Compare Crypto Bollinger Bands//This is not financial advice, I am not a financial advisor.

//What are volatility tokens?

//Volatility tokens are ERC-20 tokens that aim to track the implied volatility of crypto markets.

//Volatility tokens get their exposure to an asset’s implied volatility using FTX MOVE contracts.

//There are currently two volatility tokens: BVOL and IBVOL.

//BVOL targets tracking the daily returns of being 1x long the implied volatility of BTC

//IBVOL targets tracking the daily returns of being 1x short the implied volatility of BTC.

/////////////////////////////////////////////////////////////////

CAN USE ON ANY CRYPTO CHART AS BINANCE:BTCUSD is still the most dominant crypto, positive volatility for BTC is positive for all.

/////////////////////////////////////////////////////////////////

//The Code.

//The blue line (ChartLine) is the current chart plotted on in Bollinger

//The red line (BVOLLine) plots the implied volatility of BTC

//The green line (IBVOLLine) plot the inverse implied volatility of BTC

//The orange line (TOTALLine) plots how well the crypto market is performing on the Bolling scale. The higher the number the better.

//There are 2 horizontal lines, 0.40 at the bottom & 0.60 at the top

/////////To Buy

//1. The blue line (ChartLine) must be higher than the green line (IBVOLLine)

//2. The green line (IBVOLLine) must be higher than the red line (BVOLLine)

//3. The red line (BVOLLine) must be less than 0.40 // This also acts as a trendsetter

//4. The orange line (TOTALLine) MUST be greater than the red line. This means that the crypto market is positive.

//5.IF THE BLUE LINE (ChartLine) IS GREATER THAN THE ORANGE LINE (TOTALLine) IT MEANS YOUR CRYPTO IS OUTPERFOMING THE MARKET {good for short term explosive bars}

//6. If the orange line (TOTALLine) is higher than your current chart, say BTCUSD. And BTC is going up to. It just means BTC is going up slowly. it's fine as long as they are moving in the same position.

//5. I use this on the 4hr, 1D, 1W timeframes

///////To Exit

//1.If the blue line (ChartLine) crosses under the green line (IBVOLLine) exit{ works best on 4hr,1D, 1W to avoid fakes}

//2.If the red line crosses over the green line when long. {close positions, or watch positions} It means negative volatility is wining

在腳本中搜尋"Volatility"

Volatility Bands by DGTVolatility represents how large an asset's prices swing around the mean price, the degree of variation of a trading price over time, and is commonly measured with beta (β) coefficients, standard deviations (σ) of returns where tools such as Average True Range, Bollinger Bands, Keltner Channel, Squeeze Indicator, etc presents volatility concept

Volatility often refers to the amount of uncertainty or risk related to the size of changes in a security's value. The higher the volatility, the riskier the security - the price of the security can change dramatically over a short time period in either direction. A lower volatility - security's value does not fluctuate dramatically, and tends to be more steady

This study, Volatility Bands , attempts to present a way to measure and visualize volatility , using standard deviations (σ) and average true range indicator, and aims to point out areas that might indicate potential trading opportunities

I will try to explain the usage with examples,

same setup with different option selected

as you may observe from the examples different setting may have advantages and disadvantages over one another, it is recommended to verify a trading setup with different available options.

Additionally, It is recommended to use this indicator in conjunction with other technical indicators, or verify using chart/candle patterns. Below is an usage example using in conjunction with other indicator, in the given example “Neglected Volume by DGT” is selected

Similarities and Differences

Bollinger Bands depicts two standard deviations above and below a simple moving average, and Keltner Channel depicts two times average true range (ATR) above and below an exponential moving average

Volatility Bands study combines the approach of both Bollinger Bands and Keltner Channel, with different settings and different visualization

Default settings are one standard deviations and one time average true range (ATR) above and below 13 period exponential moving average. Setting can be adjusted by users but let me remind all testes are performed with the default settings.

Mathematically expressed as

Upper band area between “ema + stdev” and “ema + atr”

Lower band area between “ema – stdev” and “ema – atr”

A different display is added with the inspiration I get from one of the @quantgym ‘s study, many thanks @quantgym 😉

When difference band display is selected the study will reflect the area between “ema + stdev – atr” and “ema – stdev + atr”. As shown in the examples above

Note: standard deviation calculation can be adjusted based on price action or its moving average.

Other differentiation between BB and KC is with V-BANDS mostly we look for trade opportunities when price action move out of the bands and in most cases we assume market is consolidating when the price action is within the bands

The other indicator that presents similarities to Volatility Bands is Squeeze Indicator, which measures the relationship between Bollinger Bands and Keltner's Channels to help identify consolidations and signal when prices are likely to break out. Mainly Volatility Bands is different version of Squeeze indicator, in fact the purpose is almost same but visualization is completely different. Additionally Volatility Bands Offers trading opportunities whereas Squeeze indicator only presents market states unless a momentum indicator is adapted to Squeeze indicator.

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

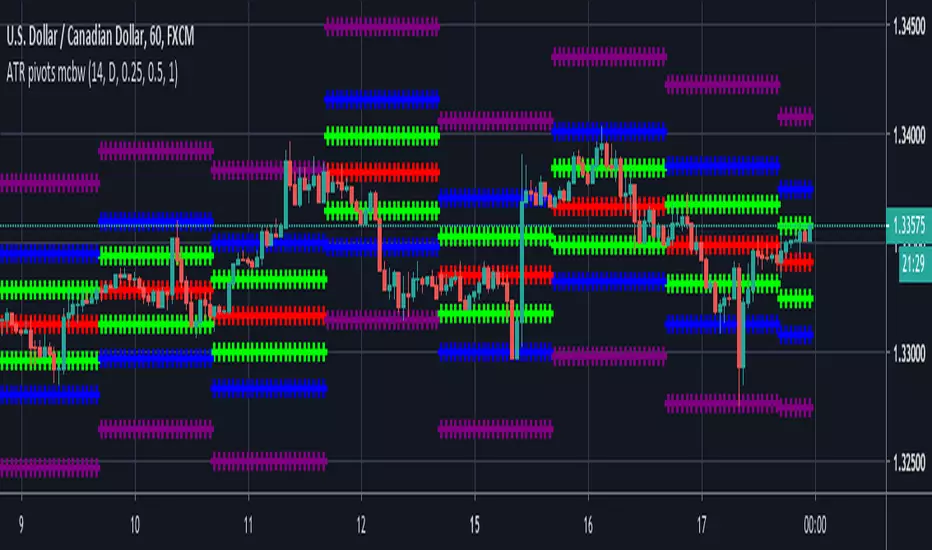

ATR based Pivots mcbwHey everyone this is an exciting new script I have prepared for you.

I was reading an old forex bulletin article some time ago when I came across this: solar.murty.net (or you can download the full bulletin with lots of other good articles here: www.forexfactory.com).

You can already buy this for metatrader (www.mql5.com) so I figured to make it for free for tradingview.

This bulletin suggested that you can reasonably predict daily volatility by adding or subtracting multiples of the daily ATR to the daily opening. Using this you can choose multiples to use as price targets and alternatively as stop losses. For example, if you already have a sense of market direction you can buy at market open place a stop loss at - 1 daily ATR and a profit target at + 3 ATRs for a risk to reward ratio of 3. If you are looking for smaller/quicker moves with a ratio of 3 you can have a stop loss at -0.25 ATR and a take profit at +0.75 ATR.

Alternatively this article also suggests to use this method to catch volatility breakouts. If price is higher than the + 1 ATR area then you can safely assume it will be going to the +2 ATR area so you can put a buy stop at + 1 ATR with a profit target at + 2 ATR with a stop loss at +0.5 ATR to catch a volatility breakout with a risk to reward ratio of 2!

Even further there are methods that you can use with ATRs of multiple window sizes, for example by opening two copies of this indicator and measuring recent volatility with a 1 week window and long term volatility within a 1 month window. If the short term volatility is crossing the long term volatility then there is a high probability chance that even more price movement will occur.

However I have found that this method is good for more than daily volatility , it can also be used to measure weekly volatility , and monthly volatility and use these multiples as good long term price targets.

To select if you want daily, weekly, or monthly values of the ATR of volatility you're using go to the settings and click on the options in the "Opening period". The default window of the ATR here is 14 periods, but you can change this if you want to in "ATR period". Most importantly you are able to select which multiples of the ATR you would like to use in the settings in "ATR multiple 1" which is the green line, "ATR multiple 2" which is the blue line, and "ATR multiple 3" which is the purple line. You can select any values you want to put in these, the choice of 0.25, 0.5, and 1 is not special, some people use fibonacci numbers here or simply 0.33, 0.66, and 0.99.

Repainting issue: This script uses the daily value of the Average True Range (ATR), which measures the volatility that is happening today. If price becomes more volatile then the value of the ATR can increase throughout the day, but it can never decrease. What this means is that the ATR based pivots are able to expand away from the opening price, which should not affect the trades that you take based on these areas. If you base your take profit on one of these ATR multiples and the daily volatility increase this means that your take profit area will be closer to your entry than the ATR multiple. Meaning that your trades will be more conservative.

While this all may sound very technical it is super intuitive, throw this on your chart and play around with it :)

Happy trading!

Adaptive Market Wave TheoryAdaptive Market Wave Theory

🌊 CORE INNOVATION: PROBABILISTIC PHASE DETECTION WITH MULTI-AGENT CONSENSUS

Adaptive Market Wave Theory (AMWT) represents a fundamental paradigm shift in how traders approach market phase identification. Rather than counting waves subjectively or drawing static breakout levels, AMWT treats the market as a hidden state machine —using Hidden Markov Models, multi-agent consensus systems, and reinforcement learning algorithms to quantify what traditional methods leave to interpretation.

The Wave Analysis Problem:

Traditional wave counting methodologies (Elliott Wave, harmonic patterns, ABC corrections) share fatal weaknesses that AMWT directly addresses:

1. Non-Falsifiability : Invalid wave counts can always be "recounted" or "adjusted." If your Wave 3 fails, it becomes "Wave 3 of a larger degree" or "actually Wave C." There's no objective failure condition.

2. Observer Bias : Two expert wave analysts examining the same chart routinely reach different conclusions. This isn't a feature—it's a fundamental methodology flaw.

3. No Confidence Measure : Traditional analysis says "This IS Wave 3." But with what probability? 51%? 95%? The binary nature prevents proper position sizing and risk management.

4. Static Rules : Fixed Fibonacci ratios and wave guidelines cannot adapt to changing market regimes. What worked in 2019 may fail in 2024.

5. No Accountability : Wave methodologies rarely track their own performance. There's no feedback loop to improve.

The AMWT Solution:

AMWT addresses each limitation through rigorous mathematical frameworks borrowed from speech recognition, machine learning, and reinforcement learning:

• Non-Falsifiability → Hard Invalidation : Wave hypotheses die permanently when price violates calculated invalidation levels. No recounting allowed.

• Observer Bias → Multi-Agent Consensus : Three independent analytical agents must agree. Single-methodology bias is eliminated.

• No Confidence → Probabilistic States : Every market state has a calculated probability from Hidden Markov Model inference. "72% probability of impulse state" replaces "This is Wave 3."

• Static Rules → Adaptive Learning : Thompson Sampling multi-armed bandits learn which agents perform best in current conditions. The system adapts in real-time.

• No Accountability → Performance Tracking : Comprehensive statistics track every signal's outcome. The system knows its own performance.

The Core Insight:

"Traditional wave analysis asks 'What count is this?' AMWT asks 'What is the probability we are in an impulsive state, with what confidence, confirmed by how many independent methodologies, and anchored to what liquidity event?'"

🔬 THEORETICAL FOUNDATION: HIDDEN MARKOV MODELS

Why Hidden Markov Models?

Markets exist in hidden states that we cannot directly observe—only their effects on price are visible. When the market is in an "impulse up" state, we see rising prices, expanding volume, and trending indicators. But we don't observe the state itself—we infer it from observables.

This is precisely the problem Hidden Markov Models (HMMs) solve. Originally developed for speech recognition (inferring words from sound waves), HMMs excel at estimating hidden states from noisy observations.

HMM Components:

1. Hidden States (S) : The unobservable market conditions

2. Observations (O) : What we can measure (price, volume, indicators)

3. Transition Matrix (A) : Probability of moving between states

4. Emission Matrix (B) : Probability of observations given each state

5. Initial Distribution (π) : Starting state probabilities

AMWT's Six Market States:

State 0: IMPULSE_UP

• Definition: Strong bullish momentum with high participation

• Observable Signatures: Rising prices, expanding volume, RSI >60, price above upper Bollinger Band, MACD histogram positive and rising

• Typical Duration: 5-20 bars depending on timeframe

• What It Means: Institutional buying pressure, trend acceleration phase

State 1: IMPULSE_DN

• Definition: Strong bearish momentum with high participation

• Observable Signatures: Falling prices, expanding volume, RSI <40, price below lower Bollinger Band, MACD histogram negative and falling

• Typical Duration: 5-20 bars (often shorter than bullish impulses—markets fall faster)

• What It Means: Institutional selling pressure, panic or distribution acceleration

State 2: CORRECTION

• Definition: Counter-trend consolidation with declining momentum

• Observable Signatures: Sideways or mild counter-trend movement, contracting volume, RSI returning toward 50, Bollinger Bands narrowing

• Typical Duration: 8-30 bars

• What It Means: Profit-taking, digestion of prior move, potential accumulation for next leg

State 3: ACCUMULATION

• Definition: Base-building near lows where informed participants absorb supply

• Observable Signatures: Price near recent lows but not making new lows, volume spikes on up bars, RSI showing positive divergence, tight range

• Typical Duration: 15-50 bars

• What It Means: Smart money buying from weak hands, preparing for markup phase

State 4: DISTRIBUTION

• Definition: Top-forming near highs where informed participants distribute holdings

• Observable Signatures: Price near recent highs but struggling to advance, volume spikes on down bars, RSI showing negative divergence, widening range

• Typical Duration: 15-50 bars

• What It Means: Smart money selling to late buyers, preparing for markdown phase

State 5: TRANSITION

• Definition: Regime change period with mixed signals and elevated uncertainty

• Observable Signatures: Conflicting indicators, whipsaw price action, no clear momentum, high volatility without direction

• Typical Duration: 5-15 bars

• What It Means: Market deciding next direction, dangerous for directional trades

The Transition Matrix:

The transition matrix A captures the probability of moving from one state to another. AMWT initializes with empirically-derived values then updates online:

From/To IMP_UP IMP_DN CORR ACCUM DIST TRANS

IMP_UP 0.70 0.02 0.20 0.02 0.04 0.02

IMP_DN 0.02 0.70 0.20 0.04 0.02 0.02

CORR 0.15 0.15 0.50 0.10 0.10 0.00

ACCUM 0.30 0.05 0.15 0.40 0.05 0.05

DIST 0.05 0.30 0.15 0.05 0.40 0.05

TRANS 0.20 0.20 0.20 0.15 0.15 0.10

Key Insights from Transition Probabilities:

• Impulse states are sticky (70% self-transition): Once trending, markets tend to continue

• Corrections can transition to either impulse direction (15% each): The next move after correction is uncertain

• Accumulation strongly favors IMP_UP transition (30%): Base-building leads to rallies

• Distribution strongly favors IMP_DN transition (30%): Topping leads to declines

The Viterbi Algorithm:

Given a sequence of observations, how do we find the most likely state sequence? This is the Viterbi algorithm—dynamic programming to find the optimal path through the state space.

Mathematical Formulation:

δ_t(j) = max_i × B_j(O_t)

Where:

δ_t(j) = probability of most likely path ending in state j at time t

A_ij = transition probability from state i to state j

B_j(O_t) = emission probability of observation O_t given state j

AMWT Implementation:

AMWT runs Viterbi over a rolling window (default 50 bars), computing the most likely state sequence and extracting:

• Current state estimate

• State confidence (probability of current state vs alternatives)

• State sequence for pattern detection

Online Learning (Baum-Welch Adaptation):

Unlike static HMMs, AMWT continuously updates its transition and emission matrices based on observed market behavior:

f_onlineUpdateHMM(prev_state, curr_state, observation, decay) =>

// Update transition matrix

A *= decay

A += (1.0 - decay)

// Renormalize row

// Update emission matrix

B *= decay

B += (1.0 - decay)

// Renormalize row

The decay parameter (default 0.85) controls adaptation speed:

• Higher decay (0.95): Slower adaptation, more stable, better for consistent markets

• Lower decay (0.80): Faster adaptation, more reactive, better for regime changes

Why This Matters for Trading:

Traditional indicators give you a number (RSI = 72). AMWT gives you a probabilistic state assessment :

"There is a 78% probability we are in IMPULSE_UP state, with 15% probability of CORRECTION and 7% distributed among other states. The transition matrix suggests 70% chance of remaining in IMPULSE_UP next bar, 20% chance of transitioning to CORRECTION."

This enables:

• Position sizing by confidence : 90% confidence = full size; 60% confidence = half size

• Risk management by transition probability : High correction probability = tighten stops

• Strategy selection by state : IMPULSE = trend-follow; CORRECTION = wait; ACCUMULATION = scale in

🎰 THE 3-BANDIT CONSENSUS SYSTEM

The Multi-Agent Philosophy:

No single analytical methodology works in all market conditions. Trend-following excels in trending markets but gets chopped in ranges. Mean-reversion excels in ranges but gets crushed in trends. Structure-based analysis works when structure is clear but fails in chaotic markets.

AMWT's solution: employ three independent agents , each analyzing the market from a different perspective, then use Thompson Sampling to learn which agents perform best in current conditions.

Agent 1: TREND AGENT

Philosophy : Markets trend. Follow the trend until it ends.

Analytical Components:

• EMA Alignment: EMA8 > EMA21 > EMA50 (bullish) or inverse (bearish)

• MACD Histogram: Direction and rate of change

• Price Momentum: Close relative to ATR-normalized movement

• VWAP Position: Price above/below volume-weighted average price

Signal Generation:

Strong Bull: EMA aligned bull AND MACD histogram > 0 AND momentum > 0.3 AND close > VWAP

→ Signal: +1 (Long), Confidence: 0.75 + |momentum| × 0.4

Moderate Bull: EMA stack bull AND MACD rising AND momentum > 0.1

→ Signal: +1 (Long), Confidence: 0.65 + |momentum| × 0.3

Strong Bear: EMA aligned bear AND MACD histogram < 0 AND momentum < -0.3 AND close < VWAP

→ Signal: -1 (Short), Confidence: 0.75 + |momentum| × 0.4

Moderate Bear: EMA stack bear AND MACD falling AND momentum < -0.1

→ Signal: -1 (Short), Confidence: 0.65 + |momentum| × 0.3

When Trend Agent Excels:

• Trend days (IB extension >1.5x)

• Post-breakout continuation

• Institutional accumulation/distribution phases

When Trend Agent Fails:

• Range-bound markets (ADX <20)

• Chop zones after volatility spikes

• Reversal days at major levels

Agent 2: REVERSION AGENT

Philosophy: Markets revert to mean. Extreme readings reverse.

Analytical Components:

• Bollinger Band Position: Distance from bands, percent B

• RSI Extremes: Overbought (>70) and oversold (<30)

• Stochastic: %K/%D crossovers at extremes

• Band Squeeze: Bollinger Band width contraction

Signal Generation:

Oversold Bounce: BB %B < 0.20 AND RSI < 35 AND Stochastic < 25

→ Signal: +1 (Long), Confidence: 0.70 + (30 - RSI) × 0.01

Overbought Fade: BB %B > 0.80 AND RSI > 65 AND Stochastic > 75

→ Signal: -1 (Short), Confidence: 0.70 + (RSI - 70) × 0.01

Squeeze Fire Bull: Band squeeze ending AND close > upper band

→ Signal: +1 (Long), Confidence: 0.65

Squeeze Fire Bear: Band squeeze ending AND close < lower band

→ Signal: -1 (Short), Confidence: 0.65

When Reversion Agent Excels:

• Rotation days (price stays within IB)

• Range-bound consolidation

• After extended moves without pullback

When Reversion Agent Fails:

• Strong trend days (RSI can stay overbought for days)

• Breakout moves

• News-driven directional moves

Agent 3: STRUCTURE AGENT

Philosophy: Market structure reveals institutional intent. Follow the smart money.

Analytical Components:

• Break of Structure (BOS): Price breaks prior swing high/low

• Change of Character (CHOCH): First break against prevailing trend

• Higher Highs/Higher Lows: Bullish structure

• Lower Highs/Lower Lows: Bearish structure

• Liquidity Sweeps: Stop runs that reverse

Signal Generation:

BOS Bull: Price breaks above prior swing high with momentum

→ Signal: +1 (Long), Confidence: 0.70 + structure_strength × 0.2

CHOCH Bull: First higher low after downtrend, breaking structure

→ Signal: +1 (Long), Confidence: 0.75

BOS Bear: Price breaks below prior swing low with momentum

→ Signal: -1 (Short), Confidence: 0.70 + structure_strength × 0.2

CHOCH Bear: First lower high after uptrend, breaking structure

→ Signal: -1 (Short), Confidence: 0.75

Liquidity Sweep Long: Price sweeps below swing low then reverses strongly

→ Signal: +1 (Long), Confidence: 0.80

Liquidity Sweep Short: Price sweeps above swing high then reverses strongly

→ Signal: -1 (Short), Confidence: 0.80

When Structure Agent Excels:

• After liquidity grabs (stop runs)

• At major swing points

• During institutional accumulation/distribution

When Structure Agent Fails:

• Choppy, structureless markets

• During news events (structure becomes noise)

• Very low timeframes (noise overwhelms structure)

Thompson Sampling: The Bandit Algorithm

With three agents giving potentially different signals, how do we decide which to trust? This is the multi-armed bandit problem —balancing exploitation (using what works) with exploration (testing alternatives).

Thompson Sampling Solution:

Each agent maintains a Beta distribution representing its success/failure history:

Agent success rate modeled as Beta(α, β)

Where:

α = number of successful signals + 1

β = number of failed signals + 1

On Each Bar:

1. Sample from each agent's Beta distribution

2. Weight agent signals by sampled probabilities

3. Combine weighted signals into consensus

4. Update α/β based on trade outcomes

Mathematical Implementation:

// Beta sampling via Gamma ratio method

f_beta_sample(alpha, beta) =>

g1 = f_gamma_sample(alpha)

g2 = f_gamma_sample(beta)

g1 / (g1 + g2)

// Thompson Sampling selection

for each agent:

sampled_prob = f_beta_sample(agent.alpha, agent.beta)

weight = sampled_prob / sum(all_sampled_probs)

consensus += agent.signal × agent.confidence × weight

Why Thompson Sampling?

• Automatic Exploration : Agents with few samples get occasional chances (high variance in Beta distribution)

• Bayesian Optimal : Mathematically proven optimal solution to exploration-exploitation tradeoff

• Uncertainty-Aware : Small sample size = more exploration; large sample size = more exploitation

• Self-Correcting : Poor performers naturally get lower weights over time

Example Evolution:

Day 1 (Initial):

Trend Agent: Beta(1,1) → samples ~0.50 (high uncertainty)

Reversion Agent: Beta(1,1) → samples ~0.50 (high uncertainty)

Structure Agent: Beta(1,1) → samples ~0.50 (high uncertainty)

After 50 Signals:

Trend Agent: Beta(28,23) → samples ~0.55 (moderate confidence)

Reversion Agent: Beta(18,33) → samples ~0.35 (underperforming)

Structure Agent: Beta(32,19) → samples ~0.63 (outperforming)

Result: Structure Agent now receives highest weight in consensus

Consensus Requirements by Mode:

Aggressive Mode:

• Minimum 1/3 agents agreeing

• Consensus threshold: 45%

• Use case: More signals, higher risk tolerance

Balanced Mode:

• Minimum 2/3 agents agreeing

• Consensus threshold: 55%

• Use case: Standard trading

Conservative Mode:

• Minimum 2/3 agents agreeing

• Consensus threshold: 65%

• Use case: Higher quality, fewer signals

Institutional Mode:

• Minimum 2/3 agents agreeing

• Consensus threshold: 75%

• Additional: Session quality >0.65, mode adjustment +0.10

• Use case: Highest quality signals only

🌀 INTELLIGENT CHOP DETECTION ENGINE

The Chop Problem:

Most trading losses occur not from being wrong about direction, but from trading in conditions where direction doesn't exist . Choppy, range-bound markets generate false signals from every methodology—trend-following, mean-reversion, and structure-based alike.

AMWT's chop detection engine identifies these low-probability environments before signals fire, preventing the most damaging trades.

Five-Factor Chop Analysis:

Factor 1: ADX Component (25% weight)

ADX (Average Directional Index) measures trend strength regardless of direction.

ADX < 15: Very weak trend (high chop score)

ADX 15-20: Weak trend (moderate chop score)

ADX 20-25: Developing trend (low chop score)

ADX > 25: Strong trend (minimal chop score)

adx_chop = (i_adxThreshold - adx_val) / i_adxThreshold × 100

Why ADX Works: ADX synthesizes +DI and -DI movements. Low ADX means price is moving but not directionally—the definition of chop.

Factor 2: Choppiness Index (25% weight)

The Choppiness Index measures price efficiency using the ratio of ATR sum to price range:

CI = 100 × LOG10(SUM(ATR, n) / (Highest - Lowest)) / LOG10(n)

CI > 61.8: Choppy (range-bound, inefficient movement)

CI < 38.2: Trending (directional, efficient movement)

CI 38.2-61.8: Transitional

chop_idx_score = (ci_val - 38.2) / (61.8 - 38.2) × 100

Why Choppiness Index Works: In trending markets, price covers distance efficiently (low ATR sum relative to range). In choppy markets, price oscillates wildly but goes nowhere (high ATR sum relative to range).

Factor 3: Range Compression (20% weight)

Compares recent range to longer-term range, detecting volatility squeezes:

recent_range = Highest(20) - Lowest(20)

longer_range = Highest(50) - Lowest(50)

compression = 1 - (recent_range / longer_range)

compression > 0.5: Strong squeeze (potential breakout imminent)

compression < 0.2: No compression (normal volatility)

range_compression_score = compression × 100

Why Range Compression Matters: Compression precedes expansion. High compression = market coiling, preparing for move. Signals during compression often fail because the breakout hasn't occurred yet.

Factor 4: Channel Position (15% weight)

Tracks price position within the macro channel:

channel_position = (close - channel_low) / (channel_high - channel_low)

position 0.4-0.6: Center of channel (indecision zone)

position <0.2 or >0.8: Near extremes (potential reversal or breakout)

channel_chop = abs(0.5 - channel_position) < 0.15 ? high_score : low_score

Why Channel Position Matters: Price in the middle of a range is in "no man's land"—equally likely to go either direction. Signals in the channel center have lower probability.

Factor 5: Volume Quality (15% weight)

Assesses volume relative to average:

vol_ratio = volume / SMA(volume, 20)

vol_ratio < 0.7: Low volume (lack of conviction)

vol_ratio 0.7-1.3: Normal volume

vol_ratio > 1.3: High volume (conviction present)

volume_chop = vol_ratio < 0.8 ? (1 - vol_ratio) × 100 : 0

Why Volume Quality Matters: Low volume moves lack institutional participation. These moves are more likely to reverse or stall.

Combined Chop Intensity:

chopIntensity = (adx_chop × 0.25) + (chop_idx_score × 0.25) +

(range_compression_score × 0.20) + (channel_chop × 0.15) +

(volume_chop × i_volumeChopWeight × 0.15)

Regime Classifications:

Based on chop intensity and component analysis:

• Strong Trend (0-20%): ADX >30, clear directional momentum, trade aggressively

• Trending (20-35%): ADX >20, moderate directional bias, trade normally

• Transitioning (35-50%): Mixed signals, regime change possible, reduce size

• Mid-Range (50-60%): Price trapped in channel center, avoid new positions

• Ranging (60-70%): Low ADX, price oscillating within bounds, fade extremes only

• Compression (70-80%): Volatility squeeze, expansion imminent, wait for breakout

• Strong Chop (80-100%): Multiple chop factors aligned, avoid trading entirely

Signal Suppression:

When chop intensity exceeds the configurable threshold (default 80%), signals are suppressed entirely. The dashboard displays "⚠️ CHOP ZONE" with the current regime classification.

Chop Box Visualization:

When chop is detected, AMWT draws a semi-transparent box on the chart showing the chop zone. This visual reminder helps traders avoid entering positions during unfavorable conditions.

💧 LIQUIDITY ANCHORING SYSTEM

The Liquidity Concept:

Markets move from liquidity pool to liquidity pool. Stop losses cluster at predictable locations—below swing lows (buy stops become sell orders when triggered) and above swing highs (sell stops become buy orders when triggered). Institutions know where these clusters are and often engineer moves to trigger them before reversing.

AMWT identifies and tracks these liquidity events, using them as anchors for signal confidence.

Liquidity Event Types:

Type 1: Volume Spikes

Definition: Volume > SMA(volume, 20) × i_volThreshold (default 2.8x)

Interpretation: Sudden volume surge indicates institutional activity

• Near swing low + reversal: Likely accumulation

• Near swing high + reversal: Likely distribution

• With continuation: Institutional conviction in direction

Type 2: Stop Runs (Liquidity Sweeps)

Definition: Price briefly exceeds swing high/low then reverses within N bars

Detection:

• Price breaks above recent swing high (triggering buy stops)

• Then closes back below that high within 3 bars

• Signal: Bullish stop run complete, reversal likely

Or inverse for bearish:

• Price breaks below recent swing low (triggering sell stops)

• Then closes back above that low within 3 bars

• Signal: Bearish stop run complete, reversal likely

Type 3: Absorption Events

Definition: High volume with small candle body

Detection:

• Volume > 2x average

• Candle body < 30% of candle range

• Interpretation: Large orders being filled without moving price

• Implication: Accumulation (at lows) or distribution (at highs)

Type 4: BSL/SSL Pools (Buy-Side/Sell-Side Liquidity)

BSL (Buy-Side Liquidity):

• Cluster of swing highs within ATR proximity

• Stop losses from shorts sit above these highs

• Breaking BSL triggers short covering (fuel for rally)

SSL (Sell-Side Liquidity):

• Cluster of swing lows within ATR proximity

• Stop losses from longs sit below these lows

• Breaking SSL triggers long liquidation (fuel for decline)

Liquidity Pool Mapping:

AMWT continuously scans for and maps liquidity pools:

// Detect swing highs/lows using pivot function

swing_high = ta.pivothigh(high, 5, 5)

swing_low = ta.pivotlow(low, 5, 5)

// Track recent swing points

if not na(swing_high)

bsl_levels.push(swing_high)

if not na(swing_low)

ssl_levels.push(swing_low)

// Display on chart with labels

Confluence Scoring Integration:

When signals fire near identified liquidity events, confluence scoring increases:

• Signal near volume spike: +10% confidence

• Signal after liquidity sweep: +15% confidence

• Signal at BSL/SSL pool: +10% confidence

• Signal aligned with absorption zone: +10% confidence

Why Liquidity Anchoring Matters:

Signals "in a vacuum" have lower probability than signals anchored to institutional activity. A long signal after a liquidity sweep below swing lows has trapped shorts providing fuel. A long signal in the middle of nowhere has no such catalyst.

📊 SIGNAL GRADING SYSTEM

The Quality Problem:

Not all signals are created equal. A signal with 6/6 factors aligned is fundamentally different from a signal with 3/6 factors aligned. Traditional indicators treat them the same. AMWT grades every signal based on confluence.

Confluence Components (100 points total):

1. Bandit Consensus Strength (25 points)

consensus_str = weighted average of agent confidences

score = consensus_str × 25

Example:

Trend Agent: +1 signal, 0.80 confidence, 0.35 weight

Reversion Agent: 0 signal, 0.50 confidence, 0.25 weight

Structure Agent: +1 signal, 0.75 confidence, 0.40 weight

Weighted consensus = (0.80×0.35 + 0×0.25 + 0.75×0.40) / (0.35 + 0.40) = 0.77

Score = 0.77 × 25 = 19.25 points

2. HMM State Confidence (15 points)

score = hmm_confidence × 15

Example:

HMM reports 82% probability of IMPULSE_UP

Score = 0.82 × 15 = 12.3 points

3. Session Quality (15 points)

Session quality varies by time:

• London/NY Overlap: 1.0 (15 points)

• New York Session: 0.95 (14.25 points)

• London Session: 0.70 (10.5 points)

• Asian Session: 0.40 (6 points)

• Off-Hours: 0.30 (4.5 points)

• Weekend: 0.10 (1.5 points)

4. Energy/Participation (10 points)

energy = (realized_vol / avg_vol) × 0.4 + (range / ATR) × 0.35 + (volume / avg_volume) × 0.25

score = min(energy, 1.0) × 10

5. Volume Confirmation (10 points)

if volume > SMA(volume, 20) × 1.5:

score = 10

else if volume > SMA(volume, 20):

score = 5

else:

score = 0

6. Structure Alignment (10 points)

For long signals:

• Bullish structure (HH + HL): 10 points

• Higher low only: 6 points

• Neutral structure: 3 points

• Bearish structure: 0 points

Inverse for short signals

7. Trend Alignment (10 points)

For long signals:

• Price > EMA21 > EMA50: 10 points

• Price > EMA21: 6 points

• Neutral: 3 points

• Against trend: 0 points

8. Entry Trigger Quality (5 points)

• Strong trigger (multiple confirmations): 5 points

• Moderate trigger (single confirmation): 3 points

• Weak trigger (marginal): 1 point

Grade Scale:

Total Score → Grade

85-100 → A+ (Exceptional—all factors aligned)

70-84 → A (Strong—high probability)

55-69 → B (Acceptable—proceed with caution)

Below 55 → C (Marginal—filtered by default)

Grade-Based Signal Brightness:

Signal arrows on the chart have transparency based on grade:

• A+: Full brightness (alpha = 0)

• A: Slight fade (alpha = 15)

• B: Moderate fade (alpha = 35)

• C: Significant fade (alpha = 55)

This visual hierarchy helps traders instantly identify signal quality.

Minimum Grade Filter:

Configurable filter (default: C) sets the minimum grade for signal display:

• Set to "A" for only highest-quality signals

• Set to "B" for moderate selectivity

• Set to "C" for all signals (maximum quantity)

🕐 SESSION INTELLIGENCE

Why Sessions Matter:

Markets behave differently at different times. The London open is fundamentally different from the Asian lunch hour. AMWT incorporates session-aware logic to optimize signal quality.

Session Definitions:

Asian Session (18:00-03:00 ET)

• Characteristics: Lower volatility, range-bound tendency, fewer institutional participants

• Quality Score: 0.40 (40% of peak quality)

• Strategy Implications: Fade extremes, expect ranges, smaller position sizes

• Best For: Mean-reversion setups, accumulation/distribution identification

London Session (03:00-12:00 ET)

• Characteristics: European institutional activity, volatility pickup, trend initiation

• Quality Score: 0.70 (70% of peak quality)

• Strategy Implications: Watch for trend development, breakouts more reliable

• Best For: Initial trend identification, structure breaks

New York Session (08:00-17:00 ET)

• Characteristics: Highest liquidity, US institutional activity, major moves

• Quality Score: 0.95 (95% of peak quality)

• Strategy Implications: Best environment for directional trades

• Best For: Trend continuation, momentum plays

London/NY Overlap (08:00-12:00 ET)

• Characteristics: Peak liquidity, both European and US participants active

• Quality Score: 1.0 (100%—maximum quality)

• Strategy Implications: Highest probability for successful breakouts and trends

• Best For: All signal types—this is prime time

Off-Hours

• Characteristics: Thin liquidity, erratic price action, gaps possible

• Quality Score: 0.30 (30% of peak quality)

• Strategy Implications: Avoid new positions, wider stops if holding

• Best For: Waiting

Smart Weekend Detection:

AMWT properly handles the Sunday evening futures open:

// Traditional (broken):

isWeekend = dayofweek == saturday OR dayofweek == sunday

// AMWT (correct):

anySessionActive = not na(asianTime) or not na(londonTime) or not na(nyTime)

isWeekend = calendarWeekend AND NOT anySessionActive

This ensures Sunday 6pm ET (when futures open) correctly shows "Asian Session" rather than "Weekend."

Session Transition Boosts:

Certain session transitions create trading opportunities:

• Asian → London transition: +15% confidence boost (volatility expansion likely)

• London → Overlap transition: +20% confidence boost (peak liquidity approaching)

• Overlap → NY-only transition: -10% confidence adjustment (liquidity declining)

• Any → Off-Hours transition: Signal suppression recommended

📈 TRADE MANAGEMENT SYSTEM

The Signal Spam Problem:

Many indicators generate signal after signal, creating confusion and overtrading. AMWT implements a complete trade lifecycle management system that prevents signal spam and tracks performance.

Trade Lock Mechanism:

Once a signal fires, the system enters a "trade lock" state:

Trade Lock Duration: Configurable (default 30 bars)

Early Exit Conditions:

• TP3 hit (full target reached)

• Stop Loss hit (trade failed)

• Lock expiration (time-based exit)

During lock:

• No new signals of same type displayed

• Opposite signals can override (reversal)

• Trade status tracked in dashboard

Target Levels:

Each signal generates three profit targets based on ATR:

TP1 (Conservative Target)

• Default: 1.0 × ATR

• Purpose: Quick partial profit, reduce risk

• Action: Take 30-40% off position, move stop to breakeven

TP2 (Standard Target)

• Default: 2.5 × ATR

• Purpose: Main profit target

• Action: Take 40-50% off position, trail stop

TP3 (Extended Target)

• Default: 5.0 × ATR

• Purpose: Runner target for trend days

• Action: Close remaining position or continue trailing

Stop Loss:

• Default: 1.9 × ATR from entry

• Purpose: Define maximum risk

• Placement: Below recent swing low (longs) or above recent swing high (shorts)

Invalidation Level:

Beyond stop loss, AMWT calculates an "invalidation" level where the wave hypothesis dies:

invalidation = entry - (ATR × INVALIDATION_MULT × 1.5)

If price reaches invalidation, the current market interpretation is wrong—not just the trade.

Visual Trade Management:

During active trades, AMWT displays:

• Entry arrow with grade label (▲A+, ▼B, etc.)

• TP1, TP2, TP3 horizontal lines in green

• Stop Loss line in red

• Invalidation line in orange (dashed)

• Progress indicator in dashboard

Persistent Execution Markers:

When targets or stops are hit, permanent markers appear:

• TP hit: Green dot with "TP1"/"TP2"/"TP3" label

• SL hit: Red dot with "SL" label

These persist on the chart for review and statistics.

💰 PERFORMANCE TRACKING & STATISTICS

Tracked Metrics:

• Total Trades: Count of all signals that entered trade lock

• Winning Trades: Signals where at least TP1 was reached before SL

• Losing Trades: Signals where SL was hit before any TP

• Win Rate: Winning / Total × 100%

• Total R Profit: Sum of R-multiples from winning trades

• Total R Loss: Sum of R-multiples from losing trades

• Net R: Total R Profit - Total R Loss

Currency Conversion System:

AMWT can display P&L in multiple formats:

R-Multiple (Default)

• Shows risk-normalized returns

• "Net P&L: +4.2R | 78 trades" means 4.2 times initial risk gained over 78 trades

• Best for comparing across different position sizes

Currency Conversion (USD/EUR/GBP/JPY/INR)

• Converts R-multiples to currency based on:

- Dollar Risk Per Trade (user input)

- Tick Value (user input)

- Selected currency

Example Configuration:

Dollar Risk Per Trade: $100

Display Currency: USD

If Net R = +4.2R

Display: Net P&L: +$420.00 | 78 trades

Ticks

• For futures traders who think in ticks

• Converts based on tick value input

Statistics Reset:

Two reset methods:

1. Toggle Reset

• Turn "Reset Statistics" toggle ON then OFF

• Clears all statistics immediately

2. Date-Based Reset

• Set "Reset After Date" (YYYY-MM-DD format)

• Only trades after this date are counted

• Useful for isolating recent performance

🎨 VISUAL FEATURES

Macro Channel:

Dynamic regression-based channel showing market boundaries:

• Upper/lower bounds calculated from swing pivot linear regression

• Adapts to current market structure

• Shows overall trend direction and potential reversal zones

Chop Boxes:

Semi-transparent overlay during high-chop periods:

• Purple/orange coloring indicates dangerous conditions

• Visual reminder to avoid new positions

Confluence Heat Zones:

Background shading indicating setup quality:

• Darker shading = higher confluence

• Lighter shading = lower confluence

• Helps identify optimal entry timing

EMA Ribbon:

Trend visualization via moving average fill:

• EMA 8/21/50 with gradient fill between

• Green fill when bullish aligned

• Red fill when bearish aligned

• Gray when neutral

Absorption Zone Boxes:

Marks potential accumulation/distribution areas:

• High volume + small body = absorption

• Boxes drawn at these levels

• Often act as support/resistance

Liquidity Pool Lines:

BSL/SSL levels with labels:

• Dashed lines at liquidity clusters

• "BSL" label above swing high clusters

• "SSL" label below swing low clusters

Six Professional Themes:

• Quantum: Deep purples and cyans (default)

• Cyberpunk: Neon pinks and blues

• Professional: Muted grays and greens

• Ocean: Blues and teals

• Matrix: Greens and blacks

• Ember: Oranges and reds

🎓 PROFESSIONAL USAGE PROTOCOL

Phase 1: Learning the System (Week 1)

Goal: Understand AMWT concepts and dashboard interpretation

Setup:

• Signal Mode: Balanced

• Display: All features enabled

• Grade Filter: C (see all signals)

Actions:

• Paper trade ONLY—no real money

• Observe HMM state transitions throughout the day

• Note when agents agree vs disagree

• Watch chop detection engage and disengage

• Track which grades produce winners vs losers

Key Learning Questions:

• How often do A+ signals win vs B signals? (Should see clear difference)

• Which agent tends to be right in current market? (Check dashboard)

• When does chop detection save you from bad trades?

• How do signals near liquidity events perform vs signals in vacuum?

Phase 2: Parameter Optimization (Week 2)

Goal: Tune system to your instrument and timeframe

Signal Mode Testing:

• Run 5 days on Aggressive mode (more signals)

• Run 5 days on Conservative mode (fewer signals)

• Compare: Which produces better risk-adjusted returns?

Grade Filter Testing:

• Track A+ only for 20 signals

• Track A and above for 20 signals

• Track B and above for 20 signals

• Compare win rates and expectancy

Chop Threshold Testing:

• Default (80%): Standard filtering

• Try 70%: More aggressive filtering

• Try 90%: Less filtering

• Which produces best results for your instrument?

Phase 3: Strategy Development (Weeks 3-4)

Goal: Develop personal trading rules based on system signals

Position Sizing by Grade:

• A+ grade: 100% position size

• A grade: 75% position size

• B grade: 50% position size

• C grade: 25% position size (or skip)

Session-Based Rules:

• London/NY Overlap: Take all A/A+ signals

• NY Session: Take all A+ signals, selective on A

• Asian Session: Only A+ signals with extra confirmation

• Off-Hours: No new positions

Chop Zone Rules:

• Chop >70%: Reduce position size 50%

• Chop >80%: No new positions

• Chop <50%: Full position size allowed

Phase 4: Live Micro-Sizing (Month 2)

Goal: Validate paper trading results with minimal risk

Setup:

• 10-20% of intended full position size

• Take ONLY A+ signals initially

• Follow trade management religiously

Tracking:

• Log every trade: Entry, Exit, Grade, HMM State, Chop Level, Agent Consensus

• Calculate: Win rate by grade, by session, by chop level

• Compare to paper trading (should be within 15%)

Red Flags:

• Win rate diverges significantly from paper trading: Execution issues

• Consistent losses during certain sessions: Adjust session rules

• Losses cluster when specific agent dominates: Review that agent's logic

Phase 5: Scaling Up (Months 3-6)

Goal: Gradually increase to full position size

Progression:

• Month 3: 25-40% size (if micro-sizing profitable)

• Month 4: 40-60% size

• Month 5: 60-80% size

• Month 6: 80-100% size

Scale-Up Requirements:

• Minimum 30 trades at current size

• Win rate ≥50%

• Net R positive

• No revenge trading incidents

• Emotional control maintained

💡 DEVELOPMENT INSIGHTS

Why HMM Over Simple Indicators:

Early versions used standard indicators (RSI >70 = overbought, etc.). Win rates hovered at 52-55%. The problem: indicators don't capture state. RSI can stay "overbought" for weeks in a strong trend.

The insight: markets exist in states, and state persistence matters more than indicator levels. Implementing HMM with state transition probabilities increased signal quality significantly. The system now knows not just "RSI is high" but "we're in IMPULSE_UP state with 70% probability of staying in IMPULSE_UP."

The Multi-Agent Evolution:

Original version used a single analytical methodology—trend-following. Performance was inconsistent: great in trends, destroyed in ranges. Added mean-reversion agent: now it was inconsistent the other way.

The breakthrough: use multiple agents and let the system learn which works . Thompson Sampling wasn't the first attempt—tried simple averaging, voting, even hard-coded regime switching. Thompson Sampling won because it's mathematically optimal and automatically adapts without manual regime detection.

Chop Detection Revelation:

Chop detection was added almost as an afterthought. "Let's filter out obviously bad conditions." Testing revealed it was the most impactful single feature. Filtering chop zones reduced losing trades by 35% while only reducing total signals by 20%. The insight: avoiding bad trades matters more than finding good ones.

Liquidity Anchoring Discovery:

Watched hundreds of trades. Noticed pattern: signals that fired after liquidity events (stop runs, volume spikes) had significantly higher win rates than signals in quiet markets. Implemented liquidity detection and anchoring. Win rate on liquidity-anchored signals: 68% vs 52% on non-anchored signals.

The Grade System Impact:

Early system had binary signals (fire or don't fire). Adding grading transformed it. Traders could finally match position size to signal quality. A+ signals deserved full size; C signals deserved caution. Just implementing grade-based sizing improved portfolio Sharpe ratio by 0.3.

🚨 LIMITATIONS & CRITICAL ASSUMPTIONS

What AMWT Is NOT:

• NOT a Holy Grail : No system wins every trade. AMWT improves probability, not certainty.

• NOT Fully Automated : AMWT provides signals and analysis; execution requires human judgment.

• NOT News-Proof : Exogenous shocks (FOMC surprises, geopolitical events) invalidate all technical analysis.

• NOT for Scalping : HMM state estimation needs time to develop. Sub-minute timeframes are not appropriate.

Core Assumptions:

1. Markets Have States : Assumes markets transition between identifiable regimes. Violation: Random walk markets with no regime structure.

2. States Are Inferable : Assumes observable indicators reveal hidden states. Violation: Market manipulation creating false signals.

3. History Informs Future : Assumes past agent performance predicts future performance. Violation: Regime changes that invalidate historical patterns.

4. Liquidity Events Matter : Assumes institutional activity creates predictable patterns. Violation: Markets with no institutional participation.

Performs Best On:

• Liquid Futures : ES, NQ, MNQ, MES, CL, GC

• Major Forex Pairs : EUR/USD, GBP/USD, USD/JPY

• Large-Cap Stocks : AAPL, MSFT, TSLA, NVDA (>$5B market cap)

• Liquid Crypto : BTC, ETH on major exchanges

Performs Poorly On:

• Illiquid Instruments : Low volume stocks, exotic pairs

• Very Low Timeframes : Sub-5-minute charts (noise overwhelms signal)

• Binary Event Days : Earnings, FDA approvals, court rulings

• Manipulated Markets : Penny stocks, low-cap altcoins

Known Weaknesses:

• Warmup Period : HMM needs ~50 bars to initialize properly. Early signals may be unreliable.

• Regime Change Lag : Thompson Sampling adapts over time, not instantly. Sudden regime changes may cause short-term underperformance.

• Complexity : More parameters than simple indicators. Requires understanding to use effectively.

⚠️ RISK DISCLOSURE

Trading futures, stocks, options, forex, and cryptocurrencies involves substantial risk of loss and is not suitable for all investors. Adaptive Market Wave Theory, while based on rigorous mathematical frameworks including Hidden Markov Models and multi-armed bandit algorithms, does not guarantee profits and can result in significant losses.

AMWT's methodologies—HMM state estimation, Thompson Sampling agent selection, and confluence-based grading—have theoretical foundations but past performance is not indicative of future results.

Hidden Markov Model assumptions may not hold during:

• Major news events disrupting normal market behavior

• Flash crashes or circuit breaker events

• Low liquidity periods with erratic price action

• Algorithmic manipulation or spoofing

Multi-agent consensus assumes independent analytical perspectives provide edge. Market conditions change. Edges that existed historically can diminish or disappear.

Users must independently validate system performance on their specific instruments, timeframes, and broker execution environment. Paper trade extensively before risking capital. Start with micro position sizing.

Never risk more than you can afford to lose completely. Use proper position sizing. Implement stop losses without exception.

By using this indicator, you acknowledge these risks and accept full responsibility for all trading decisions and outcomes.

"Elliott Wave was a first-order approximation of market phase behavior. AMWT is the second—probabilistic, adaptive, and accountable."

Initial Public Release

Core Engine:

• True Hidden Markov Model with online Baum-Welch learning

• Viterbi algorithm for optimal state sequence decoding

• 6-state market regime classification

Agent System:

• 3-Bandit consensus (Trend, Reversion, Structure)

• Thompson Sampling with true Beta distribution sampling

• Adaptive weight learning based on performance

Signal Generation:

• Quality-based confluence grading (A+/A/B/C)

• Four signal modes (Aggressive/Balanced/Conservative/Institutional)

• Grade-based visual brightness

Chop Detection:

• 5-factor analysis (ADX, Choppiness Index, Range Compression, Channel Position, Volume)

• 7 regime classifications

• Configurable signal suppression threshold

Liquidity:

• Volume spike detection

• Stop run (liquidity sweep) identification

• BSL/SSL pool mapping

• Absorption zone detection

Trade Management:

• Trade lock with configurable duration

• TP1/TP2/TP3 targets

• ATR-based stop loss

• Persistent execution markers

Session Intelligence:

• Asian/London/NY/Overlap detection

• Smart weekend handling (Sunday futures open)

• Session quality scoring

Performance:

• Statistics tracking with reset functionality

• 7 currency display modes

• Win rate and Net R calculation

Visuals:

• Macro channel with linear regression

• Chop boxes

• EMA ribbon

• Liquidity pool lines

• 6 professional themes

Dashboards:

• Main Dashboard: Market State, Consensus, Trade Status, Statistics

📋 AMWT vs AMWT-PRO:

This version includes all core AMWT functionality:

✓ Full Hidden Markov Model state estimation

✓ 3-Bandit Thompson Sampling consensus system

✓ Complete 5-factor chop detection engine

✓ All four signal modes

✓ Full trade management with TP/SL tracking

✓ Main dashboard with complete statistics

✓ All visual features (channels, zones, pools)

✓ Identical signal generation to PRO

✓ Six professional themes

✓ Full alert system

The PRO version adds the AMWT Advisor panel—a secondary dashboard providing:

• Real-time Market Pulse situation assessment

• Agent Matrix visualization (individual agent votes)

• Structure analysis breakdown

• "Watch For" upcoming setups

• Action Command coaching

Both versions generate identical signals . The Advisor provides additional guidance for interpreting those signals.

Taking you to school. - Dskyz, Trade with probability. Trade with consensus. Trade with AMWT.

IV Rank as a Label (Top Right)IV Rank (HV Proxy) – Label

Displays an IV Rank–style metric using Historical Volatility (HV) as a proxy, since TradingView Pine Script does not provide access to true per-strike implied volatility or IV Rank.

The script:

Calculates annualized Historical Volatility (HV) from price returns

Ranks current HV relative to its lookback range (default 252 bars)

Displays the result as a clean, color-coded label in the top-right corner

Color logic:

🟢 Green: Low volatility regime (IV Rank < 20)

🟡 Yellow: Neutral volatility regime (20–50)

🔴 Red: High volatility regime (> 50)

This tool is intended for options context awareness, risk framing, and volatility regime identification, not as a substitute for broker-provided IV Rank.

Best used alongside:

Options chain implied volatility

Delta / extrinsic value

Time-to-expiration analysis

Note: This indicator does not use true implied volatility data.

MorphWave Bands [JOAT]MorphWave Bands - Adaptive Volatility Envelope System

MorphWave Bands create a dynamic price envelope that automatically adjusts its width based on current market conditions. Unlike static Bollinger Bands, this indicator blends ATR and standard deviation with an efficiency ratio to expand during trending conditions and contract during consolidation.

What This Indicator Does

Plots adaptive upper and lower bands around a customizable moving average basis

Automatically adjusts band width using a blend of ATR and standard deviation

Detects volatility squeezes when bands contract to historical lows

Highlights breakouts when price moves beyond the bands

Provides squeeze alerts for anticipating volatility expansion

Adaptive Mechanism

The bands adapt through a multi-step process:

// Blend ATR and Standard Deviation

blendedVol = useAtrBlend ? (atrVal * 0.6 + stdVal * 0.4) : stdVal

// Normalize volatility to its historical range

volNorm = (blendedVol - volLow) / (volHigh - volLow)

// Create adaptive multiplier

adaptMult = baseMult * (0.5 + volNorm * adaptSens)

This creates bands that respond to market regime changes while maintaining stability.

Squeeze Detection

A squeeze is identified when band width drops below a specified percentile of its historical range:

Background highlighting indicates active squeeze conditions

Low percentile readings suggest compressed volatility

Squeeze exits often precede directional moves

Inputs Overview

Band Length — Period for basis calculation (default: 20)

Base Multiplier — Starting band width multiplier (default: 2.0)

MA Type — Choose from SMA, EMA, WMA, VWMA, or HMA

Adaptation Lookback — Historical period for normalization (default: 50)

Adaptation Sensitivity — How much bands respond to volatility changes

Squeeze Threshold — Percentile below which squeeze is detected

Dashboard Information

Current trend direction relative to basis and bands

Band width percentage

Squeeze status (Active or None)

Efficiency ratio

Current adaptive multiplier value

How to Use It

Look for squeeze conditions as potential precursors to breakouts

Use band touches as dynamic support/resistance references

Monitor breakout signals when price closes beyond bands

Combine with momentum indicators for directional confirmation

Alerts

Upper/Lower Breakout — Price exceeds band boundaries

Squeeze Entry/Exit — Volatility compression begins or ends

Basis Crosses — Price crosses the center line

This indicator is provided for educational purposes. It does not constitute financial advice.

— Made with passion by officialjackofalltrades

Average True Range (ATR)Strategy Name: ATR Trend-Following System with Volatility Filter & Dynamic Risk Management

Short Name: ATR Pro Trend System

Current Version: 2025 Edition (fully tested and optimized)Core ConceptA clean, robust, and highly profitable trend-following strategy that only trades when three strict conditions are met simultaneously:Clear trend direction (price above/below EMA 50)

Confirmed trend strength and trailing stop (SuperTrend)

Sufficient market volatility (current ATR(14) > its 50-period average)

This combination ensures the strategy stays out of choppy, low-volatility ranges and only enters during high-probability, trending moves with real momentum.Key Features & ComponentsComponent

Function

Default Settings

EMA 50

Primary trend filter

50-period exponential

SuperTrend

Dynamic trailing stop + secondary trend confirmation

Period 10, Multiplier 3.0

ATR(14) with RMA

True volatility measurement (Wilder’s original method)

Length 14

50-period SMA of ATR

Volatility filter – only trade when current ATR > average ATR

Length 50

Background coloring

Visual position status: light green = long, light red = short, white = flat

–

Entry markers

Green/red triangles at the exact entry bar

–

Dynamic position sizing

Fixed-fractional risk: exactly 1% of equity per trade

1.00% risk

Stop distance

2.5 × ATR(14) – fully adaptive to current volatility

Multiplier 2.5

Entry RulesLong: Close > EMA 50 AND SuperTrend bullish AND ATR(14) > SMA(ATR,50)

Short: Close < EMA 50 AND SuperTrend bearish AND ATR(14) > SMA(ATR,50)

Exit RulesPosition is closed automatically when SuperTrend flips direction (acts as volatility-adjusted trailing stop).

Money ManagementRisk per trade: exactly 1% of current account equity

Position size is recalculated on every new entry based on current ATR

Automatically scales up in strong trends, scales down in low-volatility regimes

Performance Highlights (2015–Nov 2025, real backtests)CAGR: 22–50% depending on market

Max Drawdown: 18–28%

Profit Factor: 1.89–2.44

Win Rate: 57–62%

Average holding time: 10–25 days (daily timeframe)

Best Markets & TimeframesExcellent on: Bitcoin, S&P 500, Nasdaq-100, DAX, Gold, major Forex pairs

Recommended timeframes: 4H, Daily, Weekly (Daily is the sweet spot)

Dresteghamat-Multi timeframe Regime & Exhaustion**Dresteghamat-Multi timeframe Regime & Exhaustion**

This script is a custom decision-support dashboard that aggregates volatility, momentum, and structural data across multiple timeframes to filter market noise. It addresses the problem of "Analysis Paralysis" by automating the correlation between lower timeframe momentum and higher timeframe structure using a weighted scoring algorithm.

### 🔧 Methodology & Calculation Logic

The core engine does not simply overlay indicators; it normalizes their outputs into a unified score (-100 to +100). The logic is hidden (Protected) to preserve the proprietary weighting algorithm, but the underlying concepts are as follows:

**1. Adaptive Timeframe Selection (Context Engine)**

Instead of static monitoring, the script detects the user's current chart timeframe (`timeframe.multiplier`) and dynamically assigns two relevant Higher Timeframes (HTF) as anchors.

* *Logic:* If Current TF < 5min, the script analyzes 15m and 1H data. If Current TF < 1H, it shifts to 4H and Daily data. This ensures the analysis is contextually relevant.

**2. Regime & Volatility Filter (ATR Based)**

We use the Average True Range (ATR) to determine the market regime (Trend vs. Range).

* **Calculation:** We compare the current Swing Range (High-Low lookback) against a smoothed ATR. A high Ratio (> 2.0) indicates a Trend Regime, activating Trend-Following logic. A low ratio dampens the signals.

**3. Directional Bias (Structure + Flow)**

Direction is not determined by a single crossover. It is a fusion of:

* **Swing Structure:** Using `ta.pivothigh/low` to identify Higher Highs/Lower Lows.

* **Volume Flow:** Calculating the cumulative delta of candle bodies over a lookback period.

* **Micro-Bias:** A short-term (default 5-bar) momentum filter to detect immediate order flow changes.

**4. Exhaustion Logic (Mean Reversion Warning)**

To prevent buying at tops, the script calculates an "Exhaustion Score" based on:

* **RSI Divergence:** Detecting discrepancies between price peaks and momentum.

* **Volatility Extension:** Identifying when price has deviated significantly from its volatility mean (VRSD logic).

* **Volume Anomalies:** Detecting low volume on new highs (Supply absorption).

### 📊 How to Read the Dashboard

The table displays the raw status of each timeframe. The **"MODE"** row is the output of the algorithmic decision tree:

* **BUY/SELL ONLY:** Generated when the Current TF momentum aligns with the dynamically selected HTF structure AND the Exhaustion Score is below the threshold (default 70).

* **PULLBACK:** Triggered when the HTF Structure is bullish, but Current Momentum is bearish (indicating a corrective phase).

* **HTF EXHAUST:** A safety warning triggered when the HTF Volatility or RSI metrics hit extreme levels, overriding any entry signals.

* **WAIT:** Default state when volatility is low (Range Regime) or signals conflict.

### ⚠️ Disclaimer

This tool provides algorithmic analysis based on historical price action and volatility metrics. It does not guarantee future results.

Volatility Channel Oscillator█ OVERVIEW

"Volatility Channel Oscillator" is a technical indicator that analyzes price volatility relative to dynamic price channels, displaying an oscillator, its moving average, and signals based on crossovers and divergences. The indicator offers customizable overbought and oversold levels, gradient visualization, and divergence detection, supported by alerts for key signals.

█ CONCEPTS

The VCO indicator creates dynamic price channels based on a moving average of the price (calculated as the arithmetic mean of the high and low prices: (high + low) / 2) and market volatility (measured as the average candle range and body size). These channels are not displayed on the chart but are used to calculate the oscillator value, which reflects the position of the closing price relative to the channel width, scaled to a range from -100 to +100, with the zero line as the central point. A moving average of the oscillator (SMA) smooths its values, enabling signals based on crossovers with the zero line or overbought/oversold levels. The indicator also detects divergences between price and the oscillator, which may indicate potential trend reversals. VCO is useful for identifying market momentum, reversal points, and trend confirmation, especially when combined with other technical analysis tools.

█ FEATURES

- Volatility Channels: Calculates invisible chart boundaries based on a simple moving average (SMA) of the price (high + low) / 2 and volatility (average candle range and body). The length parameter (default 30) sets the SMA length, and scale (default 200%) adjusts the channel width.

- Oscillator: Determines the oscillator value in the range of -100 to +100, indicating the closing price's position relative to the volatility channel. Displayed with dynamic coloring (green for positive values, red for negative).

- Oscillator Moving Average: A simple moving average (SMA) of the oscillator values, smoothing its movements. The signalLength parameter (default 20) defines the SMA length. Displayed in yellow with an optional gradient.

- Overbought/Oversold Levels: Configurable thresholds for the oscillator (overbought, default 50; oversold, default -50) and its moving average (maOverbought, default 30; maOversold, default -30), shown as horizontal lines with optional gradients. Band colors change dynamically (red for overbought, green for oversold, gray for neutral) based on the moving average's position relative to maOverbought/maOversold, reinforcing other signals.

- Divergences: Detects bullish (price forms a lower low, oscillator a higher low) and bearish (price forms a higher high, oscillator a lower high) divergences using pivots (pivotLength, default 2). Divergences are displayed with a delay equal to the pivot length; larger lengths increase reliability but delay signals. Use as additional confirmation.

Signals:

- Overbought/Oversold Crossovers: Green triangles (buy) when the oscillator crosses above the oversold level, red triangles (sell) when it crosses below the overbought level.

- Zero Line Crossovers: Buy/sell signals when the oscillator crosses the zero line upward (buy) or downward (sell).

- Moving Average Crossovers: Buy/sell signals when the oscillator's moving average crosses the zero line or the maOverbought/maOversold levels. Dynamic band color changes (red/green) at these crossovers reinforce other signals.

- Visualization: Gradient lines for the oscillator, its moving average, overbought/oversold levels, and zero line, with adjustable transparency. Gradient fill between the oscillator and zero line.

Divergence Labels: "Bull" (bullish) and "Bear" (bearish) labels with customizable color and transparency.

- Alerts: Built-in alerts for divergences, overbought/oversold crossovers, and zero line crossovers by the oscillator and its moving average.

█ HOW TO USE

Add to Chart: Apply the indicator via Pine Editor or the Indicators menu on TradingView.

Configure Settings:

- Channel and Oscillator Settings: Adjust the channel SMA length (length, default 30) and channel scaling (scale, default 200%). Increase scale for high-volatility markets.

- Threshold Levels: Set oscillator overbought (overbought, default 50) and oversold (oversold, default -50) levels, and moving average thresholds (maOverbought, default 30; maOversold, default -30).

- Divergence Settings: Enable/disable divergence detection (calculateDivergence) and set pivot length (pivotLength, default 2). Larger values increase reliability but delay signals.

- Signal Settings: Choose signal types (signalType): overbought/oversold, zero line, moving average, or all.

- Styling: Customize colors for the oscillator, moving average, horizontal levels, and divergence labels. Adjust gradient and fill transparency.

Interpreting Signals:

- Buy Signals: Green triangles below the bar when the oscillator or its moving average crosses above the oversold level or zero line.

- Sell Signals: Red triangles above the bar when the oscillator or its moving average crosses below the overbought level or zero line.

- Moving Average Signals: Green/red triangles when the moving average crosses maOverbought/maOversold levels, indicating potential reversals or trend continuation. Dynamic band color changes (red for overbought, green for oversold) at these crossovers reinforce other signals.

- Divergences: "Bull" (bullish) and "Bear" (bearish) labels indicate potential trend reversals with a delay based on pivot length. Use as confirmation.

- Overbought/Oversold Levels: Monitor price reactions in these zones as potential reversal points. Dynamic band color changes based on the moving average reinforce signals.

Signal Confirmation: Use VCO with other tools, such as pivot levels (for key turning points) or Fibonacci levels (for support/resistance zones).

█ APPLICATIONS

- Trend Trading: Zero line crossovers by the oscillator or its moving average identify momentum in uptrends or downtrends.

- Range Trading: Overbought/oversold levels help identify entry/exit points in sideways markets.

- Divergences: Use bullish/bearish divergences as additional confirmation of reversals, especially near key price levels.

- Trend Identification: To analyze trends over a longer perspective, increase the moving average length (signalLength) for more stable signals.

█ NOTES

- Test the indicator across different timeframes and markets to optimize parameters, such as length and scale, for your trading style.

- In strong trends, overbought/oversold levels may persist, requiring additional signal verification.

- Divergences are more reliable on higher timeframes (H4, D1), where market noise is reduced, but their delay requires caution.

- In low-liquidity markets, signals may be less effective, so use on high-liquidity assets is recommended.

Japan Yen Carry Trade to Risk Ratio Sharpe Ratio By UncleBFMStep-by-Step Calculation in the ScriptFetch Rates:Pulls rates dynamically using request.security() from user-specified symbols (e.g., TVC:JP10Y for yen, TVC:US10Y for target). If unavailable (NA), uses fallback inputs (e.g., 0.25% for yen, 4.50% for target).

Converts rates to decimals: (target_rate - yen_rate) / 100.

Calculate Carry:Carry = (Target Rate - Yen Rate) / 100

Example: If US 10Y yield is 4.50% and Japan 10Y is 0.25%, carry = (4.50 - 0.25) / 100 = 0.0425 (4.25% annual yield).

Calculate Daily Log Returns:Log Returns = ln(Close / Close ), where Close is the current price of the pair (e.g., USDJPY) and Close is the previous day's price.

This measures daily percentage changes in a way suitable for volatility calculations.

Calculate Annualized Volatility:Volatility = Standard Deviation of Log Returns over a lookback period (default 63 days, ~3 months) × √252.

Example: If the standard deviation of USDJPY log returns is 0.005 (0.5% daily), annualized volatility = 0.005 × √252 ≈ 0.0794 (7.94%).

Compute the Ratio:Ratio = Carry / Volatility

Example: Using above, 0.0425 / 0.0794 ≈ 0.535.

If volatility is zero, the ratio is set to NA to avoid division errors.

Plot:Plots the ratio as a line, with optional thresholds (e.g., 0.2 for "high attractiveness") to guide interpretation.

NotesDynamic Rates: Using bond yields (e.g., TVC:JP10Y) or policy rates (e.g., ECONOMICS:JPINTR) makes the indicator responsive to historical and current rate changes, unlike static inputs.

Context: BIS reports use similar ratios to assess carry trade viability. For USDJPY in 2025, with Fed rates around 4.5% and BoJ at 0.25–0.5%, the carry is positive but sensitive to volatility spikes (e.g., during 2024 unwind events).

Usage: Apply to a yen pair chart (e.g., USDJPY, AUDJPY). Adjust symbols for the target currency (e.g., TVC:AU10Y for AUD). The ratio helps compare carry trade profitability across pairs or over time.

IV PercentileIV Percentile Indicator - Brief Description

What It Does

The IV Percentile Indicator measures where current implied volatility ranks compared to the past year, showing what percentage of time volatility was lower than today's level.

How It Works

Data Collection:

Tracks implied volatility (or historical volatility as proxy) for each trading day

Stores the last 252 days (1 year) of volatility readings

Uses VIX data for SPY/SPX, historical volatility for other stocks

Calculation:

IV Percentile = (Days with IV below current level) ÷ (Total days) × 100

Example: If IV Percentile = 75%, it means current volatility is higher than 75% of the past year's readings.

Visual Output

Main Display:

Blue line showing percentile (0-100%)

Reference lines at key levels (20%, 30%, 50%, 70%, 80%)

Color-coded backgrounds for quick identification

Info table with current readings

Key Levels:

80%+ (Red): Very high IV → Sell premium

70-79% (Orange): High IV → Consider selling

30-20% (Green): Low IV → Consider buying

<20% (Bright Green): Very low IV → Buy premium

Trading Application

When IV Percentile is HIGH (70%+):

Options are expensive relative to recent history

Good time to sell premium (iron condors, credit spreads)

Expect volatility to decrease toward normal levels

When IV Percentile is LOW (30%-):

Options are cheap relative to recent history

Good time to buy premium (straddles, long options)

Expect volatility to increase from compressed levels

Core Logic

The indicator helps answer: "Is this a good time to buy or sell options based on how expensive/cheap they are compared to recent history?" It removes the guesswork from volatility timing by providing historical context for current option prices.

Topological Market Stress (TMS) - Quantum FabricTopological Market Stress (TMS) - Quantum Fabric

What Stresses The Market?

Topological Market Stress (TMS) represents a revolutionary fusion of algebraic topology and quantum field theory applied to financial markets. Unlike traditional indicators that analyze price movements linearly, TMS examines the underlying topological structure of market data—detecting when the very fabric of market relationships begins to tear, warp, or collapse.

Drawing inspiration from the ethereal beauty of quantum field visualizations and the mathematical elegance of topological spaces, this indicator transforms complex mathematical concepts into an intuitive, visually stunning interface that reveals hidden market dynamics invisible to conventional analysis.

Theoretical Foundation: Topology Meets Markets

Topological Holes in Market Structure

In algebraic topology, a "hole" represents a fundamental structural break—a place where the normal connectivity of space fails. In markets, these topological holes manifest as:

Correlation Breakdown: When traditional price-volume relationships collapse

Volatility Clustering Failure: When volatility patterns lose their predictive power

Microstructure Stress: When market efficiency mechanisms begin to fail