SpeedBullish Strategy Confirm V6.2SpeedBullish Strategy Confirm V6.2

SpeedBullish V6.2 is an advanced price-action + indicator-based strategy designed to confirm trend strength and signal entries with high precision. This version builds on the W/M pattern structure and adds dynamic filtering with EMA, MACD Histogram, RSI, ATR, and Volume.

✅ Signal Conditions

🔹 Buy Signal:

Price above EMA10 or EMA15

MACD Histogram crosses above 0

RSI > 50

(Optional) Higher low via Pivot Low

(Optional) ATR > ATR SMA * Multiplier

(Optional) Volume > SMA * Multiplier

🔻 Sell Signal:

Price below EMA10 or EMA15

MACD Histogram crosses below 0

RSI < 50

(Optional) Lower high via Pivot High

(Optional) Confirmed high volatility and volume

⚙️ Strategy Features

MACD Histogram for momentum shift detection

RSI filtering for momentum confirmation

EMA10/15 for trend direction

ATR-based volatility filter

Volume confirmation filter

Dynamic TP/SL + Trailing Stop

Webhook Integration for MT5 auto-trade

Visual signal markers + background highlight

🔔 Alerts

Alerts are sent in JSON format via alert() with the current symbol, action (buy/sell), and price. Webhook endpoint and secret key are configurable.

📈 How to Use

Attach the strategy to any symbol and timeframe

Customize filters and confirmations to fit your market conditions

Enable webhook alerts for integration with your MT5 Expert Advisor or trading bot

Backtest and optimize before live deployment

在腳本中搜尋"bot"

Cyber Strategy V1Сyber Strategy V1 – Indicator Testing & Strategy Execution Framework

✅ Overview

Cyber Strategy V1 is a closed-source strategy framework engineered to turn any of yours external indicator into a systematic, rule-based trading system. Designed for rigorous testing and live deployment, it combines multi-signal inputs, confirmations and automated execution paths to help traders and developers validate signal quality and manage risk with precision.

✅ Core Functionality

Multi-Source Independent Signal Inputs

Reversal Logic

Take Profit: up to 5 staggered TP levels, specified as percentage

Stop Loss: configurable via fixed percentage or dynamic SL that trails a reverse signals.

✅ Statistical Drawdown Analysis

For all profitable trades, tracks the maximum intratrade drawdown.

Computes percentile levels of profitable trades that hits minimum drawdowns to inform:

Entry buffer zones (e.g. avoid entering during transient noise)

Partial entry scaling prices.

✅ Signal Confirmation

Optional confirmation delays: hold entry until other signal section send a confirmation from another indicator.

✅ Automated Execution Integrations

Cornix Text Alerts: Generates pre-formatted alerts compatible with Cornix for semi-automated or bot trading.

Webhook Support: Emits JSON payloads on order-fill events to any endpoint, enabling full automation through third-party services or custom order-routing systems.

Important Notes

⚠️ THIS STRATEGY DOES NOT INCLUDE INDICATORS. Examples shown on screenshots use third-party tools. NO PROPRIETARY INDICATORS INCLUDED: Cyber Strategy V1 relies entirely on external signal inputs.

⚠️ All backtesting parameters are customizable; thorough backtesting under realistic slippage, fees and spread assumptions is essential before live deployment.

Trend Harvester PRO Trend Harvester PRO – Adaptive Trend-Following Strategy for Crypto

Trend Harvester PRO is a fully systematic trend-following strategy built for cryptocurrency markets on intraday timeframes — particularly optimized for the 1-hour chart. The script combines ZLEMA-based trend tracking, momentum confirmation, and a volatility-aware filter to detect high-probability directional moves with clarity and precision.

This is not a mashup of random indicators — each component serves a specific purpose in validating trends, avoiding choppy zones, and timing entries responsibly.

🔍 Strategy Logic Overview

The core objective is to detect sustainable, real-time trends and exit with multi-stage profit targets. To do this, the script uses several layers of confirmation:

1. 📊 ZLEMA Trend Engine (Zero Lag EMA)

This is the backbone of the strategy.

ZLEMA (Zero-Lag EMA) is a moving average that minimizes lag by adjusting for past data offset.

The strategy uses a fast ZLEMA and a slow ZLEMA, combined with a slope calculation, to assess the current trend.

When:

Fast ZLEMA > Slow ZLEMA

The ZLEMA is rising (positive slope)

→ The market is considered in an uptrend.

Conversely, if:

Fast ZLEMA < Slow ZLEMA

The slope is negative

→ The market is considered in a downtrend.

This setup detects not just direction, but also whether the trend has meaningful acceleration.

2. ⚡ Momentum Confirmation

Trend direction alone isn’t enough — we also need momentum agreement.

The script calculates a smoothed Rate of Change (ROC) to evaluate if momentum supports the direction of the ZLEMA trend.

For long trades: ROC must be positive

For short trades: ROC must be negative

This prevents taking trades where price is crossing moving averages but lacks follow-through power.

3. 🌪️ Volatility Filter

Choppy markets are common in crypto. To reduce false signals:

The script compares short-term volatility (10-bar standard deviation of price changes) to longer-term volatility.

If the ratio is too high (i.e., short-term volatility is spiking), the strategy avoids entry.

This ensures trades are only taken when the market is relatively calm and directional — avoiding false breakouts.

4. 🧠 Confirmation Bars + Trend State

Signals only trigger after a certain number of consecutive bars confirm trend direction (confirmBars).

This prevents reacting to just 1 candle and requires consistent evidence of trend.

A state machine is used to track current trend status:

+1 = confirmed uptrend

-1 = confirmed downtrend

0 = neutral / no trade

This trend state changes only after all conditions are met and confirmation bars pass.

5. 🧊 Cooldown Enforcement

After a trade exits (from TP or a trend reversal), the strategy enforces a cooldown period before new entries are allowed. This:

Prevents back-to-back entries on trend flips

Reduces overtrading

Helps avoid whipsaws or same-bar reversal trades

6. 🎯 Multi-Level Take Profits (TP1 & TP2)

Once a trade is entered:

Two limit exits are set automatically:

TP1: Closes 50% of the position at a configurable profit level

TP2: Closes the remaining 50%

If the trend weakens before TP2 is reached, the position is closed early.

Both long and short trades use the same logic, with user-defined percentages.

This system allows for partial profit-taking while keeping a portion of the trade running.

7. 🧾 Built-in Dashboard

The script includes a real-time dashboard showing:

Trend direction: Bullish, Bearish, or Neutral

Whether TP1 / TP2 was hit

Entry price

If currently in a trade

How many bars the trade has been open

This helps monitor strategy performance at a glance without needing extra labels.

8. 🔔 Webhook-Compatible Alerts

The strategy includes custom alerts that can be used for:

Long and Short entries

TP1 and TP2 hits

Exiting trades

These can be integrated into automated bot systems or used manually.

🔒 Non-Repainting Logic

The strategy uses only confirmed bar data (i.e., values from closed bars).

There are no repainting indicators.

Entries and exits are placed using strategy.entry and strategy.exit on confirmed conditions.

✅ How to Use It

Apply the strategy to 1H altcoin charts (BTC, ETH, SOL, etc.).

Tune the TP percentages (longTP1Pct, longTP2Pct, etc.) based on volatility.

Use the dashboard to monitor trend state and trade progress.

Combine with additional tools (like support/resistance or volume) for higher confluence.

Use the date filter to run backtests over defined periods.

⚠️ Risk Management Notice

This strategy does not include stop losses by default. It is designed to exit based on trend reversal or take-profit limits.

Always backtest thoroughly and use realistic sizing.

Do not risk more than 5–10% of your account on any trade.

Past results do not guarantee future performance. This tool is for educational and research purposes.

🧬 What Makes This Original

Trend Harvester PRO was built from scratch with tightly integrated logic:

ZLEMA tracks early trend direction with low lag

ROC confirms momentum in the same direction

Volatility filter avoids false setups

Multi-bar confirmation and cooldown logic control trade pacing

Dual TP exits manage partial profit-taking

A live dashboard makes real-time tracking intuitive

Unlike mashups of indicators with no synergy, each component here directly supports the quality of trade decisions, and the logic is modular, transparent, and non-repainting.

SmartScale Envelope DCA This is a Dollar-Cost Averaging (DCA) long strategy that buys when price dips below a moving average envelope and adds to the position in a stepwise, risk-controlled way. It uses up to 8 buy-ins, applies a cooldown between entries, and exits based on either a take profit from average entry price or a stop loss. Backtest range limits trades to the last 365 days for backtest control.

All input settings can and should be adjusted to the chart, as volatility in price action varies. Simply go into the inputs settings, and start from the top and move down to get better backtest results. Moving from the top down has been proven to give the best results. Then, move to properties and set your order size, pyramiding, and so on. It may be necessary to then fine tune your adjustments a second time to dial it in.

Works well on 1 hour time frames and in volatility.

Happy Trading!

Prime Trend ReactorIntroduction

Prime Trend Reactor is an advanced crypto trend-following strategy designed to deliver precision entries and exits based on a multi-factor trend consensus system.

It combines price action, adaptive moving averages, momentum oscillators, volume analysis, volatility signals, and higher timeframe trend confirmation into a non-repainting, fully systematic approach.

This strategy is original: it builds a unique trend detection matrix by blending multiple forms of price-derived signals through weighted scoring, rather than simply stacking indicators.

It is not a mashup of public indicators — it is engineered from the ground up using custom formulas and strict non-repainting design.

It is optimized for 1-hour crypto charts but can be used across any asset or timeframe.

⚙️ Core Components

Prime Trend Reactor integrates the following custom components:

1. Moving Averages System

Fast EMA (8), Medium EMA (21), Slow EMA (50), Trend EMA (200).

Detects short-term, medium-term, and long-term trend structures.

EMA alignment is scored as part of the trend consensus system.

2. Momentum Oscillators

RSI (Relative Strength Index) with Smoothing.

RMI (Relative Momentum Index) custom-calculated.

Confirms price momentum behavior aligned with trend.

3. Volume Analysis

CMF (Chaikin Money Flow) for accumulation/distribution pressure.

OBV (On Balance Volume) EMA Cross for volume flow confirmation.

4. Volatility and Price Structure

Vortex Indicator (VI+ and VI-) for trend strength and directional bias.

Mean-Extreme Price Engine blends closing price with extremes (high/low) based on user-defined ratio.

5. Structure Breakout Detection

Detects structure breaks based on highest high/lowest low pivots.

Adds weight to trend strength on fresh breakouts.

6. Higher Timeframe Confirmation (HTF)

Uses higher timeframe EMAs and close to confirm macro-trend direction.

Smartly pulls HTF data with barmerge.lookahead_off to avoid repainting.

🔥 Entry and Exit Logic

Long Entry: Triggered when multi-factor trend consensus turns strongly bullish.

Short Entry: Triggered when consensus flips strongly bearish.

Take Profits (TP1/TP2):

TP1: Partial 50% profit at small target.

TP2: Full 100% close at larger target.

Exit on Trend Reversal:

If trend consensus reverses before hitting TP2, the strategy exits early to protect capital.

TP Hits and Trend Reversals fire real-time webhook-compatible alerts.

🧩 Trend Consensus Matrix (Original Concept)

Instead of relying on a single indicator, Prime Trend Reactor calculates a weighted score using:

EMA Alignment

Momentum Oscillators (RSI + RMI)

Volume Analysis

Volatility (Vortex)

Higher Timeframe Bias

Each component adds a weighted contribution to the final trend strength score.

Only when the weighted score exceeds a user-defined threshold does the system allow entries.

This multi-dimensional scoring system is original and engineered specifically to avoid noisy or lagging traditional signals.

📈 Visualization and Dashboard

Custom EMA Clouds dynamically fill between Fast/Medium EMAs.

Colored Candles show real-time trend direction.

Dynamic Dashboard displays:

Current Position (Long/Short/Flat)

Entry Price

TP1 and TP2 Hit Status

Bars Since Entry

Win Rate (%)

Profit Factor

Current Trend Signal

Consensus Score (%)

🛡️ Non-Repainting Design

All trend calculations are based on current and confirmed past data.

HTF confirmations use barmerge.lookahead_off.

No same-bar entries and exits — enforced logic prevents overlap.

No lookahead bias.

Strict variable handling ensures confirmed-only trend state transitions.

✅ 100% TradingView-approved non-repainting behavior.

📣 Alerts and Webhooks

This strategy includes full TradingView webhook support:

Long/Short Entries

TP1 Hit (Partial Exit)

TP2 Hit (Full Exit)

Exit on Trend Reversal

All alerts use constant-string JSON formatting compliant with TradingView multi-exchange bots:

📜 TradingView Mandatory Disclaimer

This strategy is a tool to assist in market analysis. It does not guarantee profitability. Trading financial markets involves risk. You are solely responsible for your trading decisions. Past performance does not guarantee future results.

Sniper Core XT🔫 SNIPER CORE XT — ZLEMA-Based Trend + Momentum Strategy for Crypto

⚙️ How It Works (What Makes It Unique):

Sniper Core XT is a fully automated, non-repainting crypto strategy that combines a purpose-built trend detection system with volatility, volume, and momentum confirmation. It is designed from scratch in Pine Script v5 and optimized for bot deployment, copy trading, or semi-manual execution on the 1H timeframe.

Unlike a simple indicator mashup, this strategy builds its logic around one core component — ZLEMA (Zero-Lag Exponential Moving Average) — and then selectively adds only supporting filters that refine trend detection and execution logic.

🧠 Core Logic & Components:

ZLEMA Trend Engine:

The main trend signal comes from a fast vs. slow ZLEMA crossover. ZLEMA is chosen for its responsiveness and minimal lag, giving traders earlier entries without the noise of standard EMAs.

Vortex Direction & Strength Filter:

Uses Vortex Indicator internals to measure directional conviction. The strategy only enters if the vortex aligns with ZLEMA direction and shows minimum strength based on a customizable threshold.

Volume Confirmation via ZLEMA of Volume:

Filters out weak moves by confirming that current volume exceeds the ZLEMA-smoothed average of volume, creating adaptive volume thresholds.

Adaptive Momentum Filter:

Momentum is measured by a normalized rate-of-change adjusted for volatility (ATR). This helps avoid flat market entries and overextends.

Hardcoded Stop Loss (2%) and Dual TP:

TP1: 50% profit scale-out

TP2: Full closure

Stop loss exits on bar close, not using built-in SL/TP orders — this allows reentry if conditions remain favorable.

Real-Time Non-Canvas Dashboard:

A lightweight table shows entry price, trend direction, TP1/TP2/SL hit status, and bars in trade — all configurable for screen position and font size.

One-Bar Cooldown Mechanism:

Prevents entering and exiting on the same bar. Reinforces realistic execution logic and avoids repaint artifacts.

🧪 Strategy Use & Applications:

Designed for 1H trading of trending crypto pairs

Works well in medium-to-high volatility conditions

Fully supports multi-exchange alerts for integration with:

WunderTrading

3Commas

Cornix

PineConnector

🛡️ Strategy Style:

Feature Value

Repainting ❌ Never

Entry Cooldown ✅ 1-Bar

SL Handling ✅ 2% from entry (hardcoded)

TP1/TP2 ✅ Built-in (limit orders)

Alert Compatible ✅ Fully supported

Timeframe 🕒 1H recommended

⚠️ Disclaimer:

This is not financial advice. All signals are based on historical logic and may differ in live markets. Always use proper position sizing and risk management.

📌 Publishing Notes

This strategy is original and built from scratch. While it uses ZLEMA and Vortex as components, all logic — including volume filters, momentum filters, TP/SL logic, and dashboard — has been custom-coded and tested specifically for crypto trend-following on the 1H timeframe.

Alpha Trigger CoreAlpha Trigger Core — Trend Momentum Strategy with Dual Take Profit System

Alpha Trigger Core is a precision-engineered trend-following strategy developed for crypto and altcoin markets. Unlike simple indicator mashups, this system was built from the ground up with a specific logic framework that integrates trend, momentum, volatility, and structure validation into a single unified strategy.

It is not a random combination of indicators, but rather a coordinated system of filters that work together to increase signal quality and minimize false positives. This makes it especially effective on trending assets like BTC, ETH, AVAX, and SOL on the 1-hour chart.

🔍 How It Works

This strategy fuses multiple advanced filters into a cohesive signal engine:

🔹 Trend Identification

A hybrid model combining:

Kalman Filter — Smooths price noise with predictive tracking.

SuperTrend Overlay — Confirms directional bias using ATR.

ZLEMA Envelope — Defines dynamic upper/lower bounds based on price velocity.

🔹 Momentum Filter

Uses a ZLEMA-smoothed CCI to identify accelerating moves.

Long entries require a rising 3-bar CCI sequence.

Short entries require a falling 3-bar CCI sequence.

🔹 Volatility Strength Filter (Vortex Indicator)

Validates entries only when Vortex Diff exceeds a customizable threshold.

Prevents low-volatility "chop zone" trades.

🔹 Wick Trap Filter

Filters out false breakouts driven by liquidity wicks.

Validates that body structure supports the breakout.

📈 Entry & Exit Logic

Long Entry: All trend, momentum, volatility filters must align bullishly and wick traps must be absent.

Short Entry: All filters must align bearishly, with no wick rejection.

Early Exit: Uses ZLEMA slope crossover to exit before a full trend reversal is confirmed.

🎯 Take Profit System

TP1: Takes 50% profit at a user-defined % target.

TP2: Closes remaining 100% at second target.

Cooldown: Prevents immediate reentry and ensures clean position transitions.

📊 Real-Time Strategy Dashboard

Tracks and displays:

Position status (Long, Short, Flat)

Entry Price

TP1/TP2 Hit status

Win Rate (%)

Profit Factor

Bars Since Entry

Fully customizable position & font size

🤖 Bot-Ready Multi-Exchange Alerts

Compatible with WonderTrading, 3Commas, Binance, Bybit, and more.

Customizable comment= tags for entry, exit, TP1, and TP2.

Fully alert-compatible for webhook integrations.

📌 Suggested Use

Best used on trending crypto pairs with moderate-to-high volatility. Recommended on the 1H timeframe for altcoins and majors. Can be used for manual confirmation or automated trading.

🔒 Script Transparency

This is a closed-source script. However, the description above provides a transparent breakdown of the strategy’s core logic, filters, and execution model — ensuring compliance with TradingView’s publishing guidelines.

⚠️ Trading Disclaimer

This script is for educational purposes only and is not financial advice. Always conduct your own analysis before making investment decisions. Past performance does not guarantee future results. Use this strategy at your own risk.

IronBot v4IronBot v4 – Trading Strategy Overview

1. Quick Context

IronBot v4 is a trading strategy designed for users who want a simple yet effective approach to reading the markets. It uses a combination of Fibonacci retracement levels, custom logic triggers, and innovative modules (EMA validation, Iron Impulse Shield and Iron Auto Volume Detector) to identify potential entry and exit points, strengthening the strategy’s detection of sudden market volatility or shifts in trading volume.

2. Theoretical Details

Fibonacci Analysis

The script identifies recent market highs and lows, then calculates key Fibonacci levels (high- and low-based). These levels can help confirm potential reversals or trends.

EMA Option

When enabled, the exponential moving average (EMA) offers additional validation for trade entries. If the current price remains above a certain EMA threshold, long positions may be favored; conversely, if it stays below the EMA, short positions may be initiated.

IIS (Iron Impulse Shield)

IIS helps to filter out risky trades by measuring recent price shocks or surges. If an extreme movement is detected, the strategy may temporarily disable longs or shorts to avoid false signals.

IAVD (Iron Auto Volume Detector)

This functionality automatically detects the average market volume over a defined period (regardless of the market, since it relies on real data). When entering a position, it ensures that overall volume is high enough to confirm a genuinely active, robust market. By providing an additional filter, it can strengthen the decision-making process whenever the market’s participation level is in question.

Panel

IronBot v4 displays a real-time backtest panel that summarizes the selected configuration (including the current pair, analysis window, enabled filters), as well as showing net profit, applicable exchange fees, country taxes, and the final net balance. This gives traders an immediate overview of strategy performance and risk metrics.

What Pinescript Adds Visually

The script plots:

Fibonacci levels (highlighting potential reversal zones)

Trend lines indicating bullish (green) or bearish (red) lean

Optional EMA line

Optional Fibonacci forecast lines for anticipating future moves

Automatic labeling of entry, take-profit, and stop-loss levels, indicating the profit percentage of each trade.

3. Explanation of Inputs

The strategy exposes multiple inputs that can be toggled or configured by the user:

Analysis Window : Dictates how many bars to consider for high/low calculations and the fib retracement thresholds.

TRADES

Display TP/SL: For displaying Take profits and Stop loss.

Display Forecast: When enabled, this feature calculates and projects possible future Fibonacci retracements using historical data, helping traders anticipate potential upcoming trade setups.

Leverage: Only used for the Panel and not for trades. Lets you amplify your position size; higher leverage increases potential gains but also heightens risk. TradingView strategy is using properties for doing this.

Exchange Maker Fees & Exchange Taker Fees: Only used for the Panel and not for trades. Define the percentage cost applied by your exchange for maker and taker trades, respectively. These fees are accounted for in final profit calculations of the Panel.

Country Tax: Only used for the Panel and not for trades. Specifies a tax percentage to be deducted from net profits.

STOP LOSS and TAKE PROFITS

Stop-Loss & Take-Profit Parameters: Controls the percentage distances at which the strategy will exit positions. Additionally, you can configure up to four distinct take-profit levels (TP1 through TP4). Each level should be higher target than the previous one, and you can assign a specific percentage of the total position to close at each TP, ensuring the sum equals 100%. A break-even feature is also available when multiple TPs are used.

EMA

EMA (Exponential Moving Average) Option: When enabled, the strategy opens long trades only if the current price is above the specified EMA length, and opens short trades only if it is below that threshold.

PANELS

Show Panel: For displaying the backtest integrated panel.

IRON IMPULSE SHIELD (IIS)

IIS (Iron Impulse Shield) Option: When enabled, IIS continuously monitors recent price volatility depending on the analysis window set. If the market experiences an extreme surge or drop beyond a specified threshold, IIS temporarily blocks new long or short positions.

IRON AUTO VOLUME DETECTOR (IAVD)

IAVD (Iron Auto Volume Detector) Option: When enabled, it continuously measures the average market volume over a special period, irrespective of the specific trading pair. This ensures that IronBot v4 focuses on markets with robust participation, reducing the likelihood of entering trades during low-liquidity conditions.

By changing these values, IronBot v4 reacts differently to market structure and risk management requirements. Stop-loss and take-profit levels will adjust accordingly, while advanced filters (like EMA or IIS) influence when trades can open.

4. TradingView Strategy Properties

IronBot v4 uses the built-in TradingView “strategy” functionality. In particular:

Order Placement: The code calls strategy.entry() and strategy.close() for direct orders, ensuring signals are sent immediately (no limit orders are used). This helps connect with exchange signal bots for automated execution.

Initial Capital: The code uses initial capital defined in properties for calculating Net balance in the integrated panel.

On bar close: This strategy fill orders on bar close.

Pyramiding: This strategy can take only 1 successive trade in the same direction

Be careful to configure your leverage input depending on your strategy properties.

5. Visualization

5. Purpose & Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always confirm your own risk tolerance and consult a financial professional before placing live trades. Trading leveraged products can involve substantial risk of loss.

DCA (ASAP) V0 PTTScript Name: DCA (ASAP) V0 PTT

Detailed Description:

This script implements the Dollar-Cost Averaging (DCA) strategy, allowing you to automatically manage buy/sell orders safely and efficiently. Below are the key features of this script:

1. Purpose and Operation:

o Supports both Long and Short trading modes.

o Designed to optimize profitability using the DCA method, where Safety Orders are triggered when the price moves against the predicted direction.

o Helps users maintain their Target Profit in various market conditions.

2. Main Features:

o Automatic Order Placement: The initial Base Order is opened as soon as no active order exists.

o Safety Order Management: Safety Orders are automatically placed when the price moves against the initial order. The volume and distance of these orders are customizable.

o Order Closing: Orders are closed upon reaching the Target Profit, accounting for transaction fees.

o Detailed Information Display: Displays open orders, trading statistics, and performance metrics directly on the chart.

3. Customizable Parameters:

o Base Order Size: The size of the initial order.

o Target Profit (%): Target profit as a percentage of the total order volume.

o Safety Order Size: The size of each Safety Order.

o Price Deviation (%): The percentage distance between consecutive Safety Orders.

o Safety Order Volume Scale: The scaling factor for increasing the volume of subsequent Safety Orders.

o Max Safety Orders: The maximum number of Safety Orders allowed per deal.

4. Unique Features:

o Backtest Range Support: Enables you to limit backtesting to a specific time range of interest.

o Comprehensive Statistics: Displays detailed tables including open trades, pending orders, ROI, trading days, and realized profit.

o Integrated Trading Fees: Includes transaction fees in profit calculations for precise results.

5. Usage Instructions:

o Select the trading mode (Long or Short) from the "Strategy" input.

o Customize parameters such as Base Order, Safety Order, and Target Profit according to your requirements and the asset being traded.

o Monitor the performance of the strategy through the displayed information tables.

Notes:

• This script does not disclose detailed calculation logic but provides an overview of the concepts and usage.

• Designed for trading on exchanges that support margin or spot trading.

TradeShields Strategy Builder🛡 WHAT IS TRADESHIELDS?

This no-code strategy builder is designed for traders on TradingView, offering an intuitive platform to create, backtest, and automate trading strategies. While identifying signals is often straightforward, the real challenge in trading lies in managing risk and knowing when not to trade. It equips users with advanced tools to address this challenge, promoting disciplined decision-making and structured trading practices.

This is not just a collection of indicators but a comprehensive toolkit that helps identify high-quality opportunities while placing risk management at the core of every strategy. By integrating customizable filters, robust controls, and automation capabilities, it empowers traders to align their strategies with their unique objectives and risk tolerance.

_____________________________________

🛡 THE GOAL: SHIELD YOUR STRATEGY

The mission is simple: to shield your strategy from bad trades . Whether you're a seasoned trader or just starting, the hardest part of trading isn’t finding signals—it’s avoiding trades that can harm your account. This framework prioritizes quality over quantity , helping filter out suboptimal setups and encouraging disciplined execution.

With tools to manage risk, avoid overtrading, and adapt to changing market conditions, it protects your strategy against impulsive decisions and market volatility.

_____________________________________

🛡 HOW TO USE IT

1. Apply Higher Timeframe Filters

Begin by analyzing broader market trends using tools like the 200 EMA, Ichimoku Cloud, or Supertrend on higher timeframes (e.g., daily or 4-hour charts).

- Example: Ensure the price is above the 200 EMA on the daily chart for long trades or below it for short trades.

2. Identify the Appropriate Entry Signal

Choose an entry signal that aligns with your model and the asset you're trading. Options include:

Supertrend changes for trend reversals.

Bollinger Band touches for mean-reversion trades.

RSI strength/weakness for overbought or oversold conditions.

Breakouts of key levels (e.g., daily or weekly highs/lows) for momentum trades.

MACD and TSI flips.

3. Determine Take-Profit and Stop-Loss Levels

Set clear exit strategies to protect your capital and lock in profits:

Use single, dual, or triple take-profit levels based on percentages or price levels.

Choose a stop-loss type, such as fixed percentage, ATR-based, or trailing stops.

Optionally, set breakeven adjustments after hitting your first take-profit target.

4. Apply Risk Management Filters

Incorporate risk controls to ensure disciplined execution:

Limit the number of trades per day, week, or month to avoid overtrading.

Use time-based filters to trade during specific sessions or custom windows.

Avoid trading around high-impact news events with region-specific filters.

5. Automate and Execute

Leverage the advanced automation features to streamline execution. Alerts are tailored specifically for each supported platform, ensuring seamless integration with tools like PineConnector, 3Commas, Zapier, and more.

_____________________________________

🛡 CORE FOCUS: RISK MANAGEMENT, AUTOMATION, AND DISCIPLINED TRADING

This builder emphasizes quality over quantity, encouraging traders to approach markets with structure and control. Its innovative tools for risk management and automation help optimize performance while reducing effort, fostering consistency and long-term success.

_____________________________________

🛡 KEY FEATURES

General Settings

Theme Customization : Light and dark themes for a tailored interface.

Timezone Adjustment : Align session times and news schedules with your local timezone.

Position Sizing : Define lot sizes to manage risk effectively.

Directional Control : Choose between long-only, short-only, or both directions for trading.

Time Filters

Day-of-Week Selection : Enable or disable trading on specific days.

Session-Based Trading : Restrict trades to major market sessions (Asia, London, New York) or custom windows.

Custom Time Windows : Precisely control the timeframes for trade execution.

Risk Management Tools

Trade Limits : Maximum trades per day, week, or month to avoid overtrading.

Automatic Trade Closures : End-of-session, end-of-day, or end-of-week options.

Duration-Based Filters : Close trades if take-profit isn’t reached within a set timeframe or if they remain unprofitable beyond a specific duration.

Stop-Loss and Take-Profit Options : Fixed percentage or ATR-based stop-losses, single/dual/triple take-profit levels, and breakeven stop adjustments.

Economic News Filters

Region-Specific Filters : Exclude trades around major news events in regions like the USA, UK, Europe, Asia, or Oceania.

News Avoidance Windows : Pause trades before and after high-impact events or automatically close trades ahead of scheduled news releases.

Higher Timeframe Filters

Multi-Timeframe Tools : Leverage EMAs, Supertrend, or Ichimoku Cloud on higher timeframes (Daily, 4-hour, etc.) for trend alignment.

Chart Timeframe Filters

Precision Filtering : Apply EMA or ADX-based conditions to refine trade setups on current chart timeframes.

Entry Signals

Customizable Options : Choose from signals like Supertrend, Bollinger Bands, RSI, MACD, Ichimoku Cloud, or EMA pullbacks.

Indicator Parameter Overrides : Fine-tune default settings for specific signals.

Exit Settings

Flexible Take-Profit Targets : Single, dual, or triple targets. Exit at significant levels like daily/weekly highs or lows.

Stop-Loss Variability : Fixed, ATR-based, or trailing stop-loss options.

Alerts and Automation

Third-Party Integrations : Seamlessly connect with platforms like PineConnector, 3Commas, Zapier, and Capitalise.ai.

Precision-Formatted Alerts : Alerts are tailored specifically for each platform, ensuring seamless execution. For example:

- PineConnector alerts include risk-per-trade parameters.

- 3Commas alerts contain bot-specific configurations.

_____________________________________

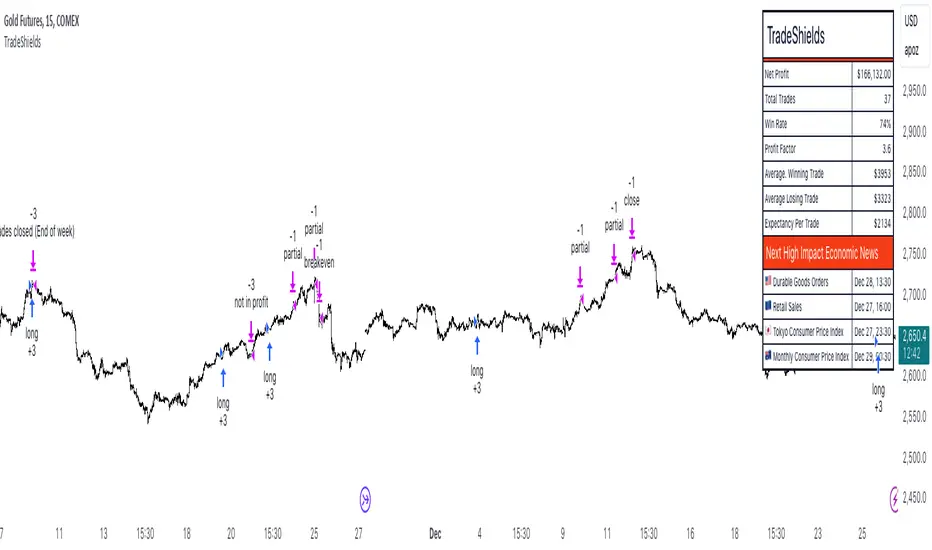

🛡 PUBLISHED CHART SETTINGS: 15m COMEX:GC1!

Time Filters : Trades are enabled from Tuesday to Friday, as Mondays often lack sufficient data coming off the weekend, and weekends are excluded due to market closures. Custom time sessions are turned off by default, allowing trades throughout the day.

Risk Filters : Risk is tightly controlled by limiting trades to a maximum of 2 per day and enabling a mechanism to close trades if they remain open too long and are unprofitable. Weekly trade closures ensure that no positions are carried over unnecessarily.

Economic News Filters : By default, trades are allowed during economic news periods, giving traders flexibility to decide how to handle volatility manually. It is recommended to enable these filters if you are creating strategies on lower timeframes.

Higher Timeframe Filters : The setup incorporates confluence from higher timeframe indicators. For example, the 200 EMA on the daily timeframe is used to establish trend direction, while the Ichimoku cloud on the 30-minute timeframe adds additional confirmation.

Entry Signals : The strategy triggers trades based on changes in the Supertrend indicator.

Exit Settings : Trades are configured to take partial profits at three levels (1%, 2%, and 3%) and use a fixed stop loss of 2%. Stops are moved to breakeven after reaching the first take profit level.

_____________________________________

🛡 WHY CHOOSE THIS STRATEGY BUILDER?

This tool transforms trading from reactive to proactive, focusing on risk management and automation as the foundation of every strategy. By helping users avoid unnecessary trades, implement robust controls, and automate execution, it fosters disciplined trading.

NexTrade

Overview of NexTrade: The Future of Crypto Trading

Introduction

NexTrade is a cutting-edge algorithmic trading platform designed to optimize cryptocurrency trading strategies. Developed by myself, a software engineer with a passion for quantitative development. Over the past year, I have focused on learning and applying quantitative techniques to the crypto space, ultimately crafting a platform that leverages advanced market analysis, automation, and robust risk management to help investors maximize returns while minimizing risk. NexTrade is engineered to help you capitalize on market movements in a fast-paced and highly competitive space, that is Cryptocurrency.

Key Features and Advantages

Sophisticated Market Analysis: NexTrade uses a comprehensive market analysis framework that examines historical trends, price movements, and market conditions across multiple cryptocurrency exchanges. The algorithm identifies trading opportunities by chart analysis on higher timeframes in order to follow trends, allowing it to execute trades at optimal moments.

Multi-Exchange Integration: NexTrade connects to multiple leading cryptocurrency exchanges, such as Binance, Kraken, and Coinbase Pro, to ensure access to diverse liquidity pools. This multi-exchange connectivity allows the platform to execute trades at the most favorable prices, optimizing profitability and minimizing slippage across various platforms. However, we suggest using the exchange with lowest fees possible.

Risk Management: NexTrade’s risk management features such as Stop Losses, ATR Trailing SL, and ADX chop indicator allows us to ensure we are effectively managing our risk.

Backtesting and Optimization: Before going live, NexTrade’s trading strategies undergo rigorous backtesting using historical market data. This enables users to see how strategies would have performed under various conditions, providing transparency and confidence in the platform’s potential for generating consistent returns. Ongoing optimization ensures that strategies evolve in response to market changes.

Real-Time Performance Monitoring: Users have access to detailed, real-time performance reports, tracking key metrics such as trades executed, profits, losses, and overall portfolio performance. This transparency allows investors to make informed decisions and monitor their investments closely at any time.

Market Opportunity

The cryptocurrency market continues to experience rapid growth, with trillions of dollars in trading volume annually. However, it is also notoriously volatile, creating both risk and reward opportunities for traders. To successfully navigate this market, investors need sophisticated tools that can automate the trading process and optimize decisions based on accurate market analysis.

NexTrade was developed to address this need. With its combination of data-driven market analysis, automated execution, and risk management, NexTrade is positioned to help investors gain an edge in a market that is often unpredictable and challenging. The platform offers a reliable, scalable solution to crypto trading, designed for both beginners and seasoned professionals.

Why Invest in NexTrade?

Scalable and Flexible: Whether you’re trading small amounts or large volumes, NexTrade can scale to accommodate your needs. The platform supports multiple exchanges, giving users the flexibility to diversify and grow their investments. Users can start with as low as $100!

Risk-Adjusted Returns: By focusing on risk management, NexTrade aims to deliver returns that are balanced with the level of risk the investor is willing to accept. The algorithm continuously adjusts trading strategies to align with market conditions, maximizing the potential for profits while minimizing the likelihood of significant losses.

24/7 Trading: The cryptocurrency market operates around the clock, and NexTrade is designed to take advantage of this. Its automated nature means that it can execute trades at any time, without the need for human intervention.

Conclusion

NexTrade offers a sophisticated yet accessible solution for investors looking to capitalize on the growth of the cryptocurrency market. With its focus on data-driven analysis, automated trade execution, and advanced risk management, NexTrade empowers investors to achieve optimal returns while managing risk effectively. Whether you are new to crypto or an experienced trader, NexTrade provides the tools needed to stay competitive and succeed in a fast-moving market.

By investing in NexTrade, you are gaining access to a proven algorithmic trading platform that has the potential to enhance your crypto trading strategy and deliver consistent results. The future of cryptocurrency trading is automated, risk-managed, and optimized—and NexTrade is leading the way.

If users wish the enable the chop detector on the bot, which uses ADX, they can turn it on in the settings after the strategu is added to the chart. By default, it is set to false.

TFMTFM Strategy Explanation

Overview

The TFM (Timeframe Multiplier) strategy is a PineScript trading bot that utilizes multiple timeframes to identify entry and exit points.

Inputs

1. tfm (Timeframe Multiplier): Multiplies the chart's timeframe to create a higher timeframe for analysis.

2. lns (Long and Short): Enables or disables short positions.

Logic

Calculations

1. chartTf: Gets the chart's timeframe in seconds.

2. tfTimes: Calculates the higher timeframe by multiplying chartTf with tfm.

3. MintickerClose and MaxtickerClose: Retrieve the minimum and maximum closing prices from the higher timeframe using request.security.

- MintickerClose: Finds the lowest low when the higher timeframe's close is below its open.

- MaxtickerClose: Finds the highest high when the higher timeframe's close is above its open.

Entries and Exits

1. Long Entry: When the current close price crosses above MaxtickerClose.

2. Short Entry (if lns is true): When the current close price crosses below MintickerClose.

3. Exit Long: When the short condition is met (if lns is false) or when the trade is manually closed.

Strategy

1. Attach the script to a chart.

2. Adjust tfm and lns inputs.

3. Monitor entries and exits.

Example Use Cases

1. Intraday trading with tfm = 2-5.

2. Swing trading with tfm = 10-30.

Tips

1. Experiment with different tfm values.

2. Use lns to control short positions.

3. Combine with other indicators for confirmation.

NNFX RSI EMA FVMA MACD ALGOThis Pine Script introduces a cutting-edge trading strategy that seamlessly integrates multiple technical indicators—namely, the Flexible Variable Moving Average ( FVMA ), Relative Strength Index ( RSI ), Moving Average Convergence Divergence ( MACD ), and Exponential Moving Average ( EMA )—to deliver a sophisticated trading experience. This script stands out due to its comprehensive approach, robust risk management, and the inclusion of crucial data tables for various timeframes, making it an invaluable tool for traders seeking to enhance their market performance.

Originality of the Strategy:

The originality of this script lies in its unique combination of multiple powerful indicators, enabling traders to benefit from diverse perspectives on market dynamics. This mashup enhances decision-making processes, providing multiple layers of confirmation for trade entries and exits. The strategy is designed to offer an innovative solution for traders looking to improve their performance through well-defined rules and a solid framework.

Flexible Variable Moving Average (FVMA):

The FVMA adapts dynamically to market conditions, offering a more responsive trend line than traditional moving averages. This flexibility allows for quick identification of trends and reversals, crucial for fast-paced trading environments.

Exponential Moving Average (EMA):

By giving greater weight to recent price data, the EMA enhances sensitivity to price changes, allowing for more accurate entries and exits when used alongside the FVMA. This combination maximizes the effectiveness of the strategy in identifying optimal trading opportunities.

Relative Strength Index (RSI):

The RSI helps identify overbought or oversold conditions, integrating seamlessly with other indicators to enhance the strategy's ability to pinpoint potential reversal points. This aspect of the strategy ensures that traders can make informed decisions based on market momentum.

Moving Average Convergence Divergence (MACD):

The MACD serves as an essential confirmation tool, providing insights into trend strength and momentum. This enhances the accuracy of entry and exit signals, allowing traders to make more informed decisions based on robust technical analysis.

Multi-Take Profit (TP) and Stop Loss (SL) Levels:

The strategy supports multiple TPs, allowing traders to lock in profits at various levels while effectively managing risk through a robust SL system. This flexibility caters to diverse trading styles and risk profiles, ensuring that the strategy can adapt to individual trader needs.

Default Properties:

Take Profit Levels: TP1 is set to 2.0, and TP2 is set to 2.9, which is designed to enhance profit potential while maintaining a solid risk-reward ratio.

Stop Loss: A SL is set at 2% of the 5% account balance, which helps to preserve capital and manage risk effectively, adhering to the guideline of not risking more than 5-10% of the account balance per trade.

Labeling System for Exits: Automatic labeling of TP and SL exits on the chart provides clear visualization of trading outcomes. This feature supports informed decision-making and performance tracking, aligning with the guideline of providing transparent results.

Custom Alerts System:

The inclusion of customizable alerts for trade entries, exits, and SL/TP hits keeps traders informed in real-time, enabling prompt actions without constant market monitoring. This is crucial for effective trade management and helps traders respond quickly to market changes.

API Boxes for Automated Trading:

The strategy features API boxes, allowing traders to set up automated trading based on indicator signals. This functionality enables seamless integration with trading platforms, enhancing efficiency and streamlining the trading process, which is particularly valuable for traders looking to optimize their execution.

Data Tables for Enhanced Analysis:

The script includes data tables displaying critical insights across various timeframes: 2-hour, daily, weekly, and monthly. These tables provide a comprehensive overview of market conditions, allowing traders to analyze trends and make informed decisions based on a broad spectrum of data. By leveraging this information, traders can identify high-probability setups and align their strategies with prevailing market trends, significantly increasing their chances of success.

Default Properties:

Initial Capital: £1,000, ensuring a realistic starting point for traders.

Risk per Trade: 5% of the account balance, promoting sustainable trading practices.

Commission: 0.1%, reflecting realistic transaction costs that traders may encounter.

Slippage: 1%, accounting for potential market volatility during trade execution.

Take Profit Levels:

TP1: 2.0

TP2: 2.9

Stop Loss (SL): 2% of the 5% account balance, which is well within acceptable risk parameters.

Compliance with TradingView Guidelines:

This script fully complies with TradingView's guidelines, specifically:

Strategy Results:

The strategy is designed to publish backtesting results that do not mislead traders. The realistic parameters outlined in the default properties ensure that traders have a clear understanding of potential outcomes.

The dataset used for backtesting has sufficient trades to produce a reliable sample size, aligning with the guideline of ideally having more than 100 trades.

Any deviations from recommended practices are justified in the script description, ensuring transparency and adherence to best practices.

The script explains the default properties in detail, providing a thorough understanding of how these settings influence performance.

Why This Script is Worth Paying For:

This Pine Script offers an unparalleled trading experience through its unique combination of technical indicators, comprehensive trade management features, and detailed data tables for multiple timeframes. Here are compelling reasons to invest in this strategy:

Holistic Approach: The integration of multiple indicators ensures a well-rounded perspective on market conditions, increasing the likelihood of successful trades.

Advanced Risk Management: The flexibility of multiple TPs and SLs empowers traders to tailor their risk profiles according to individual strategies, enhancing overall profitability.

Automated Trading Capability: The inclusion of API boxes for automated trading streamlines execution, allowing traders to capitalize on opportunities without the need for manual intervention.

Comprehensive Data Analysis: The detailed data tables provide invaluable insights across different timeframes, enabling traders to make informed decisions based on robust market analysis.

In summary, this innovative Pine Script represents a powerful tool designed to empower traders at all levels. Its originality, synergistic functionality, and comprehensive features create a dynamic and effective trading environment, justifying its value and positioning it as a must-have for anyone serious about achieving consistent trading success.

Rsi Long-Term Strategy [15min]Hello, I would like to present to you The "RSI Long-Term Strategy" for 15min tf

The "RSI Long-Term Strategy " is designed for traders who prefer a combination of momentum and trend-following techniques. The strategy focuses on entering long positions during significant market corrections within an overall uptrend, confirmed by both RSI and volume. The use of long-term SMAs ensures that trades are made in line with the broader market trend. The stop-loss feature provides risk management by limiting losses on trades that do not perform as expected. This strategy is particularly well-suited for longer-term traders who monitor 15-minute charts but look for substantial trend reversals or continuations.

Indicators and Parameters:

Relative Strength Index (RSI):

- The RSI is calculated using a 10-period length. It measures the magnitude of recent price changes to evaluate overbought or oversold conditions. The script defines oversold conditions when the RSI is at or below 30 and overbought conditions when the RSI is at or above 70.

Volume Condition:

-The strategy incorporates a volume condition where the current volume must be greater than 2.5 times the 20-period moving average of volume. This is used to confirm the strength of the price movement.

Simple Moving Averages (SMA):

- The strategy uses two SMAs: SMA1 with a length of 250 periods and SMA2 with a length of 500 periods. These SMAs help identify long-term trends and generate signals based on their crossover.

Strategy Logic:

Entry Logic:

A long position is initiated when all the following conditions are met:

The RSI indicates an oversold condition (RSI ≤ 30).

SMA1 is above SMA2, indicating an uptrend.

The volume condition is satisfied, confirming the strength of the signal.

Exit Logic:

The strategy closes the long position when SMA1 crosses under SMA2, signaling a potential end of the uptrend (a "Death Cross").

Stop-Loss:

A stop-loss is set at 5% below the entry price to manage risk and limit potential losses.

Buy and sell signals are highlighted with circles below or above bars:

Green Circle : Buy signal when RSI is oversold, SMA1 > SMA2, and the volume condition is met.

Red Circle : Sell signal when RSI is overbought, SMA1 < SMA2, and the volume condition is met.

Black Cross: "Death Cross" when SMA1 crosses under SMA2, indicating a potential bearish signal.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

I hope the strategy will be helpful, as always, best regards and safe trades

;)

Quatro SMA Strategy [4h]Hello, I would like to present to you The "Quatro SMA" strategy

Strategy is based on four simple moving averages of different lengths and monitoring trading volume. The key idea is to identify strong market trends by comparing short-term moving averages with the long-term SMA. The strategy generates buy signals when all short-term SMAs are above the SMA(200) and the volume confirms the strength of the move. Similarly, sell signals are generated when all short-term SMAs are below the SMA(200), and the volume is sufficiently high.

The strategy manages risk by applying a stop loss and three different Take Profit levels (TP1, TP2, TP3), with varying percentages of the position closed at each level.

Each Take Profit level is triggered at a specific percentage gain, with the position being closed gradually depending on the achieved targets. The percentage of the position closed at each TP level is also defined by the user.

Indicators and Parameters:

Simple Moving Averages (SMA):

The script utilizes four simple moving averages with different lengths (4, 16, 32, 200). The first three SMAs (SMA1, SMA2, SMA3) are used to determine the trend direction, while the fourth SMA (with a length of 200) serves as a support/resistance line.

Volume:

The script monitors trading volume and checks if the current volume exceeds 2.5 times the average volume of the last 40 candles. High volume is considered as confirmation of trend strength.

Entry Conditions:

- Long Position: Triggered when SMA1 > SMA2 > SMA3, the closing price is above SMA(200), and the volume condition is met.

- Short Position: Triggered when SMA1 < SMA2 < SMA3, the closing price is below SMA(200), and the volume condition is met.

Exit Conditions:

- Long Position: Closed when SMA1 < SMA2 < SMA3 and the closing price is above SMA(200).

- Short Position: Closed when SMA1 > SMA2 > SMA3 and the closing price is below SMA(200).

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

I hope the strategy will be helpful, as always, best regards and safe trades

;)

HilalimSB Strategy HilalimSB A Wedding Gift 🌙

What is HilalimSB🌙?

First of all, as mentioned in the title, HilalimSB is a wedding gift.

HilalimSB - Revealing the Secrets of the Trend

HilalimSB is a powerful indicator designed to help investors analyze market trends and optimize trading strategies. Designed to uncover the secrets at the heart of the trend, HilalimSB stands out with its unique features and impressive algorithm.

Hilalim Algorithm and Fixed ATR Value:

HilalimSB is equipped with a special algorithm called "Hilalim" to detect market trends. This algorithm can delve into the depths of price movements to determine the direction of the trend and provide users with the ability to predict future price movements. Additionally, HilalimSB uses its own fixed Average True Range (ATR) value. ATR is an indicator that measures price movement volatility and is often used to determine the strength of a trend. The fixed ATR value of HilalimSB has been tested over long periods and its reliability has been proven. This allows users to interpret the signals provided by the indicator more reliably.

ATR Calculation Steps

1.True Range Calculation:

+ The True Range (TR) is the greatest of the following three values:

1. Current high minus current low

2. Current high minus previous close (absolute value)

3. Current low minus previous close (absolute value)

2.Average True Range (ATR) Calculation:

-The initial ATR value is calculated as the average of the TR values over a specified period

(typically 14 periods).

-For subsequent periods, the ATR is calculated using the following formula:

ATRt=(ATRt−1×(n−1)+TRt)/n

Where:

+ ATRt is the ATR for the current period,

+ ATRt−1 is the ATR for the previous period,

+ TRt is the True Range for the current period,

+ n is the number of periods.

Pine Script to Calculate ATR with User-Defined Length and Multiplier

Here is the Pine Script code for calculating the ATR with user-defined X length and Y multiplier:

//@version=5

indicator("Custom ATR", overlay=false)

// User-defined inputs

X = input.int(14, minval=1, title="ATR Period (X)")

Y = input.float(1.0, title="ATR Multiplier (Y)")

// True Range calculation

TR1 = high - low

TR2 = math.abs(high - close )

TR3 = math.abs(low - close )

TR = math.max(TR1, math.max(TR2, TR3))

// ATR calculation

ATR = ta.rma(TR, X)

// Apply multiplier

customATR = ATR * Y

// Plot the ATR value

plot(customATR, title="Custom ATR", color=color.blue, linewidth=2)

This code can be added as a new Pine Script indicator in TradingView, allowing users to calculate and display the ATR on the chart according to their specified parameters.

HilalimSB's Distinction from Other ATR Indicators

HilalimSB emerges with its unique Average True Range (ATR) value, presenting itself to users. Equipped with a proprietary ATR algorithm, this indicator is released in a non-editable form for users. After meticulous testing across various instruments with predetermined period and multiplier values, it is made available for use.

ATR is acknowledged as a critical calculation tool in the financial sector. The ATR calculation process of HilalimSB is conducted as a result of various research efforts and concrete data-based computations. Therefore, the HilalimSB indicator is published with its proprietary ATR values, unavailable for modification.

The ATR period and multiplier values provided by HilalimSB constitute the fundamental logic of a trading strategy. This unique feature aids investors in making informed decisions.

Visual Aesthetics and Clear Charts:

HilalimSB provides a user-friendly interface with clear and impressive graphics. Trend changes are highlighted with vibrant colors and are visually easy to understand. You can choose colors based on eye comfort, allowing you to personalize your trading screen for a more enjoyable experience. While offering a flexible approach tailored to users' needs, HilalimSB also promises an aesthetic and professional experience.

Strong Signals and Buy/Sell Indicators:

After completing test operations, HilalimSB produces data at various time intervals. However, we would like to emphasize to users that based on our studies, it provides the best signals in 1-hour chart data. HilalimSB produces strong signals to identify trend reversals. Buy or sell points are clearly indicated, allowing users to develop and implement trading strategies based on these signals.

For example, let's imagine you wanted to open a position on BTC on 2023.11.02. You are aware that you need to calculate which of the buying or selling transactions would be more profitable. You need support from various indicators to open a position. Based on the analysis and calculations it has made from the data it contains, HilalimSB would have detected that the graph is more suitable for a selling position, and by producing a sell signal at the most ideal selling point at 08:00 on 2023.11.02 (UTC+3 Istanbul), it would have informed you of the direction the graph would follow, allowing you to benefit positively from a 2.56% decline.

Technology and Innovation:

HilalimSB aims to enhance the trading experience using the latest technology. With its innovative approach, it enables users to discover market opportunities and support their decisions. Thus, investors can make more informed and successful trades. Real-Time Data Analysis: HilalimSB analyzes market data in real-time and identifies updated trends instantly. This allows users to make more informed trading decisions by staying informed of the latest market developments. Continuous Update and Improvement: HilalimSB is constantly updated and improved. New features are added and existing ones are enhanced based on user feedback and market changes. Thus, HilalimSB always aims to provide the latest technology and the best user experience.

Social Order and Intrinsic Motivation:

Negative trends such as widespread illegal gambling and uncontrolled risk-taking can have adverse financial effects on society. The primary goal of HilalimSB is to counteract these negative trends by guiding and encouraging users with data-driven analysis and calculable investment systems. This allows investors to trade more consciously and safely.

What is HilalimSB Strategy🌙?

HilalimSB Strategy is a strategy that is supported by the HilalimSB algorithm created by the creator of HilalimSB and continues transactions with take profit and stop loss levels determined by users who strategically and automatically open transactions as a result of the data it receives and automatically closes transactions under necessary conditions. It is a first in the tradingview world with its unique take profit and stop loss markings. HilalimSB Strategy is open to users' initiatives and is a trading strategy developed on BTC.

What does the HilalimSB Strategy target?

The main purpose of HilalimSB Strategy is to reduce the transaction load of traders and to be integrated into various brokerage firms and operated by automatic trading bots, and it is aimed to serve this purpose. In addition to the strategies currently available in the markets, HilalimSB Strategy offers a useful infrastructure to traders with its useful interface. HilalimSB Strategy, which was decided to be published as a result of various calculations, was offered to the users with its unique visual effects after the completion of the testing procedures under market conditions.

HilalimSB Strategy and Heikin Ashi

HilalimSB Strategy produces data in Heikin Ashi chart types, but since Heikin Ashi chart types have their own calculation method, HilalimSB Strategy has been published in a way that cannot produce data in this chart type due to HilalimSB Strategy's ideology of appealing to all types of users, and any confusion that may arise is prevented in this way.

After the necessary conditions determined by the creator of HilalimSB are met, HilalimSB Heikin Ashi will be shared exclusively with invited users only, upon request, to users who request an invitation.

Differences between HilalimSB Strategy and HilalimSB

HilalimSB Strategy has been shared as a strategy and its features have been explained above. HilalimSB is a trading indicator and this is the main difference between them.We can explain it briefly this way.

Here are the differences between indicators and strategies:

1.Purpose and Use:

Indicators: Analyze market data to provide information about price movements and trends. They typically generate buy and sell signals and give traders clues about when to make trades in the market.

Strategies: These are plans for trading based on specific rules. They use signals from indicators and other market data to execute buy and sell transactions.

2.Features:

Indicators: Operate independently and are based on specific mathematical formulas. Examples include moving averages, RSI, and MACD.

Strategies: Combine one or more indicators and other market analysis tools to create a comprehensive trading plan. This plan determines entry and exit points, risk management, and trade size.

3.Scope:

Indicators: Are single analysis tools focusing on specific time frames or price movements.

Strategies: Are comprehensive trading plans that typically involve multiple trades over a certain period.

4.Decision Making:

Indicators: Provide information to traders and help in the decision-making process.

Strategies: Are direct decision-making mechanisms that execute trades automatically according to predetermined rules.

5.Automation:

Indicators: Are mostly interpreted manually and used based on the trader’s discretion.

Strategies: Can be used in automated trading systems and execute trades automatically according to the set rules.

The shared image is a 1-hour chart of BTCUSDC.P determined by the user as 1 percent take profit and 1 percent stop loss. And transactions were opened on Binance with the commission rate determined as 0.017 for the USDC trading pair.

HilalimSB Strategy, which presents users with completely concrete data, has proven itself in testing processes and is a project of SB that aims to reach all user profiles.🌙

[Support and Resistance with Trend Lines] with Backtest (TSO) with Backtest (TSO)

===========================================================================

===========================================================================

This indicator serves as a comprehensive full-cycle trading system, providing alerts at each stage of the trade, from opening to closure. The algorithm uses most recent and historical S&R (Support and Resistance) levels with most recent and historical Trend Lines, generating signals for trades when Breaks/Bounces occur (Trade Open Signal triggers can be configured via very customizable indicator Input "Signal Trigger Matrix" settings). With signal for trade open, TP (Take Profit and SL (Stop Loss) levels are calculated as well and marked on the chart including alerts for each action of the trade. The indicator offers a variety of automated approaches for TP (Take-Profit) and SL (Stop-Loss) settings. These include static current/historical S&R (Support and Resistance) levels or S&R/Trend Lines dynamic breaks for TP (Take-Profit) and various SL (Stop-Loss) approaches, including ATR Trailing SL, opposite S&R (Support and Resistance) levels SL, opposite Trend Lines SL and more. This diverse set of tools ensure flexibility in tailoring TP (Take-Profit) and SL (Stop-Loss) parameters to different market conditions, contributing to a more adaptive and robust trading system. Additionally, a series of signal analysis tools, including market sentiment, candle bar analysis, divergence, and volume, enhance the precision of trading signals.

* Works with popular timeframes: 1M, 3M, 5M, 15M, 30M, 45M, 1H.

* Works well with Futures and Indices, can be used to trade Stocks, Crypto and FOREX.

* Includes LIVE alert/labels Breakouts and Bounces signal trigger feature, which can be used for scalping (NOTE: This approach cannot be backtested).

* Every action of the trade is calculated on a confirmed closed candle bar state (barstate.isconfirmed), so the indicator will never repaint.

==============================================================

Indicator examples:

---------------------------------------------------------------------------

Strategy Config: SRTL_MES_15M3Y_EODoff_ALL

Here is a nice example of MES (Micro E-Mini S&P 500 Index Futures) configuration, which uses S&R (Support and Resistance) breakouts as signal trigger with Elliot Wave confirmation and previous S&R historical levels for TP (Take-Profit).

---------------------------------------------------------------------------

An example of an intraday Tesla trade. Also the green arrows will be displayed IMMEDIATELY when Breakout/Reverse Bounce occurs (same an Alert will be triggered immediately).

===========================================================================

Trading open/close/TP/SL labels, plots and colors explanations:

---------------------------------------------------------------------------

>>> S&R (Support and Resistance) levels/lines: orange - support, blue - resistance (can be hidden).

>>> Trend Lines: yellow - support, green - resistance (can be hidden).

>>> Blue labels show resistance breakouts and bounces, light-blue - bullish, dark-blue - bearish

>>> Yellow labels show resistance breakouts and bounces, light-yellow - bullish, dark-yellow - bearish

>>> Green/Red arrows on top/bottom of candle bar will show LIVE breakouts (if turned on)

>>>>> LONG open: green "house" looking arrow below candle bar.

>>>>> SHORT open: red "house" looking arrow above candle bar.

>>>>> LONG/SHORT take-profit target: green/red circles (multi-profit > TP2/3/4/5 smaller circles).

>>>>> LONG/SHORT stop-loss target: green/red + crosses.

>>>>> LONG/SHORT take-profit hits: green/red diamonds.

>>>>> LONG/SHORT stop-loss hits: green/red X-crosses.

>>>>> LONG/SHORT EOD (End of Day | Intraday style) close (profitable trade): green/red squares.

>>>>> LONG/SHORT EOD (End of Day | Intraday style) close (loss trade): green/red PLUS(+)-crosses.

===========================================================================

STATS TABLE ///////////////////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Trading STATS table on the chart showing current trade direction, Last TP (Take-Profit) Taken, Current Trade PL (profit/loss in price difference from trade open to the very current state).

---------------------------------------------------------------------------

CUSTOM TRADING DATE RANGE /////////////////////////////////////////////////

---------------------------------------------------------------------------

>>>>> This feature can be used to manually set indicator trading range from and to a specific date and time. NOTE: This is not intended for a very long date range backtesting, utilize TradingView Strategy Tester for that.

* Use TradingView “Strategy Tester” to see Backtesting results

NOTE: If Strategy Tester does not show any results with Date Ranged fully unchecked, there may be an issue where a script opens a trade, but there is not enough TradingView power to set the Take-Profit and Stop-Loss and somehow an open trade gets stuck and never closes, so there are “no trades present”. In such case - manually check “Start”/“End” dates or use “Deep Backtesting” feature!

---------------------------------------------------------------------------

INTRADAY ACTIVE TRADING SESSION CONFIGURATION /////////////////////////////

---------------------------------------------------------------------------

>>> Regional Active Trading Session Hours Schedule: If selected - trades will only open during regional active trading session, if 'OFF', there will be no trading schedule and trades will open 24/7.

>>> EOD(End of Day) Close - On/Off: Close the trade if it's still open at the end of active trading session (on the very last candle bar). NOTE: If no region is selected at 'Regional Active Trading Session Schedule' - there will be no EOD(End of Day) Close and trades will run overnight until either SL(Stop-Loss) or TP(Take-Profit) is hit!

>>>>> EOD(End of Day) Close - 1 candle bar before last: This is specifically for stocks as while usually indices can be closed 15minutes after the market closes, for stocks - the last candle bar closes at the same time with the market active trading session, which if closed - trades can't be closed until next day/session! Enable this setting for the trade to close/alert 1 candle bar before the last one, so there is still time to close the trade at the Broker (NOTE: depending on the timeframe, 1 candle bar can be: 15sec, 30sec, 1min, 3min, 5min, 15min, 30min, 45min, 1h).

---------------------------------------------------------------------------

SIGNAL TRIGGER MATRIX ////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Trading Engine: This setting turns on TradingView Strategy trading engine for backtesting.

>>> Market Session Only: With this setting turned on, all signal trigger Breaks/Bounces will be hidden during Pre/Post market time.

>>> Plot S&R Levels/Lines: Plot S&R (Support and Resistance) on chart. Note: historical levels/lines will only be plotted if hit (Break/Bounce).

>>> Plot Trend Lines Levels/Lines: Plot Trend Lines levels/lines on chart. Note: historical levels/lines will only be plotted if hit (Break/Bounce).

>>> Use S&R Current Levels | Use S&R Historical Levels | Use Trend Lines Current Levels | Use Trend Lines Historical Levels |: Choose which levels should be used for Breaks/Bounces to be captured on. If all triggers are turned on/checked - whatever happens 1st wins the trigger.

>>> Breaks | Bounces: 'Breaks': Turn on Breaks through levels/lines signal trigger. | 'Bounces': Turn on Bounces off levels/lines signal trigger.

>>> Signal: Regular | Signal: S&R Combo | Signal: TL Combo | Signal: S&R + TL Combo | Signal: Repeat Action |: Trade open signal trigger execution approach MATRIX (If 1 or more turned on at the same time - whatever comes first will be the trade signal trigger). 'Regular': A single Break/Bounce must occur on a closed bar for signal trigger. 'S&R Combo': A combination of 2 Current + Historical S&R (Support and Resistance) Break/Bounce must happen in the same direction on same bar for signal trigger. 'TL Combo': A combination of 2 Current + Historical Trend Lines Break/Bounce must happen in the same direction on same bar for signal trigger. 'S&R + TL Combo': a combination of ANY S&R and Trend Line Break/Bounce must happen in the same direction on same bar for signal trigger. 'Repeat Action': Initial and then confirmation (2nd/3rd/etc. consecutive occurence) Break/Bounce must occur on same level/line for signal trigger.

>>> Historical - Look Back (# of days): How far back (in # of days) will historical S&R/Trend Lines will be used for Trade Open signals/TP/SL/etc.

>>> Historical - Look Back Invalidation (# of days): IF THERE IS TOO MUCH HISTORICAL LEVELS/LINES ON CHART - LOWER THIS SETTING + MAKE SURE IT'S SMALLER THAN 'Historical - Look Back (# of days)'. With big Look back period (5+ days) - it can become very messy with too many historical levels/lines. To clear oldest historical levels/lines - set Look Back Invalidation # of days to less than Historical Look Back # of days. (After X # of Look Back Invalidation days - older levels/lines will become invalidated and no longer used for opening trades/TP (Take-Profit)/SL (Stop-Loss), while newer levels/lines will still be discovered.

>>> S&R/Trend Lines - Support/Resistance combined into 1 entity: Every level or a line becomes simply a level or a line, regardless if it originally was a support or resistance. By default, depending on the level/line originally being support or resistance - the signal direction will be such as: Resistance is broken > LONG / bounced > SHORT; Support is broken > SHORT / bounced > LONG; with this setting on, either level or line can be both broken or bounced off in ANY direction, trade open direction will depend on current market sentiment only.

---------------------------------------------------------------------------

S&R CONFIGURATION ////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> S&R Search - Left Bars (current): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with below - Right Bars).

>>> S&R Search - Right Bars (current): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with above - Left Bars).

>>> S&R Search - Custom Resolution (current): This is a custom timeframe setting specifically for S&R Search, it disregards current chart timeframe. This is great to use for scalping, for example: with main chart set to 1min and the custom timeframe set to 3min or 5min - there will be stronger support/resistance levels with more detailed price action.

>>> S&R Search - Left Bars (historical): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with below - Right Bars).

>>> S&R Search - Right Bars (historical): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with above - Left Bars).