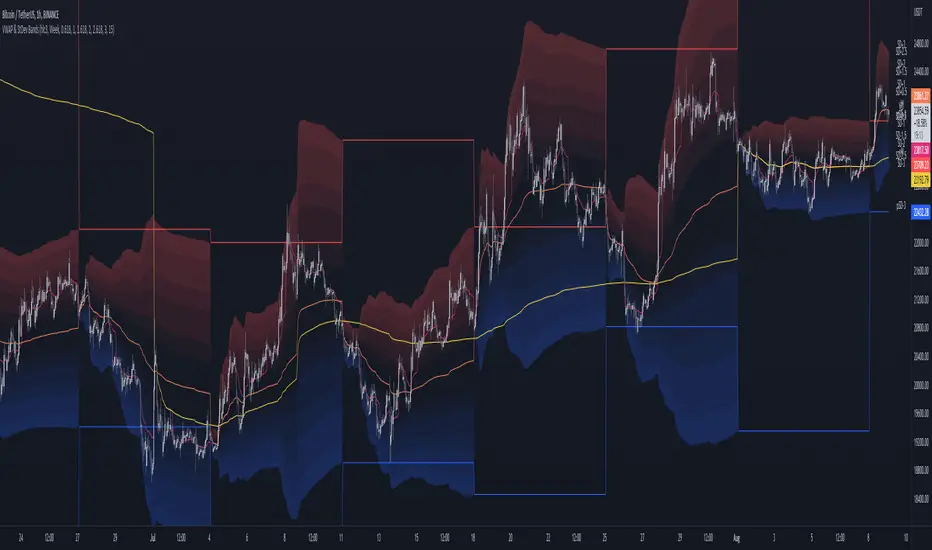

MTFT VWAPs Auto AnchoredMulti Time Frame Tools

Multi Time Frame Tools (MTFT) is a suite of scripts aimed to establish a standard timeframe-based color scheme. This can be utilized to overlay different timeframes calculations/values over a single timeframe. As one example, this would allow to observe the 5-month moving average, 5-week moving average, and 5-day moving average overlaid over each other. This would allow to study a chart, get accustomed to the color scheme and study all these at the same time much easier.

All indicators calculated using the below specific timeframes as input, will always use the color scheme outlined below. This is to get you in habit of recognizing the different timeframes overlaid in top of each other. These can be personalized.

Longer TF analysis.

Yearly - Black

Semi-Annual - Yellow

Quarterly - White

Monthly - Maroon

Weekly - Royal Blue

Daily - Lime

Shorter TF analysis.

4 hour - Fuchsia

1 hour - Orange

30 min - Red

15 min - Brown

10 min - Purple

5 min - Lilac

All color coordination is able to be modified in either the “Inputs” or “Style” section. If you need to make changes, make sure to select “Save as Default” on the bottom right of the settings menu.

Recommended Chart Color Layout

I played around with color coordination a lot. The final product was what worked best for me. I personally use the following chart settings to accent all available TF colors.

-> Click on the settings wheel on your chart. -> Click on “Appearance”.

Background - Solid -> On the top row pick the 6th color from the left.

Vert Grid Lines and Horz Grid Lines -> On the top row pick the 7th color from the left.

You may of course change these and the indicator line colors as you like.

Adding indicator to Chart

-> Open the TradingView “Indicators & Strategies” library, the icon has “ƒx”. -> All premium scripts will be located under “Invite-Only Scripts” -> Click indicator to add to your chart.

MTFT VWAPs Auto Anchored

The Anchored Volume-Weighted Average Price, Anchored VWAP, is a commonly discussed FinTwit tool. I personally found it through Brian Shannon on Twitter. I have seen big FinTwit accounts solely focus on this strategy alone and have seen other big FinTwit accounts mix with their other indicators. I will be providing very basic info to utilize this script; it is up to you to dive deep into learning this strategy. I am not an expert with the tool or a financial advisor. As with all aspects of life, I recommend you research, learn, discern and practice extensively in order to become a master.

The script has the following features.

1. Three user selected time frames auto anchored VWAPS. It will auto anchor to the start of the timeframe. Timeframes(TF) include: Yearly(Y), Semi-annually(S), Quarterly(Q), Monthly(M), Weekly(W), Daily(D), and 4 hour. Image below shows the D candlestick as the active timeframe, the anchored VWAPs for the Year, Quarter, and Month.

2. Auto hide lower timeframe calculations. Auto Hide feature will hide smaller TF calculations when a larger timeframe is selected as the display TF. Example, when the Daily timeframe candlestick selected the Weekly and Daily Anchored VWAPs are hidden because they produce very noisy results. If a lower TF is selected such as the 30 min candlestick, the previously hidden Daily and Weekly Open Anchored VWAPs are now displayed. Notice that this specific indicator calculates different with every different timeframe that is selected. The lower TF calculations are more accurate as they include additional information. Image below shows the 30 min timeframe selected with the Daily, Weekly, and Monthly Open Anchored VWAPs displayed.

3. Auto Anchor using Pivot High/Low locations. Script finds the pivot highs/lows with a user selected look back/forward period. Additionally, as new pivot highs/lows appear you can choose to keep up to 4 each previous pivot high/low anchored VWAPs displayed. Image below has a 40 look back/forward period selected, and 2 past AVWAPs enabled.

You may notice in the above image that there is a gap between the AVWAP plot and the marked pivot point. This is not something that can be avoided as the script has to look forward in order to verify the pivot. The calculation is still correct, this can be verified by manually adding an “Anchored VWAP” drawing and seeing the values align. Image below shows that they match. White lines are the manually added “Anchored VWAP” drawings. If you verify this for yourself, make sure to select the correct input source in the settings of the drawing.

4. Auto Anchored on IPO High/Low. Looks for the first available candlestick in a chart and anchors to the high and low. This is useful with newer companies with recent IPOs.

IMPORTANT NOTE to TradingView admin: One of the lessons I would consider most important in attaining clarity regarding trading, is “TheStrat” by Rob Smith. His lesson on “actionable signals” is something that can be applied to any strategy. For this reason, I am including “MTFT TheStrat Patterns Pro” script in all images that will depict confluence for a better trade selection.

Example using TheStrat Pro MTFT with this indicator.

Look for a “TheStrat actionable signal” or a “TheStrat Reversal signal” on a smaller timeframe that has an instance of this indicator on a larger timeframe calculation that is in range of the candlestick that formed your actionable signal. This means that the indicators plot you are observing must be above the low and below the high of the candlestick that is the actionable signal/reversal signal.

The Image below shows what this would look like with this indicator. The selected candlestick is the 2-day, it shows a 1-3-1 pattern and the Quarter Anchored VWAP in range. This actionable signal could be played in both directions. If the high is breached, you would enter a long position from the high of the inside candlestick. If the low is breached than you would enter a short. For targets you would look at the previous pivots, for this example all targets were hit. Note that the “Entry” and “Targets” line were added manually and are not part of the script. Setups won’t always play out so nice and clean, but given that there is so many stocks and so many signals this is just a thought to improve the quality of the signal as it has extra confluence. If you are interested in learning further, research ‘TheStrat’ by Rob Smith.

JMF MTF historical Vwap map and static levels. What is a vwap map?

This is a Multi time frame Historical vwap heatmap. The study plots lines and maps out historical vwap zones based on closing vwap value of the time frame selected and the time frames high range. Show casing high volume concentration areas and low volume area's from each time frame chosen on chart.

Static Vwap Lines can be turned off in settings, as well as the map, you can use each individually or paired together for a more complete overview of the levels. You can also refine the search by using the "Gap %" input. This will filter out and search for average price's that have gapped up or down "X" percent from the previous days average price. Leaving you with Static vwaps and map zones from the most important "Gap Day's". This helps clean up the over all visual, but be careful choosing a higher gap percentage, that you don't lose too much granularity the map offers.

What will a "Static vwap and Map look like"

The look will vary greatly depending on where the stock is in its historical range. If the name is in a consolidation range with a lot of recent average prices directly above and below, you will have a heavy, crowded, Darker/intense heat signature from the map, You will also see levels in map mode over lapping and lines bundled together. These high traffic area's can act as great support or resistance since they are showing a congregation of historical average prices where participants have previously interacted. On the contrary, if you see "open air" in the map, or large areas of blank chart where no heat signature is mapping, this is an area of LOW volume and average prices. Current price will or can move quickly through these areas IF price accepts inside the open air range. If price does NOT accept inside the open air range, Then the blank low volume zone can and will act as support or resistance given the situation.

Capture the gaps.

I look to capture these "Gaps" created by the map and static levels both long or short. I have noticed over time that the higher time frame maps zones are WELL respected intraday, Daily, Weekly, Monthly etc. I look for areas where we are clearing a high volume zone, we break above, hold and accept into open air, and start to move through the open air zones up or down.

I also use the more granular smaller levels as support and resistance intraday while in plays.

Time frames and settings .

User has 3 inputs for seperate time frames to show. You can show a combo of all 3 timeframes, or you can show only a single time frame of your choosing, or two. Mix and match with the string input time frames.

Acceptable inputs are - 5,10,15,30,60,90,240,D,W,M,2D,4W,3M and so on. Any combination of string input timeframe should work, that means numbers (5,10,15,etc) or letters (D,W,M,etc) or combination of the two.

Look and feel

Each time frame has its own color input, transparency input, line style input, and line weight input. User can customize any of the lines or maps to their liking with a wide variety of styles, widths, and colors.

Any or all of the time frames can be enabled or disabled as well, to make the map as busy, or as calm as you would like.

Enjoy !

In the end I encourage any who tries the Heatmap to really sit down and spend some time playing around with the settings in order to find out how they like the map set up. I usually run the default settings on a intraday 5min chart, and then another instance of the study on a 15min chart with W,M,3M. plotted. That way I can see granular intraday levels, and macro long term levels in the same view. See what fit's you the best, and how you like to trade. Most of all ENJOY!

Good luck -

JMF.

IMPORTANT INFO -

As always, the creator of this code is NOT a licensed investment advisor. No output of this tool is to be taken as investment advice or a recommendation to buy or sell any security.

Trading is risky, any one using this tool acknowledges they CAN LOSE some if not all of their initial investment even with this tool enabled.

User assumes ALL RESPONSIBILITY when using this tool in their technical analysis .

Bollinger Bands Scalper + VWAPGet more consistent scalps by trading in-between Bollinger Band Deviations.

FEATURES:

1) 3 Bollinger Bands with default settings to 1, 2, and 3 deviations for more consistent scalps

2) Trendicator: a dynamic color changing moving average that helps you see trend quickly

3) Robust VWAP tool with up to 3 different deviations as well as different anchor points to help you see strong support and resistances

4) Calming "purple cloud" color palette helps you focus on price action

5) Discover new trading strategies with a wide range of customizability

Impatient TS VWAP BandsImpatient VWAP bands are based of Traderskew's VWAP bands but are for more impatient traders.

Wicking or crossing down through the upper band indicates a good short trade entry for range-bound trading periods while wicking or crossing up through the lower band indicates a good long entry in range-bound conditions.

By default, impatience is disabled. If it is turned on, adjusting impatience determines how quickly the bands approach price: higher impatience approaches price faster. Rebound indicates how far from price the bands bounce after hitting price.

Three Legged Goose FuturesThree-Legged Goose is an all-in-one intraday trading system.

Three-Legged Goose Futures is the same system as our "Three-Legged Goose" indicator, simply optimized for futures trading by working across all futures market sessions.

Three-Legged Goose Futures ONLY works on futures charts, please use our original Three-Legged Goose for equities.

It features a sleek and customizable Opening range overlay with infinitely generating price targets, Average Daily Range Zones, Curated Anchored VWAPs, Total Volume and ATR analysis, as well as our state of the art Market Momentum Trend detection.

Three-Legged Goose also has important Daily levels, including the Previous Day's High and Low and the Current Days Open, three fully customizable Exponential Moving Averages, a customizable ema cloud, and a toggleable standard vwap .

Three-Legged Goose Futures also includes overnight highs and lows as well as previous New York Session highs and lows.

Using this indicator allows you to get rid of any unnecessary indicators that are taking up those valuable slots in TradingView.

AVWAP + ORBS:

The Opening Range Breakout system builds off of our recommended 15min opening range and does all of your price target calculations based on the width of the opening range. These targets are fully customizable within the settings,

to allow fine-tuning from ticker to ticker. We have programmed three Anchored vwaps at different time intervals to act as a dynamic trend-finding instrument. These, along with the opening range breakout system, can help you quickly spot the day's trend and dynamic support and resistance long before your standard moving averages have caught up with price intraday.

Average Daily Range Zones:

We believe these zones to be essential to trading, especially with our system. These zones tend to act as areas of major support and resistance as well as give an idea of the projected volatility of the underlying.

Market Momentum Trend Detection:

We paint our momentum analysis directly on your candles. By taking the overall Market Internals + the underlying's Price movement, we can determine areas where we feel comfortable adding risk on or taking risk off.

This will help those that struggle at identifying trends and valid reversals.

All of the default settings are our recommended settings.

Please check the Author Instructions Below for how to gain access to our indicators.

EMA + VWAP (CriptoAprendices)CriptoAprendices 2022

Estrategia EMA 9 + VWAP (Day Trading)

Lo ideal es usar EMA DE 9 + VWAP (Session) y operar en grafico de 5 minutos

4EMA SET & VWAP帶有價格及名稱標籤可自訂的4條EMA線和VWAP

Customizable 4 EMA lines and VWAP with price and name labels.

Bollinger BandsThis is the combination of three indicators (BOLLINGE BAND+VWAP+EMA200)

CREATED BY ANKR SINGH

VWAP BANDS [qrsq]Description

This indicator is used to find support and resistance utilizing both buying and selling volume. It can be used on lower and higher time frames to understand where price is likely to reject or bounce.

How it works

Instead of calculating the VWAP using the total volume, this script estimates the buying/selling volume and respectively calculates their individual VWAP's. The standard deviations of these are then calculated to create the set of two bands. The top bands being the VWAP from buying volume and bottom bands are from selling volume, with the option to use a double band on either pair.

How to use it

I like to use the bands for LTF scalping as well as HTF swings, I also like to use it alongside my SMA VWAP BANDS.

For scalping:

I tend to use either the 5m or 15m TF

I then set the indicator's TF to 1m

I will take a scalp based on the bands confluence with other PA methods, if price is being either supported or rejected.

For swings:

I tend to use a variety of TFs, including: 30m, 1H, 4H, D

I then set the indicator's TF to "Chart"

I will take a swing based on the bands confluence with other PA methods, if price is being either supported or rejected.

I also tend to use them on perpetual contracts as the volume seems to be more consistent and hence results in more accurate support and resistance.

Henry's Vwap-VolumeThis Indicator is meant to provide Futures Volume and Vwap Signal in spot charts of Nifty and Banknifty Traders.

Concepts and Features of this indicators are as follows :

1) Now u don't have to select and change to futures scrip often or have both spot and futures chart in same window to watch the Futures Volume and Vwap.

2) U get Both Volume and Vwap signal as a indicator in single pane.

3) Its for Nifty and Banknifty Traders specially.

4)Volume with moving average is from the futures chart of banknifty or nifty,also may select any other futures script as per ur need.

(MOVING AVERAGE of VOLUME is plotted in Blue columns over the Volume.)

5)Vwap signal is also derived from the futures chart of banknifty or nifty,also may select any other futures script as per ur need.

(VWAP SIGNAL is plotted in GREEN or RED as background.If futures price higher than Vwap then Green , opposite for Red. )

6)The idea of this script is to give extra confirmation of a clear down or uptrend while u are in the spot chart.(nifty and banknifty)

7) U can select and change any scrip u like.But I urge to use futures chart of banknifty or nifty.

I hope this indicator will help a lot of retail investor save their hard earned money in the stock market and benefit from Mr. NK's strategy.

How to Use :

Go Long - when background is Green.

Go Short -when background is Red.

(Also take confirmation from the blue columns -moving average of volumes.volume higher or less than it.)

Limitations :

U can only use it for intraday,less than 1D timeframe.

Will not work in sideways market.

Take help of other indicators also like Rsi,adx,etc.

Best of Luck,

Henry

Ultimate IndicatorThis is a combination of all the price chart indicators I frequently switch between. It contains my day time highlighter (for day trading), multi-timeframe long-term trend indicator for current commodity in the bottom right, customizable trend EMA which also has multi-timeframe drawing capabilities, VWAP, customizable indicators with separate settings from the trend indicator including: EMA, HL2 over time, Donchian Channels, Keltner Channels, Bollinger Bands, and Super Trend. The settings for these are right below the trend settings and can have their length and multiplier adjusted. All of those also have multi-timeframe capabilities separate from the trend multi-time settings.

The Day Trade Highlight option will draw faint yellow between 9:15-9:25, red between 9:25-9:45, yellow between 9:45-10:05. There will be one white background at 9:30am to show the opening of the market. while the market is open there will be a very faint blue background. For the end of the day there will be yellow between 15:45-15:50, red between 15:50-16:00, and yellow between 16:00-16:05. During the night hours, there is no coloring. The purpose of this highlight is to show the opening / closing times of the market and the hot times for large moves.

The indicators can also be colored in the following ways:

1. Simple = Makes all colors for the indicator Gray

2. Trend = Will use the Donchian Channels to get the short-trend direction and by default will color the short-term direction as Blue or Red. Unless using Super Trend, the Donchian Channel is used to find short-term trend direction.

3. Trend Adv = Will use the Donchian Channels to get the short-trend direction and by default will color the short-term direction as Blue or Red. Unless using Super Trend, the Donchian Channel is used to find short-term trend direction. If there is a short-term up-trend during a long-term down-trend, the Blue will become Navy. If short-term down-trend during long-term up-trend, the Red will be Brown.

4. Squeeze = Compares the Bollinger Bands width to the Keltner Channels width and will color based on relative squeeze of the market: Teal = no squeeze. Yellow = little squeeze. Red = decent squeeze. White = huge squeeze. if you do not understand this one, try drawing the Bollinger Bands while using the Squeeze color option and it should become more apparent how this works. I also recommend leaving the length and multiplier to the default 20 and 2 if using this setting and only changing the timeframe to get longer/shorter lengths as I've seen that changing the length or multiplier can more or less make it not work at all.

Along with the indicator settings are options to draw lines/labels/fills for the indicator. I enjoy having only fills for a cleaner look.

The Labels option will show Buy/Sell signals when the short-term trend flips to agree with the long-term trend.

The Trend Bars option will do the same as the Labels option but instead will color the bars white when a Buy/Sell option is given.

The Range Bars option shows will color a bar white when the Close of a candle is outside of a respective ranging indicator option (Bollinger or Keltner).

The Trend Bars will draw white candles no matter which indicator selection you make (even "Off"). However, Range Bars will only draw white when either Bollinger or Keltner are selected.

The Donchian Channels and Super Trend are trending indicators and should be used during trending markets. I like to use the MACD in conjunction with these indicators for possibly earlier entries.

The Bollinger Bands and Keltner Channel are ranging indicators and should be used during ranging markets. I like to use the RSI in conjunction with these indicators and will use 60/40 for overbought and oversold areas rather than 70/30. During a range, I wait for an overbought or oversold indication and will buy/sell when it crosses back into the middle area and close my position when it touches the opposite band.

I have a MACD/RSI combination indicator if you'd like that as well :D

As always, trade at your own risk. This is not some secret indicator that will 100% win. As always, the trades you see in the picture use a 1:1.5 or 1:2 risk to reward ratio, for today (August 8, 2022) it won 5/6 times with one trade still open at the end of the day. Manage your account correctly and you'll win in the long term. Hit me up with any questions or suggestions. Happy Trading!

MTF VWAP & StDev BandsMulti Timeframe Volume Weighted Average Price with Standard Deviation Bands

I used the script "Koalafied VWAP D/W/M/Q/Y" by Koalafied_3 and made some changes, such as adding more standard deviation bands.

The script can display the daily, weekly, monthly, quarterly and yearly VWAP.

Standard deviation bands values can be changed (default values are 0.618, 1, 1.618, 2, 2.618, 3).

Also the previous standard deviation bands can be displayed.

WAP ⸗ Weighted Average PricingsOur W.A.P ( Weighted Average Pricing s ) indicator is made of four different types of "WAPs". We have added the two common types known as VWAP and TWAP . In addition, we added our two custom types known as CWAP and GWAP . Each is plotted using a fully customizable two-tone color palette represented by Bullish or Bearish. In addition, each WAP has a toggle line-extensions and price labels option.

This indicator has been pre-configured for Day-Trading and Scalping .

• VWAP : Volume Weighted Average Pricing

• TWAP : Time Weighted Average Pricing

• CWAP : Cumulative Weighted Average Pricing

• GWAP : Geometric Weighted Average Pricing

Additional script features allow for fully adjustable settings and configurations:

• Adjustable; Colors

• Adjustable; Resolutions

• Adjustable; Parameters

• Adjustable; Price Labels

• Adjustable; Line Extensions

• Adjustable; Toggles

Spot v Perp aggrRollingVWAPThis indicator is a rolling VWAP that shows an aggregated BTC VWAP for both spot markets and futures markets

Spot VWAP is shown in BTC orange while perp VWAP is shown in blue

This is useful for identifying which market (spot or perps) is pushing trending moves

If the spot VWAP is more closely following the trend, then spot is pushing the move

If the perp VWAP is more closely following the trend, then perps are pushing the move

e.g. In the following picture you can see that the move down was followed much more closely by the spot VWAP, therefore you can assume that the move is being pushed my spot

VWAP For NIFTY & BANKNIFTY [Zero54]NIFTY and BANKNIFTY Being Index do not have VWAP (because there is no volume generated). This is a simple script that displays NIFTY's future VWAP on NIFTY's Spot chart and similarly, displays BANKNIFTY's future VWAP on BANKNIFTY's sport chart. Fast and quick. Just few lines of code. No hefty un-necessary calculations.

No settings necessary. The script automatically detects NIFTY and BANKNIFTY and displays the corresponding VWAP.

Enjoy and share the knowledge. If you love this script, please boost/love this script and add a comment. Cheers!

NSE:NIFTY

NSE:BANKNIFTY