OPEN-SOURCE SCRIPT

已更新 vol_bracket

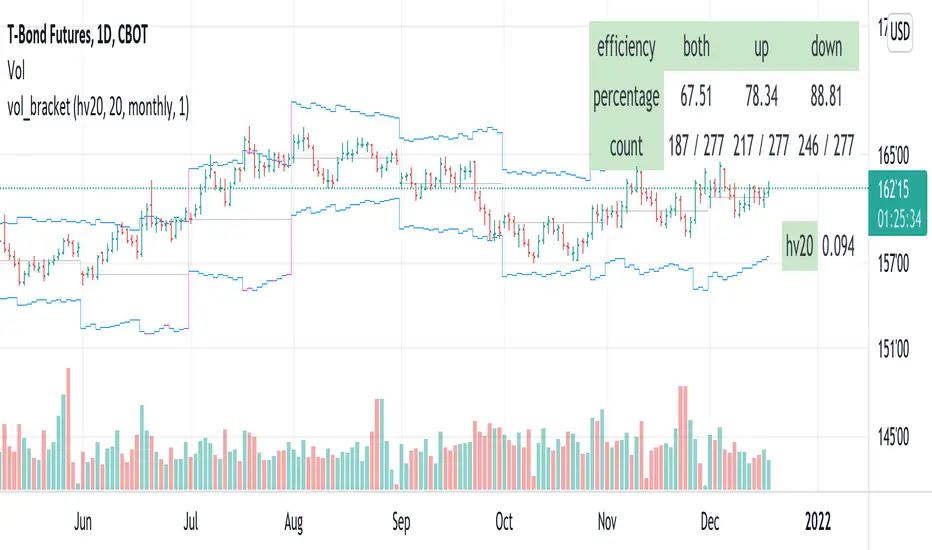

This simple script shows an "N" standard deviation volatility bracket, anchored at the opening price of the current month, week, or quarter. This anchor is meant to coincide roughly with the expiration of options issued at the same interval. You can choose between a manually-entered IV or the hv30 volatility model.

Unlike my previous scripts, which all show the volatility bracket as a rolling figure, the anchor helps to visualize the volatility estimate in relation to price as it ranges over the (approximate) lifetime of a single, real contract.

Unlike my previous scripts, which all show the volatility bracket as a rolling figure, the anchor helps to visualize the volatility estimate in relation to price as it ranges over the (approximate) lifetime of a single, real contract.

發行說明

- Fixed a bug where the monthly bracket started one day late for instruments with an overnight session.- Added a daily bracket.

發行說明

Added an "efficiency" table. Efficiency is the ratio of periods in which price closed within the period's bracket (both), below the top bound (up), or above the bottom bound (down), to those in which it did not.發行說明

- added table to display current vol and model發行說明

to make the script more readable:- color brackets "blue" if close is inside, "fuchsia" if outside

- changed the bracket to "circles" style on the daily chart... stepline style is too messy

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。