The Magnificent 7 Oscillator is a sophisticated momentum-based technical indicator designed to analyze the collective performance of the seven largest technology companies in the U.S. stock market (Apple, Microsoft, Alphabet, Amazon, NVIDIA, Tesla, and Meta). This indicator incorporates established momentum factor research and provides three distinct analytical modes: absolute momentum tracking, equal-weighted market comparison, and relative performance analysis. The tool integrates five different oscillator methodologies and includes advanced breadth analysis capabilities.

Theoretical Foundation

Momentum Factor Research

The indicator's foundation rests on seminal momentum research in financial markets. Jegadeesh and Titman (1993) demonstrated that stocks with strong price performance over 3-12 month periods tend to continue outperforming in subsequent periods¹. This momentum effect was later incorporated into formal factor models by Carhart (1997), who extended the Fama-French three-factor model to include a momentum factor (UMD - Up Minus Down)².

The momentum calculation methodology follows the academic standard:

Momentum(t) = [P(t) - P(t-n)] / P(t-n) × 100

Where P(t) is the current price and n is the lookback period.

The focus on the "Magnificent 7" stocks reflects the increasing market concentration observed in recent years. Fama and French (2015) noted that a small number of large-cap stocks can drive significant market movements due to their substantial index weights³. The combined market capitalization of these seven companies often exceeds 25% of the total S&P 500, making their collective momentum a critical market indicator.

Indicator Architecture

Core Components

1. Data Collection and Processing

The indicator employs robust data collection with error handling for missing or invalid security data. Each stock's momentum is calculated independently using the specified lookback period (default: 14 periods).

2. Composite Oscillator Calculation

Following Fama-French factor construction methodology, the indicator offers two weighting schemes:

- Equal Weight: Each active stock receives identical weighting (1/n)

- Market Cap Weight: Reserved for future enhancement

3. Oscillator Transformation Functions

The indicator provides five distinct oscillator types, each with established technical analysis foundations:

a) Momentum Oscillator (Default)

- Pure rate-of-change calculation

- Centered around zero

- Direct implementation of Jegadeesh & Titman methodology

b) RSI (Relative Strength Index)

- Wilder's (1978) relative strength methodology

- Transformed to center around zero for consistency

- Scale: -50 to +50

c) Stochastic Oscillator

- George Lane's %K methodology

- Measures current position within recent range

- Transformed to center around zero

d) Williams %R

- Larry Williams' range-based oscillator

- Inverse stochastic calculation

- Adjusted for zero-centered display

e) CCI (Commodity Channel Index)

- Donald Lambert's mean reversion indicator

- Measures deviation from moving average

- Scaled for optimal visualization

Operational Modes

Mode 1: Magnificent 7 Analysis

Tracks the collective momentum of the seven constituent stocks. This mode is optimal for:

- Technology sector analysis

- Growth stock momentum assessment

- Large-cap performance tracking

Mode 2: S&P 500 Equal Weight Comparison

Analyzes momentum using an equal-weighted S&P 500 reference (typically RSP ETF). This mode provides:

- Broader market momentum context

- Size-neutral market analysis

- Comparison baseline for relative performance

Mode 3: Relative Performance Analysis

Calculates the momentum differential between Magnificent 7 and S&P 500 Equal Weight. This mode enables:

- Sector rotation analysis

- Style factor assessment (Growth vs. Value)

- Relative strength identification

Formula: Relative Performance = MAG7_Momentum - SP500EW_Momentum

Signal Generation and Thresholds

Signal Classification

The indicator generates three signal states:

- Bullish: Oscillator > Upper Threshold (default: +2.0%)

- Bearish: Oscillator < Lower Threshold (default: -2.0%)

- Neutral: Oscillator between thresholds

Relative Performance Signals

In relative performance mode, specialized thresholds apply:

- Outperformance: Relative momentum > +1.0%

- Underperformance: Relative momentum < -1.0%

Alert System

Comprehensive alert conditions include:

- Threshold crossovers (bullish/bearish signals)

- Zero-line crosses (momentum direction changes)

- Relative performance shifts

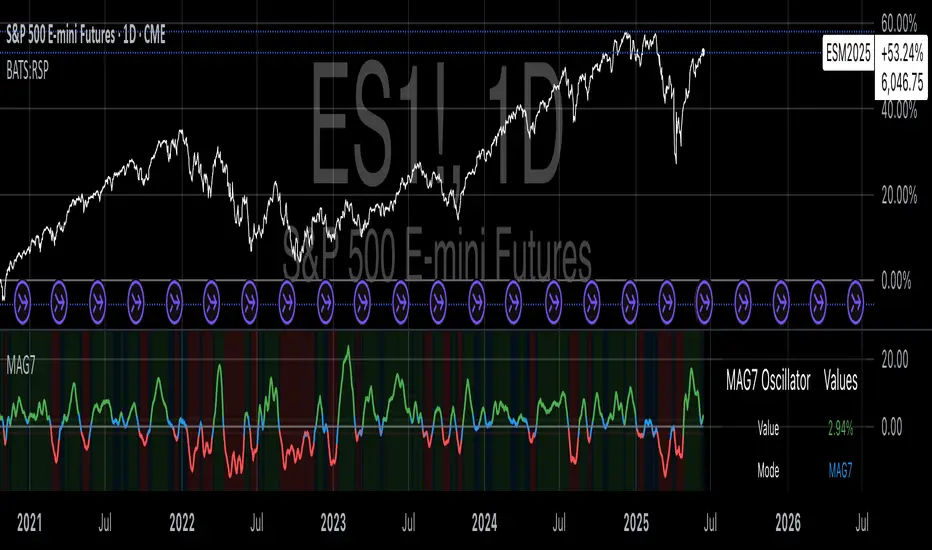

- Breadth Analysis Component

The indicator incorporates market breadth analysis, calculating the percentage of constituent stocks with positive momentum. This feature provides insights into:

- Strong Breadth (>60%): Broad-based momentum

- Weak Breadth (<40%): Narrow momentum leadership

- Mixed Breadth (40-60%): Neutral momentum distribution

Visual Design and User Interface

Theme-Adaptive Display

The indicator automatically adjusts color schemes for dark and light chart themes, ensuring optimal visibility across different user preferences.

Professional Data Table

A comprehensive data table displays:

- Current oscillator value and percentage

- Active mode and oscillator type

- Signal status and strength

- Component breakdowns (in relative performance mode)

- Breadth percentage

- Active threshold levels

Custom Color Options

Users can override default colors with custom selections for:

- Neutral conditions (default: Material Blue)

- Bullish signals (default: Material Green)

- Bearish signals (default: Material Red)

Practical Applications

Portfolio Management

- Sector Allocation: Use relative performance mode to time technology sector exposure

- Risk Management: Monitor breadth deterioration as early warning signal

- Entry/Exit Timing: Utilize threshold crossovers for position sizing decisions

Market Analysis

- Trend Identification: Zero-line crosses indicate momentum regime changes

- Divergence Analysis: Compare MAG7 performance against broader market

- Volatility Assessment: Oscillator range and frequency provide volatility insights

Strategy Development

- Factor Timing: Implement growth factor timing strategies

- Momentum Strategies: Develop systematic momentum-based approaches

- Risk Parity: Use breadth metrics for risk-adjusted portfolio construction

Configuration Guidelines

Parameter Selection

- Momentum Period (5-100): Shorter periods (5-20) for tactical analysis, longer periods (50-100) for strategic assessment

- Smoothing Period (1-50): Higher values reduce noise but increase lag

- Thresholds: Adjust based on historical volatility and strategy requirements

Timeframe Considerations

- Daily Charts: Optimal for swing trading and medium-term analysis

- Weekly Charts: Suitable for long-term trend analysis

- Intraday Charts: Useful for short-term tactical decisions

Limitations and Considerations

Market Concentration Risk

The indicator's focus on seven stocks creates concentration risk. During periods of significant rotation away from large-cap technology stocks, the indicator may not represent broader market conditions.

Momentum Persistence

While momentum effects are well-documented, they are not permanent. Jegadeesh and Titman (1993) noted momentum reversal effects over longer time horizons (2-5 years).

Correlation Dynamics

During market stress, correlations among the constituent stocks may increase, reducing the diversification benefits and potentially amplifying signal intensity.

Performance Metrics and Backtesting

The indicator includes hidden plots for comprehensive backtesting:

- Individual stock momentum values

- Composite breadth percentage

- S&P 500 Equal Weight momentum

- Relative performance calculations

These metrics enable quantitative strategy development and historical performance analysis.

References

¹Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. Journal of Finance, 48(1), 65-91.

Carhart, M. M. (1997). On persistence in mutual fund performance. Journal of Finance, 52(1), 57-82.

Fama, E. F., & French, K. R. (2015). A five-factor asset pricing model. Journal of Financial Economics, 116(1), 1-22.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Theoretical Foundation

Momentum Factor Research

The indicator's foundation rests on seminal momentum research in financial markets. Jegadeesh and Titman (1993) demonstrated that stocks with strong price performance over 3-12 month periods tend to continue outperforming in subsequent periods¹. This momentum effect was later incorporated into formal factor models by Carhart (1997), who extended the Fama-French three-factor model to include a momentum factor (UMD - Up Minus Down)².

The momentum calculation methodology follows the academic standard:

Momentum(t) = [P(t) - P(t-n)] / P(t-n) × 100

Where P(t) is the current price and n is the lookback period.

The focus on the "Magnificent 7" stocks reflects the increasing market concentration observed in recent years. Fama and French (2015) noted that a small number of large-cap stocks can drive significant market movements due to their substantial index weights³. The combined market capitalization of these seven companies often exceeds 25% of the total S&P 500, making their collective momentum a critical market indicator.

Indicator Architecture

Core Components

1. Data Collection and Processing

The indicator employs robust data collection with error handling for missing or invalid security data. Each stock's momentum is calculated independently using the specified lookback period (default: 14 periods).

2. Composite Oscillator Calculation

Following Fama-French factor construction methodology, the indicator offers two weighting schemes:

- Equal Weight: Each active stock receives identical weighting (1/n)

- Market Cap Weight: Reserved for future enhancement

3. Oscillator Transformation Functions

The indicator provides five distinct oscillator types, each with established technical analysis foundations:

a) Momentum Oscillator (Default)

- Pure rate-of-change calculation

- Centered around zero

- Direct implementation of Jegadeesh & Titman methodology

b) RSI (Relative Strength Index)

- Wilder's (1978) relative strength methodology

- Transformed to center around zero for consistency

- Scale: -50 to +50

c) Stochastic Oscillator

- George Lane's %K methodology

- Measures current position within recent range

- Transformed to center around zero

d) Williams %R

- Larry Williams' range-based oscillator

- Inverse stochastic calculation

- Adjusted for zero-centered display

e) CCI (Commodity Channel Index)

- Donald Lambert's mean reversion indicator

- Measures deviation from moving average

- Scaled for optimal visualization

Operational Modes

Mode 1: Magnificent 7 Analysis

Tracks the collective momentum of the seven constituent stocks. This mode is optimal for:

- Technology sector analysis

- Growth stock momentum assessment

- Large-cap performance tracking

Mode 2: S&P 500 Equal Weight Comparison

Analyzes momentum using an equal-weighted S&P 500 reference (typically RSP ETF). This mode provides:

- Broader market momentum context

- Size-neutral market analysis

- Comparison baseline for relative performance

Mode 3: Relative Performance Analysis

Calculates the momentum differential between Magnificent 7 and S&P 500 Equal Weight. This mode enables:

- Sector rotation analysis

- Style factor assessment (Growth vs. Value)

- Relative strength identification

Formula: Relative Performance = MAG7_Momentum - SP500EW_Momentum

Signal Generation and Thresholds

Signal Classification

The indicator generates three signal states:

- Bullish: Oscillator > Upper Threshold (default: +2.0%)

- Bearish: Oscillator < Lower Threshold (default: -2.0%)

- Neutral: Oscillator between thresholds

Relative Performance Signals

In relative performance mode, specialized thresholds apply:

- Outperformance: Relative momentum > +1.0%

- Underperformance: Relative momentum < -1.0%

Alert System

Comprehensive alert conditions include:

- Threshold crossovers (bullish/bearish signals)

- Zero-line crosses (momentum direction changes)

- Relative performance shifts

- Breadth Analysis Component

The indicator incorporates market breadth analysis, calculating the percentage of constituent stocks with positive momentum. This feature provides insights into:

- Strong Breadth (>60%): Broad-based momentum

- Weak Breadth (<40%): Narrow momentum leadership

- Mixed Breadth (40-60%): Neutral momentum distribution

Visual Design and User Interface

Theme-Adaptive Display

The indicator automatically adjusts color schemes for dark and light chart themes, ensuring optimal visibility across different user preferences.

Professional Data Table

A comprehensive data table displays:

- Current oscillator value and percentage

- Active mode and oscillator type

- Signal status and strength

- Component breakdowns (in relative performance mode)

- Breadth percentage

- Active threshold levels

Custom Color Options

Users can override default colors with custom selections for:

- Neutral conditions (default: Material Blue)

- Bullish signals (default: Material Green)

- Bearish signals (default: Material Red)

Practical Applications

Portfolio Management

- Sector Allocation: Use relative performance mode to time technology sector exposure

- Risk Management: Monitor breadth deterioration as early warning signal

- Entry/Exit Timing: Utilize threshold crossovers for position sizing decisions

Market Analysis

- Trend Identification: Zero-line crosses indicate momentum regime changes

- Divergence Analysis: Compare MAG7 performance against broader market

- Volatility Assessment: Oscillator range and frequency provide volatility insights

Strategy Development

- Factor Timing: Implement growth factor timing strategies

- Momentum Strategies: Develop systematic momentum-based approaches

- Risk Parity: Use breadth metrics for risk-adjusted portfolio construction

Configuration Guidelines

Parameter Selection

- Momentum Period (5-100): Shorter periods (5-20) for tactical analysis, longer periods (50-100) for strategic assessment

- Smoothing Period (1-50): Higher values reduce noise but increase lag

- Thresholds: Adjust based on historical volatility and strategy requirements

Timeframe Considerations

- Daily Charts: Optimal for swing trading and medium-term analysis

- Weekly Charts: Suitable for long-term trend analysis

- Intraday Charts: Useful for short-term tactical decisions

Limitations and Considerations

Market Concentration Risk

The indicator's focus on seven stocks creates concentration risk. During periods of significant rotation away from large-cap technology stocks, the indicator may not represent broader market conditions.

Momentum Persistence

While momentum effects are well-documented, they are not permanent. Jegadeesh and Titman (1993) noted momentum reversal effects over longer time horizons (2-5 years).

Correlation Dynamics

During market stress, correlations among the constituent stocks may increase, reducing the diversification benefits and potentially amplifying signal intensity.

Performance Metrics and Backtesting

The indicator includes hidden plots for comprehensive backtesting:

- Individual stock momentum values

- Composite breadth percentage

- S&P 500 Equal Weight momentum

- Relative performance calculations

These metrics enable quantitative strategy development and historical performance analysis.

References

¹Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. Journal of Finance, 48(1), 65-91.

Carhart, M. M. (1997). On persistence in mutual fund performance. Journal of Finance, 52(1), 57-82.

Fama, E. F., & French, K. R. (2015). A five-factor asset pricing model. Journal of Financial Economics, 116(1), 1-22.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

Where others speculate, we systematize.

edgetools.org

edgetools.org

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

Where others speculate, we systematize.

edgetools.org

edgetools.org

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。