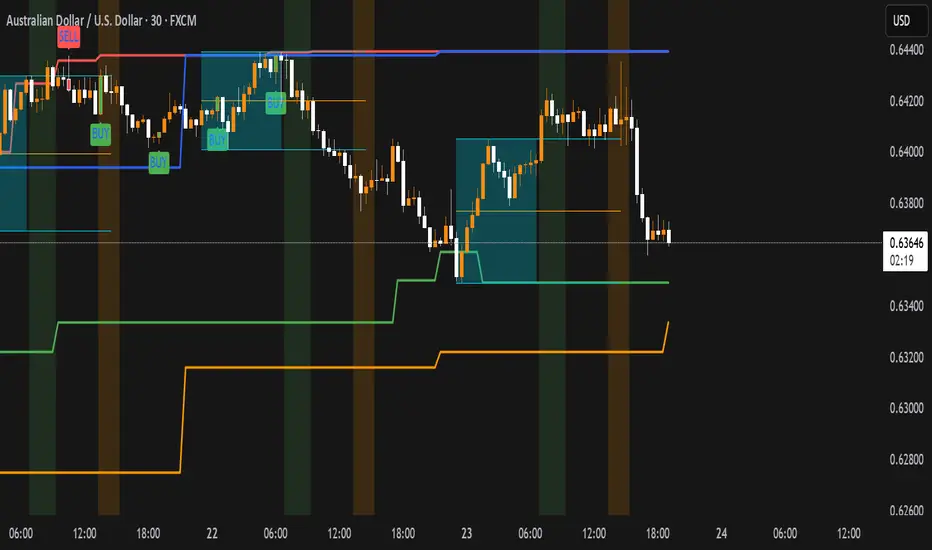

ORB With Buffer, Target & Stop LossThe "ORB With Buffer" is a comprehensive technical analysis tool designed to identify, plot, and visualize key levels associated with price breakouts. It offers a dynamic representation of breakout zones, buffer areas, target levels, and stop-loss levels on both sides of the market.

Key Features:

ORB Levels (Opening Range Breakout):

The indicator identifies and plots the Opening Range Breakout levels, marking the high and low points of the initial trading period. In our case the ORB range is locked to 15 Minutes irrespective of the chart's timeframe.

Buffer Areas for Breakout:

Buffer zones are displayed around the ORB levels, representing a range where traders cant wait to join the direction to counter fake ORB breakouts

Targets:

The indicator calculates and visualizes target levels. Approximately 1% of instrument's price from entry point

Stop Loss Levels:

Stop-loss levels are indicated on both sides of the market, offering traders a clear reference point to manage risk.

Pine Script®指標