for your comparison: Global M2 Money Supply // Days Offset =📈 Global M2 Money Supply Overlay – Offset Adjustable

This script plots an aggregated, FX-adjusted global M2 money supply index directly on your TradingView chart. It pulls M2 data from multiple global regions—including North America, Europe, Asia, Latin America, and more—and normalizes it for comparison in USD terms.

You can apply a custom time offset to the M2 line using the settings, allowing you to test potential leading or lagging correlations between global liquidity and market price action (e.g., Bitcoin, equities, commodities).

💡 Ideal for macro traders, long-term investors, and anyone interested in liquidity-driven market behavior.

Features:

Combines M2 data from 20+ countries and currency zones

FX-adjusted for consistency in USD terms

Offset slider to shift M2 data forward or backward in time

Scaled to trillions for readability

Plots directly on the main chart for visual comparison

基本面分析

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + Order Blocks + Fibonacci OTE Levels

A High-Probability Entry Engine for Smart Money Concept Traders

This script combines three powerful Smart Money Concepts (SMC) into a single tool: Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

It’s designed to simplify SMC trading by highlighting confluence zones where price is likely to reverse or continue — with clear visual zones, entry arrows, and take profit projections.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies when price sweeps above/below the highest high or lowest low within a user-defined lookback period and closes back inside.

Plots orange labels on the chart to signal potential liquidity events (LG-H / LG-L).

Plots Order Blocks After Liquidity Grabs

After a liquidity grab, the script looks for displacement candles (strong bullish or bearish moves) and draws highlighted OB zones extending several bars to the right.

These zones represent potential institutional footprints for price reversals.

Draws Fibonacci OTE Levels (Optimal Trade Entry)

Uses recent swing high and low pivots to automatically calculate OTE zones (default: 62% and 75% retracement levels).

Draws these retracement zones for both bullish and bearish setups.

Marks Valid OTE Entry Zones

Buy/Sell zones only trigger when:

A liquidity grab occurs,

Price enters the OTE zone,

And a strong confirming candle is present.

Plots green/red arrows for valid buy/sell OTE entries.

Auto-Draws Take Profit Zones

TP1 = Previous swing high/low

TP2 = Risk-based R-multiplied extension (e.g., 1.5R — customizable)

Alerts

Triggers alerts when valid buy or sell OTE setups are detected.

⚙️ Customization Features:

Toggle each feature: Liquidity Grabs, Order Blocks, Fibonacci OTE levels

Set Fibonacci retracement percentages (e.g., 0.62 / 0.75)

Adjust lookback window for liquidity detection

Customize the take-profit multiplier (R-based)

Full control over visuals: colors, labels, and lines

💡 How to Use:

Use this script to scan for high-confluence trade setups based on Smart Money principles.

Combine with session timing (e.g., New York open), major swing structure, or Kill Zone windows for maximum edge.

Look for arrows inside OB zones or OTE levels following liquidity sweeps for cleaner entries.

🔗 Works Best With:

✅ First FVG — Opening Range Fair Value Gap Detector: Identify early inefficiencies to set the narrative for the day.

✅ Liquidity Levels — Smart Swing Lows: Spot key structural lows that can fuel stop hunts and reversals.

✅ ICT Turtle Soup — Liquidity Reversal: Add a classic reversal pattern to your toolkit to catch fakeouts cleanly.

Together, these tools build a complete Smart Money ecosystem for entry precision, risk management, and price behavior forecasting.

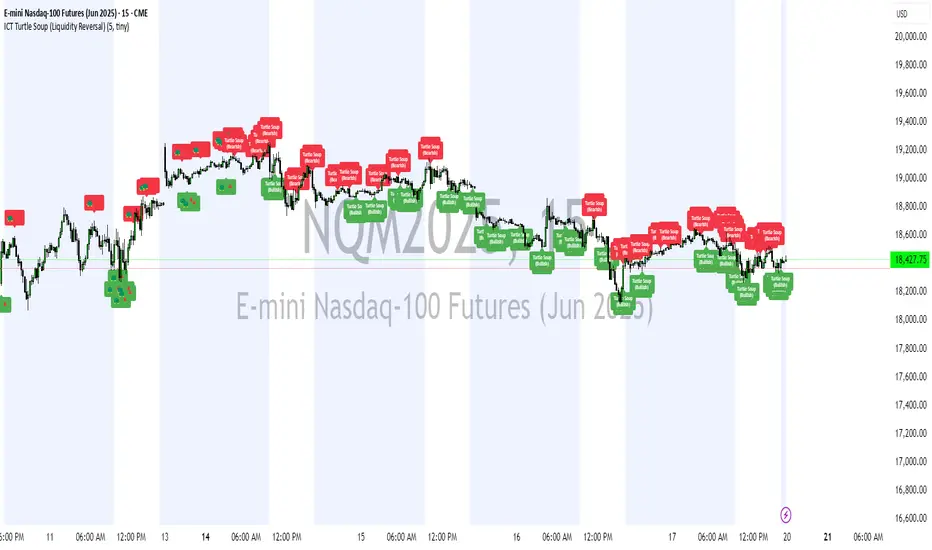

ICT Turtle Soup (Liquidity Reversal)ICT Turtle Soup — Liquidity Reversal Detection

Trap the Trap: A Precision Reversal Strategy from the Inner Circle Trader Playbook

This indicator implements the Turtle Soup liquidity reversal setup — a widely used ICT (Inner Circle Trader) concept that targets false breakouts beyond recent swing highs or lows. These patterns typically occur when price grabs liquidity above or below a known level, then snaps back, trapping retail traders and creating a high-probability reversal scenario.

🔍 What This Script Does:

Detects Liquidity Sweeps Above/Below Key Swing Levels

Uses a customizable swing lookback to identify recent swing highs and lows.

Triggers a Bearish Turtle Soup when price runs above a previous swing high and closes back below.

Triggers a Bullish Turtle Soup when price sweeps below a prior swing low and closes back above.

Plots Clear Visual Signals

Reversal signals appear as 🐢🔻 (Bearish) or 🐢🔺 (Bullish) markers directly on your chart.

Optional labels can be enabled for enhanced journaling and review.

Real-Time Alerts

Receive alert notifications when a Turtle Soup setup is detected — ideal for scalpers or intraday traders watching for reversals around liquidity pools.

⚙️ Customization Options:

Set the swing lookback sensitivity (default: 5)

Enable or disable labels

Choose label font size

Customize colors for bullish and bearish signals

💡 How to Use:

Deploy on intraday timeframes (e.g. 5m–15m) for high-resolution liquidity analysis.

Watch for signals at key highs/lows, session extremes, or zones where liquidity is likely resting.

Combine with tools like FVGs, Order Blocks, and OTE zones for layered confirmation.

🔗 Combine With These Tools for a Complete SMC Edge:

✅ First FVG — Opening Range Fair Value Gap Detector

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

✅ Liquidity Levels — Smart Swing Lows

Together, these tools form a high-precision Smart Money toolkit — helping traders map, anticipate, and act on institutional-level liquidity events with clarity and confidence.

ICT Turtle Soup Ultimate V2📜 ICT Turtle Soup Ultimate V2 — Advanced Liquidity Reversal System

Overview:

The ICT Turtle Soup Ultimate V2 is a next-generation liquidity reversal indicator built on the principles of smart money concepts (SMC) and the classic ICT Turtle Soup setup. It is designed to detect false breakouts (liquidity grabs) at key swing points, enhanced by proprietary logic that filters out low-quality signals using a combination of trend context, kill zone timing, candle wick behavior, and multi-timeframe imbalance zones.

This tool is ideal for intraday traders seeking high-probability entry signals near liquidity pools and imbalance zones — where smart money makes its move.

🔍 What This Script Does

🧠 Liquidity Grab Detection (Turtle Soup Core Logic)

The script scans for recent swing highs/lows using a user-defined lookback.

A signal is generated when price breaks above/below a previous swing level but closes back inside — indicating a liquidity run and likely reversal.

A special Wick Trap Mode enhances this logic by detecting long-wick fakeouts — where the wick grabs stops but the candle body closes opposite the breakout direction.

📉 Trend Filter with ATR Buffer

Optional trend filter uses a simple moving average (SMA) to gauge market direction.

Instead of hard filtering, it applies an ATR-based buffer to allow for entries near the trend line, reducing signal suppression from micro-fluctuations.

🕰️ Kill Zone Session Filtering

Only show signals during institutional trading hours:

London Session

New York AM

Or any custom user-defined session

Helps traders avoid low-volume hours and focus on where stop hunts and price expansions typically occur.

🧱 Multi-Timeframe FVG Confluence (Optional)

Signal validation is strengthened by checking if price is within a higher timeframe Fair Value Gap — commonly used to identify imbalances or inefficiencies.

Filters out setups that lack underlying displacement or order flow justification.

🎨 Visual Feedback

Plots 🔺 bullish and 🔻 bearish markers at signal candles.

Optionally displays:

Swing High/Low Labels (SH / SL)

Reversal distance labels

Background color shading on valid signals

Includes built-in alerts for automated trade notification.

🔑 Unique Benefits

Wick Trap Detection: A proprietary approach to detecting stop hunts via wick behavior, not just candle closes.

ATR-based trend filtering: Avoids unnecessary filtering while still maintaining directional bias.

All-in-one system: No need to stack multiple indicators — swing detection, reversal logic, session filtering, and imbalance confirmation are all integrated.

💡 How to Use

Enable Wick Trap Mode to detect stealthy liquidity grabs with strong wicks.

Use Kill Zone filters to trade only when institutions are active.

Optionally enable FVG confluence to improve confidence in reversal zones.

Watch for Bullish signals near SL levels and Bearish signals near SH levels.

Combine with your own execution strategy or other SMC tools for optimal results.

🔗 Best Used With:

Maximize your edge by combining this script with complementary SMC-based tools:

✅ First FVG — Opening Range Fair Value Gap Detector

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

✅ Liquidity Levels — Smart Swing Highs and Lows with horizontal line projections

ICT Turtle Soup (Liquidity Reversal)ICT Turtle Soup — Liquidity Reversal Detection

Classic Liquidity Trap Reversal Strategy for Smart Money Traders

This indicator implements the ICT Turtle Soup concept — a classic liquidity-based reversal pattern — which occurs when price runs above or below a recent swing level to grab liquidity, then sharply reverses. This pattern is commonly used in Smart Money Concepts (SMC) and Inner Circle Trader (ICT) strategies to anticipate false breakouts and high-probability reversals.

🔍 What This Script Does:

Identifies Swing Highs & Lows

Detects recent swing highs and lows using a customizable lookback period.

Tracks Liquidity Grabs

A bearish Turtle Soup setup is triggered when price breaks above a recent swing high but closes back below it.

A bullish Turtle Soup setup is triggered when price breaks below a recent swing low but closes back above it.

These conditions often signal liquidity traps, where price sweeps resting orders before reversing.

Plots Signals Directly on the Chart

Turtle Soup setups are marked with 🐢🔻 (bearish) and 🐢🔺 (bullish) labels.

Optional full-text labels can also be displayed for clarity and journaling.

Includes Alert Conditions

Alerts can be enabled to notify you of bullish or bearish Turtle Soup reversals in real-time.

⚙️ Customization Features:

Adjustable swing lookback period

Enable/disable Turtle Soup labels

Set label font size

Choose your preferred bullish/bearish signal colors

💡 How to Use:

Add this script to your chart (ideally on intraday timeframes such as 5m–15m).

Wait for a Turtle Soup signal near a key swing high/low or liquidity zone.

Combine with other confirmation tools (e.g., FVGs, Order Blocks, OTE) for stronger setups.

Use alerts to stay ahead of fast-moving reversals.

🧠 Why It Works:

Turtle Soup setups are rooted in liquidity theory — they exploit the market’s tendency to sweep obvious swing levels before reversing. These moves often trap retail traders and mark the beginning of Smart Money entries.

🔗 Best Used With:

Maximize the edge by combining this with other SMC tools:

✅ First FVG — Opening Range Fair Value Gap Detector

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

✅ Liquidity Levels — Smart Swing Lows

Together, they create a complete ecosystem for identifying, confirming, and executing liquidity-driven trade setups with precision.

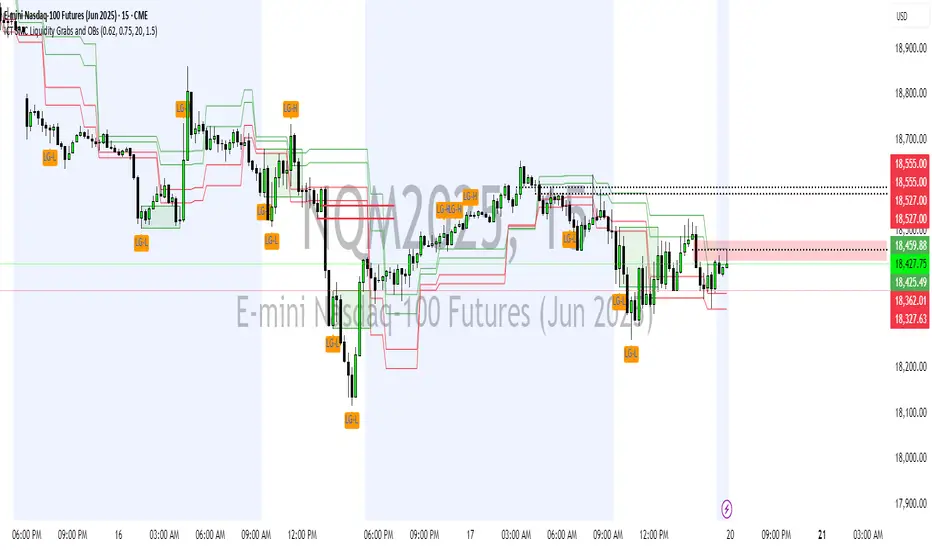

Liquidity Levels (Smart Swing Lows)Liquidity Levels — Smart Swing Low Detection

Efficient Liquidity Sweep Visualization for Smart Money Traders

This script automatically identifies and plots liquidity-rich swing lows based on pivot logic, filters them to remove redundant levels, and overlays daily highs/lows for added context — giving Smart Money Concept (SMC) traders a clean, actionable map of liquidity.

It’s designed to be minimal yet powerful: perfect for spotting potential liquidity grabs, mitigation zones, and sweep targets with zero chart clutter.

🔍 What This Script Does:

Detects Smart Swing Lows

Uses fixed pivot detection (left = 3, right = customizable) to identify structurally significant swing lows.

Filters out swing lows that are too close together using a percentage-based spacing threshold to reduce noise.

Mitigation Cleanup Logic

Tracks whether recent price action breaches past swing lows.

If breached, the swing level is automatically removed, keeping only relevant, unmitigated liquidity levels on your chart.

Plots Daily Highs and Lows

Each new trading day, horizontal rays mark the prior day’s high and low — useful for identifying resting liquidity and possible sweep zones.

Labeling and Style Customization

Optional labels for swing lows.

Full control over label size, color, and visibility to match any chart aesthetic.

Timeframe Filtering

Runs exclusively on 5m, 10m, and 15m charts to ensure optimal reliability and signal clarity.

⚙️ Customization Features:

Pivot sensitivity (Right side control)

Minimum distance between swing lows (in %)

Label visibility, size, and color

Line width and colors for both swing levels and daily highs/lows

Mitigation cleanup lookback length

💡 How to Use:

Add the script to a qualifying intraday chart (5–15m).

Use the swing low levels to monitor liquidity-rich zones.

Combine with your personal strategy to identify liquidity grabs, potential reversal zones, or entry points following a sweep.

Let the built-in cleanup logic remove any already-mitigated levels so you can focus on active targets.

🚀 What Makes It Unique:

This isn’t just another pivot plotter — it’s a smart, self-cleaning SMC tool designed for modern liquidity-based trading strategies.

A must-have for traders using concepts like liquidity grabs, mitigation blocks, or sweep-to-reverse trade models.

🔗 Best used in combination with:

✅ First FVG — Opening Range Fair Value Gap Detector: Pinpoint the day’s first imbalance zone for intraday setups.

✅ ICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels: Confluence-based entries powered by liquidity logic, order blocks, and premium/discount zones.

Used together, these scripts form a complete Smart Money toolkit — helping you build high-probability setups with confidence, clarity, and clean charts.

First FVG Custom Time RangeFirst FVG — Opening Range Fair Value Gap Detector

Smart Money Opening Imbalance Strategy Tool

This script automatically detects and highlights the first Fair Value Gap (FVG) that forms between 9:30 and 10:00 AM Eastern Time (New York session open) — a critical period often referred to as the Opening Range. It’s designed for Smart Money traders looking to isolate early-morning inefficiencies that may influence market behavior throughout the trading day.

🔍 What This Script Does:

Automatically Detects the First FVG in the Opening Range

Scans price action between 9:30 and 10:00 AM ET and identifies the first valid bullish or bearish FVG that forms.

Only one FVG is shown per day — ensuring a clean, focused view.

Draws a Visual Zone

Once detected, the FVG zone is extended forward on the chart (customizable duration).

A labeled zone helps users track how price reacts to it throughout the session.

Optional Retest Alerts

Alerts you when price re-enters the zone — a potential reaction point used by SMC traders.

Customization Options

Set your preferred session time window

Adjust zone duration (in bars)

Customize label font size, colors, and visibility

Enable/disable alert on retest

📈 Why the First FVG Matters:

Time-Sensitive Setup: The first FVG typically forms no earlier than 9:31 AM ET and represents a potential “time distortion” or imbalance zone created by aggressive market participants during the open.

Behavioral Study: Many traders journal how price behaves around this zone each day — whether it acts as support, resistance, or gets traded through later in the session.

Predictive Value: Observing how this zone is respected or broken can provide anticipatory insight into intraday price action, rather than reactive analysis.

Great for New Traders: This opening FVG is often recommended as a starting reference point for building trade models and understanding how institutional imbalances unfold.

🚀 What Makes It Unique:

This tool doesn’t spam your chart with every FVG. It laser-focuses on a single, time-bound zone backed by institutional logic — the first presented imbalance of the day during the opening range.

Use it to:

Monitor price behavior around early inefficiencies

Plan journal entries and pattern recognition

Align intraday setups with a high-probability SMC model

Whether you’re scalping, journaling market structure, or refining entries based on liquidity behavior — this script helps you make the first 30 minutes count.

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

Smart Money Concepts Trading Assistant

This script is built for traders who follow ICT (Inner Circle Trader) and Smart Money Concepts. It intelligently combines three critical components of SMC trading: Liquidity Grabs, Order Blocks, and Fibonacci-based Optimal Trade Entry (OTE) zones — giving traders visual cues for potential high-probability reversals and entry points.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies swing highs/lows where price sweeps liquidity, then immediately reverses.

Labels them with orange markers when price takes out previous highs/lows but closes back inside.

Draws Order Blocks

After a liquidity grab, the script looks for strong bullish or bearish candles and automatically highlights the OB zone.

These OB zones are visualized with transparent colored boxes extending several bars forward.

Plots Fibonacci OTE Levels

Uses recent swing high/low pivots to dynamically draw customizable OTE retracement levels (e.g., 62% and 75%) for both long and short setups.

Highlights Optimal Entry Zones

Marks valid OTE-based buy/sell opportunities only when:

Liquidity has been taken,

Price enters the OTE zone,

And a strong confirming candle appears.

Adds visual zones, trade labels, and optional alerts for each qualified entry.

Includes Take Profit Targets

Automatically calculates take-profit levels based on previous structure and risk-reward ratios.

TP1 is the previous swing, and TP2 is an extended R-multiple (customizable by user).

⚙️ Customization Options:

Toggle each feature (Liquidity Grabs, OBs, Fibonacci Levels)

Adjust Fibonacci levels (default: 62% and 75%)

Set lookback period for liquidity checks

Customize the R-multiple for TP2 levels

💡 How to Use:

Enable desired features from the input panel.

Watch for Buy/Sell OTE zones highlighted in green/red.

Confirm with liquidity sweep and OB support for stronger signals.

Use the automatically generated TP levels to manage risk.

🚀 What Makes It Unique:

Unlike other open-source mashups, this script synchronizes multiple SMC concepts into a single tool that:

Waits for high-confidence conditions (not just blind fib or OB detection)

Validates entries using multiple confluences

Visually marks actionable setups

Automates trade management zones

Whether you're trend-trading, scalping, or swing trading ICT-style, this tool offers a streamlined, smart-money-aligned workflow directly on your chart.

ICT SMC Liquidity Grabs and OBsICT SMC Liquidity Grabs + OB + Fibonacci OTE Levels

Smart Money Concepts Trading Assistant

This script is built for traders who follow ICT (Inner Circle Trader) and Smart Money Concepts. It intelligently combines three critical components of SMC trading: Liquidity Grabs, Order Blocks, and Fibonacci-based Optimal Trade Entry (OTE) zones — giving traders visual cues for potential high-probability reversals and entry points.

🔍 What This Script Does:

Detects Liquidity Grabs

Identifies swing highs/lows where price sweeps liquidity, then immediately reverses.

Labels them with orange markers when price takes out previous highs/lows but closes back inside.

Draws Order Blocks

After a liquidity grab, the script looks for strong bullish or bearish candles and automatically highlights the OB zone.

These OB zones are visualized with transparent colored boxes extending several bars forward.

Plots Fibonacci OTE Levels

Uses recent swing high/low pivots to dynamically draw customizable OTE retracement levels (e.g., 62% and 75%) for both long and short setups.

Highlights Optimal Entry Zones

Marks valid OTE-based buy/sell opportunities only when:

Liquidity has been taken,

Price enters the OTE zone,

And a strong confirming candle appears.

Adds visual zones, trade labels, and optional alerts for each qualified entry.

Includes Take Profit Targets

Automatically calculates take-profit levels based on previous structure and risk-reward ratios.

TP1 is the previous swing, and TP2 is an extended R-multiple (customizable by user).

⚙️ Customization Options:

Toggle each feature (Liquidity Grabs, OBs, Fibonacci Levels)

Adjust Fibonacci levels (default: 62% and 75%)

Set lookback period for liquidity checks

Customize the R-multiple for TP2 levels

💡 How to Use:

Enable desired features from the input panel.

Watch for Buy/Sell OTE zones highlighted in green/red.

Confirm with liquidity sweep and OB support for stronger signals.

Use the automatically generated TP levels to manage risk.

🚀 What Makes It Unique:

Unlike other open-source mashups, this script synchronizes multiple SMC concepts into a single tool that:

Waits for high-confidence conditions (not just blind fib or OB detection)

Validates entries using multiple confluences

Visually marks actionable setups

Automates trade management zones

Whether you're trend-trading, scalping, or swing trading ICT-style, this tool offers a streamlined, smart-money-aligned workflow directly on your chart.

SPDR Sectors TableThis script generates an interactive and customizable SPDR Sectors Table designed to monitor and analyze the performance of the 11 main sectors of the S&P 500 via sector-specific ETFs. It offers a dynamic overview of daily or periodic sector movements, making it a valuable tool for traders, analysts, and investors implementing sector rotation strategies.

█ DEFINITIONS

SPDR Sectors ETFs are exchange-traded funds managed by State Street Global Advisors, which divide the S&P 500 into the following 11 sectors:

- Communication Services (XLC)

- Consumer Discretionary (XLY)

- Consumer Staples (XLP)

- Energy (XLE)

- Financials (XLF)

- Health Care (XLV)

- Industrials (XLI)

- Materials (XLB)

- Real Estate (XLRE)

- Technology (XLK)

- Utilities (XLU)

These ETFs aim to replicate the performance of their respective sectors as defined by the Global Industry Classification Standard (GICS). The funds are periodically rebalanced to match changes in the S&P 500 composition, offering an accurate snapshot of sectoral trends.

█ INDICATOR

The table displays each sector's ticker and full name, following official GICS terminology and SPDR color coding. It also shows percentage performance, calculated daily on intraday charts or based on the selected time frame.

Users can sort the table by either percentage performance or the relative weight of each ETF in the S&P 500. The default weight values reflect data updated as of 17 April 2025, and can be manually adjusted based on the most recent sector weightings available on the official SPDR website.

MÈGAS ALGO : CNA (Cognitio Analysis) [INDICATOR]Overview

The CNA (Cognitio Analysis) is a comprehensive financial analysis tool designed to evaluate the overall health and potential of a market or company based on fundamental metrics. It aggregates data across five key metric groups—**Growth**, **Profitability**, **Cash Flow**, **Income**, and **Valuation**—to provide a final interpretation of market conditions. The indicator dynamically adapts to the selected fiscal period (Quarter, Year, or Trailing Twelve Months) and delivers insights into dominant trends and conflicting signals.

Key Features

1. Customizable Fiscal Period:

- Users can select between "Quarter", "Year", or "Trailing Twelve Months" (TTM) to analyze data for their desired timeframe.

2. Dynamic Table Visualization:

- Displays raw metric values, aggregated scores, and the final interpretation in an intuitive

table.

- Highlights the final interpretation with dynamic background colors (`color.teal` for bullish,

`color.red` for bearish, etc.).

3. Comprehensive Data Integration:

- Pulls financial data using TradingView's `request.financial()` function for metrics like

revenue, earnings, margins, and valuation ratios.

4. Normalization and Scoring:

- Normalizes data to create a consistent scoring system, ensuring accurate comparisons across

metrics.

How It Works

1. Metric Group Analysis

- Growth Metrics: Measures revenue growth, earnings per share (EPS) growth, and tax

efficiency.

- Profitability Metrics: Analyzes net profit margin, return on equity (ROE), and EBITDA margin.

- Cash Metrics: Assesses operating cash flow margin, free cash flow to operating cash flow

ratio, and cash flow coverage.

- Income Metrics: Examines gross profit margin, operating profit margin, and EBIT margin.

- Valuation Metrics: Evaluates price-to-earnings (P/E), price-to-sales (P/S), and enterprise

value-to-EBITDA (EV/EBITDA).

2. Dynamic Scoring System

- Metrics are normalized to ensure consistency across different scales.

- A geometric mean is used to calculate scores for each metric group, ensuring that all metrics

within a group contribute equally to the final score.

3. Dominant Trend Identification

- Scores from all five metric groups are aggregated to determine the **dominant trend** of the

market.

- The dominant trend is categorized as:

- Bullish: Strong fundamentals across most metrics.

- Bearish: Weak fundamentals across most metrics.

- Neutral: Balanced conditions with no clear direction.

- Unclear: Mixed signals dominate, requiring further monitoring.

4. Conflicting Signals Interpretation

- The indicator identifies scenarios where metrics conflict (e.g., high growth but low valuation).

- These conflicting signals provide nuanced insights into market conditions, highlighting rare opportunities or potential risks.

How to Use the Indicator

1. Select Fiscal Period:

- Choose between "FQ", "FY", or "TTM" to analyze data for the desired timeframe.

2. Review Metric Scores:

- Examine the scores for each metric group (Growth, Profitability, Cash, Income, Valuation) to

understand the underlying performance.

3. Interpret Final Output:

- The final interpretation provides a summary of the dominant trend and conflicting signals,

helping users make informed decisions.

4. Dynamic Coloring:

- Use the dynamic background colors in the table to quickly identify market sentiment

(bullish, bearish, neutral, or mixed).

Applications

- Identifying Opportunities:

- Look for bullish dominant trends combined with undervalued growth opportunities for

potential long positions.

- Avoiding Risks:

- Watch out for bearish dominant trends with overvaluation alerts to avoid potential losses.

- Monitoring Neutral Markets:

- Use the indicator to identify neutral markets and wait for clearer signals before making

decisions.

Conclusion

The CNA (Cognitio Analysis) is a powerful tool for traders and investors seeking to make informed decisions based on fundamental analysis. By combining detailed metric evaluations, dynamic scoring, and sentiment-based interpretations, this indicator provides a comprehensive view of market conditions. Whether you're identifying undervalued opportunities, avoiding overvalued risks, or monitoring neutral markets, this indicator equips you with the insights needed to navigate complex financial landscapes.

Please Note:

This indicator is provided for informational and educational purposes only. It is not financial advice, and it should not be considered a recommendation to buy, sell, or trade any financial instrument. Trading involves significant risks, including the potential loss of your entire investment. Always conduct your own research and consult with a licensed financial advisor before making any trading decisions.

The results and images provided are based on algorithms and historical/paid real-time market data but do not guarantee future results or accuracy. Use this tool at your own risk, and understand that past performance is not indicative of future outc

MACD Liquidity Tracker SystemMACD Liquidity Tracker System

🔹 Enhanced MACD with candle coloring, entry markers, and customizable signal logic.

🧠 Features:

This tool combines a color-coded MACD histogram with signal-based candle colors and small shape markers (🔼🔽) for clear market momentum and entry visualization.

📊 Visuals:

MACD Histogram (Sub-panel):

4 dynamic colors to show momentum direction:

🔹 Bright Blue = MACD > 0 & rising (strong bullish)

🔹 Dark Blue = MACD > 0 & falling (weakening bullish)

🔹 Bright Magenta = MACD < 0 & falling (strong bearish)

🔹 Dark Magenta = MACD < 0 & rising (weakening bearish)

Price Candles (Main Chart):

🔹 Bright Blue = Active Long signal

🔹 Bright Magenta = Active Short signal

Entry Markers:

🔼 Blue triangle (below candle) = Start of Long

🔽 Magenta triangle (above candle) = Start of Short

⚙️ System Types (select in settings):

Normal:

🔹 Long = MACD > 0

🔹 Short = MACD < 0

Fast: (Based on histogram color)

🔹 Long = Bright Blue OR Dark Magenta

🔹 Short = Dark Blue OR Bright Magenta

Safe:

🔹 Long = Only Bright Blue

🔹 Short = All other colors

🔔 Alerts:

Alerts trigger only on the first bar of a new Long/Short signal.

Easy to set up using TradingView’s alert system.

📌 How to Use:

Add the indicator to your chart

Open settings and select a System Type

Adjust MACD parameters if needed

Use histogram color + candle color for momentum and signal confirmation

Set alerts for clean entries if desired

💡 Ideal for traders seeking visual clarity and flexible MACD-based strategies.

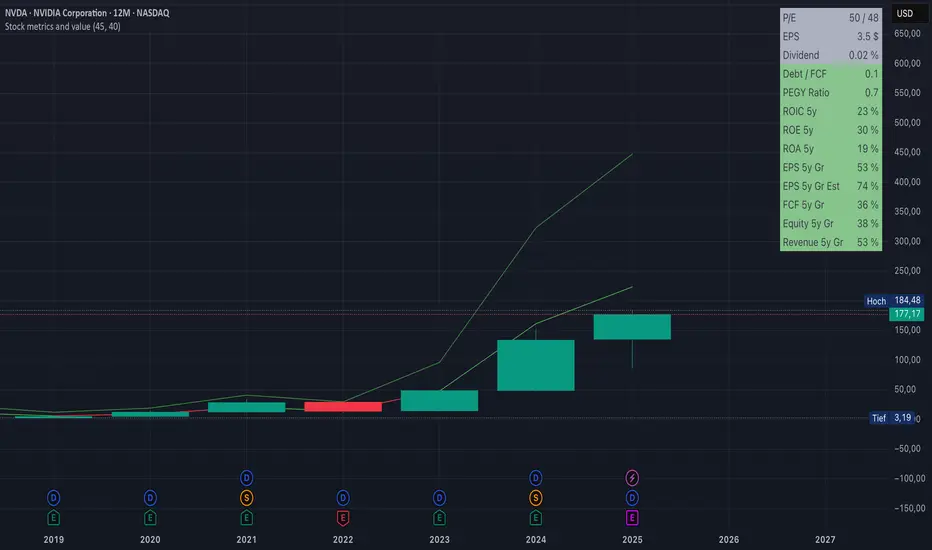

Stock metrics and valueThis indicator shows:

- the valuation metrics for a stock on a table on top right: PE, EPS, dividend, ROIC, ROE, ROA, EPS growth, FCF growth, Equity growth, revenue Growth

- the fair value and the value with 50% margin of safety as chart lines

The lines will be red when they are above the current price and red when they are below the current price.

The colors on the table will be red when the values are below 10% and green when they are above, that means when everything is green the metrics for the stock are good.

Cot DeltaCOT Delta by Jacopo

Designed to visualize and analyze data related to the Commitment of Traders (COT) report, which is published by the Commodity Futures Trading Commission (CFTC) in the United States. Its primary purpose is to display the long and short positions of traders on futures contracts, divided by categories like Commercial, Noncommercial, and Nonreportable.

Main Features:

Selection Mode: The user can choose from several modes to display COT data, such as "Auto", "Root", "Base currency", or "Currency". This determines which currency will be shown on the chart.

Contract Type: It is possible to select whether to display data for Futures, Options, or both (Futures + Options).

COT Category: The user can choose one of the trader categories like Commercial Positions, Noncommercial Positions, or Nonreportable Positions to analyze positions based on the type of market participant.

Data Visualization: The chart shows long, short, and net positions (long - short) with separate lines, using different colors for each type of position:

Long positions in green.

Short positions in red.

Net difference (long - short) in white.

Data Table: A table is displayed to present the data clearly, with the following columns:

Long: Long positions.

Short: Short positions.

Total: The net sum of positions (long - short).

Changes: The difference between current and previous data (delta) in both absolute and percentage terms.

Variation Visualization: The table also shows the variations from the previous period (both in absolute and percentage terms), with conditional background colors to highlight positive or negative changes.

Optional CFTC Code: The user can input a custom CFTC code to analyze specific data, if necessary.

In Summary:

This indicator provides a clear and precise visualization of trader positions (long and short) on futures and options contracts, making it easier to analyze market dynamics related to commercial and non-commercial traders. The combination of a chart and table allows for real-time tracking of position changes.

Buffett Indicator (Wilshire 5000 / GDP)The Buffett Indicator (Wilshire 5000 / GDP) is a macroeconomic metric used to assess whether the U.S. stock market is overvalued or undervalued. It is calculated by dividing the total market capitalization (represented by the Wilshire 5000 Index) by the U.S. Gross Domestic Product (GDP). A value above 1 (or 100%) may indicate an overvalued market, while a value below 1 suggests potential undervaluation. This indicator is best suited for long-term investment analysis.

Gas/Oil SpreadGas/Oil Spread Analyzer with Static Overbought/Oversold Zones

This indicator measures the spread between the actual price of natural gas and its oil-based equivalent, derived from a defined oil/gas ratio. It helps traders identify potential mispricings and mean-reversion opportunities between the two energy commodities.

Key Features:

- Calculates spread: Gas Price – Oil-Based Equivalent Price

- Supports dynamic or static oil/gas ratio

- Plots a smoothed version of the spread (SMA)

- Displays static overbought and oversold zones to highlight extreme deviations

Use Cases:

- Detect overvalued or undervalued gas relative to oil

- Spot potential reversion setups in intermarket trading

- Evaluate energy market dislocations and hedging opportunities

Oil/gas ratio MAOil/Gas Ratio-Based Equivalent Price

This indicator calculates the gas-equivalent price based on the current oil price and a defined oil/gas ratio. It helps identify relative overvaluation or undervaluation of natural gas compared to oil.

Features:

- Choose between a static or dynamic (SMA-based) oil/gas ratio

- Displays the fair value of gas derived from oil prices

- Works with any oil ticker symbol (e.g. BRENT, USOIL, etc.)

Useful for traders analyzing intermarket relationships and looking for relative value signals between energy commodities.

AI-123's BTC vs Gold (Lag Correlation)

DISCLAIMER

I made this indicator with the help of ChatGPT and using what I have learned so far from The Pine Script Mastery Course, LOTS of edits based on what I have learned so far had to be made as well as additions and modifications to my liking thanks to what I have learned so far. I am aware this already exists but I have done my best to make a first ever script/indicator while learning how to properly publish as well, so please bear that in mind.

Overview

This indicator analyzes the correlation between Bitcoin (BTC) and Gold (XAUUSD), with a customizable lag applied to the Gold price, providing insight into the macro relationship between these two assets.

It is designed for traders and investors who want to track how Bitcoin and Gold move in relation to each other, particularly when Gold is lagged by a specific number of days.

Key Features:

BTC and Gold (Lagged) Price Overlay: Display Bitcoin (BTC) and Gold (XAUUSD) prices on the chart, with an adjustable lag applied to the Gold price.

Rolling Correlation Calculation: Measures the correlation between Bitcoin and lagged Gold prices over a customizable lookback period.

Adjustable Lag: The number of days that Gold is lagged relative to Bitcoin is fully customizable (default: 20 days).

Customizable Correlation Length: Allows you to choose the lookback period for the correlation (default: 50 days), providing flexibility for short-term or long-term analysis.

Normalized Plotting: Prices of Bitcoin and Gold are normalized for better visual alignment with the correlation values. BTC is divided by 1000, and Gold by 100.

Correlation Scaling: The correlation value is amplified by 10 for better visual clarity and comparison with price data.

Zero Line: Horizontal line representing a correlation of 0, making it easier to identify positive or negative correlation shifts.

Maximum Correlation Lines: Horizontal lines at +10 and -10 values for extreme correlation scenarios.

Input Settings:

Gold Symbol: Customize the Gold ticker (default: OANDA:XAUUSD).

Bitcoin Symbol: Customize the Bitcoin ticker (default: BINANCE:BTCUSDT).

Lag (in trading days): Adjust the number of trading days to lag the Gold price relative to Bitcoin (default: 20).

Correlation Length (days): Set the number of days over which the rolling correlation is calculated (default: 50).

How to Use:

Price Comparison: The BTC (Spot) and Lagged Gold plots give you a side-by-side visual comparison of the two assets, normalized for clarity.

Correlation Line: The correlation line helps you gauge the strength and direction of the relationship between BTC and lagged Gold. Positive values indicate a strong positive correlation, while negative values indicate a negative correlation.

Visual Analysis: Watch how the correlation shifts with changes in lag and correlation length to identify potential market dynamics between Bitcoin and Gold.

Potential Applications:

Macro Trading: Track how Bitcoin and Gold behave in relation to each other during periods of economic uncertainty or inflation.

Sentiment Analysis: Use the correlation data to understand the sentiment between digital and traditional assets.

Strategic Timing: Identify potential opportunities where Bitcoin and Gold show a strong correlation or diverge based on the lag adjustment.

Understanding Macro Trends/Correlations.

Disclaimer:

This indicator is for informational purposes only. The correlation between Bitcoin and Gold does not guarantee future performance, and users should conduct their own research and use risk management strategies when making trading decisions.

Notes: This script uses historical data, so results may vary across different timeframes.

Customization options allow users to adjust the lag and correlation length to better fit their trading strategy.

Future Enhancements: Additional Correlation Line: A second correlation line for different lengths of lag or different assets.

Color-Coding of Correlation: Future updates may include color-coded correlation strength, visually indicating positive or negative correlation more effectively.

Kimchi premium with BTC gap [BIGTAKER]📊 Kimchi Premium with BTC gap

The BIGTAKER Kimchi Premium Indicator is a real-time tool that accurately tracks and visualizes the price discrepancy (Kimchi Premium) between the Korean KRW markets (Upbit or Bithumb) and global cryptocurrency exchanges.

In addition to displaying the premium on altcoins, it compares the difference against Bitcoin's premium and highlights abnormal divergence through signal alerts and visual cues.

🔧 Key Features

KRW Market Selection

Users can select either Upbit or Bithumb as the reference Korean exchange. Only altcoins listed on the selected exchange will be analyzed and shown.

Multi-Exchange Global Pricing

The global reference price is not fixed to a single exchange like Binance. Instead, the indicator dynamically uses the price data from the exchange that the user opens on TradingView — such as OKX, BYBIT, BITGET, GATE.IO, MEXC, and more.

If the global symbol is supported on TradingView, the corresponding market price is retrieved and converted into KRW using the FX rate, allowing real-time global-vs-Korea price comparison.

Accurate Premium Calculation

Altcoin Premium = ((KRW Price - Global Price in KRW) / Global Price in KRW) × 100

BTC Premium = ((BTC_KRW - BTC_USDT×FX) / (BTC_USDT×FX)) × 100

Premium Gap Signal Alerts

When the gap between altcoin premium and Bitcoin premium exceeds a user-defined threshold (e.g., 3%), the chart highlights the bar with a yellow background, and a signal alert is triggered.

Visual Data Representation

Bar colors automatically change based on premium intensity

BTC Kimchi Premium and Coinbase-Binance Premium lines are plotted together

The latest candle shows a label with the coin name and premium value

Integrated Alerts

Fully compatible with TradingView alerts — allowing users to receive instant notifications when the premium gap crosses the defined threshold.

⚙️ User Settings

Select Exchange: Choose domestic KRW market (Upbit / Bithumb)

Premium Gap Threshold (%): Set the minimum gap between altcoin and BTC premium to trigger signals (default: 3%)

🧠 Use Cases

Premium Gap Trading Strategies

Identify altcoins with unusually high premium divergence compared to BTC and take positions based on mean-reversion logic.

Market Overheating Detection

Detect abnormal buying pressure or local overvaluation when an altcoin’s premium rapidly expands beyond normal ranges.

Tracking Global vs. Korean Market Flow

Monitor capital flows by comparing KRW market premiums to real-time global market pricing.

PRIME 2.0PRIME 2.0 — Precision Entry Tool

PRIME 2.0 is a smart price action-based indicator designed for intraday traders who want to catch high-probability moves during the London session. It uses a combination of market structure shifts (CHOCH – Change of Character) and session-based timing to identify potential entries.

🔍 Key Features:

Session-Based Logic: Activates after the London market opens, filtering noise from other sessions.

CHOCH Detection: Spots shifts in market structure by identifying crossover and crossunder of candle highs/lows.

Visual Entry Points: Plots real-time entry points based on structure change.

🧠 Who Is It For?

Scalpers and day traders

Traders who follow Smart Money Concepts (SMC)

Anyone looking to improve entry precision without clutter

⚠️ Disclaimer:

This indicator does not generate buy/sell signals or exit points. It is meant to be used as a tool within a broader trading strategy. Combine it with your own risk management and market knowledge for best results

Balancelink : Partition Function 1.0This script computes the partition function values 𝑝(𝑛) using Euler’s Pentagonal Number Theorem and displays them in a horizontally wrapped table directly on the chart. The partition function is a classic function in number theory that counts the number of ways an integer 𝑛 can be expressed as a sum of positive integers, disregarding the order of the summands.

Key Features

Efficient Calculation:

The script computes 𝑝(𝑛) for all orders from 0 up to a user-defined maximum (set by the "End Order" input). The recursive computation leverages Euler’s Pentagonal Number Theorem, ensuring the function is calculated correctly for each order.

Display Range Selection:

Users can select a specific range of orders (for example, from 𝑛 = 100 to 𝑛 = 200 to display.) This means you can focus on a particular segment of the partition function results without cluttering the chart.

Horizontally Wrapped Table:

The partition values are organized into a clean, horizontal table with a customizable number of columns per row (default is 20). When the number of values exceeds the maximum columns, the table automatically wraps onto a new set of rows for better readability.

Medium Text Size:

The table cells use a medium (normal) text size for easy viewing and clarity.

How to Use

Inputs:

Start Order (n): The starting index from which you want to display the partition function (default is 100).

End Order (n): The ending index up to which the partition function values will be displayed (default is 200).

Max Columns Per Row: Determines how many results are shown per row before wrapping to the next (default is 20).

Calculation:

The script calculates all 𝑝(𝑛) values from 0 up to the specified "End Order". It then extracts and displays only the values in the chosen range.

Visualization:

The computed values are shown in a neatly arranged table at the top right of your TradingView chart, making it simple to scroll through and inspect the partition function values.

Use Cases

Educational & Research:

Ideal for educators and students exploring concepts of integer partitions and number theory.

Data Analysis & Pattern Recognition:

Useful for those interested in the behavior and growth of partition numbers as 𝑛 increases.

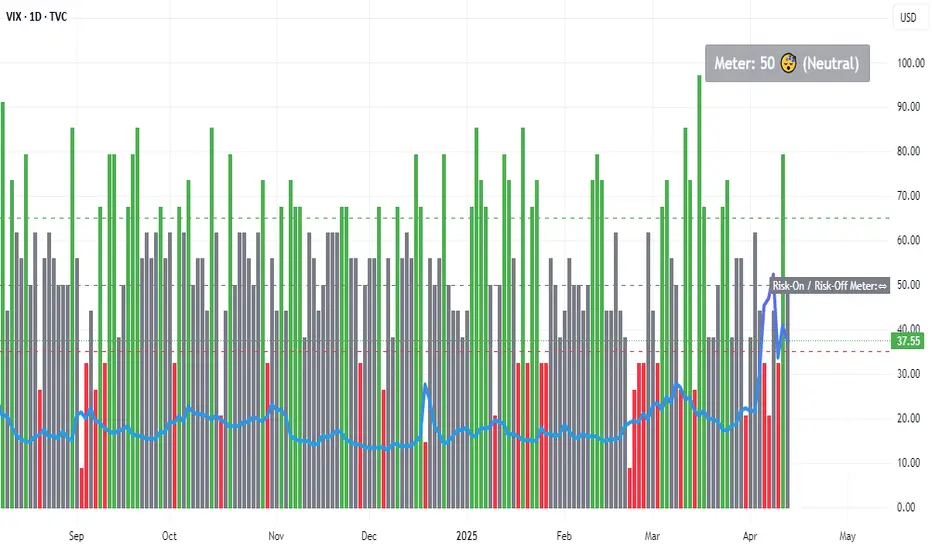

Risk-On / Risk-Off MeterThe risk on/off meter helps you assess the market's overall risk sentiment.

Try using it on the VIX daily chart.

The calculation is based on the following values:

Risk-On Assets

spx dax nas100 copper oil audusd nzdusd btc audjpy

Risk-Off Assets

gold usdjpy usdchf vix us02y us10y us30y dxy

Below a calculated value of 25, Risk Of is displayed as being above a value of 65 Risk On. The neutral market phase is in between. The indicator is used purely as a market sentiment indicator and does not provide any trading recommendations.

Yield Curve 1.2Yield Curve is a macroeconomic analysis tool designed to visualize and interpret changes in the shape of government bond yield curves across major economies.

Use it in any 1H Chart

It tracks the difference between 10-year and 2-year government bond yields for key countries (e.g. US, EUR, JPY, AUD, GBP, etc.) and compares the current yield levels to their values recorded every Monday at 2:00 UTC. Based on this comparison, the indicator categorizes the yield curve movement into common market regimes such as:

Bull Flattener

Bear Steepener

Parallel Shift

and others.

Each regime gives insight into how markets are adjusting their expectations for future interest rates, economic growth, or central bank policy.

The indicator presents this analysis in a clear table format, showing:

Current and Monday yields

Yield changes (in basis points)

Yield spread (10Y - 2Y)

Detected regime type

A simplified grade and brief explanation for each case

Color coding is used throughout the table to help visually distinguish between steepening, flattening, and parallel shift scenarios.