OPEN-SOURCE SCRIPT

已更新 MY_CME Open Interest

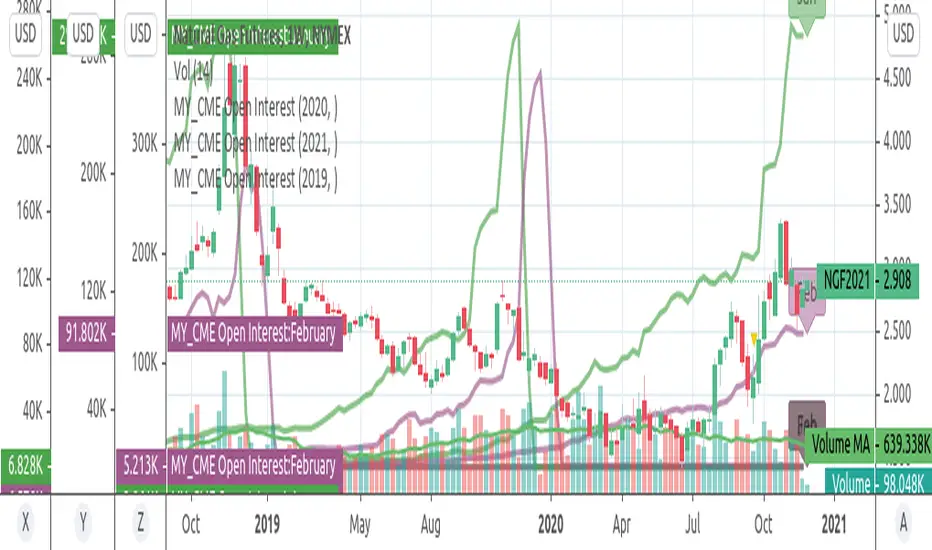

end-of-day Open Interest as provided by CME for D interval.

Can select Commodity (Gold.Silver,Crude), year, contract (Feb,April,June,AugOct,Dec)

Can select Commodity (Gold.Silver,Crude), year, contract (Feb,April,June,AugOct,Dec)

發行說明

Now uses QUANDL/CHRIS/CME_GCn continuous datasetActual dataset is #2 (eg SI2 silver), previous contract is #1 (eg SI1)

Automatically selects actual future from chart ticket,

can be overriden with a different commodity contract, eg.: GC3

發行說明

Plot e-o-d CME Open Interest + CFTC weekly COT Open Interest (optional) for contracts (Feb/Jun/Aug/Oct/Dec) years (2016/17/18/19) Gold/Silver/WTI發行說明

Select the year via config. Select the contracts months via config

Scripts tries to take ticker as base. Overridable via config, eg "GC" or "ES" or"CL"or "EC" etc

Dunno where to get all these codes thou, there's some mess out there

Database used is the CHRIS continuous by quandl, exported to tradingview:

quandl.com/data/CHRIS-Wiki-Continuous-Futures

(use previous link to search datasets and codes)

Load indicator multiple times to compare contracts over multiple years

Added codess for all 12 months contracts

CFTC total OI can also be plotted

發行說明

fixed needed confirmation for Year&Prod on startup發行說明

better chart attached+fixed def val for Year

發行說明

CFTC Open Interest fixed, now for Fut+Opt發行說明

added more future years till 2023, source is there anywayThese are my five public views I use for trading:

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。