UTSStrategyHelperLibrary "UTSStrategyHelper"

TODO: add library description here

stopLossPrice(sig, atr, factor, isLong)

Calculates the stop loss price using a distance determined by ATR multiplied by a factor. Example for Long trade SL: PRICE - (ATR * factor).

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

takeProfitPrice(sig, atr, factor, isLong)

Calculates the take profit price using a distance determined by ATR multiplied by a factor. Example for Long trade TP: PRICE + (ATR * factor). When take profit price is reached usually 50 % of the position is closed and the other 50 % get a trailing stop assigned.

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

trailingStopPrice(initialStopPrice, atr, factor, priceSource, isLong)

Calculates a trailing stop price using a distance determined by ATR multiplied by a factor. It takes an initial price and follows the price closely if it changes in a favourable way.

Parameters:

initialStopPrice (float) : (float): The initial stop price which, for consistency also should be ATR * factor behind price: e.g. Long trade: PRICE - (ATR * factor)

atr (float) : (float): The value of the atr. Ideally the ATR value at trade open is taken and used for subsequent calculations.

factor (float)

priceSource (float) : (float): The current price.

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

hasGreaterPositionSize(positionSize)

Determines if the strategy's position size has grown since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSmallerPositionSize(positionSize)

Determines if the strategy's position size has decreased since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasUnchangedPositionSize(positionSize)

Determines if the strategy's position size has changed since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

exporthasLongPosition(positionSize)

Determines if the strategy has an open long position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasShortPosition(positionSize)

Determines if the strategy has an open short position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasAnyPosition(positionSize)

Determines if the strategy has any open position, regardless of short or long.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSignal(value)

Determines if the given argument contains a valid value (means not 'na').

Parameters:

value (float) : (float): The actual value.

Returns: (bool): A boolean value.

Library

UTSConvenienceToolsLibrary "UTSConvenienceTools"

Convenience tool library containing helper functions for drawing and charting.

isDarkColor(color)

Determines on base of the luminance of the given color if the color can be considered a 'dark' color. Usefull for determining the readable font color for arbitrary colored backgrounds. Credits out to:

Parameters:

color (color) : (color): The actual color value.

Returns: (bool): A boolean value.

smallLabelLowerRight(txt, yPos, bgColor)

Displays the specified `txt` in a small label at the `yPos` of the current bar. The label points to the lower right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

smallLabelUpperRight(txt, yPos, bgColor)

Displays the specified `txt` in a small label at the `yPos` of the current bar. The label points to the upper right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

smallLabelCenter(txt, yPos, bgColor)

Displays the specified `txt` in a small label at the `yPos` of the current bar. The label points to the center.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

smallLabelDown(txt, yPos, bgColor)

Displays the specified `txt` in a small label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

smallLabelUp(txt, yPos, bgColor)

Displays the specified `txt` in a small label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

normalLabelLowerRight(txt, yPos, bgColor)

Displays the specified `txt` in a normal label at the `yPos` of the current bar. The label points to the lower right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

normalLabelUpperRight(txt, yPos, bgColor)

Displays the specified `txt` in a normal label at the `yPos` of the current bar. The label points to the upper right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

normalLabelCenter(txt, yPos, bgColor)

Displays the specified `txt` in a normal label at the `yPos` of the current bar. The label points to the center.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

normalLabelDown(txt, yPos, bgColor)

Displays the specified `txt` in a normal label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

normalLabelUp(txt, yPos, bgColor)

Displays the specified `txt` in a normal label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

largeLabelLowerRight(txt, yPos, bgColor)

Displays the specified `txt` in a large label at the `yPos` of the current bar. The label points to the lower right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

largeLabelUpperRight(txt, yPos, bgColor)

Displays the specified `txt` in a large label at the `yPos` of the current bar. The label points to the upper right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

largeLabelCenter(txt, yPos, bgColor)

Displays the specified `txt` in a large label at the `yPos` of the current bar. The label points to the center.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

largeLabelDown(txt, yPos, bgColor)

Displays the specified `txt` in a large label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

largeLabelUp(txt, yPos, bgColor)

Displays the specified `txt` in a large label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

autoLabelLowerRight(txt, yPos, bgColor)

Displays the specified `txt` in a auto label at the `yPos` of the current bar. The label points to the lower right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

autoLabelUpperRight(txt, yPos, bgColor)

Displays the specified `txt` in a auto label at the `yPos` of the current bar. The label points to the upper right.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

autoLabelCenter(txt, yPos, bgColor)

Displays the specified `txt` in a auto label at the `yPos` of the current bar. The label points to the center.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

autoLabelDown(txt, yPos, bgColor)

Displays the specified `txt` in a auto label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned above the candle pass 'high'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

autoLabelUp(txt, yPos, bgColor)

Displays the specified `txt` in a auto label at the `yPos` of the current bar. The label points down.

Parameters:

txt (string)

yPos (float) : (float): The y-position value. To have it positioned below the candle pass 'low'.

bgColor (color) : (color): The background color value.

Returns: (bool): A boolean value.

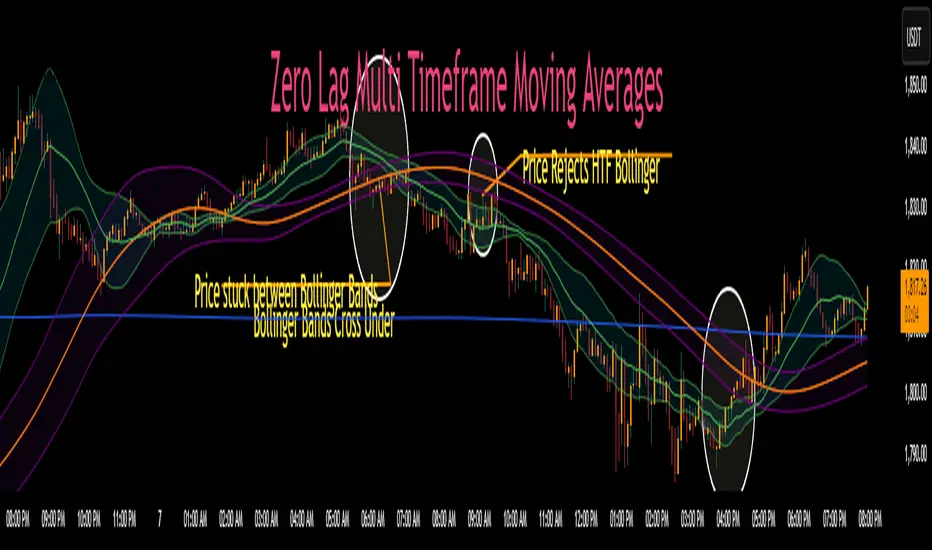

Zero Lag MTF Moving Average by CoffeeshopCryptoBased on Moving Average Types supplied by @TradingView www.tradingview.com

Ideas and code enhanced to show higher timeframe by @CoffeeShopCrypto

It’s time to take the guesswork out of moving averages and multiple timeframes when day trading. Moving averages are a cornerstone of many trading strategies, often viewed as dynamic support and resistance levels. Traders rely on these levels to anticipate price reactions, whether it’s a bounce in a trending market or a reversal in a ranging one. Additionally, the direction and alignment of multi timeframe moving averages—whether they’re moving in the same direction or diverging—provide critical clues about market momentum and potential reversals. However, the traditional higher timeframe moving average indicators force traders to wait for higher timeframe candles to close, creating lag and missed opportunities.

The Old Way

For example: If you are on a 5 minute chart and you want to observe the location and direction of a 30 minute chart Moving Average, you'll need to wait for a total of 6 candles to close, and again every 6 candles after that. This only creates more lag.

The New Way

Now there is no waiting for high timeframe session candles to close. No matter what timeframe Moving Average you want to know about, this indicator will show you its location on your current chart at any time in real time.

For those who prefer Bollinger Bands, this indicator adds a whole new dimension to your strategy. Traders often wait for price action to break outside the lower time frame Bollinger bands before considering a trade, while still seeking key support or resistance levels beyond them. But if you don't know the position of your higher time frame Bollinger, you could be trading into a trap. With Zero Lag Multi Timeframe Moving Average, you can view both your current and higher timeframe Bollinger Bands simultaneously with zero waiting. This lets you instantly see when price action is traveling between the bands of either timeframe or breaking through both—indicating a strong trend in that direction. Additionally, when both sets of Bollinger Bands overlap at the same price levels, it highlights areas of strong consolidation and ranging conditions, giving you a clear picture of market dynamics. This is a key element in price action that tells you there is currently no direction to the market and both the current and higher time frames are flat.

Enter Zero Lag Multi Timeframe Moving Average—the ultimate tool for real-time higher timeframe moving averages and Bollinger Bands. This innovative indicator eliminates the delay, delivering instant, precise values for higher timeframe averages and bands, even on open candles. Seamlessly combining current and higher timeframe data, it allows traders to identify key moments where moving averages or Bollinger Bands align or diverge, signaling market conditions. Whether you’re gauging the strength of a trend, pinpointing potential reversals, or identifying consolidation zones, Zero Lag Multi Timeframe Moving Average gives you the clarity needed to make better trading decisions according to market conditions.

Why is this "Mashup" of moving averages different and important?

Honestly its really about the calculation thats imported through the "import library" function.

Heres what it does:

The ZLMTF-MA is designed to help traders easily see where higher timeframe moving averages and Bollinger Bands are—without needing to switch chart timeframes or wait for those larger candles to close. It works by adjusting common moving average types like SMA, EMA, and VWMA to show what they would look like if they were based on a higher timeframe, right on your current chart. This helps users stay focused on their main timeframe while still having a clear view of the bigger picture, making it easier to spot trend direction, key support and resistance levels, and overall market structure. The goal is to keep things simple, fast, and more visually informative for everyday traders.

Bollinger Bands

When working with Bollinger Bands, a common strategy is to take the trades once price action has escaped through the top or bottom of your current Bollinger Band.

A false breakout occurs when both Bollinger Bands are not moving in the same direction as eachother or when they are overlapping.

Moving Averages as Support and Resistance:

Traders who use Moving Averages as support or resistance, looking for rejections or failures of these areas can now see multiple timeframe price action instantly and simultaneously.

Trading Setup Examples:

Price Action Scenario 1:

Higher Timeframe Ranging-

When price action breaks through a current moving average headed toward a higher timeframe moving average, trades are taken with caution if the moving averages are converging.

Price Action Scenario 2:

Strong Trending Market -

If the moving averages are in the same direction, and your price action is now leading the low timeframe moving average, you have re-entered a strong trend.

Price Action Scenario 3:

High Timeframe Rejections -

If you have a rejection of a higher timeframe moving average, and your both averages are still diverging, this is the end of a pullback as you re-enter a strong trend in the original direction

Price Action Scenario 4:

Trend Reversals -

If you close beyond both the low and high timeframe moving averages, you can consider that price action is strong enough to change direction here and you should prepare for trade setups in the opposite direction of the previous.

HTF MA Label Information:

Even if your high timeframe moving average is turned off, you can still see this label.

It gives you a quick reminder of what high timeframe settings you have used to see MA values.

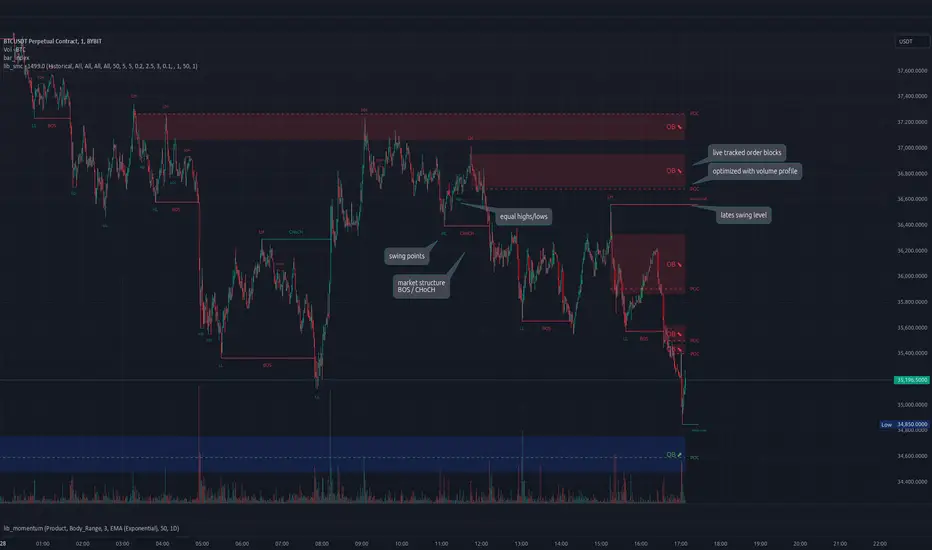

lib_smcLibrary "lib_smc"

This is an adaptation of LuxAlgo's Smart Money Concepts indicator with numerous changes. Main changes include integration of object based plotting, plenty of performance improvements, live tracking of Order Blocks, integration of volume profiles to refine Order Blocks, and many more.

This is a library for developers, if you want this converted into a working strategy, let me know.

buffer(item, len, force_rotate)

Parameters:

item (float)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (int)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (Profile type from robbatt/lib_profile/32)

len (int)

force_rotate (bool)

swings(len)

INTERNAL: detect swing points (HH and LL) in given range

Parameters:

len (simple int) : range to check for new swing points

Returns: values are the price level where and if a new HH or LL was detected, else na

method init(this)

Namespace types: OrderBlockConfig

Parameters:

this (OrderBlockConfig)

method delete(this)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

method clear_broken(this, broken_buffer)

INTERNAL: delete internal order blocks box coordinates if top/bottom is broken

Namespace types: map

Parameters:

this (map)

broken_buffer (map)

Returns: any_bull_ob_broken, any_bear_ob_broken, broken signals are true if an according order block was broken/mitigated, broken contains the broken block(s)

create_ob(id, mode, start_t, start_i, top, end_t, end_i, bottom, break_price, early_confirmation_price, config, init_plot, force_overlay)

INTERNAL: set internal order block coordinates

Parameters:

id (int)

mode (int) : 1: bullish, -1 bearish block

start_t (int)

start_i (int)

top (float)

end_t (int)

end_i (int)

bottom (float)

break_price (float)

early_confirmation_price (float)

config (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

Returns: signals are true if an according order block was broken/mitigated

method align_to_profile(block, align_edge, align_break_price)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

align_edge (bool)

align_break_price (bool)

method create_profile(block, opens, tops, bottoms, closes, values, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

opens (array)

tops (array)

bottoms (array)

closes (array)

values (array)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

method create_profile(block, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

track_obs(swing_len, hh, ll, top, btm, bull_bos_alert, bull_choch_alert, bear_bos_alert, bear_choch_alert, min_block_size, max_block_size, config_bull, config_bear, init_plot, force_overlay, enabled, extend_blocks, clear_broken_buffer_before, align_edge_to_value_area, align_break_price_to_poc, profile_args_bull, profile_args_bear, use_soft_confirm, soft_confirm_offset, use_retracements_with_FVG_out)

Parameters:

swing_len (int)

hh (float)

ll (float)

top (float)

btm (float)

bull_bos_alert (bool)

bull_choch_alert (bool)

bear_bos_alert (bool)

bear_choch_alert (bool)

min_block_size (float)

max_block_size (float)

config_bull (OrderBlockConfig)

config_bear (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

enabled (bool)

extend_blocks (simple bool)

clear_broken_buffer_before (simple bool)

align_edge_to_value_area (simple bool)

align_break_price_to_poc (simple bool)

profile_args_bull (ProfileArgs type from robbatt/lib_profile/32)

profile_args_bear (ProfileArgs type from robbatt/lib_profile/32)

use_soft_confirm (simple bool)

soft_confirm_offset (float)

use_retracements_with_FVG_out (simple bool)

method draw(this, config, extend_only)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

config (OrderBlockConfig)

extend_only (bool)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: array

Parameters:

blocks (array)

config (OrderBlockConfig)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: map

Parameters:

blocks (map)

config (OrderBlockConfig)

method cleanup(this, ob_bull, ob_bear)

removes all Profiles that are older than the latest OrderBlock from this profile buffer

Namespace types: array

Parameters:

this (array type from robbatt/lib_profile/32)

ob_bull (OrderBlock)

ob_bear (OrderBlock)

_plot_swing_points(mode, x, y, show_swing_points, linecolor_swings, keep_history, show_latest_swings_levels, trail_x, trail_y, trend)

INTERNAL: plot swing points

Parameters:

mode (int) : 1: bullish, -1 bearish block

x (int) : x-coordingate of swing point to plot (bar_index)

y (float) : y-coordingate of swing point to plot (price)

show_swing_points (bool) : switch to enable/disable plotting of swing point labels

linecolor_swings (color) : color for swing point labels and lates level lines

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

show_latest_swings_levels (bool)

trail_x (int) : x-coordinate for latest swing point (bar_index)

trail_y (float) : y-coordinate for latest swing point (price)

trend (int) : the current trend 1: bullish, -1: bearish, to determine Strong/Weak Low/Highs

_pivot_lvl(mode, trend, hhll_x, hhll, super_hhll, filter_insignificant_internal_breaks)

INTERNAL: detect whether a structural level has been broken and if it was in trend direction (BoS) or against trend direction (ChoCh), also track the latest high and low swing points

Parameters:

mode (simple int) : detect 1: bullish, -1 bearish pivot points

trend (int) : current trend direction

hhll_x (int) : x-coordinate of newly detected hh/ll (bar_index)

hhll (float) : y-coordinate of newly detected hh/ll (price)

super_hhll (float) : level/y-coordinate of superior hhll (if this is an internal structure pivot level)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: coordinates of internal structure that has been broken (x,y): start of structure, (trail_x, trail_y): tracking hh/ll after structure break, (bos_alert, choch_alert): signal whether a structural level has been broken

_plot_structure(x, y, is_bos, is_choch, line_color, line_style, label_style, label_size, keep_history)

INTERNAL: plot structural breaks (BoS/ChoCh)

Parameters:

x (int) : x-coordinate of newly broken structure (bar_index)

y (float) : y-coordinate of newly broken structure (price)

is_bos (bool) : whether this structural break was in trend direction

is_choch (bool) : whether this structural break was against trend direction

line_color (color) : color for the line connecting the structural level and the breaking candle

line_style (string) : style (line.style_dashed/solid) for the line connecting the structural level and the breaking candle

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the structural level and the breaking candle

label_size (string) : size (size.small/tiny) for the label above/below the line connecting the structural level and the breaking candle

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure_values(length, super_hh, super_ll, filter_insignificant_internal_breaks)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: trend: direction 1:bullish -1:bearish, (bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up): whether and which level broke in a bullish direction, trailing high, (bbear_bos_alert, bear_choch_alert, tm_x, btm_y, trail_dn_x, trail_dn): same in bearish direction

structure_plot(trend, bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up, hh, bear_bos_alert, bear_choch_alert, btm_x, btm_y, trail_dn_x, trail_dn, ll, color_bull, color_bear, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history)

detect (and plot) structural breaks and the resulting new trend

Parameters:

trend (int) : crrent trend 1: bullish, -1: bearish

bull_bos_alert (bool) : if there was a bullish bos alert -> plot it

bull_choch_alert (bool) : if there was a bullish choch alert -> plot it

top_x (int) : latest shwing high x

top_y (float) : latest swing high y

trail_up_x (int) : trailing high x

trail_up (float) : trailing high y

hh (float) : if there was a higher high

bear_bos_alert (bool) : if there was a bearish bos alert -> plot it

bear_choch_alert (bool) : if there was a bearish chock alert -> plot it

btm_x (int) : latest swing low x

btm_y (float) : latest swing low y

trail_dn_x (int) : trailing low x

trail_dn (float) : trailing low y

ll (float) : if there was a lower low

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure(length, color_bull, color_bear, super_hh, super_ll, filter_insignificant_internal_breaks, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history, enabled)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

enabled (bool)

_check_equal_level(mode, len, eq_threshold, enabled)

INTERNAL: detect equal levels (double top/bottom)

Parameters:

mode (int) : detect 1: bullish/high, -1 bearish/low pivot points

len (int) : lookback period for equal level (swing point) detection

eq_threshold (float) : maximum price offset for a level to be considered equal

enabled (bool)

Returns: eq_alert whether an equal level was detected and coordinates of the first and the second level/swing point

_plot_equal_level(show_eq, x1, y1, x2, y2, label_txt, label_style, label_size, line_color, line_style, keep_history)

INTERNAL: plot equal levels (double top/bottom)

Parameters:

show_eq (bool) : whether to plot the level or not

x1 (int) : x-coordinate of the first level / swing point

y1 (float) : y-coordinate of the first level / swing point

x2 (int) : x-coordinate of the second level / swing point

y2 (float) : y-coordinate of the second level / swing point

label_txt (string) : text for the label above/below the line connecting the equal levels

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the equal levels

label_size (string) : size (size.tiny) for the label above/below the line connecting the equal levels

line_color (color) : color for the line connecting the equal levels (and it's label)

line_style (string) : style (line.style_dotted) for the line connecting the equal levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

equal_levels_values(len, threshold, enabled)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

enabled (bool) : whether detection is enabled

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels_plot(eqh_x1, eqh_y1, eqh_x2, eqh_y2, eql_x1, eql_y1, eql_x2, eql_y2, color_eqh, color_eql, show, keep_history)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

eqh_x1 (int) : coordinates of first point of equal high

eqh_y1 (float) : coordinates of first point of equal high

eqh_x2 (int) : coordinates of second point of equal high

eqh_y2 (float) : coordinates of second point of equal high

eql_x1 (int) : coordinates of first point of equal low

eql_y1 (float) : coordinates of first point of equal low

eql_x2 (int) : coordinates of second point of equal low

eql_y2 (float) : coordinates of second point of equal low

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels(len, threshold, color_eqh, color_eql, enabled, show, keep_history)

detect (and plot) equal levels (double top/bottom)

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert) whether an equal high was detected, (eql_alert) same for equal lows

_detect_fvg(mode, enabled, o, h, l, c, filter_insignificant_fvgs, change_tf)

INTERNAL: detect FVG (fair value gap)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

enabled (bool) : whether detection is enabled

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

Returns: whether a new FVG was detected and its top/mid/bottom levels

_clear_broken_fvg(mode, upper_boxes, lower_boxes)

INTERNAL: clear mitigated FVGs (fair value gaps)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

upper_boxes (array) : array that stores the upper parts of the FVG boxes

lower_boxes (array) : array that stores the lower parts of the FVG boxes

_plot_fvg(mode, show, top, mid, btm, border_color, extend_box)

INTERNAL: plot (and clear broken) FVG (fair value gap)

Parameters:

mode (int) : plot 1: bullish, -1 bearish gap

show (bool) : whether plotting is enabled

top (float) : top level of fvg

mid (float) : center level of fvg

btm (float) : bottom level of fvg

border_color (color) : color for the FVG box

extend_box (int) : how many bars into the future the FVG box should be extended after detection

fvgs_values(o, h, l, c, filter_insignificant_fvgs, change_tf, enabled)

detect (and plot / clear broken) FVGs (fair value gaps), and return alerts and level values

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

enabled (bool) : whether detection is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs_plot(bullish_fvg_alert, bull_top, bull_mid, bull_btm, bearish_fvg_alert, bear_top, bear_mid, bear_btm, color_bull, color_bear, extend_box, show)

Parameters:

bullish_fvg_alert (bool)

bull_top (float)

bull_mid (float)

bull_btm (float)

bearish_fvg_alert (bool)

bear_top (float)

bear_mid (float)

bear_btm (float)

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs(o, h, l, c, filter_insignificant_fvgs, change_tf, color_bull, color_bear, extend_box, enabled, show)

detect (and plot / clear broken) FVGs (fair value gaps)

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert): whether a new bullish FVG was detected, (bearish_fvg_alert): same for bearish FVGs

OrderBlock

Fields:

id (series int)

dir (series int)

left_top (chart.point)

right_bottom (chart.point)

break_price (series float)

early_confirmation_price (series float)

ltf_high (array)

ltf_low (array)

ltf_volume (array)

plot (Box type from robbatt/lib_plot_objects/49)

profile (Profile type from robbatt/lib_profile/32)

trailing (series bool)

extending (series bool)

awaiting_confirmation (series bool)

touched_break_price_before_confirmation (series bool)

soft_confirmed (series bool)

has_fvg_out (series bool)

hidden (series bool)

broken (series bool)

OrderBlockConfig

Fields:

show (series bool)

show_last (series int)

show_id (series bool)

show_profile (series bool)

args (BoxArgs type from robbatt/lib_plot_objects/49)

txt (series string)

txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

delete_when_broken (series bool)

broken_args (BoxArgs type from robbatt/lib_plot_objects/49)

broken_txt (series string)

broken_txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

broken_profile_args (ProfileArgs type from robbatt/lib_profile/32)

use_profile (series bool)

profile_args (ProfileArgs type from robbatt/lib_profile/32)

ToolsLibrary "Tools"

Common tools

movingAverage(maType, maSource, maLength)

dynamically returns MA

Parameters:

maType (string) : ma type

maSource (float) : ma source

maLength (simple int) : ma length

Returns: ta.{sma,rma,ema,wma,vwma,hma}

Killzones And Macros LibraryKillzones & Macros Library for Trading Sessions

This Pine Script library is designed to help traders identify and act during high-volatility trading windows, commonly referred to as "Killzones." These are specific times during the day when institutional traders are most active, resulting in increased liquidity and price movement. The library provides boolean fields that return true when the current time falls within one of the killzones or macroeconomic event windows, allowing for enhanced trade timing and precision.

Killzones Include:

London Open, New York Open, Midnight Open, London Lunch, New York PM, and more.

Capture high-volume periods like Power Hour, Equities Open, and Asian Range.

Macros:

Identify key moments like London 02:33, New York 08:50, and other significant times aligned with market movements or events.

This library is perfect for integrating into your custom strategies, backtesting, or setting alerts for optimal trade execution during major trading sessions and events.

MathOperatorLibrary "MathOperator"

Methods to handle operators.

method add(value_a, value_b)

Add value a to b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method subtract(value_a, value_b)

subtract value b from a.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method multiply(value_a, value_b)

multiply value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method divide(value_a, value_b)

divide value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method remainder(value_a, value_b)

remainder of a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: float.

method equal(value_a, value_b)

equality of value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method not_equal(value_a, value_b)

inequality of value a with b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method over(value_a, value_b)

value a is over b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method under(value_a, value_b)

value a is under b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method over_equal(value_a, value_b)

value a is over equal b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method under_equal(value_a, value_b)

value a is under equal b.

Namespace types: series float, simple float, input float, const float

Parameters:

value_a (float) : float, value a.

value_b (float) : float, value b.

Returns: bool.

method and_(value_a, value_b)

logical and of a with b

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method or_(value_a, value_b)

logical or of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method not_(value_a)

logical not of a.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

Returns: bool.

method xor_(value_a, value_b)

logical xor of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method xnor_(value_a, value_b)

logical xnor of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method nand_(value_a, value_b)

logical nand of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

method nor_(value_a, value_b)

logical nor of a with b.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

value_a (bool) : bool, value a.

value_b (bool) : bool, value b.

Returns: bool.

Alert Sender Library [TradingFinder]Library "AlertSenderLibrary_TradingFinder"

🔵 Introduction

The "Alert Sender Library" is a management and production program for "Alert Messages" that enables the creation of unique messages for any type of signal generated by indicators or strategies.

These messages include the direction of the signal, symbol, time frame, the date and time the condition was triggered, prices related to the signal, and a personal message from you. To make better and more optimal use of this "library", you should carefully study " Key Features" and "How to Use".

🔵 Key Features

Automatic Detection of Appropriate Type :

Using two parameters, "AlertType" and "DetectionType", which you must enter at the beginning into the "AlertSender" function, the type of the alert message is determined.

For example, if you select one of the "DetectionType"s such as "Order Block Signal", "Signal", and "Setup", your alert type will be chosen based on "Long" and "Short". Whether it's "Long" or "Short" depends on the "AlertType" you have set to either "Bullish" or "Bearish".

Automatic Symbol Detection :

Whenever you add an alert for a specific symbol, if you want the name of that symbol to be in your message text, you must manually write the name of the symbol in your message. One of the capabilities of the "Alert Sender" is the automatic detection of the symbol and adding it to the message text.

Automatic Time Frame Detection :

When adding your alert, the "Alert Sender" detects the time frame of the symbol you intend to add the alert for and adds it to the text. This feature is very practical and can prevent traders from making mistakes.

For example, a trader might add alerts for a specific symbol using a specific indicator in different time frames, taking the main signal in the 1-hour time frame and only a confirmation signal in the 15-minute time frame. This feature helps to identify in which time frame the signal is set.

Detection of Date and Time When the Signal is Triggered :

You can have the date and time at the moment the message is sent. This feature has various uses. For example, if you use the Webhook URL feature to send messages to a Telegram channel, there might be issues with alert delivery on your server, causing delays, and you might receive the message when it has lost its validity.

With this feature, you can match the sending time of the message from TradingView with the receipt time in your messenger and detect if there is a delay in message delivery.

Important :

You can also set the Time Zone you wish to receive the date and time based on.

Display of "Key Prices" :

Key prices can vary based on the type of signals. For example, when the "DetectionType" is in "Order Block Signal" mode, the key prices are the "Distal" and "Proximal" prices. Or if the "DetectionType" is in "Setup" mode, the key prices are "Entry", "Stop Loss", and "Take Profit".

Receipt of Personal "Messages" :

You can enter your personal message using "input.string" or "input.text_area" in addition to the messages that are automatically created.

Beautiful and Functional Display of Messages :

The titles of messages sent by "AlertSender" are displayed using related emojis to prevent mistakes due to visual errors, enhancing beauty.

🔵 How to Use

🟣 Familiarity with Function and Parameters

AlertSender(Condition, Alert, AlertName, AlertType, DetectionType, SetupData, Frequency, UTC, MoreInfo, Message, o, h, l, c, Entry, TP, SL, Distal, Proximal)

Parameters:

- Condition (bool)

- Alert (string)

- AlertName (string)

- AlertType (string)

- DetectionType (string)

- SetupData (string)

- Frequency (string)

- UTC (string)

- MoreInfo (string)

- Message (string)

- o (float)

- h (float)

- l (float)

- c (float)

- Entry (float)

- TP (float)

- SL (float)

- Distal (float)

- Proximal (float)

To add "Alert Sender Library", you must first add the following code to your script.

import TFlab/AlertSenderLibrary_TradingFinder/1

🟣 Parameters

"Condition" : This parameter is a Boolean. You need to set it based on the condition that, when met (or fired), you want to receive an alert. The output should be either "true" or "false".

"Alert" : This parameter accepts one of two inputs, "On" or "Off". If set to "On", the alarm is active; if "Off", the alarm is deactivated. This input is useful when you have numerous alerts in an indicator or strategy and need to activate only a few of them. "Alert" is a string parameter.

Alert = input.string('On', 'Alert', , 'If you turn on the Alert, you can receive alerts and notifications after setting the "Alert".', group = 'Alert')

"AlertName" : This is a string parameter where you can enter the name you choose for your alert.

AlertName = input.string('Order Blocks Finder ', 'Alert Name', group = 'Alert')

"AlertType" : The inputs for this parameter are "Bullish" or "Bearish". If the condition selected in the "Condition" parameter is of a bullish bias, you should set this parameter to "Bullish", and if the condition is of a bearish bias, it should be set to "Bearish". "AlertType" is a string parameter.

"DetectionType" : This parameter's predefined inputs include "Order Block Signal", "Signal", "Setup", and "Analysis". You may provide other inputs, but some functionalities, like "Key Price", might be lost. "DetectionType" is a string parameter.

"SetupData" :

If "DetectionType" is set to "Setup", you must specify "SetupData" as either "Basic" or "Full". In "Basic" mode, only the "Entry" price needs to be defined in the function, and "TP" (Take Profit) and "SL" (Stop Loss) can be any number or NA. In "Full" mode, you need to define "Entry", "SL", and "TP". "Setup" is a string parameter.

"Frequency" : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Frequency = input.string('Once Per Bar', 'Message Frequency', , 'The triggering frequency. Possible values are: All (all function calls trigger the alert), Once Per Bar (the first function call during the bar triggers the alert), Per Bar Close (the function call triggers the alert only when it occurs during the last script iteration of the real-time bar, when it closes). The default is alert.freq_once_per_bar.', group = 'Alert')

"UTC" : With this parameter, you can set the Time Zone for the date and time of the alert's dispatch. "UTC" is a string parameter and can be set as "UTC-4", "UTC+1", "UTC+9", or any other Time Zone.

UTC = input.string('UTC', 'Show Alert time by Time Zone', group = 'Alert')

"MoreInfo" : This parameter can take one of two inputs, "On" or "Off", which are strings. Additional information, including "Time" and "Key Price", is included. If set to "On", this information is received; if "Off", it is not displayed in the sent message.

MoreInfo = input.string('On', 'Display More Info', , group = 'Alert')

"Message" : This parameter captures the user's personal message through an input and displays it at the end of the sent message. It is a string input.

MessageBull = input.text_area('Long Position', 'Long Signal Message', group = 'Alert') MessageBear = input.text_area('Short Position', 'Short Signal Message', group = 'Alert')

"o" (Open Price): A floating-point number representing the opening price of the candle. This input is necessary when the "DetectionType" is set to "Signal". Otherwise, it can be any number or "na".

"h" (High Price): A float variable for the highest price of the candle. Required when "DetectionType" is "Signal"; in other cases, any number or "na" is acceptable.

"l" (Low Price): A float representing the lowest price of the candle. This field must be filled if "DetectionType" is "Signal". If not, it can be any number or "na".

"c" (Close Price): A floating-point variable indicating the closing price of the candle. Needed for "Signal" type detections; otherwise, it can take any value or "na".

"Entry" : A float variable indicating the entry price into a trading setup. This is relevant when "DetectionType" is in "Setup" mode. In other scenarios, it can be any number or "na". It denotes the price at which the trade setup is entered.

"TP" (Take Profit): A float that is necessary when "DetectionType" is "Setup" and "SetupData" is "Full". Otherwise, it can be any number or "na". It signifies the price target for taking profits in a trading setup.

"SL" (Stop Loss): A float required when "DetectionType" is "Setup" and "SetupData" is "Full". It can be any number or "na" in other cases. This value represents the price at which a stop loss is set to limit losses.

"Distal" : A float important for "Order Block Signal" detection. It can be any number or "na" if not in use. This variable indicates the price reaching the distal line of an order block.

"Proximal" : A float needed for "Order Block Signal" detection mode. It can take any value or "na" otherwise. It marks the price reaching the proximal line of an order block.

TUF_LOGICThe TUF_LOGIC library incorporates three-valued logic (also known as trilean logic) into Pine Script, enabling the representation of states beyond the binary True and False to include an 'Uncertain' state. This addition is particularly apt for financial market contexts where information may not always be black or white, accommodating scenarios of partial or ambiguous data.

Key Features:

Trilean Data Type: Defines a tri type, facilitating the representation of True (1), Uncertain (0), and False (-1) states, thus accommodating a more nuanced approach to logical evaluation.

Validation and Conversion: Includes methods like validate, to ensure trilean variables conform to expected states, and to_bool, for converting trilean to boolean values, enhancing interoperability with binary logic systems.

Core Logical Operations: Extends traditional logical operators (AND, OR, NOT, XOR, EQUALITY) to work within the trilean domain, enabling complex conditionals that reflect real-world uncertainties.

Specialized Logical Operations:

Implication Operators: Features IMP_K (Kleene's), IMP_L (Łukasiewicz's), and IMP_RM3, offering varied approaches to logical implication within the trilean framework.

Possibility, Necessity, and Contingency Operators: Implements MA ("it is possible that..."), LA ("it is necessary that..."), and IA ("it is unknown/contingent that..."), derived from Tarski-Łukasiewicz's modal logic attempts, enriching the library with modal logic capabilities.

Unanimity Functions: The UNANIMOUS operator assesses complete agreement among trilean values, useful for scenarios requiring consensus or uniformity across multiple indicators or conditions.

This library is developed to support scenarios in financial trading and analysis where decisions might hinge on more than binary outcomes. By incorporating modal logic aspects and providing a framework for handling uncertainty through the MA, LA, and IA operations, TUF_LOGIC bridges the gap between classical binary logic and the realities of uncertain information, making it a valuable tool for developing sophisticated trading strategies and analytical models.

Library "TUF_LOGIC"

3VL Implementation (TUF stands for True, Uncertain, False.)

method validate(self)

Ensures a valid trilean variable. This works by clamping the variable to the range associated with the trilean type.

Namespace types: tri

Parameters:

self (tri)

Returns: Validated trilean object.

method to_bool(self)

Converts a trilean object into a boolean object. True -> True, Uncertain -> na, False -> False.

Namespace types: tri

Parameters:

self (tri)

Returns: A boolean variable.

method NOT(self)

Negates the trilean object. True -> False, Uncertain -> Uncertain, False -> True

Namespace types: tri

Parameters:

self (tri)

Returns: Negated trilean object.

method AND(self, comparator)

Logical AND operation for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The first trilean object.

comparator (tri) : The second trilean object to compare with.

Returns: `tri` Result of the AND operation as a trilean object.

method OR(self, comparator)

Logical OR operation for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The first trilean object.

comparator (tri) : The second trilean object to compare with.

Returns: `tri` Result of the OR operation as a trilean object.

method EQUALITY(self, comparator)

Logical EQUALITY operation for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The first trilean object.

comparator (tri) : The second trilean object to compare with.

Returns: `tri` Result of the EQUALITY operation as a trilean object, True if both are equal, False otherwise.

method XOR(self, comparator)

Logical XOR (Exclusive OR) operation for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The first trilean object.

comparator (tri) : The second trilean object to compare with.

Returns: `tri` Result of the XOR operation as a trilean object.

method IMP_K(self, comparator)

Material implication using Kleene's logic for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The antecedent trilean object.

comparator (tri) : The consequent trilean object.

Returns: `tri` Result of the implication operation as a trilean object.

method IMP_L(self, comparator)

Logical implication using Łukasiewicz's logic for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The antecedent trilean object.

comparator (tri) : The consequent trilean object.

Returns: `tri` Result of the implication operation as a trilean object.

method IMP_RM3(self, comparator)

Logical implication using RM3 logic for trilean objects.

Namespace types: tri

Parameters:

self (tri) : The antecedent trilean object.

comparator (tri) : The consequent trilean object.

Returns: `tri` Result of the RM3 implication as a trilean object.

method MA(self)

Evaluates to True if the trilean object is either True or Uncertain, False otherwise.

Namespace types: tri

Parameters:

self (tri) : The trilean object to evaluate.

Returns: `tri` Result of the operation as a trilean object.

method LA(self)

Evaluates to True if the trilean object is True, False otherwise.

Namespace types: tri

Parameters:

self (tri) : The trilean object to evaluate.

Returns: `tri` Result of the operation as a trilean object.

method IA(self)

Evaluates to True if the trilean object is Uncertain, False otherwise.

Namespace types: tri

Parameters:

self (tri) : The trilean object to evaluate.

Returns: `tri` Result of the operation as a trilean object.

UNANIMOUS(self, comparator)

Evaluates the unanimity between two trilean values.

Parameters:

self (tri) : The first trilean value.

comparator (tri) : The second trilean value.

Returns: `tri` Returns True if both values are True, False if both are False, and Uncertain otherwise.

method UNANIMOUS(self)

Evaluates the unanimity among an array of trilean values.

Namespace types: array

Parameters:

self (array) : The array of trilean values.

Returns: `tri` Returns True if all values are True, False if all are False, and Uncertain otherwise.

tri

Three Value Logic (T.U.F.), or trilean. Can be True (1), Uncertain (0), or False (-1).

Fields:

v (series int) : Value of the trilean variable. Can be True (1), Uncertain (0), or False (-1).

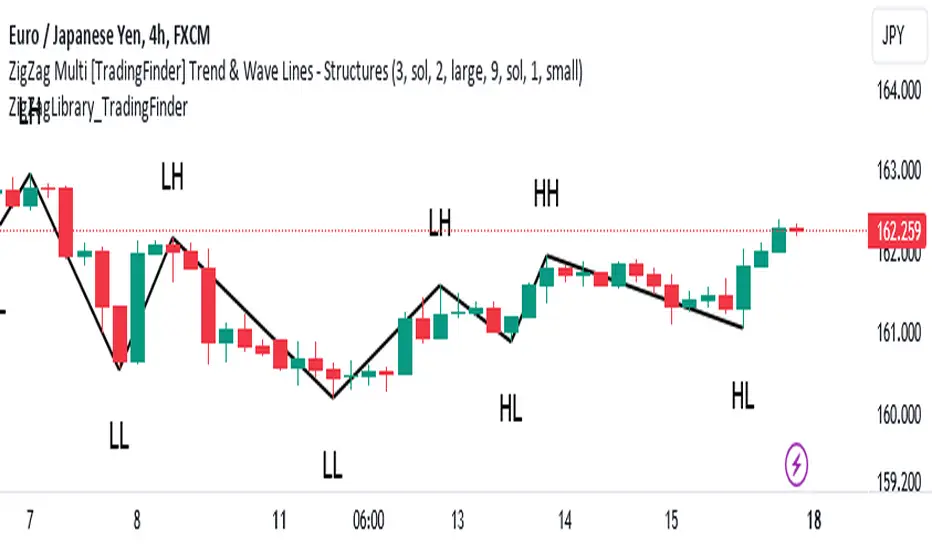

ZigZag Library [TradingFinder]🔵 Introduction

The "Zig Zag" indicator is an analytical tool that emerges from pricing changes. Essentially, it connects consecutive high and low points in an oscillatory manner. This method helps decipher price changes and can also be useful in identifying traditional patterns.

By sifting through partial price changes, "Zig Zag" can effectively pinpoint price fluctuations within defined time intervals.

🔵 Key Features

1. Drawing the Zig Zag based on Pivot points :

The algorithm is based on pivots that operate consecutively and alternately (switch between high and low swing). In this way, zigzag lines are connected from a swing high to a swing low and from a swing low to a swing high.

Also, with a very low probability, it is possible to have both low pivots and high pivots in one candle. In these cases, the algorithm tries to make the best decision to make the most suitable choice.

You can control what period these decisions are based on through the "PiPe" parameter.

2.Naming and labeling each pivot based on its position as "Higher High" (HH), "Lower Low" (LL), "Higher Low" (HL), and "Lower High" (LH).

Additionally, classic patterns such as HH, LH, LL, and HL can be recognized. All traders analyzing financial markets using classic patterns and Elliot Waves can benefit from the "zigzag" indicator to facilitate their analysis.

" HH ": When the price is higher than the previous peak (Higher High).

" HL ": When the price is higher than the previous low (Higher Low).

" LH ": When the price is lower than the previous peak (Lower High).

" LL ": When the price is lower than the previous low (Lower Low).

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/ZigZagLibrary_TradingFinder/1 as ZZ

Function "ZigZag" Parameters :

🟣 Logical Parameters

1. HIGH : You should place the "high" value here. High is a float variable.

2. LOW : You should place the "low" value here. Low is a float variable.

3. BAR_INDEX : You should place the "bar_index" value here. Bar_index is an integer variable.

4. PiPe : The desired pivot period for plotting Zig Zag is placed in this parameter. For example, if you intend to draw a Zig Zag with a Swing Period of 5, you should input 5.

PiPe is an integer variable.

Important :

Apart from the "PiPe" indicator, which is part of the customization capabilities of this indicator, you can create a multi-time frame mode for the indicator using 3 parameters "High", "Low" and "BAR_INDEX". In this way, instead of the data of the current time frame, use the data of other time frames.

Note that it is better to use the current time frame data, because using the multi-time frame mode is associated with challenges that may cause bugs in your code.

🟣 Setting Parameters

5. SHOW_LINE : It's a boolean variable. When true, the Zig Zag line is displayed, and when false, the Zig Zag line display is disabled.

6. STYLE_LINE : In this variable, you can determine the style of the Zig Zag line. You can input one of the 3 options: line.style_solid, line.style_dotted, line.style_dashed. STYLE_LINE is a constant string variable.

7. COLOR_LINE : This variable takes the input of the line color.

8. WIDTH_LINE : The input for this variable is a number from 1 to 3, which is used to adjust the thickness of the line that draws the Zig Zag. WIDTH_LINE is an integer variable.

9. SHOW_LABEL : It's a boolean variable. When true, labels are displayed, and when false, label display is disabled.

10. COLOR_LABEL : The color of the labels is set in this variable.

11. SIZE_LABEL : The size of the labels is set in this variable. You should input one of the following options: size.auto, size.tiny, size.small, size.normal, size.large, size.huge.

12. Show_Support : It's a boolean variable that, when true, plots the last support line, and when false, disables its plotting.

13. Show_Resistance : It's a boolean variable that, when true, plots the last resistance line, and when false, disables its plotting.

Suggestion :

You can use the following code snippet to import Zig Zag into your code for time efficiency.

//import Library

import TFlab/ZigZagLibrary_TradingFinder/1 as ZZ

// Input and Setting

// Zig Zag Line

ShZ = input.bool(true , 'Show Zig Zag Line', group = 'Zig Zag') //Show Zig Zag

PPZ = input.int(5 ,'Pivot Period Zig Zag Line' , group = 'Zig Zag') //Pivot Period Zig Zag

ZLS = input.string(line.style_dashed , 'Zig Zag Line Style' , options = , group = 'Zig Zag' )

//Zig Zag Line Style

ZLC = input.color(color.rgb(0, 0, 0) , 'Zig Zag Line Color' , group = 'Zig Zag') //Zig Zag Line Color

ZLW = input.int(1 , 'Zig Zag Line Width' , group = 'Zig Zag')//Zig Zag Line Width

// Label

ShL = input.bool(true , 'Label', group = 'Label') //Show Label

LC = input.color(color.rgb(0, 0, 0) , 'Label Color' , group = 'Label')//Label Color

LS = input.string(size.tiny , 'Label size' , options = , group = 'Label' )//Label size

Show_Support= input.bool(false, 'Show Last Support',

tooltip = 'Last Support' , group = 'Support and Resistance')

Show_Resistance = input.bool(false, 'Show Last Resistance',

tooltip = 'Last Resistance' , group = 'Support and Resistance')

//Call Function

ZZ.ZigZag(high ,low ,bar_index ,PPZ , ShZ ,ZLS , ZLC, ZLW ,ShL , LC , LS , Show_Support , Show_Resistance )

ZigZag LibraryThis is yet another ZigZag library.

🔵 Key Features

1. Lightning-Fast Performance : Optimized code ensures minimal lag and swift chart updates.

2. Real-Time Swing Detection : No more waiting for swings to finalize! This library continuously identifies the latest swing formation.

3. Amplitude-Aware : Discover significant swings earlier, even if they haven't reached the standard bar length.

4. Customizable Visualization : Draw ZigZag on-demand using polylines for a tailored analysis experience.

Stay tuned for more features as this library is being continuously enhanced. For the latest updates, please refer to the release information.

🔵 API

// Import this library. Remember to check the latest version of this library and replace the version number below.

import algotraderdev/zigzag/1 as zz

// Initialize the ZigZag instance.

var zz.ZigZag zig = zz.ZigZag.new().init(

zz.Settings.new(

swingLen = 5,

lineColor = color.blue,

lineStyle = line.style_solid,

lineWidth = 1))

// Analyze the ZigZag using the latest bar's data.

zig.tick()

// Draw the ZigZag.

if barstate.islast

zig.draw()

lib_fvgLibrary "lib_fvg"

further expansion of my object oriented library toolkit. This lib detects Fair Value Gaps and returns them as objects.

Drawing them is a separate step so the lib can be used with securities. It also allows for usage of current/close price to detect fill/invalidation of a gap and to adjust the fill level dynamically. FVGs can be detected while forming and extended indefinitely while they're unfilled.

method draw(this)

Namespace types: FVG

Parameters:

this (FVG)

method draw(fvgs)

Namespace types: FVG

Parameters:

fvgs (FVG )

is_fvg(mode, precondition, filter_insignificant, filter_insignificant_atr_factor, live)

Parameters:

mode (int) : switch for detection 1 for bullish FVGs, -1 for bearish FVGs

precondition (bool) : allows for other confluences to block/enable detection

filter_insignificant (bool) : allows to ignore small gaps

filter_insignificant_atr_factor (float) : allows to adjust how small (compared to a 50 period ATR)

live (bool) : allows to detect FVGs while the third bar is forming -> will cause repainting

Returns: a tuple of (bar_index of gap bar, gap top, gap bottom)

create_fvg(mode, idx, top, btm, filled_at_pc, config)

Parameters:

mode (int) : switch for detection 1 for bullish FVGs, -1 for bearish FVGs

idx (int) : the bar_index of the FVG gap bar

top (float) : the top level of the FVG

btm (float) : the bottom level of the FVG

filled_at_pc (float) : the ratio (0-1) that the fill source needs to retrace into the gap to consider it filled/invalidated/ready for removal

config (FVGConfig) : the plot configuration/styles for the FVG

Returns: a new FVG object if there was a new FVG, else na

detect_fvg(mode, filled_at_pc, precondition, filter_insignificant, filter_insignificant_atr_factor, live, config)

Parameters:

mode (int) : switch for detection 1 for bullish FVGs, -1 for bearish FVGs

filled_at_pc (float)

precondition (bool) : allows for other confluences to block/enable detection

filter_insignificant (bool) : allows to ignore small gaps

filter_insignificant_atr_factor (float) : allows to adjust how small (compared to a 50 period ATR)

live (bool) : allows to detect FVGs while the third bar is forming -> will cause repainting

config (FVGConfig)

Returns: a new FVG object if there was a new FVG, else na

method update(this, fill_src)

Namespace types: FVG

Parameters:

this (FVG)

fill_src (float) : allows for usage of different fill source series, e.g. high for bearish FVGs, low vor bullish FVGs or close for both

method update(all, fill_src)

Namespace types: FVG

Parameters:

all (FVG )

fill_src (float)

method remove_filled(unfilled_fvgs)

Namespace types: FVG

Parameters:

unfilled_fvgs (FVG )

method delete(this)

Namespace types: FVG

Parameters:

this (FVG)

method delete_filled_fvgs_buffered(filled_fvgs, max_keep)

Namespace types: FVG

Parameters:

filled_fvgs (FVG )

max_keep (int) : the number of filled, latest FVGs to retain on the chart.

FVGConfig

Fields:

box_args (|robbatt/lib_plot_objects/36;BoxArgs|#OBJ)

line_args (|robbatt/lib_plot_objects/36;LineArgs|#OBJ)

box_show (series__bool)

line_show (series__bool)

keep_filled (series__bool)

extend (series__bool)

FVG

Fields:

config (|FVGConfig|#OBJ)

startbar (series__integer)

mode (series__integer)

top (series__float)

btm (series__float)

center (series__float)

size (series__float)

fill_size (series__float)

fill_lvl_target (series__float)

fill_lvl_current (series__float)

fillbar (series__integer)

filled (series__bool)

_fvg_box (|robbatt/lib_plot_objects/36;Box|#OBJ)

_fill_line (|robbatt/lib_plot_objects/36;Line|#OBJ)

arraysLibrary "arraymethods"

Supplementary array methods.

delete(arr, index)

remove int object from array of integers at specific index

Parameters:

arr : int array

index : index at which int object need to be removed

Returns: void

delete(arr, index)

remove float object from array of float at specific index

Parameters:

arr : float array

index : index at which float object need to be removed

Returns: float

delete(arr, index)

remove bool object from array of bool at specific index

Parameters:

arr : bool array

index : index at which bool object need to be removed

Returns: bool

delete(arr, index)

remove string object from array of string at specific index

Parameters:

arr : string array

index : index at which string object need to be removed

Returns: string

delete(arr, index)

remove color object from array of color at specific index

Parameters:

arr : color array

index : index at which color object need to be removed

Returns: color

delete(arr, index)

remove line object from array of lines at specific index and deletes the line

Parameters:

arr : line array

index : index at which line object need to be removed and deleted

Returns: void

delete(arr, index)

remove label object from array of labels at specific index and deletes the label

Parameters:

arr : label array

index : index at which label object need to be removed and deleted

Returns: void

delete(arr, index)

remove box object from array of boxes at specific index and deletes the box

Parameters:

arr : box array

index : index at which box object need to be removed and deleted

Returns: void

delete(arr, index)

remove table object from array of tables at specific index and deletes the table

Parameters:

arr : table array

index : index at which table object need to be removed and deleted

Returns: void

delete(arr, index)

remove linefill object from array of linefills at specific index and deletes the linefill

Parameters:

arr : linefill array

index : index at which linefill object need to be removed and deleted

Returns: void

popr(arr)

remove last int object from array

Parameters:

arr : int array

Returns: int

popr(arr)

remove last float object from array

Parameters:

arr : float array

Returns: float

popr(arr)

remove last bool object from array

Parameters:

arr : bool array

Returns: bool

popr(arr)

remove last string object from array

Parameters:

arr : string array

Returns: string

popr(arr)

remove last color object from array

Parameters:

arr : color array

Returns: color

popr(arr)

remove and delete last line object from array

Parameters:

arr : line array

Returns: void

popr(arr)

remove and delete last label object from array

Parameters:

arr : label array

Returns: void

popr(arr)

remove and delete last box object from array

Parameters:

arr : box array

Returns: void

popr(arr)

remove and delete last table object from array

Parameters:

arr : table array

Returns: void

popr(arr)

remove and delete last linefill object from array

Parameters:

arr : linefill array

Returns: void

shiftr(arr)

remove first int object from array

Parameters:

arr : int array

Returns: int

shiftr(arr)

remove first float object from array

Parameters:

arr : float array

Returns: float

shiftr(arr)

remove first bool object from array

Parameters:

arr : bool array

Returns: bool

shiftr(arr)

remove first string object from array

Parameters:

arr : string array

Returns: string

shiftr(arr)

remove first color object from array

Parameters:

arr : color array

Returns: color

shiftr(arr)

remove and delete first line object from array

Parameters:

arr : line array

Returns: void

shiftr(arr)

remove and delete first label object from array

Parameters:

arr : label array

Returns: void

shiftr(arr)

remove and delete first box object from array

Parameters:

arr : box array

Returns: void

shiftr(arr)

remove and delete first table object from array

Parameters:

arr : table array

Returns: void

shiftr(arr)

remove and delete first linefill object from array

Parameters:

arr : linefill array

Returns: void

push(arr, val, maxItems)

add int to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : int array

val : int object to be pushed

maxItems : max number of items array can hold

Returns: int

push(arr, val, maxItems)

add float to the end of an array with max items cap. Objects are removed from start to maintain max items cap

Parameters:

arr : float array

val : float object to be pushed

maxItems : max number of items array can hold

Returns: float