OPEN-SOURCE SCRIPT

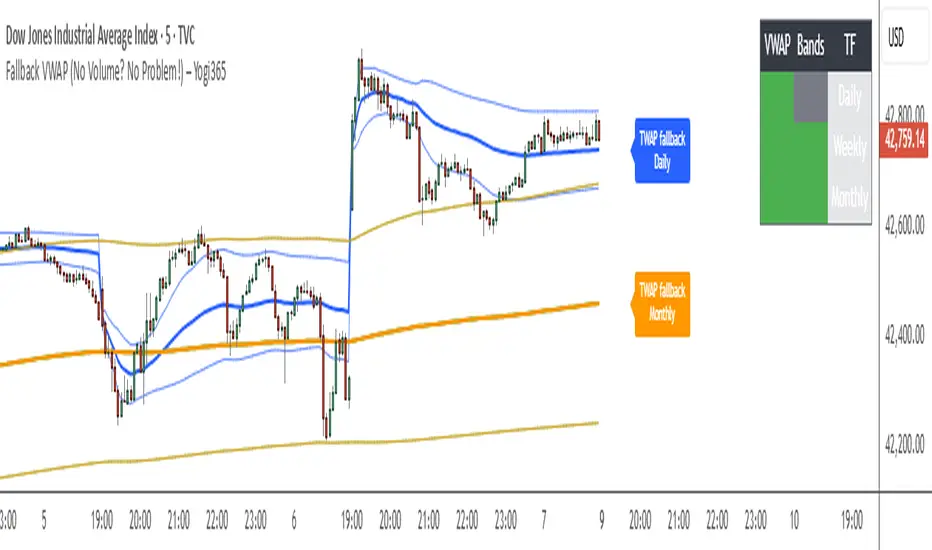

Fallback VWAP (No Volume? No Problem!) – Yogi365

Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。