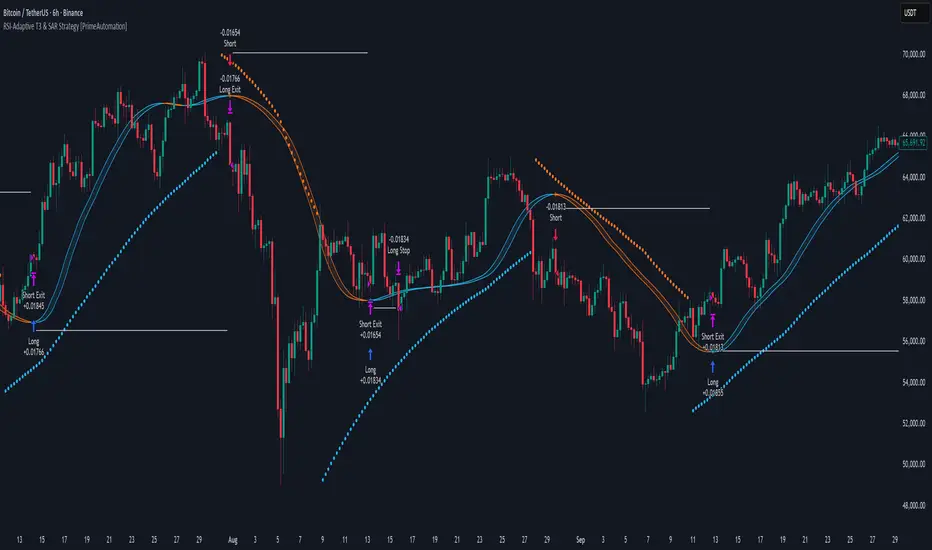

RSI-Adaptive T3 & SAR Strategy [PrimeAutomation]⯁ OVERVIEW

The RSI-Adaptive T3 and SAR Confluence Strategy combines adaptive smoothing with dynamic trend confirmation to identify precise trend reversals and continuation opportunities. It fuses the power of an RSI-based adaptive T3 moving average with the Parabolic SAR filter , aiming to trade in harmony with dominant momentum shifts while maintaining tight control through automatic stop-loss placement.

The RSI-Adaptive T3 is a precision trend-following tool built around the legendary T3 smoothing algorithm developed by Tim Tillson, designed to enhance responsiveness while reducing lag compared to traditional moving averages. Current implementation takes it a step further by dynamically adapting the smoothing length based on real-time RSI conditions — allowing the T3 to “breathe” with market volatility. This dynamic length makes the curve faster in trending moves and smoother during consolidations.

To help traders visualize volatility and directional momentum, adaptive volatility bands are plotted around the T3 line, with visual crossover markers and a dynamic info panel on the chart. It’s ideal for identifying trend shifts, spotting momentum surges, and adapting strategy execution to the pace of the market.

⯁ LOGIC

The T3 moving average length dynamically adjusts based on RSI values — when RSI is high, the smoothing period shortens to react faster; when RSI is low, the period increases for stability in slow markets.

A Parabolic SAR filter confirms directional bias, ensuring trades only occur in alignment with the broader market trend.

Long Entries: Trigger when the T3 curve crosses upward while the current price remains above the SAR — signaling bullish momentum alignment.

Short Entries: Trigger when the T3 crosses downward while the price remains below the SAR — confirming bearish trend alignment.

Stops: Dynamic stops are placed using the highest or lowest price over a set lookback period, adapting automatically to market volatility.

⯁ FEATURES

RSI-Adaptive T3 Filter: Adjusts smoothing in real time to market conditions, blending responsiveness with noise reduction.

SAR Confluence Check: Prevents counter-trend entries by confirming momentum direction via the Parabolic SAR.

Automatic Stop Placement: Uses recent highs or lows as stop-loss anchors, minimizing risk exposure.

Color-coded Visualization: The T3 line dynamically changes color based on slope direction, making momentum shifts visually intuitive.

Smoothed Trend Structure: Reduces market noise, allowing cleaner, more reliable trend recognition across different assets.

⯁ CONCLUSION

The RSI-Adaptive T3 and SAR Confluence Strategy delivers an advanced fusion of adaptive smoothing and structural confirmation. By combining RSI-driven reactivity with Parabolic SAR trend validation, this strategy offers a balanced approach to identifying sustainable momentum reversals while maintaining strong risk management through automatic stop levels. Ideal for traders who seek precision entries aligned with adaptive trend dynamics.

在腳本中搜尋"algo"

ILM & IFVG StrategyPlease feel free to adjust in any way possible. Let me know if you can create something better from this initial coding.

//═══════════════════════════════════════════════════════════════════════

// Inverted Liquidity Model (ILM) – Strategy

//═══════════════════════════════════════════════════════════════════════

//

// The **Inverted Liquidity Model (ILM)** is a liquidity-based algorithm

// built to capture high-probability reversals after:

//

// • A liquidity sweep (SSL/BSL taken)

// • Rejection back inside the range

// • A Fair Value Gap (FVG) forms

// • That FVG becomes invalidated → becomes an IFVG entry zone

//

// ILM combines:

// • LTF BOS / CHOCH structure confirmation

// • HTF structure (expansion) filtering

// • Premium / Discount filter (17:00 CST session midline)

// • Optional ATR volatility filter

// • Optional trading session restrictions

// • Optional partial profit-taking + runners

//

// When all conditions align, the strategy enters:

// ✔ Long after sweep of SSL + valid long IFVG + trend confirmation

// ✔ Short after sweep of BSL + valid short IFVG + trend confirmation

//

// Stops are placed at the sweep wick.

// Full target is set at the next structural high/low.

// Optional partial TP sends a runner to full target.

//

// Visual tools (labels, sweep lines, IFVG boxes, midline) assist

// with review and forward testing.

//

//───────────────────────────────────────────────────────────────────────

// USER CONFIGURABLE FEATURES

//───────────────────────────────────────────────────────────────────────

//

// • **Liquidity & Structure**

// - pivotLen → swing length for pivots / liquidity

// - htfOn → toggle higher-timeframe pivots

// - htfTF → timeframe for HTF structure/liquidity

// - useStructureFilter → enforce LTF BOS/CHOCH trend

// - useHtfExpansionFilter → enforce HTF trend

// - showStructureLabels → show BOS/CHOCH labels

// - showHtfStructureLabels → show HTF BOS/CHOCH labels

//

// • **Premium / Discount Midline**

// - usePremiumDiscountFilter → only long in discount / short in premium

// - pdSession → session used for midline (default 17:00 CST)

// - showPdMidLine → show 50% midline

//

// • **FVG / IFVG Detection**

// - useBodyGapFVG → FVG uses candle bodies instead of wicks

// - useDisplacementFVG → require displacement bar

// - dispAtrMult → minimum ATR threshold for displacement

// - showIFVG → draw IFVG boxes

//

// • **ATR / Volatility / Sessions**

// - useRangeFilter → require minimum ATR%

// - atrLen → ATR period

// - minAtrPerc → minimum ATR% of price

// - useSessionFilter → restrict trading hours

// - sessionTimes → allowed trading session

//

// • **Sweep Visualization**

// - showSweepLines → draw sweep lines at SSL/BSL sweeps

// - sweepLineWidth → thickness of sweep lines

//

// • **Exits: Partial Targets & Runners**

// - usePartialTargets → enable partial TP logic

// - tp1QtyPercent → percent closed at TP1

// - tp1FractionOfPath → TP1 relative to path to full target

//

// • **Formatting / Visibility**

// - labelFontSizeInput → tiny / small / normal / large / huge

// - showEntries → entry markers

// - showTargets → target lines

//

//═══════════════════════════════════════════════════════════════════════

// END OF STRATEGY DESCRIPTION

//═══════════════════════════════════════════════════════════════════════

Moving Average Band StrategyOverview

The Moving Average Band Strategy is a fully customizable breakout and trend-continuation system designed for traders who need both simplicity and control.

The strategy creates adaptive bands around a user-selected moving average and executes trades when price breaks out of these bands, with advanced risk-management settings including optional Risk:Reward targets.

This script is suitable for intraday, swing, and positional traders across all markets — equities, futures, crypto, and forex.

Key Features

✔ Six Moving Average Types

Choose the MA that best matches your trading style:

SMA

EMA

WMA

HMA

VWMA

RMA

✔ Dynamic Bands

Upper Band built from MA of highs

Lower Band built from MA of lows

Adjustable band offset (%)

Color-coded band fill indicating price position

✔ Configurable Strategy Preferences

Toggle Long and/or Short trades

Toggle Risk:Reward Take-Profit

Adjustable Risk:Reward Ratio

Default position sizing: % of equity (configurable via strategy settings)

Entry Conditions

Long Entry

A long trade triggers when:

Price crosses above the Upper Band

Long trades are enabled

No existing long position is active

Short Entry

A short trade triggers when:

Price crosses below the Lower Band

Short trades are enabled

No existing short position is active

Clear entry markers and price labels appear on the chart.

Risk Management

This strategy includes a complete set of risk-controls:

Stop-Loss (Fixed at Entry)

Long SL: Lower Band

Short SL: Upper Band

These levels remain constant for the entire trade.

Optional Risk:Reward Take-Profit

Enabled/disabled using a toggle switch.

When enabled:

Long TP = Entry + (Risk × Risk:Reward Ratio)

Short TP = Entry – (Risk × Risk:Reward Ratio)

When disabled:

Exits are handled by reverse crossover signals.

Exit Conditions

Long Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Short Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Exit markers and price labels are plotted automatically.

Visual Tools

To improve clarity:

Upper & Lower Band (blue, adjustable width)

Middle Line

Dynamic band fill (green/red/yellow)

SL & TP line plotting when in position

Entry/Exit markers

Price labels for all executed trades

These are built to help users visually follow the strategy logic.

Alerts Included

Every trading event is covered:

Long Entry

Short Entry

Long SL / TP / Cross Exit

Short SL / TP / Cross Exit

Combined Alert for webhook/automation (JSON-formatted)

Perfect for algo trading, Discord bots, or automation platforms.

Best For

This strategy performs best in:

Trending markets

Breakout environments

High-momentum instruments

Clean intraday swings

Works seamlessly on:

Stocks

Index futures

Commodities

Crypto

Forex

⚠️ Important Disclaimer

This script is for educational purposes only.

Trading involves risk. Backtest results are not indicative of future performance.

Always validate settings and use proper position sizing.

Ajay R5.41🔻 Ajay Gold 3H Power Indicator 🔻

Precision-Based Smart Sell System for Gold (XAU/USD)

💡 Overview

This indicator is specifically designed for Gold (XAU/USD) and delivers best results on the 3-Hour Timeframe (3H TF).

It is a Smart Money Logic-based Sell Confirmation System, combining institutional structure and candle behavior to generate highly accurate bearish signals.

⚙️ Technical Foundation

The indicator uses multiple advanced confirmations:

📉 EMA Trend Filter → Confirms downtrend

💪 RSI Overbought Rejection → Momentum reversal signal

📊 MACD Bearish Cross → Confirms trend strength

🕯️ Bearish Candle Structure → Price action validation

When all conditions align, a clear 🔻 Sell Signal is plotted on the chart.

💎 Hidden Feature

This indicator includes a hidden feature that activates only when the correct market structure forms.

It helps reduce false signals and increases accuracy without being visible on the chart — fully automated internal logic.

📆 Recommended Settings

Symbol: XAU/USD (Gold)

Timeframe: 3-Hour (3H)

Market: Forex / Commodity

Mode: Sell-Only Confirmation Indicator

Performance: Best precision and consistency on 3H TF

📈 How to Use

Select XAU/USD on chart and set 3H timeframe.

Add the indicator to the chart.

Wait for the 🔻 Sell Signal and confirm the market structure after candle close.

Take entry according to your risk management.

⚠️ Disclaimer

This indicator is for educational and analytical purposes only.

No system is 100% accurate — always backtest and demo trade before using in real trading.

💬 Credits

Developed by Ajay Sahu (India)

Based on Institutional & Smart Money Logic

Best results on 3H TF

Hidden Algorithm for XAU/USD traders

Long-only Swing/Scalp (anchored exits + TP harness) Traders PostThis is the Traders Post friendly drag and drop version of the swing/ scalp strategy for the algo traders out there. Let me know your thoughts, constructive criticism is always welcome.

Ajay Nayak - EMA ATR Trailinge strategy RSI aur RSI ke SMA ke crossover par CALL aur PUT signal generate karti hai.

Saath me ATR based stoploss aur crossover target bhi diya gaya hai.

Algo trading ke liye useful hai.

Twin Range Filter StrategyClarity Over Confusion: See price action through a全新的 lens. Watch as erratic, choppy movements are smoothed into a clear, actionable trajectory. The path of least resistance becomes obvious.

Confidence Over Hesitation: Receive high-probability entry and exit signals with a proven logic that waits for the market to commit before you do. No more second-guessing.

Discipline Over Emotion: Our algorithm enforces a systematic approach, helping you avoid emotional FOMO chasing and panic selling. Stick to the plan and execute with precision.

What Can You Expect?

Dynamic Adaptability: Unlike static indicators, continuously adapts to volatility. It widens its filter in turbulent markets to avoid whipsaws and tightens it in trending markets to capture more of the move.

The Power of Two: By synthesizing data from two distinct market perspectives, it confirms strength and filters out weakness, providing a confluence that standalone indicators simply cannot match.

Clean, Unambiguous Signals: We’ve eliminated the clutter. The software provides clear visual alerts (Green Arrows for Long, Red Arrows for Short) right on your chart, telling you exactly when the equilibrium has shifted.

Who is this for?

Swing Traders looking to capture the heart of a trend and avoid false breakouts.

Day Traders needing a reliable filter to navigate volatile intraday action.

Systematic Traders seeking a robust logic layer to add to their automated strategy.

Anyone overwhelmed by indicator overload and craving a single, trusted source of truth on their chart

AYUSH ALGO TRAGING STRATEGY TEST VERSION 1)Very good strategy , it uses two moving avg crossovers and also rsi and atr for confirmation, this strategy is fully automated

Institution Accumulation/DistributionLeveraging the Williams%R oscillator, the script has been optimized to pick out key turning point in the market specifically at Resistance (Overbought) or Support (Oversold)

The algo has been programmed to print both buy and sell alerts at extremes/when conditions flip eg a long position will be closed simultaneously opening a short position above resistance.

Best used as a scalping tool targeting 30m and below works well with currency pairs

SuperTrend Strategy with Trend-Based Exits🟩 SuperTrend Strategy with Trend-Based Exits

This is a fully automated trend-following strategy based on the popular SuperTrend indicator, enhanced with a position sizing algorithm tied to stop-loss distance and dynamic entry/exit rules. The strategy is designed for futures trading with an emphasis on sustainable risk, realistic backtesting, and transparent logic.

🧠 Concept and Methodology

The strategy uses the SuperTrend indicator, which is derived from ATR (Average True Range) and is widely used to capture medium- to long-term market trends.

Key features:

✅ Entries are triggered only when the SuperTrend direction changes (trend reversal).

✅ Exits are performed using a dynamic stop-loss placed at the SuperTrend line.

✅ Position size is automatically calculated based on the trader’s fixed dollar risk per trade and the current distance to the stop-loss.

✅ Rounding logic is included to ensure quantity is valid for the exchange’s lot size.

This strategy does not use any take-profit or classic trailing stop — the position is only closed when the trend reverses or the stop is hit by touching the SuperTrend line.

⚙️ Default Parameters

ATR Length: 300

Factor: 7.5

Risk per trade: $90 (3% of the default $3,000 capital)

Lot step: 10

Commission: 0.05%

These default parameters are not universal. They were optimized specifically for STXUSDT swap at 15M timeframe at Bybit and may not produce viable results on other pairs and timeframes.

Users are encouraged to customize the settings according to specific asset’s volatility, timeframe and other characteristics.

❗ These default settings yield meaningful backtesting results on STXUSDT with a reasonable number of trades (105+) over 7-month period. If applied to other assets, results may vary significantly.

📈 Position Sizing Logic

The strategy uses a dynamic position sizing formula:

Pine Script®

position_size = floor((risk_per_trade / stop_loss_distance) / lot_step) * lot_step

This ensures the trader always risks a fixed dollar amount per trade and never exceeds a sustainable equity exposure (recommended 2% or less).

✅ Realism in Backtesting

To ensure realistic and non-misleading backtest results, this strategy includes:

— Slippage and commission settings matching average exchange conditions (commission = 0.05%, slippage 5 ticks).

— Position sizing based on stop-loss distance (not fixed contract quantity).*

— A fixed risk-per-trade model that adheres to responsible capital management principles.

— This is in compliance with TradingView's Script publishing rules and House Rules.

📌 How to Use

Apply the strategy to a clean chart (preferably 15M for STXUSDT by default).

If using another asset, adjust:

- ATR Length

- Factor

- Risk per trade

- Qty step (lot precision for the symbol)

Avoid using with other indicators unless you understand their purpose.

Use the Strategy Tester to evaluate performance and optimize parameters.

⚠️ Disclaimer

This is not financial advice. Always perform forward testing and assess risk before deploying any strategy on live capital. The strategy is designed for educational and experimental use.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #3 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #4 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST Signal Line Length (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is KST, Williams Alligator, Moving Average, ATR and Choppiness Index.

The KST (Know Sure Thing) is a momentum oscillator developed by Martin Pring. It combines multiple Rate of Change (ROC) values, smoothed over different timeframes, to identify trend direction and momentum strength. First of all, what is ROC? ROC (Rate of Change) is a momentum indicator that measures the percentage change in price between the current price and the price a set number of periods ago.

ROC = 100 * (Current Price - Price N Periods Ago) / Price N Periods Ago

In our case N is the KST ROC Length inputs from settings, here we will calculate 4 different ROCs to obtain KST value:

KST = ROC1_smooth × 1 + ROC2_smooth × 2 + ROC3_smooth × 3 + ROC4_smooth × 4

ROC1 = ROC(close, KST ROC Length #1), smoothed by KST SMA Length #1,

ROC2 = ROC(close, KST ROC Length #2), smoothed by KST SMA Length #2,

ROC3 = ROC(close, KST ROC Length #3), smoothed by KST SMA Length #3,

ROC4 = ROC(close, KST ROC Length #4), smoothed by KST SMA Length #4

Also for this indicator the signal line is calculated:

Signal = SMA(KST, KST Signal Line Length)

When the KST line rises, it indicates increasing momentum and suggests that an upward trend may be developing. Conversely, when the KST line declines, it reflects weakening momentum and a potential downward trend. A crossover of the KST line above its signal line is considered a buy signal, while a crossover below the signal line is viewed as a sell signal. If the KST stays above zero, it indicates overall bullish momentum; if it remains below zero, it points to bearish momentum. The KST indicator smooths momentum across multiple timeframes, helping to reduce noise and provide clearer signals for medium- to long-term trends.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

The next indicator is Moving Average. It has a lot of different types which can be chosen to filter trades and the Least Squares MA is used by default settings. Let's briefly explain what is it.

The Least Squares Moving Average (LSMA) — also known as Linear Regression Moving Average — is a trend-following indicator that uses the least squares method to fit a straight line to the price data over a given period, then plots the value of that line at the most recent point. It draws the best-fitting straight line through the past N prices (using linear regression), and then takes the endpoint of that line as the value of the moving average for that bar. The LSMA aims to reduce lag and highlight the current trend more accurately than traditional moving averages like SMA or EMA.

Key Features:

It reacts faster to price changes than most moving averages.

It is smoother and less noisy than short-term EMAs.

It can be used to identify trend direction, momentum, and potential reversal points.

ATR (Average True Range) is a volatility indicator that measures how much an asset typically moves during a given period. It was introduced by J. Welles Wilder and is widely used to assess market volatility, not direction.

To calculate it first of all we need to get True Range (TR), this is the greatest value among:

High - Low

abs(High - Previous Close)

abs(Low - Previous Close)

ATR = MA(TR, n) , where n is number of periods for moving average, in our case equals 14.

ATR shows how much an asset moves on average per candle/bar. A higher ATR means more volatility; a lower ATR means a calmer market.

The Choppiness Index is a technical indicator that quantifies whether the market is trending or choppy (sideways). It doesn't indicate trend direction — only the strength or weakness of a trend. Higher Choppiness Index usually approximates the sideways market, while its low value tells us that there is a high probability of a trend.

Choppiness Index = 100 × log10(ΣATR(n) / (MaxHigh(n) - MinLow(n))) / log10(n)

where:

ΣATR(n) = sum of the Average True Range over n periods

MaxHigh(n) = highest high over n periods

MinLow(n) = lowest low over n periods

log10 = base-10 logarithm

Now let's understand how these indicators work in conjunction and why they were chosen for this strategy. KST indicator approximates current momentum, when it is rising and KST line crosses over the signal line there is high probability that short term trend is reversing to the upside and strategy allows to take part in this potential move. Alligator's jaw (blue) line is used as an approximation of a short term trend, taking trades only above it we want to avoid trading against trend to increase probability that long trade is going to be winning.

Almost the same for Moving Average, but it approximates the long term trend, this is just the additional filter. If we trade in the direction of the long term trend we increase probability that higher risk to reward trade will hit the take profit. Choppiness index is the optional filter, but if it turned on it is used for approximating if now market is in sideways or in trend. On the range bounded market the potential moves are restricted. We want to decrease probability opening trades in such condition avoiding trades if this index is above threshold value.

When trade is open script sets the stop loss and take profit targets. ATR approximates the current volatility, so we can make a decision when to exit a trade based on current market condition, it can increase the probability that strategy will avoid the excessive stop loss hits, but anyway user can setup how many ATRs to use as a stop loss and take profit target. As was said in the Methodology stop loss level is obtained by subtracting number of ATRs from trade opening candle low, while take profit by adding to this candle's close.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2025.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 60%

Maximum Single Position Loss: -5.53%

Maximum Single Profit: +8.35%

Net Profit: +5175.20 USDT (+51.75%)

Total Trades: 120 (56.67% win rate)

Profit Factor: 1.747

Maximum Accumulated Loss: 1039.89 USDT (-9.1%)

Average Profit per Trade: 43.13 USDT (+0.6%)

Average Trade Duration: 27 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 1h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrexio commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation.

Smart Fib StrategySmart Fibonacci Strategy

This advanced trading strategy combines the power of adaptive SMA entries with Fibonacci-based exit levels to create a comprehensive trend-following system that self-optimizes based on historical market conditions. Credit goes to Julien_Eche who created the "Best SMA Finder" which received an Editors Pick award.

Strategy Overview

The Smart Fibonacci Strategy employs a two-pronged approach to trading:

1. Intelligent Entries: Uses a self-optimizing SMA (Simple Moving Average) to identify optimal entry points. The system automatically tests multiple SMA lengths against historical data to determine which period provides the most robust trading signals.

2. Fibonacci-Based Exits: Implements ATR-adjusted Fibonacci bands to establish precise exit targets, with risk-management options ranging from conservative to aggressive.

This dual methodology creates a balanced system that adapts to changing market conditions while providing clear visual reference points for trade management.

Key Features

- **Self-Optimizing Entries**: Automatically calculates the most profitable SMA length based on historical performance

- **Adjustable Risk Parameters**: Choose between low-risk and high-risk exit targets

- **Directional Flexibility**: Trade long-only, short-only, or both directions

- **Visualization Tools**: Customizable display of entry lines and exit bands

- **Performance Statistics**: Comprehensive stats table showing key metrics

- **Smoothing Option**: Reduces noise in the Fibonacci bands for cleaner signals

Trading Rules

Entry Signals

- **Long Entry**: When price crosses above the blue center line (optimal SMA)

- **Short Entry**: When price crosses below the blue center line (optimal SMA)

### Exit Levels

- **Low Risk Option**: Exit at the first Fibonacci band (1.618 * ATR)

- **High Risk Option**: Exit at the second Fibonacci band (2.618 * ATR)

Strategy Parameters

Display Settings

- Toggle visibility of the stats table and indicator components

Strategy Settings

- Select trading direction (long, short, or both)

- Choose exit method (low risk or high risk)

- Set minimum trades threshold for SMA optimization

SMA Settings

- Option to use auto-optimized or fixed-length SMA

- Customize SMA length when using fixed option

Fibonacci Settings

- Adjust ATR period and SMA basis for Fibonacci bands

- Enable/disable smoothing function

- Customize Fibonacci ratio multipliers

Appearance Settings

- Modify colors, line widths, and transparency

Optimization Methodology

The strategy employs a sophisticated optimization algorithm that:

1. Tests multiple SMA lengths against historical data

2. Evaluates performance based on trade count, profit factor, and win rate

3. Calculates a "robustness score" that balances profitability with statistical significance

4. Selects the SMA length with the highest robustness score

This ensures that the strategy's entry signals are continuously adapting to the most effective parameters for current market conditions.

Risk Management

Position sizing is fixed at $2,000 per trade, allowing for consistent exposure across all trading setups. The Fibonacci-based exit system provides two distinct risk management approaches:

- **Conservative Approach**: Using the first Fibonacci band for exits produces more frequent but smaller wins

- **Aggressive Approach**: Using the second Fibonacci band allows for larger potential gains at the cost of increased volatility

Ideal Usage

This strategy is best suited for:

- Trending markets with clear directional moves

- Timeframes from 4H to Daily for most balanced results

- Instruments with moderate volatility (stocks, forex, commodities)

Traders can further enhance performance by combining this strategy with broader market analysis to confirm the prevailing trend direction.

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

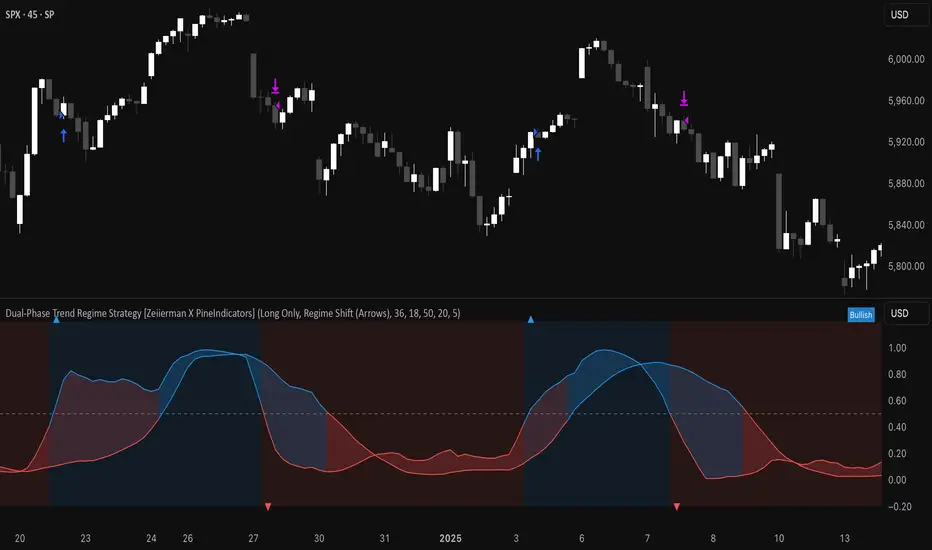

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

External Signals Strategy Tester v5External Signals Strategy Tester v5 – User Guide (English)

1. Purpose

This Pine Script strategy is a universal back‑tester that lets you plug in any external buy/sell series (for example, another indicator, webhook feed, or higher‑time‑frame condition) and evaluate a rich set of money‑management rules around it – with a single click on/off workflow for every module.

2. Core Workflow

Feed signals

Buy Signal / Sell Signal inputs accept any series (price, boolean, output of request.security(), etc.).

A crossover above 0 is treated as “signal fired”.

Date filter

Start Date / End Date restricts the test window so you can exclude unwanted history.

Trade engine

Optional Long / Short enable toggles.

Choose whether opposite signals simply close the trade or reverse it (flip direction in one transaction).

Risk modules – all opt‑in via check‑boxes

Classic % block – fixed % Take‑Profit / Stop‑Loss / Break‑Even.

Fibonacci Bollinger Bands (FBB) module

Draws dynamic VWMA/HMA/SMA/EMA/DEMA/TEMA mid‑line with ATR‑scaled Fibonacci envelopes.

Every line can be used for stops, trailing, or multi‑target exits.

Separate LONG and SHORT sub‑modules

Each has its own SL plus three Take‑Profits (TP1‑TP3).

Per TP you set line, position‑percentage to close, and an optional trailing flag.

Executed TP/SLs deactivate themselves so they cannot refire.

Trailing behaviour

If Trail is checked, the selected line is re‑evaluated once per bar; the order is amended via strategy.exit().

3. Inputs Overview

Group Parameter Notes

Trade Settings Enable Long / Enable Short Master switches

Close on Opposite / Reverse Position How to react to a counter‑signal

Risk % Use TP / SL / BE + their % Traditional fixed‑distance management

Fibo Bands FIBO LEVELS ENABLE + visual style/length Turn indicator overlay on/off

FBB LONG SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a long is open

FBB SHORT SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a short is open

Line choices: Basis, 0.236, 0.382, 0.5, 0.618, 0.764, 1.0 – long rules use lower bands, short rules use upper bands automatically.

4. Algorithm Details

Position open

On the very first bar after entry, the script checks the direction and activates the corresponding LONG or SHORT module, deactivating the other.

Order management loop (every bar)

FBB Stop‑Loss: placed/updated at chosen band; if trailing, follows the new value.

TP1‑TP3: each active target updates its limit price to the selected band (or holds static if trailing is off).

The classic % block runs in parallel; its exits have priority because they call strategy.close_all().

Exit handling

When any strategy.exit() fires, the script reads exit_id and flips the *_Active flag so that order will not be recreated.

A Stop‑Loss (SL) also disables all remaining TPs for that leg.

5. Typical Use Cases

Scenario Suggested Setup

Scalping longs into VWAP‐reversion Enable LONG TP1 @ 0.382 (30 %), TP2 @ 0.618 (40 %), SL @ 0.236 + trailing

Fade shorts during news spikes Enable SHORT SL @ 1.0 (no trail) and SHORT TP1,2,3 on consecutive lowers with small size‑outs

Classic trend‑follow Use only classic % TP/SL block and disable FBB modules

6. Hints & Tips

Signal quality matters – this script manages exits, it does not generate entries.

Keep TV time zone in mind when picking start/end dates.

For portfolio‑style testing allocate smaller default_qty_value than 100 % or use strategy.percent_of_equity sizing.

You can combine FBB exits with fixed‑% ones for layered management.

7. Limitations / Safety

No pyramiding; the script holds max one position at a time.

All calculations are bar‑close; intra‑bar touches may differ from real‑time execution.

The indicator overlay is optional, so you can run visual‑clean tests by unchecking FIBO LEVELS ENABLE.

Dskyz (DAFE) MAtrix with ATR-Powered Precision Dskyz (DAFE) MAtrix with ATR-Powered Precision

This cutting‐edge futures trading strategy built to thrive in rapidly changing market conditions. Developed for high-frequency futures trading on instruments such as the CME Mini MNQ, this strategy leverages a matrix of sophisticated moving averages combined with ATR-based filters to pinpoint high-probability entries and exits. Its unique combination of adaptable technical indicators and multi-timeframe trend filtering sets it apart from standard strategies, providing enhanced precision and dynamic responsiveness.

imgur.com

Core Functional Components

1. Advanced Moving Averages

A distinguishing feature of the DAFE strategy is its robust, multi-choice moving averages (MAs). Clients can choose from a wide array of MAs—each with specific strengths—in order to fine-tune their trading signals. The code includes user-defined functions for the following MAs:

imgur.com

Hull Moving Average (HMA):

The hma(src, len) function calculates the HMA by using weighted moving averages (WMAs) to reduce lag considerably while smoothing price data. This function computes an intermediate WMA of half the specified length, then a full-length WMA, and finally applies a further WMA over the square root of the length. This design allows for rapid adaptation to price changes without the typical delays of traditional moving averages.

Triple Exponential Moving Average (TEMA):

Implemented via tema(src, len), TEMA uses three consecutive exponential moving averages (EMAs) to effectively cancel out lag and capture price momentum. The final formula—3 * (ema1 - ema2) + ema3—produces a highly responsive indicator that filters out short-term noise.

Double Exponential Moving Average (DEMA):

Through the dema(src, len) function, DEMA calculates an EMA and then a second EMA on top of it. Its simplified formula of 2 * ema1 - ema2 provides a smoother curve than a single EMA while maintaining enhanced responsiveness.

Volume Weighted Moving Average (VWMA):

With vwma(src, len), this MA accounts for trading volume by weighting the price, thereby offering a more contextual picture of market activity. This is crucial when volume spikes indicate significant moves.

Zero Lag EMA (ZLEMA):

The zlema(src, len) function applies a correction to reduce the inherent lag found in EMAs. By subtracting a calculated lag (based on half the moving average window), ZLEMA is exceptionally attuned to recent price movements.

Arnaud Legoux Moving Average (ALMA):

The alma(src, len, offset, sigma) function introduces ALMA—a type of moving average designed to be less affected by outliers. With parameters for offset and sigma, it allows customization of the degree to which the MA reacts to market noise.

Kaufman Adaptive Moving Average (KAMA):

The custom kama(src, len) function is noteworthy for its adaptive nature. It computes an efficiency ratio by comparing price change against volatility, then dynamically adjusts its smoothing constant. This results in an MA that quickly responds during trending periods while remaining smoothed during consolidation.

Each of these functions—integrated into the strategy—is selectable by the trader (via the fastMAType and slowMAType inputs). This flexibility permits the tailored application of the MA most suited to current market dynamics and individual risk management preferences.

2. ATR-Based Filters and Risk Controls

ATR Calculation and Volatility Filter:

The strategy computes the Average True Range (ATR) over a user-defined period (atrPeriod). ATR is then used to derive both:

Volatility Assessment: Expressed as a ratio of ATR to closing price, ensuring that trades are taken only when volatility remains within a safe, predefined threshold (volatilityThreshold).

ATR-Based Entry Filters: Implemented as atrFilterLong and atrFilterShort, these conditions ensure that for long entries the price is sufficiently above the slow MA and vice versa for shorts. This acts as an additional confirmation filter.

Dynamic Exit Management:

The exit logic employs a dual approach:

Fixed Stop and Profit Target: Stops and targets are set at multiples of ATR (fixedStopMultiplier and profitTargetATRMult), helping manage risk in volatile markets.

Trailing Stop Adjustments: A trailing stop is calculated using the ATR multiplied by a user-defined offset (trailOffset), which captures additional profits as the trade moves favorably while protecting against reversals.

3. Multi-Timeframe Trend Filtering

The strategy enhances its signal reliability by leveraging a secondary, higher timeframe analysis:

15-Minute Trend Analysis:

By retrieving 15-minute moving averages (fastMA15m and slowMA15m) via request.security, the strategy determines the broader market trend. This secondary filter (enabled or disabled through useTrendFilter) ensures that entries are aligned with the prevailing market direction, thereby reducing the incidence of false signals.

4. Signal and Execution Logic

Combined MA Alignment:

The entry conditions are based primarily on the alignment of the fast and slow MAs. A long condition is triggered when the current price is above both MAs and the fast MA is above the slow MA—complemented by the ATR filter and volume conditions. The reverse applies for a short condition.

Volume and Time Window Validation:

Trades are permitted only if the current volume exceeds a minimum (minVolume) and the current hour falls within the predefined trading window (tradingStartHour to tradingEndHour). An additional volume spike check (comparing current volume to a moving average of past volumes) further filters for optimal market conditions.

Comprehensive Order Execution:

The strategy utilizes flexible order execution functions that allow pyramiding (up to 10 positions), ensuring that it can scale into positions as favorable conditions persist. The use of both market entries and automated exits (with profit targets, stop-losses, and trailing stops) ensures that risk is managed at every step.

5. Integrated Dashboard and Metrics

For transparency and real-time analysis, the strategy includes:

On-Chart Visualizations:

Both fast and slow MAs are plotted on the chart, making it easy to see the market’s technical foundation.

Dynamic Metrics Dashboard:

A built-in table displays crucial performance statistics—including current profit/loss, equity, ATR (both raw and as a percentage), and the percentage gap between the moving averages. These metrics offer immediate insight into the health and performance of the strategy.

Input Parameters: Detailed Breakdown

Every input is meticulously designed to offer granular control:

Fast & Slow Lengths:

Determine the window size for the fast and slow moving averages. Smaller values yield more sensitivity, while larger values provide a smoother, delayed response.

Fast/Slow MA Types:

Choose the type of moving average for fast and slow signals. The versatility—from basic SMA and EMA to more complex ones like HMA, TEMA, ZLEMA, ALMA, and KAMA—allows customization to fit different market scenarios.

ATR Parameters:

atrPeriod and atrMultiplier shape the volatility assessment, directly affecting entry filters and risk management through stop-loss and profit target levels.

Trend and Volume Filters:

Inputs such as useTrendFilter, minVolume, and the volume spike condition help confirm that a trade occurs in active, trending markets rather than during periods of low liquidity or market noise.

Trading Hours:

Restricting trade execution to specific hours (tradingStartHour and tradingEndHour) helps avoid illiquid or choppy markets outside of prime trading sessions.

Exit Strategies:

Parameters like trailOffset, profitTargetATRMult, and fixedStopMultiplier provide multiple layers of risk management and profit protection by tailoring how exits are generated relative to current market conditions.

Pyramiding and Fixed Trade Quantity:

The strategy supports multiple entries within a trend (up to 10 positions) and sets a predefined trade quantity (fixedQuantity) to maintain consistent exposure and risk per trade.

Dashboard Controls:

The resetDashboard input allows for on-the-fly resetting of performance metrics, keeping the strategy’s performance dashboard accurate and up-to-date.

Why This Strategy is Truly Exceptional

Multi-Faceted Adaptability:

The ability to switch seamlessly between various moving average types—each suited to particular market conditions—enables the strategy to adapt dynamically. This is a testament to the high level of coding sophistication and market insight infused within the system.

Robust Risk Management:

The integration of ATR-based stops, profit targets, and trailing stops ensures that every trade is executed with well-defined risk parameters. The system is designed to mitigate unexpected market swings while optimizing profit capture.

Comprehensive Market Filtering:

By combining moving average crossovers with volume analysis, volatility thresholds, and multi-timeframe trend filters, the strategy only enters trades under the most favorable conditions. This multi-layered filtering reduces noise and enhances signal quality.

-Final Thoughts-

The Dskyz Adaptive Futures Elite (DAFE) MAtrix with ATR-Powered Precision strategy is not just another trading algorithm—it is a multi-dimensional, fully customizable system built on advanced technical principles and sophisticated risk management techniques. Every function and input parameter has been carefully engineered to provide traders with a system that is both powerful and transparent.

For clients seeking a state-of-the-art trading solution that adapts dynamically to market conditions while maintaining strict discipline in risk management, this strategy truly stands in a class of its own.

****Please show support if you enjoyed this strategy. I'll have more coming out in the near future!!

-Dskyz

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

Buy on 5% dip strategy with time adjustment

This script is a strategy called "Buy on 5% Dip Strategy with Time Adjustment 📉💡," which detects a 5% drop in price and triggers a buy signal 🔔. It also automatically closes the position once the set profit target is reached 💰, and it has additional logic to close the position if the loss exceeds 14% after holding for 230 days ⏳.

Strategy Explanation

Buy Condition: A buy signal is triggered when the price drops 5% from the highest price reached 🔻.

Take Profit: The position is closed when the price hits a 1.22x target from the average entry price 📈.

Forced Sell Condition: If the position is held for more than 230 days and the loss exceeds 14%, the position is automatically closed 🚫.

Leverage & Capital Allocation: Leverage is adjustable ⚖️, and you can set the percentage of capital allocated to each trade 💸.

Time Limits: The strategy allows you to set a start and end time ⏰ for trading, making the strategy active only within that specific period.

Code Credits and References

Credits: This script utilizes ideas and code from @QuantNomad and jangdokang for the profit table and algorithm concepts 🔧.

Sources:

Monthly Performance Table Script by QuantNomad:

ZenAndTheArtOfTrading's Script:

Strategy Performance

This strategy provides risk management through take profit and forced sell conditions and includes a performance table 📊 to track monthly and yearly results. You can compare backtest results with real-time performance to evaluate the strategy's effectiveness.

The performance numbers shown in the backtest reflect what would have happened if you had used this strategy since the launch date of the SOXL (the Direxion Daily Semiconductor Bull 3x Shares ETF) 📅. These results are not hypothetical but based on actual performance from the day of the ETF’s launch 📈.

Caution ⚠️

No Guarantee of Future Results: The results are based on historical performance from the launch of the SOXL ETF, but past performance does not guarantee future results. It’s important to approach with caution when applying it to live trading 🔍.

Risk Management: Leverage and capital allocation settings are crucial for managing risk ⚠️. Make sure to adjust these according to your risk tolerance ⚖️.

Dynamic Breakout Master by tradingbauhaus 🌟 Code Description:

This Pine Script implements a trading strategy called "Dynamic Breakout Master" 💥. The core idea of the strategy is to identify breakouts (price movements) at key support 💙 and resistance 🔴 levels, through a dynamic channel that adapts to the market’s conditions. Here's how it works:

🔧 Customizable Input Parameters:

🧭 Pivot Period: This defines the number of bars (candles) to the left and right used to detect pivots (highs and lows) that mark the support and resistance zones.

📊 Data Source: You can choose whether to use highs and lows or closes and opens of the candles to identify the pivots.

📏 Max Channel Width: Specifies the maximum width allowed for the support/resistance channel, expressed as a percentage over the last 300 bars.

💪 Minimum Pivot Strength: This defines the minimum number of pivots needed for a support or resistance level to be considered valid.

🏔 Max Support/Resistance Zones: Limits the number of key zones displayed on the chart.

📅 Lookback Period: Adjusts how many bars back the system should check to find and validate support and resistance levels.

🎨 Custom Colors: You can choose colors for the support, resistance, and in-channel zones.

📉 Moving Averages (MA): The strategy allows adding up to two moving averages (SMA or EMA) to assist in making trading decisions.

📊 Calculating Support/Resistance Levels:

The system uses an algorithm to identify pivots from prices and calculates dynamic support and resistance zones 🔒🔓.

The closer the pivots are and the stronger their influence, the more relevant the zone becomes for the strategy.

The dynamic channel is drawn on the chart, with a maximum width limit for these zones defined by the input parameter.

📈 Trading Logic:

🚀 Identifying Breakouts:

The strategy looks for when the price breaks (breakouts) a resistance or support level.

If the price breaks upward through the resistance level, a buy order 📈 is triggered.

If the price breaks downward through the support level, a sell order 📉 is triggered.

🔔 Alerts:

Resistance Break (ResBreak) and Support Break (SupBreak) alerts are configured to notify users when a significant breakout occurs.

💰 Commissions:

The strategy includes a commission (0.1%) to simulate transaction costs for each trade.

📊 Chart Visualization:

The support and resistance zones are displayed as colored rectangles:

🔴 Resistance (red) and

🔵 Support (blue).

Pivots of support and resistance can be labeled as P (for resistance) and V (for support).

Breakouts of support or resistance levels are marked with triangles that appear on the chart 🔺🔻.

📈 Trading Strategy:

If the price breaks upward through the resistance level, a long position (buy) 📈 is opened.

If the price breaks downward through the support level, a short position (sell) 📉 is opened.

🏆 Conclusion:

This script is a dynamic breakout strategy 💥 that allows traders to capture significant price movements when support or resistance channels break. The customizable parameters let users fine-tune the strategy according to their preferences, while the visual alerts on the chart make it easier to follow trading opportunities. The inclusion of moving averages and key price zones adds an extra layer of analysis to improve decision-making 💡.

Autonomous 5-Minute RobotKey Components of the Strategy:

Trend Detection:

A 50-period simple moving average (SMA) is used to define the market trend. If the current close is above the SMA, the market is considered to be in an uptrend (bullish), and if it's below, it's considered a downtrend (bearish).

The strategy also looks at the trend over the last 30 minutes (6 candles in a 5-minute chart). The strategy compares the previous close with the current close to detect an uptrend or downtrend.

Volume Analysis:

The strategy calculates buyVolume and sellVolume based on price movement within each candle.

The condition for entering a long position is when the market is in an uptrend, and the buy volume is greater than the sell volume.

The condition for entering a short position is when the market is in a downtrend, and the sell volume is greater than the buy volume.

Trade Execution:

The strategy enters a long position when the trend is up and the buy volume is higher than the sell volume.

The strategy enters a short position when the trend is down and the sell volume is higher than the buy volume.

Positions are closed based on stop-loss and take-profit conditions.

Stop-loss is set at 3% below the entry price.

Take-profit is set at 29% above the entry price.

Exit Conditions:

Long trades will be closed if the price falls 3% below the entry price or rises 29% above the entry price.

Short trades will be closed if the price rises 3% above the entry price or falls 29% below the entry price.

Visuals:

The SMA (50-period) is plotted on the chart to show the trend.

Buy and sell signals are marked with labels on the chart for easy identification.

With this being said this algo is still being worked on to be autonomous

Analyze the Market Direction: Determine whether the market is in an uptrend or downtrend over the past 30 minutes (using the last 6 candles in a 5-minute chart).

Use Trend Indicators and Volume: Implement trend-following indicators like moving averages or the SMA/EMA crossover and consider volume to decide when to enter or exit a trade.

Enter and Exit Trades: The robot will enter long positions when the trend is up and short positions when the trend is down. Additionally, it will close positions based on volume signals and price action (e.g., volume spikes, price reversals).

Adaptive Trend Flow Strategy with Filters for SPXThe Adaptive Trend Flow Strategy with Filters for SPX is a complete trading algorithm designed to identify traits and offer actionable alerts for the SPX index. This Pine Script approach leverages superior technical signs and user-described parameters to evolve to marketplace conditions and optimize performance.

Key Features and Functionality

Dynamic Trend Detection: Utilizes a dual EMA-based totally adaptive method for fashion calculation.

The script smooths volatility the usage of an EMA filter and adjusts sensitivity through the sensitivity enter. This allows for real-time adaptability to market fluctuations.

Trend Filters for Precision:

SMA Filter: A Simple Moving Average (SMA) guarantees that trades are achieved best while the rate aligns with the shifting average trend, minimizing false indicators.

MACD Filter: The Moving Average Convergence Divergence (MACD) adds some other layer of confirmation with the aid of requiring alignment among the MACD line and its sign line.

Signal Generation:

Long Signals: Triggered when the fashion transitions from bearish to bullish, with all filters confirming the pass.

Short Signals: Triggered while the trend shifts from bullish to bearish, imparting opportunities for final positions.

User Customization:

Adjustable parameters for EMAs, smoothing duration, and sensitivity make certain the strategy can adapt to numerous buying and selling patterns.

Enable or disable filters (SMA or MACD) based totally on particular market conditions or consumer possibilities.

Leverage and Position Sizing: Incorporates a leverage aspect for dynamic position sizing.

Automatically calculates the exchange length based on account fairness and the leverage element, making sure hazard control is in area.

Visual Enhancements: Plots adaptive fashion ranges (foundation, top, decrease) for actual-time insights into marketplace conditions.

Color-coded bars and heritage to visually represent bullish or bearish developments.

Custom labels indicating crossover and crossunder occasions for clean sign visualization.

Alerts and Automation: Configurable alerts for each lengthy and quick indicators, well matched with automated buying and selling structures like plugpine.Com.

JSON-based alert messages consist of account credentials, motion type, and calculated position length for seamless integration.

Backtesting and Realistic Assumptions: Includes practical slippage, commissions, and preliminary capital settings for backtesting accuracy.

Leverages excessive-frequency trade sampling to make certain strong strategy assessment.

How It Works

Trend Calculation: The method derives a principal trend basis with the aid of combining fast and gradual EMAs. It then uses marketplace volatility to calculate adaptive upper and decrease obstacles, creating a dynamic channel.

Filter Integration: SMA and MACD filters work in tandem with the fashion calculation to ensure that handiest excessive-probability signals are accomplished.

Signal Execution: Signals are generated whilst the charge breaches those dynamic tiers and aligns with the fashion and filters, ensuring sturdy change access situations.

How to Use

Setup: Apply the approach to SPX or other well suited indices.

Adjust person inputs, together with ATR length, EMA smoothing, and sensitivity, to align together with your buying and selling possibilities.

Enable or disable the SMA and MACD filters to test unique setups.

Alerts: Configure signals for computerized notifications or direct buying and selling execution through third-celebration systems.

Use the supplied JSON payload to integrate with broking APIs or automation tools.

Optimization:

Experiment with leverage, filter out settings, and sensitivity to find most effective configurations to your hazard tolerance and marketplace situations.

Considerations and Best Practices

Risk Management: Always backtest the method with realistic parameters, together with conservative leverage and commissions.

Market Suitability: While designed for SPX, this method can adapt to other gadgets by means of adjusting key parameters.

Limitations: The method is trend-following and can underperform in enormously risky or ranging markets. Regularly evaluate and modify parameters primarily based on recent market conduct.

If you have any questions please let me know - I'm here to help!

DemaRSI StrategyThis is a repost to a old script that cant be updated anymore, the request was made on Feb, 27, 2016.

Here's a engaging description for the tradingview script:

**DemaRSI Strategy: A Proven Trading System**

Join thousands of traders who have already experienced the power of this highly effective strategy. The DemaRSI system combines two powerful indicators - DEMA (Double Exponential Moving Average) and RSI (Relative Strength Index) - to generate profitable trades with minimal risk.

**Key Features:**

* **Trend-Following**: Our algorithm identifies strong trends using a combination of DEMA and RSI, allowing you to ride the waves of market momentum.

* **Risk Management**: The system includes built-in stop-loss and take-profit levels, ensuring that your gains are protected and losses are minimized.

* **Session-Based Trading**: Trade during specific sessions only (e.g., London or New York) for even more targeted results.

* **Customizable Settings**: Adjust the length of moving averages, RSI periods, and other parameters to suit your trading style.

**What You'll Get:**

* A comprehensive strategy that can be used with any broker or platform

* Easy-to-use interface with customizable settings

* Real-time performance metrics and backtesting capabilities

**Start Trading Like a Pro Today!**

This script is designed for intermediate to advanced traders who want to take their trading game to the next level. With its robust risk management features, this strategy can help you achieve consistent profits in various market conditions.

**Disclaimer:** This script is not intended as investment advice and should be used at your own discretion. Trading carries inherent risks, and losses are possible.

~Llama3

MultiLayer Awesome Oscillator Saucer Strategy [Skyrexio]Overview

MultiLayer Awesome Oscillator Saucer Strategy leverages the combination of Awesome Oscillator (AO), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Awesome Oscillator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Awesome Oscillator shall create the "Saucer" long signal (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created "Saucer signal".

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one "Saucer" signal another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's go through all concepts used in this strategy to understand how they works together. Let's start from the easies one, the EMA. Let's briefly explain what is EMA. The Exponential Moving Average (EMA) is a type of moving average that gives more weight to recent prices, making it more responsive to current price changes compared to the Simple Moving Average (SMA). It is commonly used in technical analysis to identify trends and generate buy or sell signals. It can be calculated with the following steps:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy uses EMA an initial long term trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

Let's go to the next, short-term trend filter which consists of Alligator and Fractals. Let's briefly explain what do these indicators means. The Williams Alligator, developed by Bill Williams, is a technical indicator designed to spot trends and potential market reversals. It uses three smoothed moving averages, referred to as the jaw, teeth, and lips:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When these lines diverge and are properly aligned, the "alligator" is considered "awake," signaling a strong trend. Conversely, when the lines overlap or intertwine, the "alligator" is "asleep," indicating a range-bound or sideways market. This indicator assists traders in identifying when to act on or avoid trades.

The Williams Fractals, another tool introduced by Bill Williams, are used to pinpoint potential reversal points on a price chart. A fractal forms when there are at least five consecutive bars, with the middle bar displaying the highest high (for an up fractal) or the lowest low (for a down fractal), relative to the two bars on either side.

Key Points:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often combine fractals with other indicators to confirm trends or reversals, improving the accuracy of trading decisions.