MoneyMakers Scalping Signals1-5 min frame, a versatile market indicator designed to highlight emerging trends and structural shifts in crypto price action before they fully develop. By combining price dynamics, momentum behavior and market context into a clean visual output, it helps traders make more informed decisions without noise or lag. Suitable for both short- and mid-term analysis, the indicator offers a clearer view of potential reversal zones, trend continuations and key market cycles.

Multitimeframe

RSI Trendline Breakout BB Exit -by RiazMalikUse this strategy based on RSI and bolinger bands

When RSI trend line breaks take position when RSI touches bolinger bands exit

ETH Trading bot H1 Money maker i dont know what i did but it is looking good ; make sure you arent in a trade before you start the bot

PA SystemPA System

短简介 Short Description(放在最上面)

中文:

PA System 是一套以 AL Brooks 价格行为为核心的策略(Strategy),将 结构(HH/HL/LH/LL)→ 回调(H1/L1)→ 二次入场(H2/L2 微平台突破) 串成完整可回测流程,并可选叠加 BoS/CHoCH 结构突破过滤 与 Liquidity Sweep(扫流动性)确认。内置风险管理:定风险仓位、部分止盈、保本、移动止损、时间止损、冷却期。

English:

PA System is an AL Brooks–inspired Price Action strategy that chains Market Structure (HH/HL/LH/LL) → Pullback (H1/L1) → Second Entry (H2/L2 via Micro Range Breakout) into a complete backtestable workflow, with optional BoS/CHoCH structure-break filtering and Liquidity Sweep confirmation. Built-in risk management includes risk-based sizing, partial exits, breakeven, trailing stops, time stop, and cooldown.

⸻

1) 核心理念 Core Idea

中文:

这不是“指标堆叠”,而是一条清晰的价格行为决策链:

结构确认 → 回调出现 → 小平台突破(二次入场)→ 风控出场。

策略把 Brooks 常见的“二次入场”思路程序化,同时用可选的结构突破与扫流动性模块提升信号质量、减少震荡误入。

English:

This is not an “indicator soup.” It’s a clear price-action decision chain:

Confirmed structure → Pullback → Micro-range breakout (second entry) → Risk-managed exits.

The system programmatically implements the Brooks-style “second entry” concept, and optionally adds structure-break and liquidity-sweep context to reduce chop and improve trade quality.

⸻

2) 主要模块 Main Modules

A. 结构识别 Market Structure (HH/HL/LH/LL)

中文:

使用 pivot 摆动点确认结构,标记 HH/HL/LH/LL,并可显示最近一组摆动水平线,方便对照结构位置。

English:

Uses confirmed pivot swings to label HH/HL/LH/LL and optionally plots the most recent swing levels for clean structure context.

B. 状态机 Market Regime (State Machine + “Always In”)

中文:

基于趋势K强度、EMA关系与波动范围,识别市场环境(Breakout/Channel/Range)以及 Always-In 方向,用于过滤不合适的交易环境。

English:

A lightweight regime engine detects Breakout/Channel/Range and an “Always In” directional bias using momentum and EMA/range context to avoid low-quality conditions.

C. 二次入场 Second Entry Engine (H1→H2 / L1→L2)

中文:

• H1/L1:回调到结构附近并出现反转迹象

• H2/L2:在 H1/L1 后等待最小 bars,然后触发 Micro Range Breakout(小平台突破)并要求信号K收盘强度达标

这一段是策略的“主发动机”。

English:

• H1/L1: Pullback into structure with reversal intent

• H2/L2: After a minimum wait, triggers on Micro Range Breakout plus a configurable close-strength filter

This is the main “entry engine.”

D. 可选过滤器 Optional Filters (Quality Boost)

BoS/CHoCH(结构突破过滤)

中文: 可识别 BoS / CHoCH,并可要求“入场前最近 N bars 必须有同向 break”。

English: Detects BoS/CHoCH and can require a recent same-direction break within N bars.

Liquidity Sweeps(扫流动性确认)

中文: 画出 pivot 高/低的流动性水平线,检测“刺破后收回”的 sweep,并可要求入场前出现同向 sweep。

English: Tracks pivot-based liquidity levels, confirms sweeps (pierce-and-reclaim), and can require a recent sweep before entry.

E. FVG 可视化 FVG Visualization

中文: 提供 FVG 区域盒子与管理模式(仅保留未回补 / 仅保留最近N),主要用于区域理解与复盘,不作为强制入场条件(可自行扩展)。

English: Displays FVG boxes with retention modes (unfilled-only or last-N). Primarily for context/analysis; not required for entries (you can extend it as a filter/target).

⸻

3) 风险管理 Risk Management (Built-In)

中文:

• 定风险仓位:按账户权益百分比计算仓位

• SL/TP:基于结构 + ATR 缓冲,且限制最大止损 ATR 倍

• 部分止盈:到达指定 R 后减仓

• 保本:到达指定 R 后推到 BE

• 移动止损:到达指定 R 后开始跟随

• 时间止损:持仓太久不动则退出

• 冷却期:出场后等待 N bars 再允许新单

English:

• Risk-based sizing: position size from equity risk %

• SL/TP: structure + ATR buffer with max ATR risk cap

• Partial exits at an R threshold

• Breakeven at an R threshold

• Trailing stop activation at an R threshold

• Time stop to reduce chop damage

• Cooldown after exit to avoid rapid re-entries

⸻

4) 推荐使用方式 Recommended Usage

中文:

• 推荐从 5m / 15m / 1H 开始测试

• 想更稳:开启 EMA Filter + Break Filter + Sweep Filter,并提高 Close Strength

• 想更多信号:关闭 Break/Sweep 过滤或降低 Swing Length / Close Strength

• 回测时务必设置合理的手续费与滑点,尤其是期货/指数

English:

• Start testing on 5m / 15m / 1H

• For higher quality: enable EMA Filter + Break Filter + Sweep Filter and increase Close Strength

• For more signals: disable Break/Sweep filters or reduce Swing Length / Close Strength

• Use realistic commissions/slippage in backtests (especially for futures/indices)

⸻

5) 重要说明 Notes

中文:

结构 pivot 需要右侧确认 bars,因此结构点存在天然滞后(确认后不会再变)。策略逻辑尽量避免不必要的对象堆叠,并对数组/对象做了稳定管理,适合长期运行与复盘。

English:

Pivot-based structure requires right-side confirmation (inherent lag; once confirmed it won’t change). The script is designed for stability and resource-safe object management, suitable for long sessions and review.

⸻

免责声明 Disclaimer(建议原样保留)

中文:

本脚本仅用于教育与研究目的,不构成任何投资建议。策略回测结果受市场条件、手续费、滑点、交易时段、数据质量等影响显著。使用者需自行验证并承担全部风险。过往表现不代表未来结果。

English:

This script is for educational and research purposes only and does not constitute financial advice. Backtest results are highly sensitive to market conditions, fees, slippage, session settings, and data quality. Use at your own risk. Past performance is not indicative of future results.

CryptoFlux Dynamo [JOAT]CryptoFlux Dynamo: Velocity Scalping Strategy

WHAT THIS STRATEGY IS

CryptoFlux Dynamo is an open-source Pine Script v6 strategy designed for momentum-based scalping on cryptocurrency perpetual futures. It combines multiple technical analysis methods into a unified system that adapts its behavior based on current market volatility conditions.

This script is published open-source so you can read, understand, and modify the complete logic. The description below explains everything the strategy does so that traders who cannot read Pine Script can fully understand how it works before using it.

HOW THIS STRATEGY IS ORIGINAL AND WHY THE INDICATORS ARE COMBINED

This strategy uses well-known indicators (MACD, EMA, RSI, MFI, Bollinger Bands, Keltner Channels, ATR). The originality is not in the individual indicators themselves, but in the specific way they are integrated into a regime-adaptive system. Here is the detailed justification for why these components are combined and how they work together:

The Problem Being Solved:

Standard indicator-based strategies use fixed thresholds. For example, a typical MACD strategy might enter when the histogram crosses above zero. However, in cryptocurrency markets, volatility changes dramatically throughout the day and week. A MACD crossover during a low-volatility consolidation period has very different implications than the same crossover during a high-volatility trending period. Using the same entry thresholds and stop distances in both conditions leads to either:

Too many false signals during consolidation (if thresholds are loose)

Missing valid opportunities during expansion (if thresholds are tight)

Stops that are too tight during volatility spikes (causing premature exits)

Stops that are too wide during compression (giving back profits)

The Solution Approach:

This strategy first classifies the current volatility regime using normalized ATR (ATR as a percentage of price), then dynamically adjusts ALL other parameters based on that classification. This creates a context-aware system rather than a static threshold comparison.

How Each Component Contributes to the System:

ATR-Based Regime Classification (The Foundation)

The strategy calculates ATR over 21 periods, smooths it with a 13-period EMA to reduce noise from wicks, then divides by price to get a normalized percentage. This ATR% is classified into three regimes:

- Compression (ATR% < 0.8%): Market is consolidating, breakouts are more likely but false signals are common

- Expansion (ATR% 0.8% - 1.6%): Normal trending conditions

- Velocity (ATR% > 1.6%): High volatility, larger moves but also larger adverse excursions

This regime classification then controls stop distances, profit targets, trailing stop offsets, and signal strength requirements. The regime acts as a "meta-parameter" that tunes the entire system.

EMA Ribbon (8/21/34) - Trend Structure Detection

The three EMAs establish trend direction and structure. When EMA 8 > EMA 21 > EMA 34, the trend structure is bullish. The slope of the middle EMA (21) is calculated over 8 bars and converted to degrees using arctangent. This slope measurement quantifies trend strength, not just direction.

Why these specific periods? The 8/21/34 sequence follows Fibonacci-like spacing and provides good separation on 5-minute cryptocurrency charts. The fast EMA (8) responds to immediate price action, the mid EMA (21) represents the short-term trend, and the slow EMA (34) acts as a trend filter.

The EMA ribbon works with the regime classification: during compression regimes, the strategy requires stronger ribbon alignment before entry because false breakouts are more common.

MACD (8/21/5) - Momentum Measurement

The MACD uses faster parameters (8/21/5) than the standard (12/26/9) because cryptocurrency markets move faster than traditional markets. The histogram is smoothed with a 5-period EMA to reduce noise.

The key innovation is the adaptive histogram baseline. Instead of using a fixed threshold, the strategy calculates a rolling baseline from the smoothed absolute histogram value, then multiplies by a sensitivity factor (1.15). This means the threshold for "significant momentum" automatically adjusts based on recent momentum levels.

The MACD works with the regime classification: during velocity regimes, the histogram baseline is effectively higher because recent momentum has been stronger, preventing entries on relatively weak momentum.

RSI (21 period) and MFI (21 period) - Independent Momentum Confirmation

RSI measures momentum using price changes only. MFI (Money Flow Index) measures momentum using price AND volume. By requiring both to confirm, the strategy filters out price moves that lack volume support.

The 21-period length is longer than typical (14) to reduce noise on 5-minute charts. The trigger threshold (55 for longs, 45 for shorts) is slightly offset from 50 to require momentum in the trade direction, not just neutral readings.

These indicators work together: a signal requires RSI > 55 AND MFI > 55 for longs. This dual confirmation reduces false signals from price manipulation or low-volume moves.

Bollinger Bands (1.5 mult) and Keltner Channels (1.8 mult) - Squeeze Detection

When Bollinger Bands contract inside Keltner Channels, volatility is compressing and a breakout is likely. This is the "squeeze" condition. When the bands expand back outside the channels, the squeeze "releases."

The strategy uses a 1.5 multiplier for Bollinger Bands (tighter than standard 2.0) and 1.8 for Keltner Channels. These values were chosen to identify meaningful squeezes on 5-minute cryptocurrency charts without triggering too frequently.

The squeeze detection works with the regime classification: squeeze releases during compression regimes receive additional signal strength points because breakouts from consolidation are more significant.

Volume Impulse Detection - Institutional Participation Filter

The strategy calculates a volume baseline (34-period SMA) and standard deviation. A "volume impulse" is detected when current volume exceeds the baseline by 1.15x OR when the volume z-score exceeds 0.5.

This filter ensures entries occur when there is meaningful market participation, not during low-volume periods where price moves are less reliable.

Volume impulse is required for all entries and adds points to the composite signal strength score.

Cycle Oscillator - Trend Alignment Filter

The strategy calculates a 55-period EMA as a cycle basis, then measures price deviation from this basis as a percentage. When price is more than 0.15% above the cycle basis, the cycle is bullish. When more than 0.15% below, the cycle is bearish.

This filter prevents counter-trend entries. Long signals require bullish cycle alignment; short signals require bearish cycle alignment.

BTC Dominance Filter (Optional) - Market Regime Filter

The strategy can optionally use BTC.D (Bitcoin Dominance) as a market regime filter. When BTC dominance is rising (slope > 0.12), the market is in "risk-off" mode and long entries on altcoins are filtered. When dominance is falling (slope < -0.12), short entries are filtered.

This filter is optional because the BTC.D data feed may lag during low-liquidity periods.

How The Components Work Together (The Mashup Justification):

The strategy uses a composite scoring system where each signal pathway contributes points:

Trend Break pathway (30 points): Requires EMA ribbon alignment + positive slope + price breaks above recent structure high

Momentum Surge pathway (30 points): Requires MACD histogram > adaptive baseline + MACD line > signal + RSI > 55 + MFI > 55 + volume impulse

Squeeze Release pathway (25 points): Requires BB inside KC (squeeze) then release + momentum bias + histogram confirmation

Micro Pullback pathway (15 points): Requires shallow retracement to fast EMA within established trend + histogram confirmation + volume impulse

Additional modifiers:

+5 points if volume impulse is present, -5 if absent

+5 points in velocity regime, -2 in compression regime

+5 points if cycle is aligned, -5 if counter-trend

A trade only executes when the composite score reaches the minimum threshold (default 55) AND all filters agree (session, cycle bias, BTC dominance if enabled).

This scoring system is the core innovation: instead of requiring ALL conditions to be true (which would generate very few signals) or ANY condition to be true (which would generate too many false signals), the strategy requires ENOUGH conditions to be true, with different conditions contributing different weights based on their reliability.

HOW THE STRATEGY CALCULATES ENTRIES AND EXITS

Entry Logic:

1. Calculate current volatility regime from ATR%

2. Calculate all indicator values (MACD, EMA, RSI, MFI, squeeze, volume)

3. Evaluate each signal pathway and sum points

4. Check all filters (session, cycle, dominance, kill switch)

5. If composite score >= 55 AND all filters pass, generate entry signal

6. Calculate position size based on risk per trade and regime-adjusted stop distance

7. Execute entry with regime name as comment

Position Sizing Formula:

RiskCapital = Equity * (0.65 / 100)

StopDistance = ATR * StopMultiplier(regime)

RawQuantity = RiskCapital / StopDistance

MaxQuantity = Equity * (12 / 100) / Price

Quantity = min(RawQuantity, MaxQuantity)

Quantity = round(Quantity / 0.001) * 0.001

This ensures each trade risks approximately 0.65% of equity regardless of volatility, while capping total exposure at 12% of equity.

Stop Loss Calculation:

Stop distance is ATR multiplied by a regime-specific multiplier:

Compression regime: 1.05x ATR (tighter stops because moves are smaller)

Expansion regime: 1.55x ATR (standard stops)

Velocity regime: 2.1x ATR (wider stops to avoid premature exits during volatility)

Take Profit Calculation:

Target distance is ATR multiplied by regime-specific multiplier and base risk/reward:

Compression regime: 1.6x ATR * 1.8 base R:R * 0.9 regime bonus = approximately 2.6x ATR

Expansion regime: 2.05x ATR * 1.8 base R:R * 1.0 regime bonus = approximately 3.7x ATR

Velocity regime: 2.8x ATR * 1.8 base R:R * 1.15 regime bonus = approximately 5.8x ATR

Trailing Stop Logic:

When adaptive trailing is enabled, the strategy calculates a trailing offset based on ATR and regime:

Compression regime: 1.1x base offset (looser trailing to avoid noise)

Expansion regime: 1.0x base offset (standard)

Velocity regime: 0.8x base offset (tighter trailing to lock in profits during fast moves)

The trailing stop only activates when it would be tighter than the initial stop.

Momentum Fail-Safe Exits:

The strategy closes positions early if momentum reverses:

Long positions close if MACD histogram turns negative OR EMA ribbon structure breaks (fast EMA crosses below mid EMA)

Short positions close if MACD histogram turns positive OR EMA ribbon structure breaks

This prevents holding through momentum reversals even if stop loss hasn't been hit.

Kill Switch:

If maximum drawdown exceeds 6.5%, the strategy disables new entries until manually reset. This prevents continued trading during adverse conditions.

HOW TO USE THIS STRATEGY

Step 1: Apply to Chart

Use a 5-minute chart of a high-liquidity cryptocurrency perpetual (BTC/USDT, ETH/USDT recommended)

Ensure at least 200 bars of history are loaded for indicator stabilization

Use standard candlestick charts only (not Heikin Ashi, Renko, or other non-standard types)

Step 2: Understand the Visual Elements

EMA Ribbon: Three lines (8/21/34 periods) showing trend structure. Bullish when stacked upward, bearish when stacked downward.

Background Color: Shows current volatility regime

- Indigo/dark blue = Compression (low volatility)

- Purple = Expansion (normal volatility)

- Magenta/pink = Velocity (high volatility)

Bar Colors: Reflect signal strength divergence. Brighter colors indicate stronger directional bias.

Triangle Markers: Entry signals. Up triangles below bars = long entry. Down triangles above bars = short entry.

Dashboard (top-right): Real-time display of regime, ATR%, signal strengths, position status, stops, targets, and risk metrics.

Step 3: Interpret the Dashboard

Regime: Current volatility classification (Compression/Expansion/Velocity)

ATR%: Normalized volatility as percentage of price

Long/Short Strength: Current composite signal scores (0-100)

Cycle Osc: Price deviation from 55-period EMA as percentage

Dominance: BTC.D slope and filter status

Position: Current position direction or "Flat"

Stop/Target: Current stop loss and take profit levels

Kill Switch: Status of drawdown protection

Volume Z: Current volume z-score

Impulse: Whether volume impulse condition is met

Step 4: Adjust Parameters for Your Needs

For more conservative trading: Increase "Minimum Composite Signal Strength" to 65 or higher

For more aggressive trading: Decrease to 50 (but expect more false signals)

For higher timeframes (15m+): Increase "Structure Break Window" to 12-15, increase "RSI Momentum Trigger" to 58

For lower liquidity pairs: Increase "Volume Impulse Multiplier" to 1.3, increase slippage in strategy properties

To disable short selling: Uncheck "Enable Short Structure"

To disable BTC dominance filter: Uncheck "BTC Dominance Confirmation"

STRATEGY PROPERTIES (BACKTEST SETTINGS)

These are the exact settings used in the strategy's Properties dialog box. You must use these same settings when evaluating the backtest results shown in the publication:

Initial Capital: $100,000

Justification: This amount is higher than typical retail accounts. I chose this value to demonstrate percentage-based returns that scale proportionally. The strategy uses percentage-based position sizing (0.65% risk per trade), so a $10,000 account would see the same percentage returns with 10x smaller position sizes. The absolute dollar amounts in the backtest should be interpreted as percentages of capital.

Commission: 0.04% (commission_value = 0.04)

Justification: This reflects typical perpetual futures exchange fees. Major exchanges charge between 0.02% (maker) and 0.075% (taker). The 0.04% value is a reasonable middle estimate. If your exchange charges different fees, adjust this value accordingly. Higher fees will reduce net profitability.

Slippage: 1 tick

Justification: This is conservative for liquid pairs like BTC/USDT on major exchanges during normal conditions. For less liquid altcoins or during high volatility, actual slippage may be higher. If you trade less liquid pairs, increase this value to 2-3 ticks for more realistic results.

Pyramiding: 1

Justification: No position stacking. The strategy holds only one position at a time. This simplifies risk management and prevents overexposure.

calc_on_every_tick: true

Justification: The strategy evaluates on every price update, not just bar close. This is necessary for scalping timeframes where waiting for bar close would miss opportunities. Note that this setting means backtest results may differ slightly from bar-close-only evaluation.

calc_on_order_fills: true

Justification: The strategy recalculates immediately after order fills for faster response to position changes.

RISK PER TRADE JUSTIFICATION

The default risk per trade is 0.65% of equity. This is well within the TradingView guideline that "risking more than 5-10% on a trade is not typically considered viable."

With the 12% maximum exposure cap, even if the strategy takes multiple consecutive losses, the total risk remains manageable. The kill switch at 6.5% drawdown provides additional protection by halting new entries during adverse conditions.

The position sizing formula ensures that stop distance (which varies by regime) is accounted for, so actual risk per trade remains approximately 0.65% regardless of volatility conditions.

SAMPLE SIZE CONSIDERATIONS

For statistically meaningful backtest results, you should select a dataset that generates at least 100 trades. On 5-minute BTC/USDT charts, this typically requires:

2-3 months of data during normal market conditions

1-2 months during high-volatility periods

3-4 months during low-volatility consolidation periods

The strategy's selectivity (requiring 55+ composite score plus all filters) means it generates fewer signals than less filtered approaches. If your backtest shows fewer than 100 trades, extend the date range or reduce the minimum signal strength threshold.

Fewer than 100 trades produces statistically unreliable results. Win rate, profit factor, and other metrics can vary significantly with small sample sizes.

STRATEGY DESIGN COMPROMISES AND LIMITATIONS

Every strategy involves trade-offs. Here are the compromises made in this design and the limitations you should understand:

Selectivity vs. Opportunity Trade-off

The 55-point minimum threshold filters many potential trades. This reduces false signals but also misses valid setups that don't meet all criteria. Lowering the threshold increases trade frequency but decreases win rate. There is no "correct" threshold; it depends on your preference for fewer higher-quality signals vs. more signals with lower individual quality.

Regime Classification Lag

The ATR-based regime detection uses historical data (21 periods + 13-period smoothing). It cannot predict sudden volatility spikes. During flash crashes or black swan events, the strategy may be classified in the wrong regime for several bars before the classification updates. This is an inherent limitation of any lagging indicator.

Indicator Parameter Sensitivity

The default parameters (MACD 8/21/5, EMA 8/21/34, RSI 21, etc.) are tuned for BTC/ETH perpetuals on 5-minute charts during 2024 market conditions. Different assets, timeframes, or market regimes may require different parameters. There is no guarantee that parameters optimized on historical data will perform similarly in the future.

BTC Dominance Filter Limitations

The CRYPTOCAP:BTC.D data feed may lag during low-liquidity periods or weekends. The dominance slope calculation uses a 5-bar SMA, adding additional delay. If you notice the filter behaving unexpectedly, consider disabling it.

Backtest vs. Live Execution Differences

TradingView backtesting does not replicate actual broker execution. Key differences:

Backtests assume perfect fills at calculated prices; real execution involves order book depth, latency, and partial fills

The calc_on_every_tick setting improves backtest realism but still cannot capture sub-bar price action or order book dynamics

Commission and slippage settings are estimates; actual costs vary by exchange, time of day, and market conditions

Funding rates on perpetual futures are not modeled in backtests and can significantly impact profitability over time

Exchange-specific limitations (position limits, liquidation mechanics, order types) are not modeled

Market Condition Dependencies

This strategy is designed for trending and breakout conditions. During extended sideways consolidation with no clear direction, the strategy may generate few signals or experience whipsaws. No strategy performs well in all market conditions.

Cryptocurrency-Specific Risks

Cryptocurrency markets operate 24/7 without session boundaries. This means:

No natural "overnight" risk reduction

Volatility can spike at any time

Liquidity varies significantly by time of day

Exchange outages or issues can occur at any time

WHAT THIS STRATEGY DOES NOT DO

To be straightforward about limitations:

This strategy does not guarantee profits. Past backtest performance does not indicate future results.

This strategy does not predict the future. It reacts to current conditions based on historical patterns.

This strategy does not account for funding rates, which can significantly impact perpetual futures profitability.

This strategy does not model exchange-specific execution issues (partial fills, requotes, outages).

This strategy does not adapt to fundamental news events or black swan scenarios.

This strategy is not optimized for all market conditions. It may underperform during extended consolidation.

IMPORTANT RISK WARNINGS

Past performance does not guarantee future results. The backtest results shown reflect specific historical market conditions and parameter settings. Markets change constantly, and strategies that performed well historically may underperform or lose money in the future. A single backtest run does not constitute proof of future profitability.

Trading involves substantial risk of loss. Cryptocurrency derivatives are highly volatile instruments. You can lose your entire investment. Only trade with capital you can afford to lose completely.

This is not financial advice. This strategy is provided for educational and informational purposes only. It does not constitute investment advice, trading recommendations, or any form of financial guidance. The author is not a licensed financial advisor.

You are responsible for your own decisions. Before using this strategy with real capital:

Thoroughly understand the code and logic by reading the open-source implementation

Forward test with paper trading or very small positions for an extended period

Verify that commission, slippage, and execution assumptions match your actual trading environment

Understand that live results will differ from backtest results

Consider consulting with a qualified financial advisor

No guarantees or warranties. This strategy is provided "as is" without any guarantees of profitability, accuracy, or suitability for any purpose. The author is not responsible for any losses incurred from using this strategy.

OPEN-SOURCE CODE STRUCTURE

The strategy code is organized into these sections for readability:

Configuration Architecture: Input parameters organized into logical groups (Core Controls, Optimization Constants, Regime Intelligence, Signal Pathways, Risk Architecture, Visualization)

Helper Functions: calcQty() for position sizing, clamp01() and normalize() for value normalization, calcMFI() for Money Flow Index calculation

Core Indicator Engine: EMA ribbon, ATR and regime classification, MACD with adaptive baseline, RSI, MFI, volume analytics, cycle oscillator, BTC dominance filter, squeeze detection

Signal Pathway Logic: Trend break, momentum surge, squeeze release, micro pullback pathways with composite scoring

Entry/Exit Orchestration: Signal filtering, position sizing, entry execution, stop/target calculation, trailing stop logic, momentum fail-safe exits

Visualization Layer: EMA plots, regime background, bar coloring, signal labels, dashboard table

You can read and modify any part of the code. Understanding the logic before deployment is strongly recommended.

- Made with passion by officialjackofalltrades

Elite MTF EMA Reclaim StrategyThis script is a 6-minute execution MTF EMA “retest → reclaim” strategy. It looks for trend-aligned pullbacks into fast EMAs, then enters when price reclaims and (optionally) retests the reclaim level—while filtering out chop (low trend strength/volatility or recent EMA20/50 crosses) and enforcing higher-timeframe alignment (Daily + 1H, or whichever you select).

How to use

Run it on a 6-minute chart (that’s what the presets are tuned for).

Pick your Market (Forex / XAUUSD / Crypto / Indices) and a Preset:

Elite = strictest, cleanest (fewer signals)

Balanced = middle ground

Aggressive = most signals, loosest filters

Set HTF Alignment Mode:

D + H1 (recommended) for highest quality

Off if you want more trades / LTF-only testing

Leave Kill Chop = ON (recommended). If you’re not getting trades, this is usually the blocker.

Choose entry behavior:

If Require Retest = true, entries happen on the retest after reclaim (cleaner, later).

If Require Retest = false, entries trigger on reclaim using Reclaim Timing Default:

“Preset” uses the strategy’s recommended default per market/preset

or force Reclaim close / Next bar confirmation

For backtesting, keep Mode = Strategy (Backtest). For alerts/visual-only, set Mode = Indicator (Signals Only).

Use Show Signals (All Modes) to toggle triangles on/off without affecting trades.

Tip: If TradingView says “not enough data,” switch symbol history to “All,” reduce HTF alignment (try H1 only), or backtest a more recent date range.

Liquidity Maxing [JOAT]Liquidity Maxing - Institutional Liquidity Matrix

Introduction

Liquidity Maxing is an open-source strategy for TradingView built around institutional market structure concepts. It identifies structural shifts, evaluates trades through multi-factor confluence, and implements layered risk controls.

The strategy is designed for swing trading on 4-hour timeframes, focusing on how institutional order flow manifests in price action through structure breaks, inducements, and liquidity sweeps.

Core Functionality

Liquidity Maxing performs three primary functions:

Tracks market structure to identify when control shifts between buyers and sellers

Scores potential trades using an eight-factor confluence system

Manages position sizing and risk exposure dynamically based on volatility and user-defined limits

The goal is selective trading when multiple conditions align, rather than frequent entries.

Market Structure Engine

The structure engine tracks three key events:

Break of Structure (BOS): Price pushes beyond a prior pivot in the direction of trend

Change of Character (CHoCH): Control flips from bullish to bearish or vice versa

Inducement Sweeps (IDM): Market briefly runs stops against trend before moving in the real direction

The structure module continuously updates strong highs and lows, labeling structural shifts visually. IDM markers are optional and disabled by default to maintain chart clarity.

The trade engine requires valid structure alignment before considering entries. No structure, no trade.

Eight-Factor Confluence System

Instead of relying on a single indicator, Liquidity Maxing uses an eight-factor scoring system:

Structure alignment with current trend

RSI within healthy bands (different ranges for up and down trends)

MACD momentum agreement with direction

Volume above adaptive baseline

Price relative to main trend EMA

Session and weekend filter (configurable)

Volatility expansion/contraction via ATR shifts

Higher-timeframe EMA confirmation

Each factor contributes one point to the confluence score. The default minimum confluence threshold is 6 out of 8, but you can adjust this from 1-8 based on your preference for trade frequency versus selectivity.

Only when structure and confluence agree does the strategy proceed to risk evaluation.

Dynamic Risk Management

Risk controls are implemented in multiple layers:

ATR-based stops and targets with configurable risk-to-reward ratio (default 2:1)

Volatility-adjusted position sizing to maintain consistent risk per trade as ranges expand or compress

Daily and weekly risk budgets that halt new entries once thresholds are reached

Correlation cooldown to prevent clustered trades in the same direction

Global circuit breaker with maximum drawdown limit and emergency kill switch

If any guardrail is breached, the strategy will not open new positions. The dashboard clearly displays risk state for transparency.

Market Presets

The strategy includes configuration presets optimized for different market types:

Crypto (BTC/ETH): RSI bands 70/30, volume multiplier 1.2, enhanced ATR scaling

Forex Majors: RSI bands 75/25, volume multiplier 1.5

Indices (SPY/QQQ): RSI bands 70/30, volume multiplier 1.3

Custom: Default values for user customization

For crypto assets, the strategy automatically applies ATR volatility scaling to account for higher volatility characteristics.

Monitoring and Dashboards

The strategy includes optional monitoring layers:

Risk Operations Dashboard (top-right):

Trend state

Confluence score

ATR value

Current position size percentage

Global drawdown

Daily and weekly risk consumption

Correlation guard state

Alert mode status

Performance Console (top-left):

Net profit

Current equity

Win rate percentage

Average trade value

Sharpe-style ratio (rolling 50-bar window)

Profit factor

Open trade count

Optional risk tint on chart background provides visual indication of "safe to trade" versus "halted" state.

All visualization elements can be toggled on/off from the inputs for clean chart viewing or full telemetry during parameter tuning.

Alerts and Automation

The strategy supports alert integration with two formats:

Standard alerts: Human-readable messages for long, short, and risk-halt conditions

Webhook format: JSON-formatted payloads ready for external execution systems (optional)

Alert messages are predictable and unambiguous, suitable for manual review or automated forwarding to execution engines.

Built-in Validation Suite

The strategy includes an optional validation layer that can be enabled from inputs. It checks:

Internal consistency of structure and confluence metrics

Sanity and ordering of risk parameters

Position sizing compliance with user-defined floors and caps

This validation is optional and not required for trading, but provides transparency into system operation during development or troubleshooting.

Strategy Parameters

Market Presets:

Configuration Preset: Choose between Crypto (BTC/ETH), Forex Majors, Indices (SPY/QQQ), or Custom

Market Structure Architecture:

Pivot Length: Default 5 bars

Filter by Inducement (IDM): Default enabled

Visualize Structure: Default enabled

Structure Lookback: Default 50 bars

Risk & Capital Preservation:

Risk:Reward Ratio: Default 2.0

ATR Period: Default 14

ATR Multiplier (Stop): Default 2.0

Max Drawdown Circuit Breaker: Default 10%

Risk per Trade (% Equity): Default 1.5%

Daily Risk Limit: Default 6%

Weekly Risk Limit: Default 12%

Min Position Size (% Equity): Default 0.25%

Max Position Size (% Equity): Default 5%

Correlation Cooldown (bars): Default 3

Emergency Kill Switch: Default disabled

Signal Confluence:

RSI Length: Default 14

Trend EMA: Default 200

HTF Confirmation TF: Default Daily

Allow Weekend Trading: Default enabled

Minimum Confluence Score (0-8): Default 6

Backtesting Considerations

When backtesting this strategy, consider the following:

Commission: Default 0.05% (adjustable in strategy settings)

Initial Capital: Default $100,000 (adjustable)

Position Sizing: Uses percentage of equity (default 2% per trade)

Timeframe: Optimized for 4-hour charts, though can be tested on other timeframes

Results will vary significantly based on:

Market conditions and volatility regimes

Parameter settings, especially confluence threshold

Risk limit configuration

Symbol characteristics (crypto vs forex vs equities)

Past performance does not guarantee future results. Win rate, profit factor, and other metrics should be evaluated in context of drawdown periods, trade frequency, and market conditions.

How to Use This Strategy

This is a framework that requires understanding and parameter tuning, not a one-size-fits-all solution.

Recommended workflow:

Start on 4-hour timeframe with default parameters and appropriate market preset

Run backtests and study performance console metrics: focus on drawdown behavior, win rate, profit factor, and trade frequency

Adjust confluence threshold to match your risk appetite—higher thresholds mean fewer but more selective trades

Set realistic daily and weekly risk budgets appropriate for your account size and risk tolerance

Consider ATR multiplier adjustments based on market volatility characteristics

Only connect alerts or automation after thorough testing and parameter validation

Treat this as a risk framework with an integrated entry engine, not merely an entry signal generator. The risk controls are as important as the trade signals.

Strategy Limitations

Designed for swing trading timeframes; may not perform optimally on very short timeframes

Requires sufficient market structure to identify pivots; may struggle in choppy or low-volatility environments

Crypto markets require different parameter tuning than traditional markets

Risk limits may prevent entries during favorable setups if daily/weekly budgets are exhausted

Correlation cooldown may delay entries that would otherwise be valid

Backtesting results depend on data quality and may not reflect live trading with slippage

Design Philosophy

Many indicators tell you when price crossed a moving average or RSI left oversold. This strategy addresses questions institutional traders ask:

Who is in control of the market right now?

Is this move structurally significant or just noise?

Do I want to add more risk given what I've already done today/week?

If I'm wrong, exactly how painful can this be?

The strategy provides disciplined, repeatable answers to these questions through systematic structure analysis, confluence filtering, and multi-layer risk management.

Technical Implementation

The strategy uses Pine Script v6 with:

Custom types for structure, confluence, and risk state management

Functional programming approach for reusable calculations

State management through persistent variables

Optional visual elements that can be toggled independently

The code is open-source and can be modified to suit individual needs. All important logic is visible in the source code.

Disclaimer

This script is provided for educational and informational purposes only. It is not intended as financial, investment, trading, or any other type of advice or recommendation. Trading involves substantial risk of loss and is not suitable for all investors. Past performance, whether real or indicated by historical tests of strategies, is not indicative of future results.

No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between backtested results and actual results subsequently achieved by any particular trading strategy.

The user should be aware of the risks involved in trading and should trade only with risk capital. The authors and publishers of this script are not responsible for any losses or damages, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on this script.

This strategy uses technical analysis methods and indicators that are not guaranteed to be accurate or profitable. Market conditions change, and strategies that worked in the past may not work in the future. Users should thoroughly test any strategy in a paper trading environment before risking real capital.

Commission and slippage settings in backtests may not accurately reflect live trading conditions. Real trading results will vary based on execution quality, market liquidity, and other factors not captured in backtesting.

The user assumes full responsibility for all trading decisions made using this script. Always consult with a qualified financial advisor before making investment decisions.

Enjoy - officialjackofalltrades

10>20,p>50 DEMARenders daily EMA, 10, 20 and 50 on any timeframe below 1D

30m timeframe works well.

Use trend of 10 > 20 + price > 50 for long and 10 < 20 + price < 50 for shorts or exits.

Trend Following $BTC - Multi-Timeframe Structure + ReversTREND FOLLOWING STRATEGY - MULTI-TIMEFRAME STRUCTURE BREAKOUT SYSTEM

Strategy Overview

This is an enhanced Turtle Trading system designed for cryptocurrency spot trading. It combines Donchian Channel breakouts with multi-timeframe structure filtering and ATR-based dynamic risk management. The strategy trades both long and short positions using reverse signal exits to maximize trend capture.

Core Features

Multi-Timeframe Structure Filtering

The strategy uses Swing High/Low analysis to identify market structure trends. You can customize the structure timeframe (default: 3 minutes) to match your trading style. Only enters trades aligned with the identified trend direction, avoiding counter-trend positions that often lead to losses.

Reverse Signal Exit System

Instead of using fixed stop-losses or time-based exits, this strategy exits positions only when a reverse entry signal triggers. This approach maximizes trend profits and reduces premature exits during normal market retracements.

ATR Dynamic Pyramiding

Automatically adds positions when price moves 0.5 ATR in your favor. Supports up to 2 units maximum (adjustable). This pyramid scaling enhances profitability during strong trends while maintaining disciplined risk management.

Complete Risk Management

Fixed position sizing at 5000 USD per unit. Includes realistic commission fees of 0.06% (Binance spot rate). Initial capital set at 10,000 USD. All backtest parameters reflect real-world trading conditions.

Trading Logic

Entry Conditions

Long Entry: Close price breaks above the 20-period high AND structure trend is bullish (price breaks above Swing High)

Short Entry: Close price breaks below the 20-period low AND structure trend is bearish (price breaks below Swing Low)

Position Scaling

Long positions: Add when price rises 0.5 ATR or more

Short positions: Add when price falls 0.5 ATR or more

Maximum 2 units including initial entry

Exit Conditions

Long Exit: Triggers when short entry signal appears (price breaks 20-period low + structure turns bearish)

Short Exit: Triggers when long entry signal appears (price breaks 20-period high + structure turns bullish)

Default Parameters

Channel Settings

Entry Channel Period: 20 (Donchian Channel breakout period)

Exit Channel Period: 10 (reserved parameter)

ATR Settings

ATR Period: 20

Stop Loss ATR Multiplier: 2.0

Add Position ATR Multiplier: 0.5

Structure Filter

Swing Length: 300 (Swing High/Low calculation period)

Structure Timeframe: 3 minutes

Adjust these based on your trading timeframe and asset volatility

Position Management

Maximum Units: 2 (including initial entry)

Capital Per Unit: 5000 USD

Visualization Features

Background Colors

Light Green: Bullish market structure

Light Red: Bearish market structure

Dark Green: Long position entry

Dark Red: Short position entry

Optional Display Elements (Default: OFF)

Entry and exit channel lines

Structure high/low reference lines

ATR stop-loss indicator

Next position add level

Entry/exit labels

Alert Message Format

The strategy sends notifications with the following format:

Entry: "5m Long EP:90450.50"

Add Position: "15m Add Long 2/2 EP:91000.25"

Exit: "5m Close Long Reverse Signal"

Where the first part shows your current chart timeframe and EP indicates Entry Price

Backtest Settings

Capital Allocation

Initial Capital: 10,000 USD

Per Entry: 5,000 USD (split into 2 potential entries)

Leverage: 0x (spot trading only)

Trading Costs

Commission: 0.06% (Binance spot VIP0 rate)

Slippage: 0 (adjust based on your experience)

Best Use Cases

Ideal Scenarios

Trending markets with clear directional movement

Moderate to high volatility assets

Timeframes from 1-minute to 4-hour charts

Best suited for major cryptocurrencies with good liquidity

Not Recommended For

Highly volatile choppy/ranging markets

Low liquidity small-cap coins

Extreme market conditions or black swan events

Usage Recommendations

Timeframe Guidelines

1-5 minute charts: Use for scalping, consider Swing Length 100-160

15-30 minute charts: Good for short-term trading, Swing Length 50-100

1-4 hour charts: Suitable for swing trading, Swing Length 20-50

Optimization Tips

Always backtest on historical data before live trading

Adjust swing length based on asset volatility and your timeframe

Different cryptocurrencies may require different parameter settings

Enable visualization options initially to understand entry/exit points

Monitor win rate and drawdown during backtesting

Technical Details

Built on Pine Script v6

No repainting - uses proper bar referencing with offset

Prevents lookahead bias with lookahead=off parameter

Strategy mode with accurate commission and slippage modeling

Multi-timeframe security function for structure analysis

Proper position state tracking to avoid duplicate signals

Risk Disclaimer

This strategy is provided for educational and research purposes only. Past performance does not guarantee future results. Backtesting results may differ from live trading due to slippage, execution delays, and changing market conditions. The strategy performs best in trending markets and may experience drawdowns during ranging conditions. Always practice proper risk management and never risk more than you can afford to lose. It is recommended to paper trade first and start with small position sizes when going live.

How to Use

Add the strategy to your TradingView chart

Select your desired timeframe (1m to 4h recommended)

Adjust parameters based on your risk tolerance and trading style

Review backtest results in the Strategy Tester tab

Set up alerts for automated notifications

Consider paper trading before risking real capital

Tags

Trend Following, Turtle Trading, Donchian Channel, Structure Breakout, ATR, Cryptocurrency, Spot Trading, Risk Management, Pyramiding, Multi-Timeframe Analysis

---

Strategy Name: Trend Following BTC

Version: v1.0

Pine Script Version: v6

Last Updated: December 2025

BTC Mon 8am Buy / Wed 2pm Sell (NY Time, Daily + Intraday)This strategy implements a fixed weekly time-based trading schedule for Bitcoin, using New York market hours as the reference clock. It is designed to test whether a consistent pattern exists between early-week accumulation and mid-week distribution in BTC price behavior.

Entry Rule — Monday 8:00 AM (NY Time)

The strategy enters a long position every Monday at exactly 08:00 AM Eastern Time, one hour after the U.S. equities market pre-open activity begins influencing global liquidity.

This timing attempts to capture early-week directional moves in Bitcoin, which sometimes occur as traditional markets come online.

Exit Rule — Wednesday 2:00 PM (NY Time)

The strategy closes the position every Wednesday at 2:00 PM Eastern Time, a point in the week where:

U.S. equity markets are still open

BTC often experiences mid-week volatility rotations

Liquidity is generally high

This exit removes exposure before later-week uncertainty and gives a consistent, measurable time window for each trade.

Timeframe Compatibility

Works on intraday charts (recommended 1h or lower) using precise time-based triggers.

Also runs on daily charts, where entries and exits occur on the Monday and Wednesday bars respectively (daily charts cannot show intraday timestamps).

All timestamps are synced to America/New_York regardless of the exchange’s native timezone.

Trading Frequency

Exactly one trade per week, preventing overtrading and allowing comparison of weekly performance across years of historical BTC price data.

Purpose of the Strategy

This is not a value-based or trend-following system, but a behavioral/time-cycle analysis tool.

It helps evaluate whether a repeating short-term edge exists based solely on:

Weekday timing

Liquidity cycles

Institutional market influence

BTC’s habitual early-week momentum patterns

It is ideal for:

Backtesting weekly BTC behavior

Studying time-based edges

Comparing alternative weekday/time combinations

Visualizing weekly P&L structure

Risk Notes

This strategy does not attempt to predict price direction and should not be assumed profitable without robust backtesting.

Time-based edges can appear, disappear, or invert depending on macro conditions.

There is no stop loss or risk management included by default, so the strategy reflects raw timing-based performance.

Estrategia TEMA Pro [Límite Ops por Ventana]good money

jucale

keep faith

dont stop working

eat vegatables

Dual MTF Confirmed Trend Strategy (5m Entry / 15m MACD & RSI) v1That is a detailed Dual Multi-Timeframe (MTF) Confirmed Trend Strategy written in Pine Script for TradingView. The core idea of this strategy is to only take entry signals on a faster timeframe (5-minute) when the trend is strongly confirmed on a slower, higher timeframe (15-minute). This aims to reduce false signals and trade in the direction of the dominant trend. Here is an explanation of how the strategy works, broken down by section:

1. 5-Minute Entry Filters 🚀This section calculates several indicators on the current 5-minute chart to identify potential trade setups. A position is only considered if all 5-minute conditions align.

Supertrend: A trend-following indicator based on Average True Range (ATR).

Long Condition: The closing price must be above the Supertrend line.

Short Condition: The closing price must be below the Supertrend line.

Gann Hi-Lo (GHL): A trend indicator using Simple Moving Averages (SMA) of the high and low prices. GHL Line: Switches between the SMA of the Highs and the SMA of the Lows based on price action.

Long Condition: The closing price must be above the GHL line.

Short Condition: The closing price must be below the GHL line.

Exponential Moving Averages (EMAs): It uses a 50-period EMA and a 100-period EMA to confirm the short-term trend direction.

Long Condition: The closing price must be above both the 50 EMA and the 100 EMA.

Short Condition: The closing price must be below both the 50 EMA and the 100 EMA.

2. 15-Minute MTF Confirmation Filters ⏳This is the crucial step where the strategy verifies the trend on the slower, 15-minute timeframe using the request security function. This step acts as a gatekeeper to ensure the 5-minute trade aligns with the larger trend.

MACD Histogram (12, 26, 9): The difference between the MACD Line and the Signal Line.

Long Confirmation: The 15m MACD Histogram must be greater than 0 (MACD line is above the Signal line, indicating bullish momentum).

Short Confirmation: The 15m MACD Histogram must be less than 0 (MACD line is below the Signal line, indicating bearish momentum).

RSI (Relative Strength Index) (14): A momentum oscillator. The 50 level is often used to determine the general market trend.

Long Confirmation: The 15m RSI must be greater than 50 (indicating stronger bullish momentum).

Short Confirmation: The 15m RSI must be less than 50 (indicating stronger bearish momentum).

The Total 15m Confirmation is only true if both the MACD and the RSI confirmation signals align.

3. Trade Orders (Entry Logic) ⚖️

The strategy only executes a trade when the 5-minute entry conditions are met AND the 15-minute confirmation conditions are met.

Final Long Condition:

5m Conditions (Supertrend, GHL, EMA alignment) AND

15m Confirmation (MACD Hist > 0 AND RSI > 50)

Final Short Condition:

5m Conditions (Supertrend, GHL, EMA alignment) AND

15m Confirmation (MACD Hist < 0 AND RSI < 50)

When a trade signal is generated, the strategy:

Closes any opposite position (e.g., closes a "Short" trade if a "Long" signal appears).

Enters the new position (e.g., enters a "Long" trade).

This is designed as a reversal strategy where a new entry automatically closes the previous opposing trade.

In Summary

The strategy operates on a principle of Trend Alignment:

5-Minute Chart: Is used for Signal Timing (when exactly to enter the market).

15-Minute Chart: Is used for Trend Validation (is the overall market momentum supporting the signal?).

It's an attempt to capture short-term moves (5m signals) that are backed by strong medium-term momentum (15m confirmation), thereby aiming for higher probability trades.

This is not investment advice; it is recommended to perform optimization and backtesting for the assets intended for implementation.

Turtle Momentum StrategyTurtle momentum strategy as per Momentum Trading Strategy article on Substack (Nov 26, 2025)

MTF Scalper - alemicihanMulti-Timeframe Scalper Strategy: Aligning the Big Picture for Quick Gains

This article presents a robust futures trading strategy designed for high-frequency scalping in the crypto market. It’s built on the principle of minimizing risk by ensuring that short-term entries are always aligned with the dominant, higher-timeframe trend.

The Core Concept: Alignment is Key

A Balanced Trend Follower approach, now refined for rapid scalping, uses a Multi-Timeframe (MTF) confirmation system to filter out market noise and increase the probability of a successful trade.

The strategy operates on a Low Timeframe (LTF) chart (e.g., 3m, 5m, or 15m) but only executes trades if the direction is validated by three Higher Timeframes (HTF).

ComponentPurposeFunctionHTF (D, 4h, 1h) EMA => Trend Confirmation =>Checks if the current price is above/below all three Exponential Moving Averages (EMA 20). This provides a strong directional bias.

LTF (5m) Stochastic RSI => Momentum Entry => Generates the actual buy/sell signal by spotting a swift crossover, indicating fresh momentum in the direction of the confirmed HTF trend.

How The Signal Is Generated

Trend Alignment: The system first confirms the trend. If the price is trading above the Daily, 4-Hour, and 1-Hour EMAs, the market is deemed to be in a Strong LONG Trend. Only LONG signals are permitted.

Momentum Trigger: Once the trend is confirmed, a Long Signal is generated only when the Stochastic K-Line crosses above the D-Line, indicating a momentum shift (a pullback ending) towards the main trend direction.

Short Signal: The inverse logic applies to the Short Trend confirmation and entry signal.

Mandatory Risk Management: ATR-Based Exit

Given the high leverage nature of futures and scalping, static Stop-Loss (SL) and Take-Profit (TP) levels are inefficient. This strategy uses the Average True Range (ATR) indicator to dynamically set profit and loss targets based on current market volatility.

Stop Loss (SL): Set dynamically at 1.5 x ATR below (for long) or above (for short) the entry price. This gives the trade enough room to breathe without risking excessive capital.

Take Profit (TP): Set dynamically at 3.0 x ATR, establishing a robust Risk-to-Reward Ratio of 1:2.

Final Thoughts on Testing

This sophisticated approach combines the reliability of MTF analysis with the speed of momentum indicators. However, data analysis is key. Backtesting these parameters (EMA, ATR Multipliers, RSI/Stochastic lengths) on your chosen asset (like BTC/USDT or ETH/USDT) and timeframe is crucial to achieving optimal performance.

ILM & IFVG StrategyPlease feel free to adjust in any way possible. Let me know if you can create something better from this initial coding.

//═══════════════════════════════════════════════════════════════════════

// Inverted Liquidity Model (ILM) – Strategy

//═══════════════════════════════════════════════════════════════════════

//

// The **Inverted Liquidity Model (ILM)** is a liquidity-based algorithm

// built to capture high-probability reversals after:

//

// • A liquidity sweep (SSL/BSL taken)

// • Rejection back inside the range

// • A Fair Value Gap (FVG) forms

// • That FVG becomes invalidated → becomes an IFVG entry zone

//

// ILM combines:

// • LTF BOS / CHOCH structure confirmation

// • HTF structure (expansion) filtering

// • Premium / Discount filter (17:00 CST session midline)

// • Optional ATR volatility filter

// • Optional trading session restrictions

// • Optional partial profit-taking + runners

//

// When all conditions align, the strategy enters:

// ✔ Long after sweep of SSL + valid long IFVG + trend confirmation

// ✔ Short after sweep of BSL + valid short IFVG + trend confirmation

//

// Stops are placed at the sweep wick.

// Full target is set at the next structural high/low.

// Optional partial TP sends a runner to full target.

//

// Visual tools (labels, sweep lines, IFVG boxes, midline) assist

// with review and forward testing.

//

//───────────────────────────────────────────────────────────────────────

// USER CONFIGURABLE FEATURES

//───────────────────────────────────────────────────────────────────────

//

// • **Liquidity & Structure**

// - pivotLen → swing length for pivots / liquidity

// - htfOn → toggle higher-timeframe pivots

// - htfTF → timeframe for HTF structure/liquidity

// - useStructureFilter → enforce LTF BOS/CHOCH trend

// - useHtfExpansionFilter → enforce HTF trend

// - showStructureLabels → show BOS/CHOCH labels

// - showHtfStructureLabels → show HTF BOS/CHOCH labels

//

// • **Premium / Discount Midline**

// - usePremiumDiscountFilter → only long in discount / short in premium

// - pdSession → session used for midline (default 17:00 CST)

// - showPdMidLine → show 50% midline

//

// • **FVG / IFVG Detection**

// - useBodyGapFVG → FVG uses candle bodies instead of wicks

// - useDisplacementFVG → require displacement bar

// - dispAtrMult → minimum ATR threshold for displacement

// - showIFVG → draw IFVG boxes

//

// • **ATR / Volatility / Sessions**

// - useRangeFilter → require minimum ATR%

// - atrLen → ATR period

// - minAtrPerc → minimum ATR% of price

// - useSessionFilter → restrict trading hours

// - sessionTimes → allowed trading session

//

// • **Sweep Visualization**

// - showSweepLines → draw sweep lines at SSL/BSL sweeps

// - sweepLineWidth → thickness of sweep lines

//

// • **Exits: Partial Targets & Runners**

// - usePartialTargets → enable partial TP logic

// - tp1QtyPercent → percent closed at TP1

// - tp1FractionOfPath → TP1 relative to path to full target

//

// • **Formatting / Visibility**

// - labelFontSizeInput → tiny / small / normal / large / huge

// - showEntries → entry markers

// - showTargets → target lines

//

//═══════════════════════════════════════════════════════════════════════

// END OF STRATEGY DESCRIPTION

//═══════════════════════════════════════════════════════════════════════

EMA 50/200 Pullback + RSI (BTC/USDT 15m - 2 Bar Logic)I recognize that combining indicators requires clear justification on how the components interact Therefore the new scripts description will explicitly detail the strategys operational logic

Objective The strategy is a Trend Following Pullback System designed for high frequency time frames 15m

Synergy The EMA50 EMA200 defines the primary Trend Direction Trend Filter It then utilizes a 2 Bar Pullback Logic to find an entry point where the price has momentarily reversed against the trendline and the RSI 14 serves as a Momentum Filter RSI greater than 50 for Long RSI less than 50 for Short to minimize false signals

Qullamagi EMA Breakout Autotrade (Crypto Futures L+S)Title: Qullamagi EMA Breakout – Crypto Autotrade

Overview

A crypto-focused, Qullamagi-style EMA breakout strategy built for autotrading on futures and perpetual swaps.

It combines a 5-MA trend stack (EMA 10/20, SMA 50/100/200), volatility contraction boxes, volume spikes and an optional higher-timeframe 200-MA filter. The script supports both long and short trades, partial take profit, trailing MA exits and percent-of-equity position sizing for automated crypto futures trading.

Key Features (Crypto)

Qullamagi MA Breakout Engine – trades only when price is aligned with a strong EMA/SMA trend and breaks out of a tight consolidation range. Longs use: Close > EMA10 > EMA20 > SMA50 > SMA100 > SMA200. Shorts are the mirror condition with all MAs sloping in the trend direction.

Strict vs Loose Modes – Strict (Daily) is designed for cleaner swing trades on 1H–4H (full MA stack, box+ATR and volume filters, optional HTF filter). Loose (Intraday) focuses on 10/20/50 alignment with relaxed filters for more frequent 15m–30m signals.

Volatility & Volume Filters for Crypto – ATR-based box height limit to detect volatility contraction, wide-candle filter to avoid chasing exhausted breakouts, and a volume spike condition requiring current volume to exceed an SMA of volume.

Higher-Timeframe Trend Filter (Optional) – uses a 200-period SMA on a higher timeframe (default: 1D). Longs only when HTF close is above the HTF 200-SMA, shorts only when it is below, helping avoid trading against dominant crypto trends.

Autotrade-Oriented Trade Management – position size as % of equity, initial stop anchored to a chosen MA (EMA10 / EMA20 / SMA50) with optional buffer, partial take profit at a configurable R-multiple, trailing MA exit for the remainder, and an optional cooldown after a full exit.

Markets & Timeframes

Best suited for BTC, ETH and major altcoin futures/perpetuals (Binance, Bybit, OKX, etc.).

Strict preset: 1H–4H charts for classic Qullamagi-style trend structure and fewer fake breakouts.

Loose preset: 15m–30m charts for higher trade frequency and more active intraday trading.

Always retune ATR length, box length, volume multiplier and position size for each symbol and exchange.

Strategy Logic (Quick Summary)

Long (Strict): MA stack in bullish alignment with all MAs sloping up → tight volatility box (ATR-based) → volume spike above SMA(volume) × multiplier → breakout above box high (close or intrabar) → optional HTF close above 200-SMA.

Short: Mirror logic: bearish MA stack, tight box, volume spike and breakdown below box low with optional HTF downtrend.

Best Practices for Crypto

Backtest on each symbol and timeframe you plan to autotrade, including commissions and slippage.

Start on higher timeframes (1H/4H) to learn the behavior, then move to 15m–30m if you want more signals.

Use the higher-timeframe filter when markets are strongly trending to reduce counter-trend trades.

Keep position-size percentage conservative until you fully understand the drawdowns.

Forward-test / paper trade before connecting to live futures accounts.

Webhook / Autotrade Integration

Designed to work with TradingView webhooks and external crypto trading bots.

Alert messages include structured fields such as: EVENT=ENTRY / SCALE_OUT / EXIT, SIDE=LONG / SHORT, STRATEGY=Qullamagi_MA.

Map each EVENT + SIDE combination to your bot logic (open long/short, partial close, full close, etc.) on your preferred exchange.

Important Notes & Disclaimer

Crypto markets are highly volatile and can change regime quickly. Backtest and forward-test thoroughly before using real capital. Higher timeframes generally produce cleaner MA structures and fewer fake breakouts.

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading leveraged crypto products involves substantial risk of loss. Always do your own research, manage risk carefully, and never trade with money you cannot afford to lose.

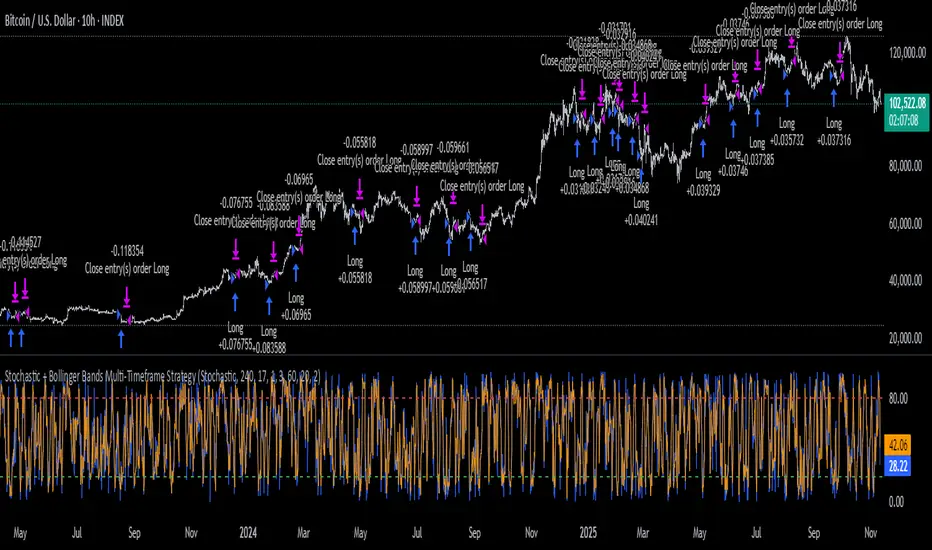

Stochastic + Bollinger Bands Multi-Timeframe StrategyThis strategy fuses the Stochastic Oscillator from the 4-hour timeframe with Bollinger Bands from the 1-hour timeframe, operating on a 10-hour chart to capture a unique volatility rhythm and temporal alignment discovered through observational alpha.

By blending momentum confirmation from the higher timeframe with short-term volatility extremes, the strategy leverages what some traders refer to as “rotating volatility” — a phenomenon where multi-timeframe oscillations sync to reveal hidden trade opportunities.

🧠 Strategy Logic

✅ Long Entry Condition:

Stochastic on the 4H timeframe:

%K crosses above %D

Both %K and %D are below 20 (oversold zone)

Bollinger Bands on the 1H timeframe:

Price crosses above the lower Bollinger Band, indicating a potential reversal

→ A long trade is opened when both momentum recovery and volatility reversion align.

✅ Long Exit Condition:

Stochastic on the 4H:

%K crosses below %D

Both %K and %D are above 80 (overbought zone)

Bollinger Bands on the 1H:

Price reaches or exceeds the upper Bollinger Band, suggesting exhaustion

→ The long trade is closed when either signal suggests a potential reversal or overextension.

🧬 Temporal Structure & Alpha

This strategy is deployed on a 10-hour chart — a non-standard timeframe that may align more effectively with multi-timeframe mean reversion dynamics.

This subtle adjustment exploits what some traders identify as “temporal drift” — the desynchronization of volatility across timeframes that creates hidden rhythm in price action.

→ For example, Stochastic on 4H (lookback 17) and Bollinger Bands on 1H (lookback 20) may periodically sync around 10H intervals, offering unique alpha windows.

📊 Indicator Components

🔹 Stochastic Oscillator (4H, Length 17)

Detects momentum reversals using %K and %D crossovers

Helps define overbought/oversold zones from a mid-term view

🔹 Bollinger Bands (1H, Length 20, ±2 StdDev)

Measures price volatility using standard deviation around a moving average

Entry occurs near lower band (support), exits near upper band (resistance)

🔹 Multi-Timeframe Logic

Uses request.security() to safely reference 4H and 1H indicators from a 10H chart

Avoids repainting by using closed higher-timeframe candles only

📈 Visualization

A plot selector input allows toggling between:

Stochastic Plot (%K & %D, with overbought/oversold levels)

Bollinger Bands Plot (Upper, Basis, Lower from 1H data)

This helps users visually confirm entry/exit triggers in real time.

🛠 Customization

Fully configurable Stochastic and BB settings

Timeframes are independently adjustable

Strategy settings like position sizing, slippage, and commission are editable

⚠️ Disclaimer

This strategy is intended for educational and informational purposes only.

It does not constitute financial advice or a recommendation to buy or sell any asset.

Market conditions vary, and past performance does not guarantee future results.

Always test any trading strategy in a simulated environment and consult a licensed financial advisor before making real-world investment decisions.

Kronos Scalper (RAVINDRA KHADSE) 11.11.2025Nice — below is a ready-to-copy TradingView Pine Script (v5) strategy named “Kronos Scalper”.

It’s a self-contained scalping strategy (non-repainting) with configurable EMAs trend filter, RSI entry filter, ATR-based stop loss / take profit, optional trailing stop, plots and entry/exit labels. Drop it into TradingView’s Pine editor and Add to Chart → Strategy Tester.

Final Scalping Strategy - RELAXED ENTRY, jangan gopoh braderEMA Scalping System (MTF) Guide (1HR direction, 15 min entry)

Objective

To capture small, consistent profits by entering trades when 15-minute momentum aligns with the 1-hour trend.

Trades are executed only during high-liquidity London and New York sessions to increase the probability of execution and success.

Strategy Setup

Chart Timeframe (Execution): 15-Minute (M15).

Trend Filter (HTF): 1-Hour (H1) chart data is used for the long-term EMA.

Long-Term Trend Filter: 50-Period EMA (based on H1 data).

Short-Term Momentum Signal: 20-Period EMA (based on M15 data).

Risk

Metric: 14-period ATR for dynamic Stop Loss calculation.

✅ Trading Rules🟢

Long (Buy) Entry Conditions

Session: Must be within the London (0800-1700 GMT) or New York (1300-2200 GMT) sessions.

HTF Trend: Current price must be above the 1-Hour EMA 50.

Momentum Signal: Price crosses above the 15-Minute EMA 20.

Confirmation: The bar immediately following the crossover must close above the 15-Minute EMA 20.

Ent

ry: A market order is executed on the close of the confirmation candle.

🔴 Short (Sell) Entry Conditions

Session: Must be within the London (0800-1700 GMT) or New York (1300-2200 GMT) sessions.

HTF Trend: Current price must be below the 1-Hour EMA 50.

Momentum Signal: Price crosses below the 15-Minute EMA 20.

Confirmation: The bar immediately following the crossover must close below the 15-Minute EMA 20.

Entry: A market order is executed on the close of the confirmation candle.

🛑 Trade Management & Exits

Stop Loss (SL): Placed dynamically at 2.0 times the 14-period ATR distance from the entry candle's low (for Buys) or high (for Sells).

Take Profit (TP): Placed dynamically to achieve a 1.5 Risk-Reward Ratio (RR) (TP distance = 1.5 x SL d

istance).

📊 On-Chart Visuals

Detailed Labels: A box appears on the entry bar showing the action, SL/TP prices, Risk/Reward in Pips, and the exact R:R ratio.

Horizontal Lines: Dashed lines display the calculated SL (Red) and TP (Green) levels while the trade is active.

Background: The chart background is shaded to highlight the active London and New York tradi

ng sessions.

RSI + MACD Multi-Timeframe StrategyThis strategy combines the Relative Strength Index (RSI) from the daily timeframe with the Moving Average Convergence Divergence (MACD) from the 4-hour timeframe to generate precise long entry and exit signals.

The system uses a multi-timeframe approach to align longer-term trend conditions with shorter-term momentum shifts — allowing traders to catch dips with confirmation and exit before reversals.

🧠 Strategy Logic

✅ Long Entry Condition:

- RSI on the daily (1D) timeframe is oversold (below your defined threshold)

- MACD on the 4H timeframe crosses above the signal line

→ A long trade is opened when these two align

✅ Long Exit Condition:

- RSI on the daily timeframe is overbought

- MACD on the 4H timeframe crosses below the signal line

→ The long trade is closed when these two conditions are met

💡 This strategy currently supports long entries only. Short logic can be added if needed.

📊 Indicator Components

🔹 RSI (Relative Strength Index):

- A momentum oscillator that measures the speed and magnitude of price changes.

- Helps identify overbought (potential sell) and oversold (potential buy) conditions.

- Applied on the 1D timeframe (by default) to reflect broader market trend or exhaustion levels.

🔹 MACD (Moving Average Convergence Divergence):

- A trend-following momentum indicator based on moving averages.

- The MACD Line (fast EMA - slow EMA) crossing above the Signal Line indicates bullish momentum.

- Used here on the 4-hour timeframe (by default) for shorter-term momentum confirmation.

🔹 Multi-Timeframe (MTF) Logic:

- Uses request.security() to pull higher timeframe data (1D for RSI, 4H for MACD).

- Ensures no repainting, as it only uses closed candles from the higher timeframe.

- Aligns longer-term signals with shorter-term entries, reducing false signals.

📈 Plotting Options

The script includes a plot selector input allowing you to toggle between:

- RSI Plot (with overbought/oversold lines)

- MACD Plot (MACD line and signal line)

- This helps visualize signal conditions clearly on your chart.

🛠 Customization

- RSI & MACD settings are fully configurable

- RSI and MACD timeframes can be adjusted independently

⚠️ Disclaimer

This strategy is provided for educational and informational purposes only.

It is not financial advice or a recommendation to buy or sell any asset.

Past performance does not guarantee future results. Always test strategies in a simulated environment before live use, and consult with a licensed financial advisor for investment decisions.

Tristan's Multi-Indicator Reversal StrategyMulti-Indicator Reversal Strategy - Buy Low, Sell High

A comprehensive reversal detection system that combines multiple proven technical indicators to identify high-probability entry points for catching reversals at market extremes.

📊 Strategy Overview

This strategy is designed for traders who want to buy at lows and sell at highs by detecting when stocks are overextended and ready to reverse. It works by requiring multiple technical indicators to align before generating a signal, significantly reducing false entries.

Best Used On:

Timeframe: 1-hour charts (also works on 15min, 30min, 4hour)

Session: NY Trading Session (9:30 AM - 4:00 PM ET)

Assets: Stocks, ETFs, Crypto (particularly volatile tech stocks like ZM, TSLA, AAPL)

Trading Style: Swing trading, Intraday reversals

🔧 Technical Components

The strategy combines FIVE powerful technical indicators:

1. RSI (Relative Strength Index)

2. MACD (Moving Average Convergence Divergence)

3. Williams %R

4. Bollinger Bands

5. Volume Analysis

6. Divergence Detection (Optional)

🎨 Visual Signals

Entry Signals:

🟢 Green Triangle (below candle) = BUY LONG signal

🔴 Red Triangle (above candle) = SELL SHORT signal

Exit Signals:

🟣 Purple Label = Position closed (shows "x2", "x3" if multiple entries)

Additional Indicators:

💎 Aqua Diamond = Bullish divergence detected

💎 Fuchsia Diamond = Bearish divergence detected

🔵 Blue Background = NY Session active

🟡 Yellow Bar Tint = Volume spike detected

⚪ Small Circles = Near-signal conditions (2+ indicators aligned)

Live Counter:

Top corner shows: "Bull: X/4" and "Bear: X/4"

Indicates how many indicators currently align

⚙️ How to Use This Strategy

For Beginners (More Signals):

Set "Min Indicators Aligned" to 2

Turn OFF "Require Divergence"

Turn OFF "Require Volume Spike"

Turn OFF "Require Reversal Candle Pattern"

Keep "Allow Multiple Entries" OFF

This gives you more frequent signals to learn from.

For Advanced Traders (High Probability):

Set "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Turn ON "Require Reversal Candle Pattern"

Adjust stop loss to your risk tolerance

This filters for only the highest-quality setups.

Recommended Settings for 1-Hour Charts:

Min Indicators Aligned: 3

Stop Loss: 2.5%

Take Profit: 5.0%

RSI Length: 14

Williams %R Length: 14

Volume Multiplier: 1.5x

Session: NY only (for stocks)

BUY SIGNAL generated when:

2-4 indicators show oversold/bullish conditions:

RSI < 30 and turning up

MACD crossing bullish or histogram positive

Williams %R < -80 and turning up

Price at/below lower Bollinger Band

Optional confirmations (if enabled):

Bullish divergence detected

Volume spike present

Bullish reversal candle pattern

Session filter: Signals only during NY trading hours