MacroJP: US Macro Conditions & Forward GuidanceMacroJP is a comprehensive, free-to-use TradingView indicator designed to provide a clear snapshot of the US macroeconomic environment. It consolidates key economic metrics into a single, interactive dashboard, allowing traders and investors to quickly assess current conditions and adjust their portfolio biases accordingly.

How It Works:

• Data Aggregation:

The indicator pulls monthly data from reputable free economic sources—specifically, ISM Manufacturing PMI, US CPI YoY, US M2 Money Supply, and US Treasury yields (10-year and 2-year). This robust dataset forms the backbone of the analysis.

• Composite Calculations:

By calculating a Composite Inflation Indicator (the average of CPI YoY and the yield spread) and evaluating the year-over-year change in M2, MacroJP gauges both the inflationary pressures and liquidity trends in the economy. These composite metrics offer a nuanced view that goes beyond single-indicator analysis.

Regime Classification:

The core strength of MacroJP lies in its quadrant classification system. It categorises the macro environment into four distinct regimes based on the direction of economic growth (derived from PMI) and inflation (from the Composite Inflation Indicator):

• Expansion (Reflation): Indicative of a recovering economy with rising production and moderate inflation—ideal for a bullish equity bias.

• Stagflation Risk: A scenario of weak growth coupled with high inflation, where a defensive posture is recommended.

• Slowdown (Deflationary): Characterised by contracting economic activity and falling prices, suggesting a move towards cash or high-quality bonds.

• Disinflationary Boom: Reflects strong growth with stable or falling inflation—an optimal environment for equities with some bond diversification.

Forward Guidance:

To enhance its predictive capability, MacroJP incorporates leading indicators by shifting key data points. For instance, it uses a forward-shifted M2 YoY value and a one-month shifted CPI proxy to offer insights into near-term trends. This approach helps in anticipating changes, providing a sort of “forward guidance” that can inform strategic asset allocation.

User Education:

The indicator features an intuitive table with on-hover tooltips that explain each metric, its relevance, and recommended investment biases. This educational layer is designed to empower users to not only monitor the economic pulse but also to understand the ‘why’ behind each reading, making it a valuable tool for both novice and experienced investors.

MacroJP brings clarity to complex macroeconomic dynamics, allowing users to make more informed decisions in volatile markets. Its seamless integration of free public data and detailed on-chart annotations makes it an indispensable tool for anyone looking to understand the broader economic context impacting their investments.

— Jaroslav

Forecasting

EMA Ribbon with 100 MA BY TIJUThe EMA Ribbon with 100 MA is a powerful and visually intuitive indicator designed to help traders identify trends, momentum, and potential support/resistance levels using multiple Exponential Moving Averages (EMAs). By plotting a series of EMAs with varying periods, the script creates a "ribbon" effect on the chart, making it easier to spot trend direction and strength at a glance.

Key Features:

Multiple EMAs for Trend Analysis:

The script plots 8 EMAs with periods ranging from 20 to 55, creating a gradient ribbon effect.

The 100-period EMA is added as a thick blue line, acting as a key level for long-term trend analysis.

Customizable Periods:

Each EMA period is fully customizable, allowing traders to tailor the indicator to their preferred trading style and timeframe.

Visual Clarity:

The EMAs are color-coded, making it easy to distinguish between different periods and identify the overall trend direction.

Dynamic Support/Resistance:

The EMAs act as dynamic support and resistance levels, helping traders identify potential entry and exit points.

Drop Candles Feature:

The script includes an option to drop the first N candles, ensuring cleaner calculations and avoiding false signals during the initial periods.

How to Use:

Trend Identification:

Uptrend: When the shorter-period EMAs are stacked above the longer-period EMAs, it indicates a strong uptrend.

Downtrend: When the longer-period EMAs are stacked above the shorter-period EMAs, it indicates a strong downtrend.

Consolidation: When the EMAs are intertwined, it suggests a sideways or weak trend.

Support/Resistance Levels:

Use the EMAs as dynamic support/resistance levels. For example, in an uptrend, the price may bounce off the lower EMAs.

100-Period EMA:

The 100-period EMA (thick blue line) acts as a key level for long-term trend analysis. A price above this line suggests a bullish bias, while a price below suggests a bearish bias.

Customization:

Adjust the EMA periods and colors to suit your trading strategy.

Use the Drop first N candles option to avoid false signals during the initial periods.

Example Use Cases:

Trend Following:

Enter long positions when the price is above the EMA ribbon and the EMAs are stacked in an uptrend.

Enter short positions when the price is below the EMA ribbon and the EMAs are stacked in a downtrend.

Dynamic Support/Resistance:

Use the EMAs as dynamic support/resistance levels for setting stop-loss or take-profit targets.

Confirmation Tool:

Combine the EMA Ribbon with other indicators (e.g., RSI, MACD) to confirm trade signals.

Settings:

MA-1 to MA-8 Periods: Adjust the periods for the 8 EMAs (default: 20, 25, 30, 35, 40, 45, 50, 55).

MA-100 Period: Adjust the period for the 100 EMA (default: 100).

Source: Choose the price source for the EMAs (default: Close).

Drop First N Candles: Drop the first N candles to avoid false signals (default: 1).

Why Use EMA Ribbon ?

Versatility: Suitable for all trading styles (scalping, day trading, swing trading) and timeframes.

Visual Appeal: The color-coded ribbon makes it easy to interpret the trend at a glance.

Customizable: Tailor the indicator to your specific trading strategy.

Dynamic Levels: Use the EMAs as dynamic support/resistance levels for better risk management.

Ivan Gomes StrategyIG Signals+ - Ivan Gomes Strategy

This script is designed for scalping and binary options trading, generating buy and sell signals at the beginning of each candle. Although it is mainly optimized for short-term operations, it can also be used for medium and long-term strategies with appropriate adjustments.

How It Works

• The indicator provides buy or sell signals at the start of the candle, based on a statistical probability of candle patterns, depending on the timeframe.

• It is essential to enter the trade immediately after the signal appears and exit at the end of the same candle.

• If the first operation results in a loss (Loss), the script will send another trade signal at the start of the next candle. However, if the first trade results in a win (Gain), no new signal will be generated.

• The signals follow cycles of 3 candles, regardless of the timeframe. However, if a Doji candle appears, the cycle is interrupted, and no signals will be generated until the next valid cycle starts.

• The strategy consists of up to two trades per cycle: if the first trade is not successful, the second trade serves as an additional attempt to recover.

Key Points to Consider

1. Avoid trading in sideways markets – If price levels do not fluctuate significantly, the accuracy of the signals may decrease.

2. Trade in the direction of the trend – Using Ichimoku clouds or other trend indicators can help confirm trend direction and improve signal reliability. If the market is in an uptrend (bullish trend) and the indicator generates a sell signal, the most prudent decision would be to wait for a buy signal that aligns with the main trend. The same applies to downtrends, where buy signals may be riskier.

These decisions should be based on chart reading and supported by other technical analysis tools, such as support and resistance levels, which indicate zones where price might face obstacles or reverse direction. Additionally, Fibonacci retracement levels can help identify possible pullback points within a trend. Moving averages are also useful for visualizing the general market direction and confirming whether an indicator signal aligns with the overall price structure. Combining these tools can increase trade accuracy and prevent unnecessary trades against the main trend, reducing risks.

3. Works based on probability statistics – The algorithm analyzes candle formations and their statistical probabilities depending on the timeframe to optimize trade entries.

4. Best suited for scalping and binary options – This strategy performs best in 1-minute and 5-minute timeframes, allowing for multiple trades throughout the day.

Technical Details

• The script detects the candle cycle and assigns an index to each candle to identify patterns and possible reversals.

• It recognizes reference candles, stores their colors, and compares them with subsequent candles to determine if a signal should be triggered.

• Doji candle rules are implemented to avoid false signals in indecisive market conditions. When a Doji appears, the script does not generate signals for that cycle.

• The indicator displays visual alerts and notifications, ensuring fast execution of trades.

Disclaimer

The IG Signals+ indicator was created to assist traders who struggle to analyze the market by providing objective trade signals. However, no strategy is foolproof, and this script does not guarantee profits.

Trading involves significant financial risk, and users should test it in a demo account before trading with real money. Proper risk management is crucial for long-term success.

Autocorrelation Price Forecasting [The Quant Science]Discover how to predict future price movements using autocorrelation and linear regression models to identify potential trading opportunities.

An advanced model to predict future price movements using autocorrelation and linear regression. This script helps identify recurring market cycles and calculates potential gains, with clear visual signals for quick and informed decisions.

Main function

This script leverages an autocorrelation model to estimate the future price of an asset based on historical price relationships. It also integrates linear regression on percentage returns to provide more accurate predictions of price movements.

Insights types

1) Red label on a green candle: Bearish forecast and swing trading opportunity.

2) Red label on a red candle: Bearish forecast and trend-following opportunity.

3) Green label on a red candle: Bullish forecast and swing trading opportunity.

4) Green label on a green candle: Bullish forecast and trend-following opportunity.

IMPORTANT!

The indicator displays a future price forecast. When negative, it estimates a future price drop.

When positive, it estimates a future price increase.

Key Features

Customizable inputs

Analysis Length: number of historical bars used for autocorrelation calculation. Adjustable between 1 and 200.

Forecast Colors: customize colors for bullish and bearish signals.

Visual insights

Labels: hypothetical gains or losses are displayed as labels above or below the bars.

Dynamic coloring: bullish (green) and bearish (red) signals are highlighted directly on the chart.

Forecast line: A continuous line is plotted to represent the estimated future price values.

Practical applications

Short-term Trading: identify repetitive market cycles to anticipate future movements.

Visual Decision-making: colored signals and labels make it easier to visualize potential profit or loss for each trade.

Advanced Customization: adjust the data length and colors to tailor the indicator to your strategies.

Limitations

Prediction price models have some limitations. Trading decisions should be made with caution, considering additional market factors and risk management strategies.

Bayesian TrendEnglish Description (primary)

1. Overview

This script implements a Naive Bayesian classifier to estimate the probability of an upcoming bullish, bearish, or neutral move. It combines multiple indicators—RSI, MACD histogram, EMA price difference in ATR units, ATR level vs. its average, and Volume vs. its average—to calculate likelihoods for each market direction. Each indicator is “binned” (categorized into discrete zones) and assigned conditional probabilities for bullish/bearish/neutral scenarios. The script then normalizes these probabilities and paints bars in green if bullish is most likely, red if bearish is most likely, or blue if neutral is most likely. A small table is also displayed in the top-right corner of the chart, showing real-time probabilities.

2. How it works

Indicator Calculations: The script calculates RSI, MACD (line and histogram), EMA, ATR, and Volume metrics.

Binning: Each metric is converted into a discrete category (e.g., low, medium, high). For example, RSI < 30 is binned as “low,” while RSI > 70 is binned as “high.”

Conditional Probabilities: User-defined tables specify the conditional probabilities of each bin under three hypotheses (Up, Down, Neutral).

Naive Bayesian Formula: The script multiplies the relevant conditional probabilities, normalizes them, and derives the final probabilities (Up, Down, or Neutral).

Visualization:

Bar Colors: Bars are green when the Up probability exceeds 50%, red for Down, and blue otherwise.

Table: Displays numeric probabilities of Up, Down, and Neutral in percentage terms.

3. How to use it

Add the script to your chart.

Observe the colored bars:

Green suggests a higher probability for bullish movement.

Red suggests a higher probability for bearish movement.

Blue indicates a higher probability of sideways or uncertain conditions.

Check the table in the top-right corner to see exact probabilities (Up/Down/Neutral).

Use the input settings to adjust thresholds (RSI, MACD, Volume, etc.), define alert conditions (e.g., when Up probability crosses 50%), and decide whether to trigger alerts on bar close or in real-time.

4. Originality and usefulness

Originality: This script uniquely applies a Naive Bayesian approach to a blend of classic and volume-based indicators. It demonstrates how different indicator “zones” can be combined to produce probabilistic insights.

Usefulness: Traders can interpret the probability breakdown to gauge the script’s bias. Unlike single indicators, this approach synthesizes several signals, potentially offering a more holistic perspective on market conditions.

5. Limitations

The conditional probabilities are manually assigned and may not reflect actual market behavior across all instruments or timeframes.

Results depend on the user’s choice of thresholds and indicator settings.

Like any indicator, past performance does not guarantee future results. Always confirm signals with additional analysis.

6. Disclaimer

This script is intended for educational and informational purposes only. It does not constitute financial advice. Trading involves significant risk, and you should make decisions based on your own analysis. Neither the script’s author nor TradingView is liable for any financial losses.

Русское описание (Russian translation, optional)

Этот индикатор реализует наивный Байесовский классификатор для оценки вероятности предстоящего роста (Up), падения (Down) или бокового движения (Neutral). Он комбинирует несколько индикаторов—RSI, гистограмму MACD, разницу цены и EMA в единицах ATR, уровень ATR относительно своего среднего значения и объём относительно своего среднего—чтобы вычислить вероятности для каждого направления рынка. Каждый индикатор делится на «зоны» (low, mid, high), которым приписаны условные вероятности для бычьего/медвежьего/нейтрального исхода. Скрипт нормирует эти вероятности и раскрашивает бары в зелёный, красный или синий цвет в зависимости от того, какая вероятность выше. Также в правом верхнем углу отображается таблица с текущими значениями вероятностей.

Opening Range BoxIndicator Name: Opening Range Box with Extensions

Author: YanivBull

Description:

The Opening Range Box with Extensions is a powerful tool designed to visualize the trading range established during the first 30 minutes of a market session, a critical period for setting the day's trend. This indicator plots a box representing the high and low prices formed within this opening range, with dashed extension lines projecting these levels forward throughout the session.

Its primary purpose is to identify the boundaries of the initial trend at the start of trading. When these boundaries are breached, it serves as a trigger for potential trading opportunities: a breakout above the box high signals a possible long entry, while a breakdown below the box low indicates a potential short entry. The indicator also includes historical boxes for up to 5 previous days (configurable), allowing traders to analyze past opening ranges and their extensions for context and pattern recognition.

Key Features:

Customizable session start time (hour and minute) to adapt to various markets (e.g., NYSE, DAX, etc.).

Displays the current session's opening range box in blue and historical boxes in gray.

Plots dashed extension lines from the high and low of each box, limited to 500 bars or the end of the trading day.

Adjustable number of historical days (1-20, default 5).

Usage:

Set the Session Start Hour and Session Start Minute according to your market's opening time (relative to your chart's timezone, e.g., UTC+2). Watch for price action around the box boundaries—breakouts above the high or below the low can be used as signals for initiating long or short trades, respectively. Combine with other technical analysis tools for confirmation.

This indicator is ideal for day traders looking to capitalize on early session momentum and breakout strategies.

Smoothed EMA LinesThe "Smoothed EMA Lines" script is a technical analysis tool designed to help traders identify trends and potential support/resistance levels in financial markets. The script plots exponential moving averages (EMAs) of the closing price for five commonly used time periods: 8, 13, 21, 55, and 200.

Key features of the script include:

Overlay: The EMAs are plotted directly on the price chart, making it easy to analyze the relationship between the moving averages and price action.

Smoothing: The script applies an additional smoothing function to each EMA, using a simple moving average (SMA) of a user-defined length. This helps to reduce noise and provide a clearer picture of the trend.

Customizable lengths: Users can easily adjust the length of each EMA and the smoothing period through the script's input parameters.

Color-coded plots: Each EMA is assigned a unique color (8: blue, 13: green, 21: orange, 55: red, 200: purple) for easy identification on the chart.

Traders can use the "Smoothed EMA Lines" script to:

Identify the overall trend direction (bullish, bearish, or neutral) based on the arrangement of the EMAs.

Spot potential support and resistance levels where the price may interact with the EMAs.

Look for crossovers between EMAs as potential entry or exit signals.

Combine the EMA analysis with other technical indicators and price action patterns for a more comprehensive trading strategy.

The "Smoothed EMA Lines" script provides a clear, customizable, and easy-to-interpret visualization of key exponential moving averages, helping traders make informed decisions based on trend analysis.

Moving Average and Pearson LevelsMoving Average and Pearson Levels Indicator

This Pine Script indicator combines a customizable moving average (MA) with Pearson correlation analysis to provide traders with deeper insights into trends and key reference levels. It overlays a Pearson-adjusted moving average on price charts and highlights levels based on correlation for potential trading opportunities. With flexible parameters, it adapts to various trading styles.

Key Features

Pearson-Adjusted Moving Average

Combines a basic MA (SMA, EMA, WMA, or VWMA) with a Pearson correlation adjustment to reflect trend strength.

Adjustable: MA length, price source, smoothing, and line thickness.

Optional color changes based on trends (positive/negative).

Pearson Correlation Levels

Plots smoothed Pearson correlation with upper/lower thresholds to signal strong or weak trends.

Marks entry levels with price labels and dynamic colors when thresholds are crossed.

Customizable: Pearson length, smoothing, thresholds, and colors.

Reference Levels and Alerts

Optional dotted lines for upper, lower, and zero correlation thresholds.

Alerts for bullish MA signals (crossing the lower threshold) and bearish signals (crossing below the upper threshold).

How It Works

Moving Average: Calculates a standard moving average enhanced by a Pearson adjustment based on price trends over a given period.

Pearson Levels: Computes the strength of correlation, smoothed for better readability, and plots price lines at threshold crossings.

Visualization: Displays the MA and levels with trend-reactive colors and optional reference lines.

Usage

Ideal for traders who combine traditional MAs with statistical trend analysis.

Adjust the MA type and Pearson length for short-term or long-term strategies.

Use correlation levels for reversal signals or trend confirmation.

Customization Options

MA Parameters: Select the type, length, and smoothing of the MA; toggle visibility and color changes.

Pearson Levels: Adjust thresholds, line thickness, and label colors.

Display Options: Show/hide reference lines and the standard MA for comparison purposes.

Example Settings

MA Length: 20

Type: EMA

Pearson Length: 15

Thresholds: 0.7/-0.7

Colors: Positive (black), Negative (green), Levels (gray)

Notes

Optimize based on your preferred timeframe.

Adjust smoothing to balance responsiveness and clarity.

Try it out, customize it to your needs, and enhance your trading setup! Feedback and suggestions are welcome.

Yearly Percentage ChangeThe "Yearly Percentage Change" indicator analyzes the long-term performance of an asset over the past year (252 trading days). It helps traders identify the strength of an asset at first glance by the color of the drawing.

It calculates two key values:

The percentage change from the closing price 252 days ago (Year-over-Year performance).

The percentage change from the lowest price of the last 252 days.

These values are visualized with colored lines and a performance label.

📊 Features & Benefits

1️⃣ Yearly Percentage Change (YoY)

Compares the current closing price with the closing price from 252 days ago.

Draws a solid line from the previous year’s close to the current price.

Line color indicates market performance:

🔴 Red → Price increased up to 100%.

🟡 Yellow → Price increased between 100% and 200%.

🟢 Green → Price increased more than 200%.

2️⃣ 252-Day Low & Its Performance

Identifies the lowest price in the last 252 days.

Draws a dashed line from this low to the current price.

Line color reflects the performance since the low:

🔴 Red → Price increased up to 100%.

🟡 Yellow → Price increased between 100% and 200%.

🟢 Green → Price increased more than 200%.

3️⃣ Informative Performance Label

Displays two key values:

"YoY" → Percentage change from the closing price 252 days ago.

"Low252" → Percentage change from the lowest price in the past 252 days.

Label color depends on the YoY movement.

MTF Moving Averages (only EMA)MTF Moving Averages (only EMA)

This script provides a Multi-Timeframe (MTF) Exponential Moving Average (EMA) indicator for traders to visualize multiple EMAs across different timeframes directly on a single chart.

The indicator dynamically calculates and plots up to four EMAs per timeframe (15-minute, 30-minute, 1-hour, and Daily) with user-defined lengths, offering valuable insight into price trends and potential entry or exit points.

Key Features:

Multiple Timeframe Support: The script allows you to view EMAs from different timeframes simultaneously. This is especially useful for traders who follow trends across different timeframes to make more informed decisions.

Customizable Lengths: For each timeframe, the lengths of the EMAs are fully customizable. You can adjust the length of up to four EMAs per timeframe to suit your strategy.

EMA Calculation: The Exponential Moving Average (EMA) is used, which gives more weight to recent prices and reacts faster to price changes compared to the simple moving average (SMA).

Timeframe Flexibility: The indicator supports the following timeframes:

15-minute: Ideal for short-term traders and scalpers.

30-minute: For intraday trading with a slightly longer perspective.

1-hour: Suitable for swing traders and those who prefer a more medium-term view.

Daily: Great for longer-term trend-following strategies.

Interactive and User-Friendly: You can toggle the visibility of each EMA on each timeframe, allowing you to choose exactly which EMAs you wish to display, depending on your trading strategy.

Color-Coded for Clarity: The script uses distinct colors for each EMA on the chart:

Blue: EMA1

Green: EMA2

Red: EMA3

Purple: EMA4

Line Width Customization: Each plotted EMA line has a customizable width for better visual clarity.

Use Case:

Traders who use multiple timeframes for analysis (e.g., those using the "multi-timeframe analysis" technique) will find this script particularly useful. For example, a trader may look at the 15-minute chart to catch short-term movements, the 30-minute chart for intraday trends, the 1-hour chart for swing positions, and the Daily chart for identifying the overarching market trend. The script enables them to view the EMAs for all these timeframes in one glance without having to manually switch between them.

By observing the relationships between EMAs across multiple timeframes, traders can gain valuable insights into market conditions such as:

Crossovers: When a shorter-term EMA crosses above or below a longer-term EMA, it can signal a potential trend reversal or continuation.

Trend Strength: Multiple EMAs in alignment across different timeframes can indicate strong trend strength.

Support and Resistance: EMAs can act as dynamic support and resistance levels, guiding traders on price action levels to watch for potential price reversals.

Instructions:

Enable/Disable EMAs: Toggle on or off the EMAs for each timeframe (15-min, 30-min, 1-hour, Daily) using the script’s settings.

Adjust EMA Lengths: Change the default lengths for each EMA to match your preferred settings for different timeframes.

Monitor Key Levels: Watch how price interacts with the plotted EMAs to spot potential trading signals based on your strategy.

This indicator is designed to enhance your multi-timeframe analysis and help make more informed, data-driven trading decisions.

Enhanced KLSE Banker Flow Oscillator# Enhanced KLSE Banker Flow Oscillator

## Description

The Enhanced KLSE Banker Flow Oscillator is a sophisticated technical analysis tool designed specifically for the Malaysian stock market (KLSE). This indicator analyzes price and volume relationships to identify potential smart money movements, providing early signals for market reversals and continuation patterns.

The oscillator measures the buying and selling pressure in the market with a focus on detecting institutional activity. By combining money flow calculations with volume filters and price action analysis, it helps traders identify high-probability trading opportunities with reduced noise.

## Key Features

- Dual-Timeframe Analysis: Combines long-term money flow trends with short-term momentum shifts for more accurate signals

- Adaptive Volume Filtering: Automatically adjusts volume thresholds based on recent market conditions

- Advanced Divergence Detection: Identifies potential trend reversals through price-flow divergences

- Early Signal Detection: Provides anticipatory signals before major price movements occur

- Multiple Signal Types: Offers both early alerts and strong confirmation signals with clear visual markers

- Volatility Adjustment: Adapts sensitivity based on current market volatility for more reliable signals

- Comprehensive Visual Feedback: Color-coded oscillator, signal markers, and optional text labels

- Customizable Display Options: Toggle momentum histogram, early signals, and zone fills

- Organized Settings Interface: Logically grouped parameters for easier configuration

## Indicator Components

1. Main Oscillator Line: The primary banker flow line that fluctuates above and below zero

2. Early Signal Line: Secondary indicator showing potential emerging signals

3. Momentum Histogram: Visual representation of flow momentum changes

4. Zone Fills: Color-coded background highlighting positive and negative zones

5. Signal Markers: Visual indicators for entry and exit points

6. Reference Lines: Key levels for strong and early signals

7. Signal Labels: Optional text annotations for significant signals

## Signal Types

1. Strong Buy Signal (Green Arrow): Major bullish signal with high probability of success

2. Strong Sell Signal (Red Arrow): Major bearish signal with high probability of success

3. Early Buy Signal (Blue Circle): First indication of potential bullish trend

4. Early Sell Signal (Red Circle): First indication of potential bearish trend

5. Bullish Divergence (Yellow Triangle Up): Price making lower lows while flow makes higher lows

6. Bearish Divergence (Yellow Triangle Down): Price making higher highs while flow makes lower highs

## Parameters Explained

### Core Settings

- MFI Base Length (14): Primary calculation period for money flow index

- Short-term Flow Length (5): Calculation period for early signals

- KLSE Sensitivity (1.8): Multiplier for flow calculations, higher = more sensitive

- Smoothing Length (5): Smoothing period for the main oscillator line

### Volume Filter Settings

- Volume Filter % (65): Minimum volume threshold as percentage of average

- Use Adaptive Volume Filter (true): Dynamically adjusts volume thresholds

### Signal Levels

- Strong Signal Level (15): Threshold for strong buy/sell signals

- Early Signal Level (10): Threshold for early buy/sell signals

- Early Signal Threshold (0.75): Sensitivity factor for early signals

### Advanced Settings

- Divergence Lookback (34): Period for checking price-flow divergences

- Show Signal Labels (true): Toggle text labels for signals

### Visual Settings

- Show Momentum Histogram (true): Toggle the momentum histogram display

- Show Early Signal (true): Toggle the early signal line display

- Show Zone Fills (true): Toggle background color fills

## How to Use This Indicator

### Installation

1. Add the indicator to your TradingView chart

2. Default settings are optimized for KLSE stocks

3. Customize parameters if needed for specific stocks

### Basic Interpretation

- Oscillator Above Zero: Bullish bias, buying pressure dominates

- Oscillator Below Zero: Bearish bias, selling pressure dominates

- Crossing Zero Line: Potential shift in market sentiment

- Extreme Readings: Possible overbought/oversold conditions

### Advanced Interpretation

- Divergences: Early warning of trend exhaustion

- Signal Confluences: Multiple signal types appearing together increase reliability

- Volume Confirmation: Signals with higher volume are more significant

- Momentum Alignment: Histogram should confirm direction of main oscillator

### Trading Strategies

#### Trend Following Strategy

1. Identify market trend direction

2. Wait for pullbacks shown by oscillator moving against trend

3. Enter when oscillator reverses back in trend direction with a Strong signal

4. Place stop loss below/above recent swing low/high

5. Take profit at previous resistance/support levels

#### Counter-Trend Strategy

1. Look for oscillator reaching extreme levels

2. Identify divergence between price and oscillator

3. Wait for oscillator to cross Early signal threshold

4. Enter position against prevailing trend

5. Use tight stop loss (1 ATR from entry)

6. Take profit at first resistance/support level

#### Breakout Confirmation Strategy

1. Identify stock consolidating in a range

2. Wait for price to break out of range

3. Confirm breakout with oscillator crossing zero line in breakout direction

4. Enter position in breakout direction

5. Place stop loss below/above the breakout level

6. Trail stop as price advances

### Signal Hierarchy and Reliability

From highest to lowest reliability:

1. Strong Buy/Sell signals with divergence and high volume

2. Strong Buy/Sell signals with high volume

3. Divergence signals followed by Early signals

4. Strong Buy/Sell signals with normal volume

5. Early Buy/Sell signals with high volume

6. Early Buy/Sell signals with normal volume

## Complete Trading Plan Example

### KLSE Market Trading System

#### Pre-Trading Preparation

1. Review overall market sentiment (bullish, bearish, or neutral)

2. Scan for stocks showing significant banker flow signals

3. Note key support/resistance levels for watchlist stocks

4. Prioritize trade candidates based on signal strength and volume

#### Entry Rules for Long Positions

1. Banker Flow Oscillator above zero line (positive flow environment)

2. One or more of the following signals present:

- Strong Buy signal (green arrow)

- Bullish Divergence signal (yellow triangle up)

- Early Buy signal (blue circle) with confirming price action

3. Entry confirmation requirements:

- Volume above 65% of 20-day average

- Price above short-term moving average (e.g., 20 EMA)

- No immediate resistance within 3% of entry price

4. Entry on the next candle open after signal confirmation

#### Entry Rules for Short Positions

1. Banker Flow Oscillator below zero line (negative flow environment)

2. One or more of the following signals present:

- Strong Sell signal (red arrow)

- Bearish Divergence signal (yellow triangle down)

- Early Sell signal (red circle) with confirming price action

3. Entry confirmation requirements:

- Volume above 65% of 20-day average

- Price below short-term moving average (e.g., 20 EMA)

- No immediate support within 3% of entry price

4. Entry on the next candle open after signal confirmation

#### Position Sizing Rules

1. Base risk per trade: 1% of trading capital

2. Position size calculation: Capital × Risk% ÷ Stop Loss Distance

3. Position size adjustments:

- Increase by 20% for Strong signals with above-average volume

- Decrease by 20% for Early signals without confirming price action

- Standard size for all other valid signals

#### Stop Loss Placement

1. For Long Positions:

- Place stop below the most recent swing low

- Minimum distance: 1.5 × ATR(14)

- Maximum risk: 1% of trading capital

2. For Short Positions:

- Place stop above the most recent swing high

- Minimum distance: 1.5 × ATR(14)

- Maximum risk: 1% of trading capital

#### Take Profit Strategy

1. First Target (33% of position):

- 1.5:1 reward-to-risk ratio

- Move stop to breakeven after reaching first target

2. Second Target (33% of position):

- 2.5:1 reward-to-risk ratio

- Trail stop at previous day's low/high

3. Final Target (34% of position):

- 4:1 reward-to-risk ratio or

- Exit when opposing signal appears (e.g., Strong Sell for long positions)

#### Trade Management Rules

1. After reaching first target:

- Move stop to breakeven

- Consider adding to position if new confirming signal appears

2. After reaching second target:

- Trail stop using banker flow signals

- Exit remaining position when:

- Oscillator crosses zero line in opposite direction

- Opposing signal appears

- Price closes below/above trailing stop level

3. Maximum holding period:

- 20 trading days for trend-following trades

- 10 trading days for counter-trend trades

- Re-evaluate if targets not reached within timeframe

#### Risk Management Safeguards

1. Maximum open positions: 5 trades

2. Maximum sector exposure: 40% of trading capital

3. Maximum daily drawdown limit: 3% of trading capital

4. Mandatory stop trading rules:

- After three consecutive losing trades

- After reaching 5% account drawdown

- Resume after two-day cooling period and strategy review

#### Performance Tracking

1. Track for each trade:

- Signal type that triggered entry

- Oscillator reading at entry and exit

- Volume relative to average

- Price action confirmation patterns

- Holding period

- Reward-to-risk achieved

2. Review performance metrics weekly:

- Win rate by signal type

- Average reward-to-risk ratio

- Profit factor

- Maximum drawdown

3. Adjust strategy parameters based on performance:

- Increase position size for highest performing signals

- Decrease or eliminate trades based on underperforming signals

## Advanced Usage Tips

1. Combine with Support/Resistance:

- Signals are more reliable when they occur at key support/resistance levels

- Look for banker flow divergence at major price levels

2. Multiple Timeframe Analysis:

- Use the oscillator on both daily and weekly timeframes

- Stronger signals when both timeframes align

- Enter on shorter timeframe when confirmed by longer timeframe

3. Sector Rotation Strategy:

- Compare banker flow across different sectors

- Rotate capital to sectors showing strongest positive flow

- Avoid sectors with persistent negative flow

4. Volatility Adjustments:

- During high volatility periods, wait for Strong signals only

- During low volatility periods, Early signals can be more actionable

5. Optimizing Parameters:

- For more volatile stocks: Increase Smoothing Length (6-8)

- For less volatile stocks: Decrease KLSE Sensitivity (1.2-1.5)

- For intraday trading: Reduce all length parameters by 30-50%

## Fine-Tuning for Different Markets

While optimized for KLSE, the indicator can be adapted for other markets:

1. For US Stocks:

- Reduce KLSE Sensitivity to 1.5

- Increase Volume Filter to 75%

- Adjust Strong Signal Level to 18

2. For Forex:

- Increase Smoothing Length to 8

- Reduce Early Signal Threshold to 0.6

- Focus more on divergence signals than crossovers

3. For Cryptocurrencies:

- Increase KLSE Sensitivity to 2.2

- Reduce Signal Levels (Strong: 12, Early: 8)

- Use higher Volume Filter (80%)

By thoroughly understanding and properly implementing the Enhanced KLSE Banker Flow Oscillator, traders can gain a significant edge in identifying institutional money flow and making more informed trading decisions, particularly in the Malaysian stock market.

Average Daily Range ProjectionsCreates a trailing high and low projection based on the Average Daily Range.

Track the Session High and Low to determine the Daily Range.

Average the Daily Range by a fixed Period to create an Average Daily Range .

Track the Prior Daily Range .

Track the Current Daily Range .

Track the % of Range completion relative to the CDR & ADR(P).

From the Session Low, project an Average Daily Range High by adding the ADR.

From the Session High, project an Average Daily Range Low by subtracting the ADR.

When %R reaches 100% or greater, the ADR HI & LO will lock, showing the range break out or break down. As the Session High and Low create the Daily Range, observe the reaction of price as it reaches the limit of the expected daily range.

On strongly trending days, CDR is likely greater than PDR and ADR(P). Price can break away.

On ranging days, %R may fail to reach 100% and CDR may be lesser than PDR and ADR(P). Price can bounce around within the bounds of ADR HI & LO.

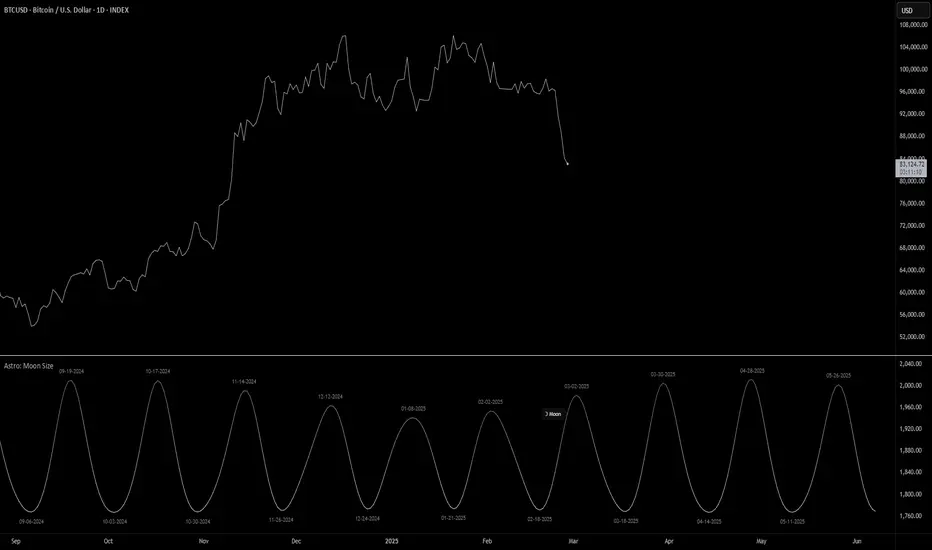

Astro: Moon SizeThe Astro: Moon Size indicator, built using AstroLib , calculates the distance and visualizes the apparent size of the Moon based on astronomical positioning. This script is tailored for the 1D timeframe and provides insights into lunar perigees (closest approach) and apogees (farthest distance), making it useful for astrologically-informed trading strategies.

New Astro Indicators Feature:

By setting the Julian Date to X number of days in the future, and offsetting the plot by X number of bars accordingly, it is now possible to visualize future projections of TradingView indicators that reference the AstroLib . This feature has been long requested and is far overdue, so thank you to everyone who pushed for this feature release. Enjoy, time travelers from the future!!

Key Features:

Moon Size Calculation: Uses Julian Date (J2000) conversion and AstroLib functions to determine the Moon's apparent distance.

Future Projection: Displays the Moon's distance from 28 up to 500 days ahead, with color gradients indicating proximity/size.

Pivot Identification: Marks local maxima (apogees) and minima (perigees) with labeled date stamps for easy reference.

Dynamic Labeling: Adapts label positioning and size based on the Moon's current trend and relative size.

Usage Notes:

⚠️ Timeframe Restriction: For now, the script only functions on the 1D timeframe and will prompt an error otherwise.

⚠️ Asset Restriction: This script is meant to be loaded on charts for assets that trade 24/7, like BTCUSD historical index.

Mr. Laz's Fibonacci MASmoothed Fibonacci Moving Average

This indicator plots six Fibonacci retracement levels overlaid on the chart, with each level smoothly adjusted using an Exponential Moving Average (EMA). The Fibonacci levels are calculated based on the highest high and lowest low over a user-defined period, and they represent key support and resistance zones that traders often watch for price reversals.

The six Fibonacci retracement levels plotted are:

0% (Fib 0): Top level (representing the highest point in the range).

23.6% (Fib 23.6%)

38.2% (Fib 38.2%)

50% (Fib 50%)

61.8% (Fib 61.8%)

100% (Fib 100): Bottom level (representing the lowest point in the range).

These levels are smoothed using a user-defined Smoothing Length, which helps reduce the "zig-zag" nature of the lines and provides a more gradual, smoother appearance as they follow the price movement. The indicator allows you to adjust the smoothing factor to control how sensitive the lines are to price changes.

The colors of the Fibonacci levels are customizable and are plotted from top to bottom as:

Red (for Fib 100%)

Green (for Fib 23.6%)

Orange (for Fib 38.2%)

White (for Fib 50%)

Blue (for Fib 61.8%)

Purple (for Fib 0%)

This indicator is useful for identifying key support and resistance zones based on Fibonacci retracement levels, with the added benefit of smoothing to make the lines more visually appealing and less prone to sudden shifts.

Global Liquidity Indicator in USDThis indicator aggregates the total central bank balance sheets and M2 money supply for the USA, Canada, China, European Union, Japan, and the UK, converting all values to USD and normalizing them to trillions for easy visualization. It plots three lines: Total Balance Sheet, Total M2, and Combined Total, providing a comprehensive view of global liquidity trends.

Key Features:

Dynamic Coloring: Customize line colors based on direction—green for upward trends, red for downward (or any colors you choose), with independent on/off toggles for each line.

Real-Time Currency Conversion: Uses live forex rates (e.g., USD/CNY, USD/EUR) for accurate USD conversions.

Cumulative Price Change AlertCumulative Price Change Alert

Version: 1.0

Author: QCodeTrader 🚀

Overview 🔍

The Cumulative Price Change Alert indicator analyzes the percentage change between the current and previous open prices and sums these changes over a user-defined number of bars. It then generates visual buy and sell signals using arrows and labels on the chart, helping traders spot cumulative price momentum and potential trading opportunities.

Key Features ⚙️

Customizable Timeframe 🕒:

Use a custom timeframe or default to the chart's timeframe for price data.

User-Defined Summation 🔢:

Specify the number of bars to sum, allowing you to analyze cumulative price changes.

Custom Buy & Sell Conditions 🔔:

Set individual percentage change thresholds and cumulative sum thresholds to tailor signals for

your strategy.

Visual Alerts 🚀:

Displays green upward arrows for buy signals and red downward arrows for sell signals directly

on the chart.

Informative Labels 📝:

Provides labels with formatted percentage change and cumulative sum details for the analyzed

bars.

Versatile Application 📊:

Suitable for stocks, forex, crypto, commodities, and more.

How It Works ⚡

Price Change Calculation ➗:

The indicator calculates the percentage change between the current bar's open price and the

previous bar's open price.

Cumulative Sum ➕:

It then sums these percentage changes over the last N bars (as specified by the user).

Signal Generation 🚦:

Buy Signal 🟢: When both the individual percentage change and the cumulative sum exceed

their respective buy thresholds, a green arrow and label are displayed.

Sell Signal 🔴: Conversely, if the individual change and cumulative sum fall below the sell

thresholds, a red arrow and label are shown.

How to Use 💡

Add the Indicator ➕:

Apply the indicator to your chart.

Customize Settings ⚙️:

Set a custom timeframe if desired.

Define the number of bars to sum.

Adjust the buy/sell percentage change and cumulative sum thresholds to match your trading

strategy.

Interpret Visual Cues 👀:

Monitor the chart for green or red arrows and corresponding labels that signal potential buy or

sell opportunities based on cumulative price movements.

Settings Explained 🛠️

Custom Timeframe:

Select an alternative timeframe for analysis, or leave empty to use the current chart's timeframe.

Number of Last Bars to Sum:

Determines how many bars are used to compute the cumulative percentage change.

Buy Condition - Min % Change:

The minimum individual percentage change required to consider a buy signal.

Buy Condition - Min Sum of Bars:

The minimum cumulative percentage change over the defined bars needed for a buy signal.

Sell Condition - Max % Change:

The maximum individual percentage change threshold for a sell signal.

Sell Condition - Max Sum of Bars:

The maximum cumulative percentage change over the defined bars for triggering a sell signal.

Best Use Cases 🎯

Momentum Identification 📈:

Quickly spot strong cumulative price movements and momentum shifts.

Entry/Exit Signals 🚪:

Use the visual signals to determine potential entry and exit points in your trading.

Versatile Strategy Application 🔄:

Effective for scalping, swing trading, and longer-term analysis across various markets.

UPD: uncheck labels for better performance