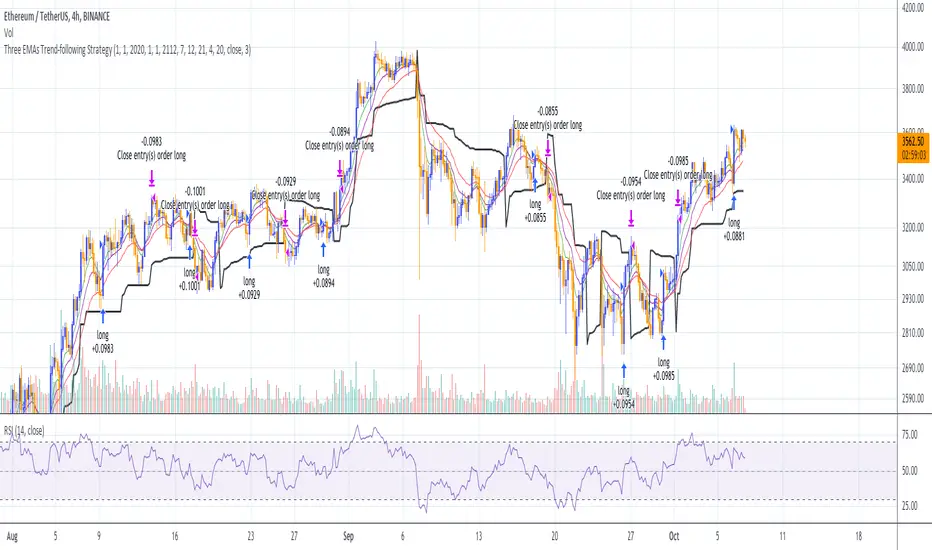

Three EMAs Trend-following Strategy (by Coinrule)Trend-following strategies are great because they give you the peace of mind that you're trading in line with the market.

However, by definition, you're always following . That means you're always a bit later than your want to be. The main challenges such strategies face are:

Confirming that there is a trend

Following the trend, hopefully, early enough to catch the majority of the move

Hopping off the trade when it seems to have run its course

This EMA Trend-following strategy attempts to address such challenges while allowing for a dynamic stop loss.

ENTRY

The trading system requires three crossovers on the same candle to confirm that a new trend is beginning:

Price crossing over EMA 7

Price crossing over EMA 14

Price crossing over EMA 21

The first benefit of using all three crossovers is to reduce false signals. The second benefit is that you know that a strong trend is likely to develop relatively soon, with the help of the fast setup of the three EMAs.

EXIT

The strategy comes with a fixed take profit and a volatility stop, which acts as a trailing stop to adapt to the trend's strength. That helps you get out of the way as soon as market conditions change. Depending on your long term confidence in the asset, you can edit the fixed take profit to be more conservative or aggressive.

The position is closed when:

The price increases by 4%

The price crosses below the volatility stop.

The best time frame for this strategy based on our backtest is the 4-hr. Shorter timeframes can also work well, although they exhibit larger volatility in their returns. In general, this approach suits medium timeframes. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

You can execute this strategy on your favourite exchange at coinrule.com

在腳本中搜尋"Exponential"

User Selectable Moving Average GuppyA version of the popular "Moving Average Ribbon" or "Guppy" indicators, except nearly everything about it is user selectable. The user can change the source, period, and type of moving average used for every single line on the chart. Note: The visuals are fairly intensive and may take a moment to catch up after adjusting settings.

Credit: This script utilizes the "Color Gradient Framework" tutorial by LucF (PineCoders) to create gradient visuals, which are also customizable for the user.

Moving Average Options:

Running (SMoothed) Moving Average (RMA or SMMA) - Slowest

Simple Moving Average (SMA) - Slow

Exponential Moving Average (EMA) - Responds faster to price than SMA

Weighted Moving Average (WMA)

Volume-Weighted Moving Average (VWMA)

Triple EMA (TEMA)

Exponential Hull Moving Average (EHMA) - Hull with Smoothing (Slower than Hull)

Least Squares Moving Average (LSMA) - Simple Linear Regression

Arnaud Legoux Moving Average (ALMA) - Adjustable, set offset=1 to be current, offset=0.85 for good smoothing (Slower)

Hull Moving Average (HMA) - Normally responds fastest to price of all options

Value Added :

This script is unique in that it allows the user to chart the "Guppy", except nearly everything about it is customizable. The user can change the source, period, and type of moving average used for every single line.

Typically, the Guppy is plotted with simple moving average or exponential moving average, which respond much slower to price than the Hull Moving Average, which this indicator uses as default. (Elimination of lag)

The Hull MA settings for the highest time frame moving averages should work well for assessing the overall macro trend, with a nice visual presentation. Additional labels and alerts for the macro trend are available.

Furthermore, this script provides many more options for type of moving average than is typical for a moving average indicator that provides the user with options, including advanced options such as Hull, TEMA, and ALMA.

The visual presentation is customizable and should provide some entertainment for users who want to create pretty charts.

MACD PRO by LDZ1LANDZZ1 MACD Pro was developed to show the first signs of reversal, direction, and also trend strength.

Unlike normal MACD, this indicator has 3 lines as information. A white line (short EMA), a purple line (sign), and a yellow line (long EMA).

The Purple Line "Signal" is a 17-period Exponential Moving Average.

The White Line "Short EMA" is a 34-period Exponential Moving Average.

The Yellow Line "Long EMA" is a 72-Period Exponential Moving Average.

When the background color turns green it indicates that we are above 0 (positive trend) and above the Signal line (positive trend)

When the background color turns Yellow it indicates that we are above 0 (positive trend) but below the Signal line (Indicating Attention to a possible trend reversal or price correction)

When the background color turns Red it indicates that we are below 0 (negative trend) and below the Signal line (negative trend)

When the background color turns Orange it indicates that we are below 0 (negative trend) and above the signal line (Indicating attention to a possible trend reversal or price correction)

The Yellow line is like a watershed, when the White Line "Short EMA" crosses above or below it, it indicates that a stronger price movement may occur.

Tip:

Only enter Long Positions when the background color turns green and the Short EMA (White line) is above the yellow line and/or the white dotted horizontal line.

Only enter Short Positions when the background color turns red and the Long EMA (Yellow line) is below the white dotted horizontal line.

Note the difference of MACD Pro by LANDZZ1 as the traditional MACD.

----------------------------------------------------------

Description in Portuguese-BR

MACD Pro by LANDZZ1 foi desenvolvido para mostrar os primeiros sinais de reversão, direção e também força da tendência.

Diferente do MACD normal, este indicador tem como informação 3 linhas. Uma linha branca (short EMA), uma linha roxa(signal) e uma linha amarela (long EMA).

A Linha Roxa "Signal" é uma Média Móvel Exponencial de 17 períodos.

A Linha branca "Short EMA" é uma Média Móvel Exponencial de 34 períodos.

A Linha Amarela "Long EMA" é uma Média Móvel Exponencial de 72 Períodos.

Quando a cor de fundo ficar verde indica que estamos acima de 0 (tendência positiva) e acima da linha de Sinal (tendência positiva)

Quando a cor de fundo ficar Amarelo indica que estamos acima de 0 (tendência positiva) porém abaixo da linha de Sinal (Indicando Atenção a uma possível reversão de tendência ou correção de preço)

Quando a cor de fundo ficar vermelho indica que estamos abaixo de 0 (tendência negativa) e abaixo da linha de Sinal (tendência negativa)

Quando a cor de fundo ficar laranja indica que estamos abaixo de 0 (tendência negativa) e acima da linha de sinal (Indicando atenção a uma possível reversão de tendência ou correção do preço)

A linha amarela é como um divisor de águas, quando a linha branca (Short EMA) cruza para cima ou para baixo dela, indica que um movimento mais forte forte de preço poderá ocorrer.

Dica:

Apenas entre em Long Positions quando a cor de fundo ficar verde e se a Short EMA (linha Branca) estiver acima da linha amarela e/ou da linha horizontal pontilhada branca.

Apenas entre em Short Positions quando a cor de fundo ficar Vermelha e se a Long EMA (linha Amarela) estiver abaixo da linha horizontal pontilhada branca.

Repare a diferença do MACD Pro by LANDZZ1 como o MACD tradicional.

ADX / RSI Strategy by Trade Rush (created by SirPoggy) This is one of many new strategies coming soon which were seen on Trade Rush

This one is the ADX / RSI Strategy seen here:

https:www.youtube.com/watch?v=uSkGE0ujyn4

While the strategy has been modified slightly to use the DMI instead of the ADX, the core of the strategy is essentially the same

Long signals are generated when the RSI is above 70, close is above the 200EMA, and the ADX is above 25 (added is the plus DMI over 25 and minus DMI below 20)

Stop loss is placed below /above the 21 EMA, however, there is a deviation required to ensure price is not too close to where a stop loss would be placed.

Short signals are generated when the RSI is below 30, close is below the 200EMA, and the ADX is above 25 (added is the minus DMI over 25 and plus DMI below 20)

I do not recommend using this strategy but I have provided this code for educational purposes.

Thanks!

Let me know which strategy you'd like coded next in the comments below.

RSI Cross [xaurr]This is simple but profitable rsi cross strategy, to find optimal values you can change rsi and ema periods.

Good Luck!

TradePro's Trading Idea Cipher Divergence EMA Pb StrategyHere I present you on of Trade Pro's Trading Idea: Cipher B+ Divergence EMA Pullback Strategy.

Optimized the crypto pairBTC/USDT in the 30 minute chart.

There is the possibility to switch between short and long positions.

You can choose between 2 different take profit/stop loss types: The Lowest Low/ Highest High Stop Loss/ Take Profit and the ATR Take Profit/ Stop Loss.

-----------------------------------------------------------------------------------

How does the strategy work?

ENTRY

Long

The price must be above the 200 EMA .

The price needs to make a pullback into the 50 EMA .

Right after that, the Cipher B indicator must give a buy signal, it must be below the zero line and the Money Flow cloud must be green.

Short

Contrary to the premise of long positions.

EXIT

Lowest Low/ Highest High Exit

The Lowest Low (long) / highest high (short) serves as the stop loss. The TP is formed on the basis of a factor.

(Long for example: *Lowest Low* multiplied by *Profitfactor* = TP).

ATR Exit

The value of ATR at the time of buying is multiplied by the value entered in "Profit factor ATR" and "Stop factor ATR". As soon as the price reaches this value, it is closed.

Important

The script must be optimized for each coin or currency pair. However, only the values for the profit factor, the stop loss and Lowest Low / Highest High are relevant.

Also, by changing the Chanel Length and the Chanel Average, you can create strong profit changes.

The results of the strategy are without commissions and leverage.

If you have any questions or feedback, please let me know in the comments.

If you need more information about the strategy and want to know exactly how to apply it, check out my profile. There I have created a tutorial for the function of the script.

3GBH - Multiple MA'sIncluded in this indicator:

- Fast/Slow EMA's

- Fast/Slow SMA's

- Fast/Slow WMA's

- Fast/Slow HMA's

- Fast/Slow RMA's

-----

Use of of the type of Moving Averages.

Or use them all.

-----

User-friendly.

You can change all the inputs, they are labelled for ease-of-use.

You can toggle On/Off any or all of the options.

Ichimoku EMA RSI - Crypto only long StrategyHey there!

Here I show you an Ichimoku Cloud Strategy.

I discovered the strategy on a YouTube channel and tried to transfer it as a strategy into a script.

He said in his video that you would make more profit with this strategy than holding the coin.

Tested with the crypto pair ETH/USDT in the four hour chart.

Period: beginning of 2017 until today.

The strategy should also work with foreign exchange. But then the settings have to be adjusted.

There is the possibility to activate two EMA's and a Stochastic RSI .

-----------------------------------------------------------------------------------

How does the strategy work?

ENTRY

The green Ichimoku lead line must above the red Ichimoku lead line - only the two lead lines are activated.

A green candle must closed above the green lead line.

EXIT

A red candle must close below the green Ichimoku lead line.

OPTIONAL ENTRY

EMA

Once you activate the EMA , long positions will only be taken once the EMA1 is above the EMA2.

Thereby I could observe a significant increase of the profit as well as a decrease of the maximum drawdown.

RSI

As soon as you activate the Stochastic RSI , long positions are only taken when the K line is above the D line.

In the future, I may add an oversold - undersold parameter.

The results of the strategy are without commissions and levers.

If you have any questions or feedback, please let me know in the comments.

If you need more information about the strategy and want to know exactly how to apply it, check out my profile.

I wish you good luck with the strategy!

Shaded Tripple MAsThree moving averages that have shaded area between its sma and ema versions. Default lengths are 50, 100 and 200.

Custom Multi-Timeframe Screener with AlertsThis is a multi-timeframe screener with alerts. Use this way you can create a screener on indicators using 2 or more timeframes.

In TradingView there is a limit of 40 security function calls. Every timeframe requires another security call so you can screen fewer symbols with any additional timeframe.

In this example, I use 2 timeframes, so the maximum amount of symbols you can scan is 40/2 = 20.

For 3 timeframes - 13, 4tfs - 10, 5tfs - 8 symbols and so on.

In this simplistic example, I require a cross of EMAs on the current timeframe and confirmation that one EMA above/below another from the second timeframe.

Of course, you can create much more complicated functions for this screener.

Params

- higher timeframe

- ema params

- 20 symbol inputs for instruments you want to use in this screener

Alerts

You can create an alert from it easily by selecting the screener name from the list and then selecting "Any alert() function call".

No additional configuration is required, message and alert on close is generated in the code.

You should better change the default name for your alert. Sometimes because of big amount of inputs you might receive an error.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

Moving Average Percentage Hunter by HassonyaIn this indicator study, we aim to capture the moving averages to which the bar close is closest. The indicator shows the moving averages, which are closest to the percentage value we selected, on the label. It indicates the names of the closest averages at the top of the label with a (near) note next to them. If none of the averages are close to the specified percentage value, there will be a no nearness warning. The indicator supports the heikin ashi candles. For this setting, check the I'm using heikin ashi candles box.

Thanks to this feature of the indicator, you will be able to see bar proximity to the moving averages you use continuously. You can make purchases and sales by using this feature to your advantage. This way you can easily catch reaction turns.

If you want, you can turn off moving averages in the settings section. You can open it whenever you need. You can do this in the show moving averages box. Appears if you check it, disappears if you uncheck it.

There are 5 moving average options. SMA, EMA, WMA, TMA and HullMA moving averages. Moving average names and values in the list are dynamically adjusted. When you change the settings, the moving average names and values in the list will change automatically. At the bottom of the settings, you can determine the lengths of the moving averages yourself. In the next update, each moving average will have a different average option.

You can enter percentage values, fractional figures. for example (3.5, 5.2 vb.) The indicator will show you the value you give and the proximity of the value below that value. You can adjust this setting in MA Percentage Nearness.

More detailed options will be available in the next update. Range of values, options below, above, and so on.

In the settings section, there is a Show distance option. If you check this option, you can continuously see the percentage values of the distance to the moving averages on the label. For this feature, you have to check the show distance box.

The alarm feature will come in the next update.

Thanks for support. Good Luck.

4-Hour Stochastic EMA TrendThis trading strategy relies heavily on catching the trend. You

may have success using this strategy on as low as the one hour

chart or as high as the daily chart; however, I’ve had most

success trading it on the four hour chart. This strategy consists

of four indicators, which are:

1. 5 Period Exponential Moving Average (closed)

2. 15 Period Exponential Moving Average (closed)

3. 50 Period Exponential Moving Average (closed)

4. Stochastic indicator K=13 D=5 Smooth=5 (13,5,5) 80/20

Levels

Refer

3 EMA Stochastik RSI ATR SL TP only LONGHey there!

Here i will show you the 3 EMA RSI Stochastic Crossover strategy with an ATR SL and TP.

The strategy works as follows:

For long positions, the EMA's must be in the following order:

The 8 E M A must be above the 14 E M A and the 14 E M A must be above the 50 E M A.

The buy signal is given to us by the Stochastic RSI indicators.

The K line must cross the D line above. The following candle must then close above all E M A's.

The stop loss is determined by three times the value of the ATR.

The take profit is determined by two times the value of the ATR.

In this strategy only long positions are traded.

Custom WaterMark + 4EMA [SilentKreator]4 Ema + Custom Watermark, you can customize everything, in the watermark you can write your name, is a tool to visually protect your work, mainly for streamers and analysts.

Durbtrade Bollinger Bands WidthFirst published script. Actually, this is my 1st script ever! I know its not flashy or anything, but I finally decided to try learning some pine... and to try and get rid of the dang 0 on my profile, haha. So here are the results after many hours.

I like using the BB Width indicator, and I wanted it to change color based on whether is was rising or falling. I also have it to automatically plot a horizontal line at 0 so I don't have to draw a line every time I apply the indicator to a new chart. And I changed the default precision to 3.

I noticed that there aren't that many BB Width scripts. and I don't think there is anything like this out there that I know of, so I hope someone else besides me will find it useful.

Please feel free to comment.

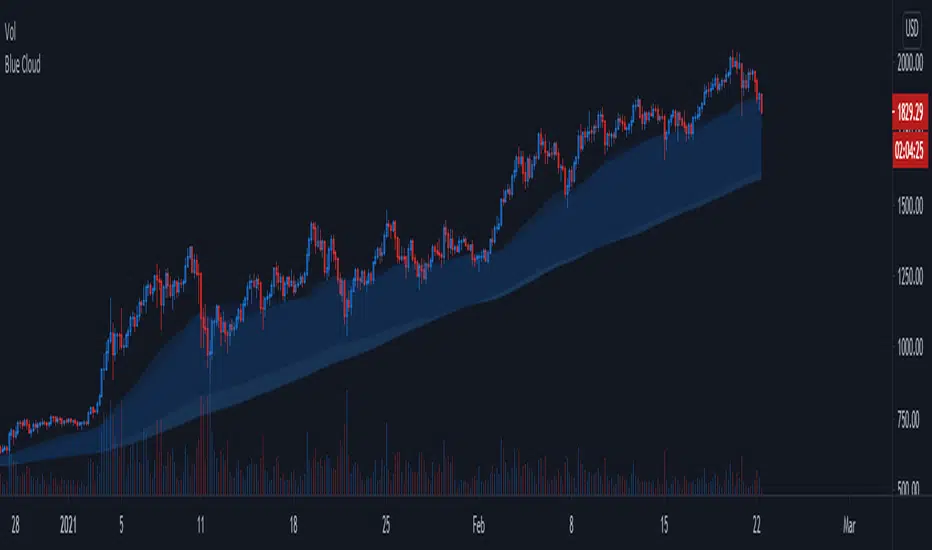

Blue CloudTrend Indicator

- Based on 4h 50/200 ma/ema

- Static, same accross all timeframes

- Works best with trending assets (espacially altcoins)

- 4h 50/200 ma/ema 's are transparent by default but can be enabled to improve visibility

Blue Cloud = Bullish, cloud often acts as support

Red Cloud = Bearish, cloud often acts as resistance

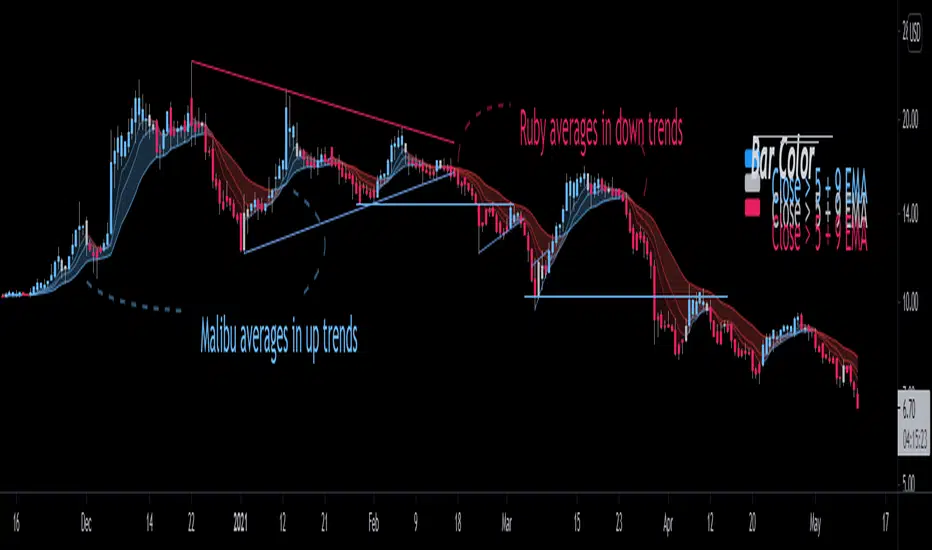

Bjorgum EMAThis is an answer back to repeated requests for a simple version of Bjorgum Triple EMA Strat, which is not recommended for use with Heiken Ashi candles as it results in "double smoothing" of the averages and can give late signals as a result.

The inputs are raw and super basic. At its core its really just 3 EMAs that you can customize the source and length. The averages and shadowing change color based on if they are either rising or falling.

default values are 5, 9, and 21 EMA on open as source.

Bar color is dictated by the bar close over or under the 5 and 9 EMA.

This is suitable for use on HA candle.

EMA Cross Levels + Standard DeviationPlots the price level that the most recent EMA crossover occurred at(Green if bullish and red if bearish).

Also calculates standard deviation over a shorter window-length/lookback period (of 'n_std_fast' length) and another over a much longer span of periods(n='n_std_slow', > 'n_std_fast').

These are the two dotted lines appearing as bands around the cross-level line.

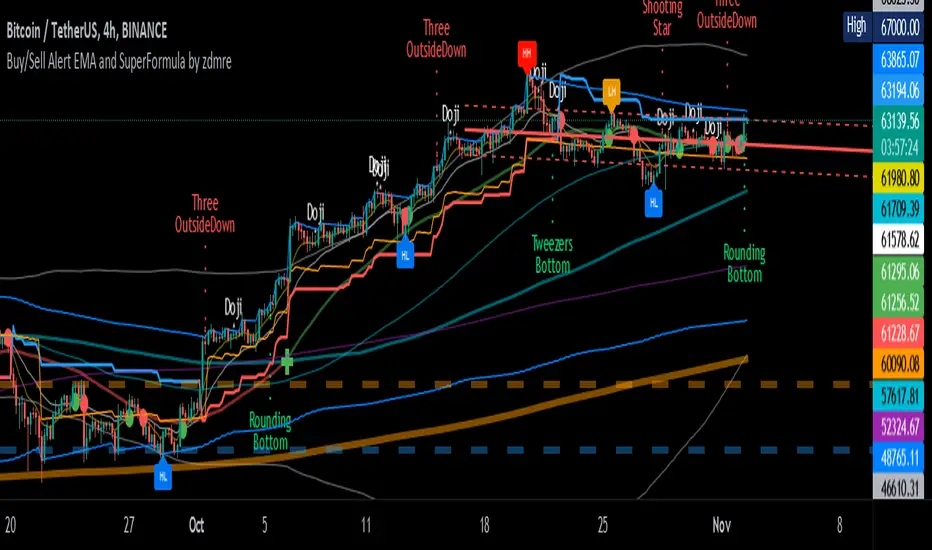

Buy/Sell Alert EMA with SuperFormula by zdmre*** Use it at your own risk

This indicator has 3 indicators and gives a buy/sell signal depending on the EMA.

3 indicators:

- Ichimoku

- Bollinger Band

- EMA

It also shows the value on the candle as a warning in the Buy and Sell signals. This value is calculated with a special formula I have created.

On the other hand Bollinger Band and Ichimoku Cloud are also included to check the accuracy of the signals.

For this indicator, I recommend a minimum of 4 hours chart.

Custom Moving Average (EMA & SMA)This script is a custom visualization tool to plot 4 Moving Averages (MA).

Each MA is customizable; you can:

enable (disable) the plot of MA;

select whether the MA is an EMA or an SMA;

the length;

the source (open, close, ...);

the offset value (default is 0).

Note:

The 1st MA is an EMA with length 50.

The others MAs are SMA with length 9, 30 and 100 respectively.

Momentum Explosion 2CCI RSI"Momentum Explosion Template for Mobile Metatrader", that is a trading system trend momentum based on two Commodity Channel Index (CCI) , RSI and two Moving Averages.The trading signals are generated by the crossing of the moving averages confirmed by the agreement of the two CCIs and the RSI.

Two Moving averages Filtered by double CCI and RSI

Credit is to Dimitri Author Beejay (Forex Factory)

Trading Rules Momentum Explosion

Buy

EMA 8 crosses upward SMA 26.

CCI 34 periods > 0

CCI 55 periods > 0

RSI 26 > 48.

Sell

EMA 8 crosses downward SMA 26.

CCI 34 periods < 0

CCI 55 periods < 0

RSI 26 < 48.

Triple EMA Scalper low lag stratHi all,

This strategy is based on the Amazing scalper for majors with risk management by SoftKill21

The change is in lines 11-20 where the sma's are replaced with Triple ema's to

lower the lag.

The original author is SoftKill21. His explanation is repeated below:

Best suited for 1M time frame and majors currency pairs.

Note that I tried it at 3M time frame.

Its made of :

Ema ( exponential moving average ) , long period 25

Ema ( exponential moving average ) Predictive, long period 50,

Ema ( exponential moving average ) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA . and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA , and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips