Hybrid Linear Regression Channel with Fibonacci LevelsHow to Use the LRC Fib Hybrid Indicator (Detailed Guide)

1. Read the Trend

2.The thick blue line is the linear regression midline.

If it’s sloping upward → uptrend (favor longs).

If sloping downward → downtrend (favor shorts).

The gray channel bounds are ±2 standard deviations (adjustable).

3. Understand Fibonacci Levels

Fib lines are projected parallel to the regression slope using the channel width as 100%:

Red dashed lines (0.0 to 0.786): Support zones in uptrends.

Blue dashed line (0.5): Midline/neutral.

Green dashed lines (1.0 to 2.618): Resistance zones in downtrends.

Strongest levels: 0.618 (support) and 1.618 (resistance).

4. Buy Signal (Long Entry)

Triggered when:

Midline is rising (uptrend confirmed).

Price crosses above a red Fib level (0.0–0.786).

Volume > 20-period average (if confirmation enabled).

Action:

Enter long on the green triangle (▲).

Stop Loss: Below the lower gray channel or recent swing low.

Take Profit: At 1.0, 1.272, or 1.618 green Fibs.

5. Sell Signal (Short Entry)

Triggered when:

Midline is falling (downtrend).

Price crosses below a green Fib level (1.272–2.618).

Volume > average.

Action:

Enter short on the red triangle (▼).

Stop Loss: Above the upper gray channel.

Take Profit: At 1.0, 0.786, or 0.618 red Fibs.

6. Use the Info Table (Bottom-Right)

Shows live prices of all Fib levels, current trend ("Up"/"Down"), and signal status ("BUY"/"SELL"/"None").

7. Customize via Settings (Gear Icon)

Regression Length: 50–200 (shorter = faster response).

Std Dev Multiplier: 1.5–3.0 (tighter/wider channel).

Toggle Fibs: Hide unused levels to declutter.

Volume Confirmation: Turn off for pure price action.

8. Set Alerts

Right-click chart → Add Alert → Select "Buy Signal" or "Sell Signal" → Enable popup/email/webhook.

9. Best Practices

Best in trending markets (avoid chop).

Wait for volume spike on bounce.

Combine with higher timeframe bias.

Use 0.618/1.618 as primary reversal zones.

This indicator gives you adaptive trend, precise entries, volume filter, and dynamic targets — all in one clean overlay.

Forecasting

Predicta Futures – Scalping Predictor with Confidence FilterPredicta Futures is an advanced short-term forecasting indicator that combines historical pattern similarity analysis with weighted technical signals to predict price movements 1–10 minutes ahead.

**Core Functionality**

The script scans up to 5,000 historical bars to identify structurally similar price patterns. It aggregates forward outcomes from matched patterns and integrates real-time signals from RSI, MACD, Bollinger Bands, volume momentum, and volatility. A composite confidence score filters signals, displaying only those meeting the user-defined threshold (default ≥68%).

**Key Outputs**

- Buy/sell triangles with text labels

- Dashed projection line to predicted price

- Dotted target and ATR-based stop lines

- Info panel showing forecast direction, confidence %, expected move %, pattern count, order book status, and data access details

**Customization & Performance**

- Execution modes: Fast, Balanced, Accurate

- Adaptive sampling with recency bias option

- Filters for volatility and market hours

- Adjustable weights, lookback period, and prediction horizon

**Use Cases**

Scalping, intraday trading, futures, cryptocurrencies, equities.

*Order book metrics are simulated (platform limitation). Technical analysis tool; not financial advice.*

PDH PDL Open ClosePDH/PDL/Open/Close Levels Indicator

Overview

This Pine Script indicator plots the Previous Day High (PDH), Previous Day Low (PDL), Previous Day Open (PDO), and Previous Day Close (PDC) levels on your chart. It's designed for traders who rely on key daily levels to identify potential support, resistance, and intraday reference points. The indicator supports multiple timeframes, allowing you to visualize these levels from higher timeframes (e.g., weekly or monthly) directly on lower timeframe charts.

Built with Pine Script v6, it's lightweight, customizable, and overlays seamlessly on any symbol. Lines extend slightly into the future for better visibility, and labels provide clear identification with price values.

Key Features

- Multi-Timeframe Support: Choose from predefined timeframes (5m to 1M) via the input settings to fetch and plot levels from the selected period.

- Clean Visualization:

- PDH and PDL: Solid black lines for high/low levels.

- PDO: Dotted blue line for the opening price.

- PDC: Dotted red line for the closing price.

- Dynamic Labels: Automatically placed at the end of each line, showing the timeframe and exact price (e.g., "1D High: 150.25").

- Efficient Updates: Lines and labels update in real-time without cluttering the chart—old elements are automatically cleaned up.

- Extension Handling: Lines extend 2 bars ahead by default, adjustable if needed via code modifications.

How to Use

1. Add to Chart**: Copy the script into TradingView's Pine Editor, save, and add it to your chart.

2. Customize Timeframe: In the indicator settings, select your desired timeframe (default: 1D). This pulls levels from the previous period of that timeframe.

3. Interpret Levels:

- Use PDH/PDL as potential resistance/support zones.

- PDO/PDC can highlight session biases (e.g., gap fills or continuation patterns).

- Ideal for day trading, swing setups, or aligning with higher timeframe context.

4. Best Practices: Works on any market (stocks, forex, crypto). Combine with volume or momentum indicators for confluence.

Settings

- Timeframe: Dropdown with options: 5m, 10m, 15m, 30m, 45m, 1H, 2H, 3H, 4H, 1D, 1W, 1M.

- No other inputs for simplicity—colors, styles, and extensions are hardcoded for a clean default look. Edit the script to tweak (e.g., line colors or extension length).

Liquidity Regime OscillatorThe Liquidity Signal Line is a macro-driven confirmation tool designed to capture the underlying global liquidity regime in a single, smoothed oscillator. It measures the combined directional flow of monetary and financial conditions using high-impact macro data: Federal Reserve assets (WALCL), Treasury General Account (TGA), and the Overnight Reverse Repo facility (RRP) – adjusted by key market proxies such as the U.S. Dollar Index, credit spreads (HYG/LQD), and equity risk appetite (SPHB/SPHQ). These components are normalized, weighted, and then double-smoothed into a stable signal that translates complex liquidity dynamics into a simple 0–100 scale.

Liquidity expansion provides fuel for risk assets, while contraction drains leverage and risk appetite. The Signal Line acts as a confirmation overlay for trend and allocation strategies, showing whether systemic liquidity is broadly supportive or restrictive. Readings above 50 indicate an expansionary environment (risk-on bias), below 50 a contractionary one (risk-off bias). Because the calculation uses higher-timeframe macro data, it can be displayed on any chart to give traders a consistent, regime-aware signal that bridges macro policy and technical execution.

Geometric Price-Time Triangle Calculator═══════════════════════════════════════════════════

GEOMETRIC PRICE-TIME TRIANGLE CALCULATOR

═══════════════════════════════════════════════════

Calculates Point C of a geometric triangle using different rotation angles from any selected price swing. Based on Bradley F. Cowan's Price-Time Vector (PTV) methods from "Four-Dimensional Stock Market Structures and Cycles."

📐 WHAT IT DOES

────────────────────────────────────────────────────

Select two points (A and B) on any swing, choose an angle, and the indicator calculates where Point C would be mathematically. It's just vector rotation applied to price charts.

This shows you where Point C lands in both price AND time based on pure geometry - not a prediction, just a calculation.

🎯 FEATURES

────────────────────────────────────────────────────

✓ 10 Different Angles

• Gann ratios: 18.435° (1x3), 26.565° (1x2), 45° (1x1), 63.435° (2x1), 71.565° (3x1)

• Other angles: 30°, 60°, 90°, 120°, 150°

✓ Visual Triangle

• Adjustable colors and opacity for points A, B, C

• Line styles: Solid, Dashed, Dotted

• Extend lines: None, Left, Right, Both

✓ Crosshair at Point C

• Shows where Point C is located

• Vertical line = bar position

• Horizontal line = price level

✓ Data Table

• Shows all calculations

• Price-to-Bar ratio

• Point C location (price and bars from A/B)

• Toggle on/off

🔧 HOW TO USE

────────────────────────────────────────────────────

1. Pick your swing start date (Point A)

2. Pick your swing end date (Point B) - make sure these dates capture the actual high/low of your swing

3. Choose an angle from the dropdown

4. Look at Point C - that's where the geometry puts it

Different angles = different Point C locations. Whether price actually goes there is up to the market.

📊 THE ANGLES

────────────────────────────────────────────────────

- 18.435° (1x3) - Shallow rotation

- 26.565° (1x2) - Moderate rotation

- 45° (1x1) - Gann's balanced ratio

- 60° - Equilateral triangle (default)

- 63.435° (2x1) - Steeper rotation

- 71.565° (3x1) - Very steep rotation

- 90° - Right angle

- 120°-150° - Obtuse angles

💡 PRACTICAL USE

────────────────────────────────────────────────────

→ See where geometric patterns would complete

→ Test if your market respects certain angles

→ Find where multiple angles converge

→ Compare projected Point C to actual price action

→ Use 90° to see symmetrical price/time relationships

→ Backtest historical swings to see what worked

⚙️ HOW IT WORKS

────────────────────────────────────────────────────

1. Takes your AB swing

2. Calculates the BA vector (reverse direction)

3. Normalizes price and time using Price-to-Bar ratio

4. Rotates the vector by your selected angle

5. Converts back to chart coordinates

Basic trigonometry. That's all it is.

📚 BACKGROUND

────────────────────────────────────────────────────

Based on Bradley F. Cowan's Price-Time Vector (PTV) concept from "Four-Dimensional Stock Market Structures and Cycles" and W.D. Gann's geometric angle analysis. Cowan observed that markets sometimes complete geometric patterns. This tool calculates where those patterns would complete mathematically. Whether price actually respects these geometric relationships is something you need to test yourself.

⚠️ IMPORTANT

────────────────────────────────────────────────────

- This is geometric calculation, not prediction

- Point C shows where the math puts it, not where price will go

- Some angles might work for your market, some won't

- Test it yourself on historical data

- Price-to-Bar Ratio stays constant regardless of angle

- Don't trade based on this alone

- Works on all timeframes and assets

🎨 CUSTOMIZATION

────────────────────────────────────────────────────

- Show/hide triangle

- Individual colors for A, B, C points

- Adjust opacity (0-100)

- Line styles for each triangle side

- Extend lines left/right/both/none

- Show/hide data table

- Crosshair color and width

- Customizable table colors

═══════════════════════════════════════════════════

Local Hurst Slope [Dynamic Regime]1. HOW THE INDICATOR WORKS (Math → Market Edge)Step

Math

Market Intuition

1. Log-Returns

r_t = log(P_t / P_{t-1})

Removes scale, makes series stationary

2. R/S per τ

R = max(cum_dev) - min(cum_dev)

S = stdev(segment)

Measures memory strength over window τ

3. H(τ) = log(R/S) / log(τ)

Di Matteo (2007)

H > 0.5 → Trend memory

H < 0.5 → Mean-reversion

4. Slope = dH/d(log τ)

Linear regression of H vs log(τ)

Slope > 0.12 → Trend accelerating

Slope < -0.08 → Reversion emerging

LEADING EDGE: The slope changes 3–20 bars BEFORE price confirms

→ You enter before the crowd, exit before the trap

Slope > +0.12 + Strong Trend = Bullish = Long

Slope +0.05 to +0.12 = Weak Trend = Cautious = Hold/Trail

Slope -0.05 to +0.05 = Random = No Edge

Slope-0.08 to -0.05 = Weak Reversion = Bearish setup = Prepare Short

Slope < -0.08 = Strong Reversion = Bearish= Short

PRO TIPS

Only trade in direction of 200-day SMA

Filters false signals

Avoid trading 3 days before/after earnings

Volatility kills edge

Use on ETFs (SPY, QQQ)

Cleaner than single stocks

Combine with RSI(14)

RSI < 30 + Hurst short = nuclear reversal

Low and Preceding High (Breakout + Bullis fgv + Extending Fib)🚀 Last Low & Preceding High: Bullish Reversal Strategy

This indicator identifies high-probability long setups by confirming a Bullish Market Structure Shift (BMS) coupled with a strong momentum filter.

🧠 Indicator Logic (How It Works)

The core function of this tool is to automatically locate the key structural points that lead to a bullish bias:

Structure Identification: It first defines a Range between the two most recent Pivot Lows. Within this range, it finds the Preceding High (the highest close before the current low) and the true Low Anchor (the lowest low/tail of the pivot low).

Breakout and Momentum Filter: A valid signal requires two conditions to be met on the current bar:

Bullish Breakout: The price must close above the Preceding High.

Marubozu Confirmation: A strong Bullish Marubozu candle (minimal wicks) must be present in the impulse move from the low, filtering for institutional strength.

Fibonacci Discount Zones: Upon confirmation, the indicator calculates and plots the discount zones (0.50, 0.618, 0.786) using the true extremes (tail-to-tail anchors). These zones start extending from the breakout candle and represent high-value areas for potential entries.

🎯 Entry and Risk Management

The strategy provides clear rules for execution once the logic is confirmed:

Entry Execution:

Wait for Retracement: Enter a Long position when the price retraces back into the colored Discount Zones (0.50 to 0.786).

Risk Control:

🛑 Stop Loss (SL): Placed below the Low Line (the swing low that initiated the move).

✅ Take Profit (TP): Placed above the High Line (the high that was broken).

Final note

"Special thanks to Mr. Mazen (@dr0chart) for developing this strategy."

Simulated Fear & Greed (CNN-calibrated v2)🧭 Fear & Greed Index — TradingView Version (Simulated CNN Model)

🔍 Purpose

The Fear & Greed Index is a sentiment indicator that quantifies market emotion on a scale from 0 to 100, where:

0 represents Extreme Fear (capitulation, oversold conditions), and

100 represents Extreme Greed (euphoria, overbought conditions).

It helps traders assess whether the market is driven by fear (risk aversion) or greed (risk appetite) — giving a high-level view of potential turning points in market sentiment.

⚙️ How It Works in TradingView

Because TradingView cannot directly access CNN’s or alternative external sentiment feeds, this indicator simulates the Fear & Greed Index by analyzing in-chart technical data that reflect investor psychology.

It uses a multi-factor model, converting price and volume signals into a composite sentiment score.

🧩 Components Used (Simulated Metrics)

Category Metric Emotional Interpretation

Volatility ATR (Average True Range) High ATR = Fear, Low ATR = Greed

Momentum RSI + MACD Histogram Rising momentum = Greed, Falling = Fear

Volume Activity Volume Z-Score High positive deviation = Greed, Low = Fear

Trend Context SMA Regime Bias (50/200) Downtrend adds Fear penalty, Uptrend supports Greed

These elements are normalized into a 0–100 scale using percentile ranks (like statistical scoring) and then combined using user-adjustable weights.

⚖️ CNN-Style Calibration

The script follows CNN’s five sentiment bands for clarity:

Range Zone Colour Description

0–25 Extreme Fear 🔴 Red Panic, forced selling, capitulation risk

25–45 Fear 🟠 Orange Uncertainty, hesitation, early accumulation phase

45–55 Neutral ⚪ Gray Balanced sentiment, indecision

55–75 Greed 🟢 Light Green Optimism, trend continuation

75–100 Extreme Greed 💚 Bright Green Euphoria, risk of reversal

This structure aligns visually with CNN’s public gauge, making it easy to interpret.

Earnings CountdownAdd to a chart to show a text box with how long to next earnings.

Being updated to add functionality from original open source Pine script

Roboquant RP Profits NY Open Retest StrategyRoboquant RP Profits NY Open Retest Strategy A good strategy for CL

Volumatic VIDYA – Pro+1. Professional & Clear (recommended for TradingView)

Volumatic VIDYA Pro+ combines a dynamic VIDYA trend filter, Delta Volume pressure, and automatic pattern recognition (Double/Triple Tops & Bottoms, Head & Shoulders).

A complete technical tool for detecting momentum shifts, trend reversals, and trade entries across multiple timeframes.

2. Short & Catchy

Adaptive VIDYA trendline + Delta Volume + Pattern detection in one tool.

Instantly visualize market bias, structure, and momentum strength.

3. Educational / Analytical

Analyze market dynamics with VIDYA-based trend filtering, volume delta analysis, and automated pattern recognition.

Ideal for traders who combine price action with quantitative confirmation.

[KF] Multi-Duration Rate Expectations IndicatorAfter last fed cut in Oct then following jump in rates, I was frustrated at not having access to good rate expectations vs actual because the market usually prices in prior to fed action. This indicator was developed to make futures market rate expectations accessible and interpretable without requiring professional bond analytics systems.

Summary

This Pine Script indicator reveals what the futures market expects for interest rates across three key durations: Fed Funds (overnight), 2-Year, and 10-Year Treasury yields. By comparing futures-implied rates against current spot yields, it provides a clear visual signal of whether the market expects rates to rise, fall, or remain steady.

Understanding Rate Futures

Fed Funds futures (ZQ1!) use a simple design where the expected rate equals 100 minus the futures price. If ZQ1! trades at 96.12, the market expects a 3.88% Fed Funds rate. Treasury futures work differently - they trade as bond prices (typically 102-115) that move inversely to yields. Converting Treasury futures to implied yields requires complex bond mathematics involving duration and conversion factors.

This indicator solves the Treasury futures complexity by implementing a self-calibrating sensitivity model. It observes the historical relationship between futures prices and yields, then uses this to project rate expectations. The model also compares front-month to next-month contracts to detect expected rate direction, automatically adapting as market conditions change.

How to Use

Add the indicator to any chart and select your desired duration in the settings. The display shows the futures-implied rate, current yield, and the difference between them. Green indicates the market expects higher rates, red means lower expectations, and gray shows expectations in line with current rates.

The indicator excels at identifying divergences between market expectations and current rates, which often precede rate movements or futures repricing. Comparing expectations across different durations reveals insights about yield curve positioning and Fed policy anticipation.

Technical Note

While Fed Funds futures provide exact rate expectations, Treasury futures conversions are sophisticated approximations that provide reliable directional signals and reasonable magnitude estimates sufficient for most trading applications.

High and low statisticsHigh/Low Pattern Analyzer (All Timeframes)

Ever wonder if there's a hidden pattern in the market?

Does the high of the week usually happen on a Tuesday?

Does the low of the month always form in the first week?

Which 15-minute candle really sets the high for the entire day?

This indicator is a powerful statistical tool designed to answer these questions by analyzing historical price action to find patterns in when the high and low of a period are formed.

The Core Idea: Daily High & Low of the Week

The simplest and most popular feature of this indicator is the "Daily high and low of the week" analysis.

What it does:

It looks back over your chosen number of weeks (e.g., the last 100) and finds out which day of the week (Monday, Tuesday, Wednesday, etc.) made the final high and which day made the final low for each of those weeks.

How to use it:

Go to the script settings.

Enable the "Daily High/Low of the Week" module.

Set your chart to the 1D (Daily) timeframe.

A table will appear on your chart (bottom-right by default) showing the exact count and percentage for each day. This lets you see at a glance if there's a strong tendency for the market you're watching.

Advanced Analysis: Other Timeframes

This script goes far beyond just the daily chart. It includes four other independent analysis modules:

1. 4-Hour High/Low of the Week

What it does: For intraday and swing traders. This module finds which 4-hour candle session (e.g., the 08:00 candle, the 16:00 candle) tends to form the high or low of the entire week.

Key Feature (DST Aware): This table is "season-aware." It knows that the 08:00 "summertime" (DST) candle is the same trading session as the 07:00 "wintertime" (STD) candle. It groups them together so your data is never split or messy.

2. Weekly High/Low of the Month

What it does: For a monthly perspective. This module finds which week of the month (Week 1, 2, 3, 4, or 5) is most likely to form the monthly high or low.

How to use: Enable it and set your chart to the 1W (Weekly) timeframe.

3. Monthly High/Low of the Year

What it does: The ultimate "big picture" view. This module finds which month (Jan, Feb, Mar, etc.) most frequently forms the high or low for the entire year.

How to use: Enable it and set your chart to the 1M (Monthly) timeframe.

The Power User Module: Custom Timeframe Analysis

This is the most powerful feature. It lets you analyze any timeframe combination you want.

What it does: It finds out which "Lower Timeframe" (LTF) candle made the high or low of any "Higher Timeframe" (HTF) you choose.

Example: Do you want to know which 15-minute candle makes the Daily high?

Set your chart to the 15M timeframe.

Go to the "Custom Timeframe Analysis" settings.

Set the "Higher Timeframe" to "1D".

The script will draw a "season-aware" table (just like the 4H module) showing you the exact 15-minute candles (09:15, 09:30, etc.) that are statistically most likely to form the day's high or low.

Other Features

Show Labels: Each module has an option to "Show labels," which will draw a label (e.g., "Daily High of the Week") directly on the chart at the exact bar that made the high or low.

Custom Dividers: Each module has its own optional, color-customizable divider (e.g., weekly, monthly) that you can toggle on to see the periods more clearly.

Clean Settings: All modules are disabled by default (except for "Daily") to keep your chart clean. You only need to enable the specific analysis you want to see.

This tool was built to turn your curiosity about market patterns into actionable, statistical data. Enjoy!

VIX/VVIX Spike RiskVIX/VVIX Spike Risk Analyzer

The VIX/VVIX Spike Risk Analyzer analyzes historical VIX behavior under similar market conditions to forecast future VIX spike risk.

By combining current VIX and VVIX levels as dual filters, it identifies historical precedents and calculates the probability and magnitude of VIX spikes over the next 1, 5, and 10 trading days.

IMPORTANT: This indicator must be applied to the VIX chart (CBOE:VIX) to function correctly.

Methodology

1. Dual-Filter Pattern Matching

The indicator uses both VIX and VVIX as simultaneous filters to identify historically analogous market conditions:

By requiring BOTH metrics to match historical levels, the indicator creates more precise market condition filters than using VIX alone. This dual-filter approach significantly improves predictive accuracy because:

VIX alone might be at 15, but VVIX can tell us if that 15 is stable (low VVIX) or explosive (high VVIX)

High VVIX + Low VIX often precedes major spikes

Low VVIX + Low VIX suggests sustained calm

2. Tolerance Settings

VIX Matching (Default: ±10% Relative)

Uses relative percentage matching for consistency across different VIX regimes

Example: VIX at 15 matches 13.5-16.5 (±10%)

Can switch to absolute tolerance (±5 points) if preferred

VVIX Matching (Default: ±10 Points Absolute)

Uses absolute point matching as VVIX scales differently

Example: VVIX at 100 matches 90-110

Can switch to relative percentage if preferred

3. Historical Analysis Window

The indicator scans up to 500 bars backward (limited by VVIX data availability) to find all historical periods where both VIX and VVIX were at similar levels. Each match becomes a "sample" for statistical analysis.

4. Forward-Looking Spike Analysis

For each historical match, the indicator measures VIX behavior over the next 1, 5, and 10 days

Display Metrics Explained

Average Highest Spike

Shows the average of the maximum VIX spikes observed.

Highest Single Spike

Shows the single largest spike ever recorded

Probability No 10% Spike

Shows what percentage of historical cases stayed BELOW a 10% spike:

Probability No 20% Spike

Shows what percentage of historical cases stayed BELOW a 20% spike:

Note : You'll see many more shaded bars than the sample count because each match creates up to 5 consecutive shaded bars (bars 1-5 after the match all "look back" and see it).

Short Volatility Strategies:

Enter when there's a LOW probability of big vol spikes based on today's metrics

Long Volatility Strategies

Enter when there's a HIGH probability of big vol spikes based on today's metrics

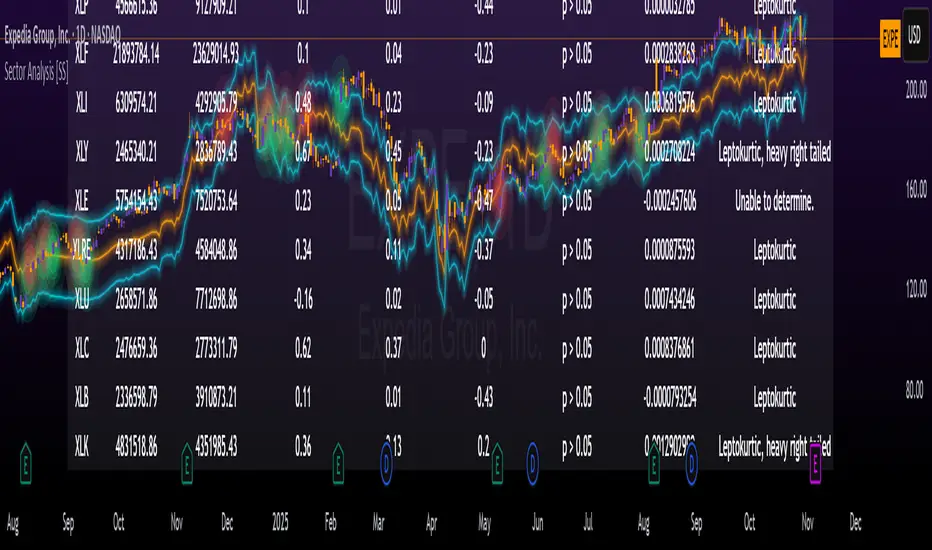

Sector Analysis [SS]Introducing the most powerful sector analysis tool/indicator available, to date, in Pine!

This is a whopper indicator, so be sure to read carefully to ensure you understand its applications and uses!

First of all, because this is a whopper, let's go over the key functional points of the indicator.

The indicator compares the 11 main sector ETFs against whichever ticker you are looking at.

The functions include the following:

Ability to pull technicals from the sectors, such as RSI, Stochastic and Z-Score;

Ability to look at the correlation of the sector ETF to the current ticker you are looking at.

Ability to calculate the R2 value between the ticker you are looking at and each sector.

The ability to run a Two Tailed T-Test against the log returns of the Ticker of interest and the Sector (to analyze statistically significant returns between sectors/tickers).

The ability to analyze the distribution of returns across all sector ETFs.

The ability to pull buying and selling volume across all sector ETFs.

The ability to create an integrated moving average using a sector ETF to predict the expected close range of a ticker of interest.

These are the highlight functions. Below, I will go more into them, what they mean and how to use them.

Pulling Technicals

This is pretty straight forward. You can pull technicals, such as RSI, Stochastic and Z-Score from all the sector ETFs and view them in a table.

See below for the example:

Pulling Correlation

In order to see which sector your ticker of interest follows more closely, we need to look first at correlation and then at R2.

The correlation will look at the immediate relationship over a specified time. A highly positive value, indicates a strong, symbiotic relationship, which the sector and the ticker follow each other. This would be represented by a correlation of 0.8 or higher.

A strong negative correlation, such as -0.8 or lower, indicates that the sector and the ticker are completely opposite. When one goes up, the other goes down and vice versa.

You can adjust your correlation assessment length directly in the settings menu:

If you want to use a sector ETF to find the expected range for a ticker of interest, it is important to locate the highest, POSITIVE, correlation value. Here are the results for MSFT at a correlation lookback of 200:

In this example, we can see the best relationship is with the ETF XLK.

Analysis of R2

R2 is an important metric. It essentially measures how much of the variance between 2 tickers are explained by a simple, linear relationship.

A high R2 means that a huge degree of variance can be explained between the 2 tickers. A low R2 means that it cannot and that the 2 tickers are likely not integrated or closely related.

In general, if you want to use the sector ETF to find the mean and trading range and identify over-valuation/over-extension and under-extension statistically, you need to see both a high correlation and a high R-Squared. These 2 metrics should be analyzed together.

Let's take a look at MSFT:

Here, despite the correlation implying that XLK was the ticker we should use to analyze, when we look at the R Squared, we see actually, we should be using XLI.

XLI has a strong positive relationship with MSFT, albeit a bit less than XLK, but the R2 is solid, > 0.9, indicating the XLI explains much of MSFT's variance.

Two Tailed T-Test

A two tailed T-test analyzes whether there is a statistically significant difference between 2 different groups, or in our case, tickers.

The T-Test is conducted on the log returns of the ticker of interest and the sector. You then can see the P value results, whether it is significant or not. Let's look at MSFT again:

Looking at this, we can see there is no statistically significant difference in returns between MSFT and any of the sectors.

We can also see the SMA of the log returns for more detailed comparison.

If we were to observe a significant finding on the T-Test metrics, this would indicate that one sector either outperforms or underperforms your ticker to a statistically significant degree! If you stumble upon this, you would check the average log returns to compare against the average returns of your ticker of interest, to see whether there is better performance or worse performance from the sector ETF vs. your ticker of interest.

Analyzing the Distribution

The indicator will also analyze the distribution of returns.

This is an interesting option as it can help you ascertain risk. Normally distributed returns imply mean reverting behavviour. Deviations from that imply trending behaviour with higher risk expectancy. If we look at the distribution statistics currently over the last 200 trading days, here are the results:

Here, we can see all show signs of trending, as none of the returns are normally distributed. The highest risk sectors are XLK and XLY.

Why are they the highest risk?

Because the indicator has found a heavy right tailed distribution, indicated sudden and erratic mean reversion/losses are possible.

Creating an MA

Now for the big bonus of the indicator!

The indicator can actually create a regression based range from closely correlated sectors, so you can see, in sectors that are strongly correlated to your ticker, whether your ticker is over-bought, oversold or has mean reverted.

Let's look at MSFT using XLI, our previously identified sector with a high correlation and high R2 value:

The results are pretty impressive.

You can see that MSFT has rode the mean of the sector on the daily timeframe for quite some time. Each time it over extended itself above the sector implied range, it mean reverted.

Currently, if you were to trade based on Pairs or statistics, MSFT is no trade as it is currently trading at its sector mean.

If you are a visual person, you can have the indicator plot the mean reversion points directly:

Green represents a bullish mean reversion and red a bearish mean reversion.

Concluding Remarks

If you like pair trading, following the link between sectors and tickers or want a more objective way to determine whether a ticker is over-bought or oversold, this indicator can help you.

In addition to doing this, the indicator can provide risk insights into different sectors by looking at the distribution, as well as identify under-performing sectors or tickers.

It can also shed light on sectors that may be technically over-bought or oversold by looking at Z-Score, stochastics and RSI.

Its a whopper and I really hope you find it helpful and useful!

Thanks everyone for reading and checking this out!

Safe trades!

Mum Formasyonları TespitiIt is used to detect candles.

It is designed to analyze all the candles that form.

The most frequently formed candles are displayed on the price chart.

Gann Astronomical Turning PointsThis is a comprehensive Pine Script that implements W.D. Gann's astronomical theories to identify potential market turning points. Here's a detailed breakdown of the script:

Overview

The script identifies and displays astronomical events (sun angles, moon phases, and Mercury retrogrades) that Gann theorists believe correlate with market turning points. It also analyzes historical price performance following these events to provide statistical significance.

Key Components

1. Input Parameters

Date Range: Users can set the analysis period (start and end dates)

Display Options: Toggle visibility of different astronomical events and tables

Analysis Settings: Configure the lookback period for price change analysis (1-20 days)

2. Astronomical Calculations

The script includes several functions to calculate celestial positions:

getDaysSinceEpoch(t): Calculates days since January 1, 2000 (reference point)

getSunLongitude(t): Computes the Sun's position in the ecliptic (0-360°)

getMoonPhase(t): Determines the Moon's phase angle relative to the Sun

getMercuryLongitude(t): Calculates Mercury's position in the ecliptic

3. Gann Critical Angles (Sun Events)

The script identifies when the Sun reaches four critical angles that Gann considered significant:

0° Aries (Spring Equinox)

90° Cancer (Summer Solstice)

180° Libra (Fall Equinox)

270° Capricorn (Winter Solstice)

These are detected by tracking when the Sun's longitude crosses these specific angles.

4. Moon Phases

Four key moon phases are identified:

New Moon: Moon passes between Earth and Sun

First Quarter: Moon is 90° east of Sun

Full Moon: Moon is opposite the Sun

Last Quarter: Moon is 270° east of Sun

5. Mercury Retrograde Periods

The script detects when Mercury appears to move backward in its orbit:

Identifies start and end dates of retrograde motion

Displays these periods as highlighted zones on the chart

6. Price Change Analysis

For each astronomical event, the script:

Calculates the percentage price change over a user-defined lookback period

Categorizes changes as positive or negative

Stores this data for statistical analysis

7. Statistical Significance

The script calculates several metrics for each event type:

Average Price Change: Mean percentage change following events

Up/Down Ratio: Number of positive vs. negative changes

Accuracy Percentage: How often the dominant direction occurred

8. Visual Elements

The script includes multiple display components:

Event Labels

Sun Angles: Orange sun symbols displayed above price bars

Moon Phases: Moon phase emojis displayed below price bars

Mercury Retrograde: Red boxes highlighting the retrograde periods

Information Tables

Events Table: Shows upcoming and recent astronomical events

Significance Analysis Table: Displays statistical performance of each event type

Forecast Section: Identifies the next upcoming event and predicted direction

9. Forecasting Functionality

The script predicts market direction for the next astronomical event based on:

Historical average price change for that event type

Statistical accuracy of previous similar events

Color-coded forecast (green for bullish, red for bearish)

This script offers an interesting implementation of Gann's astronomical theories, but should be used as part of a broader analysis rather than as a standalone trading system.

Disclaimer: This indicator is for educational purposes only. Past performance does not guarantee future results. Always conduct your own research and risk assessment before trading.

VIX Regime AnalyzerVIX Regime Analyzer

The VIX Regime Analyzer is an analytical tool that examines historical VIX patterns to provide insights into how your asset typically performs under similar volatility conditions.

Key Features:

Historical Pattern Matching: Automatically scans up to 1,000 bars of history to find all periods when VIX was at levels similar to today, using customizable tolerance ranges (absolute or percentage-based).

Forward-Looking Statistics: For each VIX regime match, calculates what actually happened to your asset over the next 1, 5, 10, and 20 trading days, providing both average returns and probability of positive outcomes.

Regime Classification System: Intelligently categorizes the current market environment as bullish or bearish: Visual Historical Context:

Background shading throughout your chart highlights every historical period when VIX matched current levels, color-coded by subsequent performance (green for gains, red for losses).

User Inputs:

VIX Level Tolerance (+/-): How closely VIX must match (default: ±5 points)

Use Relative Tolerance (%): Switch to percentage-based matching for consistency across different VIX levels

Lookback Period: How many bars to analyze

Highlight Historical VIX Matches: Toggle background highlighting of past matching periods

The Data Table

The statistics box appears in the right handside of your chart and contains three main sections:

Section 1: VIX REGIME

Current VIX: The live VIX closing price

Range: The tolerance band being searched (e.g., if VIX is 18 with ±5 tolerance, range is 13-23)

Historical Samples: Number of matching periods found in the lookback window (minimum 10 required for statistical validity)

Section 2: FORWARD RETURN

Shows the average percentage change in your asset over different timeframes following similar VIX levels:

Avg Next Day: What typically happened by the next trading session

Avg Next 5 Days: Average 5-day forward performance

Avg Next 10 Days: Average 10-day forward performance

Avg Next 20 Days: Average 20-day forward performance (approximately 1 month)

Section 3: PROBABILITY UP

Shows the win rate - the percentage of times your asset closed higher after VIX matched current levels:

Next Day: Probability of being up the next session

Next 5 Days: Probability of being up after 5 days

Next 10 Days: Probability of being up after 10 days

Next 20 Days: Probability of being up after 20 days

Colors:

🟢 Green: Bullish regimes (various strengths)

🔴 Red: Bearish regimes (various strengths)

🟡 Yellow: Choppy/uncertain regime

When "Highlight Historical VIX Matches" is enabled:

Scroll back through your chart and you'll see colored backgrounds highlighting every period when VIX matched today's level. The color tells you whether that match led to gains (green) or losses (red). This provides instant visual pattern recognition - you can quickly see if similar VIX levels historically led to bullish or bearish outcomes.

Practical Example:

If you see that most historical periods with similar VIX levels are highlighted in green, it suggests the current VIX level has historically been a bullish signal for your asset.

How The Indicator Makes Decisions

The regime classification uses both magnitude AND probability to avoid false signals:

Example of Strong Classification:

Average 5-day return: +1.5%

Win rate: 65%

Result: STRONG BULLISH (both high return and high probability)

Example of Weak Signal:

Average 5-day return: +2.0%

Win rate: 35%

Result: CHOPPY (high average but low consistency = unreliable)

This dual-factor approach ensures the indicator doesn't mislead you with regimes that had a few huge winners but mostly losers, or vice versa.

Best Practices

Combine with your existing strategy: Use this as a regime filter rather than standalone signals

Check sample size: More historical matches = more reliable statistics

Consider multiple timeframes: If 5-day and 20-day metrics disagree, proceed with caution

Asset-specific tuning: Different assets may require different tolerance settings

VIX spikes: The indicator is particularly useful during VIX spikes to understand if panic is justified

What Makes This Different

Unlike simple VIX indicators that just plot the fear index, this tool:

Quantifies the actual impact of VIX levels on YOUR specific asset

Provides probability-based forecasts rather than subjective interpretation

Shows historical context visually so you can see patterns at a glance

Uses rigorous statistical criteria to avoid false regime classifications

Trailing 12M % Gain/Lossthis script shows profit or loss for training 12 months, works only on daily time frame

Buy&Hold Profitcalculator in EuroTitle: Buy & Hold Strategy in Euro

Description:

This Pine Script implements a simple yet flexible Buy & Hold strategy denominated in Euros, suitable for a wide range of assets including cryptocurrencies, forex pairs, and stocks.

Key Features:

Custom Investment Amount: Define your invested capital in Euros.

Flexible Start & End Dates: Specify exact entry and exit dates for the strategy.

Automatic Currency Conversion: Supports assets priced in USD or USDT, converting the invested capital to chart currency using the EUR/USD exchange rate.

Single Entry and Exit: Executes a one-time Buy & Hold position based on the defined timeframe.

Profit and Performance Tracking: Calculates total profit/loss in Euros and percentage returns.

Smart Exit Label: Displays a dynamic label at the exit showing final position value, net profit/loss, and return percentage. The label automatically adjusts its position above or below the price bar for optimal visibility.

Visual Enhancements:

Position value and profit/loss plotted on the chart.

Background color highlights the active investment period.

Buy and Sell markers clearly indicate entry and exit points.

This strategy is ideal for traders and investors looking to simulate long-term positions and evaluate performance in Euro terms, even when trading USD-denominated assets.

Usage Notes:

Best used on daily charts for medium- to long-term analysis.

Adjust start and end dates, as well as invested capital, to simulate different scenarios.

Works with any asset, but currency conversion is optimized for USD or USDT-pegged instruments.

3D Institutional Battlefield [SurgeGuru]Professional Presentation: 3D Institutional Flow Terrain Indicator

Overview

The 3D Institutional Flow Terrain is an advanced trading visualization tool that transforms complex market structure into an intuitive 3D landscape. This indicator synthesizes multiple institutional data points—volume profiles, order blocks, liquidity zones, and voids—into a single comprehensive view, helping you identify high-probability trading opportunities.

Key Features

🎥 Camera & Projection Controls

Yaw & Pitch: Adjust viewing angles (0-90°) for optimal perspective

Scale Controls: Fine-tune X (width), Y (depth), and Z (height) dimensions

Pro Tip: Increase Z-scale to amplify terrain features for better visibility

🌐 Grid & Surface Configuration

Resolution: Adjust X (16-64) and Y (12-48) grid density

Visual Elements: Toggle surface fill, wireframe, and node markers

Optimization: Higher resolution provides more detail but requires more processing power

📊 Data Integration

Lookback Period: 50-500 bars of historical analysis

Multi-Source Data: Combine volume profile, order blocks, liquidity zones, and voids

Weighted Analysis: Each data source contributes proportionally to the terrain height

How to Use the Frontend

💛 Price Line Tracking (Your Primary Focus)

The yellow price line is your most important guide:

Monitor Price Movement: Track how the yellow line interacts with the 3D terrain

Identify Key Levels: Watch for these critical interactions:

Order Blocks (Green/Red Zones):

When yellow price line enters green zones = Bullish order block

When yellow price line enters red zones = Bearish order block

These represent institutional accumulation/distribution areas

Liquidity Voids (Yellow Zones):

When yellow price line enters yellow void areas = Potential acceleration zones

Voids indicate price gaps where minimal trading occurred

Price often moves rapidly through voids toward next liquidity pool

Terrain Reading:

High Terrain Peaks: High volume/interest areas (support/resistance)

Low Terrain Valleys: Low volume areas (potential breakout zones)

Color Coding:

Green terrain = Bullish volume dominance

Red terrain = Bearish volume dominance

Purple = Neutral/transition areas

📈 Volume Profile Integration

POC (Point of Control): Automatically marks highest volume level

Volume Bins: Adjust granularity (10-50 bins)

Height Weight: Control how much volume affects terrain elevation

🏛️ Order Block Detection

Detection Length: 5-50 bar lookback for block identification

Strength Weighting: Recent blocks have greater impact on terrain

Candle Body Option: Use full candles or body-only for block definition

💧 Liquidity Zone Tracking

Multiple Levels: Track 3-10 key liquidity zones

Buy/Sell Side: Different colors for bid/ask liquidity

Strength Decay: Older zones have diminishing terrain impact

🌊 Liquidity Void Identification

Threshold Multiplier: Adjust sensitivity (0.5-2.0)

Height Amplification: Voids create significant terrain depressions

Acceleration Zones: Price typically moves quickly through void areas

Practical Trading Application

Bullish Scenario:

Yellow price line approaches green order block terrain

Price finds support in elevated bullish volume areas

Terrain shows consistent elevation through key levels

Bearish Scenario:

Yellow price line struggles at red order block resistance

Price falls through liquidity voids toward lower terrain

Bearish volume peaks dominate the landscape

Breakout Setup:

Yellow price line consolidates in flat terrain

Minimal resistance (low terrain) in projected direction

Clear path toward distant liquidity zones

Pro Tips

Start Simple: Begin with default settings, then gradually customize

Focus on Yellow Line: Your primary indicator of current price position

Combine Timeframes: Use the same terrain across multiple timeframes for confluence

Volume Confirmation: Ensure terrain peaks align with actual volume spikes

Void Anticipation: When price enters voids, prepare for potential rapid movement

Order Blocks & Voids Architecture

Order Blocks Calculation

Trigger: Price breaks fractal swing points

Bullish OB: When close > swing high → find lowest low in lookback period

Bearish OB: When close < swing low → find highest high in lookback period

Strength: Based on price distance from block extremes

Storage: Global array maintains last 50 blocks with FIFO management

Liquidity Voids Detection

Trigger: Price gaps exceeding ATR threshold

Bull Void: Low - high > (ATR200 × multiplier)

Bear Void: Low - high > (ATR200 × multiplier)

Validation: Close confirms gap direction

Storage: Global array maintains last 30 voids

Key Design Features

Real-time Updates: Calculated every bar, not just on last bar

Global Persistence: Arrays maintain state across executions

FIFO Management: Automatic cleanup of oldest entries

Configurable Sensitivity: Adjustable lookback periods and thresholds

Scientific Testing Framework

Hypothesis Testing

Primary Hypothesis: 3D terrain visualization improves detection of institutional order flow vs traditional 2D charts

Testable Metrics:

Prediction Accuracy: Does terrain structure predict future support/resistance?

Reaction Time: Faster identification of key levels vs conventional methods

False Positive Reduction: Lower rate of failed breakouts/breakdowns

Control Variables

Market Regime: Trending vs ranging conditions

Asset Classes: Forex, equities, cryptocurrencies

Timeframes: M5 to H4 for intraday, D1 for swing

Volume Conditions: High vs low volume environments

Data Collection Protocol

Terrain Features to Quantify:

Slope gradient changes at price inflection points

Volume peak clustering density

Order block terrain elevation vs subsequent price action

Void depth correlation with momentum acceleration

Control Group: Traditional support/resistance + volume profile

Experimental Group: 3D Institutional Flow Terrain

Statistical Measures

Signal-to-Noise Ratio: Terrain features vs random price movements

Lead Time: Terrain formation ahead of price confirmation

Effect Size: Performance difference between groups (Cohen's d)

Statistical Power: Sample size requirements for significance

Validation Methodology

Blind Testing:

Remove price labels from terrain screenshots

Have traders identify key levels from terrain alone

Measure accuracy vs actual price action

Backtesting Framework:

Automated terrain feature extraction

Correlation with future price reversals/breakouts

Monte Carlo simulation for significance testing

Expected Outcomes

If hypothesis valid:

Significant improvement in level prediction accuracy (p < 0.05)

Reduced latency in institutional level identification

Higher risk-reward ratios on terrain-confirmed trades

Research Questions:

Does terrain elevation reliably indicate institutional interest zones?

Are liquidity voids statistically significant momentum predictors?

Does multi-timeframe terrain analysis improve signal quality?

How does terrain persistence correlate with level strength?

LuxAlgo BigBeluga hapharmonic

Eagles CompassFree script

Helps detect specific body/wick ratios on chart for 1HR,2HR,4HR timeframes

Designed to help you detect large squeezes, bounces, and other moves

Ideally use in conjunction with an RSI to filter for false positives

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.