COT Comm OsciDescription

The COT Comm Osci is a sentiment oscillator based on net positions from the weekly Commitments of Traders (COT) report.

It transforms net positions of Commercials, Noncommercials, or Nonreportables into a 0–100 index.

A value of 100 = highest net position within the selected timeframe.

A value of 0 = lowest net position.

You can define three historical intervals (e.g. 26/ 52 / 156 weeks).

Tip

To improve your analysis, it's recommended to add a separate COT indicator that visualizes raw Long/Short or net positions directly. This helps interpret the oscillator in context.

This script is based on “Commercial Index–Buschi” by MagicEins and has been extended with new features and error handling.

Features

Select between Commercial, Noncommercial, or Nonreportable trader groups

Proper handling of HG Futures (Copper)

Displays a warning if the root code is invalid (unsupported market symbol)

Cftc

COT3 - Flip Strength Index - Invincible3This indicator uses the TradingView COT library to visualize institutional positioning and potential sentiment or trend shifts. It compares the long% vs short% of commercial and non-commercial traders for both Pair A and Pair B, helping traders identify trend strength, market overextension, and early reversal signals.

🔷 COT RSI

The COT RSI normalizes the net positioning difference between non-commercial and commercial traders over (N=13, 26, and 52)-week periods. It ranges from 0 to 100, highlighting when sentiment is at bullish or bearish extremes.

COT RSI (N)= ((NC - C)−min)/(max-min) x100

🟡 COT Index

The COT Index tracks where the current non-commercial net position lies within its 1-year and 3-year historical range. It reflects institutional accumulation or distribution phases.

Strength represents the magnitude of that positioning bias, visualized through normalized RSI-style metrics.

COT Index (N)= (NC net)/(max-min) x100

🔁 Flip Detection

Flip refers to the crossovers between long% and short%, indicating a change in directional bias among trader groups. When long positions exceed shorts (or vice versa), it signals a possible market flip in sentiment or trend.

For example, Pair B commercial flip is calculated as:

Long% = (Long/Open Interest)×100

Short% = (Short/Open Interest)×100

Flip = Long%−Short%

A bullish flip occurs when long% overtakes short%, and vice versa for a bearish flip. These flips often precede price trend changes or confirm sentiment breakouts.

Flip captures how far current positioning deviates from historical norms — highlighting periods of institutional overconfidence or exhaustion, often leading to significant market turns.

This combination offers a multi-layered edge for identifying when smart money is flipping direction, and whether that flip has strong conviction or is likely to fade.

..........................................................................................................................................................

COT-NocTradingIndicator Description:

Commitments of Traders (COT) Data Indicator

The Commitments of Traders (COT) Data Indicator on TradingView provides insights into market sentiment based on the weekly CFTC (Commodity Futures Trading Commission) reports. It plots three key lines derived from this data, offering valuable information for traders seeking to understand positioning trends among large speculators, commercial hedgers, and small traders.

Lines Plotted:

Commercials: Reflects positions held by commercial entities engaged in the production or sale of the underlying commodity. Their positions often act as a hedge against physical market exposure.

Non Commercials: Represents positions held by large speculators, typically hedge funds and large financial institutions, who often take more significant positions based on their market outlook.

Retail Traders: Shows positions held by small traders, including individual retail traders and smaller institutional players, providing insights into the broader retail sentiment.

Labeling:

Each line is accompanied by a label to clearly identify its corresponding group, enhancing clarity and ease of interpretation for traders analyzing the indicator.

Usage:

Trend Confirmation: Monitor the positioning of commercial and non commercial relative to retail traders to confirm trends and potential reversals.

Sentiment Analysis: Assess shifts in market sentiment based on changes in positioning across different trader categories.

Trading Signals: Use crossovers, divergences, and extreme positioning relative to historical data to generate potential trading signals.

This indicator is valuable for traders looking to incorporate institutional positioning data into their trading strategies, offering a deeper understanding of market dynamics beyond price action alone.

ILM CFTC COT Legacy PlotUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Disaggregated COT

www.cftc.gov

This script is very similar to COT Financial Plot indicator except that it plots the data for Futures in Legacy buckets Commercial vs. Non-Commercial

ILM CFTC COT Disaggregated PlotUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Disaggregated COT

www.cftc.gov

This script is very similar to COT Financial Plot indicator except that it plots the data for Disaggregated Futures

ILM COT Financial Table - CFTCUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Financials

www.cftc.gov

This script shows the Financial COT for the respective instrument by deriving the CFTC code.

Option is provided to override the CFTC code

User can also configure the historical CFTC data view

The script calculates the Long% vs Short% for various categories (Dealers/Asset Managers/Leveraged Funds/Other Reportables) and color codes the column appropriately.

The goal of this script is to show all the financial CFTC data on a single page to digest the data better in a tabular form

Fixed the default TradingView Library which has some errors with CFTC code mapping.

For example, SPX CFTC Code #13874+ which is the most important one where big players take positions is not there in the default Library.

LibraryCOT█ OVERVIEW

This library is a Pine programmer's tool that provides functions to access Commitment of Traders (COT) data for futures. Four of our scripts use it:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Financial Metrics

• Commitment of Traders: Total

If you do not program in Pine and want to use COT data, please see the indicators linked above.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

Accessing COT data from a Pine script requires the generation of a ticker ID string for use with request.security() . The ticker string must be encoded in a special format that includes both CFTC and TradingView-specific content. The format of the ticker IDs is somewhat complex; this library's functions make their generation easier. Note that if you know the COT ticker ID string for specific data, you can enter it from the chart's "Symbol Search" dialog box.

A ticker for COT data in Pine has the following structure:

COT:__<_metricDirection><_metricType>

where an underscore prefixing a component name inside <> is only included if the component is not a null string, and:

Is a digit representing the type of the COT report the data comes from: "" for legacy COT data, "2" for disaggregated data and "3" for financial data.

Is a six digit code that represents a commodity. Example: wheat futures (root "ZW") have the code "001602".

Is either "F" if the report data should exclude Options data, or "FO" if such data is included.

Is the TradingView code of the metric. This library's `metricNameAndDirectionToTicker()` function creates both

the and components of a COT ticker from the metric names and directions listed in the above chart.

The different metrics are explained in the CFTC's Explanatory Notes .

Is the direction of the metric: "Long", "Short", "Spreading" or "No direction".

Not all directions are applicable to all metrics. The valid ones are listed next to each metric in the above chart.

Is the type of the metric, possible values are "All", "Old" and "Other".

The difference between the types is explained in the "Old and Other Futures" section of the CFTC's Explanatory Notes .

As an example, the Legacy report Open Interest data for ZW futures (options included) in the old standard has the ticker "COT:001602_FO_OI_OLD". The same data using the current standard without futures has the ticker "COT:001602_F_OI".

█ USING THE LIBRARY

The first functions in the library are helper functions that generate components of a COT ticker ID. The last function, `COTTickerid()`, is the one that generates the full ticker ID string by calling some of the helper functions. We use it like this in our example:

exampleTicker = COTTickerid(

COTType = "Legacy",

CFTCCode = convertRootToCOTCode("Auto"),

includeOptions = false,

metricName = "Open Interest",

metricDirection = "No direction",

metricType = "All")

This library's chart displays the valid values for the `metricName` and `metricDirection` arguments. They vary for each of the three types of COT data (the `COTType` argument). The chart also displays the COT ticker ID string in the `exampleTicker` variable.

Look first. Then leap.

The library's functions are:

rootToCFTCCode(root)

Accepts a futures root and returns the relevant CFTC code.

Parameters:

root : Root prefix of the future's symbol, e.g. "ZC" for "ZC1!"" or "ZCU2021".

Returns: The part of a COT ticker corresponding to `root`, or "" if no CFTC code exists for the `root`.

currencyToCFTCCode(curr)

Converts a currency string to its corresponding CFTC code.

Parameters:

curr : Currency code, e.g., "USD" for US Dollar.

Returns: The corresponding to the currency, if one exists.

optionsToTicker(includeOptions)

Returns the part of a COT ticker using the `includeOptions` value supplied, which determines whether options data is to be included.

Parameters:

includeOptions : A "bool" value: 'true' if the symbol should include options and 'false' otherwise.

Returns: The part of a COT ticker: "FO" for data that includes options and "F" for data that doesn't.

metricNameAndDirectionToTicker(metricName, metricDirection)

Returns a string corresponding to a metric name and direction, which is one component required to build a valid COT ticker ID.

Parameters:

metricName : One of the metric names listed in this library's chart. Invalid values will cause a runtime error.

metricDirection : Metric direction. Possible values are: "Long", "Short", "Spreading", and "No direction".

Valid values vary with metrics. Invalid values will cause a runtime error.

Returns: The part of a COT ticker ID string, e.g., "OI_OLD" for "Open Interest" and "No direction",

or "TC_L" for "Traders Commercial" and "Long".

typeToTicker(metricType)

Converts a metric type into one component required to build a valid COT ticker ID.

See the "Old and Other Futures" section of the CFTC's Explanatory Notes for details on types.

Parameters:

metricType : Metric type. Accepted values are: "All", "Old", "Other".

Returns: The part of a COT ticker.

convertRootToCOTCode(mode, convertToCOT)

Depending on the `mode`, returns a CFTC code using the chart's symbol or its currency information when `convertToCOT = true`.

Otherwise, returns the symbol's root or currency information. If no COT data exists, a runtime error is generated.

Parameters:

mode : A string determining how the function will work. Valid values are:

"Root": the function extracts the futures symbol root (e.g. "ES" in "ESH2020") and looks for its CFTC code.

"Base currency": the function extracts the first currency in a pair (e.g. "EUR" in "EURUSD") and looks for its CFTC code.

"Currency": the function extracts the quote currency ("JPY" for "TSE:9984" or "USDJPY") and looks for its CFTC code.

"Auto": the function tries the first three modes (Root -> Base Currency -> Currency) until a match is found.

convertToCOT : "bool" value that, when `true`, causes the function to return a CFTC code.

Otherwise, the root or currency information is returned. Optional. The default is `true`.

Returns: If `convertToCOT` is `true`, the part of a COT ticker ID string.

If `convertToCOT` is `false`, the root or currency extracted from the current symbol.

COTTickerid(COTType, CTFCCode, includeOptions, metricName, metricDirection, metricType)

Returns a valid TradingView ticker for the COT symbol with specified parameters.

Parameters:

COTType : A string with the type of the report requested with the ticker, one of the following: "Legacy", "Disaggregated", "Financial".

CTFCCode : The for the asset, e.g., wheat futures (root "ZW") have the code "001602".

includeOptions : A boolean value. 'true' if the symbol should include options and 'false' otherwise.

metricName : One of the metric names listed in this library's chart.

metricDirection : Direction of the metric, one of the following: "Long", "Short", "Spreading", "No direction".

metricType : Type of the metric. Possible values: "All", "Old", and "Other".

Returns: A ticker ID string usable with `request.security()` to fetch the specified Commitment of Traders data.

█ AVAILABLE METRICS

Different COT types provide different metrics. The table of all metrics available for each of the types can be found below.

+------------------------------+------------------------+

| Legacy (COT) Metric Names | Directions |

+------------------------------+------------------------+

| Open Interest | No direction |

| Noncommercial Positions | Long, Short, Spreading |

| Commercial Positions | Long, Short |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No direction |

| Traders Noncommercial | Long, Short, Spreading |

| Traders Commercial | Long, Short |

| Traders Total Reportable | Long, Short |

| Concentration Gross LT 4 TDR | Long, Short |

| Concentration Gross LT 8 TDR | Long, Short |

| Concentration Net LT 4 TDR | Long, Short |

| Concentration Net LT 8 TDR | Long, Short |

+------------------------------+------------------------+

+-----------------------------------+------------------------+

| Disaggregated (COT2) Metric Names | Directions |

+-----------------------------------+------------------------+

| Open Interest | No Direction |

| Producer Merchant Positions | Long, Short |

| Swap Positions | Long, Short, Spreading |

| Managed Money Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Producer Merchant | Long, Short |

| Traders Swap | Long, Short, Spreading |

| Traders Managed Money | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-----------------------------------+------------------------+

+-------------------------------+------------------------+

| Financial (COT3) Metric Names | Directions |

+-------------------------------+------------------------+

| Open Interest | No Direction |

| Dealer Positions | Long, Short, Spreading |

| Asset Manager Positions | Long, Short, Spreading |

| Leveraged Funds Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Dealer | Long, Short, Spreading |

| Traders Asset Manager | Long, Short, Spreading |

| Traders Leveraged Funds | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-------------------------------+------------------------+

Noncommercial long futures position to overall Open InterestThis is an indicator that gets data from Quandl and presents weekly CFTC futures data (www.cftc.gov). In this indicator, the noncommercial long/short positions are calculated as a percentage of overall Open Interest. This indicates the bullish/bearish sentiment of the market.

Futures OI and Net positionsThis is an indicator that gets data from Quandl and presents weekly CFTC futures data (www.cftc.gov). In this indicator, Open Interest (OI) and net noncommercial positions are presented. Net_noncommercial positions are calculated as noncommercial_long - noncommercial_short.

COT Net Non-Commercials vs Commercials (Updated MTF Non-Repaint)Hello there,

With this script, you can see CFTC COT Non Commercial and Commercial Positions together.

This way, you can analyze net values greater than 0 and smaller, as well as very dense and very shallow positions of producers and speculators.

Green - Non Commercials - Speculators

Red - Commercials - Producers

This script is multi time-frame and non-repaint script.

Data pulled through Quandl.

And the latest version codes have been used.

As time goes by, I will try to make useful modifications to this scheme.

Regards.

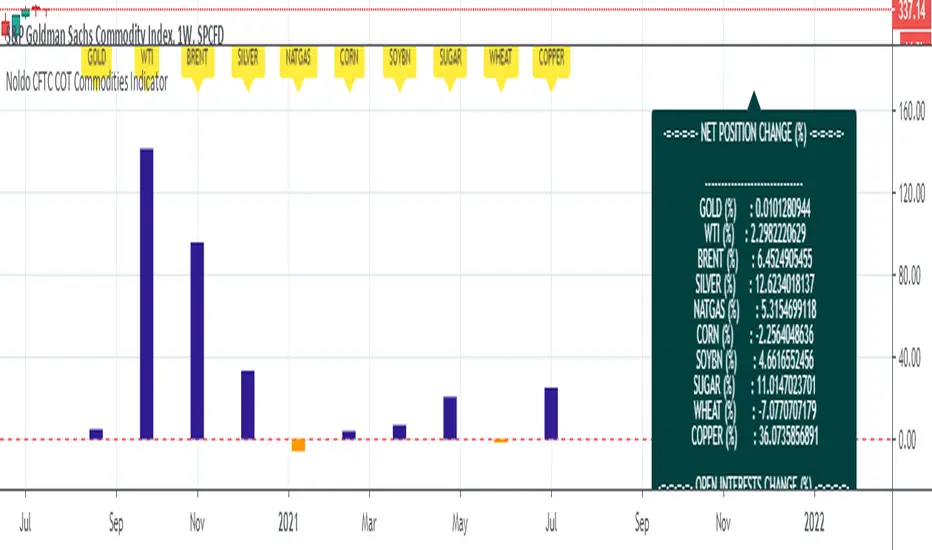

Noldo CFTC COT Commodities IndicatorHi.

Hello, this script has the same logic as Noldo CFTC COT Forex indicator :

It is the version for the future markets.

Major future assets are the subject.

Usage

This script works only on SPGSCI (S&P Goldman Sachs Commodity Index).

You must open SPGSCI :

www.tradingview.com

It only works on 1W graphics.

Because COT data is announced on Tuesday, it will cause repaint every Tuesday.

However, since it is a terminal, this factor is not strong enough to affect your decisions.

For use, you should open the bottom panel, go a little to the right in the history section and enlarge the panel you have opened.

The terminal will take its form in the presentation and provide analysis on the big screen.

COT data are pulled via Quandl.

Regards.

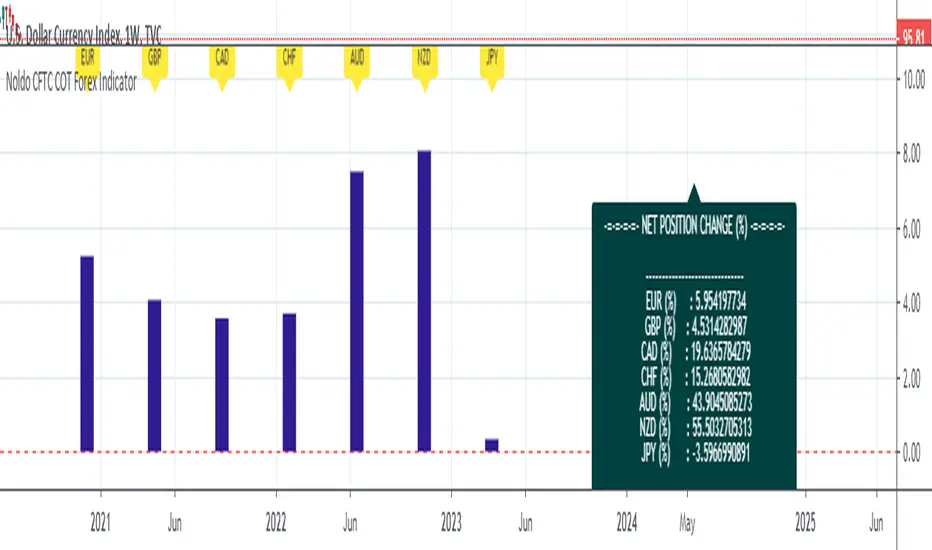

Noldo CFTC COT Forex IndicatorHello.

I decided to publish the COT Forex Indicator, which I created for convenience, as an open source.

The period DXY is determined by the differences between the two signals on the Pivot Reversal Strategy on the weekly chart.(1W)

Thus, relative period point search is automated.

When the new signal comes, after the closing, the number of bars between the previous bar before the new signal comes both directions.

This elapsed time is our period in which we will look back on relative changes.

If there is no signal, the period remains constant, thereby allowing us to notice excessive changes.

And in this period, COT data exchange and price changes are reflected in the terminal.

The automatic time-keeping of the period and the automatic generation of the relative differences of the terminals according to the period prevents a great loss of time.

Thus, we create one of the strong columns that enable us to make decisions.

The other column is the signals we obtained as a result of technical analysis.

The last column is the economic agenda and data tracking.

That's why I made my decision to share this:

Real life should not be distracted,

should not be drowned in the sea of technical analysis.

COT data is one of the most important and valuable tools that bring us signs of real life,

It should not be forgotten !

A lot of time is lost while doing these analyzes, and I wanted this to be much more practical and tidy!

And we can see if there are factors that will back up our incoming signals.

Usage

This script works only on DXY .

You must open DXY.

It only works on 1W graphics.

Because COT data is announced on Tuesday, it will cause repaint every Tuesday.

However, since it is a terminal, this factor is not strong enough to affect your decisions.

For use, you should open the bottom panel, go a little to the right in the history section and enlarge the panel you have opened.

The terminal will take its form in the presentation and provide analysis on the big screen.

COT data are pulled via Quandl.

General kind request:

Authors who know the technical broad expression of the security function or have an idea about its creation, please reach me.

Best regards.

Open Interest Market Facilitation IndexOriginal script from ChartChampions :

Let's start.

This script was created by using Open Interest instead of Volume in the Market Facilitation Index.

Thus, it can make a difference in the Future and CFD Markets.

If your financial instrument is not from these markets, that is, if Open Interest is not used, you can choose Volume.

You can set "FUTURES" and "OTHERS" from the menu.

If you use the Open Interest (FUTURES) option in the menu on 1W bars and defined Future markets, it will not repaint.

This is the best use for Open Interests, as data is extracted from Quandl and CFTC COT reports are published once a week.

Color Change Rules :

In my version :

Green Bars = Green

Fade Bars = Orange

Fake Bars = Blue

Squat Bars = Red

To show the difference in the presentation, both the Futures option using Open Interest and the Others option using Volume were published to compare.

You can observe the difference.

Best regards.

Accumulation/Distribution Open Interest Money Flow Hi, this script is the version of Accumulation / Distribution Money Flow (ADMF) that uses Open Interes ts in the required markets instead of Volume.

Can be set from the menu. (Futures/Others)

NOTE: I only modified this script.

The original script belongs to cl8DH.

Original of the script:

I think it will make a difference in the future and commodity markets.

Since the system uses CFTC data, use only for 1W timeframe.

With my best regards..

DXY COT Commercial Net PositionsThis script was created due to the lack of position of US Dollar Index Futures (DXY).

It is designed to perform a much more liquid and inclusive position analysis.

As the exponential ratios do not mean anything to positions, weights are used as multipliers instead of exponential functions.

Swedish Krona (SEK) Futures are not directly quoted in Quandl, therefore weighted in Euro / dollar parity.

By perceiving these positions as inverse correlations, you can also identify where the world economy is doing well.

COT Commercial Net Positions are calculated as (Short - Long) because of Commercials act according to the reverse of the market.

In this way, you can follow up normally instead of reverse correlation.

Because except in extreme cases, in which case capitals usually shift to Gold.

This is not the case, since there is no capital inflow to other currencies, it is not a strong sell position to the dollar index.

When there is a shift in bonds, we see the effect of the dollar in general.

I created for the Dollar Index in order not to deviate from the concept.

I wanted to share it with everyone as I thought that you have important clues about how investors take positions.

Modified currency weights :

Euro : % 61.8

Japanese Yen : % 13.6

British Pound : %11.9

Canadian Dollar : % 9.1

Swiss Franc : % 3.6

NOTE : You can use it for all instruments except crypto coins, especially US Dollar Index (DXY).

Since the COT data is taken, it will not repaint in 1 week (1W) timeframe.

The log can also be repaint according to the time of data publication.

It will repaint in lower time frames.

I hope it will help your analysis and your scripts,regards.

Open Interest Stochastic Money Flow IndexThis is the improved version of Stochastic Money Flow Index script that uses Open Interest instead of volume in Future markets.

I think it will make a difference especially in Future and CFD markets.

Since the system will pull data from Quandl, CFTC reports may cause repaint when disclosed.

So if you use it during the weekly time frame (1W), it will definitely not repaint.

You can also use the volume by selecting "Others" from the menu.This option applies to each instrument, you can use it on any financial instrument with or without COT data.

Bitcoin is included in the "Futures" option.

In Futures, you can observe the difference of Open Interest's success by comparing, since it counts exchanges between the two parties singularly, it reacts more firmly to speculative movements.

This script also includes alerts and bar color options, you can use from the menu.

It is also suitable for mutable variables.This script was freed from the integer loads.You can modify it in any adaptive or fractional period.

I hope it will help your analyzes, regards .

COT Commercial Positions (Updated)

This script aims to look at the markets from a manufacturer's point of view.

Producers or large enterprises gradually sell their goods as the price increases.

Because both the amount of product and position in their hands is too high, otherwise they can not find buyers, and they have to make a safe profit.

Therefore, I have shown short positions in green and long positions in red.

Blue is the net position formed by subtracting long positions from short positions.

This script is created with the latest Quandl data number codes.

Please let me know if you see a missing or a code update.

I recommend using it in a weekly (1W) time frame.

CAUTION : Since Bitcoin producer positions are very sparse, speculative long positions have been preferred in Bitcoin.

If you're looking for Bitcoin,

select Bitcoin from the menu.

Regards.

Open Interest Exponential Ease of MovementModified Ease of Movement :

* Open Interests used on Futures instead of Volume (Includes Bitcoin)

* Exponential Moving Average used instead of Simple Moving Average

* Division Number cancelled. (Division Number gives wrong signals inside strong trends.)

NOTE : This code is open source under the MIT License. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

Stay tuned. Best regards !

Open Interest Money Flow Index (OIMFI)CAUTION : This system was inspired from seiglerj' s "Money Flow Index " script. Open Interests are used instead of volume.

What is the Money Flow Index ( MFI )?

The Money Flow Index ( MFI ) is a technical oscillator that uses price and volume for identifying overbought or oversold conditions in an asset. It can also be used to spot divergences which warn of a trend change in price. The oscillator moves between 0 and 100.

Unlike conventional oscillators such as the Relative Strength Index ( RSI ), the Money Flow Index incorporates both price and volume data, as opposed to just price. For this reason, some analysts call MFI the volume-weighted RSI .

What Does the Money Flow Index ( MFI ) Tell You?

One of the primary ways to use the Money Flow Index is when there is a divergence. A divergence is when the oscillator is moving in the opposite direction of price. This is a signal of a potential reversal in the prevailing price trend.

For example, a very high Money Flow Index that begins to fall below a reading of 80 while the underlying security continues to climb is a price reversal signal to the downside. Conversely, a very low MFI reading that climbs above a reading of 20 while the underlying security continues to sell off is a price reversal signal to the upside.

Traders also watch for larger divergences using multiple waves in the price and MFI . For example, a stock peaks at $10, pulls back to $8, and then rallies to $12. The price has made two successive highs, at $10 and $12. If MFI makes a lower higher when the price reaches $12, the indicator is not confirming the new high. This could foreshadow a decline in price.

The overbought and oversold levels are also used to signal possible trading opportunities. Moves below 10 and above 90 are rare. Traders watch for the MFI to move back above 10 to signal a long trade, and to drop below 90 to signal a short trade.

Other moves out of overbought or oversold territory can also be useful. For example, when an asset is in an uptrend, a drop below 20 (or even 30) and then a rally back above it could indicate a pullback is over and the price uptrend is resuming. The same goes for a downtrend. A short-term rally could push the MFI up to 70 or 80, but when it drops back below that could be the time to enter a short trade in preparation for another drop .

Reference : www.investopedia.com

WARNING :

** Since each instrument in the list has its own unique contract data, you must first enter its name to display it. I recommend you to select OANDA from the markets. Finally, when the COT reports are issued, it may repaints. However, this repaint is usually close to closing or after close .(When COT reports are so sharp ) So use this script only 1W ( 1 week ) or 1 M ( 1 month ) timeframe.

** This data is taken to Tradingview with the help of Quandl. This is a very low possibility, but the system will not work if there is a malfunction.

FEATURES :

*** Working with all futures (Including : Bitcoin )

*** If you dont work with "Futures" , you can select "Others" from switchable menu and use volume for all instruments.

*** New generation elegant design used : Adaptive coloring Overbought - Oversold Levels according to the closing price.

NOTE : This code is open source under the MIT License. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

Stay tuned. Best wishes !

Weiss Wave Open Interest BarsFirstly :

LazyBear ' s "Weiss Wave " codes are used for open interests.

Original Weiss Wave Volume :

Let's start :

Open Interest vs. Volume: An Overview

Volume and open interest are two key measurements that describe the liquidity and activity of contracts In the options and futures markets. However, their meanings and applications are different. Volume refers to the number of contracts traded in a given period, while open interest denotes the number of active contracts.

Volume

Trading volume measures the number of options or futures contracts being exchanged between buyers and sellers, identifying the level of activity for that particular contract. For every buyer, there is a seller, and the transaction itself counts toward the daily volume.

Open Interest

Open interest indicates the number of options or futures contracts that are held by traders and investors in active positions. These positions have not been closed out, expired, or exercised. Open interest decreases when holders and writers of options (or buyers and sellers of futures) close out their positions. To close out positions, they must take offsetting positions or exercise their options. Open interest increases once again when investors and traders open new long positions or writers/sellers take on new short positions. Open interest also increases when new options or futures contracts are created.

Options or futures contract trading volume can only increase while open interest can either increase or decrease. While trading volume indicates the number of contracts that have been bought or sold, open interest identifies the number of contracts that are currently held.

Reference : www.investopedia.com

*** Worked to define all futures . You can look them in codes (between line : 13 to line 94 )

** CAUTION 1 : Since each instrument in the list has its own unique contract data, you must first enter its name to display it. I recommend you to select OANDA from the markets. Finally, when the COT reports are issued, it may repaints. However, this repaint is usually close to closing or after close .(When COT reports are so sharp ) So use this script only 1W ( 1 week ) or 1 M ( 1 month ) timeframe.

** CAUTION 2 : This data is taken to Tradingview with the help of Quandl. This is a tremendous possibility, but the system will not work if there is a malfunction.

Best regards.