Illyad Strategy 1.0 - Automate your alerts by connecting to MT5Illyad Strategy 1.0 – Automated Prop Trading System (30m Timeframe)

Description:

The Illyad Strategy 1.0 is a rule-based automated trading system designed for serious traders and prop-firm challenges.

🔑 Key Features:

Optimised to work best on the 30-minute timeframe.

Built-in money management to keep drawdown controlled.

Dynamic stop-loss / take-profit levels.

Works across forex, indices, and stocks.

Compatible with TradingView alerts → MT5 automation.

⚙️ Optimisation:

Each symbol has its own behaviour. For best results, you should optimise the parameters (moving averages, signal intensity, SL/TP ratios) on the symbol you want to trade. The algo adapts differently to EURUSD vs NASDAQ vs stocks like TSLA, so proper tuning is critical.

💡 Best Use Case:

Prop firm accounts (FTMO, MyForexFunds, AquaFunded, etc.).

Consistent returns without emotional decision-making.

Traders who want to scale multiple accounts at once.

⚠️ Disclaimer:

This script is for educational purposes. Past results do not guarantee future returns. Always backtest and forward test on demo before going live.

📲 Next Step:

This is the public version. If you’d like to connect it directly to MT5/MT4 for fully automated trading, visit my profile or contact me for details.

移動平均線

Simple SMA StrategySimple strategy to buy based on closing above SMA, and sell based on closing below SMA.

You can change the SMA value and your start date to customize the strategy for your initial entry date and SMA value. SMA is based on chart time frame.

SPX EMA 9/21 + VWAP Strategy1. Temporality: 2 minutes.

2. EMA 9 and EMA 21:

• Purchase Call: when EMA 9 crosses up EMA 21 and the price is > VWAP.

• Put : when EMA 9 crosses down EMA 21 and the price is < VWAP.

3. Stop and Take Profit:

• Stop: candle closure on the other side of the VWAP.

• TP: configurable in points (e.g. +10 pts, +20 pts) or up to the opposite crossing of EMAs.

• Long enters when EMA 9 crosses up 21 and the price is above VWAP.

• Short enters when the EMA 9 crosses down the 21 and the price is below VWAP.

• TP and SL in SPX points (configurable in inputs).

• You can run in 2 minutes on SPX.

EMA and BB Analysis for US100 V250829This TradingView strategy generates buy and sell signals based on exponential moving average (EMA) crossovers, limited by other factors such as Bollinger Bands, volume, and EMA distance.

It uses EMAs of 16, 24, 32, and 64 periods, as well as the angles of each of these EMAs.

Entry Conditions:

EMA Crossover Entry:

When EMA16 crosses EMA64 and the following conditions are met:

EMA16, EMA24, EMA32 are aligned — for a buy signal:

EMA16 > EMA24

EMA24 > EMA32

EMA32 > EMA48

(and the opposite for a sell signal)

EMA Angles:

The angles of the EMAs must also follow the same alignment.

Divergence Entry:

When the distance between EMAs 16, 24, 32, and 48 increases.

Entry Limitations:

Once an entry is detected, it is filtered by several conditions:

When the distance between the entry candle and EMA96 is more than two candles of the maximum size over three periods.

The stop loss is set as two candles of the maximum size over three periods. If this stop loss exceeds 6,000 points (adjustable parameter), the entry is invalid.

When the price is at the edge of the Bollinger Band with a 1200-period setting (equivalent to a 1-hour Bollinger Band).

When the Bollinger Band's middle line is descending and a buy signal is triggered (and vice versa).

When volume drops below a certain threshold.

When a sideways market movement is detected.

All these entry limitations are configurable parameters and can be enabled or disabled.

EMA 1/8 Cross - Fixed Pip TP/SLEMA 1/8 Cross – Fixed Pip TP/SL

This strategy is based on the crossover between EMA 8 and EMA 14 as trading signals:

Long entry → when EMA 1 crosses above EMA 8

Short entry → when EMA 1 crosses below EMA 8

Features:

Fixed pip Take Profit (TP) and Stop Loss (SL), fully adjustable in the settings.

Customizable EMA Fast/Slow lengths for optimization.

Pip size input to match different broker definitions (e.g., XAUUSD often uses 0.10 as one pip).

Suitable for testing scalping or swing trading across multiple timeframes.

⚠️ Disclaimer:

This script is intended for backtesting and educational purposes only. Please optimize parameters and apply proper risk management before using it on live accounts.

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

MACDEMAAutomatic Strategy for Litecoin on 5-Minute Chart in BingX Perpetual Futures. Combines MACD and 10- & 55-Period EMA. ✅

JeropasMG v17This bot uses a martingale strategy applied to simple moving average crossover signals.

When a buy or sell signal is generated, it opens a position with the configured base size.

If the trade is a loser, the bot increases the size of the next entry by multiplying it by the defined factor (for example, x2), repeating the process until the maximum number of steps allowed is reached.

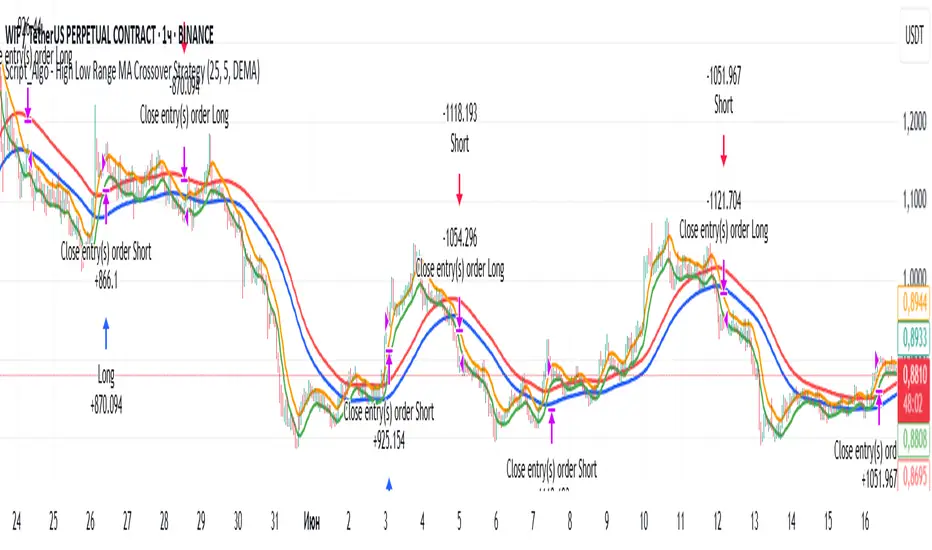

Script_Algo - High Low Range MA Crossover Strategy🎯 Core Concept

This strategy uses modified moving averages crossover, built on maximum and minimum prices, to determine entry and exit points in the market. A key advantage of this strategy is that it avoids most false signals in trendless conditions, which is characteristic of traditional moving average crossover strategies. This makes it possible to improve the risk/reward ratio and, consequently, the strategy's profitability.

📊 How the Strategy Works

Main Mechanism

The strategy builds 4 moving averages:

Two senior MAs (on high and low) with a longer period

Two junior MAs (on high and low) with a shorter period

Buy signal 🟢: when the junior MA of lows crosses above the senior MA of highs

Sell signal 🔴: when the junior MA of highs crosses below the senior MA of lows

As seen on the chart, it was potentially possible to make 9X on the WIFUSDT cryptocurrency pair in just a year and a half. However, be careful—such results may not necessarily be repeated in the future.

Special Feature

Position closing priority ❗: if an opposite signal arrives while a position is open, the strategy first closes the current position and only then opens a new one

⚙️ Indicator Settings

Available Moving Average Types

EMA - Exponential MA

SMA - Simple MA

SSMA - Smoothed MA

WMA - Weighted MA

VWMA - Volume Weighted MA

RMA - Adaptive MA

DEMA - Double EMA

TEMA - Triple EMA

Adjustable Parameters

Senior MA Length - period for long-term moving averages

Junior MA Length - period for short-term moving averages

✅ Advantages of the Strategy

🛡️ False Signal Protection - using two pairs of modified MAs reduces the number of false entries

🔄 Configuration Flexibility - ability to choose MA type and calculation periods

⚡ Automatic Switching - the strategy automatically closes the current position when receiving an opposite signal

📈 Visual Clarity - all MAs are displayed on the chart in different colors

⚠️ Disadvantages and Risks

📉 Signal Lag - like all MA-based strategies, it may provide delayed signals during sharp movements

🔁 Frequent Switching - in sideways markets, it may lead to multiple consecutive position openings/closings

📊 Requires Optimization - optimal parameters need to be selected for different instruments and timeframes

💡 Usage Recommendations

Backtest - test the strategy's performance on historical data

Optimize Parameters - select MA periods suitable for the specific trading instrument

Use Filters - add additional filters to confirm signals

Manage Risks - always use stop-loss and take-profit orders.

You can safely connect to the exchange via webhook and enjoy trading.

Good luck and profits to everyone!!

Quanta Trading Course - Basic StrategyA simple Trading strategy optimize for Nifty 1 Hour Chart. Which is Long only.

EMA Crossover StrategyAs the name suggests. It is an EMA crossover with a custom buy, sell signal on the chart with the take profit signal on the chart itself. SL would be the original candle low on the candle where the buy sell signal is generated. kindly give a feedback on the script so i can update it.

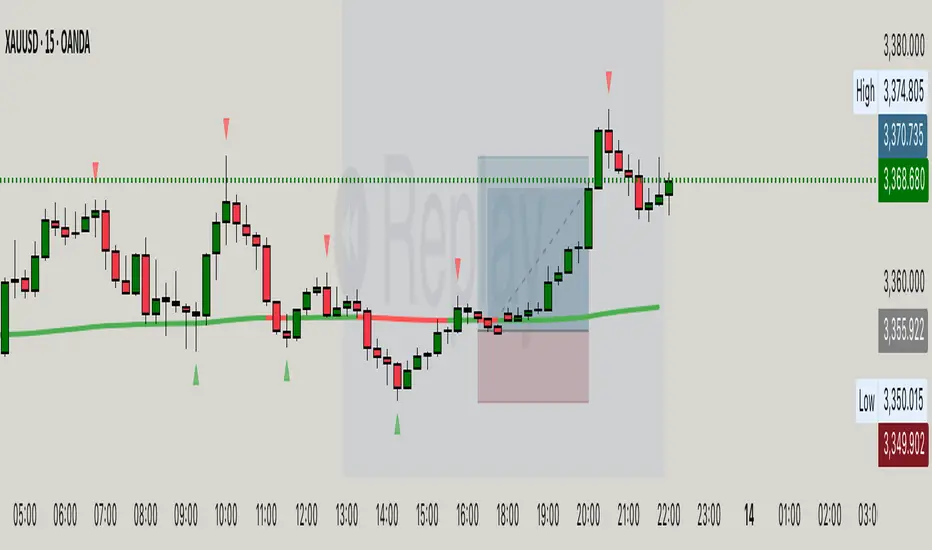

XAUUSD Trap & Reversal ScannerThis strategy is designed for XAUUSD (Gold) on 5m/15m timeframes.

It detects and trades reversal traps confirmed by classic patterns:

Double Tops / Double Bottoms

Head & Shoulders / Inverse H&S

Fair Value Gaps (FVG / IFVG)

Trap Sweeps (stop hunts)

Additional filters:

EMA200 trend confirmation

London & New York trading session filter (12:00–17:00 UTC)

Risk management with ATR-based stop loss

Partial profit-taking (50% at 1:1, remainder at 1:RR up to 1:4)

Script_Algo - Fibo Correction Strategy🔹 Core Concept

The strategy is built on combining Fibonacci retracement levels, candlestick pattern confirmation, and trend filtering for trade selection. It performs well on the 1-hour timeframe across many cryptocurrency pairs. Particularly on LINKUSDT over the past year and a half, despite the not very optimal 1:1 risk/reward ratio.

The logic is simple: after a strong impulse move, the price often retraces to key Fibonacci levels (specifically, the 61.8% level). If a confirming candlestick (pattern) appears at this moment, the strategy looks for an entry in the direction of the main trend.

🔹 Indicators Used in the Strategy

ATR (Average True Range) — Used to calculate the stop-loss and take-profit levels.

EMA (9 and 21) — Additional moving averages for assessing the direction of movement (not directly used in entry conditions, but the logic can be expanded to include them).

SMA (Trend Filter, 20 by default) — The trend direction filter. Trades are only opened in its direction.

Fibonacci Levels — The 61.8% retracement level is calculated based on the high and low of the previous candle.

🔹 Entry Conditions

🟢 Long (Buy):

Previous Candle:

Must be green (close higher than open).

Must have a body not smaller than a specified minimum.

The upper wick must not exceed 30% of the body size.

→ This filters out "weak" or "indecisive" candles.

Current Candle:

Price touches or breaches the Fibonacci 61.8% retracement level from the previous range.

Closes above this level.

Closes above the Trend Filter (SMA) line.

A position is opened only if there are no other open trades at the moment.

🔴 Short (Sell):

Previous Candle:

Must be red (close lower than open).

Must have a body not smaller than a specified minimum.

The lower wick must not exceed 30% of the body size.

Current Candle:

Price touches or breaches the Fibonacci 61.8% retracement level from the previous range.

Closes below this level.

Closes below the Trend Filter (SMA) line.

A trade is opened only if there are no other open positions.

🔹 Risk Management

Stop-Loss = ATR × multiplier (default is 5).

Take-Profit = ATR × the same multiplier.

Thus, the default risk/reward ratio is 1:1, but it can be easily adjusted by changing the coefficient. Although, strangely enough, this ratio has shown the best results on some assets on the 1-hour timeframe.

🔹 Chart Visualization

Fibonacci level for Long — Green line with circles.

Fibonacci level for Short — Red line with circles.

Trend Filter line (SMA) — Blue.

🔹 Strengths of the Strategy

✅ Utilizes a proven market pattern — retracement to the 61.8% level.

✅ Further filters entries using trend and candlestick patterns.

✅ Simple, transparent logic that is easy to expand (e.g., adding other Fib levels, an EMA filter, etc.).

🔹 Limitations

⚠️ Performs better in trending markets; can generate false signals during ranging (sideways) conditions.

⚠️ The fixed 1:1 risk/reward ratio is not always optimal and could be refined.

⚠️ Performance depends on the selected timeframe and ATR parameters.

📌 Summary:

The strategy seeks corrective entries in the direction of the trend, confirmed by candlestick patterns. It is versatile and can be applied to forex pairs, cryptocurrencies, and stocks.

⚠️ Not financial advice. Pay close attention to risk management to avoid blowing your account. The strategy is not repainting — I have personally verified it through real testing — but it may not necessarily replicate the same results in the future, as the market is constantly changing. Test it, profit, and good luck to everyone!

Golden Cross Strategy & BacktesterGolden Cross Strategy & Backtester 📈🚀

Overview

This script provides a complete backtesting environment for the classic Golden Cross trend-following strategy. It is designed to be simple, visual, and easy to use. 💪

The strategy operates on the following logic:

🔼 Long Entry: A "Buy" signal is generated when the short-term moving average (Short MA) crosses above the long-term moving average (Long MA).

🔽 Exit: The position is closed when the short-term moving average crosses back below the long-term moving average (a "Death Cross").

The background of the chart will be shaded green 🎨 during periods when the strategy is holding an active position.

How to Use for Backtesting 🔬

This is a strategy script, which means its main purpose is to test the historical performance of this trading idea.

Add this script to your chart.

Open the "Strategy Tester" panel at the bottom of your chart.

In the "Overview" and "Performance" tabs, you can see detailed results 📊, such as the Net Profit and Max Drawdown, to evaluate the strategy's effectiveness.

Customization ⚙️

You can easily customize the strategy's parameters without editing the code.

Click the Settings/Gear icon (⚙️) next to the script's name on your chart.

In the "Inputs" tab, you can change:

📏 Short MA Length: The period for the fast-moving average (default is 50).

📏 Long MA Length: The period for the slow-moving average (default is 200).

In the "Properties" tab, you can change:

💰 Initial Capital: The starting balance for the backtest.

Feel free to test different settings to find what works best for your preferred asset and timeframe! Happy testing! 🎉

K-TREND Strategy k trend is very useful and high profitablility , it gives entry signals with buy/sell entry signalwith stoploss and targets

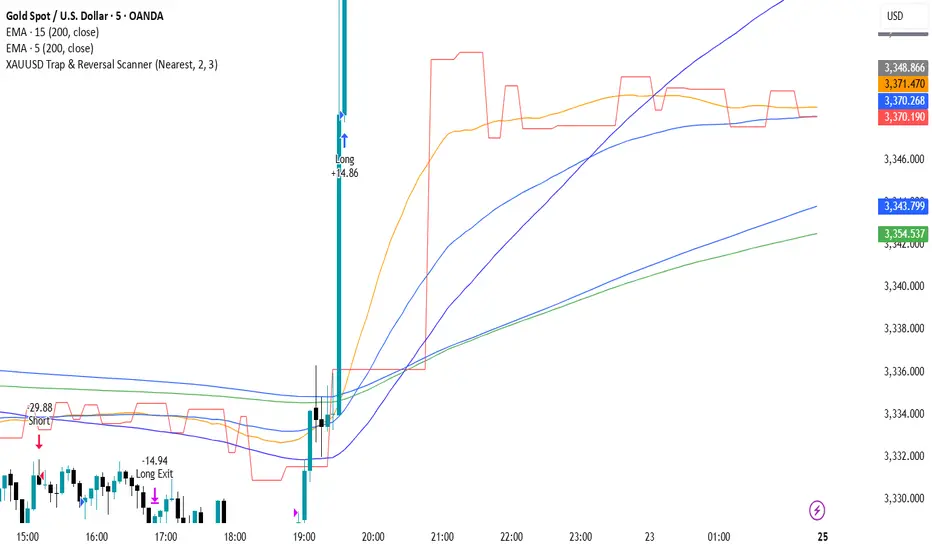

PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

Panda's Orb StrategyORB strategy I created using ChatGBT!

Please message me for any bugs or recomendations!

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable

Combines multiple layers of confirmation: EMA bands + FVG + RSI

Adaptive to volatility: ATR-based exits scale with market conditions

Clear, actionable visuals: Easy to monitor and manage trades

MomentumThe strategy uses EMA200, ADX/DMI, RSI, and volume. Pivot levels and Heikin-Ashi ensure safe entries, while cooldowns and opposite-locks prevent overtrading. Exits are managed with ATR trailing stops and trend-reversal signals.

Hassi XAUUSD Advanced FVG EMA/BOS/RSI/Volume + Session FilterWhat it does :

This strategy automates a popular ICT-style idea on XAUUSD (Gold): trade only when price taps back into a Fair Value Gap (FVG), but filter entries with trend, structure, momentum, volume, and session rules. It manages risk with fixed TP/SL (points) and shows a compact backtest panel on chart.

Core Logic

1) Market Structure (BOS)

Detects recent swing highs/lows and flags a Break of Structure:

BOS Up when price breaks the latest swing high.

BOS Down when price breaks the latest swing low.

2) FVG Detection (3-candle)

Bullish FVG when low > high and low > high .

Bearish FVG when high < low and high < low .

The most recent qualifying gap is drawn as a shaded box (optional).

3) Bias & Filters

Trend Bias: price vs EMA (default 200). Longs only above EMA; shorts only below.

Momentum: optional RSI filter (default 14); avoid longs in OB & shorts in OS.

Volume: optional filter requiring current volume > SMA(20) × multiplier.

Sessions: optional London / New York (PKT) time windows.

Entries & Exits

Long Entry (all must be true)

Above EMA, RSI bullish, volume ok, session ok, BOS Up.

A recent Bullish FVG exists (within N bars).

Price taps back into the FVG (low ≤ top & close > bottom) with a bullish candle.

Short Entry (mirror)

Below EMA, RSI bearish, volume ok, session ok, BOS Down.

A recent Bearish FVG exists (within N bars).

Price taps (high ≥ bottom & close < top) with a bearish candle.

Risk / R:R

Exits use fixed points on XAUUSD (default TP 100, SL 50).

On many gold feeds 1.0 = 10 points; inputs convert to price automatically.

“One-trade-at-a-time”: a new signal won’t fire until the previous position is flat.

Chart Labels

On entry, the script plots BUY/SELL plus fixed TP/SL lines & labels anchored to the entry bar (they don’t drift with price).

Visuals & Tools

EMA line (green/red by bias).

Swing points (tiny triangles) to see structure.

FVG boxes (green/red, optional).

Session shading (subtle blue overlay).

Stats Panel (top-right):

Total Trades, TP Hits, SL Hits, Win Rate, Profit Factor, Net P&L.

Inputs (quick guide)

EMA Length (default 200)

Swing Lookback for BOS (default 5)

FVG Box Length (how far the zone extends to the right)

TP / SL (points) for XAUUSD + display Risk:Reward

Sessions (PKT): London & New York windows + toggle

Filters: Volume (multiplier), RSI (length, OB/OS)

Visibility: show/hide FVG boxes & TP/SL drawings

Alerts

Buy Signal / Sell Signal on valid entries

Position Opened / Position Closed notifications

Best Practices & Notes

Designed for XAUUSD 15-minute. You can test other timeframes, but retune TP/SL points and filters accordingly.

Broker ticks differ: if your symbol steps are not 0.1, adjust TP/SL points.

Use with a HTF confluence (e.g., D1/4H bias, key S/R, news awareness).

Backtests are approximations; real results vary with spreads, slippage, and execution.

Disclaimer: This tool is for educational purposes. It is not financial advice. Always test before using on live capital.