Mandelbrot-Fibonacci Cascade Vortex (MFCV)Mandelbrot-Fibonacci Cascade Vortex (MFCV) - Where Chaos Theory Meets Sacred Geometry

A Revolutionary Synthesis of Fractal Mathematics and Golden Ratio Dynamics

What began as an exploration into Benoit Mandelbrot's fractal market hypothesis and the mysterious appearance of Fibonacci sequences in nature has culminated in a groundbreaking indicator that reveals the hidden mathematical structure underlying market movements. This indicator represents months of research into chaos theory, fractal geometry, and the golden ratio's manifestation in financial markets.

The Theoretical Foundation

Mandelbrot's Fractal Market Hypothesis Traditional efficient market theory assumes normal distributions and random walks. Mandelbrot proved markets are fractal - self-similar patterns repeating across all timeframes with power-law distributions. The MFCV implements this through:

Hurst Exponent Calculation: H = log(R/S) / log(n/2)

Where:

R = Range of cumulative deviations

S = Standard deviation

n = Period length

This measures market memory:

H > 0.5: Trending (persistent) behavior

H = 0.5: Random walk

H < 0.5: Mean-reverting (anti-persistent) behavior

Fractal Dimension: D = 2 - H

This quantifies market complexity, where higher dimensions indicate more chaotic behavior.

Fibonacci Vortex Theory Markets don't move linearly - they spiral. The MFCV reveals these spirals using Fibonacci sequences:

Vortex Calculation: Vortex(n) = Price + sin(bar_index × φ / Fn) × ATR(Fn) × Volume_Factor

Where:

φ = 0.618 (golden ratio)

Fn = Fibonacci number (8, 13, 21, 34, 55)

Volume_Factor = 1 + (Volume/SMA(Volume,50) - 1) × 0.5

This creates oscillating spirals that contract and expand with market energy.

The Volatility Cascade System

Markets exhibit volatility clustering - Mandelbrot's "Noah Effect." The MFCV captures this through cascading volatility bands:

Cascade Level Calculation: Level(i) = ATR(20) × φ^i

Each level represents a different fractal scale, creating a multi-dimensional view of market structure. The golden ratio spacing ensures harmonic resonance between levels.

Implementation Architecture

Core Components:

Fractal Analysis Engine

Calculates Hurst exponent over user-defined periods

Derives fractal dimension for complexity measurement

Identifies market regime (trending/ranging/chaotic)

Fibonacci Vortex Generator

Creates 5 independent spiral oscillators

Each spiral follows a Fibonacci period

Volume amplification creates dynamic response

Cascade Band System

Up to 8 volatility levels

Golden ratio expansion between levels

Dynamic coloring based on fractal state

Confluence Detection

Identifies convergence of vortex and cascade levels

Highlights high-probability reversal zones

Real-time confluence strength calculation

Signal Generation Logic

The MFCV generates two primary signal types:

Fractal Signals: Generated when:

Hurst > 0.65 (strong trend) AND volatility expanding

Hurst < 0.35 (mean reversion) AND RSI < 35

Trend strength > 0.4 AND vortex alignment

Cascade Signals: Triggered by:

RSI > 60 AND price > SMA(50) AND bearish vortex

RSI < 40 AND price < SMA(50) AND bullish vortex

Volatility expansion AND trend strength > 0.3

Both signals implement a 15-bar cooldown to prevent overtrading.

Advanced Input System

Mandelbrot Parameters:

Cascade Levels (3-8):

Controls number of volatility bands

Crypto: 5-7 (high volatility)

Indices: 4-5 (moderate volatility)

Forex: 3-4 (low volatility)

Hurst Period (20-200):

Lookback for fractal calculation

Scalping: 20-50

Day Trading: 50-100

Swing Trading: 100-150

Position Trading: 150-200

Cascade Ratio (1.0-3.0):

Band width multiplier

1.618: Golden ratio (default)

Higher values for trending markets

Lower values for ranging markets

Fractal Memory (21-233):

Fibonacci retracement lookback

Uses Fibonacci numbers for harmonic alignment

Fibonacci Vortex Settings:

Spiral Periods:

Comma-separated Fibonacci sequence

Fast: "5,8,13,21,34" (scalping)

Standard: "8,13,21,34,55" (balanced)

Extended: "13,21,34,55,89" (swing)

Rotation Speed (0.1-2.0):

Controls spiral oscillation frequency

0.618: Golden ratio (balanced)

Higher = more signals, more noise

Lower = smoother, fewer signals

Volume Amplification:

Enables dynamic spiral expansion

Essential for stocks and crypto

Disable for forex (no central volume)

Visual System Architecture

Cascade Bands:

Multi-level volatility envelopes

Gradient coloring from primary to secondary theme

Transparency increases with distance from price

Fill between bands shows fractal structure

Vortex Spirals:

5 Fibonacci-period oscillators

Blue above price (bullish pressure)

Red below price (bearish pressure)

Multiple display styles: Lines, Circles, Dots, Cross

Dynamic Fibonacci Levels:

Auto-updating retracement levels

Smart update logic prevents disruption near levels

Distance-based transparency (closer = more visible)

Updates every 50 bars or on volatility spikes

Confluence Zones:

Highlighted boxes where indicators converge

Stronger confluence = stronger support/resistance

Key areas for reversal trades

Professional Dashboard System

Main Fractal Dashboard: Displays real-time:

Hurst Exponent with market state

Fractal Dimension with complexity level

Volatility Cascade status

Vortex rotation impact

Market regime classification

Signal strength percentage

Active indicator levels

Vortex Metrics Panel: Shows:

Individual spiral deviations

Convergence/divergence metrics

Real-time vortex positioning

Fibonacci period performance

Fractal Metrics Display: Tracks:

Dimension D value

Market complexity rating

Self-similarity strength

Trend quality assessment

Theory Guide Panel: Educational reference showing:

Mandelbrot principles

Fibonacci vortex concepts

Dynamic trading suggestions

Trading Applications

Trend Following:

High Hurst (>0.65) indicates strong trends

Follow cascade band direction

Use vortex spirals for entry timing

Exit when Hurst drops below 0.5

Mean Reversion:

Low Hurst (<0.35) signals reversal potential

Trade toward vortex spiral convergence

Use Fibonacci levels as targets

Tighten stops in chaotic regimes

Breakout Trading:

Monitor cascade band compression

Watch for vortex spiral alignment

Volatility expansion confirms breakouts

Use confluence zones for targets

Risk Management:

Position size based on fractal dimension

Wider stops in high complexity markets

Tighter stops when Hurst is extreme

Scale out at Fibonacci levels

Market-Specific Optimization

Cryptocurrency:

Cascade Levels: 5-7

Hurst Period: 50-100

Rotation Speed: 0.786-1.2

Enable volume amplification

Stock Indices:

Cascade Levels: 4-5

Hurst Period: 80-120

Rotation Speed: 0.5-0.786

Moderate cascade ratio

Forex:

Cascade Levels: 3-4

Hurst Period: 100-150

Rotation Speed: 0.382-0.618

Disable volume amplification

Commodities:

Cascade Levels: 4-6

Hurst Period: 60-100

Rotation Speed: 0.5-1.0

Seasonal adjustment consideration

Innovation and Originality

The MFCV represents several breakthrough innovations:

First Integration of Mandelbrot Fractals with Fibonacci Vortex Theory

Unique synthesis of chaos theory and sacred geometry

Novel application of Hurst exponent to spiral dynamics

Dynamic Volatility Cascade System

Golden ratio-based band expansion

Multi-timeframe fractal analysis

Self-adjusting to market conditions

Volume-Amplified Vortex Spirals

Revolutionary spiral calculation method

Dynamic response to market participation

Multiple Fibonacci period integration

Intelligent Signal Generation

Cooldown system prevents overtrading

Multi-factor confirmation required

Regime-aware signal filtering

Professional Analytics Dashboard

Institutional-grade metrics display

Real-time fractal analysis

Educational integration

Development Journey

Creating the MFCV involved overcoming numerous challenges:

Mathematical Complexity: Implementing Hurst exponent calculations efficiently

Visual Clarity: Displaying multiple indicators without cluttering

Performance Optimization: Managing array operations and calculations

Signal Quality: Balancing sensitivity with reliability

User Experience: Making complex theory accessible

The result is an indicator that brings PhD-level mathematics to practical trading while maintaining visual elegance and usability.

Best Practices and Guidelines

Start Simple: Use default settings initially

Match Timeframe: Adjust parameters to your trading style

Confirm Signals: Never trade MFCV signals in isolation

Respect Regimes: Adapt strategy to market state

Manage Risk: Use fractal dimension for position sizing

Color Themes

Six professional themes included:

Fractal: Balanced blue/purple palette

Golden: Warm Fibonacci-inspired colors

Plasma: Vibrant modern aesthetics

Cosmic: Dark mode optimized

Matrix: Classic green terminal

Fire: Heat map visualization

Disclaimer

This indicator is for educational and research purposes only. It does not constitute financial advice. While the MFCV reveals deep market structure through advanced mathematics, markets remain inherently unpredictable. Past performance does not guarantee future results.

The integration of Mandelbrot's fractal theory with Fibonacci vortex dynamics provides unique market insights, but should be used as part of a comprehensive trading strategy. Always use proper risk management and never risk more than you can afford to lose.

Acknowledgments

Special thanks to Benoit Mandelbrot for revolutionizing our understanding of markets through fractal geometry, and to the ancient mathematicians who discovered the golden ratio's universal significance.

"The geometry of nature is fractal... Markets are fractal too." - Benoit Mandelbrot

Revealing the Hidden Order in Market Chaos Trade with Mathematical Precision. Trade with MFCV.

— Created with passion for the TradingView community

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

指標和策略

EMD Trend [InvestorUnknown]EMD Trend is a dynamic trend-following indicator that utilizes Exponential Moving Deviation (EMD) to build adaptive channels around a selected moving average. Designed for traders who value responsive trend signals with built-in volatility sensitivity, this tool highlights directional bias, market regime shifts, and potential breakout opportunities.

How It Works

Instead of using standard deviation, EMD Trend employs the exponential moving average of the absolute deviation from a moving average—producing smoother, faster-reacting upper and lower bounds:

Bullish (Risk-ON Long): Price crosses above the upper EMD band

Bearish (Risk-ON Short): Price crosses below the lower EMD band

Neutral: Price stays within the channel, indicating potential mean reversion or low momentum

Trend direction is defined by price interaction with these bands, and visual cues (color-coded bars and fills) help quickly identify market conditions.

Features

7 Moving Average Types: SMA, EMA, HMA, DEMA, TEMA, RMA, FRAMA

Custom Price Source: Choose close, hl2, ohlc4, or others

EMD Multiplier: Controls the width of the deviation envelope

Bar Coloring: Candles change color based on current trend

Intra-bar Signal Option: Enables faster updates (with optional repainting)

Speculative Zones: Fills highlight aggressive momentum moves beyond EMD bounds

Backtest Mode

Switch to Backtest Mode for performance evaluation over historical data:

Equity Curve Plot: Compare EMD Trend strategy vs. Buy & Hold

Trade Metrics Table: View number of trades, win/loss stats, profits

Performance Metrics Table: Includes CAGR, Sharpe, max drawdown, and more

Custom Start Date: Select from which date the backtest should begin

Trade Sizing: Configure capital and trade percentage per entry

Signal Filters: Choose from Long Only, Short Only, or Both

Alerts

Built-in alerts let you automate entries, exits, and trend transitions:

LONG (EMD Trend) - Trend flips to Long

SHORT (EMD Trend) - Trend flips to Short

RISK-ON LONG - Price crosses above upper EMD band

RISK-OFF LONG - Price crosses back below upper EMD band

RISK-ON SHORT - Price crosses below lower EMD band

RISK-OFF SHORT - Price crosses back above lower EMD band

Use Cases

Trend Confirmation with volatility-sensitive boundaries

Momentum Entry Filtering via breakout zones

Mean Reversion Avoidance in sideways markets

Backtesting & Strategy Building with real-time metrics

Disclaimer

This indicator is intended for informational and educational purposes only. It does not constitute investment advice. Historical performance does not guarantee future results. Always backtest and use in simulation before live trading.

Bear Market Probability Model# Bear Market Probability Model: A Multi-Factor Risk Assessment Framework

The Bear Market Probability Model represents a comprehensive quantitative framework for assessing systemic market risk through the integration of 13 distinct risk factors across four analytical categories: macroeconomic indicators, technical analysis factors, market sentiment measures, and market breadth metrics. This indicator synthesizes established financial research methodologies to provide real-time probabilistic assessments of impending bear market conditions, offering institutional-grade risk management capabilities to retail and professional traders alike.

## Theoretical Foundation

### Historical Context of Bear Market Prediction

Bear market prediction has been a central focus of financial research since the seminal work of Dow (1901) and the subsequent development of technical analysis theory. The challenge of predicting market downturns gained renewed academic attention following the market crashes of 1929, 1987, 2000, and 2008, leading to the development of sophisticated multi-factor models.

Fama and French (1989) demonstrated that certain financial variables possess predictive power for stock returns, particularly during market stress periods. Their three-factor model laid the groundwork for multi-dimensional risk assessment, which this indicator extends through the incorporation of real-time market microstructure data.

### Methodological Framework

The model employs a weighted composite scoring methodology based on the theoretical framework established by Campbell and Shiller (1998) for market valuation assessment, extended through the incorporation of high-frequency sentiment and technical indicators as proposed by Baker and Wurgler (2006) in their seminal work on investor sentiment.

The mathematical foundation follows the general form:

Bear Market Probability = Σ(Wi × Ci) / ΣWi × 100

Where:

- Wi = Category weight (i = 1,2,3,4)

- Ci = Normalized category score

- Categories: Macroeconomic, Technical, Sentiment, Breadth

## Component Analysis

### 1. Macroeconomic Risk Factors

#### Yield Curve Analysis

The inclusion of yield curve inversion as a primary predictor follows extensive research by Estrella and Mishkin (1998), who demonstrated that the term spread between 3-month and 10-year Treasury securities has historically preceded all major recessions since 1969. The model incorporates both the 2Y-10Y and 3M-10Y spreads to capture different aspects of monetary policy expectations.

Implementation:

- 2Y-10Y Spread: Captures market expectations of monetary policy trajectory

- 3M-10Y Spread: Traditional recession predictor with 12-18 month lead time

Scientific Basis: Harvey (1988) and subsequent research by Ang, Piazzesi, and Wei (2006) established the theoretical foundation linking yield curve inversions to economic contractions through the expectations hypothesis of the term structure.

#### Credit Risk Premium Assessment

High-yield credit spreads serve as a real-time gauge of systemic risk, following the methodology established by Gilchrist and Zakrajšek (2012) in their excess bond premium research. The model incorporates the ICE BofA High Yield Master II Option-Adjusted Spread as a proxy for credit market stress.

Threshold Calibration:

- Normal conditions: < 350 basis points

- Elevated risk: 350-500 basis points

- Severe stress: > 500 basis points

#### Currency and Commodity Stress Indicators

The US Dollar Index (DXY) momentum serves as a risk-off indicator, while the Gold-to-Oil ratio captures commodity market stress dynamics. This approach follows the methodology of Akram (2009) and Beckmann, Berger, and Czudaj (2015) in analyzing commodity-currency relationships during market stress.

### 2. Technical Analysis Factors

#### Multi-Timeframe Moving Average Analysis

The technical component incorporates the well-established moving average convergence methodology, drawing from the work of Brock, Lakonishok, and LeBaron (1992), who provided empirical evidence for the profitability of technical trading rules.

Implementation:

- Price relative to 50-day and 200-day simple moving averages

- Moving average convergence/divergence analysis

- Multi-timeframe MACD assessment (daily and weekly)

#### Momentum and Volatility Analysis

The model integrates Relative Strength Index (RSI) analysis following Wilder's (1978) original methodology, combined with maximum drawdown analysis based on the work of Magdon-Ismail and Atiya (2004) on optimal drawdown measurement.

### 3. Market Sentiment Factors

#### Volatility Index Analysis

The VIX component follows the established research of Whaley (2009) and subsequent work by Bekaert and Hoerova (2014) on VIX as a predictor of market stress. The model incorporates both absolute VIX levels and relative VIX spikes compared to the 20-day moving average.

Calibration:

- Low volatility: VIX < 20

- Elevated concern: VIX 20-25

- High fear: VIX > 25

- Panic conditions: VIX > 30

#### Put-Call Ratio Analysis

Options flow analysis through put-call ratios provides insight into sophisticated investor positioning, following the methodology established by Pan and Poteshman (2006) in their analysis of informed trading in options markets.

### 4. Market Breadth Factors

#### Advance-Decline Analysis

Market breadth assessment follows the classic work of Fosback (1976) and subsequent research by Brown and Cliff (2004) on market breadth as a predictor of future returns.

Components:

- Daily advance-decline ratio

- Advance-decline line momentum

- McClellan Oscillator (Ema19 - Ema39 of A-D difference)

#### New Highs-New Lows Analysis

The new highs-new lows ratio serves as a market leadership indicator, based on the research of Zweig (1986) and validated in academic literature by Zarowin (1990).

## Dynamic Threshold Methodology

The model incorporates adaptive thresholds based on rolling volatility and trend analysis, following the methodology established by Pagan and Sossounov (2003) for business cycle dating. This approach allows the model to adjust sensitivity based on prevailing market conditions.

Dynamic Threshold Calculation:

- Warning Level: Base threshold ± (Volatility × 1.0)

- Danger Level: Base threshold ± (Volatility × 1.5)

- Bounds: ±10-20 points from base threshold

## Professional Implementation

### Institutional Usage Patterns

Professional risk managers typically employ multi-factor bear market models in several contexts:

#### 1. Portfolio Risk Management

- Tactical Asset Allocation: Reducing equity exposure when probability exceeds 60-70%

- Hedging Strategies: Implementing protective puts or VIX calls when warning thresholds are breached

- Sector Rotation: Shifting from growth to defensive sectors during elevated risk periods

#### 2. Risk Budgeting

- Value-at-Risk Adjustment: Incorporating bear market probability into VaR calculations

- Stress Testing: Using probability levels to calibrate stress test scenarios

- Capital Requirements: Adjusting regulatory capital based on systemic risk assessment

#### 3. Client Communication

- Risk Reporting: Quantifying market risk for client presentations

- Investment Committee Decisions: Providing objective risk metrics for strategic decisions

- Performance Attribution: Explaining defensive positioning during market stress

### Implementation Framework

Professional traders typically implement such models through:

#### Signal Hierarchy:

1. Probability < 30%: Normal risk positioning

2. Probability 30-50%: Increased hedging, reduced leverage

3. Probability 50-70%: Defensive positioning, cash building

4. Probability > 70%: Maximum defensive posture, short exposure consideration

#### Risk Management Integration:

- Position Sizing: Inverse relationship between probability and position size

- Stop-Loss Adjustment: Tighter stops during elevated risk periods

- Correlation Monitoring: Increased attention to cross-asset correlations

## Strengths and Advantages

### 1. Comprehensive Coverage

The model's primary strength lies in its multi-dimensional approach, avoiding the single-factor bias that has historically plagued market timing models. By incorporating macroeconomic, technical, sentiment, and breadth factors, the model provides robust risk assessment across different market regimes.

### 2. Dynamic Adaptability

The adaptive threshold mechanism allows the model to adjust sensitivity based on prevailing volatility conditions, reducing false signals during low-volatility periods and maintaining sensitivity during high-volatility regimes.

### 3. Real-Time Processing

Unlike traditional academic models that rely on monthly or quarterly data, this indicator processes daily market data, providing timely risk assessment for active portfolio management.

### 4. Transparency and Interpretability

The component-based structure allows users to understand which factors are driving risk assessment, enabling informed decision-making about model signals.

### 5. Historical Validation

Each component has been validated in academic literature, providing theoretical foundation for the model's predictive power.

## Limitations and Weaknesses

### 1. Data Dependencies

The model's effectiveness depends heavily on the availability and quality of real-time economic data. Federal Reserve Economic Data (FRED) updates may have lags that could impact model responsiveness during rapidly evolving market conditions.

### 2. Regime Change Sensitivity

Like most quantitative models, the indicator may struggle during unprecedented market conditions or structural regime changes where historical relationships break down (Taleb, 2007).

### 3. False Signal Risk

Multi-factor models inherently face the challenge of balancing sensitivity with specificity. The model may generate false positive signals during normal market volatility periods.

### 4. Currency and Geographic Bias

The model focuses primarily on US market indicators, potentially limiting its effectiveness for global portfolio management or non-USD denominated assets.

### 5. Correlation Breakdown

During extreme market stress, correlations between risk factors may increase dramatically, reducing the model's diversification benefits (Forbes and Rigobon, 2002).

## References

Akram, Q. F. (2009). Commodity prices, interest rates and the dollar. Energy Economics, 31(6), 838-851.

Ang, A., Piazzesi, M., & Wei, M. (2006). What does the yield curve tell us about GDP growth? Journal of Econometrics, 131(1-2), 359-403.

Baker, M., & Wurgler, J. (2006). Investor sentiment and the cross‐section of stock returns. The Journal of Finance, 61(4), 1645-1680.

Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593-1636.

Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261-292.

Beckmann, J., Berger, T., & Czudaj, R. (2015). Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling, 48, 16-24.

Bekaert, G., & Hoerova, M. (2014). The VIX, the variance premium and stock market volatility. Journal of Econometrics, 183(2), 181-192.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Brown, G. W., & Cliff, M. T. (2004). Investor sentiment and the near-term stock market. Journal of Empirical Finance, 11(1), 1-27.

Campbell, J. Y., & Shiller, R. J. (1998). Valuation ratios and the long-run stock market outlook. The Journal of Portfolio Management, 24(2), 11-26.

Dow, C. H. (1901). Scientific stock speculation. The Magazine of Wall Street.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1989). Business conditions and expected returns on stocks and bonds. Journal of Financial Economics, 25(1), 23-49.

Forbes, K. J., & Rigobon, R. (2002). No contagion, only interdependence: measuring stock market comovements. The Journal of Finance, 57(5), 2223-2261.

Fosback, N. G. (1976). Stock market logic: A sophisticated approach to profits on Wall Street. The Institute for Econometric Research.

Gilchrist, S., & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. American Economic Review, 102(4), 1692-1720.

Harvey, C. R. (1988). The real term structure and consumption growth. Journal of Financial Economics, 22(2), 305-333.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Magdon-Ismail, M., & Atiya, A. F. (2004). Maximum drawdown. Risk, 17(10), 99-102.

Nickerson, R. S. (1998). Confirmation bias: A ubiquitous phenomenon in many guises. Review of General Psychology, 2(2), 175-220.

Pagan, A. R., & Sossounov, K. A. (2003). A simple framework for analysing bull and bear markets. Journal of Applied Econometrics, 18(1), 23-46.

Pan, J., & Poteshman, A. M. (2006). The information in option volume for future stock prices. The Review of Financial Studies, 19(3), 871-908.

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. Random House.

Whaley, R. E. (2009). Understanding the VIX. The Journal of Portfolio Management, 35(3), 98-105.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Zarowin, P. (1990). Size, seasonality, and stock market overreaction. Journal of Financial and Quantitative Analysis, 25(1), 113-125.

Zweig, M. E. (1986). Winning on Wall Street. Warner Books.

Range Filter [DW]This is an experimental study designed to filter out minor price action for a clearer view of trends.

Inspired by the QQE's volatility filter, this filter applies the process directly to price rather than to a smoothed RSI.

First, a smooth average price range is calculated for the basis of the filter and multiplied by a specified amount.

Next, the filter is calculated by gating price movements that do not exceed the specified range.

Lastly the target ranges are plotted to display the prices that will trigger filter movement.

Custom bar colors are included. The color scheme is based on the filtered price trend.

Delta Volume Columns Pro [LucF]█ OVERVIEW

This indicator displays volume delta information calculated with intrabar inspection on historical bars, and feed updates when running in realtime. It is designed to run in a pane and can display either stacked buy/sell volume columns or a signal line which can be calculated and displayed in many different ways.

Five different models are offered to reveal different characteristics of the calculated volume delta information. Many options are offered to visualize the calculations, giving you much leeway in morphing the indicator's visuals to suit your needs. If you value delta volume information, I hope you will find the time required to master Delta Volume Columns Pro well worth the investment. I am confident that if you combine a proper understanding of the indicator's information with an intimate knowledge of the volume idiosyncrasies on the markets you trade, you can extract useful market intelligence using this tool.

█ WARNINGS

1. The indicator only works on markets where volume information is available,

Please validate that your symbol's feed carries volume information before asking me why the indicator doesn't plot values.

2. When you refresh your chart or re-execute the script on the chart, the indicator will repaint because elapsed realtime bars will then recalculate as historical bars.

3. Because the indicator uses different modes of calculation on historical and realtime bars, it's critical that you understand the differences between them. Details are provided further down.

4. Calculations using intrabar inspection on historical bars can only be done from some chart timeframes. See further down for a list of supported timeframes.

If the chart's timeframe is not supported, no historical volume delta will display.

█ CONCEPTS

Chart bars

Three different types of bars are used in charts:

1. Historical bars are bars that have already closed when the script executes on them.

2. The realtime bar is the current, incomplete bar where a script is running on an open market. There is only one active realtime bar on your chart at any given time.

The realtime bar is where alerts trigger.

3. Elapsed realtime bars are bars that were calculated when they were realtime bars but have since closed.

When a script re-executes on a chart because the browser tab is refreshed or some of its inputs are changed, elapsed realtime bars are recalculated as historical bars.

Why does this indicator use two modes of calculation?

Historical bars on TradingView charts contain OHLCV data only, which is insufficient to calculate volume delta on them with any level of precision. To mine more detailed information from those bars we look at intrabars , i.e., bars from a smaller timeframe (we call it the intrabar timeframe ) that are contained in one chart bar. If your chart Is running at 1D on a 24x7 market for example, most 1D chart bars will contain 24 underlying 1H bars in their dilation. On historical bars, this indicator looks at those intrabars to amass volume delta information. If the intrabar is up, its volume goes in the Buy bin, and inversely for the Sell bin. When price does not move on an intrabar, the polarity of the last known movement is used to determine in which bin its volume goes.

In realtime, we have access to price and volume change for each update of the chart. Because a 1D chart bar can be updated tens of thousands of times during the day, volume delta calculations on those updates is much more precise. This precision, however, comes at a price:

— The script must be running on the chart for it to keep calculating in realtime.

— If you refresh your chart you will lose all accumulated realtime calculations on elapsed realtime bars, and the realtime bar.

Elapsed realtime bars will recalculate as historical bars, i.e., using intrabar inspection, and the realtime bar's calculations will reset.

When the script recalculates elapsed realtime bars as historical bars, the values on those bars will change, which means the script repaints in those conditions.

— When the indicator first calculates on a chart containing an incomplete realtime bar, it will count ALL the existing volume on the bar as Buy or Sell volume,

depending on the polarity of the bar at that point. This will skew calculations for that first bar. Scripts have no access to the history of a realtime bar's previous updates,

and intrabar inspection cannot be used on realtime bars, so this is the only to go about this.

— Even if alerts only trigger upon confirmation of their conditions after the realtime bar closes, they are repainting alerts

because they would perhaps not have calculated the same way using intrabar inspection.

— On markets like stocks that often have different EOD and intraday feeds and volume information,

the volume's scale may not be the same for the realtime bar if your chart is at 1D, for example,

and the indicator is using an intraday timeframe to calculate on historical bars.

— Any chart timeframe can be used in realtime mode, but plots that include moving averages in their calculations may require many elapsed realtime bars before they can calculate.

You might prefer drastically reducing the periods of the moving averages, or using the volume columns mode, which displays instant values, instead of the line.

Volume Delta Balances

This indicator uses a variety of methods to evaluate five volume delta balances and derive other values from those balances. The five balances are:

1 — On Bar Balance : This is the only balance using instant values; it is simply the subtraction of the Sell volume from the Buy volume on the bar.

2 — Average Balance : Calculates a distinct EMA for both the Buy and Sell volumes, and subtracts the Sell EMA from the Buy EMA.

3 — Momentum Balance : Starts by calculating, separately for both Buy and Sell volumes, the difference between the same EMAs used in "Average Balance" and

an SMA of double the period used for the "Average Balance" EMAs. The difference for the Sell side is subtracted from the difference for the Buy side,

and an RSI of that value is calculated and brought over the −50/+50 scale.

4 — Relative Balance : The reference values used in the calculation are the Buy and Sell EMAs used in the "Average Balance".

From those, we calculate two intermediate values using how much the instant Buy and Sell volumes on the bar exceed their respective EMA — but with a twist.

If the bar's Buy volume does not exceed the EMA of Buy volume, a zero value is used. The same goes for the Sell volume with the EMA of Sell volume.

Once we have our two intermediate values for the Buy and Sell volumes exceeding their respective MA, we subtract them. The final "Relative Balance" value is an ALMA of that subtraction.

The rationale behind using zero values when the bar's Buy/Sell volume does not exceed its EMA is to only take into account the more significant volume.

If both instant volume values exceed their MA, then the difference between the two is the signal's value.

The signal is called "relative" because the intermediate values are the difference between the instant Buy/Sell volumes and their respective MA.

This balance flatlines when the bar's Buy/Sell volumes do not exceed their EMAs, which makes it useful to spot areas where trader interest dwindles, such as consolidations.

The smaller the period of the final value's ALMA, the more easily you will see the balance flatline. These flat zones should be considered no-trade zones.

5 — Percent Balance : This balance is the ALMA of the ratio of the "On Bar Balance" value, i.e., the volume delta balance on the bar (which can be positive or negative),

over the total volume for that bar.

From the balances and marker conditions, two more values are calculated:

1 — Marker Bias : It sums the up/down (+1/‒1) occurrences of the markers 1 to 4 over a period you define, so it ranges from −4 to +4, times the period.

Its calculation will depend on the modes used to calculate markers 3 and 4.

2 — Combined Balances : This is the sum of the bull/bear (+1/−1) states of each of the five balances, so it ranges from −5 to +5.

█ FEATURES

The indicator has two main modes of operation: Columns and Line .

Columns

• In Columns mode you can display stacked Buy/Sell volume columns.

• The buy section always appears above the centerline, the sell section below.

• The top and bottom sections can be colored independently using eight different methods.

• The EMAs of the Buy/Sell values can be displayed (these are the same EMAs used to calculate the "Average Balance").

Line

• Displays one of seven signals: the five balances or one of two complementary values, i.e., the "Marker Bias" or the "Combined Balances".

• You can color the line and its fill using independent calculation modes to pack more information in the display.

You can thus appraise the state of 3 different values using the line itself, its color and the color of its fill.

• A "Divergence Levels" feature will use the line to automatically draw expanding levels on divergence events.

Default settings

Using the indicator's default settings, this is the information displayed:

• The line is calculated on the "Average Balance".

• The line's color is determined by the bull/bear state of the "Percent Balance".

• The line's fill gradient is determined by the advances/declines of the "Momentum Balance".

• The orange divergence dots are calculated using discrepancies between the polarity of the "On Bar Balance" and the chart's bar.

• The divergence levels are determined using the line's level when a divergence occurs.

• The background's fill gradient is calculated on advances/declines of the "Marker Bias".

• The chart bars are colored using advances/declines of the "Relative Balance". Divergences are shown in orange.

• The intrabar timeframe is automatically determined from the chart's timeframe so that a minimum of 50 intrabars are used to calculate volume delta on historical bars.

Alerts

The configuration of the marker conditions explained further is what determines the conditions that will trigger alerts created from this script. Note that simply selecting the display of markers does not create alerts. To create an alert on this script, you must use ALT-A from the chart. You can create multiple alerts triggering on different conditions from this same script; simply configure the markers so they define the trigger conditions for each alert before creating the alert. The configuration of the script's inputs is saved with the alert, so from then on you can change them without affecting the alert. Alert messages will mention the marker(s) that triggered the specific alert event. Keep in mind, when creating alerts on small chart timeframes, that discrepancies between alert triggers and markers displayed on your chart are to be expected. This is because the alert and your chart are running two distinct instances of the indicator on different servers and different feeds. Also keep in mind that while alerts only trigger on confirmed conditions, they are calculated using realtime calculation mode, which entails that if you refresh your chart and elapsed realtime bars recalculate as historical bars using intrabar inspection, markers will not appear in the same places they appeared in realtime. So it's important to understand that even though the alert conditions are confirmed when they trigger, these alerts will repaint.

Let's go through the sections of the script's inputs.

Columns

The size of the Buy/Sell columns always represents their respective importance on the bar, but the coloring mode for tops and bottoms is independent. The default setup uses a standard coloring mode where the Buy/Sell columns are always in the bull/bear color with a higher intensity for the winning side. Seven other coloring modes allow you to pack more information in the columns. When choosing to color the top columns using a bull/bear gradient on "Average Balance", for example, you will have bull/bear colored tops. In order for the color of the bottom columns to continue to show the instant bar balance, you can then choose the "On Bar Balance — Dual Solid Colors" coloring mode to make those bars the color of the winning side for that bar. You can display the averages of the Buy and Sell columns. If you do, its coloring is controlled through the "Line" and "Line fill" sections below.

Line and Line fill

You can select the calculation mode and the thickness of the line, and independent calculations to determine the line's color and fill.

Zero Line

The zero line can display dots when all five balances are bull/bear.

Divergences

You first select the detection mode. Divergences occur whenever the up/down direction of the signal does not match the up/down polarity of the bar. Divergences are used in three components of the indicator's visuals: the orange dot, colored chart bars, and to calculate the divergence levels on the line. The divergence levels are dynamic levels that automatically build from the line's values on divergence events. On consecutive divergences, the levels will expand, creating a channel. This implementation of the divergence levels corresponds to my view that divergences indicate anomalies, hesitations, points of uncertainty if you will. It precludes any attempt to identify a directional bias to divergences. Accordingly, the levels merely take note of divergence events and mark those points in time with levels. Traders then have a reference point from which they can evaluate further movement. The bull/bear/neutral colors used to plot the levels are also congruent with this view in that they are determined by the line's position relative to the levels, which is how I think divergences can be put to the most effective use. One of the coloring modes for the line's fill uses advances/declines in the line after divergence events.

Background

The background can show a bull/bear gradient on six different calculations. As with other gradients, you can adjust its brightness to make its importance proportional to how you use it in your analysis.

Chart bars

Chart bars can be colored using seven different methods. You have the option of emptying the body of bars where volume does not increase, as does my TLD indicator, and you can choose whether you want to show divergences.

Intrabar Timeframe

This is the intrabar timeframe that will be used to calculate volume delta using intrabar inspection on historical bars. You can choose between four modes. The three "Auto-steps" modes calculate, from the chart's timeframe, the intrabar timeframe where the said number of intrabars will make up the dilation of chart bars. Adjustments are made for non-24x7 markets. "Fixed" mode allows you to select the intrabar timeframe you want. Checking the "Show TF" box will display in the lower-right corner the intrabar timeframe used at any given moment. The proper selection of the intrabar timeframe is important. It must achieve maximal granularity to produce precise results while not unduly slowing down calculations, or worse, causing runtime errors. Note that historical depth will vary with the intrabar timeframe. The smaller the timeframe, the shallower historical plots you will be.

Markers

Markers appear when the required condition has been confirmed on a closed bar. The configuration of the markers when you create an alert is what determines when the alert will trigger. Five markers are available:

• Balances Agreement : All five balances are either bullish or bearish.

• Double Bumps : A double bump is two consecutive up/down bars with +/‒ volume delta, and rising Buy/Sell volume above its average.

• Divergence confirmations : A divergence is confirmed up/down when the chosen balance is up/down on the previous bar when that bar was down/up, and this bar is up/down.

• Balance Shifts : These are bull/bear transitions of the selected signal.

• Marker Bias Shifts : Marker bias shifts occur when it crosses into bull/bear territory.

Periods

Allows control over the periods of the different moving averages used to calculate the balances.

Volume Discrepancies

Stock exchanges do not report the same volume for intraday and daily (or higher) resolutions. Other variations in how volume information is reported can also occur in other markets, namely Forex, where volume irregularities can even occur between different intraday timeframes. This will cause discrepancies between the total volume on the bar at the chart's timeframe, and the total volume calculated by adding the volume of the intrabars in that bar's dilation. This does not necessarily invalidate the volume delta information calculated from intrabars, but it tells us that we are using partial volume data. A mechanism to detect chart vs intrabar timeframe volume discrepancies is provided. It allows you to define a threshold percentage above which the background will indicate a difference has been detected.

Other Settings

You can control here the display of the gray dot reminder on realtime bars, and the display of error messages if you are using a chart timeframe that is not greater than the fixed intrabar timeframe, when you use that mode. Disabling the message can be useful if you only use realtime mode at chart timeframes that do not support intrabar inspection.

█ RAMBLINGS

On Volume Delta

Volume is arguably the best complement to interpret price action, and I consider volume delta to be the most effective way of processing volume information. In periods of low-volatility price consolidations, volume will typically also be lower than normal, but slight imbalances in the trend of the buy/sell volume balance can sometimes help put early odds on the direction of the break from consolidation. Additionally, the progression of the volume imbalance can help determine the proximity of the breakout. I also find volume delta and the number of divergences very useful to evaluate the strength of trends. In trends, I am looking for "slow and steady", i.e., relatively low volatility and pauses where price action doesn't look like world affairs are being reassessed. In my personal mythology, this type of trend is often more resilient than high-volatility breakouts, especially when volume balance confirms the general agreement of traders signaled by the low-volatility usually accompanying this type of trend. The volume action on pauses will often help me decide between aggressively taking profits, tightening a stop or going for a longer-term movement. As for reversals, they generally occur in high-volatility areas where entering trades is more expensive and riskier. While the identification of counter-trend reversals fascinates many traders to no end, they represent poor opportunities in my view. Volume imbalances often precede reversals, but I prefer to use volume delta information to identify the areas following reversals where I can confirm them and make relatively low-cost entries with better odds.

On "Buy/Sell" Volume

Buying or selling volume are misnomers, as every unit of volume transacted is both bought and sold by two different traders. While this does not keep me from using the terms, there is no such thing as “buy only” or “sell only” volume. Trader lingo is riddled with peculiarities.

Divergences

The divergence detection method used here relies on a difference between the direction of a signal and the polarity (up/down) of a chart bar. When using the default "On Bar Balance" to detect divergences, however, only the bar's volume delta is used. You may wonder how there can be divergences between buying/selling volume information and price movement on one bar. This will sometimes be due to the calculation's shortcomings, but divergences may also occur in instances where because of order book structure, it takes less volume to increase the price of an asset than it takes to decrease it. As usual, divergences are points of interest because they reveal imbalances, which may or may not become turning points. To your pattern-hungry brain, the divergences displayed by this indicator will — as they do on other indicators — appear to often indicate turnarounds. My opinion is that reality is generally quite sobering and I have no reliable information that would tend to prove otherwise. Exercise caution when using them. Consequently, I do not share the overwhelming enthusiasm of traders in identifying bullish/bearish divergences. For me, the best course of action when a divergence occurs is to wait and see what happens from there. That is the rationale underlying how my divergence levels work; they take note of a signal's level when a divergence occurs, and it's the signal's behavior from that point on that determines if the post-divergence action is bullish/bearish.

Superfluity

In "The Bed of Procrustes", Nassim Nicholas Taleb writes: To bankrupt a fool, give him information . This indicator can display lots of information. While learning to use a new indicator inevitably requires an adaptation period where we put it through its paces and try out all its options, once you have become used to it and decide to adopt it, rigorously eliminate the components you don't use and configure the remaining ones so their visual prominence reflects their relative importance in your analysis. I tried to provide flexible options for traders to control this indicator's visuals for that exact reason — not for window dressing.

█ LIMITATIONS

• This script uses a special characteristic of the `security()` function allowing the inspection of intrabars — which is not officially supported by TradingView.

It has the advantage of permitting a more robust calculation of volume delta than other methods on historical bars, but also has its limits.

• Intrabar inspection only works on some chart timeframes: 3, 5, 10, 15 and 30 minutes, 1, 2, 3, 4, 6, and 12 hours, 1 day, 1 week and 1 month.

The script’s code can be modified to run on other resolutions.

• When the difference between the chart’s timeframe and the intrabar timeframe is too great, runtime errors will occur. The Auto-Steps selection mechanisms should avoid this.

• All volume is not created equally. Its source, components, quality and reliability will vary considerably with sectors and instruments.

The higher the quality, the more reliably volume delta information can be used to guide your decisions.

You should make it your responsibility to understand the volume information provided in the data feeds you use. It will help you make the most of volume delta.

█ NOTES

For traders

• The Data Window shows key values for the indicator.

• While this indicator displays some of the same information calculated in my Delta Volume Columns ,

I have elected to make it a separate publication so that traders continue to have a simpler alternative available to them. Both code bases will continue to evolve separately.

• All gradients used in this indicator determine their brightness intensities using advances/declines in the signal—not their relative position in a pre-determined scale.

• Volume delta being relative, by nature, it is particularly well-suited to Forex markets, as it filters out quite elegantly the cyclical volume data characterizing the sector.

If you are interested in volume delta, consider having a look at my other "Delta Volume" indicators:

• Delta Volume Realtime Action displays realtime volume delta and tick information on the chart.

• Delta Volume Candles builds volume delta candles on the chart.

• Delta Volume Columns is a simpler version of this indicator.

For coders

• I use the `f_c_gradientRelativePro()` from the PineCoders Color Gradient Framework to build my gradients.

This function has the advantage of allowing begin/end colors for both the bull and bear colors. It also allows us to define the number of steps allowed for each gradient.

I use this to modulate the gradients so they perform optimally on the combination of the signal used to calculate advances/declines,

but also the nature of the visual component the gradient applies to. I use fewer steps for choppy signals and when the gradient is used on discrete visual components

such as volume columns or chart bars.

• I use the PineCoders Coding Conventions for Pine to write my scripts.

• I used functions modified from the PineCoders MTF Selection Framework for the selection of timeframes.

█ THANKS TO:

— The devs from TradingView's Pine and other teams, and the PineCoders who collaborate with them. They are doing amazing work,

and much of what this indicator does could not be done without their recent improvements to Pine.

— A guy called Kuan who commented on a Backtest Rookies presentation of their Volume Profile indicator using a `for` loop.

This indicator started from the intrabar inspection technique illustrated in Kuan's snippet.

— theheirophant , my partner in the exploration of the sometimes weird abysses of `security()`’s behavior at intrabar timeframes.

— midtownsk8rguy , my brilliant companion in mining the depths of Pine graphics.

BERLIN CandlesA problem with Heikin Ashi is that while it gives you a great overview of overall direction, it is rarely possible to use it as a replacement for normal japanese

candlesticks. The reason for this is that actual price data is lost, since the candles are more akin to a moving average than a different way to see price action. Also, with Heikin Ashi, most of the actual price action is lost, because the candles can be bigger than the high and low of the underlying japanese candlestick.

With BERLIN Candles I have tried to fix that problem. By using a smoothed out version of the previous Heikin Ashi candle close as the current BERLIN Candle open, the high and low of the actual japanese candlestick for the high and low of the BERLIN Candle, and the current Heikin Ashi close as the BERLIN Candle close, while setting hard limits for BERLIN Candle open and close values so that they can never exceed the high and low of the underlying japanese candlestick.

One problem still persists though. The actual current price data is lost. However, the BERLIN Candles have solved this by adding a fifth part to the candles. The close of the underlying japanese candlesticks are indicated with a plus-sign. This way, actual price data is never lost, while keeping all of the other benefits of this type of candles.

A few added bonuses:

The addition of the 14 period ATR at the latest candle

The baseline from Ichimoku is included as an option

The 14 period ATR value of each candle can be seen in the indicator data as

the orange value

Support Resistance ChannelsHello All,

For Long time I was planning to make Support/Resistance Channels script, finally I had time and here it is.

How this script works?

- it finds and keeps Pivot Points

- when it found a new Pivot Point it clears older S/R channels then;

- for each pivot point it searches all pivot points in its own channel with dynamic width

- while creating the S/R channel it calculates its strength

- then sorts all S/R channels by strength

- it shows the strongest S/R channels, before doing this it checks old location in the list and adjust them for better visibility

- if any S/R channel was broken on last move then it gives alert and put shape below/above the candle

- The colors of the S/R channels are adjusted automatically

You can set/change following settings:

- Pivot Period

- Source : High/Low or Close/Open can be used

- Maximum Channel Width %: this is the maximum channel width rate, this is calculated using Highest/Lowest levels in last 300 bars

- Number of S/R to show : this is the number of Strongest S/R to show

- Loopback Period: While calculating S/R levels it checks Pivot Points in LoopBack Period

- Show S/R on last # Bars: To see S/R levels only on last N bars

- Start Date: the script starts calculating Pivot Point from this date, the reason I put this option is for visuality. Explained below

- You can set colors/transparency

- and You can enable/disable shapes for broken S/R levels

Examples:

You can change colors as you wish:

here " Show S/R on last # Bars " set 100:

Sometimes visuality may corrupt because of old S/R levels, to solve it you need to set "Start Date" in the options to start the script in visual part (last 292 bars)

here in first screenshot it doesn't look good (shrink), then on second screenshot I set the "Start Date" it looks better, if you change time frame don't forget to set it again :)

Enjoy!

MathSpecialFunctionsConvolve1DLibrary "MathSpecialFunctionsConvolve1D"

Convolution is one of the most important mathematical operations used in signal processing. This simple mathematical operation pops up in many scientific and industrial applications, from its use in a billion-layer large CNN to simple image denoising.

___

Reference:

www.algorithm-archive.org

numpy.org

lloydrochester.com

www.geeksforgeeks.org

f(signal, filter)

Convolve

Parameters:

signal (array) : List with signal data.

filter (array) : List with weights to apply to the signal data.

Returns: Discrete, linear convolution of `signal` and `filter`.

ErrorFunctionsLibrary "ErrorFunctions"

A collection of functions used to approximate the area beneath a Gaussian curve.

Because an ERF (Error Function) is an integral, there is no closed-form solution to calculating the area beneath the curve. Meaning all ERFs are approximations; precisely wrong, but mostly accurate. How close you need to get to the actual area depends entirely on your use case, with more precision being less efficient.

The internal precision of floats in Pine Script is 1e-16 (16 decimals, aka. double precision). This library adapts well known algorithms designed to efficiently reach double precision. Single precision alternates are also included. All of them were made free to use, modify, and distribute by their original authors.

HASTINGS

Adaptation of a single precision ERF by Cecil Hastings Jr, published through Princeton University in 1955. It was later documented by Abramowitz and Stegun as equation 7.1.26 in their 1972 Handbook of Mathematical Functions. Fast, efficient, and ideal when precision beyond a few decimals is unnecessary.

GILES

Adaptation of a single precision Inverse ERF by Michael Giles, published through the University of Oxford in 2012. It reverses the ERF, estimating an X coordinate from an area. It too is fast, efficient, and ideal when precision beyond a few decimals is unnecessary.

LIBC

Adaptation of the double precision ERF & ERFC in the standard C library (aka. libc). It is also the same ERF & ERFC that SciPy uses. While not quite as efficient as the Hastings approximation, it's still very fast and fully maximizes Pines precision.

BOOST

Adaptation of the double precision Inverse ERF & Inverse ERFC in the Boost Math C++ library. SciPy uses these as well. These reverse the ERF & ERFC, estimating an X coordinate from an area. It too isn't quite as efficient as the Giles approximation, but still fast and fully maximizes Pines precision.

While these algorithms are not exported directly, they are available through their exported counterparts.

- - -

ERROR FUNCTIONS

erf(x, precise)

An Error Function estimates the theoretical error of a measurement.

Parameters:

x (float) : (float) Upper limit of the integration.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between -1 and 1.

erfc(x, precise)

A Complementary Error Function estimates the difference between a theoretical error and infinity.

Parameters:

x (float) : (float) Lower limit of the integration.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and 2.

erfinv(x, precise)

An Inverse Error Function reverses the erf() by estimating the original measurement from the theoretical error.

Parameters:

x (float) : (float) Theoretical error.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and ± infinity.

erfcinv(x, precise)

An Inverse Complementary Error Function reverses the erfc() by estimating the original measurement from the difference between the theoretical error and infinity.

Parameters:

x (float) : (float) Difference between the theoretical error and infinity.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and ± infinity.

- - -

DISTRIBUTION FUNCTIONS

pdf(x, m, s)

A Probability Density Function estimates the probability density . For clarity, density is not a probability .

Parameters:

x (float) : (float) X coordinate for which a density will be estimated.

m (float) : (float) Mean

s (float) : (float) Sigma

Returns: (float) Between 0 and ∞.

cdf(z, precise)

A Cumulative Distribution Function estimates the area under a Gaussian curve between negative infinity and the Z Score.

Parameters:

z (float) : (float) Z Score.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and 1.

cdfinv(a, precise)

An Inverse Cumulative Distribution Function reverses the cdf() by estimating the Z Score from an area.

Parameters:

a (float) : (float) Area between 0 and 1.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between -∞ and +∞

cdfab(z1, z2, precise)

A Cumulative Distribution Function from A to B estimates the area under a Gaussian curve between two Z Scores (A and B).

Parameters:

z1 (float) : (float) First Z Score.

z2 (float) : (float) Second Z Score.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and 1.

ttt(z, precise)

A Two-Tailed Test estimates the area under a Gaussian curve between symmetrical ± Z scores and ± infinity.

Parameters:

z (float) : (float) One of the symmetrical Z Scores.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and 1.

tttinv(a, precise)

An Inverse Two-Tailed Test reverses the ttt() by estimating the absolute Z Score from an area.

Parameters:

a (float) : (float) Area between 0 and 1.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and ∞.

ott(z, precise)

A One-Tailed Test estimates the area under a Gaussian curve between an absolute Z Score and infinity.

Parameters:

z (float) : (float) Z Score.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and 1.

ottinv(a, precise)

An Inverse One-Tailed Test Reverses the ott() by estimating the Z Score from a an area.

Parameters:

a (float) : (float) Area between 0 and 1.

precise (bool) : Double precision (true) or single precision (false).

Returns: (float) Between 0 and ∞.

Trend Volatility Index (TVI)Trend Volatility Index (TVI)

A robust nonparametric oscillator for structural trend volatility detection

⸻

What is this?

TVI is a volatility oscillator designed to measure the strength and emergence of price trends using nonparametric statistics.

It calculates a U-statistic based on the Gini mean difference across multiple simple moving averages.

This allows for objective, robust, and unbiased quantification of trend volatility in tick-scale values.

⸻

What can it do?

• Quantify trend strength as a continuous value aligned with tick price scale

• Detect trend breakouts and volatility expansions

• Identify range-bound market states

• Detect early signs of new trends with minimal lag

⸻

What can’t it do?

• Predict future price levels

• Predict trend direction before confirmation

⸻

How it works

TVI computes a nonparametric dispersion metric (Gini mean difference) from multiple SMAs of different lengths.

As this metric shares the same dimension as price ticks, it can be directly interpreted on the chart as a volatility gauge.

The output is plotted using candlestick-style charts to enhance visibility of change rate and trend behavior.

⸻

Disclaimer

TVI does not predict price. It is a structural indicator designed to support discretionary judgment.

Trading carries inherent risk, and this tool does not guarantee profitability. Use at your own discretion.

⸻

Innovation

This indicator introduces a novel approach to trend volatility by applying U-statistics over time series

to produce a nonparametric, unbiased, and robust estimate of structural volatility.

日本語要約

Trend Volatility Index (TVI) は、ノンパラメトリックなU統計量(Gini平均差)を使ってトレンドの強度を客観的に測定することを目的に開発されたボラティリティ・オシレーターです。

ティック単位で連続的に変化し、トレンドのブレイク・レンジ・初動の予兆を定量的に検出します。

未来の価格や方向は予測せず、現在の構造的ばらつきだけをロバストに評価します。

Cointegration Heatmap & Spread Table [EdgeTerminal]The Cointegration Heatmap is a powerful visual and quantitative tool designed to uncover deep, statistically meaningful relationships between assets.

Unlike traditional indicators that react to price movement, this tool analyzes the underlying statistical relationship between two time series and tracks when they diverge from their long-term equilibrium — offering actionable signals for mean-reversion trades .

What Is Cointegration?

Most traders are familiar with correlation, which measures how two assets move together in the short term. But correlation is shallow — it doesn’t imply a stable or predictable relationship over time.

Cointegration, however, is a deeper statistical concept: Two assets are cointegrated if a linear combination of their prices or returns is stationary , even if the individual series themselves are non-stationary.

Cointegration is a foundational concept in time series analysis, widely used by hedge funds, proprietary trading firms, and quantitative researchers. This indicator brings that institutional-grade concept into an easy-to-use and fully visual TradingView indicator.

This tool helps answer key questions like:

“Which stocks tend to move in sync over the long term?”

“When are two assets diverging beyond statistical norms?”

“Is now the right time to short one and long the other?”

Using a combination of regression analysis, residual modeling, and Z-score evaluation, this indicator surfaces opportunities where price relationships are stretched and likely to snap back — making it ideal for building low-risk, high-probability trade setups.

In simple terms:

Cointegrated assets drift apart temporarily, but always come back together over time. This behavior is the foundation of successful pairs trading.

How the Indicator Works

Cointegration Heatmap indicator works across any market supported on TradingView — from stocks and ETFs to cryptocurrencies and forex pairs.

You enter your list of symbols, choose a timeframe, and the indicator updates every bar with live cointegration scores, spread signals, and trade-ready insights.

Indicator Settings:

Symbol list: a customizable list of symbols separated by commas

Returns timeframe: time frame selection for return sampling (Weekly or Monthly)

Max periods: max periods to limit the data to a certain time and to control indicator performance

This indicator accomplishes three major goals in one streamlined package:

Identifies stable long-term relationships (cointegration) between assets, using a heatmap visualization.

Tracks the spread — the difference between actual prices and the predicted linear relationship — between each pair.

Generates trade signals based on Z-score deviations from the mean spread, helping traders know when a pair is statistically overextended and likely to mean revert.

The math:

Returns are calculated using spread tickers to ensure alignment in time and adjust for dividends, splits, and other inconsistencies.

For each unique pair of symbols, we perform a linear regression

Yt=α+βXt+ε

Then we compute the residuals (errors from the regression):

Spreadt=Yt−(α+βXt)

Calculate the standard deviation of the spread over a moving window (default: 100 samples) and finally, define the Cointegration Score:

S=1/Standard Deviation of Residuals

This means, the lower the deviation, the tighter the relationship, so higher scores indicate stronger cointegration.

Always remember that cointegration can break down so monitor the asset over time and over multiple different timeframes before making a decision.

How to use the indicator

The heatmap table:

The indicator displays 2 very important tables, one in the middle and one on the right side. After entering your symbols, the first table to pay attention to is the middle heatmap table.

Any assets with a cointegration value of 25% is something to pay attention to and have a strong and stable relationship. Anything below is weak and not tradable.

Additionally, the 40% level is another important line to cross. Assets that have a cointegration score of over 40% will most likely have an extremely strong relationship.

Think about it this way, the higher the percentage, the tighter and more statistically reliable the relationship is.

The spread table:

After finding a good asset pair using heatmap, locate the same pair in the spread table (right side).

Here’s what you’ll see on the table:

Spread: Current difference between the two symbols based on the regression fit

Mean: Historical average of that spread

Z-score: How far current spread is from the mean in standard deviations

Signal: Trade suggestion: Short, Long, or Neutral

Since you’re expecting mean reversion, the idea is that the spread will return to the average. You want to take a trade when the z-score is either over +2 or below -2 and exit when z-score returns to near 0.

You will usually see the trade suggestion on the spread chart but you can make your own decision based on your risk level.

Keep in mind that the Z-score for each pair refers to how off the first asset is from the mean compared to the second one, so for example if you see STOCKA vs STOCKB with a Z-score of -1.55, we are regressing STOCKB (Y) on STOCKA (X).

In this case, STOCKB is the quoted asset and STOCKA is the base asset.

In this case, this means that STOCKB is much lower than expected relative to STOCKA, so the trade would be a long position on stock B and short position on stock A.

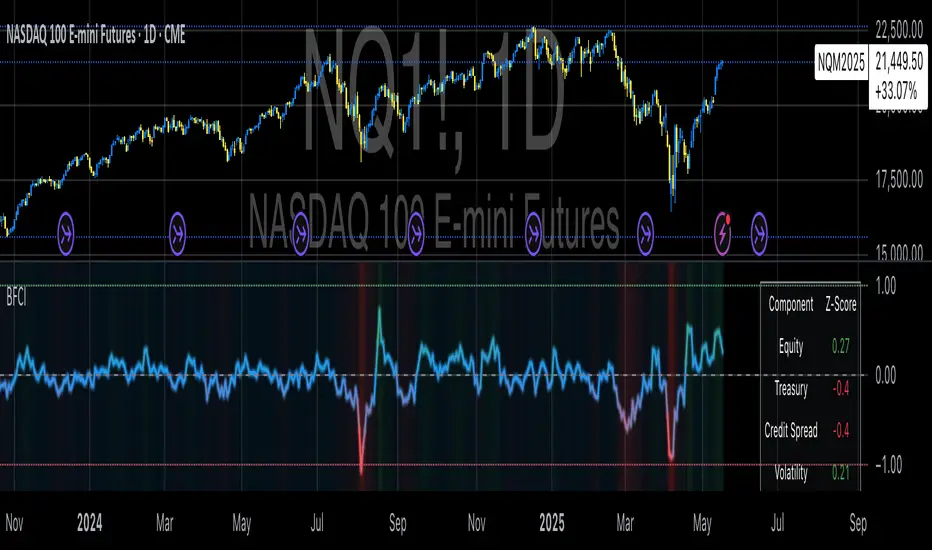

Bloomberg Financial Conditions Index (Proxy)The Bloomberg Financial Conditions Index (BFCI): A Proxy Implementation

Financial conditions indices (FCIs) have become essential tools for economists, policymakers, and market participants seeking to quantify and monitor the overall state of financial markets. Among these measures, the Bloomberg Financial Conditions Index (BFCI) has emerged as a particularly influential metric. Originally developed by Bloomberg L.P., the BFCI provides a comprehensive assessment of stress or ease in financial markets by aggregating various market-based indicators into a single, standardized value (Hatzius et al., 2010).

The original Bloomberg Financial Conditions Index synthesizes approximately 50 different financial market variables, including money market indicators, bond market spreads, equity market valuations, and volatility measures. These variables are normalized using a Z-score methodology, weighted according to their relative importance to overall financial conditions, and then aggregated to produce a composite index (Carlson et al., 2014). The resulting measure is centered around zero, with positive values indicating accommodative financial conditions and negative values representing tighter conditions relative to historical norms.

As Angelopoulou et al. (2014) note, financial conditions indices like the BFCI serve as forward-looking indicators that can signal potential economic developments before they manifest in traditional macroeconomic data. Research by Adrian et al. (2019) demonstrates that deteriorating financial conditions, as measured by indices such as the BFCI, often precede economic downturns by several months, making these indices valuable tools for predicting changes in economic activity.

Proxy Implementation Approach

The implementation presented in this Pine Script indicator represents a proxy of the original Bloomberg Financial Conditions Index, attempting to capture its essential features while acknowledging several significant constraints. Most critically, while the original BFCI incorporates approximately 50 financial variables, this proxy version utilizes only six key market components due to data accessibility limitations within the TradingView platform.

These components include:

Equity market performance (using SPY as a proxy for S&P 500)

Bond market yields (using TLT as a proxy for 20+ year Treasury yields)

Credit spreads (using the ratio between LQD and HYG as a proxy for investment-grade to high-yield spreads)

Market volatility (using VIX directly)

Short-term liquidity conditions (using SHY relative to equity prices as a proxy)

Each component is transformed into a Z-score based on log returns, weighted according to approximated importance (with weights derived from literature on financial conditions indices by Brave and Butters, 2011), and aggregated into a composite measure.

Differences from the Original BFCI

The methodology employed in this proxy differs from the original BFCI in several important ways. First, the variable selection is necessarily limited compared to Bloomberg's comprehensive approach. Second, the proxy relies on ETFs and publicly available indices rather than direct market rates and spreads used in the original. Third, the weighting scheme, while informed by academic literature, is simplified compared to Bloomberg's proprietary methodology, which may employ more sophisticated statistical techniques such as principal component analysis (Kliesen et al., 2012).

These differences mean that while the proxy BFCI captures the general direction and magnitude of financial conditions, it may not perfectly replicate the precision or sensitivity of the original index. As Aramonte et al. (2013) suggest, simplified proxies of financial conditions indices typically capture broad movements in financial conditions but may miss nuanced shifts in specific market segments that more comprehensive indices detect.

Practical Applications and Limitations

Despite these limitations, research by Arregui et al. (2018) indicates that even simplified financial conditions indices constructed from a limited set of variables can provide valuable signals about market stress and future economic activity. The proxy BFCI implemented here still offers significant insight into the relative ease or tightness of financial conditions, particularly during periods of market stress when correlations among financial variables tend to increase (Rey, 2015).

In practical applications, users should interpret this proxy BFCI as a directional indicator rather than an exact replication of Bloomberg's proprietary index. When the index moves substantially into negative territory, it suggests deteriorating financial conditions that may precede economic weakness. Conversely, strongly positive readings indicate unusually accommodative financial conditions that might support economic expansion but potentially also signal excessive risk-taking behavior in markets (López-Salido et al., 2017).

The visual implementation employs a color gradient system that enhances interpretation, with blue representing neutral conditions, green indicating accommodative conditions, and red signaling tightening conditions—a design choice informed by research on optimal data visualization in financial contexts (Few, 2009).

References

Adrian, T., Boyarchenko, N. and Giannone, D. (2019) 'Vulnerable Growth', American Economic Review, 109(4), pp. 1263-1289.

Angelopoulou, E., Balfoussia, H. and Gibson, H. (2014) 'Building a financial conditions index for the euro area and selected euro area countries: what does it tell us about the crisis?', Economic Modelling, 38, pp. 392-403.

Aramonte, S., Rosen, S. and Schindler, J. (2013) 'Assessing and Combining Financial Conditions Indexes', Finance and Economics Discussion Series, Federal Reserve Board, Washington, D.C.

Arregui, N., Elekdag, S., Gelos, G., Lafarguette, R. and Seneviratne, D. (2018) 'Can Countries Manage Their Financial Conditions Amid Globalization?', IMF Working Paper No. 18/15.

Brave, S. and Butters, R. (2011) 'Monitoring financial stability: A financial conditions index approach', Economic Perspectives, Federal Reserve Bank of Chicago, 35(1), pp. 22-43.

Carlson, M., Lewis, K. and Nelson, W. (2014) 'Using policy intervention to identify financial stress', International Journal of Finance & Economics, 19(1), pp. 59-72.

Few, S. (2009) Now You See It: Simple Visualization Techniques for Quantitative Analysis. Analytics Press, Oakland, CA.