CNTLibraryLibrary "CNTLibrary"

Custom Functions To Help Code In Pinescript V5

Coded By Christian Nataliano

First Coded In 10/06/2023

Last Edited In 22/06/2023

Huge Shout Out To © ZenAndTheArtOfTrading and his ZenLibrary V5, Some Of The Custom Functions Were Heavily Inspired By Matt's Work & His Pine Script Mastery Course

Another Shout Out To The TradingView's Team Library ta V5

//====================================================================================================================================================

// Custom Indicator Functions

//====================================================================================================================================================

GetKAMA(KAMA_lenght, Fast_KAMA, Slow_KAMA)

Calculates An Adaptive Moving Average Based On Perry J Kaufman's Calculations

Parameters:

KAMA_lenght (int) : Is The KAMA Lenght

Fast_KAMA (int) : Is The KAMA's Fastes Moving Average

Slow_KAMA (int) : Is The KAMA's Slowest Moving Average

Returns: Float Of The KAMA's Current Calculations

GetMovingAverage(Source, Lenght, Type)

Get Custom Moving Averages Values

Parameters:

Source (float) : Of The Moving Average, Defval = close

Lenght (simple int) : Of The Moving Average, Defval = 50

Type (string) : Of The Moving Average, Defval = Exponential Moving Average

Returns: The Moving Average Calculation Based On Its Given Source, Lenght & Calculation Type (Please Call Function On Global Scope)

GetDecimals()

Calculates how many decimals are on the quote price of the current market © ZenAndTheArtOfTrading

Returns: The current decimal places on the market quote price

Truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places © ZenAndTheArtOfTrading

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

ToWhole(number)

Converts pips into whole numbers © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

ToPips(number)

Converts whole numbers back into pips © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

GetPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period © ZenAndTheArtOfTrading

Parameters:

value1 (float)

value2 (float)

lookback (int)

BarsAboveMA(lookback, ma)

Counts how many candles are above the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

BarsBelowMA(lookback, ma)

Counts how many candles are below the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

BarsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

GetPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count) © ZenAndTheArtOfTrading

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

GetSwingHigh(Lookback, SwingType)

Check If Price Has Made A Recent Swing High

Parameters:

Lookback (int) : Is For The Swing High Lookback Period, Defval = 7

SwingType (int) : Is For The Swing High Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing High

GetSwingLow(Lookback, SwingType)

Check If Price Has Made A Recent Swing Low

Parameters:

Lookback (int) : Is For The Swing Low Lookback Period, Defval = 7

SwingType (int) : Is For The Swing Low Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing Low

//====================================================================================================================================================

// Custom Risk Management Functions

//====================================================================================================================================================

CalculateStopLossLevel(OrderType, Entry, StopLoss)

Calculate StopLoss Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLoss (float) : Is The Custom StopLoss Distance, Defval = 2x ATR Below Close

Returns: Float - The StopLoss Level In Actual Price As A

CalculateStopLossDistance(OrderType, Entry, StopLoss)

Calculate StopLoss Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

StopLoss (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The StopLoss Value In Pips

CalculateTakeProfitLevel(OrderType, Entry, StopLossDistance, RiskReward)

Calculate TakeProfit Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLossDistance (float)

RiskReward (float)

Returns: Float - The TakeProfit Level In Actual Price

CalculateTakeProfitDistance(OrderType, Entry, TakeProfit)

Get TakeProfit Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

TakeProfit (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The TakeProfit Value In Pips

CalculateConversionCurrency(AccountCurrency, SymbolCurrency, BaseCurrency)

Get The Conversion Currecny Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

AccountCurrency (simple string) : Is For The Account Currency Used

SymbolCurrency (simple string) : Is For The Current Symbol Currency (Front Symbol)

BaseCurrency (simple string) : Is For The Current Symbol Base Currency (Back Symbol)

Returns: Tuple Of A Bollean (Convert The Currency ?) And A String (Converted Currency)

CalculateConversionRate(ConvertCurrency, ConversionRate)

Get The Conversion Rate Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

ConvertCurrency (bool) : Is To Check If The Current Symbol Needs To Be Converted Or Not

ConversionRate (float) : Is The Quoted Price Of The Conversion Currency (Input The request.security Function Here)

Returns: Float Price Of Conversion Rate (If In The Same Currency Than Return Value Will Be 1.0)

LotSize(LotSizeSimple, Balance, Risk, SLDistance, ConversionRate)

Get Current Lot Size

Parameters:

LotSizeSimple (bool) : Is To Toggle Lot Sizing Calculation (Simple Is Good Enough For Stocks & Crypto, Whilst Complex Is For Forex)

Balance (float) : Is For The Current Account Balance To Calculate The Lot Sizing Based Off

Risk (float) : Is For The Current Risk Per Trade To Calculate The Lot Sizing Based Off

SLDistance (float) : Is The Current Position StopLoss Distance From Its Entry Price

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - Position Size In Units

ToLots(Units)

Converts Units To Lots

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots

ToUnits(Lots)

Converts Lots To Units

Parameters:

Lots (float) : Is For How Many Lots Need To Be Converted Into Units (Minimun 0.01 Units)

Returns: Int - Position Size In Units

ToLotsInUnits(Units)

Converts Units To Lots Than Back To Units

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots That Were Rounded To Units

ATRTrail(OrderType, SourceType, ATRPeriod, ATRMultiplyer, SwingLookback)

Calculate ATR Trailing Stop

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

SourceType (int) : Is To Determine Where To Calculate The ATR Trailing From, Defval = close

ATRPeriod (simple int) : Is To Change Its ATR Period, Defval = 20

ATRMultiplyer (float) : Is To Change Its ATR Trailing Distance, Defval = 1

SwingLookback (int) : Is To Change Its Swing HiLo Lookback (Only From Source Type 5), Defval = 7

Returns: Float - Number Of The Current ATR Trailing

DangerZone(WinRate, AvgRRR, Filter)

Calculate Danger Zone Of A Given Strategy

Parameters:

WinRate (float) : Is The Strategy WinRate

AvgRRR (float) : Is The Strategy Avg RRR

Filter (float) : Is The Minimum Profit It Needs To Be Out Of BE Zone, Defval = 3

Returns: Int - Value, 1 If Out Of Danger Zone, 0 If BE, -1 If In Danger Zone

IsQuestionableTrades(TradeTP, TradeSL)

Checks For Questionable Trades (Which Are Trades That Its TP & SL Level Got Hit At The Same Candle)

Parameters:

TradeTP (float) : Is The Trade In Question Take Profit Level

TradeSL (float) : Is The Trade In Question Stop Loss Level

Returns: Bool - True If The Last Trade Was A "Questionable Trade"

//====================================================================================================================================================

// Custom Strategy Functions

//====================================================================================================================================================

OpenLong(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Long Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Long"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Long Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

OpenShort(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Short Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Short"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Short Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

TP_SLExit(FromID, TPLevel, SLLevel, PercentageClose, Comment, CommentValue)

Exits Based On Predetermined TP & SL Levels

Parameters:

FromID (string) : Is The Trade ID That The TP & SL Levels Be Palced

TPLevel (float) : Is The Take Profit Level

SLLevel (float) : Is The StopLoss Level

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

CloseLong(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Long Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Long"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

CloseShort(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Short Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Short"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

BrokerCheck(Broker)

Checks Traded Broker With Current Loaded Chart Broker

Parameters:

Broker (string) : Is The Current Broker That Is Traded

Returns: Bool - True If Current Traded Broker Is Same As Loaded Chart Broker

OpenPC(LicenseID, OrderType, UseLimit, LimitPrice, SymbolPrefix, Symbol, SymbolSuffix, Risk, SL, TP, OrderComment, Spread)

Compiles Given Parameters Into An Alert String Format To Open Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Open

UseLimit (bool) : Is If We Want To Enter The Position At Exactly The Previous Closing Price

LimitPrice (float) : Is The Limit Price Of The Trade (Only For Pending Orders)

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Risk (float) : Is The Trade Risk Per Trade / Fixed Lot Sizing

SL (float) : Is The Trade SL In Price / In Pips

TP (float) : Is The Trade TP In Price / In Pips

OrderComment (string) : Is The Executed Trade Comment

Spread (float) : is The Maximum Spread For Execution

Returns: String - Pine Connector Order Syntax Alert Message

ClosePC(LicenseID, OrderType, SymbolPrefix, Symbol, SymbolSuffix)

Compiles Given Parameters Into An Alert String Format To Close Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Close

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Returns: String - Pine Connector Order Syntax Alert Message

//====================================================================================================================================================

// Custom Backtesting Calculation Functions

//====================================================================================================================================================

CalculatePNL(EntryPrice, ExitPrice, LotSize, ConversionRate)

Calculates Trade PNL Based On Entry, Eixt & Lot Size

Parameters:

EntryPrice (float) : Is The Trade Entry

ExitPrice (float) : Is The Trade Exit

LotSize (float) : Is The Trade Sizing

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - The Current Trade PNL

UpdateBalance(PrevBalance, PNL)

Updates The Previous Ginve Balance To The Next PNL

Parameters:

PrevBalance (float) : Is The Previous Balance To Be Updated

PNL (float) : Is The Current Trade PNL To Be Added

Returns: Float - The Current Updated PNL

CalculateSlpComm(PNL, MaxRate)

Calculates Random Slippage & Commisions Fees Based On The Parameters

Parameters:

PNL (float) : Is The Current Trade PNL

MaxRate (float) : Is The Upper Limit (In Percentage) Of The Randomized Fee

Returns: Float - A Percentage Fee Of The Current Trade PNL

UpdateDD(MaxBalance, Balance)

Calculates & Updates The DD Based On Its Given Parameters

Parameters:

MaxBalance (float) : Is The Maximum Balance Ever Recorded

Balance (float) : Is The Current Account Balance

Returns: Float - The Current Strategy DD

CalculateWR(TotalTrades, LongID, ShortID)

Calculate The Total, Long & Short Trades Win Rate

Parameters:

TotalTrades (int) : Are The Current Total Trades That The Strategy Has Taken

LongID (string) : Is The Order ID Of The Long Trades Of The Strategy

ShortID (string) : Is The Order ID Of The Short Trades Of The Strategy

Returns: Tuple Of Long WR%, Short WR%, Total WR%, Total Winning Trades, Total Losing Trades, Total Long Trades & Total Short Trades

CalculateAvgRRR(WinTrades, LossTrades)

Calculates The Overall Strategy Avg Risk Reward Ratio

Parameters:

WinTrades (int) : Are The Strategy Winning Trades

LossTrades (int) : Are The Strategy Losing Trades

Returns: Float - The Average RRR Values

CAGR(StartTime, StartPrice, EndTime, EndPrice)

Calculates The CAGR Over The Given Time Period © TradingView

Parameters:

StartTime (int) : Is The Starting Time Of The Calculation

StartPrice (float) : Is The Starting Price Of The Calculation

EndTime (int) : Is The Ending Time Of The Calculation

EndPrice (float) : Is The Ending Price Of The Calculation

Returns: Float - The CAGR Values

//====================================================================================================================================================

// Custom Plot Functions

//====================================================================================================================================================

EditLabels(LabelID, X1, Y1, Text, Color, TextColor, EditCondition, DeleteCondition)

Edit / Delete Labels

Parameters:

LabelID (label) : Is The ID Of The Selected Label

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

Text (string) : Is The Text Than Wants To Be Written In The Label

Color (color) : Is The Color Value Change Of The Label Text

TextColor (color)

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

EditLine(LineID, X1, Y1, X2, Y2, Color, EditCondition, DeleteCondition)

Edit / Delete Lines

Parameters:

LineID (line) : Is The ID Of The Selected Line

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

X2 (int) : Is The X2 Coordinate IN BARINDEX Xloc

Y2 (float) : Is The Y2 Coordinate IN PRICE Yloc

Color (color) : Is The Color Value Change Of The Line

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

//====================================================================================================================================================

// Custom Display Functions (Using Tables)

//====================================================================================================================================================

FillTable(TableID, Column, Row, Title, Value, BgColor, TextColor, ToolTip)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

Column (int) : Is The Current Column Of The Table That Wants To Be Edited

Row (int) : Is The Current Row Of The Table That Wants To Be Edited

Title (string) : Is The String Title Of The Current Cell Table

Value (string) : Is The String Value Of The Current Cell Table

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

ToolTip (string) : Is The ToolTip Of The Current Cell In The Table

Returns: Void

DisplayBTResults(TableID, BgColor, TextColor, StartingBalance, Balance, DollarReturn, TotalPips, MaxDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

StartingBalance (float) : Is The Account Starting Balance

Balance (float)

DollarReturn (float) : Is The Account Dollar Reture

TotalPips (float) : Is The Total Pips Gained / loss

MaxDD (float) : Is The Maximum Drawdown Over The Backtesting Period

Returns: Void

DisplayBTResultsV2(TableID, BgColor, TextColor, TotalWR, QTCount, LongWR, ShortWR, InitialCapital, CumProfit, CumFee, AvgRRR, MaxDD, CAGR, MeanDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

TotalWR (float) : Is The Strategy Total WR In %

QTCount (int) : Is The Strategy Questionable Trades Count

LongWR (float) : Is The Strategy Total WR In %

ShortWR (float) : Is The Strategy Total WR In %

InitialCapital (float) : Is The Strategy Initial Starting Capital

CumProfit (float) : Is The Strategy Ending Cumulative Profit

CumFee (float) : Is The Strategy Ending Cumulative Fee (Based On Randomized Fee Assumptions)

AvgRRR (float) : Is The Strategy Average Risk Reward Ratio

MaxDD (float) : Is The Strategy Maximum DrawDown In Its Backtesting Period

CAGR (float) : Is The Strategy Compounded Average GRowth In %

MeanDD (float) : Is The Strategy Mean / Average Drawdown In The Backtesting Period

Returns: Void

//====================================================================================================================================================

// Custom Pattern Detection Functions

//====================================================================================================================================================

BullFib(priceLow, priceHigh, fibRatio)

Calculates A Bullish Fibonacci Value (From Swing Low To High) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

BearFib(priceLow, priceHigh, fibRatio)

Calculates A Bearish Fibonacci Value (From Swing High To Low) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

GetBodySize()

Gets The Current Candle Body Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN POINTS

GetTopWickSize()

Gets The Current Candle Top Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Top Wick Size IN POINTS

GetBottomWickSize()

Gets The Current Candle Bottom Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Bottom Wick Size IN POINTS

GetBodyPercent()

Gets The Current Candle Body Size As A Percentage Of Its Entire Size Including Its Wicks © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN PERCENTAGE

GetTopWickPercent()

Gets The Current Top Wick Size As A Percentage Of Its Entire Body Size

Returns: Float - The Current Candle Top Wick Size IN PERCENTAGE

GetBottomWickPercent()

Gets The Current Bottom Wick Size As A Percentage Of Its Entire Bodu Size

Returns: Float - The Current Candle Bottom Size IN PERCENTAGE

BullishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Engulfing Candle

BearishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bearish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Engulfing Candle

Hammer(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Star(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Doji(MaxWickSize, MaxBodySize, DojiType, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Doji Candle

Parameters:

MaxWickSize (float) : To Specify The Maximum Lenght Of Its Upper & Lower Wick, Defval = 2

MaxBodySize (float) : To Specify The Maximum Lenght Of Its Candle Body IN PERCENT, Defval = 0.05

DojiType (int)

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Doji Candle

BullishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Harami Candle

BearishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Harami Candle

//====================================================================================================================================================

// Custom Time Functions

//====================================================================================================================================================

BarInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls within the given time session

BarOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls outside the given time session

DateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range © ZenAndTheArtOfTrading

Parameters:

startTime (int)

endTime (int)

Returns: A boolean - true if the current bar falls within the given dates

DayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze © ZenAndTheArtOfTrading

Parameters:

monday (bool)

tuesday (bool)

wednesday (bool)

thursday (bool)

friday (bool)

saturday (bool)

sunday (bool)

Returns: A boolean - true if the current bar's day is one of the given days

AUSSess()

Checks If The Current Australian Forex Session In Running

Returns: Bool - True If Currently The Australian Session Is Running

ASIASess()

Checks If The Current Asian Forex Session In Running

Returns: Bool - True If Currently The Asian Session Is Running

EURSess()

Checks If The Current European Forex Session In Running

Returns: Bool - True If Currently The European Session Is Running

USSess()

Checks If The Current US Forex Session In Running

Returns: Bool - True If Currently The US Session Is Running

UNIXToDate(Time, ConversionType, TimeZone)

Converts UNIX Time To Datetime

Parameters:

Time (int) : Is The UNIX Time Input

ConversionType (int) : Is The Datetime Output Format, Defval = DD-MM-YYYY

TimeZone (string) : Is To Convert The Outputed Datetime Into The Specified Time Zone, Defval = Exchange Time Zone

Returns: String - String Of Datetime

在腳本中搜尋"the strat"

Trailing Stop with RSI - Momentum-Based StrategyTrailing Stop with RSI - Momentum-Based Strategy

Description:

The Trailing Stop with RSI strategy combines momentum analysis and trailing stop functionality to help traders identify potential entry and exit points in their trading decisions. This strategy is suitable for various markets and timeframes.

Key Features:

Momentum Analysis: The strategy incorporates momentum indicators to identify potential buying and selling opportunities based on momentum shifts in the price.

Trailing Stop Functionality: The strategy utilizes a trailing stop to protect profits and dynamically adjust the stop loss level as the trade moves in the desired direction.

RSI Confirmation: The Relative Strength Index (RSI) is included to provide additional confirmation for trade entries by considering overbought and oversold conditions.

How to Use:

Entry Conditions: Long positions are triggered when positive momentum is detected, and the RSI confirms an oversold condition. Short positions are triggered when negative momentum is detected, and the RSI confirms an overbought condition.

Trailing Stop Activation: Once a position is opened, the trailing stop is activated when the specified profit level (as a percentage) is reached.

Trailing Stop Level: The trailing stop maintains a stop loss level at a specified distance (as a percentage) from the highest profit achieved since opening the position.

Exit Conditions: The trailing stop will trigger an exit and close all positions when the trailing stop level is breached.

Markets and Conditions:

This strategy can be applied to various markets, including stocks, forex, cryptocurrencies, and commodities. It can be used in trending and ranging market conditions, making it versatile for different market environments.

Important Considerations:

Adjust Parameters: Traders can modify the length of the momentum and RSI indicators to suit their preferred timeframe and trading style.

Risk Management: It is recommended to consider appropriate position sizing, risk-to-reward ratios, and overall risk management practices when using this strategy.

Backtesting and Optimization: Traders are encouraged to backtest the strategy on historical data and optimize the parameters to find the best settings for their chosen market and timeframe.

By incorporating momentum analysis, trailing stop functionality, and RSI confirmation, this strategy aims to provide traders with a systematic approach to capturing profitable trades while managing risk effectively.

The Z-score The Z-score, also known as the standard score, is a statistical measurement that describes a value's relationship to the mean of a group of values. It's measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean.

The concept of Z-score was introduced by statistician Carl Friedrich Gauss as part of his "method of the least squares," which was an important step in the development of the normal distribution and Z-score tables. It's a key concept in statistics and is used in various statistical tests.

In financial analysis, Z-scores are used to determine whether a data point is usual or unusual. You can think of it as a measure of how many standard deviations an element is from the mean. For instance, a Z-score of 1.0 would denote a value that is one standard deviation from the mean. Z-scores are also used to predict probabilities, with Z-scores having a distribution that is expected to be normal.

In trading, a Z-score is used to determine how often a trading system may produce a string of winners or losers. It can help a trader to understand whether the losses or profits they see are something that the system would most likely produce, or if it's a once in a blue moon situation. This helps traders make decisions about when to start or stop a system.

I just wanted to play a bit with the Z-score I guess.

Feel free to share your findings if you discover additional applications for this strategy or identify timeframes where it appears to perform more optimally.

How it works:

This strategy is based on a statistical concept called Z-score, which measures the number of standard deviations a data point is from the mean. In other words, it helps determine how unusual or usual a data point is.

In the context of this strategy, Z-score is applied to a 10-period EMA (Exponential Moving Average) of Heikin-Ashi candlestick close prices. The Z-score is calculated over a look-back period of 25 bars.

The EMA of the Z-score is then calculated over a 20-bar period, and the upper and lower thresholds (bounds for buy and sell signals) are defined using the 90th and 10th percentiles of this EMA score.

Long positions are taken when the Z-score crosses above the lower threshold or crosses above the mid-line (50th percentile). An additional long entry is made when the Z-score crosses above the highest value the EMA has been in the past 100 periods.

Short positions are initiated when the EMA crosses below the upper threshold, lower threshold or the highest value the EMA has been in the past 100 periods.

Positions are closed when opposing entry conditions are met, for example, a long position is closed when the short entry condition is true, and vice versa.

Set your desired start date for the strategy. This can be modified in the timestamp("YYYY MM DD") function at the top of the script.

Williams %R Strategy

The Williams %R Strategy is a trading approach that is based on the Williams Percent Range indicator, available on the TradingView platform.

This strategy aims to identify potential overbought and oversold conditions in the market, providing clear buy and sell signals for entry and exit.

The strategy utilizes the Williams %R indicator, which measures the momentum of the market by comparing the current close price with the highest high and lowest low over a specified period. When the Williams %R crosses above the oversold level, a buy signal is generated, indicating a potential upward price movement. Conversely, when the indicator crosses below the overbought level, a sell signal is generated, suggesting a possible downward price movement.

Position management is straightforward with this strategy. Upon receiving a buy signal, a long position is initiated, and the position is closed when a sell signal is generated. This strategy allows traders to capture potential price reversals and take advantage of short-term market movements.

To manage risk, it is recommended to adjust the position size based on the available capital. In this strategy, the position size is set to 10% of the initial capital, ensuring proper risk allocation and capital preservation.

It is important to note that the Williams %R Strategy should be used in conjunction with other technical analysis tools and risk management techniques. Backtesting and paper trading can help evaluate the strategy's performance and fine-tune the parameters before deploying it with real funds.

Remember, trading involves risks, and past performance is not indicative of future results. It is always advised to do thorough research, seek professional advice, and carefully consider your financial goals and risk tolerance before making any investment decisions.

HK Percentile Interpolation One

This script is designed to execute a trading strategy based on Heikin Ashi candlesticks, moving averages, and percentile levels.

Please note that you should keep your original chart in normal candlestick mode and not switch it to Heikin Ashi mode. The script itself calculates Heikin Ashi values from regular candlesticks. If your chart is already in Heikin Ashi mode, the script would be calculating Heikin Ashi values based on Heikin Ashi values, which would produce incorrect results.

The strategy begins trading from a start date that you can specify by modifying the `startDate` parameter. The format of the date is "YYYY MM DD". So, for example, to start the strategy from January 1, 2022, you would set `startDate = timestamp("2022 01 01")`.

The script uses Heikin Ashi candlesticks, which are plotted in the chart. This approach can be useful for spotting trends and reversals more easily than with regular candlestick charts. This is particularly useful when backtesting in TradingView's "Rewind" mode, as you can see how the Heikin Ashi candles behaved at each step of the strategy.

Buy and sell signals are generated based on two factors:

1. The crossing over or under of the Heikin Ashi close price and the 75th percentile price level.

2. The Heikin Ashi close price being above certain moving averages.

You have the flexibility to adjust several parameters in the script, including:

1. The stop loss and trailing stop percentages (`stopLossPercentage` and `trailStopPercentage`). These parameters allow the strategy to exit trades if the price moves against you by a certain percentage.

2. The lookback period (`lookback`) used to calculate percentile levels. This determines the range of past bars used in the percentile calculation.

3. The lengths of the two moving averages (`yellowLine_length` and `purplLine_length`). These determine how sensitive the moving averages are to recent price changes.

4. The minimum holding period (`holdPeriod`). This sets the minimum number of bars that a trade must be kept open before it can be closed.

Please adjust these parameters according to your trading preferences and risk tolerance. Happy trading!

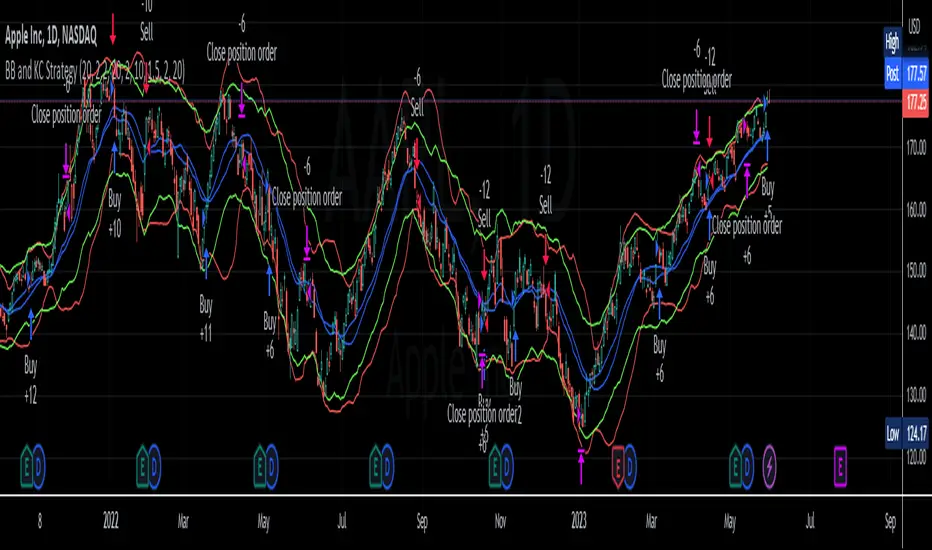

BB and KC StrategyThis script is designed as a TradingView strategy that uses Bollinger Bands (BB) and Keltner Channels (KC) as the primary indicators for generating trade signals. It aims to catch potential market trends by comparing the movements of these two popular volatility measures.

Key aspects of this strategy:

1. **Bollinger Bands and Keltner Channels:** Both are volatility-based indicators. The Bollinger Bands consist of a middle band (simple moving average) and two outer bands calculated based on standard deviation, which adjusts itself to market conditions. Keltner Channels are a set of bands placed above and below an exponential moving average of the price. The distance between the bands is calculated based on the Average True Range (ATR), a measure of price volatility.

2. **Entry Signals:** The strategy enters a long position when the upper KC line crosses above the upper BB line and the volume is above its moving average. Conversely, it enters a short position when the lower KC line crosses below the lower BB line and the volume is above its moving average.

3. **Exit Signals:** The strategy exits a position under two conditions. First, if the trade has been open for a certain number of bars defined by the user (default 20 bars). Second, a stop loss and trailing stop are in place to limit potential losses and lock in profits as the price moves favorably. The stop loss is set at a percentage of the entry price (default 1.5% for long and -1.5% for short), and the trailing stop is also a percentage of the entry price (default 2%).

4. **Trade Quantity:** The script allows specifying the investment amount for each trade, set to a default of 1000 currency units.

Remember, this is a strategy script, which means it is used for backtesting and not for real-time signals or live trading. It is also recommended that it is used as a tool to aid your trading, not as a standalone system. As with any strategy, it should be tested over different market conditions and used in conjunction with other aspects of technical and fundamental analysis to ensure robustness and effectiveness.

Initial Balance Panel Strategy for BitcoinInitial Balance Strategy

Initial Balance Strategy uses a source code of "Initial Balance Monitoring Panel" that build from "Initial Balance Markets Time Zones - Overall Highest and Lowest".

Initial Balance is based on the highest and lowest price action within the first 60 minutes of trading. Reading online this can depict which way the market can trend for the session. More information about Initial Balance Panel you can read at the end of the article.

Strategy idea

The main idea is to catch the trend move when most of the 16 Crypto pairs break the Low or High levels together. I found good results when 15 of 16 pairs is break that levels and after we manage the trade within some trail stop indicator, I choose Volatility Stop for this strategy.

Additional Strategy idea

The second one idea that was not made is to catch the pullback after fully green/red zones in Initial Balance Panel become white. That mean the main trend can be finished and we can try to catch good pullback in opposite direction.

Binance Crypto pairs

The strategy use the 16 default Crypto currencies pairs from the Binance. As additional variations of the strategy can be changing the currencies pairs and their number.

List of default pairs:

BINANCE:BTCUSDT, BINANCE:ETHUSDT, BINANCE:EOSUSDT, BINANCE:LTCUSDT, BINANCE:XRPUSDT, BINANCE:DASHUSDT, BINANCE:IOTAUSDT, BINANCE:NEOUSDT, BINANCE:QTUMUSDT, BINANCE:XMRUSDT, BINANCE:ZECUSDT, BINANCE:ETCUSDT, BINANCE:ADAUSDT, BINANCE:XTZUSDT, BINANCE:LINKUSDT, BINANCE:DOTUSDT

Summary

The strategy works very well for a buy trades with settings 15 crypto pairs of 16 that follow the trend with breaking the long initial balance level.

Initial Balance Monitoring Panel

Allows you to have an instant view of 16 Crypto pairs within a monitoring panel, monitoring Initial Balance (Asia, London, New York Stock Exchanges).

The code can easily be changed to suit the crypto pairs you are trading.

The setup of my chart would also include this indicator and the "Initial Balance Markets Time Zones - Overall Highest and Lowest" (with all IBs enabled) as shown above.

Initial Balance is based on the highest and lowest price action within the first 60 minutes of trading. Reading online this can depict which way the market can trend for the session.

The indicator has been coded for Crypto (so other symbols may not work as expected).

Though Initial Balance is based off the first 60 minutes of the trading markets opening, but Crypto is 24/7, this indicator looks at how Asia, London and New York Stock Exchanges opening trading can affect Crypto price action.

Source: Initial Balance Monitoring Panel

Intraday Mean Reversion Money Performance indicatorThe diagram shows Money Performance when buying stocks for 10 000 at every buy signal from the Intraday Mean Reversion indicator.

The indicator is best used in combination with Intraday Mean Reversion Main Indicator

The rules for trading are: Buy on Open price if the Intraday Mean Reversion Main indicator gives a buy signal. Sell on the daily close price.

According to my knowledge it is not possible to create a PineScript strategy based on these rules, because the indicator is used on Day to Day graph. Therefore this indicator can be used to analyze Money performance of this strategy.

The lines show the performance of the Intraday Mean Reversion Strategy, based on the different levels in the strategy (from 0.5 Standard deviation to 1.1 standard deviation)

Using this indicator it is possible to find stocks that often reverse towards mean after open.

Use this strategy on stocks with high positive performance. Do not use on stocks with negative performance.

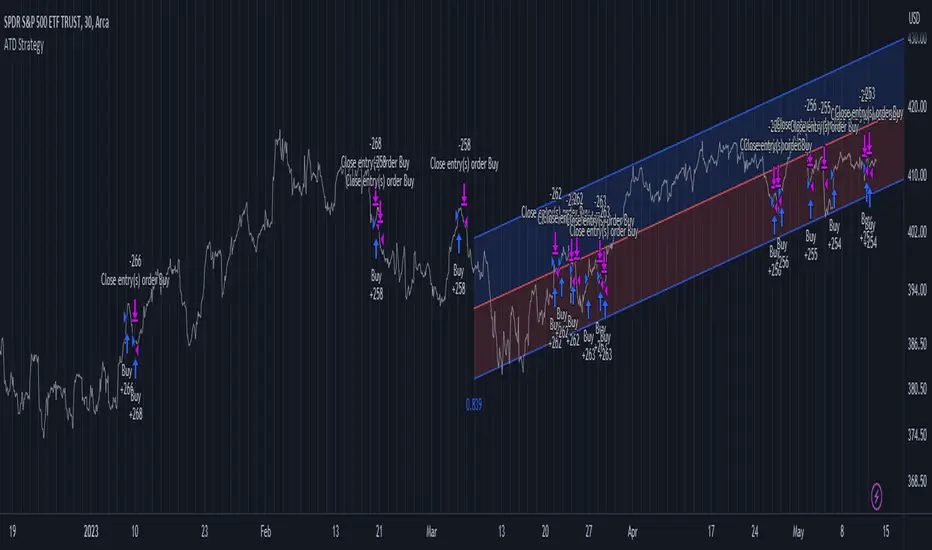

Advanced Trend Detection StrategyThe Advanced Trend Detection Strategy is a sophisticated trading algorithm based on the indicator "Percent Levels From Previous Close".

This strategy is based on calculating the Pearson's correlation coefficient of logarithmic-scale linear regression channels across a range of lengths from 50 to 1000. It then selects the highest value to determine the length for the channel used in the strategy, as well as for the computation of the Simple Moving Average (SMA) that is incorporated into the strategy.

In this methodology, a script is applied to an equity in which multiple length inputs are taken into consideration. For each of these lengths, the slope, average, and intercept are calculated using logarithmic values. Deviation, the Pearson's correlation coefficient, and upper and lower deviations are also computed for each length.

The strategy then selects the length with the highest Pearson's correlation coefficient. This selected length is used in the channel of the strategy and also for the calculation of the SMA. The chosen length is ultimately the one that best fits the logarithmic regression line, as indicated by the highest Pearson's correlation coefficient.

In short, this strategy leverages the power of Pearson's correlation coefficient in a logarithmic scale linear regression framework to identify optimal trend channels across a broad range of lengths, assisting traders in making more informed decisions.

RSI TrueLevel StrategyThis strategy is a momentum-based strategy that uses the Relative Strength Index (RSI) indicator and a TrueLevel envelope to generate trade signals.

The strategy uses user-defined input parameters to calculate TrueLevel envelopes for 14 different lengths. The TrueLevel envelope is a volatility-based technical indicator that consists of upper and lower bands. The upper band is calculated by adding a multiple of the standard deviation to a linear regression line of the price data, while the lower band is calculated by subtracting a multiple of the standard deviation from the same regression line.

The strategy generates long signals when the RSI crosses above the oversold level or when the price crosses above the selected lower band of the TrueLevel envelope. It generates short signals when the RSI crosses below the overbought level or when the price crosses below the selected upper band of the TrueLevel envelope.

The strategy allows for long and short trades and sets the trade size as a percentage of the account equity. The colors of the bands and fills are also customizable through user-defined input parameters.

In this strategy, the 12th TrueLevel band was chosen due to its ability to capture significant price movements while still providing a reasonable level of noise reduction. The strategy utilizes a total of 14 TrueLevel bands, each with varying lengths. The 12th band, with a length of 2646, strikes a balance between sensitivity to market changes and reducing false signals, making it a suitable choice for this strategy.

RSI Parameters:

In this strategy, the RSI overbought and oversold levels are set at 65 and 40, respectively. These values were chosen to filter out more noise in the market and focus on stronger trends. Traditional RSI overbought and oversold levels are set at 70 and 30, respectively. By raising the oversold level and lowering the overbought level, the strategy aims to identify more significant trend reversals and potential trade opportunities.

Of course, the parameters can be adjusted to suit individual preferences.

Net Unrealized Profit/Loss (NUPL)Indicator Overview

This indicator is derived from Market Value and Realized Value, which can be defined as:

Market Value: The current price of Bitcoin multiplied by the number of coins in circulation. This is like market cap in traditional markets i.e. share price multiplied by number of shares.

Realized Value: Rather than taking the current price of Bitcoin, Realized Value takes the price of each Bitcoin when it was last moved i.e. the last time it was sent from one wallet to another wallet. It then adds up all those individual prices and takes an average of them. It then multiplies that average price by the total number of coins in circulation.

By subtracting Realized Value from Market Value we calculate Unrealized Profit/Loss.

Unrealized Profit/Loss estimates the total paper profits/losses in Bitcoin held by investors. This is interesting to know but of greater value is identifying how this changes relatively over time.

To do this we can divide Unrealized Profit/Loss by Market Cap. This creates Net Unrealized Profit/Loss, sometimes referred to as NUPL, which is very useful to track investor sentiment over time for Bitcoin.

Relative Unrealised Profit/Loss is another name used for this analysis.

How To View The Chart

The key principle of this tool is in the ratio between market cap and Bitcoin investors taking profit.

When market cap rises much faster than profit taking we see that the market is overheating, one could say due to investor greed (red band). For the strategic investor such times have historically been favourable to take profit.

We can break down different percentages of Bitcoin Relative Unrealized Profit/Loss to determine what stage of the market we are in. This can be advantageous for the long term strategic investor.

Created By

Tamas Blummer, Tuur Demeester and Michiel Lescrauwaet

Double Supertrend Entry with ADX Filter and ATR Exits/EntriesThe Double Supertrend Entry with ADX Filter and ATR Exits/Entries indicator is a custom trading strategy designed to help traders identify potential buy and sell signals in trending markets. This indicator combines the strengths of multiple technical analysis tools, enhancing the effectiveness of the overall strategy.

Key features:

Two Supertrend Indicators - The indicator includes two Supertrend indicators with customizable parameters. These trend-following indicators calculate upper and lower trendlines based on the ATR and price. Buy signals are generated when the price crosses above both trendlines, and sell signals are generated when the price crosses below both trendlines.

ADX Filter - The Average Directional Index (ADX) is used to filter out weak trends and only generate buy/sell signals when the market exhibits a strong trend. The ADX measures the strength of the trend, and a customizable threshold level ensures that trades are only entered during strong trends.

ATR-based Exits and Entries - The indicator uses the Average True Range (ATR) to set profit target and stop-loss levels. ATR is a measure of market volatility, and these levels help traders determine when to exit a trade to secure profit or minimize loss.

Performance Statistics Table - A table is displayed on the chart, recording and showing the total number of winning trades, losing trades, percentage of profitable trades, average profit, and average loss. This information helps traders evaluate the performance of the strategy over time.

The Double Supertrend Entry with ADX Filter and ATR Exits/Entries indicator is a powerful trend-following strategy that can assist traders in making more informed decisions in the financial markets. By combining multiple technical analysis tools and providing performance statistics, this indicator helps traders improve their trading strategy and evaluate its success.

Range Filter x Hull SuiteRange Filter x Hull Suite

This indicator is a hybrid of two popular indicators, with a twist; namely the Range Filter (Guikroth version) and the Hull Suite (by Insilico) .

Originally developed as a 1 minute trend following strategy and traded during the New York Session for it's typically high volume / likely trending nature, it provides entry signals based on the following logic:

For bullish entry signals:

The first bullish* candle (*defined by the Range Filter bar color logic, blue by default - which is not necessarily technically a bullish candle as defined by the OHLC values) which appears after the consolidation candles (also defined by the Range Filter bar color logic, orange by default), and where the Hull Suite moving average is also bullish.

For bearish entry signals:

The first bearish* candle (*defined by the Range Filter bar color logic, red by default - which is not necessarily technically a bearish candle as defined by the OHLC values) which appears after the consolidation candles (also defined by the Range Filter bar color logic, orange by default), and where the Hull Suite moving average is also bearish.

The indicator aims to filter out signals where possible consolidation is occurring and comes with styling options and alternative filter options such as a triple moving average trend detection method. Signals can also be filtered by a specific trading session. Standard options for the Range Filter and Hull Suite settings are also able to be customised within the settings menu.

Alerts

Various alerts are built-in, including the custom entry signals unique to this strategy.

Note : The above features listed above are accurate at the time of publishing, but may be altered in future.

Many thanks to guikroth & Insilico for sharing their open source indicators, and also to the original developer of the strategy itself for sharing it.

Mean Reversion and TrendfollowingTitle: Mean Reversion and Trendfollowing

Introduction:

This script presents a hybrid trading strategy that combines mean reversion and trend following techniques. The strategy aims to capitalize on short-term price corrections during a downtrend (mean reversion) as well as ride the momentum of a trending market (trend following). It uses a 200-period Simple Moving Average (SMA) and a 2-period Relative Strength Index (RSI) to generate buy and sell signals.

Key Features:

Combines mean reversion and trend following techniques

Utilizes 200-period SMA and 2-period RSI

Customizable starting date

Allows for enabling/disabling mean reversion or trend following modes

Adjustable position sizing for trend following and mean reversion

Script Description:

The script implements a trading strategy that combines mean reversion and trend following techniques. Users can enable or disable either of these techniques through the input options. The strategy uses a 200-period Simple Moving Average (SMA) and a 2-period Relative Strength Index (RSI) to generate buy and sell signals.

The mean reversion mode is active when the price is below the SMA200, while the trend following mode is active when the price is above the SMA200. The script generates buy signals when the RSI is below 20 (oversold) in mean reversion mode or when the price is above the SMA200 in trend following mode. The script generates sell signals when the RSI is above 80 (overbought) in mean reversion mode or when the price falls below 95% of the SMA200 in trend following mode.

Users can adjust the position sizing for both trend following and mean reversion modes using the input options.

To use this script on TradingView, follow these steps:

Open TradingView and load your preferred chart.

Click on the 'Pine Editor' tab located at the bottom of the screen.

Paste the provided script into the Pine Editor.

Click 'Add to Chart' to apply the strategy to your chart.

Please note that the past performance of any trading system or methodology is not necessarily indicative of future results. Always use proper risk management and consult a financial advisor before making any investment decisions.

------

The following is a summary of the underlying whitepaper (onlinelibrary.wiley.com) for this strategy:

This paper proposes a theory of securities market under- and overreactions based on two psychological biases: investor overconfidence about the precision of private information and biased self-attribution, which causes asymmetric shifts in investors' confidence as a function of their investment outcomes. The authors show that overconfidence implies negative long-lag autocorrelations, excess volatility, and public-event-based return predictability. Biased self-attribution adds positive short-lag autocorrelations (momentum), short-run earnings "drift," and negative correlation between future returns and long-term past stock market and accounting performance.

The paper explains that there is empirical evidence challenging the traditional view that securities are rationally priced to reflect all publicly available information. Some of these anomalies include event-based return predictability, short-term momentum, long-term reversal, high volatility of asset prices relative to fundamentals, and short-run post-earnings announcement stock price "drift."

The authors argue that investor overconfidence can lead to stock prices overreacting to private information signals and underreacting to public signals. This overreaction-correction pattern is consistent with long-run negative autocorrelation in stock returns, excess volatility, and further implications for volatility conditional on the type of signal. The market's tendency to over- or underreact to different types of information allows the authors to address the pattern that average announcement date returns in virtually all event studies are of the same sign as the average post-event abnormal returns.

Biased self-attribution implies short-run momentum and long-term reversals in security prices. The dynamic analysis based on biased self-attribution can also lead to a lag-dependent response to corporate events. Cash flow or earnings surprises at first tend to reinforce confidence, causing a same-direction average stock price trend. Later reversal of overreaction can lead to an opposing stock price trend.

The paper concludes by summarizing the findings, relating the analysis to the literature on exogenous noise trading, and discussing issues related to the survival of overconfident traders in financial markets.

Cycle Position TradingTitle: Cycle Position Trading Strategy v1.0

Description: Cycle Position Trading Strategy is a simple yet effective trading strategy based on a 200-day Simple Moving Average (SMA). Users can select between two modes, "Buy Uptrend" and "Buy Downtrend," to customize the strategy according to their trading preferences. The strategy allows users to set their own stop loss (SL) and take profit (TP) levels, providing more flexibility and control over their trades.

Features:

Choose between two trading modes: "Buy Uptrend" and "Buy Downtrend."

Customize your stop loss (SL) and take profit (TP) levels.

Clear visual representation of the 200-day Simple Moving Average (SMA) on the chart.

How to use:

Add the strategy to your chart by searching for "Cycle Position Trading Strategy" in the TradingView "Indicators & Strategies" section.

Configure the strategy settings according to your preferences:

Select the trading mode from the dropdown menu. "Buy Uptrend" will open long positions when the closing price is above the 200-day SMA. "Buy Downtrend" will open long positions when the closing price is below the 200-day SMA.

Set your desired stop loss (SL) and take profit (TP) levels. The default values are 0.9 (10% below the entry price) for the stop loss and 1.1 (10% above the entry price) for the take profit.

Monitor the chart for trade signals based on the chosen mode and settings. The strategy will enter and exit trades automatically based on the selected mode and the configured stop loss and take profit levels.

Analyze the performance of the strategy by checking the TradingView strategy performance summary or by viewing individual trades in the "Trades" list.

Disclaimer: This strategy is intended for educational and illustrative purposes only. Use it at your own risk. Past performance is not indicative of future results. Trading stocks, cryptocurrencies, or any other financial instrument involves significant risk and may result in the loss of capital.

Version: v1.0

Release date: 2023-03-25

Author: I11L

License: Mozilla Public License 2.0 (mozilla.org)

I11L - Better Buy Low Volatility or High Volatility?This Pine Script code defines a TradingView strategy called "I11L - Better Buy Low Volatility or High Volatility?". The strategy aims to study the difference between buying when an asset's volatility is low and when it is high. It allows the user to select whether to buy during low or high volatility periods by changing the input variable mode.

Here's a brief explanation of the System:

The strategy is initialized with relevant settings such as overlay, pyramiding, default quantity type, initial capital, and others.

The mode input allows the user to choose between "Buy low Volatility" and "Buy high Volatility" options.

volatilityTargetRatio is the user-defined threshold to be used for making buy decisions. A value of 1 equals the average ATR (Average True Range) for the security. A lower value indicates lower volatility.

atrLength is the number of periods to calculate the ATR.

sellAfterNBarsLength sets the number of bars to hold the position before selling it.

The script calculates the ATR using the ta.atr() function, and then divides it by the closing price to normalize the value. It also calculates the simple moving average (SMA) of the normalized ATR over a period of 5 times the ATR length, and then computes the ratio between the normalized ATR and its average.

The script keeps track of the number of holding bars using the variable holdingBarsCounter. When there are open trades, the holding bars counter is incremented.

The decision to buy is made based on the selected mode and whether the computed ratio is above or below the user-defined threshold.

When the holding bars counter exceeds the user-defined limit, the position is closed.

The script plots the computed ratio with different colors based on the buy and close conditions. The ratio is plotted in green when a buy signal is triggered, red when a close signal is triggered, and white in all other cases. The value of 1 (the reference for the average ATR) is also plotted on the chart in white color.

This strategy helps traders study the difference between buying during low and high volatility periods and compare the performance of these conditions. It can be useful for analyzing the effectiveness of volatility-based trading strategies, such as entering positions when the market is calm or during periods of strong price movement.