OPEN-SOURCE SCRIPT

已更新 Robust Weighting Oscillator

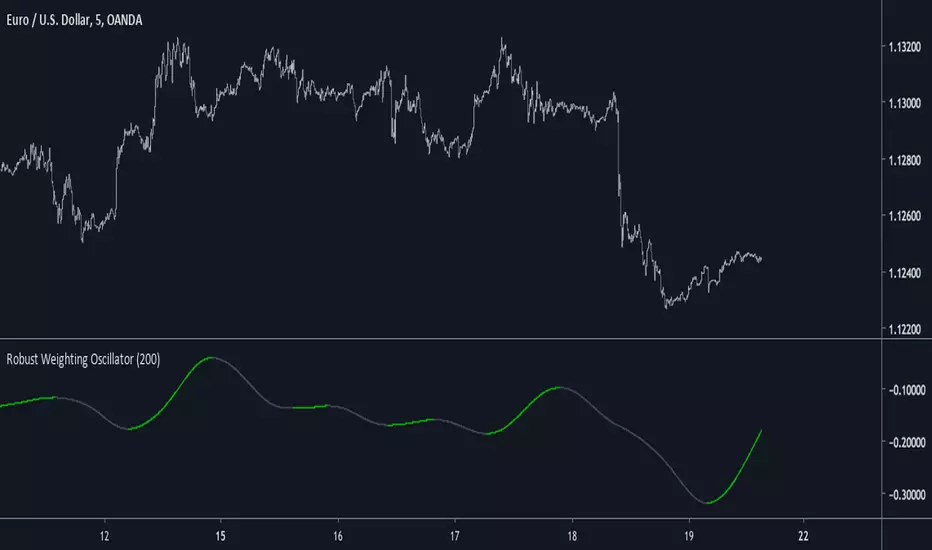

Introduction

A simple oscillator using a modified lowess architecture, good in term of smoothness and reactivity.

Lowess Regression

Lowess or local regression is a non-parametric (can be used with data not fitting a normal distribution) smoothing method. This method fit a curve to the data using least squares.

In order to have a lowess regression one must use tricube kernel for the weightings w, the weightings are determined using a k-nearest-neighbor model.

lowess is then calculated like so :

Σ(wG(y-a-bx)^2)

Our indicator use G, a ,b and remove the square as well as replacing x by y

Conclusion

The oscillator is simple and nothing revolutionary but its still interesting to have new indicators.

Lowess would be a great method to be made on pinescript, i have an estimate but its not that good. Some codes use a simple line equation in order to estimate a lowess smoother, i can describe it as ax + b where a is a smooth oscillator, b some kind of filter defined by lp + bp with lp a smooth low pass filter and bp a bandpass filter, x is a variable dependent of the smoothing span.

A simple oscillator using a modified lowess architecture, good in term of smoothness and reactivity.

Lowess Regression

Lowess or local regression is a non-parametric (can be used with data not fitting a normal distribution) smoothing method. This method fit a curve to the data using least squares.

In order to have a lowess regression one must use tricube kernel for the weightings w, the weightings are determined using a k-nearest-neighbor model.

lowess is then calculated like so :

Σ(wG(y-a-bx)^2)

Our indicator use G, a ,b and remove the square as well as replacing x by y

Conclusion

The oscillator is simple and nothing revolutionary but its still interesting to have new indicators.

Lowess would be a great method to be made on pinescript, i have an estimate but its not that good. Some codes use a simple line equation in order to estimate a lowess smoother, i can describe it as ax + b where a is a smooth oscillator, b some kind of filter defined by lp + bp with lp a smooth low pass filter and bp a bandpass filter, x is a variable dependent of the smoothing span.

發行說明

Added G in a separate calculation mode, thanks to @ aaahopper for pointing it out. Changed color for downside movements.開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。