BTC EMA 5-9 Flip Strategy AutobotThis strategy is designed for fast and accurate trend-following trades on Bitcoin.

It uses a crossover between EMA 5 and EMA 9 to detect instant trend reversals and automatically flips between Long and Short positions.

How the strategy works

EMA 5 crossing above EMA 9 → Long

EMA 5 crossing below EMA 9 → Short

Automatically closes the opposite trade during a flip

Executes trades only on candle close

Prevents double entries with internal position-state logic

Fully compatible with automated trading via webhooks (Delta Exchange)

Why this strategy works

EMA 5–9 is extremely responsive for BTC’s volatility

Captures trend reversals early

Works best on 15-minute timeframe

Clean, simple logic without over-filtering reduces missed opportunities

Performs well in both uptrends and downtrends

Automation Ready

This strategy includes alert conditions and webhook-ready JSON for automated execution.

This is a fast-reacting BTC bot designed for intraday and swing crypto trend trading.

在腳本中搜尋"bitcoin"

Tri-Align Crypto Trend (EMA + Slope)**Tri-Align Crypto Trend (EMA + Slope)**

Quickly see whether your coin is trending *with* Bitcoin. The indicator evaluates three pairs—**COIN/USDT**, **BTC/USDT**, and **COIN/BTC**—using a fast/slow EMA crossover plus the fast EMA’s slope. Each pair is tagged **Bullish / Bearish / Neutral** in a compact, color-coded table. Alerts fire when **all three** trends align (all bullish or all bearish).

**How to use**

1. Add the indicator to any crypto chart.

2. Set the three symbols (defaults: BNB/USDT, BTC/USDT, BNB/BTC) and optionally choose a signal timeframe.

3. Tune **Fast EMA**, **Slow EMA**, **Slope Lookback**, and **Min |Slope| %** to filter noise and require stronger momentum.

4. Create alerts: *Add alert →* choose the indicator and select **All Three Bullish**, **All Three Bearish**, or **All Three Aligned**.

**Logic**

* Bullish: `EMA_fast > EMA_slow` **and** fast EMA slope ≥ threshold

* Bearish: `EMA_fast < EMA_slow` **and** fast EMA slope ≤ −threshold

* Otherwise: Neutral

Tip: The **COIN/BTC** row reflects relative strength vs BTC—use it to avoid chasing coins that lag the benchmark. (For educational purposes; not financial advice.)

Tri-Align Crypto Trend (EMA + Slope)**Tri-Align Crypto Trend (EMA + Slope)**

Quickly see whether your coin is trending *with* Bitcoin. The indicator evaluates three pairs—**COIN/USDT**, **BTC/USDT**, and **COIN/BTC**—using a fast/slow EMA crossover plus the fast EMA’s slope. Each pair is tagged **Bullish / Bearish / Neutral** in a compact, color-coded table. Alerts fire when **all three** trends align (all bullish or all bearish).

**How to use**

1. Add the indicator to any crypto chart.

2. Set the three symbols (defaults: BNB/USDT, BTC/USDT, BNB/BTC) and optionally choose a signal timeframe.

3. Tune **Fast EMA**, **Slow EMA**, **Slope Lookback**, and **Min |Slope| %** to filter noise and require stronger momentum.

4. Create alerts: *Add alert →* choose the indicator and select **All Three Bullish**, **All Three Bearish**, or **All Three Aligned**.

**Logic**

* Bullish: `EMA_fast > EMA_slow` **and** fast EMA slope ≥ threshold

* Bearish: `EMA_fast < EMA_slow` **and** fast EMA slope ≤ −threshold

* Otherwise: Neutral

Tip: The **COIN/BTC** row reflects relative strength vs BTC—use it to avoid chasing coins that lag the benchmark. (For educational purposes; not financial advice.)

TT ToniTrading Adjustable Price Fee Band [%]Simple but perfectly functional indicator with Trading fee bands.

Crypto Trading is with fees and very small trades often don't make sense due to the fees we need to pay. With this band you can visualize your fees before entering a trade and take smarter decisions for tight daytrading and scalping.

You type in the fee for just one trade, the Taker Fee for a Market Order. The bands show the fees in % times 2, so what you will pay for opening and closing the trade in reality. The band therefore shows the real break-even point, with included payed fees.

It additionally helps taking trading decisions or not with very small trades (Scalping).

You can smooth the bands if you want and you can addtionally show the true datapoints if you prefer smoothend bands. I recommend no bigger smoothing than 2, if you don't want to show the datapoints. Additionally you can fill the band, and of course adjust transperency, colour and all the general TradingView stuff.

Fee Overview in the current market for the indicator input field:

BingX with 10% fee reduction code = 0,045 %

BingX: Normal = 0,050 %

Bitget, ByBit, BitUnix, Blofin, Phemex: Normal = 0,060 %

Bitget, ByBit, BitUnix, Blofin, Phemex: with 20% fee reduction code = 0,048 %

Have fun Trading, Happy Profits!

Greetings

ToniTrading

Crypto ETFs AUM📘 Description: BTC ETFs AUM Tracker

This indicator tracks the Assets Under Management (AUM) and daily inflows/outflows of the main U.S.-listed Bitcoin ETFs, allowing you to visualize institutional capital movement into Bitcoin products over time. It helps traders correlate institutional capital movement with Bitcoin price behavior.

🧩 Overview

The script adds up the daily AUM changes from selected Bitcoin ETFs to estimate the total net inflow/outflow of capital into spot BTC funds. It also accumulates those flows over time to display the total aggregated AUM balance, giving you a clearer sense of market direction and institutional sentiment. Two display modes are available: Balance view: plots the cumulative sum of net inflows (total ETF AUM). Inflows view: shows daily inflows (green) and outflows (red) as histogram columns, together with a smoothed moving average line.

⚙️ Inputs

Explained Base Settings Base Multiplier (base_multi) – Scaling factor applied to all AUM values. Leave at 1 for USD units, or adjust to display values in millions (1e6) or billions (1e9). Smoothing (c_smoothing) – Period length for the simple moving average used to calculate the smoothed mean inflow/outflow line. Show Balance (showBalance) – When enabled, displays the total cumulative AUM balance (sum of all net inflows over time). Show Inflows (showInflows) – When enabled, displays the daily inflows/outflows as colored columns. ETF Selection You can toggle which ETFs are included in the calculation:

BIT (BlackRock)

GBTC (Grayscale)

FBTC (Fidelity)

ARKB (ARK/21Shares)

BITB (Bitwise)

EZBC (Franklin Templeton)

BTCW (WisdomTree)

BTCO (Invesco Galaxy)

BRRR (Valkyrie)

HODL (VanEck)

Each switch determines whether the ETF’s AUM and daily flow data are included in the total calculation.

📊 Displayed Values Green Columns → Positive daily net inflows (AUM increased). Red Columns → Negative daily net outflows (AUM decreased). Orange Line → Smoothed moving average of net flows, used to identify persistent inflow/outflow trends. Blue Line (if enabled) → Total cumulative AUM balance (sum of all historical flows).

💡 Usage Notes Works best on daily timeframe, since ETF data is typically updated once per trading day. Not all ETFs have identical data history; missing data points are automatically skipped. The indicator doesn’t represent official fund NAV or guarantee data accuracy — it visualizes TradingView’s public financial feed. You can combine this tool with price action or on-chain metrics to analyze institutional Bitcoin flows.

Note: Some ETF data may not be available to all users depending on their TradingView data subscription or market access. Missing values are automatically skipped.

🧠 Disclaimer This script is for educational and analytical purposes only. It is not financial advice, and no investment decisions should be based solely on this indicator. Data accuracy depends on TradingView’s financial data sources and exchange reporting frequency.

BTC TOPperThe BTC TOPper indicator is a sophisticated technical analysis tool designed to identify critical price levels where Bitcoin's weekly Simple Moving Average (SMA) intersects with historically significant All-Time High (ATH) levels. This indicator is particularly valuable for long-term trend analysis and identifying potential reversal zones in Bitcoin's price action.

Key Features:

🔹 Weekly SMA Analysis: Uses a 200-period Simple Moving Average on weekly timeframe to smooth out short-term volatility and focus on long-term trends

🔹 Persistent Historical ATH Tracking: Automatically detects and "freezes" ATH levels that have been held for more than one year, creating persistent reference levels

🔹 Multi-Level Cross Detection: Tracks up to 10 different frozen ATH levels simultaneously, providing comprehensive historical context

🔹 Visual Cross Alerts: Highlights entire weeks with red background when the weekly SMA crosses any frozen ATH level, making signals impossible to miss

🔹 Advanced Smoothing Options: Includes optional secondary moving averages (SMA, EMA, SMMA, WMA, VWMA) with Bollinger Bands for enhanced analysis

🔹 Customizable Parameters: Adjustable SMA length, offset, and smoothing settings to fit different trading strategies

How It Works:

ATH Detection: Continuously monitors for new all-time highs

Level Freezing: After an ATH is held for 1+ year, it becomes a "frozen" historical level

Cross Monitoring: Watches for intersections between the 200-week SMA and any frozen ATH level

Signal Generation: Highlights the entire week when a cross occurs, providing clear visual alerts

Trading Applications:

Long-term Trend Analysis: Identify when Bitcoin approaches historically significant resistance levels

Reversal Zone Detection: Spot potential areas where price might reverse based on historical context

Support/Resistance Confirmation: Use frozen ATH levels as dynamic support and resistance zones

Market Structure Analysis: Understand how current price relates to historical market cycles

Best Practices:

Use on weekly timeframe for optimal results

Combine with other technical indicators for confirmation

Pay attention to multiple frozen levels clustering in the same price range

Consider market context and fundamentals alongside technical signals

Settings:

Length: 200 (default) - SMA period

Source: Close price

Smoothing: Optional secondary MA with multiple types available

Bollinger Bands: Optional volatility bands around secondary MA

This indicator is ideal for Bitcoin traders and analysts who want to understand the relationship between current price action and historical market structure, particularly useful for identifying potential major reversal zones based on historical ATH levels.

US Net Liquidity + M2 / US Debt (FRED)US Net Liquidity + M2 / US Debt

🧩 What this chart shows

This indicator plots the ratio of US Net Liquidity + M2 Money Supply divided by Total Public Debt.

US Net Liquidity is defined here as the Federal Reserve Balance Sheet (WALCL) minus the Treasury General Account (TGA) and the Overnight Reverse Repo facility (ON RRP).

M2 Money Supply represents the broad pool of liquid money circulating in the economy.

US Debt uses the Federal Government’s total outstanding debt.

By combining net liquidity with M2, then dividing by total debt, this chart provides a structural view of how much monetary “fuel” is in the system relative to the size of the federal debt load.

🧮 Formula

Ratio

=

(

Fed Balance Sheet

−

(

TGA

+

ON RRP

)

)

+

M2

Total Public Debt

Ratio=

Total Public Debt

(Fed Balance Sheet−(TGA+ON RRP))+M2

An optional normalization feature scales the ratio to start at 100 on the first valid bar, making long-term trends easier to compare.

🔎 Why it matters

Liquidity vs. Debt Growth: The numerator (Net Liquidity + M2) captures the monetary resources available to markets, while the denominator (Debt) reflects the expanding obligation of the federal government.

Market Signal: Historically, shifts in net liquidity and money supply relative to debt have coincided with major turning points in risk assets like equities and Bitcoin.

Context: A rising ratio may suggest that liquidity conditions are improving relative to debt expansion, which can be supportive for risk assets. Conversely, a falling ratio may highlight tightening conditions or debt outpacing liquidity growth.

⚙️ How to use it

Overlay this chart against S&P 500, Bitcoin, or gold to analyze correlations with asset performance.

Watch for trend inflections—does the ratio bottom before equities rally, or peak before risk-off periods?

Use normalization for long historical comparisons, or raw values to see the absolute ratio.

📊 Data sources

This indicator pulls from FRED (Federal Reserve Economic Data) tickers available in TradingView:

WALCL: Fed balance sheet

RRPONTSYD: Overnight Reverse Repo

WTREGEN: Treasury General Account

M2SL: M2 money stock

GFDEBTN: Total federal public debt

⚠️ Notes

Some FRED series are updated weekly, others monthly—set your chart timeframe accordingly.

If any ticker is unavailable in your plan, replace it with the equivalent FRED symbol provided in TradingView.

This indicator is intended for macro analysis, not short-term trading signals.

HIFI Altcoin Season Index (Total3 vs BTC)This indicator helps you determine whether the crypto market is in an "altcoin season" or a "bitcoin season." It doesn't compare every single altcoin to Bitcoin individually; instead, it uses a more efficient approach.

Methodology

The index calculates the difference in price performance over a selected period (default 90 days) between the total market capitalization of altcoins without Ethereum (TOTAL3) and Bitcoin (BTC).

Interpretation

Value above 75: TOTAL3 is showing significantly stronger growth than BTC, indicating an ALTCOIN SEASON. 🚀

Value below 25: BTC is outperforming TOTAL3, indicating a BITCOIN SEASON. 👑

Value between 25 and 75: The market is in a mixed or neutral phase. 🤷

Benefits

This method avoids the technical limitations of Pine Script when requesting data for a large number of symbols, making the indicator stable and reliable.

Disclaimer: This indicator is a tool for market analysis and should not be considered financial advice.

BTC Sigma CloudOverview

The BTC Sigma Cloud indicator calculates and displays 1, 2, and 3 sigma price movements for Bitcoin (BTC) on a rolling basis, visualized as a cloud. It shows historical volatility bands and projects them forward for the next 7 days.

Settings:

Vol Lookback: Default is 20 periods. Adjust to change the volatility calculation window.

Interpretation:

Cloud Bands: The cloud consists of three shaded layers representing 1σ, 2σ, and 3σ moves above and below the current price.

1σ (Innermost): 68% probability of price staying within this range.

2σ (Middle): 95% probability.

3σ (Outermost): 99.7% probability.

Historical View: The cloud tracks past price movements based on volatility.

Projection: The cloud extends 7 days forward, indicating potential price ranges based on current volatility.

Labels: Subtle labels (1σ, -1σ, 2σ, -2σ, 3σ, -3σ) mark the upper and lower bounds of each sigma level on the latest bar for clarity.

Trading Use:

Use the cloud to gauge potential support/resistance zones.

Monitor price behavior near sigma levels for breakout or reversal signals.

The projected cloud helps anticipate future price ranges for planning trades.

Notes

Best used on daily charts for Bitcoin.

Adjust the lookback period to suit shorter or longer-term analysis.

Combine with other indicators for confirmation.

Correlation Heatmap Matrix [TradingFinder] 20 Assets Variable🔵 Introduction

Correlation is one of the most important statistical and analytical metrics in financial markets, data mining, and data science. It measures the strength and direction of the relationship between two variables.

The correlation coefficient always ranges between +1 and -1 : a perfect positive correlation (+1) means that two assets or currency pairs move together in the same direction and at a constant ratio, a correlation of zero (0) indicates no clear linear relationship, and a perfect negative correlation (-1) means they move in exactly opposite directions.

While the Pearson Correlation Coefficient is the most common method for calculation, other statistical methods like Spearman and Kendall are also used depending on the context.

In financial market analysis, correlation is a key tool for Forex, the Stock Market, and the Cryptocurrency Market because it allows traders to assess the price relationship between currency pairs, stocks, or coins. For example, in Forex, EUR/USD and GBP/USD often have a high positive correlation; in stocks, companies from the same sector such as Apple and Microsoft tend to move similarly; and in crypto, most altcoins show a strong positive correlation with Bitcoin.

Using a Correlation Heatmap in these markets visually displays the strength and direction of these relationships, helping traders make more accurate decisions for risk management and strategy optimization.

🟣 Correlation in Financial Markets

In finance, correlation refers to measuring how closely two assets move together over time. These assets can be stocks, currency pairs, commodities, indices, or cryptocurrencies. The main goal of correlation analysis in trading is to understand these movement patterns and use them for risk management, trend forecasting, and developing trading strategies.

🟣 Correlation Heatmap

A correlation heatmap is a visual tool that presents the correlation between multiple assets in a color-coded table. Each cell shows the correlation coefficient between two assets, with colors indicating its strength and direction. Warm colors (such as red or orange) represent strong negative correlation, cool colors (such as blue or cyan) represent strong positive correlation, and mid-range tones (such as yellow or green) indicate correlations that are close to neutral.

🟣 Practical Applications in Markets

Forex : Identify currency pairs that move together or in opposite directions, avoid overexposure to similar trades, and spot unusual divergences.

Crypto : Examine the dependency of altcoins on Bitcoin and find independent movers for portfolio diversification.

Stocks : Detect relationships between stocks in the same industry or find outliers that move differently from their sector.

🟣 Key Uses of Correlation in Trading

Risk management and diversification: Select assets with low or negative correlation to reduce portfolio volatility.

Avoiding overexposure: Prevent opening multiple positions on highly correlated assets.

Pairs trading: Exploit temporary deviations between historically correlated assets for arbitrage opportunities.

Intermarket analysis: Study the relationships between different markets like stocks, currencies, commodities, and bonds.

Divergence detection: Spot when two typically correlated assets move apart as a possible trend change signal.

Market forecasting: Use correlated asset movements to anticipate others’ behavior.

Event reaction analysis: Evaluate how groups of assets respond to economic or political events.

❗ Important Note

It’s important to note that correlation does not imply causation — it only reflects co-movement between assets. Correlation is also dynamic and can change over time, which is why analyzing it across multiple timeframes provides a more accurate picture. Combining correlation heatmaps with other analytical tools can significantly improve the precision of trading decisions.

🔵 How to Use

The Correlation Heatmap Matrix indicator is designed to analyze and manage the relationships between multiple assets at once. After adding the tool to your chart, start by selecting the assets you want to compare (up to 20).

Then, choose the Correlation Period that fits your trading strategy. Shorter periods (e.g., 20 bars) are more sensitive to recent price movements, making them suitable for short-term trading, while longer periods (e.g., 100 or 200 bars) provide a broader view of correlation trends over time.

The indicator outputs a color-coded matrix where each cell represents the correlation between two assets. Warm colors like red and orange signal strong negative correlation, while cool colors like blue and cyan indicate strong positive correlation. Mid-range tones such as yellow or green suggest correlations that are close to neutral. This visual representation makes it easy to spot market patterns at a glance.

One of the most valuable uses of this tool is in portfolio risk management. Portfolios with highly correlated assets are more vulnerable to market swings. By using the heatmap, traders can find assets with low or negative correlation to reduce overall risk.

Another key benefit is preventing overexposure. For example, if EUR/USD and GBP/USD have a high positive correlation, opening trades on both is almost like doubling the position size on one asset, increasing risk unnecessarily. The heatmap makes such relationships clear, helping you avoid them.

The indicator is also useful for pairs trading, where a trader identifies assets that are usually correlated but have temporarily diverged — a potential arbitrage or mean-reversion opportunity.

Additionally, the tool supports intermarket analysis, allowing traders to see how movements in one market (e.g., crude oil) may impact others (e.g., the Canadian dollar). Divergence detection is another advantage: if two typically aligned assets suddenly move in opposite directions, it could signal a major trend shift or a news-driven move.

Overall, the Correlation Heatmap Matrix is not just an analytical indicator but also a fast, visual alert system for monitoring multiple markets at once. This is particularly valuable for traders in fast-moving environments like Forex and crypto.

🔵 Settings

🟣 Logic

Correlation Period : Number of bars used to calculate correlation between assets.

🟣 Display

Table on Chart : Enable/disable displaying the heatmap directly on the chart.

Table Size : Choose the table size (from very small to very large).

Table Position : Set the table location on the chart (top, middle, or bottom in various alignments).

🟣 Symbol Custom

Select Market : Choose the market type (Forex, Stocks, Crypto, or Custom).

Symbol 1 to Symbol 20: In custom mode, you can define up to 20 assets for correlation calculation.

🔵 Conclusion

The Correlation Heatmap Matrix is a powerful tool for analyzing correlations across multiple assets in Forex, crypto, and stock markets. By displaying a color-coded table, it visually conveys both the strength and direction of correlations — warm colors for strong negative correlation, cool colors for strong positive correlation, and mid-range tones such as yellow or green for near-zero or neutral correlation.

This helps traders select assets with low or negative correlation for diversification, avoid overexposure to similar trades, identify arbitrage and pairs trading opportunities, and detect unusual divergences between typically aligned assets. With support for custom mode and up to 20 symbols, it offers high flexibility for different trading strategies, making it a valuable complement to technical analysis and risk management.

BTC Correlation PercentagePurpose

This indicator displays the correlation percentage between the current trading instrument and Bitcoin (BTC/USDT) as a text label on the chart. It helps traders quickly assess how closely an asset's price movements align with Bitcoin's fluctuations.

Key Features

Precise Calculation: Shows correlation as a percentage with one decimal place (e.g., 25.6%).

Customizable Appearance: Allows adjustment of colors, position, and calculation period.

Clean & Simple: Displays only essential information without cluttering the chart.

Universal Compatibility: Works on any timeframe and with any trading pair.

Input Settings

Core Parameters:

BTC Symbol – Ticker for Bitcoin (default: BINANCE:BTCUSDT).

Correlation Period – Number of bars used for calculation (default: 50 candles).

Show Correlation Label – Toggle visibility of the correlation label.

Visual Customization:

Text Color – Label text color (default: white).

Background Color – Label background color (default: semi-transparent blue).

Border Color – Border color around the label (default: gray).

Label Position – Where the label appears on the chart (default: top-right).

Interpreting Correlation Values

70% to 100% → Strong positive correlation (asset moves in sync with BTC).

30% to 70% → Moderate positive correlation.

-30% to 30% → Weak or no correlation.

-70% to -30% → Moderate negative correlation (asset moves opposite to BTC).

-100% to -70% → Strong negative correlation.

Practical Use Cases

For Altcoins: A correlation above 50% suggests high dependence on Bitcoin’s price action.

For Futures Trading: Helps assess systemic risks tied to BTC movements.

During High Volatility: Determines whether an asset’s price change is driven by its own factors or broader market trends.

How It Works

The indicator recalculates automatically with each new candle. For the most reliable results, it is recommended for use on daily or higher timeframes.

This tool provides traders with a quick, visual way to gauge Bitcoin’s influence on other assets, improving decision-making in crypto markets. 🚀

This response is AI-generated, for reference only.

New chat

Power Metcalfe's + Fibonacci Channel## Metcalfe's Law + Fibonacci Channel - Optimized Bitcoin Valuation Model

This indicator presents an enhanced variation of the classic Bitcoin Metcalfe's Law model, combining logarithmic regression analysis with Fibonacci retracement levels to create a comprehensive valuation framework.

**Key Features:**

- **Optimized Metcalfe's Law calculation** using historical cycle data (2013-2022) for improved accuracy

- **Fibonacci channel overlay** with key levels: 0.382, 0.618, 1.272, 1.618, 2.000, 2.618, 3.000

- **Dynamic trading zones** with visual buy/sell signals based on price position relative to the channel

- **Real-time targets** displaying current Fibonacci projections and fair value estimates

**What makes it different:**

Unlike standard Metcalfe's Law implementations, this version integrates logarithmic growth principles and uses a refined dataset that accounts for Bitcoin's maturation cycles. The Fibonacci overlay provides clearer entry/exit points while maintaining the long-term growth trajectory based on network adoption.

**Best suited for:** Long-term Bitcoin holders and macro traders looking for mathematical support/resistance levels based on network adoption dynamics and scarcity.

The model automatically updates calculations and provides a comprehensive information table showing current formula parameters and key price targets.

MSTY-WNTR Rebalancing SignalMSTY-WNTR Rebalancing Signal

## Overview

The **MSTY-WNTR Rebalancing Signal** is a custom TradingView indicator designed to help investors dynamically allocate between two YieldMax ETFs: **MSTY** (YieldMax MSTR Option Income Strategy ETF) and **WNTR** (YieldMax Short MSTR Option Income Strategy ETF). These ETFs are tied to MicroStrategy (MSTR) stock, which is heavily influenced by Bitcoin's price due to MSTR's significant Bitcoin holdings.

MSTY benefits from upward movements in MSTR (and thus Bitcoin) through a covered call strategy that generates income but caps upside potential. WNTR, on the other hand, provides inverse exposure, profiting from MSTR declines but losing in rallies. This indicator uses Bitcoin's momentum and MSTR's relative strength to signal when to hold MSTY (bullish phases), WNTR (bearish phases), or stay neutral, aiming to optimize returns by switching allocations at key turning points.

Inspired by strategies discussed in crypto communities (e.g., X posts analyzing MSTR-linked ETFs), this indicator promotes an active rebalancing approach over a "set and forget" buy-and-hold strategy. In simulated backtests over the past 12 months (as of August 4, 2025), the optimized version has shown potential to outperform holding 100% MSTY or 100% WNTR alone, with an illustrative APY of ~125% vs. ~6% for MSTY and ~-15% for WNTR in one scenario.

**Important Disclaimer**: This is not financial advice. Past performance does not guarantee future results. Always consult a financial advisor. Trading involves risk, and you could lose money. The indicator is for educational and informational purposes only.

## Key Features

- **Momentum-Based Signals**: Uses a Simple Moving Average (SMA) on Bitcoin's price to detect bullish (price > SMA) or bearish (price < SMA) trends.

- **RSI Confirmation**: Incorporates MSTR's Relative Strength Index (RSI) to filter signals, avoiding overbought conditions for MSTY and oversold for WNTR.

- **Visual Cues**:

- Green upward triangle for "Hold MSTY".

- Red downward triangle for "Hold WNTR".

- Yellow cross for "Switch" signals.

- Background color: Green for MSTY, red for WNTR.

- **Information Panel**: A table in the top-right corner displays real-time data: BTC Price, SMA value, MSTR RSI, and current Allocation (MSTY, WNTR, or Neutral).

- **Alerts**: Configurable alerts for holding MSTY, holding WNTR, or switching.

- **Optimized Parameters**: Defaults are tuned (SMA: 10 days, RSI: 15 periods, Overbought: 80, Oversold: 20) based on simulations to reduce whipsaws and capture trends effectively.

## How It Works

The indicator's logic is straightforward yet effective for volatile assets like Bitcoin and MSTR:

1. **Primary Trigger (Bitcoin Momentum)**:

- Calculate the SMA of Bitcoin's closing price (default: 10-day).

- Bullish: Current BTC price > SMA → Potential MSTY hold.

- Bearish: Current BTC price < SMA → Potential WNTR hold.

2. **Secondary Filter (MSTR RSI Confirmation)**:

- Compute RSI on MSTR stock (default: 15-period).

- For bullish signals: If RSI > Overbought (80), signal Neutral (avoid overextended rallies).

- For bearish signals: If RSI < Oversold (20), signal Neutral (avoid capitulation bottoms).

3. **Allocation Rules**:

- Hold 100% MSTY if bullish and not overbought.

- Hold 100% WNTR if bearish and not oversold.

- Neutral otherwise (e.g., during choppy or extreme markets) – consider holding cash or avoiding trades.

4. **Rebalancing**:

- Switch signals trigger when the hold changes (e.g., from MSTY to WNTR).

- Recommended frequency: Weekly reviews or on 5% BTC moves to minimize trading costs (aim for 4-6 trades/year).

This approach leverages Bitcoin's influence on MSTR while mitigating the risks of MSTY's covered call drag during downtrends and WNTR's losses in uptrends.

## Setup and Usage

1. **Chart Requirements**:

- Apply this indicator to a Bitcoin chart (e.g., BTCUSD on Binance or Coinbase, daily timeframe recommended).

- Ensure MSTR stock data is accessible (TradingView supports it natively).

2. **Adding to TradingView**:

- Open the Pine Editor.

- Paste the script code.

- Save and add to your chart.

- Customize inputs if needed (e.g., adjust SMA/RSI lengths for different timeframes).

3. **Interpretation**:

- **Green Background/Triangle**: Allocate 100% to MSTY – Bitcoin is in an uptrend, MSTR not overbought.

- **Red Background/Triangle**: Allocate 100% to WNTR – Bitcoin in downtrend, MSTR not oversold.

- **Yellow Switch Cross**: Rebalance your portfolio immediately.

- **Neutral (No Signal)**: Panel shows "Neutral" – Hold cash or previous position; reassess weekly.

- Monitor the panel for key metrics to validate signals manually.

4. **Backtesting and Strategy Integration**:

- Convert to a strategy script by changing `indicator()` to `strategy()` and adding entry/exit logic for automated testing.

- In simulations (e.g., using Python or TradingView's backtester), it has outperformed buy-and-hold in volatile markets by ~100-200% relative APY, but results vary.

- Factor in fees: ETF expense ratios (~0.99%), trading commissions (~$0.40/trade), and slippage.

5. **Risk Management**:

- Use with a diversified portfolio; never allocate more than you can afford to lose.

- Add stop-losses (e.g., 10% trailing) to protect against extreme moves.

- Rebalance sparingly to avoid over-trading in sideways markets.

- Dividends: Reinvest MSTY/WNTR payouts into the current hold for compounding.

## Performance Insights (Simulated as of August 4, 2025)

Based on synthetic backtests modeling the last 12 months:

- **Optimized Strategy APY**: ~125% (by timing switches effectively).

- **Hold 100% MSTY APY**: ~6% (gains from BTC rallies offset by downtrends).

- **Hold 100% WNTR APY**: ~-15% (losses in bull phases outweigh bear gains).

In one scenario with stronger volatility, the strategy achieved ~4533% APY vs. 10% for MSTY and -34% for WNTR, highlighting its potential in dynamic markets. However, these are illustrative; real results depend on actual BTC/MSTR movements. Test thoroughly on historical data.

## Limitations and Considerations

- **Data Dependency**: Relies on accurate BTC and MSTR data; delays or gaps can affect signals.

- **Market Risks**: Bitcoin's volatility can lead to false signals (whipsaws); the RSI filter helps but isn't perfect.

- **No Guarantees**: This indicator doesn't predict the future. MSTR's correlation to BTC may change (e.g., due to regulatory events).

- **Not for All Users**: Best for intermediate/advanced traders familiar with ETFs and crypto. Beginners should paper trade first.

- **Updates**: As of August 4, 2025, this is version 1.0. Future updates may include volume filters or EMA options.

If you find this indicator useful, consider leaving a like or comment on TradingView. Feedback welcome for improvements!

Currency Weekend - shading weekend trading// ─────────────────────────────────────────────────────────────────────────────

// © 2025, Steve / Steven Anthony – "Currency Weekend"

// This script highlights the low-liquidity weekend window that often affects

// both fiat currency markets and cryptocurrencies like Bitcoin.

//

// ╭─────────────────────────────── DESCRIPTION ───────────────────────────────╮

// | This indicator shades a customizable time window on your chart, |

// | originally set to highlight the **forex weekend lull** from |

// | **Friday 21:00 UTC to Sunday 21:00 UTC**, when traditional fiat |

// | currency markets close. |

// | |

// | Traders who observe Bitcoin, Ethereum, or other crypto assets may |

// | notice reduced liquidity or increased erratic moves during this time, |

// | due to overlapping behaviors from professional forex traders who |

// | trade both markets. |

// ╰──────────────────────────────────────────────────────────────────────────╯

//

// 🔧 Flexible Configuration:

// - Define your own start and end **day + time** for shading

// - Useful for shading other custom quiet periods or session transitions

//

// 💡 Use Cases:

// - Avoid trading during low-liquidity periods

// - Spot potential weekend traps or price gaps

// - Align crypto behavior with fiat market hours

//

// 📍 Default Settings:

// - Start: Friday 21:00 UTC

// - End: Sunday 21:00 UTC

//

// Timezone is normalized to the chart’s timezone for seamless integration.

//

// ─────────────────────────────────────────────────────────────────────────────

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

TrendZonesTrendZones

This is an indicator which I use, have tested, tweaked and added features to for use in my trend following investing system. I got the idea for it when for some reason I was looking for a dynamic reference to measure the height of a channel or something. In search of this I made MA’s of the high and low borders of a Donchian channel which turned out to be two near parallel and stunningly smooth curves. This visual was so appealing that I immediately tried to turn it into a replacement for the KeltCOG which I previously used in my system. First I created a curve in the middle of the upper and lower curves, which I called COG (Center Of Gravity). Then I decided to enter only one lookback and let the script create a Donchian channel with half the lookback and use this to create the curves with an MA of whole lookback. For this reason the minimum lookback is set to 14, enough room for the Donchian Channel of 7 periods. This Donchian ChanneI has a special way of calculating the borders, involving a 5 period Median value. Thanks to this these borders are really a resistance and support level, which won’t change at a whim, e.g. when a ‘dead cat bounce’ occurs. I prevented the Donchian channel to show itself between the curves and only pop out from behind these. These pop outs now function as “strong trend zones”. I gave it colors (blue:-strong up, green: moderate up, orange: moderate down, red: strong down, near COG: gray, curves horizontal: gray) and it looked very appealing. I tested it in different time frames. In some weekend, when I was bored, I observed for a few hours the minute chart of bitcoin. It turned out that you can reliably tell that an uptrend ends when the candles go under the COG beginning a downtrend. Uptrend starts again once the candles go above COG. As Trends on minute charts only last around half an hour, this entertainment made the potential of this indicator very clear to me in just one afternoon.

Risk Management, Safe Level and Logical Stops.

In the inputs are settings for “Risk Tolerance”, and to activate “Show Logical Stop Level” (activated in example chart) and “Show Safe Level”. As a rule of thump a trade should not expose the invested capital to a risk of losing more than 2 percent. I divided my investment capital in ten equal parts which are allocated to ten different stocks or other instruments or kept liquid. This means that when a position is closed by triggering a Stop with a loss of 20 percent, the invested capital suffers only 2 percent (20% x 10% = 2%). This is why the value for “Risk Tolerance” has a default of 20. Because I put my Stops on the lower curve, a “Safe Level” can be calculated such that when you buy for a price below or at this level, the stop will protect the position sufficiently. Because I only buy when the instrument is in uptrend, the buying price should be between COG and Safe Level. Although I never do that, putting the stop at other curves is feasible and when you want to widen the stop (I never lower my stops btw) in a downtrend situation, even 1 ATR below the “Low Border”. I call these “Logical Stop Levels”, marked with dark green circles on the lower curve when safe buying by placing the Stoploss on this curve is possible, gray circles on the other curves, on the Upper Curve navy when price enters very profitable level. In a downtrend situation maroon circles appear.

Target lines

When I open a position I always set a Stoploss and a Target, for this purpose two types of Target values can be set and corresponding Target lines activated. These lines are drawn above the “High Border” at the set distance. If one expects some price to be used, differences will occur.

Other Features

Support Zone, this is 1 ATR below the “Low Border”, the maroon circles of the “Logal Stops” are placed on this “Support level”.

Stop distance and Channel Width. (activated in example chart) These are reported in a two cell table in the right lower corner of the main panel. I created this because I want to be able to check the volatility, whether the channel shows a situation in which safe buying in most levels of the channel is possible or what risk you take when you buy now and set the Stop at the nearest logical level (which is not always the “Lower curve”). This feature comes in handy for creating a setup I propose in the “Day Trading Fantasy” below.

Some General and User Settings. I never activate this, perhaps you will.

Use Of TrendZones In My System.

Create a list of stocks in uptrend. I define ‘stock in uptrend’ as in uptrend zone in all three monthly, weekly and daily charts, all three should at the same time be in uptrend. The advantage of TrendZones is that you can immediately see in which zone the candle moves.

Opening a position in a stock from the above list. I do this only when in both the daily and weekly the green dot on the lower curve indicates a buying opportunity. This is usually not the case in most of the items of the list, this feature thus provides a good timing for opening a position. Sometimes you need to wait a few weeks for this to happen.

Setting a target over a position. For this I use the Target percent line of the weekly chart with the default value of 10.

Updating the Stoploss and Target values. Every week or two weeks I set these to the new values of the “Lower Curve” and the Target line of the weekly. Attention: never shift down Stops, only up or let them stay the same when the curve moves down. I never use Stop levels on other curves.

I Check the charts whenever I like to do this. Close the position when the uptrend obviously shifts down. Otherwise I let the profits run until the Target triggers which closes the position with some profit.

For selecting stocks an checking charts for volume events, I also use a subpanel indicator called “TZanalyser”, which borrows the visual of my “Fibonacci Zone Oscillator”, is based on TrendZones and includes code from my REVE indicators. I intend to publish that as well.

Day Trading Fantasy.

Day trading is an attempt to earn a dime by opening a position in the morning and close it during the day again with a profit (or a loss). Before the market closes, you close all day trading positions.

In my fantasy the “Logical Stop Level” is repurposed for use as entry point and the ATR-based Target line is used to provide a target setting in an intraday chart, like e.g. 15 minute. To do this the “Safe Level” should be limited to between Channel width and COG. This can be done by showing “Safe Level” and “Channel Width” and then set “Risk Tolerance” to around the shown Channel Width. In this setting you can then wait for the green circle to show up for entering your trade and protect it with the stop.

I don’t know if this works fine or if it’s better than other day trade systems, because I don’t do day trading.

Take care and have fun.

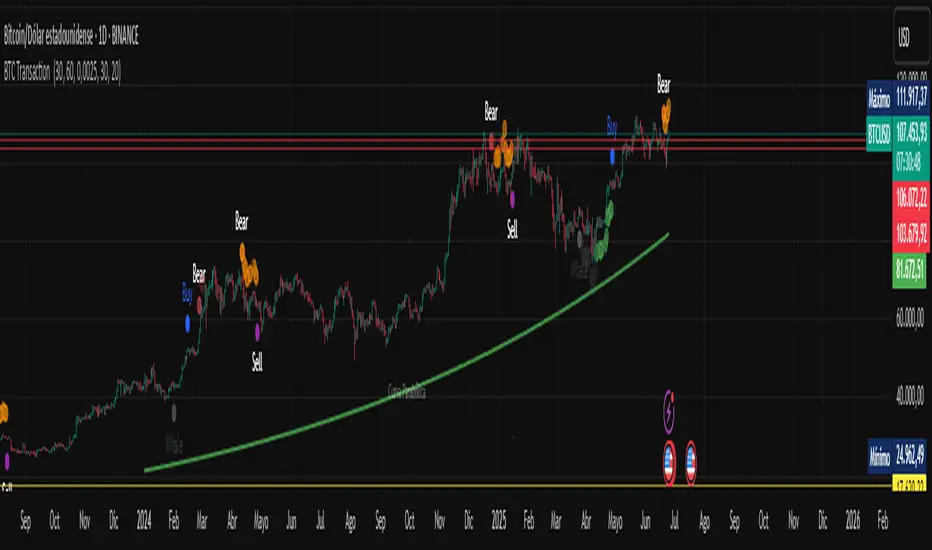

BTC Transaction Indicator Name: "Bitcoin On-Chain Volume & Dynamic Parabolic Curve Signals"

Purpose:

This indicator is designed for Bitcoin traders and long-term holders. It combines the analysis of Bitcoin's on-chain transaction volume with price action to generate "Whale" and "Bear" signals. Additionally, it features a unique dynamic parabolic curve that acts as a visual support line, adapting its visibility based on price interaction with a key Exponential Moving Average (EMA).

Key Components:

On-Chain Volume Analysis:

Utilizes Estimated Transaction Volume (ETRAV) data from the Bitcoin blockchain.

Calculates fast and slow Simple Moving Averages (SMAs) of this volume.

Identifies volume trends (up/down) and significant volume increases/decreases.

Employs fixed thresholds (2,500,000 for low volume and 25,000,000 for high volume) to define key activity levels, similar to how historical on-chain analysis defined accumulation and distribution zones.

Price Action Analysis:

Calculates fast and slow SMAs of the price.

Detects price trends (up/down), recoveries, and declines based on these price SMAs.

"Whale" and "Bear" Signals:

Whale Signals (Buy-side): Generated when there's an upward volume trend, significant volume increase, and a downward price trend followed by price recovery. These indicate potential accumulation phases.

Bear Signals (Sell-side): Generated when there's a downward volume trend, significant volume decrease, and an upward price trend followed by price decline. These indicate potential distribution phases.

Visuals: Both types of signals are plotted as small, colored circles directly on the price chart, with corresponding text labels ("Whale," "Buy," "Bear," "Sell," "Price Recovering," "Price Declining").

Dynamic Parabolic Curve:

Concept: A green parabolic (exponential) curve that serves as a dynamic visual support line.

Activation: The curve starts drawing automatically only when the price crosses over the EMA 500 (Exponential Moving Average of 500 periods). The curve's starting point is set at a user-defined percentage below the EMA 500 value at that exact crossover point.

Visibility: The curve remains visible and continues its trajectory only as long as the price stays above the EMA 500.

Deactivation: The curve disappears instantly if the price falls below or equals the EMA 500. It will only reappear if the price crosses above the EMA 500 again.

Customization: The curve's steepness (Tasa Crecimiento Curva) and its initial distance from the EMA 500 (Inicio Curva % por debajo de EMA500) are adjustable.

Dynamic Label: A "Parabólico" text label is plotted near the center of the active curve segment, with an adjustable vertical offset to ensure it stays visually appealing below the curve.

What is PLOTTED on the chart:

The small, colored circle signals for Whale/Buy and Bear/Sell activity.

The green dynamic parabolic curve.

What is NOT PLOTTED:

EMA 200, EMA 500 lines (though they are calculated internally for logic).

Raw volume data or volume Moving Averages (these are only used for signal calculation, not plotted).

Ideal for:

Bitcoin traders and investors focused on long-term trends and cycle analysis, who want visual cues for accumulation/distribution phases based on on-chain activity, complemented by a unique, dynamically appearing parabolic support curve.

Important Notes:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe for optimal on-chain data relevance.

Rainbow Price Chart This indicator is a technical and on-chain analysis tool for Bitcoin, designed to help investors better understand the different phases of the market cycle and underlying sentiment. It directly overlays on the price chart (overlay=true).

Indicator Name: "Rainbow Price Chart & V/T Ratio Signals"

General Purpose:

It combines two popular methodologies for visualizing Bitcoin's value and sentiment: the classic "Rainbow Price Chart" and signals derived from the "Value per Transaction Ratio" (V/T Ratio) based on blockchain data. It is ideal for long-term investors looking for strategic entry/exit points.

Main Components:

Rainbow Price Chart:

Concept: Divides Bitcoin's price range into different market "sentiment zones" (e.g., "Bubble Zone," "FOMO Zone," "HODL Zone," "Accumulation Zone," "Buy Zone," "Fire Sale Zone") using colored bands. These bands are calculated as ascending and descending multiples of a base Exponential Moving Average (EMA), configurable by default to 200 periods.

Visualization: The zones are represented with transparent color fills on the price chart. A detailed legend in the top right corner of the chart explains the meaning of each color and sentiment zone.

Important Note: This type of chart is designed to be viewed and analyzed correctly on a logarithmic price scale. The indicator includes a visual reminder to activate this scale.

Value per Transaction (V/T) Ratio Signals:

Concept: Measures the average value per transaction on the Bitcoin blockchain by dividing the total transacted volume in USD by the number of transactions. This ratio is smoothed with an Exponential Moving Average (by default, 7 periods) and is framed within a dynamic Linear Regression Channel (LRC) based on standard deviation.

Signal Generation: Based on the position of the smoothed V/T Ratio within this LRC channel, the indicator generates signals directly on the price chart, such as:

"BOTTOM": Low price, V/T Ratio in the lower band of the LRC.

"SEMI-LOW" / "SEMI-HIGH": Intermediate phases within the channel.

"ATH" (All-Time High): Potentially overvalued price, V/T Ratio in the upper band of the LRC.

On-Chain Data: The indicator requests external daily on-chain data for total transacted volume (TVTVR) and number of transactions (NTRAN) from the Bitcoin blockchain.

Diagnostic Panes: Includes plots of the raw on-chain data (volume and number of transactions) in a separate pane, which are useful for debugging or verifying the data source. The lines for the V/T Ratio itself and its LRC channel are not plotted by default but can be activated in the code for deeper analysis.

Ideal for:

Bitcoin investors and "hodlers" who desire a visual tool that combines price-based market cycle context with fundamental signals derived from on-chain activity, to help identify key moments for accumulation or potential distribution.

Considerations:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe.

Quantum Reversal# 🧠 Quantum Reversal

## **Quantitative Mean Reversion Framework**

This algorithmic trading system employs **statistical mean reversion theory** combined with **adaptive volatility modeling** to capitalize on Bitcoin's inherent price oscillations around its statistical mean. The strategy integrates multiple technical indicators through a **multi-layered signal processing architecture**.

---

## ⚡ **Core Technical Architecture**

### 📊 **Statistical Foundation**

- **Bollinger Band Mean Reversion Model**: Utilizes 20-period moving average with 2.2 standard deviation bands for volatility-adjusted entry signals

- **Adaptive Volatility Threshold**: Dynamic standard deviation multiplier accounts for Bitcoin's heteroscedastic volatility patterns

- **Price Action Confluence**: Entry triggered when price breaches lower volatility band, indicating statistical oversold conditions

### 🔬 **Momentum Analysis Layer**

- **RSI Oscillator Integration**: 14-period Relative Strength Index with modified oversold threshold at 45

- **Signal Smoothing Algorithm**: 5-period simple moving average applied to RSI reduces noise and false signals

- **Momentum Divergence Detection**: Captures mean reversion opportunities when momentum indicators show oversold readings

### ⚙️ **Entry Logic Architecture**

```

Entry Condition = (Price ≤ Lower_BB) OR (Smoothed_RSI < 45)

```

- **Dual-Condition Framework**: Either statistical price deviation OR momentum oversold condition triggers entry

- **Boolean Logic Gate**: OR-based entry system increases signal frequency while maintaining statistical validity

- **Position Sizing**: Fixed 10% equity allocation per trade for consistent risk exposure

### 🎯 **Exit Strategy Optimization**

- **Profit-Lock Mechanism**: Positions only closed when showing positive unrealized P&L

- **Trend Continuation Logic**: Allows winning trades to run until momentum exhaustion

- **Dynamic Exit Timing**: No fixed profit targets - exits based on profitability state rather than arbitrary levels

---

## 📈 **Statistical Properties**

### **Risk Management Framework**

- **Long-Only Exposure**: Eliminates short-squeeze risk inherent in cryptocurrency markets

- **Mean Reversion Bias**: Exploits Bitcoin's tendency to revert to statistical mean after extreme moves

- **Position Management**: Single position limit prevents over-leveraging

### **Signal Processing Characteristics**

- **Noise Reduction**: SMA smoothing on RSI eliminates high-frequency oscillations

- **Volatility Adaptation**: Bollinger Bands automatically adjust to changing market volatility

- **Multi-Timeframe Coherence**: Indicators operate on consistent timeframe for signal alignment

---

## 🔧 **Parameter Configuration**

| Technical Parameter | Value | Statistical Significance |

|-------------------|-------|-------------------------|

| Bollinger Period | 20 | Standard statistical lookback for volatility calculation |

| Std Dev Multiplier | 2.2 | Optimized for Bitcoin's volatility distribution (95.4% confidence interval) |

| RSI Period | 14 | Traditional momentum oscillator period |

| RSI Threshold | 45 | Modified oversold level accounting for Bitcoin's momentum characteristics |

| Smoothing Period | 5 | Noise reduction filter for momentum signals |

---

## 📊 **Algorithmic Advantages**

✅ **Statistical Edge**: Exploits documented mean reversion tendency in Bitcoin markets

✅ **Volatility Adaptation**: Dynamic bands adjust to changing market conditions

✅ **Signal Confluence**: Multiple indicator confirmation reduces false positives

✅ **Momentum Integration**: RSI smoothing improves signal quality and timing

✅ **Risk-Controlled Exposure**: Systematic position sizing and long-only bias

---

## 🔬 **Mathematical Foundation**

The strategy leverages **Bollinger Band theory** (developed by John Bollinger) which assumes that prices tend to revert to the mean after extreme deviations. The RSI component adds **momentum confirmation** to the statistical price deviation signal.

**Statistical Basis:**

- Mean reversion follows the principle that extreme price deviations from the moving average are temporary

- The 2.2 standard deviation multiplier captures approximately 97.2% of price movements under normal distribution

- RSI momentum smoothing reduces noise inherent in oscillator calculations

---

## ⚠️ **Risk Considerations**

This algorithm is designed for traders with understanding of **quantitative finance principles** and **cryptocurrency market dynamics**. The strategy assumes mean-reverting behavior which may not persist during trending market phases. Proper risk management and position sizing are essential.

---

## 🎯 **Implementation Notes**

- **Market Regime Awareness**: Most effective in ranging/consolidating markets

- **Volatility Sensitivity**: Performance may vary during extreme volatility events

- **Backtesting Recommended**: Historical performance analysis advised before live implementation

- **Capital Allocation**: 10% per trade sizing assumes diversified portfolio approach

---

**Engineered for quantitative traders seeking systematic mean reversion exposure in Bitcoin markets through statistically-grounded technical analysis.**

BTC Dominance Zones (For Altseason)Overview

The "BTC Dominance Zones (For Altseason)" indicator is a visual tool designed to help traders navigate the different phases of the altcoin market cycle by tracking Bitcoin Dominance (BTC.D).

It provides clear, color-coded zones directly on the BTC.D chart, offering an intuitive roadmap for the progression of alt season.

Purpose & Problem Solved

Many traders often miss altcoin rotations or get caught at market tops due to emotional decision-making or a lack of a clear framework. This indicator aims to solve that problem by providing an objective, historically informed guide based on Bitcoin Dominance, helping users to prepare before the market makes its decisive moves. It distils complex market dynamics into easily digestible sections.

Key Features & Components

Color-Coded Horizontal Zones: The indicator draws fixed horizontal bands on the BTC.D chart, each representing a distinct phase of the altcoin market cycle.

Descriptive Labels: Each zone is clearly labeled with its strategic meaning (e.g., "Alts are dead," "Danger Zone") and the corresponding BTC.D percentage range, positioned to the right of the price action for clarity.

Consistent Aesthetics: All text within the labels is rendered in white for optimal visibility across the colored zones.

Symbol Restriction: The indicator includes an automatic check to ensure it only draws its visuals when applied specifically to the CRYPTOCAP:BTC.D chart. If applied to another chart, it displays a helpful message and remains invisible to prevent confusion.

Methodology & Interpretation

The indicator's methodology is based on the historical behavior of Bitcoin Dominance during various market cycles, particularly the 2021 bull run. Each zone provides a specific interpretation for altcoin strategy:

Grey Zone (BTC.D 60-70%+): "Alts Are Dead"

Interpretation: When Bitcoin Dominance is in this grey zone (typically above 60%), Bitcoin is king, and capital remains concentrated in BTC. This indicates that alt season is largely inactive or "dead". This phase is generally not conducive for aggressive altcoin trading.

Blue Zone (BTC.D 55-60%): "Alt Season Loading"

Interpretation: As BTC.D drops into this blue zone (below 60%), it signals that the market is "heating up" for altcoins. This is the time to start planning and executing your initial positions in high-conviction large-cap and strong narrative plays, as capital begins to look for more risk.

Green Zone (BTC.D 50-55%): "Alt Season Underway"

Interpretation: Entering this green zone (below 55%) signifies that "real momentum" is building, and alt season is genuinely "underway". Money is actively flowing from Ethereum into large and mid-cap altcoins. If you've positioned correctly, your portfolio should be showing strong gains in this phase.

Orange Zone (BTC.D 45-50%): "Alt Season Ending"

Interpretation: As BTC.D dips into this orange zone (below 50%), it suggests that altcoin dominance is reaching its peak, indicating the "ending" phase of alt season. While euphoria might be high, this is a critical warning zone to prepare for profit-taking, as it's a phase of "peak risk".

Red Zone (BTC.D Below 45%): "Danger Zone - Alts Overheated"

Interpretation: This red zone (below 45%) is the most critical "DANGER ZONE". It historically marks the point of maximum froth and risk, where altcoins are overheated. This is the decisive signal to aggressively take profits, de-risk, and exit positions to preserve your capital before a potential sharp correction. Historically, dominance has gone as low as 39-40% in this phase.

How to Use

Open TradingView and search for the BTC.D symbol to load the Bitcoin Dominance chart and view the indicator.

Double click the indicator to access settings.

Inputs/Settings

The indicator's zone boundaries are set to historically relevant levels for consistency with the Alt Season Blueprint strategy. However, the colors of each zone are fully customizable through the indicator's settings, allowing users to personalize the visual appearance to their preference. You can access these color options in the indicator's "Settings" menu once it's added to your chart.

Disclaimer

This indicator is provided for informational and educational purposes only. It is not financial advice. Trading cryptocurrencies involves substantial risk of loss and is not suitable for every investor. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

About the Author

This indicator was developed by Nick from Lab of Crypto.

Release Notes

v1.0 (June 2025): Initial release featuring color-coded horizontal BTC.D zones with descriptive labels, based on Alt Season Blueprint strategy. Includes symbol restriction for correct chart application and consistent white text.

PLR-Z For Loop🧠 Overview

PLR-Z For Loop is a trend-following indicator built on the Power Law Residual Z-score model of Bitcoin price behavior. By measuring how far price deviates from a long-term power law regression and applying a custom scoring loop, this tool identifies consistent directional pressure in market structure. Designed for BTC, this indicator helps traders align with macro trends.

🧩 Key Features

Power Law Residual Model: Tracks deviations of BTC price from its long-term logarithmic growth curve.

Z-Score Normalization: Applies long-horizon statistical normalization (400/1460 bars) to smooth residual deviations into a usable trend signal.

Loop-Based Trend Filter: Iteratively scores how often the current Z-score exceeds prior values, emphasizing trend persistence over volatility.

Optional Smoothing: Toggleable exponential smoothing helps filter noise in choppier market conditions.

Directional Regime Coloring: Aqua (bullish) and Red (bearish) visuals reinforce trend alignment across plots and candles.

🔍 How It Works

Power Law Curve: Price is compared against a logarithmic regression model fitted to historical BTC price evolution (starting July 2010), defining structural support, resistance, and centerline levels.

Residual Z-Score: The residual is calculated as the log-difference between price and the power law center.

This residual is then normalized using a rolling mean (400 days) and standard deviation (1460 days) to create a long-term Z-score.

Loop Scoring Logic:

A loop compares the current Z-score to a configurable number of past bars.

Each higher comparison adds +1, and each lower one subtracts -1.

The result is a trend persistence score (z_loop) that grows with consistent directional momentum.

Smoothing Option: A user-defined EMA smooths the score, if enabled, to reduce short-term signal noise.

Signal Logic:

Long signal when trend score exceeds long_threshold.

Short signal when score drops below short_threshold.

Directional State (CD): Internally manages the current market regime (1 = long, -1 = short), controlling all visual output.

🔁 Use Cases & Applications

Macro Trend Alignment: Ideal for traders and analysts tracking Bitcoin’s structural momentum over long timeframes.

Trend Persistence Filter: Helps confirm whether the current move is part of a sustained trend or short-lived volatility.

Best Suited for BTC: Built specifically on the BNC BLX price history and Bitcoin’s power law behavior. Not designed for use with other assets.

✅ Conclusion

PLR-Z For Loop reframes Bitcoin’s long-term power law model into a trend-following tool by scoring the persistence of deviations above or below fair value. It shifts the focus from valuation-based mean reversion to directional momentum, making it a valuable signal for traders seeking high-conviction participation in BTC’s broader market cycles.

⚠️ Disclaimer

The content provided by this indicator is for educational and informational purposes only. Nothing herein constitutes financial or investment advice. Trading and investing involve risk, including the potential loss of capital. Always backtest and apply risk management suited to your strategy.

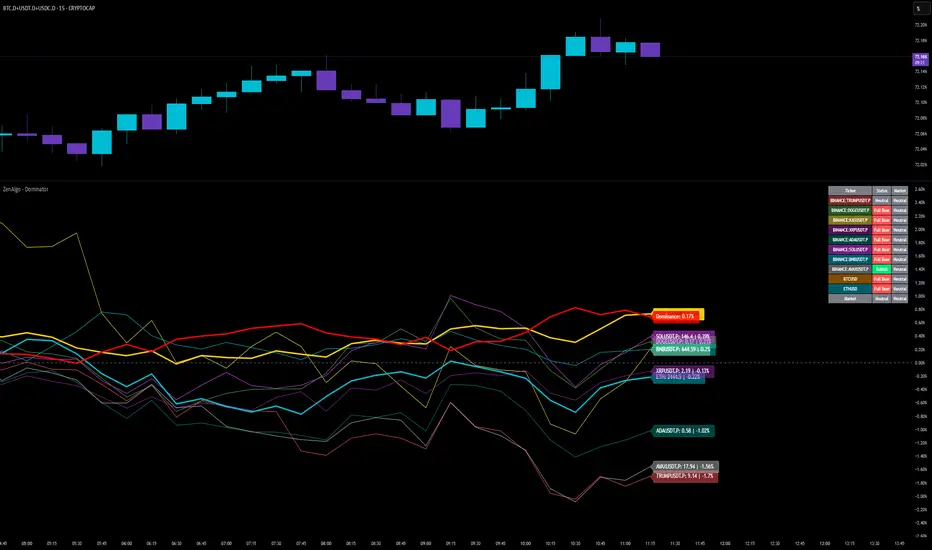

ZenAlgo - DominatorThis indicator provides a structured multi-ticker overview of market momentum and relative strength by analyzing short-term price behavior across selected assets in comparison with broader crypto dominance and Bitcoin/ETH performance.

Ticker and Market Data Handling

The script accepts up to 9 user-defined symbols (tickers) along with BTCUSD and ETHUSD. For each symbol:

It retrieves the current price.

It also requests the daily opening price from the "D" timeframe to compute intraday percentage change.

For BTC, ETH, and dominance (sum of BTC, USDT, and USDC dominance), daily change is calculated using this same method.

This comparison enables tracking relative performance from the daily open, which provides meaningful insight into intraday strength or weakness among different assets.

Dominance Logic

The indicator aggregates dominance data from BTC , USDT , and USDC using TradingView’s CRYPTOCAP indices. This combined dominance is used as a reference in directional and status calculations. ETH dominance is also analyzed independently.

Changes in dominance are used to infer whether market attention is shifting toward Bitcoin/stablecoins (typically indicating risk-off sentiment) or away from them (typically risk-on behavior, benefiting altcoins).

Price Direction Estimation

The script estimates directional bias using an EMA-based deviation technique:

A short EMA (user-defined lookback , default 4 bars) is calculated.

The current close is compared to the EMA to assess directional bias.

Recent candle changes are also inspected to confirm a consistent short-term trend (e.g., 3 consecutive higher closes for "up").

A small threshold is used to avoid classifying flat movements as trends.

This directionality logic is applied separately to:

The selected ticker's price

BTC price

Combined dominance

This allows the script to contextualize the movement of each asset within broader market conditions.

Market Status Evaluation

A custom function analyzes ETH and BTC dominance trends along with their relative strength to define the overall market regime:

Altseason is identified when BTC dominance is declining, ETH dominance rising, and ETH outperforms BTC.

BTC Season occurs when BTC dominance is rising, ETH dominance falling, and BTC outperforms ETH.

If neither condition is met, the state is Neutral .

This classification is shown alongside each ticker's row in the table and helps traders assess whether market conditions favor Bitcoin, Ethereum, or altcoins in general.

Ticker Status Classification

Each ticker is analyzed independently using the earlier directional logic. Its status is then determined as follows:

Full Bull : Ticker is trending up while dominance is declining or BTC is also rising.

Bullish : Ticker is trending up but not supported by broader bullish context.

Bearish : Ticker is trending down but without broader confirmation.

Full Bear : Ticker is trending down while dominance rises or BTC falls.

Neutral : No strong directional bias or conflicting context.

This classification reflects short-term momentum and macro alignment and is color-coded in the results table.

Table Display and Plotting

A configurable table is shown on the chart, which:

Displays the name and status of each selected ticker.

Optionally includes BTC, ETH, and market state.

Uses color-coding for intuitive interpretation.

Additionally, price changes from the daily open are plotted for each selected ticker, BTC, ETH, and combined dominance. These values are also labeled directly on the chart.

Labeling and UX Enhancements

Labels next to the current candle display price and percent change for each active ticker and for BTC, ETH, and combined dominance.

Labels update each bar, and old labels are deleted to avoid clutter.

Ticker names are dynamically shortened by stripping exchange prefixes.

How to Use This Indicator

This tool helps traders:

Spot early rotations between Bitcoin and altcoins.

Identify intraday momentum leaders or laggards.

Monitor which tickers align with or diverge from broader market trends.

Detect possible sentiment shifts based on dominance trends.

It is best used on lower to mid timeframes (15m–4h) to capture intraday to short-term shifts. Users should cross-reference with longer-term trend tools or structural indicators when making directional decisions.

Interpretation of Values

% Change : Measures intraday move from daily open. Strong positive/negative values may indicate breakouts or reversals.

Status : Describes directional strength relative to market conditions.

Market State : Gives a general bias toward BTC dominance, ETH strength, or altcoin momentum.

Limitations & Considerations

The indicator does not analyze liquidity or volume directly.

All logic is based on short-term movements and may produce false signals in ranging or low-volume environments.

Dominance calculations rely on external CRYPTOCAP indices, which may differ from exchange-specific flows.

Added Value Over Other Free Tools

Unlike basic % change tables or price overlays, this indicator:

Integrates dominance-based macro context into ticker evaluation.

Dynamically classifies market regimes (BTC season / Altseason).

Uses multi-factor logic to determine ticker bias, avoiding single-metric interpretation.

Displays consolidated information in a table and chart overlays for rapid assessment.

SSRO Z-ScoreSSRO Z-Score Indicator — Description

What it does:

This indicator measures the Stablecoin Supply Ratio (SSR) relative to Bitcoin’s market cap and calculates a normalized Z-Score of this ratio to help identify potential market tops and bottoms in the crypto market.

How it works:

The Stablecoin Supply Ratio (SSR) is calculated by dividing Bitcoin’s market capitalization by the combined market capitalization of major stablecoins (USDT, USDC, TUSD, DAI, FRAX).

The SSR is then smoothed over a user-defined lookback period to reduce noise.

A Z-Score is computed by normalizing the SSR over a specified moving window, which shows how far the current SSR deviates from its historical average in terms of standard deviations.

This Z-Score is further smoothed using an exponential moving average (EMA) to filter short-term volatility.

How to read the Z-Score:

Z-Score = 0: SSR is at its historical average.

Z-Score > 0: SSR is above average, indicating Bitcoin’s market cap is relatively high compared to stablecoin supply, potentially signaling bullish market conditions.

Z-Score < 0: SSR is below average, indicating stablecoin supply is high relative to Bitcoin’s market cap, possibly signaling bearish pressure or increased liquidity waiting to enter the market.

Upper and Lower Bands: These user-defined levels (e.g., +2 and -2) represent thresholds for extreme conditions. Values above the upper band may indicate overbought or overheated market conditions, while values below the lower band may indicate oversold or undervalued conditions.

Additional Features: