Parabolic SAR with Volatility Filter: Buy Alerts for 3commasHey folks and fellow 3commas users !

Here is a new signal generator for your DCA bot on 3commas.

This is a classic Parabolic SAR indicator with a filter for volatility.

NOTE: This is a repainting strategy by design. Recommended to use with "Once per bar" alert style for PSAR

在腳本中搜尋"Volatility"

Lakshmi - Low Volatility Range Breakout (LVRB)⚡️ Overview

The Low Volatility Range Breakout (LVRB) indicator is designed to identify consolidation phases characterized by suppressed volatility and generate actionable signals when price breaks out of these ranges. The underlying premise is rooted in the market principle that periods of low volatility often precede significant directional moves—volatility contraction leads to expansion.

Important Note on Optimization: The default parameter settings of this indicator have been specifically optimized for BTCUSDT on the 2-hour (2H) timeframe. While the indicator can be applied to other instruments and timeframes, users are encouraged to adjust the parameters accordingly to suit different trading conditions and asset characteristics.

This indicator automates the detection of "quiet" accumulation/distribution zones and provides clear visual cues and alerts when a breakout occurs.

⚡️ How to Use

1. Add the indicator to your chart. Default settings are optimized for BTCUSDT 2H.

2. Wait for a gray box to appear—this indicates a qualified low-volatility range is forming.

3. Monitor for breakout signals:

• LONG (green triangle below bar): Price broke above the range. Consider entering a long position.

• SHORT (red triangle above bar): Price broke below the range. Consider entering a short position.

4. Set alerts using "LVRB LONG" or "LVRB SHORT" to receive notifications on confirmed breakouts.

5. Adjust parameters as needed for different instruments or timeframes.

Tip: Combine with volume analysis or trend filters for higher-probability setups.

⚡️ How It Works

1. Low Volatility Bar Detection

A bar is classified as "low volatility" when it meets the following criteria:

• True Range (TR) is at or below the average TR (Simple Moving Average) multiplied by a user-defined threshold.

• (Optional) Candle Body is at or below the average body size multiplied by a separate threshold.

This dual-filter approach helps isolate bars that exhibit genuine compression in both range and directional commitment.

2. Range Box Formation

When consecutive low-volatility bars are detected, the indicator begins constructing a consolidation box:

• The box expands to encompass the high and low of qualifying bars.

• A minimum number of bars and a minimum fraction of low-volatility bars are required for the box to become "qualified" (active).

• A configurable tolerance allows for a limited number of consecutive non-low-vol bars within the sequence, accommodating minor noise without invalidating the range.

• If the box height exceeds a maximum threshold (defined as a multiple of the base ATR at sequence start), the range is invalidated.

3. Breakout Detection

Once a qualified range is established, the indicator monitors for breakouts:

• Wick Mode: Requires both a wick pierce beyond the range boundary AND a close outside the range.

• Close Mode: Requires only a close beyond the range boundary.

• (Optional) Breakout Body Filter: The breakout candle's body must exceed a multiple of the average body size at range formation.

• (Optional) Candle Direction Filter: Bullish breakouts require a green candle; bearish breakouts require a red candle.

Signals are displayed in real-time and confirmed upon bar close.

⚡️ Inputs & Parameters

• Volatility Window: Lookback period for calculating average TR and average body size.

• TR Multiplier: A bar's TR must be ≤ avgTR × this value to qualify as low-vol.

• Body Multiplier: A bar's body must be ≤ avgBody × this value (if body filter is enabled).

• Use Body Filter: Toggle the body size filter on/off.

• Min Bars in Box: Minimum number of bars required for a range to become qualified.

• Min Low-Vol Fraction: Minimum proportion of bars in the sequence that must be low-vol.

• Allowed Consecutive Non-Low-Vol Bars: Tolerance for consecutive bars that do not meet low-vol criteria.

• Max Box Height: Maximum allowed range height as a multiple of the base ATR.

• Breakout Mode: Choose between "Wick" (pierce + close) or "Close" (close only).

• Breakout Body Multiplier: Require breakout candle body ≥ avgBody × this value (1.0 = OFF).

• Require Candle Direction: Enforce green candle for LONG, red candle for SHORT.

⚡️ Visual Features

• Consolidation Boxes: Displayed in neutral (gray) color during formation. Upon a confirmed breakout, the box is colored green for bullish breakouts or red for bearish breakouts.

• Breakout Signals:

• LONG: Green upward triangle displayed below the price bar with "LONG" label.

• SHORT: Red downward triangle displayed above the price bar with "SHORT" label.

• Range Levels: Optional horizontal plots for the active range's high and low.

• Invalidated Boxes: Optionally retained in neutral (gray) color or deleted from the chart.

• Full Customization: Colors, transparency, and border width are all adjustable.

⚡️ Alerts

Two alert conditions are available:

• LVRB LONG: Triggered on a confirmed bullish breakout (bar close).

• LVRB SHORT: Triggered on a confirmed bearish breakout (bar close).

⚡️ Use Cases

• Breakout Trading: Enter positions when price escapes a well-defined low-volatility range.

• Volatility Expansion Plays: Anticipate increased volatility following periods of compression.

• Filtering Choppy Markets: Avoid trading during extended consolidation; wait for confirmed breakouts.

• Multi-Timeframe Analysis: Use on higher timeframes to identify major consolidation zones.

⚡️ Notes

• Best used in conjunction with volume analysis, trend context, or support/resistance levels for confirmation.

• Performance varies across instruments and timeframes; backtesting and parameter optimization are recommended.

⚡️ Credits

Developed by Lakshmi. Inspired by volatility contraction principles and range breakout methodologies.

⚡️ Disclaimer

This indicator is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a guarantee of profits. Trading financial instruments involves substantial risk, and you may lose more than your initial investment. Past performance, whether indicated by backtesting or historical analysis, does not guarantee future results. The use of this indicator does not ensure or promise any profits or protection against losses. Users are solely responsible for their own trading decisions and should conduct their own research and/or consult with a qualified financial advisor before making any investment decisions. By using this indicator, you acknowledge and accept that you bear full responsibility for any trading outcomes.

Asset Volatility Heatmap [SeerQuant]Asset Volatility Heatmap (AVH)

AVH is a cross-sectional volatility dashboard that ranks up to 30 assets and visualizes regime shifts as a time-series heatmap.

It computes annualized historical volatility (%) on a fixed 1D basis, then maps each asset’s volatility into a configurable color spectrum for fast, intuitive scanning of risk conditions across cryptocurrencies.

⚙️ How It Works

1. Daily, Annualized Historical Volatility

Each asset is measured on a fixed 1D timeframe (independent of your chart timeframe). Volatility is annualized and expressed in percentage terms. The user can choose between 1 of 4 volatility estimators: Close-Close (log returns stdev), Parkinson (H/L), Garman-Klass or Rogers-Satchell.

2. Heatmap

A heatmap is plotted on the lower window (sorting is turned on by default). Each row represents a rank position. (Rank #1 highest vol ... Rank #30 lowest vol). This means that tokens will move between rows over time as their volatility changes. The asset labels show the current token sitting in each rank bucket. This setting can be turned off for more of a "random" look.

3. Color Scaling

The user can select how the color range is normalized for visualization.

n = (v - scaleMin) / (scaleMax - scaleMin)

Cross-Section: Scales colors using the current bar’s cross-sectional min/max across the asset list.

Rolling: Scales colors using a lookback window of cross-sectional ranges, so today’s values are judged relative to recent volatility history.

Fixed: Uses your chosen Fixed Scale Min / Max for consistent benchmarking across time.

4. Contrast Control

The Color Contrast control option changes how aggressively the palette emphasizes extremes (useful for making “risk spikes” pop vs keeping gradients smooth).

5. Summary Table + Composite Read

The table highlights the highest vol / lowest vol token, along with average / median volatility, and a simple regime read (low / medium / high cross-sectional volatility).

✨ How to Use (Practical Reads)

Spot risk-on / risk-off transitions: When the heatmap “heats up” broadly (more hot colors across ranks), cross-sectional volatility is expanding (higher dispersion / risk).

Identify which names are driving the narrative: With sorting ON, the top ranks show which assets are currently the volatility leaders — often where attention, liquidity, and positioning stress is concentrated.

Use it as a regime overlay: Low/steady colors across most ranks tends to align with calmer conditions; sharp bright bursts signal volatility events.

✨ Customizable Settings

1. Assets

30 symbol inputs (defaults to crypto, but works across markets)

2. Calculation Settings

Length (lookback)

Volatility Estimator (Close-Close / Parkinson / GK / RS)

3. Style Settings

Color Scheme (SeerQuant / Viridis / Plasma / Magma / Turbo / Red-Blue)

Color Scaling (Cross-Section / Rolling / Fixed)

Scaling Lookback (for Rolling)

Fixed Scale Min / Max (for Fixed)

Color Contrast (emphasize extremes vs smooth gradients)

Sort Heatmap (High → Low)

Gradient Legend toggle

Focus Mode (highlights the chart symbol if included)

Ticker Label Right Padding

🚀 Features & Benefits

Cross-sectional volatility at a glance (dispersion/risk conditions)

Sortable rank heatmap for tracking “who’s hot” in volatility

Multiple estimators for different volatility philosophies

Flexible normalization (current cross-section, rolling context, or fixed benchmarks)

Clean legend + summary stats for quick context

📌 Notes

Sorting changes which token appears in each row over time (rows are rank buckets).

Volatility is computed on 1D even if your chart is lower/higher timeframe.

📜 Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always consult a licensed financial advisor before making trading decisions. Use at your own risk.

Trading Volatility Clock⏰ TRADING VOLATILITY CLOCK - Know When the Action Happens (Anywhere in the World)

A real-time session tracker with multi-timezone support for active traders who need to know when US market volatility strikes - no matter where they are in the world. Perfect for day traders, scalpers, and anyone trading liquid US markets.

══════════════════════════════════════════════════════

📊 WHAT IT DOES

This indicator displays a live clock showing:

- Current time in YOUR selected timezone (10 major timezones supported)

- Active US market session with color-coded volatility levels

- Countdown timer showing time remaining in current session

- Preview of the next upcoming session

- Optional alerts when entering high-volatility periods

══════════════════════════════════════════════════════

🌍 MULTI-TIMEZONE SUPPORT

SESSIONS ALWAYS TRACK US MARKET HOURS (Eastern Time):

No matter which timezone you select, the sessions always trigger at the correct US market times. Perfect for international traders who want to:

• See their local time while tracking US market sessions

• Know exactly when US volatility hits in their timezone

• Plan their trading day around US market hours

SUPPORTED TIMEZONES:

• America/New_York (ET) - Eastern Time

• America/Chicago (CT) - Central Time

• America/Los_Angeles (PT) - Pacific Time

• Europe/London (GMT) - Greenwich Mean Time

• Europe/Berlin (CET) - Central European Time

• Asia/Tokyo (JST) - Japan Standard Time

• Asia/Shanghai (CST) - China Standard Time

• Asia/Hong_Kong (HKT) - Hong Kong Time

• Australia/Sydney (AEDT) - Australian Eastern Time

• UTC - Coordinated Universal Time

EXAMPLE: A trader in Tokyo selects "Asia/Tokyo"

• Clock shows: 11:30 PM JST

• Session shows: "Opening Drive" 🔥 HIGH

• They know: US market just opened (9:30 AM ET in New York)

══════════════════════════════════════════════════════

🎯 WHY IT'S USEFUL

Whether you trade futures, high-volume stocks, or ETFs, volatility isn't constant throughout the day. Knowing WHEN to expect movement is critical:

🔥 HIGH VOLATILITY (Red):

• Opening Drive (9:30-10:30 AM ET) - Highest volume of the day

• Power Hour (3:00-4:00 PM ET) - Second-highest volume, final push

⚡ MEDIUM VOLATILITY (Yellow):

• Pre-Market (8:00-9:30 AM ET) - Building momentum

• Lunch Return (1:00-2:00 PM ET) - Traders returning

• Afternoon Session (2:00-3:00 PM ET) - Trend continuation

• After Hours (4:00-5:00 PM ET) - News reactions

💤 LOW VOLATILITY (Gray):

• Overnight Grind (12:00-8:00 AM ET) - Thin volume

• Mid-Morning Chop (10:30-11:30 AM ET) - Ranges form

• Lunch Hour (11:30 AM-1:00 PM ET) - Dead zone

• Evening Fade (5:00-8:00 PM ET) - Volume dropping

══════════════════════════════════════════════════════

⚙️ CUSTOMIZATION OPTIONS

TIMEZONE SETTINGS:

• Select from 10 major timezones worldwide

• Clock automatically displays in your local time

• Sessions remain locked to US market hours

SESSION TIME CUSTOMIZATION:

• Every session boundary is adjustable (in minutes from midnight ET)

• Perfect for traders who define sessions differently

• Advanced users can create custom volatility schedules

DISPLAY OPTIONS:

• Toggle next session preview on/off

• Enable/disable high volatility alerts

• Clean, unobtrusive table display in top-right corner

══════════════════════════════════════════════════════

💡 HOW TO USE

1. Add indicator to any chart (works on all timeframes)

2. Select your timezone in Settings → Timezone Settings

3. Set your chart to 1-minute timeframe for real-time updates

4. Customize session times if needed (Settings → Session Time Customization)

5. Watch the top-right corner for live session tracking

TRADING APPLICATIONS:

• Avoid trading during dead zones (lunch hour, mid-morning chop)

• Increase position size during high volatility windows

• Set alerts for Opening Drive and Power Hour

• Plan your trading day around US market volatility schedule

• International traders can track US sessions in their local time

══════════════════════════════════════════════════════

🎓 EDUCATIONAL VALUE

This indicator teaches traders:

• Market microstructure and volume patterns

• Why certain times produce better opportunities

• How institutional flows create intraday patterns

• The importance of timing in active trading

• How to adapt US market trading to any timezone

══════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

- Works best on 1-minute charts for frequent updates

- Sessions are ALWAYS based on US Eastern Time (ET)

- Timezone selection only changes the clock display

- Clock updates when new bar closes (not tick-by-tick)

- Alerts trigger once per bar when enabled

- Perfect for international traders tracking US markets

══════════════════════════════════════════════════════

📈 BEST USED WITH

- High-volume US stocks: TSLA, NVDA, AAPL, AMD, META

- Major US ETFs: SPY, QQQ, IWM, DIA

- US Futures: ES, NQ, RTY, YM, MES, MNQ

- Any liquid US instrument with clear intraday volume patterns

══════════════════════════════════════════════════════

🌏 FOR INTERNATIONAL TRADERS

This tool is specifically designed for traders outside the US who need to:

• Track US market sessions in their local timezone

• Know when to be at their desk for US volatility

• Avoid waking up for low-volatility periods

• Maximize trading efficiency around US market hours

No more timezone confusion. No more missing the opening bell. Just set your timezone and trade with confidence.

══════════════════════════════════════════════════════

This is an open-source educational tool. Feel free to modify and adapt to your trading style!

Happy Trading! 🚀

Return Volatility (σ) — auto-annualized [v6]Overview

This indicator calculates and visualizes the return-based volatility (standard deviation) of any asset, automatically adjusting for your chart's timeframe to provide both absolute and annualized volatility values.

It’s designed for traders who want to filter trades, adjust position sizing, and detect volatility events based on statistically significant changes in market activity.

Key Features

Absolute Volatility (abs σ%) – Standard deviation of returns for the current timeframe (e.g., 1H, 4H, 1D).

Annualized Volatility (ann σ%) – Converts abs σ% into an annualized figure for easier cross-timeframe and cross-asset comparison.

Relative Volatility (rel σ) – Ratio of current volatility to the long-term average (default: 120 periods).

Z-Score – Number of standard deviations the current volatility is above or below its historical average.

Auto-Timeframe Adjustment – Detects your chart’s bar size (seconds per bar) and calculates bars/year automatically for crypto’s 24/7 market.

Highlight Mode – Optional yellow background when volatility exceeds set thresholds (rel σ ≥ threshold OR z-score ≥ threshold).

Alert Conditions – Alerts trigger when relative volatility or z-score exceed defined limits.

How It Works

Return Calculation

Log returns: ln(Pt / Pt-1) (default)

or Simple returns: (Pt / Pt-1) – 1

Volatility Measurement

Standard deviation of returns over the lookback period N (default: 20 bars).

Absolute volatility = σ × 100 (% per bar).

Annualization

Uses: σₐₙₙ = σ × √(bars/year) × 100 (%)

Bars/year auto-calculated based on timeframe:

1H = 8,760 bars/year

4H ≈ 2,190 bars/year

1D = 365 bars/year

Relative and Statistical Context

Relative σ = Current σ / Historical average σ (baseLen, default: 120)

Z-score = (Current σ – Historical average σ) / Std. dev. of σ over baseLen

Trading Applications

Volatility Filter – Only allow trade entries when volatility exceeds historical norms (trend traders often benefit from this).

Risk Management – Reduce position size during high volatility spikes to manage risk; increase size in low-volatility trending environments.

Market Scanning – Identify assets with the highest relative volatility for momentum or breakout strategies.

Event Detection – Highlight significant volatility surges that may precede large moves.

Suggested Settings

Lookback (N): 20 bars for short/medium-term trading.

Base Length (M): 120 bars to establish long-term volatility baseline.

Relative Threshold: 1.5× baseline σ.

Z-score Threshold: ≥ 2.0 for statistically significant volatility shifts.

Use Log Returns: Recommended for more consistent scaling across prices.

Notes & Limitations

Volatility measures movement magnitude, not direction. Combine with trend or momentum filters for directional bias.

Very low volatility may still produce false breakouts; combine with volume and market structure analysis.

Crypto markets trade 24/7 — annualization assumes no market closures; adjust for other asset classes if needed.

💡 Best Practice: Use this indicator as a pre-trade filter for breakout or trend-following strategies, or as a risk control overlay in mean-reversion systems.

[LeonidasCrypto]EMA with Volatility GlowEMA Volatility Glow - Advanced Moving Average with Dynamic Volatility Visualization

Overview

The EMA Volatility Glow indicator combines dual exponential moving averages with a sophisticated volatility measurement system, enhanced by dynamic visual effects that respond to real-time market conditions.

Technical Components

Volatility Calculation Engine

BB Volatility Curve: Utilizes Bollinger Band width normalized through RSI smoothing

Multi-stage Noise Filtering: 3-layer exponential smoothing algorithm reduces market noise

Rate of Change Analysis: Dual-timeframe RoC calculation (14/11 periods) processed through weighted moving average

Dynamic Normalization: 100-period lookback for relative volatility assessment

Moving Average System

Primary EMA: Default 55-period exponential moving average with volatility-responsive coloring

Secondary EMA: Default 100-period exponential moving average for trend confirmation

Trend Analysis: Real-time bullish/bearish determination based on EMA crossover dynamics

Visual Enhancement Framework

Gradient Band System: Multi-layer volatility bands using Fibonacci ratios (0.236, 0.382, 0.618)

Dynamic Color Mapping: Five-tier color system reflecting volatility intensity levels

Configurable Glow Effects: Customizable transparency and intensity settings

Trend Fill Visualization: Directional bias indication between moving averages

Key Features

Volatility States:

Ultra-Low: Minimal market movement periods

Low: Reduced volatility environments

Medium: Normal market conditions

High: Increased volatility phases

Extreme: Exceptional market stress periods

Customization Options:

Adjustable EMA periods

Configurable glow intensity (1-10 levels)

Variable transparency controls

Toggleable visual components

Customizable gradient band width

Technical Calculations:

ATR-based gradient bands with noise filtering

ChartPrime-inspired multi-layer fill system

Real-time volatility curve computation

Smooth color gradient transitions

Applications

Trend Identification: Dual EMA system for directional bias assessment

Volatility Analysis: Real-time market stress evaluation

Risk Management: Visual volatility cues for position sizing decisions

Market Timing: Enhanced visual feedback for entry/exit consideration

Volatility-Adjusted Momentum Score (VAMS) [QuantAlgo]🟢 Overview

The Volatility-Adjusted Momentum Score (VAMS) measures price momentum relative to current volatility conditions, creating a normalized indicator that identifies significant directional moves while filtering out market noise. It divides annualized momentum by annualized volatility to produce scores that remain comparable across different market environments and asset classes.

The indicator displays a smoothed VAMS Z-Score line with adaptive standard deviation bands and an information table showing real-time metrics. This dual-purpose design enables traders and investors to identify strong trend continuation signals when momentum persistently exceeds normal levels, while also spotting potential mean reversion opportunities when readings reach statistical extremes.

🟢 How It Works

The indicator calculates annualized momentum using a simple moving average of logarithmic returns over a specified period, then measures annualized volatility through the standard deviation of those same returns over a longer timeframe. The raw VAMS score divides momentum by volatility, creating a risk-adjusted measure where high volatility reduces scores and low volatility amplifies them.

This raw VAMS value undergoes Z-Score normalization using rolling statistical parameters, converting absolute readings into standardized deviations that show how current conditions compare to recent history. The normalized Z-Score receives exponential moving average smoothing to create the final VAMS line, reducing false signals while preserving sensitivity to meaningful momentum changes.

The visualization includes dynamically calculated standard deviation bands that adjust to recent VAMS behavior, creating statistical reference zones. The information table provides real-time numerical values for VAMS Z-Score, underlying momentum percentages, and current volatility readings with trend indicators.

🟢 How to Use

1. VAMS Z-Score Bands and Signal Interpretation

Above Mean Line: Momentum exceeds historical averages adjusted for volatility, indicating bullish conditions suitable for trend following

Below Mean Line: Momentum falls below statistical norms, suggesting bearish conditions or downward pressure

Mean Line Crossovers: Primary transition signals between bullish and bearish momentum regimes

1 Standard Deviation Breaks: Strong momentum conditions indicating statistically significant directional moves worth following

2 Standard Deviation Extremes: Rare momentum readings that often signal either powerful breakouts or exhaustion points

2. Information Table and Market Context

Z-Score Values: Current VAMS reading displayed in standard deviations (σ), showing how far momentum deviates from its statistical norm

Momentum Percentage: Underlying annualized momentum displayed as percentage return, quantifying the directional strength

Volatility Context: Current annualized volatility levels help interpret whether VAMS readings occur in high or low volatility environments

Trend Indicators: Directional arrows and change values provide immediate feedback on momentum shifts and market transitions

3. Strategy Applications and Alert System

Trend Following: Use sustained readings beyond the mean line and 1σ band penetrations for directional trades, especially when VAMS maintains position in upper or lower statistical zones

Mean Reversion: Focus on 2σ extreme readings for contrarian opportunities, particularly effective in sideways markets where momentum tends to revert to statistical norms

Alert Notifications: Built-in alerts for mean crossovers (regime changes), 1σ breaks (strong signals), and 2σ touches (extreme conditions) help monitor multiple instruments for both continuation and reversal setups

Volatility Breaker Blocks [BigBeluga]The Volatility Breaker Blocks indicator identifies key market levels based on significant volatility at pivot highs and lows. It plots blocks that act as potential support and resistance zones, marked in green (support) and blue (resistance). Even after a breakout, these blocks leave behind shadow boxes that continue to impact price action. The sensitivity of block detection can be adjusted in the settings, allowing traders to customize the identification of volatility breakouts. The blocks print triangle labels (up or down) after breakouts, indicating potential areas of interest.

🔵 IDEA

The Volatility Breaker Blocks indicator is designed to highlight key areas in the market where volatility has created significant price action. These blocks, created at pivot highs and lows with increased volatility, act as potential support and resistance levels.

The idea is that even after price breaks through these blocks, the remaining shadow boxes continue to influence price movements. By focusing on volatility-driven pivot points, traders can better anticipate how price may react when it revisits these areas. The indicator also captures the natural tendency for price to retest broken resistance or support levels.

🔵 KEY FEATURES & USAGE

◉ High Volatility Breaker Blocks:

The indicator identifies areas of high volatility at pivot highs and lows, plotting blocks that represent these zones. Green blocks represent support zones (identified at pivot lows), while blue blocks represent resistance zones (identified at pivot highs).

Support:

Resistance:

◉ Shadow Blocks after Breakouts:

When price breaks through a block, the block doesn't disappear. Instead, it leaves behind a shadow box, which can still influence future price action. These shadow blocks act as secondary support or resistance levels.

If the price crosses these shadow blocks, the block stops extending, and the right edge of the box is fixed at the point where the price crosses it. This feature helps traders monitor important price levels even after the initial breakout has occurred.

◉ Triangle Labels for Breakouts:

After the price breaks through a volatility block, the indicator prints triangle labels (up or down) at the breakout points.

◉ Support and Resistance Retests:

One of the key concepts in this indicator is the retesting of broken blocks. After breaking a resistance block, price often returns to the shadow box, which then acts as support. Similarly, after breaking a support block, price tends to return to the shadow box, which becomes a resistance level. This concept of price retesting and bouncing off these levels is essential for understanding how the indicator can be used to identify potential entries and exits.

The natural tendency of price to retest broken resistance or support levels.

Additionaly indicator can display retest signals of broken support or resistance

◉ Customizable Sensitivity:

The sensitivity of volatility detection can be adjusted in the settings. A higher sensitivity captures fewer but more significant breakouts, while a lower sensitivity captures more frequent volatility breakouts. This flexibility allows traders to adapt the indicator to different trading styles and market conditions.

🔵 CUSTOMIZATION

Calculation Window: Defines the window of bars over which the breaker blocks are calculated. A larger window will capture longer-term levels, while a smaller window focuses on more recent volatility areas.

Volatility Sensitivity: Adjusts the threshold for volatility detection. Lower sensitivity captures smaller breakouts, while higher sensitivity focuses on larger, more significant moves.

Retest Signals: Display or hide retest signals of shadow boxes

Volatility Estimator - YZ & RSThe Yang-Zheng Volatility Estimator (YZVE) integrates both intra-candle and inter-candle dynamics, such as overnight and weekend price changes, offering a more detailed analysis compared to traditional methods. The YZVE is proposed to improve over the standard deviation by accounting for the open, high, low, and close prices of trading periods, instead of only the close prices, and attempts to supplant the Parkinson's Volatility Estimator (PVE) by a also capturing inter-candle dynamics. The YZVE is calculated by this formula:

YZ Volatility Squared σ_YZ² = k * σ_o² + σ_rs² + (1 - k) * σ_c²

where k is a weighting factor that adjusts the emphasis between the overnight and close-to-close components, popularly estimated as:

k = 0.34 / (1.34 + (N+1) / (N-1))

where N is the lookback period. Optionally, users may opt to override this calculation with a specified constant (off by default). Next, the

Overnight Volatility Squared σ_o² = (log(O_t / C_(t-1)))²

measures the volatility associated with overnight price changes, from the previous candle's closing price C_(t-1) to the current candle's opening price O_t. It captures the market's reaction to news and events that occur outside of regular trading hours to reflect risk associated with holding positions over non-trading hours and gaps.

Next, the The Rogers-Satchell Volatility Estimator (RSVE) serves as an intermediary step in the computation of YZVE. It aggregates the logarithmic ratios between high, low, open, and close prices within each trading period, focusing on intra-candle volatility without assuming zero inter-candle drift as commonly implicitly assumed in other volatility models:

Rogers-Satchell Volatility Squared σ_rs² = (log(H_t / C_t) * log(H_t / O_t)) + (log(L_t / C_t) * log(L_t / O_t))

Finally,

Close-to-Close Volatility Squared σ_c² = (log(C_t / C_(t-1)))²

measures the volatility from the close of one candle to the close of the next. It reflects the typical candle volatility, similar to naive standard deviation.

This script also includes an option for users to apply the simpler RS Volatility exclusively, focusing on intraday price movements. Additionally, it offers a choice for normalization between 0 and 1, turning the estimator into an oscillator for comparing current volatility to recent levels. Horizontal lines at user-defined levels are also available for clearer visualization. Both are off by default.

References:

Yang, D., & Zhang, Q. (2000). Drift-independent volatility estimation based on high, low, open, and close prices. The Journal of Business, 73(3), 477-491.

Rogers, L.C.G., & Satchell, S.E. (1991). Estimating variance from high, low and closing prices. Annals of Applied Probability, 1(4), 504-512.

Gamma & Volatility Levels [Pro]General Purpose

This indicator analyzes volatility levels and expected price movements, combining gamma concepts (financial options) with volatility analysis to identify support and resistance zones.

Main Components

High Volatility Level (HVL): Calculates a volatility level based on the simple moving average (SMA) of the price plus one standard deviation. This level is represented by an orange line showing where volatility is concentrated.

Expected Movement (Movimiento Esperante): Uses the Average True Range (ATR) multiplied by an adjustable factor to project potential upward and downward movement ranges from the current price. It is drawn in green (upward) and red (downward).

Gamma Levels (Nivelas Gamma): Identifies two key levels: the call resistance (highest high of the last 50 periods) in blue, and the put support (lowest low) in purple. These are based on recent extreme prices.

Additional Information: The indicator calculates the percentage distance between the current price and the HVL, displaying it in a label.

Visual Elements

Colored lines on the chart for each level.

Labels with exact values next to each line.

A table in the upper right corner summarizing all calculated values.

Options to show or hide each element according to preference.

This is a useful tool for traders who work with options or seek to identify levels of extreme volatility and dynamic support/resistance zones.

Low Volatility Breakout + TP/SL Levels█ OVERVIEW

"Low Volatility Breakout + TP/SL Levels" is a breakout indicator designed to detect and trade breakouts from periods of low volatility (consolidation). Unlike classic strategies based on fixed support/resistance levels, this indicator dynamically identifies consolidations characterized by small candle bodies and only generates a signal when the breakout occurs with a large, decisive candle. It also automatically plots 3 Take Profit levels and a Stop Loss (with two calculation modes), making it a complete breakout trading tool.

█ CONCEPTS

The strongest market moves most often start after a prolonged period of very low volatility — when candles become small and the market "falls asleep". The indicator first detects such consolidations (small bodies for at least X bars), draws a box around them, and then waits for a breakout with a candle significantly larger than the average. Additional filters (e.g., the box height cannot exceed the average candle body by too much) eliminate false consolidations and volatility traps. Immediately after the breakout, TP1, TP2, TP3, and SL levels are plotted.

█ FEATURES

Dynamic detection of low-volatility consolidations

- candles with small bodies (< average body × consolidationMultiplier)

- minimum number of bars in consolidation: confirmBars (default 5)

Automatic drawing of consolidation boxes

- green (bullish) or red (bearish) with transparent background (85)

- adjustable border thickness (border_width 1–5)

- box height filter (boxHeightMultiplier, default 6.0 × average body) – removes overly stretched/false consolidations

Breakout conditions

- current candle must be larger than average body × threshold (default 1.5)

- must be the largest candle in the entire consolidation

- must close above the highest high (long) or below the lowest low (short)

Breakout signals

- small green triangles below the bar (long)

- small red triangles above the bar (short)

Automatic Take Profit and Stop Loss levels (drawn 5 bars forward)

- two calculation modes:

• Candle Multiplier – based on average true range (high-low) over tp_sl_length period

• Percentage – fixed percentage from breakout close price (percentages must be manually adjusted to the asset and timeframe)

- 3 TP levels (default 2×, 3×, 4× or 2%, 3%, 4%)

- 1 SL level (default 2× or 1.5%)

Live TP/SL price table (top-right corner)

- displays exact current values of SL, TP1, TP2, TP3 immediately after each new signal

- colors identical to drawn lines (red background for SL, green for TP levels)

- updates automatically with every new breakout

Built-in alerts

- “Bullish Breakout Alert” and “Bearish Breakout Alert”

█ HOW TO USE

Add the indicator to your TradingView chart → Indicators → search “Low Volatility Breakout + TP/SL Levels”.

After each valid breakout you will immediately see:

- the colored box

- signal triangle

- horizontal TP/SL lines

- updated table in the top-right corner showing precise price levels for the current trade

Key settings to adjust:

Consolidation Settings

- Volatility Window (length) – period for average body calculation (default 20)

- Consolidation Multiplier – how small bodies must be to count as consolidation (default 2.0)

- Breakout Multiplier – minimum size of breakout candle (default 1.5)

- Box Height Multiplier – maximum allowed box height (default 6.0)

- Min Consolidation Bars – minimum bars required (default 5)

Risk Management Settings

- Choose TP/SL mode: Candle Multiplier or Percentage

- Adjust TP1–3 and SL multipliers/percentages to match your risk management style

Signal interpretation:

- Green triangle below bar + green box + green TP levels in table = long signal

- Red triangle above bar + red box + red SL level in table = short signal

- Boxes remain on chart until broken — they highlight accumulation/distribution zones

█ APPLICATIONS

- Trading breakouts from consolidation on all markets and timeframes

- Recommended to trade in the direction of the higher-timeframe trend or with additional confirmations (e.g., key level breaks). Aggressive mode (trading both directions) is also possible — provided box and TP/SL settings are properly optimized

- Experiment with different TP/SL ratios — higher reward-to-risk setups (e.g., SL 1×, TP3 6–8×) with lower win rate are often more profitable in the long run

- Strongly encourage testing various box parameters (consolidationMultiplier, boxHeightMultiplier, confirmBars) — small changes can dramatically affect signal frequency and quality

█ NOTES

Always test and optimize parameters for the specific instrument and timeframe.

Volatility Signal-to-Noise Ratio🙏🏻 this is VSNR: the most effective and simple volatility regime detector & automatic volatility threshold scaler that somehow no1 ever talks about.

This is simply an inverse of the coefficient of variation of absolute returns, but properly constructed taking into account temporal information, and made online via recursive math with algocomplexity O(1) both in expanding and moving windows modes.

How do the available alternatives differ (while some’re just worse)?

Mainstream quant stat tests like Durbin-Watson, Dickey-Fuller etc: default implementations are ALL not time aware. They measure different kinds of regime, which is less (if at all) relevant for actual trading context. Mix of different math, high algocomplexity.

The closest one is MMI by financialhacker, but his approach is also not time aware, and has a higher algocomplexity anyways. Best alternative to mine, but pls modify it to use a time-weighted median.

Fractal dimension & its derivatives by John Ehlers: again not time aware, very low info gain, relies on bar sizes (high and lows), which don’t always exist unlike changes between datapoints. But it’s a geometric tool in essence, so this is fundamental. Let it watch your back if you already use it.

Hurst exponent: much higher algocomplexity, mix of parametric and non-parametric math inside. An invention, not a math entity. Again, not time aware. Also measures different kinds of regime.

How to set it up:

Given my other tools, I choose length so that it will match the amount of data that your trading method or study uses multiplied by ~ 4-5. E.g if you use some kind of bands to trade volatility and you calculate them over moving window 64, put VSNR on 256.

However it depends mathematically on many things, so for your methods you may instead need multipliers of 1 or ~ 16.

Additionally if you wanna use all data to estimate SNR, put 0 into length input.

How to use for regime detection:

First we define:

MR bias: mean reversion bias meaning volatility shorts would work better, fading levels would work better

Momo bias: momentum bias meaning volatility longs would work better, trading breakouts of levels would work better.

The study plots 3 horizontal thresholds for VSNR, just check its location:

Above upper level: significant Momo bias

Above 1 : Momo bias

Below 1 : MR bias

Below lower level: significant MR bias

Take a look at the screenshots, 2 completely different volatility regimes are spotted by VSNR, while an ADF does not show different regime:

^^ CBOT:ZN1!

^^ INDEX:BTCUSD

How to use as automatic volatility threshold scaler

Copy the code from the script, and use VSNR as a multiplier for your volatility threshold.

E.g you use a regression channel and fade/push upper and lower thresholds which are RMSEs multiples. Inside the code, multiply RMSE by VSNR, now you’re adaptive.

^^ The same logic as when MM bots widen spreads with vola goes wild.

How it works:

Returns follow Laplace distro -> logically abs returns follow exponential distro , cuz laplace = double exponential.

Exponential distro has a natural coefficient of variation = 1 -> signal to noise ratio defined as mean/stdev = 1 as well. The same can be said for Student t distro with parameter v = 4. So 1 is our main threshold.

We can add additional thresholds by discovering SNRs of Student t with v = 3 and v = 5 (+- 1 from baseline v = 4). These have lighter & heavier tails each favoring mean reversion or momentum more. I computed the SNR values you see in the code with mpmath python module, with precision 256 decimals, so you can trust it I put it on my momma.

Then I use exponential smoothing with properly defined alphas (one matches cumulative WMA and another minimizes error with WMA in moving window mode) to estimate SNR of abs returns.

…

Lightweight huh?

∞

Volatility Projection Levels (VPL)### Indicator Name: **Volatility Projection Levels (VPL)**

### Description:

The **Volatility Projection Levels (VPL)** indicator is a powerful tool designed to help traders anticipate key support and resistance levels for the E-mini S&P 500 (ES) by leveraging the CBOE Volatility Index (^VIX). This indicator utilizes historical volatility data to project potential price movements for the upcoming month, offering clear visual cues that enhance swing trading strategies.

### Key Features:

- **Volatility-Based Projections**: The VPL indicator uses the previous month’s closing value of the VIX, normalizing it for monthly analysis by dividing by the square root of 12. This calculated percentage is then applied to the E-mini S&P 500’s closing price from the last day of the previous month.

- **Upper and Lower Projection Levels**: The indicator calculates two essential levels:

- **Upper Projection Level**: The previous month’s closing price of the E-mini S&P 500 plus the calculated volatility percentage.

- **Lower Projection Level**: The previous month’s closing price of the E-mini S&P 500 minus the calculated volatility percentage.

- **Continuous Visualization**: The VPL indicator plots these projection levels on the chart throughout the entire month, providing traders with a consistent reference for potential support and resistance zones. This continuous visualization allows for better anticipation of market movements.

- **Previous Month's Close Reference**: Additionally, the indicator plots the previous month’s closing price as a reference point, offering further context for current price action.

### Use Cases:

- **Swing Trading**: The VPL indicator is ideal for swing traders looking to exploit predicted price ranges within a monthly timeframe.

- **Support & Resistance Identification**: It aids traders in identifying critical levels where the market may encounter support or resistance, thus informing entry and exit decisions.

- **Risk Management**: By forecasting potential price levels, traders can set more strategic stop-loss and take-profit levels, enhancing risk management.

### Summary:

The **Volatility Projection Levels (VPL)** indicator equips traders with a forward-looking tool that incorporates volatility data into market analysis. By projecting key price levels based on historical VIX data, the VPL indicator enhances decision-making, helping traders anticipate market movements and optimize their trading strategies.

Made by Serpenttrading

L&S Volatility IndexOverview

L&S Volatility Index is a tool designed to helps traders identify overpriced or underpriced moments in the market and adjust their trading strategies accordingly.

Calculations

This tool calculates how far the price is from the 21-period simple moving average as a ratio of the average historical volatility calculated over the last 21 candles.

How It Works

A L&S Volatility Index with a value greater than 30% may indicate that the asset is overpriced or underpriced relative to its average price.

How To Use

If the L&S Volatility Index > 30, the asset is overpriced or underpriced. This means that there is a good probability of initiating a mean reversion.

If the L&S Volatility Index < 30, the asset is in a fair price region. This means that it is acceptable to buy or sell in that price region.

Where To Use

Mean Reversion Strategy

Breakout Strategy

What Makes it Original

There is already an indicator that use a normalized calculation and a different approach to calculate historical volatility, whereas this script calculation is non-normalized and historical volatility is calculated using Don Fishback's formula. All calculations are used as originally described.

Credits

The L&S Volatility Index indicator was originally written by L&S Educação Financeira.

Historical Volatility calculation is based on the book "Odds: The Key to 90% Winners" written by Don Fishback.

Volatility Percentile (H-LINES)A simple script that adjusts the Volatility Percentile Indicator visibly in order to better accommodate entries/exits and certain trading setups/strategies.

--------------------------------------------------------------------------------------------------------------------------------------------------------

TL;DR - Remember after a full reset, we are looking for initial crosses UP on the UpperSwingline and crosses DOWN on the LowerSwingline for primary and secondary signal derivation.

Vice versa also works great but the prior method mentioned is a little more consistent in my experience, but you should mess around and optimise this for your own setups and strategies anyway.

--------------------------------------------------------------------------------------------------------------------------------------------------------

ORIGINAL SCRIPT HERE:

^Click image for a redirect to that script.

ALL CREDIT GOES TO: www.tradingview.com

He wrote everything so give credit where it's due, good bit of kit this here script is.

--------------------------------------------------------------------------------------------------------------------------------------------------------

HOW I USE MY VISUALLY ALTERED VERSION OF THIS SCRIPT

First of all, the alterations I've made seem only to be consistently viable with renko charts though if you can get the sought after results using candles or any other chart type then perfect, but be wary. All my back-testing done only with LinReg, HMA and SWMA - ATR type settings exclusively on renko charts. The changes I've made to the original script essentially just turns it visibly into an oscillator and uses a couple horizontal lines to generate signals, very simple - absolutely nothing has changed in the actual code of calculating this indicator.

What I believe my adjustments have achieved is quite simple. A full reset/oscillation on the indicator tries to map the strongest parts of a move or at least the part of the move where volume and the rate of transactions is at its peak to even facilitate said move. *take this statement with a pinch of salt though I do believe it's interacting with accumulation/distribution patterns, which is expected of volatility*

For ease of communication let's refer to the area between the the first UpperSwingline cross to the subsequent LowerSwingline cross, as the primary move. Then afterwards when it crosses the UpperSwingline again to make the full reset, the area in between those two points referred to as the secondary move.

Though more interestingly/practically the indicator ends up giving you two signals. In order for this to work we have to first decide that a spike up in volatility which crosses the UpperSwingline implies a significant level of interest at that price level. Usually that means a reversal is brewing, if price has already moved, trended and is approaching a certain area of value; which causes a spike of new positions to be taken, then you know that this is a level where contrarians are looking to enter. Now here's the tricky part, when volatility crosses the LowerSwingline price action becomes a little more open for interpretation, the way I personally like to look at this secondary signal is the potential for an exhaustion period to prolong itself a little longer. I know that's not the perfect analysis for what's going on, a more in-depth look into what's going on would best be described using Elliott Wave Theory, if a cross on the UpperSwingline near a significant area of value gives us a reversal trade lets just assume for the sake of argument that a new Elliott Wave can begin forming here. Making the move from that initial UpperSwngline cross to the cross on the LowerSwingline, the area that encompasses those two points: the impulse wave. After this point my analogy kind of falls apart and sadly my knowledge just isn't what it needs to be in order for me to properly analyse what's going on here but I must digress. Price after crossing the LowerSwingline up until the point where it makes a full reset by crossing the UpperSwingline again, within this area price seems to do either one of two things:

Situation 1 - Most likely occurs after a major trend reversal from major support/resistance or area of value (price has trended to new territory, maybe spent time a little time consolidating but hasn't broken the key level, momentum shifts, price action breaks current structure and you get the signal that primary move is a reversal) = Exhaustion Period, price will continue in direction of primary move during the secondary move. This here is for our trend-followers, you wanna take a continuation trade? Just wait for the pullback/rally to hit a FiB retracement level and enter - or any other means to find a decent support/resistance to enter.

Situation 2 - Most likely occurs when market enters a range or consolidation (price was previously seen as being at either a discount or premium so Situation 1 could have already played out and now you're looking at a full reset after that, imagine this spot to be the centre line of a linear regression channel or bang in the middle of your range, could even occur if price breaks a key moving average and decides it ought to consolidate around it for a while. Basically at any point where a somewhat prolonged consolidation is expected and not a quick reversal) = Corrective Wave, price will move against the direction of primary move during the secondary move. Now you might be expecting me to say this ones for you reversal traders but not really, if this is occurring then there probably isn't a definitive direction the market has chosen so you can use this opportunity to take range trades in the direction or against the direction of whatever the current trend or latest trend was depending on whatever slight bias you may have. <--- Situation 2 is very useful for finding cleaner entries if you do have a trend bias, say price underwent Situation 1, is now at key moving average but your bias is that it will break and continue up, so you wait and allow the secondary move of Situation 2 to take your entry to a much better R:R before entering a position.

--------------------------------------------------------------------------------------------------------------------------------------------------------

Volatility Weighted Moving AverageVolatility Weighted Moving Average (VAWMA) :

The Volatility Weighted Moving Average is a short and long term trend filter that weightes asset price buy "volatility significance" (percentages of total volatility over specified period) unlike that of the WMA which formulates an average based on the product of asset price and a deceding period significance . The result is a less noisy average which weights price based on its potential significance in trend, VAWMA tends to price when volatility is high and conversaly tends away from price when volatility is low.

Example :

As seen above the VAWMA tends to price more than both the SMA and EMA. The high volatility weightings allow for the VWMA to act as a potential trailing stop.

Dynamics :

- symbol volatility watchlist, change the ticker and corrosponding exchange to watch volatility over other markets.

Full Volatility Statistics and Forecast

This is a tool designed to translate the data from the expected volatility of different assets, such as for example VIX, which measures the volatility of SP500 index.

Once get the data from the volatility asset we want to measure(for this test I have used VIX), we are going to translate it the required timeframe expected move by dividing the initial value into :

252 = if we want to use the daily timeframe, since there are ~252 aproximative daily trading days

52 = if we want to use the weekly timeframe, since there 52 trading weeks in a year

12 = if we want to use the monthly timeframe, since there are 12 months in a year

For this example I have used 252 with the daily timeframe.

In this scenario, we can see that we had 5711 total cnadles which we analysed, and in this case, we had 942 crosses, where the daily movement ended up either above or below the channel made from the opening daily candle value + expected movement from the volatility, giving as a total of 16.5% of occurances that volatility was higher than expected, and in 83.5% of the times, we can see that the price stayed within our channel.

At the same time, we can see that we had 6 max losses in a row ( OUT) AND 95 max wins in a row (IN), and at the same time in those moments when the volatility crosses happen we had a 0.51% avg movements when the top crossed happened, and 0.67% avg movements when the bot happened.

Lastly on the second part of the panel, we had E which means the expected movement of today, for example it has 61.056$ , so lets say price opened on 4083, our top is 4083 + 61 and our bot is 4083 - 61 ( giving us the daily channel). At continuation we can see that overall the avg bull candle os 0.714% and avg bear candle was 0.805% .

I hope this tool will help you with your future analysis and trades !

If you have any questions please let me know !

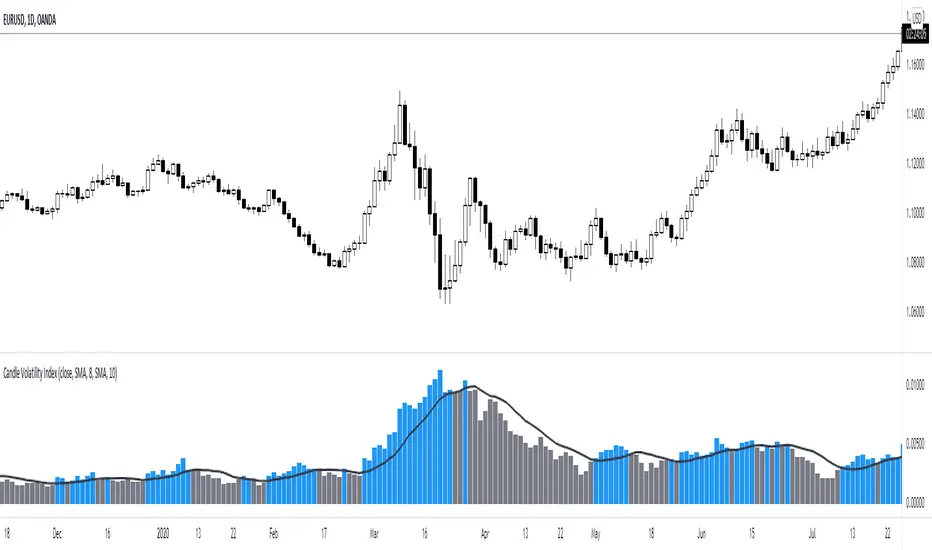

Candle Volatility Index [by NicoadW]This is the migration of the CandleVolatilitIndex from MT4.

The indicator works as following:

Step 1: The "Volatility Value" is calculated by applying a moving average to the change of the selected source (default: 10-Period-SMA applied to the change from last close to this close -> SMA(close-close , 10) )

Step 2: The signal line is calculated by applying a moving average onto the "Volatility Value" calculated in step 1.

The default settings are the same as in the original MT4 version.

Visualization:

The histogram shows the "Volatility Value" calculated in step 1.

Case 1:

The value is above the signal line (blue bar) -> Volatility is given

Case 2:

The value is below the signal line (grey bar) -> Volatility is not there

This is intended to be used as a Volume/Volatility Indicator for a NNFX-System but can be used in any strategy.

BTC Volatility Band StrategyThis script/strategy is a pullback system designed for securities with high volatility so naturally Bitcoin is an excellent choice for trading this. This could be used both on a daily chart or on lower timeframes (I found good results on 3hr timeframe but haven't tested it on anything under 1hr).

A volatility band is created by comparing the candle close price of the previous 2 candles and and it uses this change in price to create a moving average. A band is wrapped around the moving average with a standard deviation of 1 for the inner band and 2 for the outer band. If the price is above a pre-set MA (moving average filter) then it is determined we are in an uptrend so the strategy will issue a buy signal when we are in an uptrend and there is a pullback which causes the lower inner deviation band to be spiked, but if the price continues and falls through the outer deviation band then a buy signal will not issue as this detriments that the volatility spike is to great. You can see a spike "buy" event occur on the indicator where the background is coloured green. For a short/sell then there will be a spike on the upper inner band and we are below the pre-set MA filter, for this it shows with red background on the indicator.

The user can change the date range they wish to test, the moving average period for the volatility tracking and the inner and outer band deviations. On BTC I left the inner deviation and outer deviation bands on standard settings but found the 3 period volatility tracking to be good for trading 1 day chart and the 5 period volatility tracking good for the 3hr chart. Since this is not a buy and hold strategy then for trading you would probably want to stick with the most liquid coins so you can get in and out very fast on any exchange. If you wanted to tray this on less volatile markets then changing the inner deviation band to ~0.75 would work okay in various futures markets likely stocks as well. The take profit and stop loss levels are based on a multiple of the trading range looking back the past 7 candles.

Attached result is trading 1 BTCUSDT contract on Binance.

The Amplifier - Two Day Historical Bitcoin Volatility PlotThe 3rd piece to the other two pieces to our CoT study. This is the Amplifier, which turns select signals into 'Super' Buys/Sells

The other two being the 'Bitcoin Insider CoT Delta', and the on chart Price indicator most will have, if no others the 'Hunt Bitcoin CoT Buy/Sell Signals' that will indicate the key signals, ave 4 a year on the chart as they occur.

Why Bother another CoT signal?

Its different & focused on the Insider's.

Performance -

This Indicator provided a

1. Signal 1 = 26th March 2019 = SUPER LONG at $4,500 that saw a near $14,000 run up

2. Signal 2 = 18th & 24th June 2019 = SHORT at the second & final level $11,700 after repeated attempts & failure in the $13K range, the mini Echo Bitcoin Bull of 2019

3. Signal 3 = 17th December 2019 = LONG $6,900, Bitcoin rallied to Mid $10,500's

4. Signal 4 = 18th Feb 2020 = SUPER SHORT from $9,700's to a final extreme Low of $3,000, calling the CV-19 collapse

5. Signal 5 = 17th March 2020 = LONG from $5,400 no closure point yet

6. Signal 6 = 29th June 2020 = SUPER LONG reiterate from $10,700 no closure sell signal yet

7. Signal 7 = 17th May 2020 = LONG another accumulate LONG with no sell signal yet generated at Post H&S's low of $33,000

Note - This indicator only commences March 2019, as Bitcoin futures were a recent introduction and needed to settle for 6 months in both use and data, no signals were meaningful prior & data was light.

What is Provided. - Please note the need to also add the Hunt Bitcoin Historical Volatility Indicator for full understanding.

We provide 3 things with the 3 indicators.

'Insider' indications from Largest players in the futures market.

1. Bitcoin Macro Buy Signals.

a) The Bitcoin Commitment of Traders results see us focus solely on Largest 4 Short Open Interest & Largest 4 Long Open Interest aspects of the CoT Release data.

When the difference - is tight, a kind of pinch, these have been great Buy signals in Bitcoin.

We call this difference the Delta & When Delta is 5% or less Bitcoin is a Buy.

2. Bitcoin Macro Sells.

a) A sell signal is Triggered in Bitcoin at any point the Largest 4 short OI > or = to 70

3. AMPLIFIER Trade signals 'Super' Longs or Shorts -

Extreme low volatility events leads to highly impulsive & volatile subsequent moves, if either of 1 or 2 above occur, combined with extreme low volatility

a 'Super Long' or 'SUPER SELL' is generated. In the case of the short side, given Bitcoins general expansive and MACRO Bull trend since inception, we seek an additional component

that is an extreme differential/Delta reading between 4 biggest Longs & Shorts OI.

Namely CoT Delta also must be > 47.5%

We also have a Cautionary level, where it is not necessarily a good idea to accumulate Bitcon, as a better opportunity lower may avail itself, see conditions below.

So the required logic explicitly stated below for all Signals.

1. Long - Hunt Bitcoin CoT Delta < or = 5

2. SUPER Long - Hunt Bitcoin CoT Delta < or = 5; and 2 Day Historical Bitcoin Volatility = or < 20

3. Short - Largest 4 Sellers OI = or > 70

4. SUPER Short - Largest 4 Sellers OI = or > 70; AND..

Hunt Bitcoin CoT Delta = or > 47.5 AND 2 Day Historical BTC Volatility = or < 20

5. Caution - Largest 4 Sellers OI = or > 67.5 AND Hunt Bitcoin CoT Delta = or > 45

WARNING SEE Notes Below

Note 1 - = Largest 4 Open Interest Shorts

Note 2 - = Largest 4 Open Interest Longs

Note 3 - = Hunt Cot Delta = (Largest 4 sellers OI) -( Largest 4 Buyers OI)

Caution = Avoid new Bitcoin Accumulation Right Now, A sell signal might follow Enter on next Long

Note 4 - The Hunt Bitcoin COT Delta signal is a Largest 'Insider' Tracking tool based on a segment of Commitment of Traders data on Bitcoin Futures, released once a week on a Friday.

It is a Macro Timeframe signal , and should not be used for Day trading and Short Timeframe analysis , Entries may be optimised after a Hunt Bitcoin CoT Signal is generated by separate shorter Timeframe analysis.

Note 5 - The Historical Bitcoin Volatility is an additional 'Amplifier' component to the 'Hunt Bitcoin Cot Delta' Insider Signal

Note 6 - The Historical Bitcoin Volatility criteria varies by timeframe, the above levels are those applying on a Two Day TF Chart, select this custom timeframe in Trading View.

if additional criteria are met for LONG & SHORT insider signals, they may become 'Super Longs/Shorts', see conditions box above.

Daily Historical Volatility StdDev LevelsDescription:

This indicator plots Daily Standard deviation levels on price chart based on Historical Volatility (HV). It uses the most common approach for calculating historical volatility as standard deviation of logarithmic returns, based on daily closing/settlement prices.

Assets: Currency Pairs, Commodities, also works on stocks, some indices.

Time Frames: 5min to 60min. This will also work on Daily Chart, by setting "DaystoExpire" to 21

Options:

Use Daily Data to Calculate StdDev HV (default), otherwise use the charts Time Frame

Lookback = number of days/periods to calculate stddev of HV (21 by default)

Annual = number of trading days in a calender year (252 by default)

Days to Expiry = number of days for the life of this option ( for auto calculation

this is 1 for intraday, 21 for daily and annual when chart TF used)

Settlement Source = close price by default, can use another source.

Settlement Volume Weighted Average Length = by setting this to >1 then an average

is used for settlement.

Display ### Standard Deviation Levels = select what levels are to be displayed.

References:

How To Use Standard Deviation In Your Trading Day: www.youtube.com

Deviation Levels Indicator: www.youtube.com

www.macroption.com

Historical Volatility based Standard Deviation_V2 by ucsgears

Historical Volatility Strategy by Hpotter

Volatility Switch Indicator [LazyBear]The Volatility Switch (VOLSWITCH) indicator, by Ron McEwan, estimates current volatility in respect to historical data, thus indicating whether the market is trending or in mean reversion mode. Range is normalized to 0 - 1.

When Volatility Switch rises above the 0.5 level, volatility in the market is increasing, thus the price action can be expected to become choppier with abrupt moves. When the indicator falls below the 0.5 level from recent high readings, volatility decreases, which may be considered a sign of trend formation.

Trading strategy as suggested by Ron McEwan is:

- If VOLSWITCH is less than 0.5, volatility decreases, which may be considered a sign of trend formation

- If VOLSWITCH is greater than 0.5, market is in high volatility mode. Can be choppy. Use RSI to look for OB/OS levels.

I have implemented support for 2 lengths (14 and 21) Note that, Pine doesn't support loops. Once it is introduced, I will publish an updated version.

Building a strategy out of this is straightforward (refer to my strategy explanation above), I strongly encourage new Pinescript coders to try to a plotarrow() based overlay indicator to get more familiar with Pine.

More info:

---------

The Volatility (Regime) Switch Indicator : traders.com

Complete list of my indicators:

-------------------------------------

docs.google.com

Volatility BandsThe Volatility Bands script is a custom indicator designed to help traders visualize volatility levels in the market. It calculates dynamic bands around a central moving average, providing insights into potential support and resistance levels based on recent price action.

The script calculates multiple volatility bands (u0, u1, u2, d0, d1, d2) that adjust based on recent price movements. The outer bands (u2 and d2) represent extreme volatility levels, while the inner bands (u0, u1, d0, d1) indicate more immediate support and resistance.

Look for price reactions at the band levels. A touch of the upper bands may indicate overbought conditions, while a touch of the lower bands may indicate oversold conditions.

Central Moving Average: A smoothed moving average that adapts to price changes, providing a clear trend direction.

The script has no input parameters.

Script Functions:

erf(x): Calculates the error function for a given input x. Used in the calculation of the smoothing factor for the UMA.

uma(input): Provides a smoothed average that adapts to recent price changes, reducing lag compared to traditional moving averages.

dev(input, mu): Used to calculate the volatility bands around the central moving average.