OPEN-SOURCE SCRIPT

Keltner bounce from border. No repaint. V2 (by Zelibobla)

WARNING: despite of strategy doesn't use future data (not repaints) it doesn't consider broker`s commissions, which can be harmful for real life high frequency trading. Strategy will definitely fail on non-ordinary security behavior. But if new behavior will get stable, tuned params should make strategy profitable again.

This is the second version of this strategy tradingview.com/v/meiq0PyE/

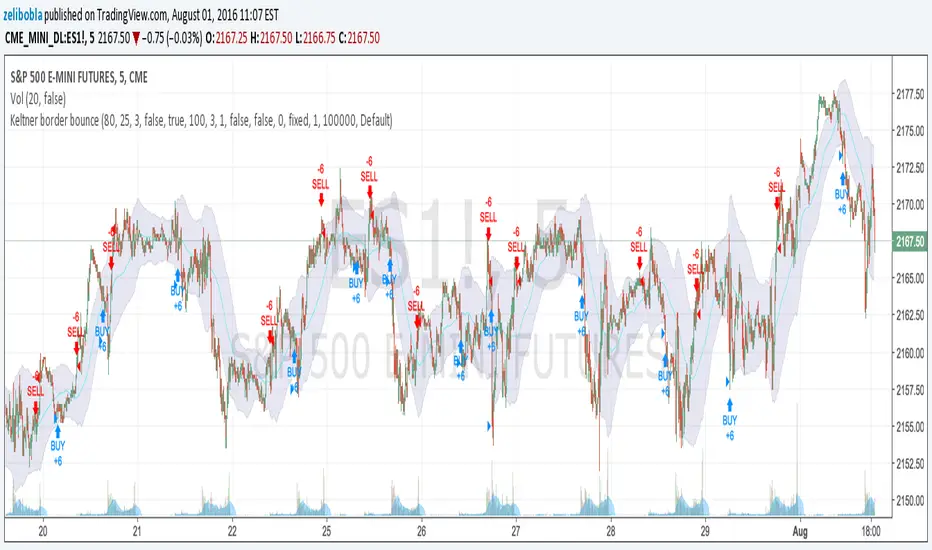

I've added emergency stop-loss ordering, parametrized trade size and enabled to switch strategy entry mode. Now it looks good on bigger timeframes such as 5min (ES1!) on screenshot. You are welcome to bring new ideas to enhance performance.

This is the second version of this strategy tradingview.com/v/meiq0PyE/

I've added emergency stop-loss ordering, parametrized trade size and enabled to switch strategy entry mode. Now it looks good on bigger timeframes such as 5min (ES1!) on screenshot. You are welcome to bring new ideas to enhance performance.

開源腳本

本著TradingView的真正精神,此腳本的創建者將其開源,以便交易者可以查看和驗證其功能。向作者致敬!雖然您可以免費使用它,但請記住,重新發佈程式碼必須遵守我們的網站規則。

免責聲明

這些資訊和出版物並不意味著也不構成TradingView提供或認可的金融、投資、交易或其他類型的意見或建議。請在使用條款閱讀更多資訊。

開源腳本

本著TradingView的真正精神,此腳本的創建者將其開源,以便交易者可以查看和驗證其功能。向作者致敬!雖然您可以免費使用它,但請記住,重新發佈程式碼必須遵守我們的網站規則。

免責聲明

這些資訊和出版物並不意味著也不構成TradingView提供或認可的金融、投資、交易或其他類型的意見或建議。請在使用條款閱讀更多資訊。