Adaptive Causal Wavelet Trend FilterThe Adaptive Causal Wavelet Trend Filter is a technical indicator implementing causal approximations of wavelet transform properties for better trend detection with adaptive volatility response.

The Adaptive Causal Wavelet Trend Filter (ACWTF) applies mathematical principles derived from wavelet analysis to financial time series, providing robust trend identification with minimal lag. Unlike conventional moving averages, it preserves significant price movements while filtering market noise through signal processing that i describe below.

I was inspired to build this indicator after reading " Wavelet-Based Trend Identification in Financial Time Series " by In, F., & Kim, S. 2013 and reading about Mexican Hat wavelet filters.

The ACWTF maintains optimal performance across varying market regimes without requiring parameter adjustments by adapting filter characteristics to current volatility conditions.

Mathematical Foundation

Inspired by the Mexican Hat wavelet (Ricker wavelet), this indicator implements causal approximations of wavelet filters optimized for real-time financial analysis. The multi-resolution approach identifies features at different scales and the adaptive component dynamically adjusts filtering characteristics based on local volatility measurements.

Key mathematical properties include:

Non-linear frequency response adaptation

Edge-preserving signal extraction

Scale-space analysis through dual filter implementation

Volatility-dependent coefficient adjustment, which I love

Filter Methods

Adaptive: Implements a volatility-weighted combination of multiple filter types to optimize the time-frequency resolution trade-off

Hull: Provides a causal approximation of wavelet edge detection properties with forward-projection characteristics

VWMA: Incorporates volume information into the filtering process for enhanced signal detection

EMA Cascade: Creates a multi-pole filter structure that approximates certain wavelet scaling properties

Suggestion: try all as they will provide slightly different signals. Try also different time-frames.

Practical Applications

Trend Direction Identification: Clear visual trend direction with reduced noise and lag

Regime Change Detection: Early identification of significant trend reversals

Market Condition Analysis: Integrated volatility metrics provide context for current market behavior

Multi-timeframe Confirmation: Alignment between primary and secondary filters offers additional confirmation

Entry/Exit Timing: Filter crossovers and trend changes provide potential trading signals

The comprehensive information panel provides:

Current filter method and trend state

Trend alignment between timeframes

Real-time volatility assessment

Price position relative to filter

Overall trading bias based on multiple factors

Implementation Notes

Log returns option provides improved statistical properties for financial time series

Primary and secondary filter lengths can be adjusted to optimize for specific instruments and timeframes

The indicator performs particularly well during trend transitions and regime changes

The indicator reduces the need for using additional indicators to check trend reversion

波動率

Convergence [by Oberlunar]

The Convergence Indicator by Oberlunar is a multi-timeframe analysis tool that identifies and visualizes trend convergence across up to 10 configurable timeframes using advanced customizable moving averages, including Hull, OberX (a Hull mod), THMA, EMA, and SMA, with an optional pseudo-Hilbert Transform.

It provides a clear visual overlay through gradual fill areas that highlight bullish and bearish trends while offering a fully configurable dynamic table to monitor live trend states across all selected timeframes with user-defined colors and positioning.

This tool is designed for traders who seek to pinpoint multi-timeframe convergence points to enhance their decision-making process in trend-following and breakout strategies.

Oberlunar 👁️⭐

RSI- RSI 8 Level Indicator

- Finally, The Bullish and Bearish 8 Level Power Zone indicator with alerts on each level!

Customize the colors however you like and remember if you need to set alerts you can also do that in the alerts section of the indicator. Just make sure what level the alert is for, and always look out for regular divergence, hidden divergence, and exaggerated divergence using this indicator that goes along with the power zones. :)

- RSI Strategy

Trading Bullish & Bearish Power Zones using regular divergence, hidden divergence, and exaggerated divergence.

P.s.

90, 80, 50, 40 Bullish Power Zones in green

65, 55, 30, 20 Bearish Power Zones in red

PRO Investing - ATR Quant.algo by proinvesting.coATR Quant.algo by PROInvesting.co

A powerful and visually intuitive trend-following system designed to capture high-momentum moves and avoid market chop.

Quant.algo combines a dynamic trend-following EMA with multi-level ATR volatility zones to provide a complete trading framework with clear entry signals, stop-loss levels, and take-profit targets.

Key Features:

Dynamic Trend EMA: A thick baseline that turns Green for uptrends and Red for downtrends. Only trade in the direction of the trend.

Multi-Level ATR Zones: Automatically adapting channels that define ideal zones for entries, stops, and profit-taking.

Volatility Filter: A smart filter that tints the background when volatility is expanding, helping you avoid sideways markets and only trade when the market is ready to move.

Pullback Entry Signals: Clear BUY and SELL arrows appear after a pullback to the EMA, providing high-probability entry points.

Simple Trading Rules:

Go LONG: When the baseline is Green, wait for a Green BUY arrow, and aim for the upper TP Zone. Place your stop below the orange Stop Zone line.

Go SHORT: When the baseline is Red, wait for a Red SELL arrow, and aim for the lower TP Zone. Place your stop above the orange Stop Zone line.

Best For:

Traders: Swing Traders & Position Traders.

Timeframes: 4-Hour (H4) and Daily (D1).

Assets: Trending markets (Indices, Forex, Crypto).

Non-Repainting RSI 30/70 SignalA simple buy and sell indicator that relies on overbought and oversold areas that you enter whenyou get either a buy or sold signal.

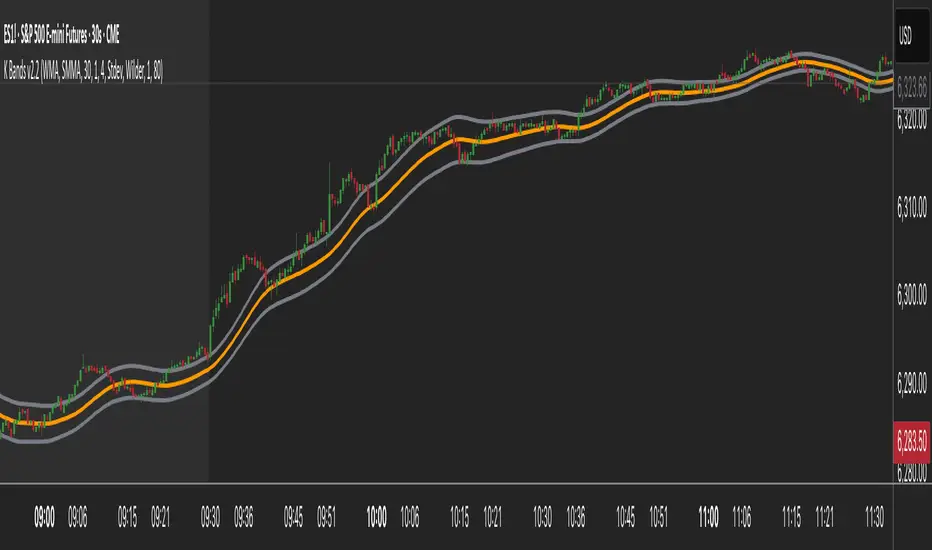

K Bands v2.2K Bands v2 - Settings Breakdown (Timeframe Agnostic)

K Bands v2 is an adaptive volatility envelope tool designed for flexibility across different trading

styles and timeframes.

The settings below allow complete control over how the bands are constructed, smoothed, and how

they respond to market volatility.

1. Upstream MA Type

Controls the core smoothing applied to price before calculating the bands.

Options:

- EMA: Fast, responsive, reacts quickly to price changes.

- SMA: Classic moving average, slower but provides stability.

- Hull: Ultra smooth, reduces noise significantly but may react differently to choppy conditions.

- GeoMean: Geometric mean smoothing, creates a unique, slightly smoother line.

- SMMA: Wilder-style smoothing, balances noise reduction and responsiveness.

- WMA: Weighted Moving Average, emphasizes recent price action for sharper responsiveness.

2. Smoothing Length

Lookback period for the upstream moving average.

- Lower values: Faster reaction, captures short-term shifts.

- Higher values: Smoother trend depiction, filters out noise.

3. Multiplier

Determines the width of the bands relative to calculated volatility.

- Lower multiplier: Tighter bands, more signals, but increased false breakouts.

- Higher multiplier: Wider bands, fewer false signals, more conservative.

4. Downstream MA Type

Applies final smoothing to the band plots after initial calculation.

Same options as Upstream MA.

5. Downstream Smoothing Length

Lookback period for downstream smoothing.

- Lower: More responsive bands.

- Higher: Smoother, visually cleaner bands.

6. Band Width Source

Selects the method used to calculate band width based on market volatility.

Options:

- ATR (Average True Range): Smooth, stable bands based on price range expansion.

- Stdev (Standard Deviation): More reactive bands highlighting short-term volatility spikes.

7. ATR Smoothing Type

Controls how the ATR or Stdev value is smoothed before applying to band width.

Options:

- Wilder: Classic, stable smoothing.

- SMA: Simple moving average smoothing.

- EMA: Faster, more reactive smoothing.

- Hull: Ultra-smooth, noise-reducing smoothing.

- GeoMean: Geometric mean smoothing.

8. ATR Length

Lookback period for smoothing the volatility measurement (ATR or Stdev).

- Lower: More reactive bands, captures quick shifts.

- Higher: Smoother, more stable bands.

9. Dynamic Multiplier Based on Volatility

Allows the band multiplier to adapt automatically to changes in market volatility.

- ON: Bands expand during high volatility and contract during low volatility.

- OFF: Bands remain fixed based on the set multiplier.

10. Dynamic Multiplier Sensitivity

Controls how aggressively the dynamic multiplier responds to volatility changes.

- Lower values: Subtle adjustments.

- Higher values: More aggressive band expansion/contraction.

K Bands v2 is designed to be adaptable across any market or timeframe, helping visualize price

structure, trend, and volatility behavior.

Dynamic Ray BandsAbout Dynamic Ray Bands

Dynamic Ray Bands is a volatility-adaptive envelope indicator that adjusts in real time to evolving market conditions. It uses a Double Exponential Moving Average (DEMA) as its central trend reference, with upper and lower bands scaled according to current volatility measured by the Average True Range (ATR).

This creates a dynamic structure that visually frames price action, helping traders identify areas of potential trend continuation, overextension, or mean reversion.

How It Works

🟡 Centerline (DEMA)

The central yellow line is a Double Exponential Moving Average, which offers a smoother, less laggy trend signal than traditional moving averages. It represents the market’s short- to medium-term “equilibrium.”

🔵 Outer Bands

Plotted at:

Upper Band = DEMA + (ATR × outerMultiplier)

Lower Band = DEMA - (ATR × outerMultiplier)

These bands define the extreme bounds of current volatility. When price breaks above or below them, it can signal strong directional momentum or overbought/oversold conditions, depending on context. They're often used as trend breakout zones or to time exits after extended runs.

🟣 Inner Bands

Plotted closer to the DEMA:

Inner Upper = DEMA + (ATR × innerMultiplier)

Inner Lower = DEMA - (ATR × innerMultiplier)

These are preliminary volatility thresholds, offering early cues for potential expansion or reversal. They may be used for scalping, tight stop zones, or pre-breakout positioning.

🔁 Dynamic Width (Bands are Dynamically Adjusted Per Tick)

The width of both inner and outer bands is based on ATR (Average True Range), which is recalculated in real time. This means:

During high volatility, the bands expand, allowing for wider price fluctuations.

During low volatility, the bands contract, tightening range expectations.

Unlike fixed-width channels or standard Bollinger Bands (which use standard deviation), this per-tick adjustment via ATR enables Dynamic Ray Bands to reduce false signals in choppy markets and remain more reactive during trending conditions.

⚙️ Inputs

DMA Length — Period for the central DEMA.

ATR Length — Lookback used for ATR volatility calculations.

Outer Band Multiplier — Controls sensitivity of extreme bands.

Inner Band Multiplier — Controls proximity of inner bands.

Show Inner Bands — Toggle for plotting the inner zone.

🔔 Alerts

Alert conditions are included for:

Price closing above/below the outer bands (trend momentum or overextension)

Price closing above/below the inner bands (early signs of strength/weakness)

🧭 Use Cases

Breakout detection — Catch price continuation beyond the outer bands.

Volatility filtering — Adjust trade logic based on band width.

Mean reversion — Monitor for snapbacks toward the DEMA after price stretches too far.

Trend guidance — Use band slope and price position to confirm direction.

⚠️ Disclaimer

This script is intended for educational and informational purposes only. It does not constitute financial advice or a recommendation to trade any specific market or security. Always test indicators thoroughly before using them in live trading.

Buy/Sell Indicator (RSI, MACD, ATR) v6+Buy Sell indicators based on EMA, Volume and MACD Has buy and sale flag indicators

Time-Specific Volume AverageA volume indicator based on historic volume.

Checks for the average volume in the past few days at the same time of day. This helps you determine when there is truly volume in the markets.

We will see often see sustained volume above the average during a clear trend. If you see spikes in volume without it being sustained above the average, it is very likely that the trend will die off quickly.

This is very helpful in determining whether to trade based on a trend following system, or a range based system.

Settings are below:

Days to average: Number of days to look back(tradingview has limits depending on your plan)

SMA Length: Number of "volume averages" to look at. Keep this at 1 if you want the average volume at the exact moment in the day. If you increase it, will also average in the past few candles of "volume averages".

SMA Multiplier: Multiplies the SMA by this amount(helps to get higher quality trends)

Rob Hoffman IRB Strategy by SniffDog30 Min Bonk Strategy. Not sure if this is beneficial for other tokens/coins. Use at you own risk.

Good strategy for starter in Rob Hoffman style of indicators.

NOTE:

1) Switch to 30 mins

2) adjust to your exchange and quantity of trade

Capital Risk OptimizerCapital Risk Optimizer 🛡️

The Capital Risk Optimizer is an educational tool designed to help traders study capital efficiency, risk management, and scaling strategies when using leverage.

This script calculates and visualizes essential metrics for managing leveraged positions, including:

Entry Price – The current market price.

Stop Loss Level – Automatically derived using the 30-bar lowest low minus 1 ATR (default: 14-period ATR), an approach designed to create a dynamic, volatility-adjusted stop loss.

Stop Loss Distance (%) – The percentage distance between entry and stop.

Maximum Safe Leverage – The highest leverage allowable without risking liquidation before your stop is reached.

Margin Required – The amount of collateral necessary to support the desired position size at the calculated leverage.

Position Size – The configurable notional value of your trade.

These outputs are presented in a clean, customizable table overlay so you can quickly understand how position sizing, volatility, and leverage interact.

By default, the script uses a 14-period ATR combined with the lowest low of the past 30 bars, providing an optimal balance between sensitivity and noise for defining stop placement. This methodology helps traders account for market volatility in a systematic way.

The Capital Risk Optimizer is particularly useful as a portfolio management tool, supporting traders who want to study how to scale into positions using risk-adjusted sizing and capital efficiency principles. It pairs best with backtested strategies, and does not directly produce signals of any kind.

How to Use:

Set your desired position size.

Adjust the ATR and lookback settings to fine-tune stop loss placement.

Study the resulting leverage and margin requirements in real time.

Use this information to simulate and visualize potential trade scenarios and capital allocation models.

Disclaimer:

This script is provided for educational and informational purposes only. It does not constitute financial advice and should not be relied upon for live trading decisions. Always do your own research and consult with a qualified professional before making any trading or investment decisions.

Supertrend AT v1.0📌 Supertrend AT v1.0 — Strategy Overview

Overview

Supertrend AT v1.0 is a fully automated trading strategy based on the Supertrend indicator.

It identifies trend reversals and places long or short entries accordingly, with built-in position sizing, stop-loss/take-profit management, and commission-aware calculations.

🚀 Key Features

✅ Entry Signals Based on Trend Reversals

Long entry when Supertrend changes from downtrend to uptrend

Short entry when Supertrend changes from uptrend to downtrend

✅ Risk-Based Position Sizing

Calculates position size so that a stop-loss only risks a fixed percentage (RPT) of total capital

✅ Reward/Risk Ratio-Based Target Price Calculation

Take-profit price is computed not by price difference, but by actual loss and desired reward-to-risk (RR) ratio

✅ Fully Commission-Aware

Commission is factored into entry, stop-loss, and take-profit price calculations

Ensure commission settings match in both the input panel and the strategy properties tab

✅ Dual Language Support

Switch between English and Korean interface

✅ Visual Trade Levels & Info Display

Entry, stop, and target prices plotted on the chart

Real-time open PnL and equity shown in an on-screen table

⚙️ How to Use

Apply Strategy to Chart

Load the strategy and configure the following parameters in both the Input tab and the Properties tab:

Commission rate (e.g., 0.05%)

Market decimal precision (e.g., 4 for 0.0001)

Adjust Entry Parameters

RPT: Risk per trade as a percentage of your total equity (e.g., 2%)

RR: Reward-to-risk ratio (e.g., 3 = target profit is 3× the potential loss)

Choose whether to allow Long or Short trades

For Auto-Trading Integration

Make sure the minimum order size is valid for your exchange

If the calculated quantity is below the exchange's minimum unit, it may result in errors

⚠️ Important Notes

❗ Non-Repainting — Supertrend is based on confirmed candles and does not repaint

❗ Backtest-Only — The strategy is for signal generation only and does not execute real trades without external automation

❗ Margin-Based Calculations — Default settings assume margin trading; adjust accordingly

📄 License & Disclaimer

This strategy is licensed under the Mozilla Public License 2.0.

This script is not financial advice. Use at your own risk.

Always test thoroughly with backtesting and paper trading before using in live markets.

Volatility Zones (STDEV %)This indicator calculates and visualizes the relative price volatility of any asset, expressed as a percentage of standard deviation over a rolling window.

🧠 How it works:

- Calculates rolling standard deviation of price (close) as a percentage of the current price.

- Classifies market into three volatility regimes :

• Low Volatility (≤2%) → Blue zone

• Medium Volatility (2–4%) → Orange zone

• High Volatility (>4%) → Red zone

📊 Why it matters:

Volatility structure reflects the underlying regime of the market — ranging, expanding, or trending. This tool helps traders:

- Spot optimal low-risk entry conditions

- Avoid chop zones or highly erratic moves

- Time breakouts or trend initiations

🛠 Usage:

- Works on any timeframe and instrument

- Adjustable lookback period

- Best used alongside trend filters or entry signals (e.g., SuperTrend, EMAs, etc.)

Kelly Optimal Leverage IndicatorThe Kelly Optimal Leverage Indicator mathematically applies Kelly Criterion to determine optimal position sizing based on market conditions.

This indicator helps traders answer the critical question: "How much capital should I allocate to this trade?"

Note that "optimal position sizing" does not equal the position sizing that you should have. The Optima position sizing given by the indicator is based on historical data and cannot predict a crash, in which case, high leverage could be devastating.

Originally developed for gambling scenarios with known probabilities, the Kelly formula has been adapted here for financial markets to dynamically calculate the optimal leverage ratio that maximizes long-term capital growth while managing risk.

Key Features

Kelly Position Sizing: Uses historical returns and volatility to calculate mathematically optimal position sizes

Multiple Risk Profiles: Displays Full Kelly (aggressive), 3/4 Kelly (moderate), 1/2 Kelly (conservative), and 1/4 Kelly (very conservative) leverage levels

Volatility Adjustment: Automatically recommends appropriate Kelly fraction based on current market volatility

Return Smoothing: Option to use log returns and smoothed calculations for more stable signals

Comprehensive Table: Displays key metrics including annualized return, volatility, and recommended exposure levels

How to Use

Interpret the Lines: Each colored line represents a different Kelly fraction (risk tolerance level). When above zero, positive exposure is suggested; when below zero, reduce exposure. Note that this is based on historical returns. I personally like to increase my exposure during market downturns, but this is hard to illustrate in the indicator.

Monitor the Table: The information panel provides precise leverage recommendations and exposure guidance based on current market conditions.

Follow Recommended Position: Use the "Recommended Position" guidance in the table to determine appropriate exposure level.

Select Your Risk Profile: Conservative traders should follow the Half Kelly or Quarter Kelly lines, while more aggressive traders might consider the Three-Quarter or Full Kelly lines.

Adjust with Volatility: During high volatility periods, consider using more conservative Kelly fractions as recommended by the indicator.

Mathematical Foundation

The indicator calculates the optimal leverage (f*) using the formula:

f* = μ/σ²

Where:

μ is the annualized expected return

σ² is the annualized variance of returns

This approach balances potential gains against risk of ruin, offering a scientific framework for position sizing that maximizes long-term growth rate.

Notes

The Full Kelly is theoretically optimal for maximizing long-term growth but can experience significant drawdowns. You should almost never use full kelly.

Most practitioners use fractional Kelly strategies (1/2 or 1/4 Kelly) to reduce volatility while capturing most of the growth benefits

This indicator works best on daily timeframes but can be applied to any timeframe

Negative Kelly values suggest reducing or eliminating market exposure

The indicator should be used as part of a complete trading system, not in isolation

Enjoy the indicator! :)

P.S. If you are really geeky about the Kelly Criterion, I recommend the book The Kelly Capital Growth Investment Criterion by Edward O. Thorp and others.

EVaR Indicator and Position SizingThe Problem:

Financial markets consistently show "fat-tailed" distributions where extreme events occur with higher frequency than predicted by normal distributions (Gaussian or even log-normal). These fat tails manifest in sudden price crashes, volatility spikes, and black swan events that traditional risk measures like volatility can underestimate. Standard deviation and conventional VaR calculations assume normally distributed returns, leaving traders vulnerable to severe drawdowns during market stress.

Cryptocurrencies and volatile instruments display particularly pronounced fat-tailed behavior, with extreme moves occurring 5-10 times more frequently than normal distribution models would predict. This reality demands a more sophisticated approach to risk measurement and position sizing.

The Solution: Entropic Value at Risk (EVAR)

EVaR addresses these limitations by incorporating principles from statistical mechanics and information theory through Tsallis entropy. This advanced approach captures the non-linear dependencies and power-law distributions characteristic of real financial markets.

Entropy is more adaptive than standard deviations and volatility measures.

I was inspired to create this indicator after reading the paper " The End of Mean-Variance? Tsallis Entropy Revolutionises Portfolio Optimisation in Cryptocurrencies " by by Sana Gaied Chortane and Kamel Naoui.

Key advantages of EVAR over traditional risk measures:

Superior tail risk capture: More accurately quantifies the probability of extreme market moves

Adaptability to market regimes: Self-calibrates to changing volatility environments

Non-parametric flexibility: Makes less assumptions about the underlying return distribution

Forward-looking risk assessment: Better anticipates potential market changes (just look at the charts :)

Mathematically, EVAR is defined as:

EVAR_α(X) = inf_{z>0} {z * log(1/α * M_X(1/z))}

Where the moment-generating function is calculated using q-exponentials rather than conventional exponentials, allowing precise modeling of fat-tailed behavior.

Technical Implementation

This indicator implements EVAR through a q-exponential approach from Tsallis statistics:

Returns Calculation: Price returns are calculated over the lookback period

Moment Generating Function: Approximated using q-exponentials to account for fat tails

EVAR Computation: Derived from the MGF and confidence parameter

Normalization: Scaled to for intuitive visualization

Position Sizing: Inversely modulated based on normalized EVAR

The q-parameter controls tail sensitivity—higher values (1.5-2.0) increase the weighting of extreme events in the calculation, making the model more conservative during potentially turbulent conditions.

Indicator Components

1. EVAR Risk Visualization

Dynamic EVAR Plot: Color-coded from red to green normalized risk measurement (0-1)

Risk Thresholds: Reference lines at 0.3, 0.5, and 0.7 delineating risk zones

2. Position Sizing Matrix

Risk Assessment: Current risk level and raw EVAR value

Position Recommendations: Percentage allocation, dollar value, and quantity

Stop Parameters: Mathematically derived stop price with percentage distance

Drawdown Projection: Maximum theoretical loss if stop is triggered

Interpretation and Application

The normalized EVAR reading provides a probabilistic risk assessment:

< 0.3: Low risk environment with minimal tail concerns

0.3-0.5: Moderate risk with standard tail behavior

0.5-0.7: Elevated risk with increased probability of significant moves

> 0.7: High risk environment with substantial tail risk present

Position sizing is automatically calculated using an inverse relationship to EVAR, contracting during high-risk periods and expanding during low-risk conditions. This is a counter-cyclical approach that ensures consistent risk exposure across varying market regimes, especially when the market is hyped or overheated.

Parameter Optimization

For optimal risk assessment across market conditions:

Lookback Period: Determines the historical window for risk calculation

Q Parameter: Controls tail sensitivity (higher values increase conservatism)

Confidence Level: Sets the statistical threshold for risk assessment

For cryptocurrencies and highly volatile instruments, a q-parameter between 1.5-2.0 typically provides the most accurate risk assessment because it helps capturing the fat-tailed behavior characteristic of these markets. You can also increase the q-parameter for more conservative approaches.

Practical Applications

Adaptive Risk Management: Quantify and respond to changing tail risk conditions

Volatility-Normalized Positioning: Maintain consistent exposure across market regimes

Black Swan Detection: Early identification of potential extreme market conditions

Portfolio Construction: Apply consistent risk-based sizing across diverse instruments

This indicator is my own approach to entropy-based risk measures as an alterative to volatility and standard deviations and it helps with fat-tailed markets.

Enjoy!

VDN1 - T3 Tilson + IFT + ATRThis strategy combines three powerful indicators to create a high-quality and low-noise trading system:

🔹 T3 Tilson: Serves as the main trend indicator. It reacts smoothly to market direction changes while reducing noise.

🔹 Inverse Fisher Transform of RSI: A momentum filter that sharpens the signal precision. Only trades in the direction of positive or negative momentum.

🔹 ATR Filter: Avoids entries during low volatility (sideways) periods. Ensures the market is active enough before executing trades.

Core Logic:

* Long Entry: T3 Tilson rising + IFT(RSI) > 0 + ATR > threshold

* Short Entry: T3 Tilson falling + IFT(RSI) < 0 + ATR > threshold

* All trades use a fixed size of 1 unit for consistent risk evaluation.

Performance Notes:

* Works exceptionally well on index futures (e.g., NAS100, US30, GER40)

* Shows low drawdown and high profit factor (PF > 3) on those assets

* Also performs decently on XAUUSD, even with only \~32% win rate — thanks to favorable risk/reward

* BTC and ETH may require modified versions due to higher volatility and whipsaws

This is a master version — clean, unoptimized, and stable.

Use this as a core engine to build and test enhanced versions (e.g., with TP/SL, dynamic filters, etc.)

Happy testing and trading!

H BollingerBollinger Bands are a widely used technical analysis indicator that helps spot relative price highs and lows. The tool comprises three lines: a central band representing the 20-period simple moving average (SMA), and upper and lower bands usually placed two standard deviations above and below the SMA. These bands adjust with market volatility, offering insights into price fluctuations and trading conditions.

How this indicator works

Bollinger Bands helps traders assess price volatility and potential price reversals. They consist of three bands: the middle band, the upper band, and the lower band. Here's how Bollinger Bands work:

Middle band: This is typically a simple moving average (SMA) of the asset's price over a specified period. The most common period used is 20 days.

Upper band: This is calculated by adding a specified number of standard deviations to the middle band. The standard deviation measures the asset's price volatility. Commonly, two standard deviations are added to the middle band.

Lower band: Similar to the upper band, it is calculated by subtracting a specified number of standard deviations from the middle band.

What do Bollinger Bands tell you?

Bollinger bands primarily indicate the level of market volatility and trading opportunities. Narrow bands indicate low market volatility, while wide bands suggest high market volatility. Bollinger bands indicators can be used by traders to assess potential buy or sell signals. For instance, a sell signal may be interpreted or generated if the asset’s price moves closer or crosses the upper band, as it may indicate that the asset is overbought. Alternatively, a buy signal may be interpreted or generated if the price moves closer to the lower band, as it may signify that the asset is oversold.

However, traders should be cautious when using Bollinger Bands as standalone indicators when making trading decisions. Experienced traders refrain from confirming signals based on one indicator. Instead, they generally combine various technical indicators and fundamental analysis methods to make informed trading decisions. Basing trading decisions on only one indicator can result in misinterpretation of signals and heavy losses.

Bollinger Bands assist in identifying whether prices are relatively high or low. They are applied as a pair—upper and lower bands—alongside a moving average. However, these bands are not designed to be used in isolation. Instead, they should be used to validate signals generated by other technical indicators.

Calculation of Bollinger Band

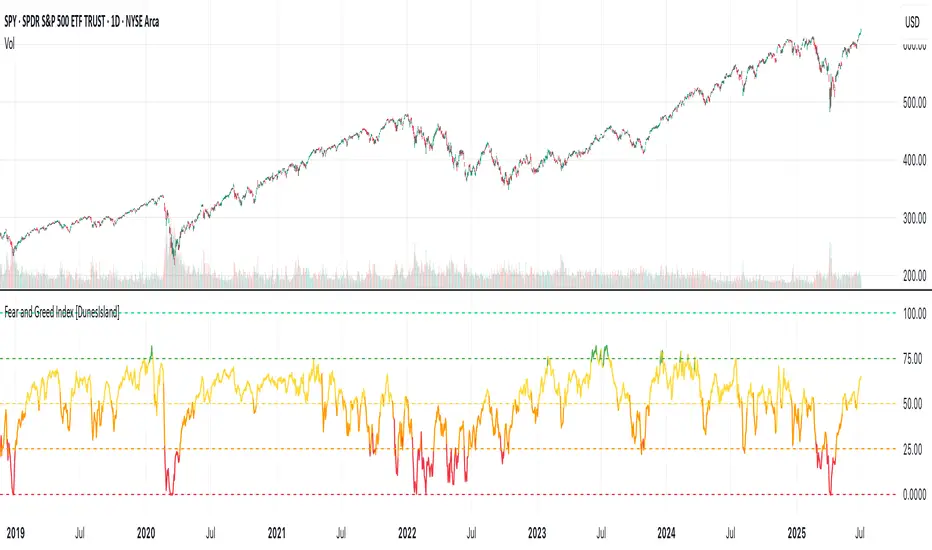

Fear and Greed Index [DunesIsland]The Fear and Greed Index is a sentiment indicator designed to measure the emotions driving the stock market, specifically investor fear and greed. Fear represents pessimism and caution, while greed reflects optimism and risk-taking. This indicator aggregates multiple market metrics to provide a comprehensive view of market sentiment, helping traders and investors gauge whether the market is overly fearful or excessively greedy.How It WorksThe Fear and Greed Index is calculated using four key market indicators, each capturing a different aspect of market sentiment:

Market Momentum (30% weight)

Measures how the S&P 500 (SPX) is performing relative to its 125-day simple moving average (SMA).

A higher value indicates that the market is trading well above its moving average, signaling greed.

Stock Price Strength (20% weight)

Calculates the net number of stocks hitting 52-week highs minus those hitting 52-week lows on the NYSE.

A greater number of net highs suggests strong market breadth and greed.

Put/Call Options (30% weight)

Uses the 5-day average of the put/call ratio.

A lower ratio (more call options being bought) indicates greed, as investors are betting on rising prices.

Market Volatility (20% weight)

Utilizes the VIX index, which measures market volatility.

Lower volatility is associated with greed, as investors are less fearful of large market swings.

Each component is normalized using a z-score over a 252-day lookback period (approximately one trading year) and scaled to a range of 0 to 100. The final Fear and Greed Index is a weighted average of these four components, with the weights specified above.Key FeaturesIndex Range: The index value ranges from 0 to 100:

0–25: Extreme Fear (red)

25–50: Fear (orange)

50–75: Neutral (yellow)

75–100: Greed (green)

Dynamic Plot Color: The plot line changes color based on the index value, visually indicating the current sentiment zone.

Reference Lines: Horizontal lines are plotted at 0, 25, 50, 75, and 100 to represent the different sentiment levels: Extreme Fear, Fear, Neutral, Greed, and Extreme Greed.

How to Interpret

Low Values (0–25): Indicate extreme fear, which may suggest that the market is oversold and could be due for a rebound.

High Values (75–100): Indicate greed, which may signal that the market is overbought and could be at risk of a correction.

Neutral Range (25–75): Suggests a balanced market sentiment, neither overly fearful nor greedy.

This indicator is a valuable tool for contrarian investors, as extreme readings often precede market reversals. However, it should be used in conjunction with other technical and fundamental analysis tools for a well-rounded view of the market.

EMAREVEX: Adaptive Multi-Timeframe Mean Reversion

📘 Strategy Overview: EMAREVEX

EMAREVEX (EMA Reversion Expert) is a professionally engineered mean-reversion strategy tailored for BTC/USDT, optimized specifically for the 15-minute and 30-minute timeframes.

It combines:

- Multi-timeframe EMA200 trend filtering (15m & 30m)

- Bollinger Band lower/upper breaches as reversion anchors

- RSI-based confirmation for oversold/overbought conditions

- A trailing stop-loss mechanism that activates only after volatility surpasses a configurable ATR threshold, then dynamically tracks price

This setup targets short-term pullback opportunities in volatile intraday environments.

🔬 Designed for quant-informed traders who seek precision entries and dynamic exit control.

⚠️ Warning:

This strategy is optimized on historical data. It should not be used without discretionary confirmation, appropriate risk management, and forward-testing under live market conditions.

Institutional Momentum Scanner [IMS]Institutional Momentum Scanner - Professional Momentum Detection System

Hunt explosive price movements like the professionals. IMS identifies maximum momentum displacement within 10-bar windows, revealing where institutional money commits to directional moves.

KEY FEATURES:

▪ Scans for strongest momentum in rolling 10-bar windows (institutional accumulation period)

▪ Adaptive filtering reduces false signals using efficiency ratio technology

▪ Three clear states: LONG (green), SHORT (red), WAIT (gray)

▪ Dynamic volatility-adjusted thresholds (8% ATR-scaled)

▪ Visual momentum flow with glow effects for signal strength

BASED ON:

- Pocket Pivot concept (O'Neil/Morales) applied to price momentum

- Adaptive Moving Average principles (Kaufman KAMA)

- Market Wizards momentum philosophy

- Institutional order flow patterns (5-day verification window)

HOW IT WORKS:

The scanner finds the maximum price displacement in each 10-bar window - where the market showed its hand. An adaptive filter (5-bar regression) separates real moves from noise. When momentum exceeds the volatility-adjusted threshold, states change.

IDEAL FOR:

- Momentum traders seeking explosive moves

- Swing traders (especially 4H timeframe)

- Position traders wanting institutional footprints

- Anyone tired of false breakout signals

Default parameters (10,5) optimized for 4H charts but adaptable to any timeframe. Remember: The market rewards patience and punishes heroes. Wait for clear signals.

"The market is honest. Are you?"

Forex Monday RangeForex Monday Range. Refers to the price range (high to low) established during Monday's trading session, typically measured from midnight Sunday to midnight Monday (New York time).

NASDAQ Smart Momentum Strategy v4.1 BoostedTry to trade Nasdaq with it in 15 min time frame just build today. GL