BTC Seasonality Strategy (Weekly)This strategy identifies potential weekend opportunities in Bitcoin (BTC) markets by leveraging the concept of seasonality, entering a position at a predefined time and day, and exiting at a specified time and day.

Key Features

Customizable Time and Day Selection:

Users can select the entry and exit days and corresponding times (in EST).

Directional Flexibility:

The strategy allows traders to choose between long or short positions.

TradingView Compliance:

The script adheres to TradingView's house rules, avoids overly complex conditions, and provides clear user-configurable inputs.

How It Works

The script determines the current weekday and hour in EST, converting TradingView's UTC time for accurate comparisons.

If the current day and hour match the selected entry conditions, a trade (long or short) is opened.

The position is closed when the current day and hour match the specified exit conditions.

Theoretical Basis

Market Seasonality:

The concept of seasonality in financial markets refers to predictable patterns based on time, such as weekends or specific days of the week. Studies have shown that cryptocurrency markets exhibit unique trading behaviors during weekends due to reduced institutional activity and higher retail participation behavioral Biases**:

Retail traders often dominate weekend markets, potentially causing predictable inefficiencies .

Reverences**

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177–189.

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82.

在腳本中搜尋"the script"

SMC StrategyThis Pine Script strategy is based on Smart Money Concepts (SMC), designed for TradingView. Here's a brief summary of what the script does:

1. Swing High and Low Calculation: It identifies recent swing highs and lows, which are used to define key zones.

2. Equilibrium, Premium, and Discount Zones:

- Equilibrium is the midpoint between the swing high and low.

- Premium Zone is above the equilibrium, indicating a potential resistance area (sell zone).

- Discount Zone is below the equilibrium, indicating a potential support area (buy zone).

3. Simple Moving Average (SMA): It uses a 50-period SMA to determine the trend direction. If the price is above the SMA, the trend is bullish; if it's below, the trend is bearish.

4. Buy and Sell Signals:

- Buy Signal: Generated when the price is in the discount zone and above the equilibrium, with the price also above the SMA.

- Sell Signal: Triggered when the price is in the premium zone and below the equilibrium, with the price also below the SMA.

5. Order Blocks: It detects basic order blocks by identifying the highest high and lowest low within the last 20 bars. These levels help confirm the buy and sell signals.

6. Liquidity Zones: It marks the swing high and low as potential liquidity zones, indicating where price may reverse due to institutional players' activity.

The strategy then executes trades based on these signals, plotting buy and sell markers on the chart and showing the key levels (zones) and trend direction.

Demo GPT - Day Trading Scalping StrategyOverview:

This strategy is designed for day trading and scalping, utilizing a combination of technical indicators, candlestick patterns, and volume analysis to determine entry and exit points. It focuses on capturing short-term price movements while ensuring that trades are executed under specific market conditions.

Key Components:

Technical Indicators Used:

Exponential Moving Average (EMA): The strategy uses the 20-period EMA to identify the trend direction. The EMA smooths out price data, helping traders make more informed decisions about potential buy or sell signals.

Volume Weighted Average Price (VWAP): VWAP is used to measure the average price a security has traded at throughout the day, based on both volume and price. This indicator helps assess whether the current price is above or below the average trading price.

Camarilla Pivot Points: The strategy calculates four levels of Camarilla pivots (S2, S3, R2, R3) based on the highest and lowest prices over the last 14 daily candles. These levels act as potential support and resistance zones, guiding entry and exit decisions.

Candlestick Analysis:

Buy Condition: A buy signal is triggered when:

The first candle (previous candle) is green (close > open).

The second candle (current candle) is also green and opens above the first candle.

The volume of the current candle exceeds the 20-period moving average of volume, indicating strong buying interest.

Sell Condition: A sell signal is triggered when:

The first candle is red (close < open).

The second candle opens below the first red candle.

The volume of the current candle also exceeds the 20-period moving average of volume, indicating strong selling pressure.

Position Management:

The strategy enters a long position (buy) when the buy condition is met and closes the long position when the sell condition is met. This approach aims to capture upward momentum while avoiding extended exposure to downside risks.

Trading Settings:

Capital Management: The strategy uses 100% of available capital for each trade, allowing for maximum exposure to potential gains.

Commission and Slippage: The script includes settings for a commission rate of 0.1% and slippage of 3, accounting for trading costs and potential price changes during order execution.

Date Filtering: The strategy allows users to set a start date (January 1, 2018) and an end date (December 31, 2069) for trade execution, providing flexibility in backtesting and live trading.

Visualization:

The script plots the 20 EMA, VWAP, and the Camarilla pivot levels on the chart for visual reference.

Buy and sell signals are visually represented with shapes on the chart, making it easy to identify potential trade opportunities at a glance.

Volume is plotted in a separate pane to assess trading activity, and a horizontal line at zero provides a reference point.

Summary:

This Day Trading Scalping Strategy is designed to exploit short-term price movements by using a combination of EMAs, VWAP, and Camarilla pivot levels, alongside candlestick patterns and volume analysis. It is well-suited for traders looking to make quick trades based on real-time market conditions while maintaining a disciplined approach to entry and exit points. The strategy is highly visual, allowing traders to quickly assess market conditions and make informed trading decisions.

Feel free to modify or adjust any aspects of the strategy according to your specific trading goals or preferences!

Gabriel's Witcher Strategy [65 Minute Trading Bot]Strategy Description: Gabriel's Witcher Strategy

Author: Gabriel

Platform: TradingView Pine Script (Version 5)

Backtested Asset: Avalanche (Coinbase Brokage for Volume adjustment)

Timeframe: 65 Minutes

Strategy Type: Comprehensive Trend-Following and Momentum Strategy with Scalping and Risk Management Features

Overview

Gabriel's Witcher Strategy is an advanced trading bot designed for the Avalanche pair on a 65-minute timeframe. This strategy integrates a multitude of technical indicators to identify and execute high-probability trading opportunities. By combining trend-following, momentum, volume analysis, and range filtering, the strategy aims to capitalize on both long and short market movements. Additionally, it incorporates scalping mechanisms and robust risk management features, including take-profit (TP) levels and commission considerations, to optimize trade performance and profitability.

====Key Components====

Source Selection:

Custom Source Flexibility: Allows traders to select from a wide range of price and volume sources (e.g., Close, Open, High, Low, HL2, HLC3, OHLC4, VWAP, On-Balance Volume, etc.) for indicator calculations, enhancing adaptability to various trading styles.

Various curves of Volume Analysis are employed:

Tick Volume Calculation: Utilizes tick volume as a fallback when actual volume data is unavailable, ensuring consistency across different data feeds.

Volume Indicators: Incorporates multiple volume-based indicators such as On-Balance Volume (OBV), Accumulation/Distribution (AccDist), Negative Volume Index (NVI), Positive Volume Index (PVI), and Price Volume Trend (PVT) for comprehensive market analysis.

Trend Indicators:

ADX (Average Directional Index): Measures trend strength using either the Classic or Masanakamura method, with customizable length and threshold settings. It's used to open positions when the mesured trend is strong, or exit when its weak.

Jurik Moving Average (JMA): A smooth moving average that reduces lag, configurable with various parameters including source, resolution, and repainting options.

Parabolic SAR: Identifies potential reversals in market trends with adjustable start, increment, and maximum settings.

Custom Trend Indicator: Utilizes highest and lowest price points over a specified timeframe to determine current and previous trend bases, visually represented with color-filled areas.

Momentum Indicators:

Relative Strength Index (RSI): Evaluates the speed and change of price movements, smoothed with a custom length and source. It's used to not enter the market for shorts in oversold or longs for overbought conditions, and to enter for long in oversold or shorts for overboughts.

Momentum-Based Calculations: Employs both Double Exponential Moving Averages (DEMA) on a MACD-based RSI to enhance momentum signal accuracy which is then further accelerated by a Hull MA. This is the technical analysis tool that determines bearish or bullish momentum.

OBV-Based Momentum Conditions: Uses two exponential moving averages of OBV to determine bullish or bearish momentum shifts, anomalities, breakouts where banks flow their funds in or Smart Money Concepts trade.

Moving Averages (MA):

Multiple MA Types: Includes Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Hull Moving Average (HMA), and Volume-Weighted Moving Average (VWMA), selectable via input parameters.

MA Speed Calculation: Measures the percentage change in MA values to determine the direction and speed of the trend.

Range Filtering:

Variance-Based Filter: Utilizes variance and moving averages to filter out trades during low-volatility periods, enhancing trade quality.

Color-Coded Range Indicators: Visualizes range filtering with color changes on the chart for quick assessment.

Scalping Mechanism:

Heikin-Ashi Candles: Optionally uses Heikin-Ashi candles for smoother price action analysis.

EMA-Based Trend Detection: Employs fast, medium, and slow EMAs to determine trend direction and potential entry points.

Fractal-Based Filtering: Detects regular or BW (Black & White) fractals to confirm trade signals.

Take Profit (TP) Management:

Dynamic TP Levels: Calculates TP levels based on the number of consecutive long or short entries, adjusting targets to maximize profits.

TP Signals and Re-Entry: Plots TP signals on the chart and allows for automatic re-entry upon TP hit, maintaining continuous trade flow.

Risk Management:

Commission Integration: Accounts for trading commissions to ensure net profitability.

Position Sizing: Configured to use a percentage of equity for each trade, adjustable via input parameters.

Pyramiding: Allows up to one additional position per direction to enhance gains during strong trends.

Alerts and Visual Indicators:

Buy/Sell Signals: Plots visual indicators (triangles and flags) on the chart to signify entry and TP points.

Bar Coloring: Changes bar colors based on ADX and trend conditions for immediate visual cues.

Price Levels: Marks significant price levels related to TP and position entries with cross styles.

Input Parameters

Source Settings:

Custom Sources (srcinput): Choose from various price and volume sources to tailor indicator calculations.

ADX Settings:

ADX Type (ADX_options): Select between 'CLASSIC' and 'MASANAKAMURA' methods.

ADX Length (ADX_len): Defines the period for ADX calculation.

ADX Threshold (th): Sets the minimum ADX value to consider a strong trend.

RSI Settings:

RSI Length (len_3): Period for RSI calculation.

RSI Source (src_3): Source data for RSI.

Trend Strength Settings:

Channel Length (n1): Period for trend channel calculation.

Average Length (n2): Period for smoothing trend strength.

Jurik Moving Average (JMA) Settings:

JMA Source (inp): Source data for JMA.

JMA Resolution (reso): Timeframe for JMA calculation.

JMA Repainting (rep): Option to allow JMA to repaint.

JMA Length (lengths): Period for JMA.

Parabolic SAR Settings:

SAR Start (start): Initial acceleration factor.

SAR Increment (increment): Acceleration factor increment.

SAR Maximum (maximum): Maximum acceleration factor.

SAR Point Width (width): Visual width of SAR points.

Trend Indicator Settings:

Trend Timeframe (timeframe): Period for trend indicator calculations.

Momentum Settings:

Source Type (srcType): Select between 'Price' and 'VWAP'.

Momentum Source (srcPrice): Source data for momentum calculations.

RSI Length (rsiLen): Period for momentum RSI.

Smooth Length (sLen): Smoothing period for momentum RSI.

OBV Settings:

OBV Line 1 (e1): EMA period for OBV line 1.

OBV Line 2 (e2): EMA period for OBV line 2.

Moving Average (MA) Settings:

MA Length (length): Period for MA calculations.

MA Type (matype): Select MA type (1: SMA, 2: EMA, 3: HMA, 4: WMA, 5: VWMA).

Range Filter Settings:

Range Filter Length (length0): Period for range filtering.

Range Filter Multiplier (mult): Multiplier for range variance.

Take Profit (TP) Settings:

TP Long (tp_long0): Percentage for long TP.

TP Short (tp_short0): Percentage for short TP.

Scalping Settings:

Scalping Activation (ACT_SCLP): Enable or disable scalping.

Scalping Length (HiLoLen): Period for scalping indicators.

Fast EMA Length (fastEMAlength): Period for fast EMA in scalping.

Medium EMA Length (mediumEMAlength): Period for medium EMA in scalping.

Slow EMA Length (slowEMAlength): Period for slow EMA in scalping.

Filter (filterBW): Enable or disable additional fractal filtering.

Pullback Lookback (Lookback): Number of bars for pullback consideration.

Use Heikin-Ashi Candles (UseHAcandles): Option to use Heikin-Ashi candles for smoother trend analysis.

Strategy Logic

Indicator Calculations:

Volume and Source Selection: Determines the primary data source based on user input, ensuring flexibility and adaptability.

ADX Calculation: Computes ADX using either the Classic or Masanakamura method to assess trend strength.

RSI Calculation: Evaluates market momentum using RSI, further smoothed with custom periods.

Trend Strength Assessment: Utilizes trend channel and average lengths to gauge the robustness of current trends.

Jurik Moving Average (JMA): Smooths price data to reduce lag and enhance trend detection.

Parabolic SAR: Identifies potential trend reversals with adjustable parameters for sensitivity.

Momentum Analysis: Combines RSI with DEMA and OBV-based conditions to confirm bullish or bearish momentum.

Moving Averages: Employs multiple MA types to determine trend direction and speed.

Range Filtering: Filters out low-volatility periods to focus on high-probability trades.

Trade Conditions:

Long Entry Conditions:

ADX Confirmation: ADX must be above the threshold, indicating a strong uptrend.

RSI and Momentum: RSI below 70 and positive momentum signals.

JMA and SAR: JMA indicates an uptrend, and Parabolic SAR is below the price.

Trend Indicator: Confirms the current trend direction.

Range Filter: Ensures market is in an upward range.

Scalping Option: If enabled, additional scalping conditions must be met.

Short Entry Conditions:

ADX Confirmation: ADX must be above the threshold, indicating a strong downtrend.

RSI and Momentum: RSI above 30 and negative momentum signals.

JMA and SAR: JMA indicates a downtrend, and Parabolic SAR is above the price.

Trend Indicator: Confirms the current trend direction.

Range Filter: Ensures market is in a downward range.

Scalping Option: If enabled, additional scalping conditions must be met.

Position Management:

Entry Execution: Places long or short orders based on the identified conditions and user-selected position types (Longs, Shorts, or Both).

Take Profit (TP): Automatically sets TP levels based on predefined percentages, adjusting dynamically with consecutive trades.

Re-Entry Mechanism: Allows for automatic re-entry upon TP hit, maintaining active trading positions.

Exit Conditions: Closes positions when TP levels are reached or when opposing trend signals are detected.

Visual Indicators:

Bar Coloring: Highlights bars in green for bullish conditions, red for bearish, and orange for neutral.

Plotting Price Levels: Marks significant price levels related to TP and trade entries with cross symbols.

Signal Shapes: Displays triangle and flag shapes on the chart to indicate trade entries and TP hits.

Alerts:

Custom Alerts: Configured to notify traders of long entries, short entries, and TP hits, enabling timely trade management and execution.

Usage Instructions

Setup:

Apply the Strategy: Add the script to your TradingView chart set to BTCUSDT with a 65-minute timeframe.

Configure Inputs: Adjust the input parameters under their respective groups (e.g., Source Settings, ADX, RSI, Trend Strength, etc.) to match your trading preferences and risk tolerance.

Position Selection:

Choose Position Type: Use the Position input to select Longs, Shorts, or Both based on your market outlook.

Execution: The strategy will automatically execute and manage positions according to the selected type, ensuring targeted trading actions.

Signal Interpretation:

Buy Signals: Blue triangles below the bars indicate potential long entry points.

Sell Signals: Red triangles above the bars indicate potential short entry points.

Take Profit Signals: Flags above or below the bars signify TP hits for long and short positions, respectively.

Bar Colors: Green bars suggest bullish conditions, red bars indicate bearish conditions, and orange bars represent neutral or consolidating markets.

Risk Management:

Default Position Size: Set to 100% of equity. Adjust the default_qty_value as needed for your risk management strategy.

Commission: Accounts for a 0.1% commission per trade. Adjust the commission_value to match your broker's fees.

Pyramiding: Allows up to one additional position per direction to enhance gains during strong trends.

Backtesting and Optimization:

Historical Testing: Utilize TradingView's backtesting features to evaluate the strategy's performance over historical data.

Parameter Tuning: Optimize input parameters to align the strategy with current market dynamics and personal trading objectives.

Alerts Configuration:

Set Up Alerts: Enable and configure alerts based on the predefined alertcondition statements to receive real-time notifications of trade signals and TP hits.

Additional Features

Comprehensive Indicator Integration: Combines multiple technical indicators to provide a holistic view of market conditions, enhancing trade signal accuracy.

Scalping Options: Offers an optional scalping mechanism to capitalize on short-term price movements, increasing trading flexibility.

Dynamic Take Profit Levels: Adjusts TP targets based on the number of consecutive trades, maximizing profit potential during favorable trends.

Advanced Volume Analysis: Utilizes various volume indicators to confirm trend strength and validate trade signals.

Customizable Range Filtering: Filters trades based on market volatility, ensuring trades are taken during optimal conditions.

Heikin-Ashi Candle Support: Optionally uses Heikin-Ashi candles for smoother price action analysis and reduced noise.

====Recommendations====

Thorough Backtesting:

Historical Performance: Before deploying the strategy in a live trading environment, perform comprehensive backtesting to understand its performance under various market conditions. These are the premium settings for Avalanche Coinbase.

Optimization: Regularly review and adjust input parameters to ensure the strategy remains effective amidst changing market volatility and trends. Backtest the strategy for each crypto and make sure you are in the right brokage when using the volume sources as it will affect the overall outcome of the trading strategy.

Risk Management:

Position Sizing: Adjust the default_qty_value to align with your risk tolerance and account size.

Stop-Loss Implementation: Although the strategy includes TP levels, they're also consided to be a stop-loss mechanisms to protect against adverse market movements.

Commission Adjustment: Ensure the commission_value accurately reflects your broker's fees to maintain realistic backtesting results. Generally, 0.1~0.3% are most of the average broker's comission fees.

Slipage: The slip comssion is 1 Tick, since the strategy is adjusted to only enter/exit on bar close where most positions are available.

Continuous Monitoring:

Strategy Performance: Regularly monitor the strategy's performance to ensure it operates as expected and make adjustments as needed. A max-drawndown hit has been added to operate in case the premium Avalanche settings go wrong, but you can turn it off an adjust the equity percentage to 50% if you are confortable with the high volatile max-drown or even 100% if your account allows you to borrow cash.

Customization:

Indicator Parameters: Tailor indicator settings (e.g., ADX length, RSI period, MA types) to better fit your specific trading style and market conditions.

Scalping Options: Enable or disable scalping based on your trading preferences and risk appetite.

Conclusion

Gabriel's Witcher Strategy is a robust and versatile trading solution designed to navigate the complexities of the Crypto market. By integrating a wide array of technical indicators and providing extensive customization options, this strategy empowers traders to execute informed and strategic trades. Its comprehensive approach, combining trend analysis, momentum detection, volume evaluation, and range filtering, ensures that trades are taken during optimal market conditions. Additionally, the inclusion of scalping features and dynamic take-profit management enhances the strategy's adaptability and profitability potential. Unlike any trading strategy, with both diligent testing and continuous monitoring under the strategy tester, it's possible to achieve sustained success by adjusting the settings to the individual Crypto that need it, for example this one is preset for Avalanche Coinbase 65 Miinutes but it can be adjust for BTCUSD or Etherium if you backtest and search for the right settings.

Streak-Based Trading StrategyThe strategy outlined in the provided script is a streak-based trading strategy that focuses on analyzing winning and losing streaks. It’s important to emphasize that this strategy is not intended for actual trading but rather for statistical analysis of streak series.

How the Strategy Works

1. Parameter Definition:

• Trade Direction: Users can choose between “Long” (buy) and “Short” (sell).

• Streak Threshold: Defines how many consecutive wins or losses are needed to trigger a trade.

• Hold Duration: Specifies how many periods the position will be held.

• Doji Threshold: Determines the sensitivity for Doji candles, which indicate market uncertainty.

2. Streak Calculation:

• The script identifies Doji candles and counts winning and losing streaks based on the closing price compared to the previous closing price.

• Streak counting occurs only when no position is currently held.

3. Trade Conditions:

• If the loss streak reaches the defined threshold and the trade direction is “Long,” a buy position is opened.

• If the win streak is met and the trade direction is “Short,” a sell position is opened.

• The position is held for the specified duration.

4. Visualization:

• Winning and losing streaks are plotted as histograms to facilitate analysis.

Scientific Basis

The concept of analyzing streaks in financial markets is well-documented in behavioral economics and finance. Studies have shown that markets often exhibit momentum and trend-following behavior, meaning the likelihood of consecutive winning or losing periods can be higher than what random statistics would suggest (see, for example, “The Behavior of Stock-Market Prices” by Eugene Fama).

Additionally, empirical research indicates that investors often make decisions based on psychological factors influenced by streaks. This can lead to irrational behavior, as they may focus on past wins or losses (see “Behavioral Finance: Psychology, Decision-Making, and Markets” by R. M. F. F. Thaler).

Overall, this strategy serves as a tool for statistical analysis of streak series, providing deeper insights into market behavior and trends rather than being directly used for trading decisions.

Bidirectional Trend Reversal StrategyBidirectional Trend Reversal Strategy

This strategy aims to identify potential trend reversals and execute trades accordingly, focusing on both long and short positions. It uses a crossover of the Simple Moving Average (SMA) with price action as a key signal. When the price crosses above the SMA and the previous period was bearish (closed lower than it opened), the script opens a long position ("o-Long"). The exit ("e-Long") occurs when the target or stop-loss levels are hit, which are dynamically set using the ATR (Average True Range).

For short trades, when the price crosses below the SMA and the previous period was bullish (closed higher than it opened), the script opens a short position ("o-Short"). The exit ("e-Short") follows the same ATR-based logic for stop-loss and take-profit.

All settings, including SMA and ATR parameters, are fully customizable, allowing users to adapt the strategy to different market conditions and personal trading preferences.

This approach provides a systematic way to capture trend reversals and manage trades with clear entry and exit signals based on market momentum and volatility.

Example Setup:

Market: Forex

Pair: USD/GBP

Order size: 100,000 Contracts (1 Lot)

Timeframe: 15 minutes

SMA: 93

ATR Length: 15

Stop-Loss (ATR Multiplier): 7

Take-Profit Multiplier: 2

Experiment with different settings to achieve the best results for your trading style and market conditions.

Friday Bond Short StrategyStrategy: Friday Bond Short Strategy (1H Timeframe)

Objective:

This strategy aims to open short positions on a specified day and hour (Eastern Time) and close those positions on another specified day and hour. The background color of the chart will turn green when a position is active, providing a visual cue of an open trade.

Parameters:

1. Entry Day:

• Defines the day of the week on which the short position will be opened.

• Value: 6 for Friday (Pine Script’s weekday numbering: Monday = 2, Friday = 6).

2. Entry Hour:

• Specifies the hour (Eastern Time) when the short position will be opened.

• Value: 13 for 13:00 ET (1:00 PM).

3. Exit Day:

• Defines the day of the week on which the short position will be closed.

• Value: 2 for Monday.

4. Exit Hour:

• Specifies the hour (Eastern Time) when the position will be closed.

• Value: 13 for 13:00 ET (1:00 PM).

How It Works:

1. Time Adjustment to Eastern Time:

• The script converts all time references to Eastern Time (America/New_York) to ensure the strategy operates according to the desired time zone.

2. Entry Conditions:

• The strategy checks if the current day of the week matches the specified entry_day and if the current hour matches the specified entry_hour.

• If both conditions are met, a short position is opened (strategy.entry("Short", strategy.short)).

3. Exit Conditions:

• Similarly, the strategy checks if the current day of the week matches the specified exit_day and if the current hour matches the specified exit_hour.

• If both conditions are met, the open short position is closed (strategy.close("Short")).

4. Background Color:

• The background color of the chart is adjusted based on whether there is an open position:

• Green Background: If the strategy has an open position (strategy.position_size > 0), the background is set to light green.

• No Background Color: If there is no open position, the background color is not set (na).

Summary:

The Friday Bond Short Strategy is designed to enter short positions on Fridays at 1:00 PM ET and close them on Mondays at 1:00 PM ET. The chart background color turns green when a short position is active, providing a clear visual indication of when the strategy is engaged in a trade.

Fractal Breakout Trend Following StrategyOverview

The Fractal Breakout Trend Following Strategy is a trend-following system which utilizes the Willams Fractals and Alligator to execute the long trades on the fractal's breakouts which have a high probability to be the new uptrend phase beginning. This system also uses the normalized Average True Range indicator to filter trades after a large moves, because it's more likely to see the trend continuation after a consolidation period. Strategy can execute only long trades.

Unique Features

Trend and volatility filtering system: Strategy uses Williams Alligator to filter the counter-trend fractals breakouts and normalized Average True Range to avoid the trades after large moves, when volatility is high

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Flexible Risk Management: Users can choose the stop-loss percent (by default = 3%) for trades, but strategy also has the dynamic stop-loss level using down fractals.

Methodology

The strategy places stop order at the last valid fractal breakout level. Validity of this fractal is defined by the Williams Alligator indicator. If at the moment of time when price breaking the last fractal price is higher than Alligator's teeth line (8 period SMA shifted 5 bars in the future) this is a valid breakout. Moreover strategy has the additional volatility filtering system using normalized ATR. It calculates the average normalized ATR for last user-defined number of bars and if this value lower than the user-defined threshold value the long trade is executed.

When trade is opened, script places the stop loss at the price higher of two levels: user defined stop-loss from the position entry price or down fractal validation level. The down fractal is valid with the rule, opposite as the up fractal validation. Price shall break to the downside the last down fractal below the Willians Alligator's teeth line.

Strategy has no fixed take profit. Exit level changes with the down fractal validation level. If price is in strong uptrend trade is going to be active until last down fractal is not valid. Strategy closes trade when price hits the down fractal validation level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 3% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Williams Fractals to open long trade when price has broken the key resistance level to the upside. This resistance level is the last up fractal and is shall be broken above the Williams Alligator's teeth line to be qualified as the valid breakout according to this strategy. The Alligator filtering increases the probability to avoid the false breakouts against the current trend.

Moreover strategy has an additional filter using Average True Range(ATR) indicator. If average value of ATR for the last user-defined number of bars is lower than user-defined threshold strategy can open the long trade according to open trade condition above. The logic here is following: we want to open trades after period of price consolidation inside the range because before and after a big move price is more likely to be in sideways, but we need a trend move to have a profit.

Another one important feature is how the exit condition is defined. On the one hand, strategy has the user-defined stop-loss (3% below the entry price by default). It's made to give users the opportunity to restrict their losses according to their risk-tolerance. On the other hand, strategy utilizes the dynamic exit level which is defined by down fractal activation. If we assume the breaking up fractal is the beginning of the uptrend, breaking down fractal can be the start of downtrend phase. We don't want to be in long trade if there is a high probability of reversal to the downside. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.19%

Maximum Single Profit: +24.97%

Net Profit: +3036.90 USDT (+30.37%)

Total Trades: 83 (28.92% win rate)

Profit Factor: 1.953

Maximum Accumulated Loss: 963.98 USDT (-8.29%)

Average Profit per Trade: 36.59 USDT (+1.12%)

Average Trade Duration: 72 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h and higher time frames and the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

HMA Crossover 1H with RSI, Stochastic RSI, and Trailing StopThe strategy script provided is a trading algorithm designed to help traders make informed buy and sell decisions based on certain technical indicators. Here’s a breakdown of what each part of the script does and how the strategy works:

Key Components:

Hull Moving Averages (HMA):

HMA 5: This is a Hull Moving Average calculated over 5 periods. HMAs are used to smooth out price data and identify trends more quickly than traditional moving averages.

HMA 20: This is another HMA but calculated over 20 periods, providing a broader view of the trend.

Relative Strength Index (RSI):

RSI 14: This is a momentum oscillator that measures the speed and change of price movements over a 14-period timeframe. It helps identify overbought or oversold conditions in the market.

Stochastic RSI:

%K: This is the main line of the Stochastic RSI, which combines the RSI and the Stochastic Oscillator to provide a more sensitive measure of overbought and oversold conditions. It is smoothed with a 3-period simple moving average.

Trading Signals:

Buy Signal:

Generated when the 5-period HMA crosses above the 20-period HMA, indicating a potential upward trend.

Additionally, the RSI must be below 45, suggesting that the market is not overbought.

The Stochastic RSI %K must also be below 39, confirming the oversold condition.

Sell Signal:

Generated when the 5-period HMA crosses below the 20-period HMA, indicating a potential downward trend.

The RSI must be above 60, suggesting that the market is not oversold.

The Stochastic RSI %K must also be above 63, confirming the overbought condition.

Trailing Stop Loss:

This feature helps protect profits by automatically selling the position if the price moves against the trade by 5%.

For sell positions, an additional trailing stop of 100 points is included.

Advanced Gold Scalping Strategy with RSI Divergence# Advanced Gold Scalping Strategy with RSI Divergence

## Overview

This Pine Script implements an advanced scalping strategy for gold (XAUUSD) trading, primarily designed for the 1-minute timeframe. The strategy utilizes the Relative Strength Index (RSI) indicator along with its moving average to identify potential trade setups based on divergences between price action and RSI movements.

## Key Components

### 1. RSI Calculation

- Uses a customizable RSI length (default: 60)

- Allows selection of the source for RSI calculation (default: close price)

### 2. Moving Average of RSI

- Supports multiple MA types: SMA, EMA, SMMA (RMA), WMA, VWMA, and Bollinger Bands

- Customizable MA length (default: 3)

- Option to display Bollinger Bands with adjustable standard deviation multiplier

### 3. Divergence Detection

- Implements both bullish and bearish divergence identification

- Uses pivot high and pivot low points to detect divergences

- Allows for customization of lookback periods and range for divergence detection

### 4. Entry Conditions

- Long Entry: Bullish divergence when RSI is below 40

- Short Entry: Bearish divergence when RSI is above 60

### 5. Trade Management

- Stop Loss: Customizable, default set to 11 pips

- Take Profit: Customizable, default set to 33 pips

### 6. Visualization

- Plots RSI line and its moving average

- Displays horizontal lines at 30, 50, and 70 RSI levels

- Shows Bollinger Bands when selected

- Highlights divergences with "Bull" and "Bear" labels on the chart

## Input Parameters

- RSI Length: Adjusts the period for RSI calculation

- RSI Source: Selects the price source for RSI (close, open, high, low, hl2, hlc3, ohlc4)

- MA Type: Chooses the type of moving average applied to RSI

- MA Length: Sets the period for the moving average

- BB StdDev: Adjusts the standard deviation multiplier for Bollinger Bands

- Show Divergence: Toggles the display of divergence labels

- Stop Loss: Sets the stop loss distance in pips

- Take Profit: Sets the take profit distance in pips

## Strategy Logic

1. **RSI Calculation**:

- Computes RSI using the specified length and source

- Calculates the chosen type of moving average on the RSI

2. **Divergence Detection**:

- Identifies pivot points in both price and RSI

- Checks for higher lows in RSI with lower lows in price (bullish divergence)

- Checks for lower highs in RSI with higher highs in price (bearish divergence)

3. **Trade Entry**:

- Enters a long position when a bullish divergence is detected and RSI is below 40

- Enters a short position when a bearish divergence is detected and RSI is above 60

4. **Position Management**:

- Places a stop loss order at the entry price ± stop loss pips (depending on the direction)

- Sets a take profit order at the entry price ± take profit pips (depending on the direction)

5. **Visualization**:

- Plots the RSI and its moving average

- Draws horizontal lines for overbought/oversold levels

- Displays Bollinger Bands if selected

- Shows divergence labels on the chart for identified setups

## Usage Instructions

1. Apply the script to a 1-minute XAUUSD (Gold) chart in TradingView

2. Adjust the input parameters as needed:

- Increase RSI Length for less frequent but potentially more reliable signals

- Modify MA Type and Length to change the sensitivity of the RSI moving average

- Adjust Stop Loss and Take Profit levels based on current market volatility

3. Monitor the chart for Bull (long) and Bear (short) labels indicating potential trade setups

4. Use in conjunction with other analysis and risk management techniques

## Considerations

- This strategy is designed for short-term scalping and may not be suitable for all market conditions

- Always backtest and forward test the strategy before using it with real capital

- The effectiveness of divergence-based strategies can vary depending on market trends and volatility

- Consider using additional confirmation signals or filters to improve the strategy's performance

Remember to adapt the strategy parameters to your risk tolerance and trading style, and always practice proper risk management.

MA MACD BB BackTesterOverview:

This Pine Script™ code provides a comprehensive backtesting tool that combines Moving Average (MA), Moving Average Convergence Divergence (MACD), and Bollinger Bands (BB). It is designed to help traders analyze market trends and make informed trading decisions by testing various strategies over historical data.

Key Features:

1. Customizable Indicators:

Moving Average (MA): Smooths out price data for clearer trend direction.

MACD: Measures trend momentum through MACD Line, Signal Line, and Histogram.

Bollinger Bands (BB): Identifies overbought or oversold conditions with upper and lower bands.

2. Flexible Trading Direction: Choose between long or short positions to adapt to different market conditions.

3. Risk Management: Efficiently allocate your capital with customizable position sizes.

4. Signal Generation:

Buy Signals: Triggered by crossovers for MACD, MA, and BB.

Sell Signals: Triggered by crossunders for MACD, MA, and BB.

5. Automated Trading: Automatically enter and exit trades based on signal conditions and strategy parameters.

How It Works:

1. Indicator Selection: Select your preferred indicator (MA, MACD, BB) and trading direction (Long/Short).

2. Risk Management Configuration: Set the percentage of capital to allocate per position to manage risk effectively.

3.Signal Detection: The algorithm identifies and plots buy/sell signals directly on the chart based on the chosen indicator.

4. Trade Execution: The strategy automatically enters and exits trades based on signal conditions and configured strategy parameters.

Use Cases:

- Backtesting: Evaluate the effectiveness of trading strategies using historical data to understand potential performance.

- Strategy Development: Customize and expand the strategy to incorporate additional indicators or conditions to fit specific trading styles.

ADDONS That Affect Strategy:

1. Indicator Parameters:

Adjustments to the settings of MACD (e.g., fast length, slow length), MA (e.g., length), and BB (e.g., length, multiplier) will directly impact the detection of signals and the strategy's performance.

2. Trading Direction:

Changing the trading direction (Long/Short) will alter the entry and exit conditions based on the detected signals.

3. Risk Management Settings:

Modifying the position size percentage affects capital allocation and overall risk exposure per trade.

ADDONS That Do Not Affect Strategy:

1. Visual Customizations:

Changes to the color, shape, and style of the plotted lines and signals do not impact the core functionality of the strategy but enhance visual clarity.

2. Text and Labels:

Modifying text labels for the signals (such as renaming "Buy MACD" to "MACD Buy Signal") is purely cosmetic and does not influence the strategy’s logic or outcomes.

Notes:

- Customization: The indicator is highly customizable to fit various trading styles and market conditions.

- Risk Management: Adjust position sizes and risk parameters according to your risk tolerance and account size.

- Optimization: Regularly backtest and optimize parameters to adapt to changing market dynamics for better performance.

Getting Started:

-Add the script to your chart.

-Adjust the input parameters to suit your analysis preferences.

-Observe the marked buy and sell signals on your chart to make informed trading decisions.

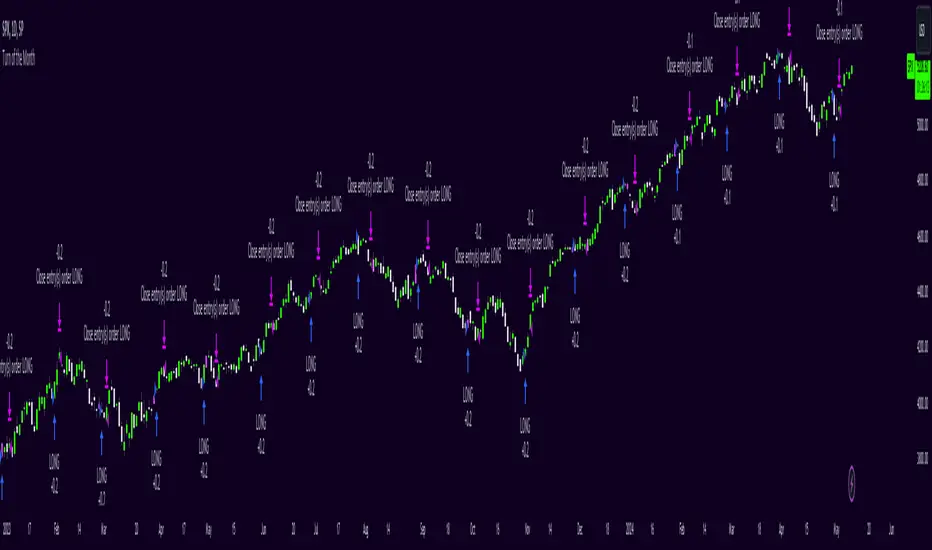

Turn of the Month Strategy [Honestcowboy]The end of month effect is a well known trading strategy in the stock market. Quite simply, most stocks go up at the end of the month. What's even better is that this effect spills over to the next phew days of the next month.

In this script we backtest this theory which should work especially well on SP500 pair.

By default the strategy buys 2 days before the end of each month and exits the position 3 days into the next month.

The strategy is a long only strategy and is extremely simple. The SP500 is one of the #1 assets people use for long term investing due to it's "9.8%" annualised return. However as a trader you want the best deal possible. This strategy is only inside the market for about 25% of the time while delivering a similar return per exposure with a lower drawdown.

Here are some hypothesis why turn of the month effect happens in the stock markets:

Increased inflow from savings accounts to stocks at end of month

Rebalancing of portfolios by fund managers at end of month

The timing of monthly cash flows received by pension funds, which are reinvested in the stock market.

The script also has some inputs to define how many days before end of the month you want to buy the asset and how long you want to hold it into the next month.

It is not possible to buy the asset exactly on this day every month as the market closes on the weekend. I've added some logic where it will check if that day is a friday, saturdady or sunday. If that is the case it will send the buy signal on the end of thursday, this way we enter on the friday and don't lose that months trading opportunity.

The backtest below uses 4% exposure per trade as to show the equity curve more clearly and because of publishing rules. However, most fund managers and investors use 100% exposure. This way you actually risk money to earn money. Feel free to adjust the settings to your risk profile to get a clearer picture of risks and rewards before implementing in your portfolio.

[Support and Resistance with Trend Lines] with Backtest (TSO) with Backtest (TSO)

===========================================================================

===========================================================================

This indicator serves as a comprehensive full-cycle trading system, providing alerts at each stage of the trade, from opening to closure. The algorithm uses most recent and historical S&R (Support and Resistance) levels with most recent and historical Trend Lines, generating signals for trades when Breaks/Bounces occur (Trade Open Signal triggers can be configured via very customizable indicator Input "Signal Trigger Matrix" settings). With signal for trade open, TP (Take Profit and SL (Stop Loss) levels are calculated as well and marked on the chart including alerts for each action of the trade. The indicator offers a variety of automated approaches for TP (Take-Profit) and SL (Stop-Loss) settings. These include static current/historical S&R (Support and Resistance) levels or S&R/Trend Lines dynamic breaks for TP (Take-Profit) and various SL (Stop-Loss) approaches, including ATR Trailing SL, opposite S&R (Support and Resistance) levels SL, opposite Trend Lines SL and more. This diverse set of tools ensure flexibility in tailoring TP (Take-Profit) and SL (Stop-Loss) parameters to different market conditions, contributing to a more adaptive and robust trading system. Additionally, a series of signal analysis tools, including market sentiment, candle bar analysis, divergence, and volume, enhance the precision of trading signals.

* Works with popular timeframes: 1M, 3M, 5M, 15M, 30M, 45M, 1H.

* Works well with Futures and Indices, can be used to trade Stocks, Crypto and FOREX.

* Includes LIVE alert/labels Breakouts and Bounces signal trigger feature, which can be used for scalping (NOTE: This approach cannot be backtested).

* Every action of the trade is calculated on a confirmed closed candle bar state (barstate.isconfirmed), so the indicator will never repaint.

==============================================================

Indicator examples:

---------------------------------------------------------------------------

Strategy Config: SRTL_MES_15M3Y_EODoff_ALL

Here is a nice example of MES (Micro E-Mini S&P 500 Index Futures) configuration, which uses S&R (Support and Resistance) breakouts as signal trigger with Elliot Wave confirmation and previous S&R historical levels for TP (Take-Profit).

---------------------------------------------------------------------------

An example of an intraday Tesla trade. Also the green arrows will be displayed IMMEDIATELY when Breakout/Reverse Bounce occurs (same an Alert will be triggered immediately).

===========================================================================

Trading open/close/TP/SL labels, plots and colors explanations:

---------------------------------------------------------------------------

>>> S&R (Support and Resistance) levels/lines: orange - support, blue - resistance (can be hidden).

>>> Trend Lines: yellow - support, green - resistance (can be hidden).

>>> Blue labels show resistance breakouts and bounces, light-blue - bullish, dark-blue - bearish

>>> Yellow labels show resistance breakouts and bounces, light-yellow - bullish, dark-yellow - bearish

>>> Green/Red arrows on top/bottom of candle bar will show LIVE breakouts (if turned on)

>>>>> LONG open: green "house" looking arrow below candle bar.

>>>>> SHORT open: red "house" looking arrow above candle bar.

>>>>> LONG/SHORT take-profit target: green/red circles (multi-profit > TP2/3/4/5 smaller circles).

>>>>> LONG/SHORT stop-loss target: green/red + crosses.

>>>>> LONG/SHORT take-profit hits: green/red diamonds.

>>>>> LONG/SHORT stop-loss hits: green/red X-crosses.

>>>>> LONG/SHORT EOD (End of Day | Intraday style) close (profitable trade): green/red squares.

>>>>> LONG/SHORT EOD (End of Day | Intraday style) close (loss trade): green/red PLUS(+)-crosses.

===========================================================================

STATS TABLE ///////////////////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Trading STATS table on the chart showing current trade direction, Last TP (Take-Profit) Taken, Current Trade PL (profit/loss in price difference from trade open to the very current state).

---------------------------------------------------------------------------

CUSTOM TRADING DATE RANGE /////////////////////////////////////////////////

---------------------------------------------------------------------------

>>>>> This feature can be used to manually set indicator trading range from and to a specific date and time. NOTE: This is not intended for a very long date range backtesting, utilize TradingView Strategy Tester for that.

* Use TradingView “Strategy Tester” to see Backtesting results

NOTE: If Strategy Tester does not show any results with Date Ranged fully unchecked, there may be an issue where a script opens a trade, but there is not enough TradingView power to set the Take-Profit and Stop-Loss and somehow an open trade gets stuck and never closes, so there are “no trades present”. In such case - manually check “Start”/“End” dates or use “Deep Backtesting” feature!

---------------------------------------------------------------------------

INTRADAY ACTIVE TRADING SESSION CONFIGURATION /////////////////////////////

---------------------------------------------------------------------------

>>> Regional Active Trading Session Hours Schedule: If selected - trades will only open during regional active trading session, if 'OFF', there will be no trading schedule and trades will open 24/7.

>>> EOD(End of Day) Close - On/Off: Close the trade if it's still open at the end of active trading session (on the very last candle bar). NOTE: If no region is selected at 'Regional Active Trading Session Schedule' - there will be no EOD(End of Day) Close and trades will run overnight until either SL(Stop-Loss) or TP(Take-Profit) is hit!

>>>>> EOD(End of Day) Close - 1 candle bar before last: This is specifically for stocks as while usually indices can be closed 15minutes after the market closes, for stocks - the last candle bar closes at the same time with the market active trading session, which if closed - trades can't be closed until next day/session! Enable this setting for the trade to close/alert 1 candle bar before the last one, so there is still time to close the trade at the Broker (NOTE: depending on the timeframe, 1 candle bar can be: 15sec, 30sec, 1min, 3min, 5min, 15min, 30min, 45min, 1h).

---------------------------------------------------------------------------

SIGNAL TRIGGER MATRIX ////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Trading Engine: This setting turns on TradingView Strategy trading engine for backtesting.

>>> Market Session Only: With this setting turned on, all signal trigger Breaks/Bounces will be hidden during Pre/Post market time.

>>> Plot S&R Levels/Lines: Plot S&R (Support and Resistance) on chart. Note: historical levels/lines will only be plotted if hit (Break/Bounce).

>>> Plot Trend Lines Levels/Lines: Plot Trend Lines levels/lines on chart. Note: historical levels/lines will only be plotted if hit (Break/Bounce).

>>> Use S&R Current Levels | Use S&R Historical Levels | Use Trend Lines Current Levels | Use Trend Lines Historical Levels |: Choose which levels should be used for Breaks/Bounces to be captured on. If all triggers are turned on/checked - whatever happens 1st wins the trigger.

>>> Breaks | Bounces: 'Breaks': Turn on Breaks through levels/lines signal trigger. | 'Bounces': Turn on Bounces off levels/lines signal trigger.

>>> Signal: Regular | Signal: S&R Combo | Signal: TL Combo | Signal: S&R + TL Combo | Signal: Repeat Action |: Trade open signal trigger execution approach MATRIX (If 1 or more turned on at the same time - whatever comes first will be the trade signal trigger). 'Regular': A single Break/Bounce must occur on a closed bar for signal trigger. 'S&R Combo': A combination of 2 Current + Historical S&R (Support and Resistance) Break/Bounce must happen in the same direction on same bar for signal trigger. 'TL Combo': A combination of 2 Current + Historical Trend Lines Break/Bounce must happen in the same direction on same bar for signal trigger. 'S&R + TL Combo': a combination of ANY S&R and Trend Line Break/Bounce must happen in the same direction on same bar for signal trigger. 'Repeat Action': Initial and then confirmation (2nd/3rd/etc. consecutive occurence) Break/Bounce must occur on same level/line for signal trigger.

>>> Historical - Look Back (# of days): How far back (in # of days) will historical S&R/Trend Lines will be used for Trade Open signals/TP/SL/etc.

>>> Historical - Look Back Invalidation (# of days): IF THERE IS TOO MUCH HISTORICAL LEVELS/LINES ON CHART - LOWER THIS SETTING + MAKE SURE IT'S SMALLER THAN 'Historical - Look Back (# of days)'. With big Look back period (5+ days) - it can become very messy with too many historical levels/lines. To clear oldest historical levels/lines - set Look Back Invalidation # of days to less than Historical Look Back # of days. (After X # of Look Back Invalidation days - older levels/lines will become invalidated and no longer used for opening trades/TP (Take-Profit)/SL (Stop-Loss), while newer levels/lines will still be discovered.

>>> S&R/Trend Lines - Support/Resistance combined into 1 entity: Every level or a line becomes simply a level or a line, regardless if it originally was a support or resistance. By default, depending on the level/line originally being support or resistance - the signal direction will be such as: Resistance is broken > LONG / bounced > SHORT; Support is broken > SHORT / bounced > LONG; with this setting on, either level or line can be both broken or bounced off in ANY direction, trade open direction will depend on current market sentiment only.

---------------------------------------------------------------------------

S&R CONFIGURATION ////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> S&R Search - Left Bars (current): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with below - Right Bars).

>>> S&R Search - Right Bars (current): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with above - Left Bars).

>>> S&R Search - Custom Resolution (current): This is a custom timeframe setting specifically for S&R Search, it disregards current chart timeframe. This is great to use for scalping, for example: with main chart set to 1min and the custom timeframe set to 3min or 5min - there will be stronger support/resistance levels with more detailed price action.

>>> S&R Search - Left Bars (historical): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with below - Right Bars).

>>> S&R Search - Right Bars (historical): This setting is for calculating optimal S&R (Support and Resistance) levels (in combination with above - Left Bars).

>>> S&R Search - Custom Resolution (historical): This is a custom timeframe setting specifically for S&R Search, it disregards current chart timeframe. This is great to use for scalping, for example: with main chart set to 1min and the custom timeframe set to 3min or 5min - there will be stronger support/resistance levels with more detailed price action.

>>> S&R - Historical S&R Levels - Extend to the right: Extend all S&R lines to the right.

>>> S&R (Current/Historical) - Live Breakout/Bounce - ALERT/SHOW: NOTE: Alert wlil trigger immediately at price Breaking thru or Bouncing off level/line and an arrow above /below the bar will show the direction of breakout/bounce. If on that same live bar - price comes back causing the Breakout/Bounce become no longer valid - the arrow will disappear as the condition of the Break/Bounce will no longer be valid.

---------------------------------------------------------------------------

TREND LINES CONFIGURATION ////////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Show: Trend Line development (where it 'did not exist' yet): It takes 2 pivots to develop a trend line, pivot is established at least 3 candle bars later from where the pivot is. With this setting turned on - it will plot dashed lines where trend lines originated connecting the 1st and 2nd pivot point up to where the trend line became established (where in reality you would now be able to draw a certain trend line). Established already generated trend line are plotted with a solid line.

>>> Trend Lines - Line Slope Confirmation: LONG breakout will only be shown if trend line is goind downslope \. SHORT breakout will only be shown if trend line is goind upslope /.

>>> Trend Lines - Search - Left Bars (current): This setting is for calculating optimal Trend Lines.

>>> Trend Lines - Search - Right Bars (current): This setting is for calculating optimal Trend Lines.

>>> Trend Lines - Custom Resolution (current): This is a custom timeframe setting specifically for S&R Search, it disregards current chart timeframe. This is great to use for scalping, for example: with main chart set to 1min and the custom timeframe set to 3min or 5min - there will be stronger support/resistance levels with more detailed price action.

>>> Trend Lines - Search - Left Bars (historical): This setting is for calculating optimal Trend Lines.

>>> Trend Lines - Search - Right Bars (historical): This setting is for calculating optimal Trend Lines.

>>> Trend Lines - Custom Resolution (historical): This is a custom timeframe setting specifically for S&R Search, it disregards current chart timeframe. This is great to use for scalping, for example: with main chart set to 1min and the custom timeframe set to 3min or 5min - there will be stronger support/resistance levels with more detailed price action.

>>> Trend Lines - Historical Trend Lines - Extend to the right: Extend all Trend Lines to the right.

>>> Trend Lines (Current/Historical) - Live Breakout/Bounce - ALERT/SHOW: NOTE: Alert will trigger immediately at price Breaking thru or Bouncing off level/line and an arrow above /below the bar will show the direction of breakout/bounce. If on that same live bar - price comes back causing the Breakout/Bounce become no longer valid - the arrow will disappear as the condition of the Break/Bounce will no longer be valid.

---------------------------------------------------------------------------

TAKE-PROFIT/STOP-LOSS CONFIGURATION ///////////////////////////////////////

---------------------------------------------------------------------------

>>> TP (Take-Profit) System: 'S&R Static Current/Historical': TP (Take-Profit) is calculated using current/historical S&R (Support & Resistance) levels at trade open and remains static. 'S&R/Trend Lines Dynamic Breaks': TP (Take-Profit) is fully dynamic and will be trigger at price above trade open price and with Breakout occurence (S&R or Trend Line current/historical breakout).

>>> TP (Take-Profit) # of targets: It is wise to divide the trade into several profit targets. With this setting - up to 5 TP (Take-Profit) targets can be approached. The trade will be equally divided up by the selected # of TP (Take-Profit) targets.

>>> SL (Stop-Loss) System: 'ATR-Trailing-SL': SL (Stop-Loss) is trail-following the ATR (Average True Range) line, NOTE: If at signal trigger, ATR will be against the trade direction - trade open signal will be skipped; 'S&R-Static-SL': SL (Stop-Loss) is set at trade open per optimal most recent S&R level and remains there until trade closes; 'TrendLines-Static-SL': SL (Stop-Loss) is set at trade open per optimal most recent trend line and remains there until trade closes; 'TrendLines-Dynamic-SL': SL (Stop-Loss) will be set per current opposite trend line and follow it until trade is open.; 'Oppos-Sig-Trd-in-Loss': SL (Stop-Loss) will trigger at opposite signal with trade currently at loss.

>>> SL (Stop-Loss) - On/Off: Without SL (Stop-Loss), unless EOD (End of Day) Close is turned on - there will be no SL (Stop-Loss) at all!

---------------------------------------------------------------------------

MARKET SENTIMENT CONFIRMATION ///////////////////////////////////////

---------------------------------------------------------------------------

>>> Market Sentiment: Signal is confirmed per Market Sentiment direction. If Market Sentiment is turned off - whatever signal comes 1st will be the trade open trigger.

---------------------------------------------------------------------------

SIGNAL ANALYSIS AND CLEANUP ///////////////////////////////////////////////

---------------------------------------------------------------------------

>>> Signal Cleanup - Bar Color: Include Bar Color (bullish/bearish) confirmation, LONG signal will only be opened if signal bar is green/bullish, SHORT if red/bearish.

>>> Signal Cleanup - Bar Directional Structure: Skip opposite bar structure types signals (For example: bearish green hammer).

>>> Signal Cleanup - Bar Doji Skip: Skip doji (indecisive) candles signals.

>>> Signal Cleanup - EWO (Elliott Wave Oscillator): Include EWO (Elliott Wave Oscillator), LONG will only be opened if EWO is bullish / SHORT if EWO is bearish.

>>> Signal Cleanup - VWAP (Volume-Weighted Average Price): Include VWAP (Volume-Weighted Average Price), LONG will only be opened if price is above VWAP / SHORT if price is below VWAP.

>>> Signal Cleanup - MA (Moving Average) Confirmation: Include MA (Moving Average), LONG will only be opened if MA is bullish / SHORT if MA is bearish.

>>> Signal Cleanup - ATR (Average True Range): Include ATR (Average True Range) confirmation, LONG will only be opened if ATR is bullish / SHORT if ATR is bearish.

>>> Signal Cleanup - Divergence(RSI + MACD): Include Divergence (RSI + MACD ) confirmation, LONG will only be opened if Divergence is bullish / SHORT if Divergence is bearish.

>>> Signal Cleanup - Volume % Strength: Include Volume strength/percentage confirmation, LONG/SHORT will only be opened with strong Volume matching the signal direction | By default, strong Volume percentage is set to 150% and weak to 50%.

>>> Signal Cleanup - Volume Above Average: Include Volume Above Moving Average (Volume closing bar closes above volume moving average) confirmation, LONG/SHORT will only be opened with Volume above average - Volume closed bar color must match the closed price color (bullish/bearish direction) + Volume bar must be closed above volume MA line).

---------------------------------------------------------------------------

===========================================================================

||||||||||||||||||||||||||||||||||| *** ||||||||||||||||||||||||||||||||||| *** |||||||||||||||||||||||||||||||||||

||||||||||||||||||||||||||||||||||| *** ||||||||||||||||||||||||||||||||||| *** |||||||||||||||||||||||||||||||||||

TP System - VERY IMPORTANT INFO!

-------------------------------------------------------------------------------------------------------------------

"TP PERCENTAGE" - amount by which current trade/position needs to be reduced/partially closed/sold.

-------------------------------------------------------------------------------------------------------------------

TP System: Dynamic

"TP PERCENTAGE" - will always be the same amount (trade/position size divided by the # of take-profit(TP) targets) and percentage to be closed will always be of the ORIGINAL trade/position.

-------------------------------------------------------------------------------------------------------------------

TP System: Static

"TP PERCENTAGE" - will always be the same amount IF take-profit(TP) targets are hit 1-by-1 (TP1 > TP2 > TP3 > TP4 > TP5), otherwise it will vary and unless it is a 1st take-profit(TP1), the REMAINING trade/position size will always be smaller than original and therefore the percentage to be closed will always be of the REMAINING trade/position and NOT the original one!

-------------------------------------------------------------------------------------------------------------------

"TP PERCENTAGE" CheatSheet (these are the only percentages you may see)

-----------------------------------------------------------------------

TP PERCENTAGE---Close/Sell Amount-------------Example (trade size: 50 stocks)

20%-------------trade size * 0.2--------------50 * 0.2 = 10 stocks

25%-------------trade size * 0.25-------------50 * 0.25 = 12.5(~13) stocks

34%-------------trade size * 0.34-------------50 * 0.34 = 17 stocks

40%-------------trade size * 0.4--------------50 * 0.4 = 20 stocks

50%-------------trade size * 0.5--------------50 * 0.5 = 25 stocks

60%-------------trade size * 0.6--------------50 * 0.6 = 30 stocks

66%-------------trade size * 0.66-------------50 * 0.66 = 33 stocks

75%-------------trade size * 0.75-------------50 * 0.75 = 37.5(~38) stocks

80%-------------trade size * 0.8--------------50 * 0.8 = 40 stocks

100%------------trade size--------------------50 = 50 stocks

-----------------------------------------------------------------------

If for any reason a portion of the current/remaining trade closed at such occurrence was slightly wrong, it is not an issue. Such occurrences are rare and with slight difference in partial TP closed is not significant to overall performance of our algorithms.

||||||||||||||||||||||||||||||||||| *** ||||||||||||||||||||||||||||||||||| *** |||||||||||||||||||||||||||||||||||

||||||||||||||||||||||||||||||||||| *** ||||||||||||||||||||||||||||||||||| *** |||||||||||||||||||||||||||||||||||

===========================================================================

Alert Settings (you don’t have to touch this section unless you will be using TradingView alerts through a Webhook to use with trading bot)

---------------------------------------------------------------------------

Here is how a LONG OPEN alert looks like.

NOTE: Each label , , etc. is customizable, you can change the text of it within indicator Input settings.

ALERT >>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

COIN: BTCUSD

TIMEFRAME: 15M

LONG: OPEN

ENTRY: 20000

TP1: 20500

TP2: 21000

TP3: 21500

TP4: 22500

TP5: 23500

SL: 19000

Leverage: 0

---------------------------------------------------------------------------

Here is how a TP1 alert will look with 5 TPs breakdown of the trade.

NOTE1: Next to TP1 taken it will show at which price it was triggered.

NOTE2: Next to "TP Percentage" it shows how much of the CURRENT/ACTIVE/REMAINING trade needs to be closed.

NOTE2: If TP2/3/4/5 comes before TP1 - the alert will tell you exactly how many percent of the trade needs to be closed!

ALERT >>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

COIN: BTCUSD

TIMEFRAME: 15M

LONG: TP1

TP1: 20500

TP Percentage: 20%

---------------------------------------------------------------------------

Here is how an alert will look for LONG - STOP-LOSS.

ALERT >>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

COIN: BTCUSD

TIMEFRAME: 15M

ENTRY: 20000

LONG: SL

SL: 19000

---------------------------------------------------------------------------

Here is how an alert will look for LONG - EOD (End of Day) In Profit close.

ALERT >>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

COIN: BTCUSD

TIMEFRAME: 15M

LONG: EOD-Close (profit)

ENTRY: 20000

EOD-Close: 21900

===========================================================================

Adding Alerts in TradngView

---------------------------------------------------------------------------

-Add indicator to chart and make sure the correct strategy is configured (check Backtesting results)

-Right-click anywhere on the TradingView chart

-Click on Add alert

-Condition: Select this indicator by it’s name

-Immediately below, change it to "alert() function calls only", as other wise there will be 2 alerts for every alert!

-Expiration: Open-ended (that may require higher tier TradingView account, otherwise the alert will need to be occasionally re-triggered)

-Alert name: Whatever you desire

-Hit “Create”

-Note: If you change ANY Settings within the indicator – you must DELETE the current alert and create a new one per steps above, otherwise it will continue triggering alerts per old Settings!

===========================================================================

Good Luck! (NOTE: Trading is very risky, past performance is not necessarily indicative of future results, so please trade responsibly!)

---------------------------------------------------------------------------

NOTE: There seems to be a strange glitch when strategy is running live, it will show "double-take" take-profits labels on the chart. This is not affecting the script logic and backtesting results, if you simply change the timeframe real quick to something else then back - it will no longer show the duplicate orders... this must be some sort of a glitch as every alert was thoroughly tested to make sure everything is working!

Universal Algorithm [BackQuant]Universal Algorithm

It is a trading strategy designed CLEAR TREND DETECTION . This script is the culmination of extensive research and development efforts aimed at providing traders with a robust tool capable of adapting to a wide array of market conditions. This description delves into the core components, methodologies, and operational parameters of Universal Algo to offer potential users a clear understanding of its functionalities and the principles underpinning its design.

Core Methodologies and Features:

Integrated Systems: Universal Algo is built around six core systems, each contributing unique analytical perspectives to enhance trade signal reliability. These systems are designed to identify clear trend opportunities for significant gains, while also employing logic to navigate through ranging markets effectively.

Adaptive Market Logic: By incorporating volatility metrics, the algorithm dynamically adjusts to changing market conditions. This ensures that the strategy remains effective across different market regimes, aiming to reduce market noise and improve signal quality.

Selective Shorting Mechanism: While the primary focus is on capturing long positions, it includes an optional shorting feature. This can be activated by users to adapt the strategy during macro downtrends, thus providing a flexible approach to market participation.

Backtesting and Forward-Testing Rigor : The strategy has undergone rigorous testing to validate its performance and reliability. It demonstrates prudent risk management by optimizing conditions under which short positions are considered, aiming to mitigate drawdowns and preserve capital.

Operational Parameters:

Customization Options: The script offers a range of user inputs, allowing for customization of the backtesting starting date, the decision to display the strategy equity curve, among other settings. These inputs cater to diverse trading needs and preferences, offering users control over their strategy implementation.

Transparency and Logic Insight: While specific calculation details and proprietary indicators are integral to maintaining the uniqueness of Universal Algo , the strategy is grounded on well-established financial analysis techniques. These include momentum analysis, volatility assessments, and adaptive thresholding, among others, to formulate its trade signals.

Realistic Trading Conditions : Backtesting, considered realistic trading conditions, including appropriate account size, commission, slippage, and sustainable risk levels per trade. The strategy is designed and tested with a focus on achieving a balance between risk and reward, striving for robustness and reliability rather than unrealistic profitability promises.

Concluding Thoughts:

Universal Algo is offered to the TradingView community as a tool for traders seeking to enhance their market analysis and trading strategies. Its development is driven by a commitment to quality, innovation, and adaptability, aiming to provide valuable insights and decision-support in various market conditions. Potential users are encouraged to evaluate Universal Algo within the context of their overall trading approach and objectives.

NASDAQ 100 Peak Hours StrategyNASDAQ 100 Peak Hours Trading Strategy

Description

Our NASDAQ 100 Peak Hours Trading Strategy leverages a carefully designed algorithm to trade within specific hours of high market activity, particularly focusing on the first two hours of the trading session from 09:30 AM to 11:30 AM GMT-5. This period is identified for its increased volatility and liquidity, offering numerous trading opportunities.

The strategy incorporates a blend of technical indicators to identify entry and exit points for both long and short positions. These indicators include:

Exponential Moving Averages (EMAs) : A short-term 9-period EMA and a longer-term 21-period EMA to determine the market trend and momentum.

Relative Strength Index (RSI) : A 14-period RSI to gauge the market's momentum.

Average True Range (ATR) : A 14-period ATR to assess market volatility and to set dynamic stop losses and trailing stops.

Volume Weighted Average Price (VWAP) : To identify the market's average price weighted by volume, serving as a benchmark for the trading day.

Our strategy uniquely applies a volatility filter using the ATR, ensuring trades are only executed in conditions that favor our setup. Additionally, we consider the direction of the EMAs to confirm the market's trend before entering trades.

Originality and Usefulness

This strategy stands out by combining these indicators within the NASDAQ 100's peak hours, exploiting the specific market conditions that prevail during these times. The inclusion of a volatility filter and dynamic stop-loss mechanisms based on the ATR provides a robust method for managing risk.