Buffett Valuation Indicator [TradeDots]The Buffett Valuation Indicator (also known as the Buffett Index or Buffett Ratio) measures the ratio of the total United States stock market to GDP.

This indicator helps determine whether the valuation changes in US stocks are justified by the GDP level.

For example, the ratio is calculated based on the standard deviations from the historical trend line. If the value exceeds +2 standard deviations, it suggests that the stock market is overvalued relative to GDP, and vice versa.

This "Buffett Valuation Indicator" is an enhanced version of the original indicator. It applies a Bollinger Band over the Valuation/GDP ratio to identify overvaluation and undervaluation across different timeframes, making it efficient for use in smaller timeframes, e.g. daily or even hourly intervals.

HOW DOES IT WORK

The Buffett Valuation Indicator measures the ratio between US stock valuation and US GDP, evaluating whether stock valuations are overvalued or undervalued in GDP terms.

In this version, the total valuation of the US stock market is represented by considering the top 10 market capitalization stocks.

Users can customize this list to include other stocks for a more balanced valuation ratio. Alternatively, users may use S&P 500 ETFs, such as SPY or VOO, as inputs.

The ratio is plotted as a line chart in a separate panel below the main chart. A Bollinger Band with a default 100-period and multiples of 1 and 2 is used to identify overvaluation and undervaluation.

For instance, if the ratio line moves above the +2 standard deviation line, it indicates that stocks are overvalued, signaling a potential selling opportunity.

APPLICATION

When the indicator is applied to a chart, we observe the ratio line's movements relative to the standard deviation lines. The further the line deviates from the standard deviation lines, the more extreme the overvaluation or undervaluation.

We look for buying opportunities when the Buffett Index moves below the first and second standard deviation lines and sell opportunities when it moves above these lines. This indicator is used as a microeconomic confirmation tool, in combination with other indicators, to achieve higher win-rate setups.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

在腳本中搜尋"富国恒生港股通高股息低波动ETF发起式联接A+高股息低波动优势"

Growth TrendThis powerful indicator plots the number of growth stocks in an uptrend, providing a comprehensive view of the market's overall direction. By applying a simple moving average, users can quickly gauge the trend and make informed trading decisions.

How does it work?

The script pulls tickers from the S & P 500 Growth ETF. It then plots the number of stocks from the ETF that are trending above a medium-term Moving Average, signaling an uptrend.

A moving average is applied to help understand the trend.

The background is shaded when 3 or more consecutive days are above (green) or below (red) the moving average.

Key Features:

Visual Trend Identification: The indicator shades the background green when three or more consecutive days are above the moving average, indicating a strong uptrend. Conversely, it shades red when three consecutive days are below the moving average, signaling a downtrend.

Breakout Insights: By tracking the trend, traders can identify when breakouts in growth stocks are more likely to occur or fail. This helps traders time their entries and exits more effectively.

Trend Strength Assessment: The indicator provides a quick visual assessment of the trend's strength, enabling traders to adjust their strategies accordingly.

Why is this indicator helpful?

Improved Trading Decisions: By understanding the overall trend and strength of growth stocks, traders can make more informed decisions about when to buy or sell.

Enhanced Risk Management: The indicator helps traders identify potential trend reversals, enabling them to adjust their positions and manage risk more effectively.

Market Insights: The Growth Stock Trend Indicator provides a valuable perspective on the market's overall direction, helping traders stay ahead of the curve.

By incorporating this indicator into their trading strategy, traders can gain a competitive edge and make more informed decisions in the growth stock market.

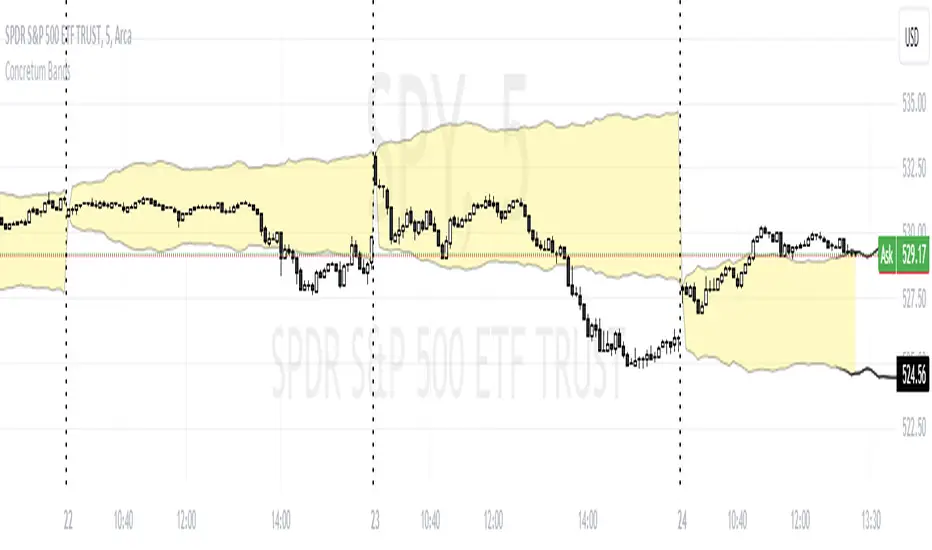

Concretum BandsDefinition

The Concretum Bands indicator recreates the Upper and Lower Bound of the Noise Area described in the paper "Beat the Market: An Effective Intraday Momentum Strategy for S&P500 ETF (SPY)" published by Concretum founder Zarattini, along with Barbon and Aziz, in May 2024.

Below we provide all the information required to understand how the indicator is calculated, the rationale behind it and how people can use it.

Idea Behind

The indicator aims to outline an intraday price region where the stock is expected to move without indicating any demand/supply imbalance. When the price crosses the boundaries of the Noise Area, it suggests a significant imbalance that may trigger an intraday trend.

How the Indicator is Calculated

The bands at time HH:MM are computed by taking the open price of day t and then adding/subtracting the average absolute move over the last n days from market open to minute HH:MM . The bands are also adjusted to account for overnight gaps. A volatility multiplier can be used to increase/decrease the width of the bands, similar to other well-known technical bands. The bands described in the paper were computed using a lookback period (length) of 14 days and a Volatility Multiplier of 1. Users can easily adjust these settings.

How to use the indicator

A trader may use this indicator to identify intraday moves that exceed the average move over the most recent period. A break outside the bands could be used as a signal of significant demand/supply imbalance.

Index investingThe Index Investing indicator simplifies decision-making for adding to Index ETF's Long-term investments. By utilizing a percentage discount methodology, it highlights potential opportunities to enhance portfolios. This straightforward tool aids in identifying favorable moments to invest based on calculated price discounts from selected reference points, making the process more systematic and less subjective.

🔶 SETTINGS

Reference Price: Choose between 'All-Time-High' or 'Start of the Year' as the basis for calculating discount levels. This allows for flexibility in strategy depending on market conditions or investment philosophy.

Discount 1 %, Discount 2 %, Discount 3 %: These inputs define the percentage below the reference price at which buy signals are generated. They represent strategic entry points at discounted prices.

🔶 Default Parameters

The default parameters of 4.13%, 8.26%, and 12.39% for the discount levels are chosen based on the average 5-year return of the NSE:NIFTY Index, which stands at approximately 12.39%. By dividing this return into three parts, we obtain a structured approach to capturing potential upside at varying levels of market retracement, providing a logical basis for the selected default values.

Users have the flexibility to modify these parameters, tailoring the indicator to fit their unique approach and market outlook.

🔶 How Levels Are Calculated

Discount levels are calculated using the formula: Discount Price = Reference Price * (1 - Discount %) . This succinct approach establishes specific entry points below the chosen reference, such as an all-time high or the year's start price.

🔶 How Are the Buy Labels Generated

Buy signals are generated when the market price(Low of the candle) crosses under any of the defined discount levels. Each level has a corresponding buy label ('Buy 1', 'Buy 2', 'Buy 3'), which is activated upon the price crossing below the specified discount level and is only reset at the beginning of a new year or upon reaching a new reference high, ensuring signals are not repetitive for the same price level.

🔶 Other Features

Alerts: The indicator provides alerts for each buy signal, notifying potential entry points at their defined discount levels. The alert triggers only once per candle.

Year Marker: A vertical line with an accompanying label marks the start of each trading year on the chart. This feature aids in visualizing the temporal context of buy signals and reference price adjustments.

PercenageDropFromATHINFO:

The PercenageDropFromATH script is fairly simple indicator, which is able to:

detect the last ATH (real ATH of the full chart, not related to the selected timeframe) and plot it

user can select a percentage of drop from this price, and once reached can receive a notification

Note that if the ATH is outside of the visibility of the currently selected timeframe the indicator will not be able to show it. Recommended settings is 1D TF!

DETAILS:

The purpose of the script is to serve to ease passive investments in ETFs and indices, once those are dropping below certain point from the ATH.

Individual stocks are not really recommended in my view, as unlike the indices which are cherry picking the best companies from the sector, individual companies can always start drifting away.

Anyway, the indicator should work on all assets, including crypto, gold, etc.

Example usage could be of setting an alert for 25% drop in SPY, and start accumulating positions on every next 10% additional drop, so DCA can be done with favorable prices.

SETTINGS

The settings are pretty straight forward:

ATH Source - source for computing the ATH, default to "high", but user can select to check only on open/close/low as well

Percentage drop target from ATH - self explaining, default to 20

ATH color - only the last ATH until the current bar is been drawn

Plot ATH drop target price - optionally the target price after the percentage drop can be plotted as well

ATH drop target color - the color of the price after the percentage drop from ATH

Variable Keltner Channel For DCAHello Everyone,

Sharing the indicator that I'm using for Dollar Cost Averaging into the stocks & ETFs in my portfolio.

Instead of entering regularly each month, entry only happens when the share price is below the indicator.

This indicator is based on Exponential Moving Average & Keltner Channel.

When 21 EMA is above 34 EMA, the line is 1 ATR below the 21 EMA. (green color)

When 21 EMA is below 34 EMA, the line is 2 ATR below the 21 EMA. (red color)

Exploring ways to refine this further, especially during sideways or transition to downtrend, do comment if you have any idea.

This strategy itself was based on SMA 50 strategy for DCA.

COSTAR [SS]This idea came to me after I wrote the post about Co-Integration and pair trading. I wondered if you could use pair trading principles as a way to determine overbought and oversold conditions in a more neutral way than RSI or Stochastics.

The results were promising and this indicator resulted :-)!

About:

COSTAR provides another, more neutral way to determine whether an equity is overbought or oversold.

Instead of relying on the traditional oscillator based ways, such as using RSI, Stochastics and MFI, which can be somewhat biased and narrow sided, COSTAR attempts to take a neutral, unbiased approached to determine overbought and oversold conditions. It does this through using a co-integrated partner, or "pair" that is closely linked to the underlying equity and succeeds on both having a high correlation and a high t-statistic on the ADF test. It then references this underlying, co-integrated partner as the "benchmark" for the co-integration relationship.

How this succeeds as being "unbiased" and "neutral" is because it is responsive to underlying drivers. If there is a market catalyst or just general bullish or bearish momentum in the market, the indicator will be referencing the integrated relationship between the two pairs and referencing that as a baseline. If there is a sustained rally on the integrated partner of the underlying ticker that is holding, but the other ticker is lagging, it will indicate that the other ticker is likely to be under-valued and thus "oversold" because it is underperforming its benchmark partner.

This is in contrast to traditional approaches to determining overbought and oversold conditions, which rely completely on a single ticker, with no external reference to other tickers and no control over whether the move could potentially be a fundamental move based on an industry or sector, or whether it is a fluke or a squeeze.

The control for this giving "false" signals comes from its extent of modelling and assessment of the degree of integration of the relationship. The parameters are set by default to assess over a 1 year period, both the correlation and the integration. Anything that passes this degree of integration is likely to have a solid, co-integrated state and not likely to be a "fluke". Thus, the reliability of the assessment is augmented by the degree of statistical significance found within the relationship. The indicator is not going to prompt you to rely on a relationship that is statistically weak, and will warn you of such.

The indicator will show you all the information you require regarding the relationship and whether it is reliable or not, so you do not need to worry!

How to Use

The first step to use COSTAR is identifying which ticker has a strong relationship with the current ticker. In the main chart, you will see that SPY is overlaid with VIX. There is a strong, negative correlation between the VIX and SPY. When VIX is entered as the paired ticker, the indicator returns the data as stationary, indicating a compatible match.

Now you have 3 ways of viewing this relationship, 2 of which are going to be directly applicable to trading.

You can view them as

Price to Price Ratio (Not very useful for trading, but if you are curious)

Z-Score: Helpful for trading

Co-integration: Helpful for trading

Here is an example of all three:

Example of Z-Score Chart:

Example of Price Ratio:

Example of Co-Integration Pair:

Using for Trading

As stated above, the two best ways to use this for trading is to either use the Z-Score Chart or the Co-Integrated Pair chart.

The Z-Score chart is based off of the price ratio data and provides an assessment of both the independent and dependent data.

The co-integration shows the dependent (the ticker you are trading) in yellow and the independent (the ticker you are referencing) in teal. When teal is above yellow, you will see it is green. This means, based on your benchmark pair, there is still more up room and the ticker you are trading is actually lagging behind.

When the yellow crosses up, it will turn red. This means that your ticker is out-performing the benchmark pair and you likely will see pullback and a "regression to the mean" through re-integration.

The indicator is capable of plotting out entries and exits, which are guided by the z-score:

How Effective is it?

I created a basic strategy in Pinescript, and the back-test results vary. Trading ES1! using NQ1! as the co-integrated pair, results were around 78% effective.

With VIX, results were around 50% effective, but with a net profit.

Generally, the efficacy surpassed that of both stochastics and RSI.

I will be releasing the strategy version of this in the coming days, still just cleaning up that code and making it more "public use" friendly.

Other Applications

If you are a pair trader, you can technically use this for pair trading as well. That's essentially all this is doing :-).

Tips

If you are trading a ticker such as MSFT, AMD, KO etc., it's best to try to find an ETF or index that has that particular ticker as a large holding and use that as your benchmark. You will see on the indicator whether there is a high correlation and whether the data is indeed stationary.

If the indicator returns "Non-stationary", you can attempt to extend your regression range from 252 to 500. If this fixes the issue, ensure that the correlation is still >= 0.5 or <= -0.5. If this does not work still, you will need to find another pair, as its likely the result of incompatibility and an insignificant relationship.

To help you identify tickers with strong relationships, consider using a correlation heatmap indicator. I have one available and I think there are a couple of other similar ish ones out there. You want to make sure the relationship is stable over time (a correlation of >= 0.50 or <= -0.5 over the past 252 to 500 days).

IMPORTANT: The long and short exits delete the signal after one is signaled. Therefore, when you look back in the chart you will notice there are no signals to exit long or short. That is because they signal as they happen. This is to keep the chart clean.

'Tis all my friends!

Hope you enjoy and let me know your questions and suggestions below!

Side note:

COSTAR stands for Co-integration Statistical Analysis and Regression. ;)

Expected Move by Option's Implied Volatility Symbols: EAT - GBDC

This script plots boxes to reflect weekly, monthly and yearly expected moves based on "At The Money" put and call option's implied volatility.

Symbols in range: This script will display Expected Move data for Symbols within the range of EAT-GDBC in alphabetical order.

Weekly Updates: Each weekend, the script is updated with fresh expected move data, a job that takes place every Saturday following the close of the markets on Friday.

In the provided script, several boxes are created and plotted on a price chart to represent the expected price moves for various timeframes.

These boxes serve as visual indicators to help traders and analysts understand the expected price volatility.

Definition of Expected Move: Expected Move refers to the anticipated range within which the price of an underlying asset is expected to move over a specific time frame, based on the current implied volatility of its options. Calculation: Expected Move is typically calculated by taking the current stock price and applying a multiple of the implied volatility. The most commonly used multiple is the one-standard-deviation move, which encompasses approximately 68% of potential price outcomes.

Example: Suppose a stock is trading at $100, and the implied volatility of its options is 20%. The one-standard-deviation expected move would be $100 * 0.20 = $20.

This suggests that there is a 68% probability that the stock's price will stay within a range of $80 to $120 over the specified time frame. Usage: Traders and investors use the expected move as a guideline for setting trading strategies and managing risk. It helps them gauge the potential price swings and make informed decisions about buying or selling options. There is a 68% chance that the underlying asset stock or ETF price will be within the boxed area at option expiry. The data on this script is updating weekly at the close of Friday, calculating the implied volatility for the week/month/year based on the "at the money" put and call options with the relevant expiry.

In summary, implied volatility reflects market expectations about future price volatility, especially in the context of options. Expected Move is a practical application of implied volatility, helping traders estimate the likely price range for an asset over a given period. Both concepts play a vital role in assessing risk and devising trading strategies in the options and stock markets.

SPDR TrackerMonitor all SPDR Index Funds in one location! The purpose of this indicator is to review which sectors are trend up vs down to better manage risk against SPY, other funds and/or individual stocks.

With this indicator it may become more apparent which sectors to begin investment in that are at lows compared to others, or use it to determine which stocks may be undervalued or overvalued against SPY.

There is a small table at the bottom where each fund symbol is presented along with it's mode value, last period change as well as last period volume - there's a tooltip that shows the description for each symbol for a quick reminder.

Review the configuration pane where:

Individual funds can have their visibility toggled

Change funds colors

Adjust display mode for each fund (SMA, EMA, VWMA, BBW, Change, ATR, VWAP - many more!)

Some presentation modes may look better on some timeframes vs others, adjust lengths and use anchor point for VWAP.

Future updates may bring about new features, I have some code organization and refactoring to do but wanted to share the idea anyways.

Feel free to drop any suggestions for feature enhancement and I hope it brings success to many, enjoy.

Seasonal Performance for Stocks & CryptoThe Seasonal Performance indicator quickly allows you to see if you are in a bullish or bearish time of year for an underlying security and where the current performance stacks up compared to the same time of year historically. Table is fully customizable from colors to what data to see.

Table Displays

Average Performance

Best Performance

Worst Performance

Last Performance

Current Performance

Note this indicator will only work with Stocks, ETF's, Index's or Crypto.

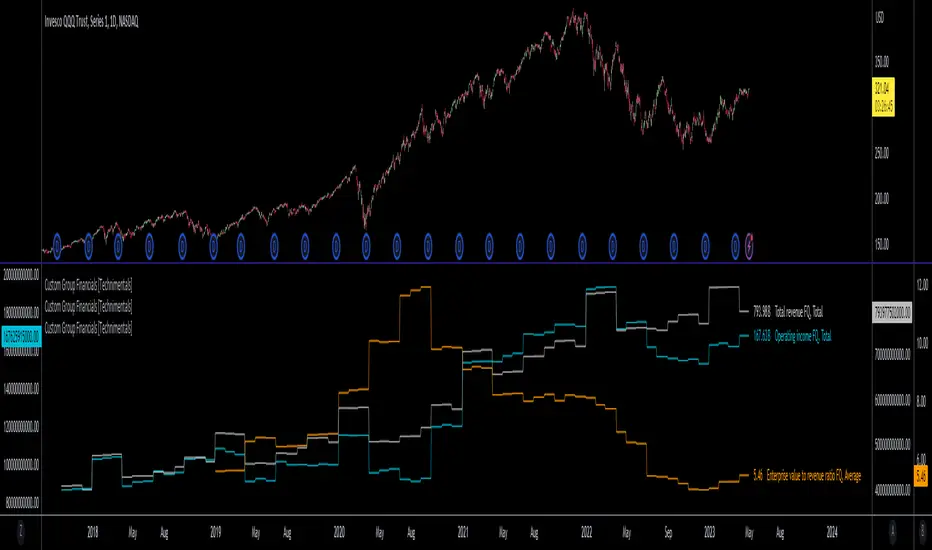

Custom Group Financials [Technimentals]This script allows the user to build custom groups and combine the same financial data from 40 different symbols simultaneously and plot it data as a total or as an average.

By default, the top 40 symbols in the QQQ are used. Between them they account for the majority of the index. This is a good workaround for the lack of ETF financial data in TradingView.

This functions much like any other financial indicator. You choose the financial data and period:

FY = Financial Year

FQ = Financial Quarter

TTM = Trailing Twelve Months

Bare in mind that some data only exists in FY data.

Thanks to @LucF for writing most of this code!

Enjoy!

ThiccZonesThis indicator is a formula that includes 4 different zones which are different sizes based on the ticker you decide to use. It was optimized for SPY and other market ETFs but works well for all stocks on the market. The formula puts a zone at the previous day's high and low, and the previous 5 day's high and low. These zones are meant to be used as support and resistance and can even overlap, creating a 'master zone'. This is different than other zone indicators because the formula for these zones is something I created myself and have been unable to find on here. I have had the most success using a 1-15 minute chart and using my zones for reversal areas. I often look for other indications of reversal as well that line up with the area of the zones. It can also be used on the break and retest of these zones. I have found that when a stock breaks one of these zones it will often retest and continue that trend.

XLY/XLP RatioThe XLY/XLP ratio is a financial indicator that measures the ratio between the two ETFs (Exchange Traded Funds) Consumer Discretionary Select Sector SPDR Fund (XLY) and Consumer Staples Select Sector SPDR Fund (XLP). This ratio is often used by traders and investors as a measure of the relative success of companies in the consumer goods and consumer services sectors.

A higher XLY/XLP ratio indicates that consumer confidence is higher and people are more willing to spend their money on non-essential items, such as entertainment or luxury goods (discretionary spending). A lower XLY/XLP ratio, on the other hand, indicates that consumer confidence is lower and people are more willing to spend their money on essential items like food and household items (staple spending).

The interpretation of the XLY/XLP ratio depends on the current market situation and the analysis of the economic and political factors that may influence consumption. If the XLY/XLP ratio rises, it could be an indication of a growing economy and increasing consumer sentiment. However, if it falls, it could be an indication of a weakening economy or declining consumer confidence.

It is important to note that the XLY/XLP indicator should not be used as the sole indicator to make trading decisions. It is advisable to also consider other indicators, such as technical and fundamental analysis, before making a decision.

SPX Fair Value Strategy UltimateThis is a strategy using the SPX Fair Value derived from Net Liquidity.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of SPX using Net Liquidity looks like this: net_liquidity/1000000000/1.1 -1625

The SPX Fair Value is then subtracted from the SPX value which creates an oscillating diff value.

When diff is greater than 350, SPX is considered overbought and we go short/sell.

When diff is less than -150, SPX is considered oversold and we cover/buy.

The net liquidity values I calculate outside of TradingView. If you'd like the strategy to work for future dates, you'll need to update them.

Paremeters:

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

Balance of Power Heikin Ashi Investing Strategy Balance of Power Heikin Ashi Investing Strategy

This is a swing strategy designed for investment help.

Its made around the Balace of Power indicator, but has been adapted on using the Monthly Heikin Ashi candle from the SPY asset in order to be used with correlation for US Stock/ETF/Index Markets.

The BOP acts as an oscilallator showing the power of a bull trend when its positive and a bearish trend when its in negative. At the same time we can spot reversals, based on the percentiles ( 99/1)

The rules for entry :

For long : The 99 percentile is ascending, and we are either in a positive value (>0), or we crossed the bottom place ( -0.35)

For short : the 99 and 1 percentile are descending, and we are either in a negative value(<0), or we crossed down the top place ( 0.6)

If you have any questions please let me know !

Stock Gaps SPY Correlation StrategyThis is daytrade stock strategy, designed to take the best out of the daily gaps that are forming between the close of previous day and opening of present day.

At the same time its logic has been adapted for SPY chart, in order to use correlation with the other stocks/assets/ etf which are linked with SP500 movement.

Lastly it has been added 2 new confirmation logics, based on the USI: advance/decline chart and percentage above vwap among all US stocks.

The rules for entry are simple :

We are at the opening daily candle, we have a long/short gap based on where the opening is happening and at the same time we are checking to see that the current different between the current difference between low and previous high (or viceversa) is higher than an established parameter(minimal deviation )

For exit, we exit based on time/clock parameter, in this case by default I selected 1h and half before close of the US session.

For testing purposes I have used 10% of the available capital, with a 0.0035$ comission per each share bought ( IBKR comissions)

If there are any questions, please let me know either here or in private !

TriautoETF(TQQQ) Short Strategy B1○ Objective.

This is a strategy for the TQQQ NASDAQ:TQQQ short strategy in the TriAuto ETF .

It is used as a hedging short rather than for profit-making purposes.

Entry and close points are indicated.

○ Strategy

The strategy is to hold a short position when the price falls below the moving average line, which is a market-conscious line that is rarely broken.

The close (settlement) is determined by using the moving average.

The moving average is based on the market-conscious QQQ NASDAQ:QQQ .

This script is used on the daily chart of the TQQQ.

It works as a hedge for long positions because open interest is held even at the major bottoms of the China and Corona shocks.

The system is set up to quickly cut its losses even if the moving average is "tricked" into falling below the moving average.

Morningstar Equity Style Box HeatmapStyle boxes are a classification scheme created by Morningstar. They visually provide a graphical representation of investing categories for equity investments. A style box is a valuable tool for investors to use when determining asset allocation.

There are 9 categories:

Large Value, Large Blend, Large Growth

Medium Value, Medium Blend, Medium Growth

Small Value, Small Blend, Small Growth

The strength of the 9 categories are found by using 9 Vanguard ETF's that follow the respective CRSP index of their category.

Donchian Screener█ OVERVIEW

This is a screener script for the Donchian Channel indicator . It's an excellent indicator for trend following, a trading strategy which tries to take advantage of long, medium or short-term moves that seem to play out in various markets.

█ DESCRIPTION

The screener works by scanning through up to 10 symbols and list down symbols that are currently breaking through the upper or lower band as definied by the Donchian Channels, at which point the market signals the start of a bullish or bearish trend.

█ HOW TO USE

After adding the indicator, open the script settings and type the symbol name and length to be used on the Donchian Channels for each stock.

█ PARAMETERS

- Use High/Low Price Breakouts: check this box if you want to use price high/low instead of price close to identify breakouts

- Panel Position: choose whether you want to position the panel on the top, middle or bottom right side of the graph (default is top)

- Default Timeframe: what timeframe to use on the screener (default is daily)

- Ticker: the ticker name you want to monitor

- Length: length parameter used on Donchian Channel indicator

█ FEATURES

The screener can scan up to 10 symbols each time.

█ LIMITATIONS

The screener will scan the symbols breaking out bands on the current bar, and as such, there maybe some delays depending on the stock/ etf /crypto you choose. Some exchanges require an additional subscription to get realtime data.

Linear Regression Relative Strength[image/x/iZvwDWEY/

Relative Strength indicator comparing the current symbol to SPY (or any other benchmark). It may help to pick the right assets to complement the portfolio build around core ETFs such as SPY.

The general idea is to show if the current symbol outperforms or underperforms the benchmark (SPY by default) when bought some certain time ago. Relative performance is displayed as percent and is calculated for three different time ranges - short (1 mo by default), mid (1 quarter), and long (half a year). To smooth the volatility, the script uses linear regression to estimate the trend and takes the start and the end points of the linear regression line to compute the relative strength.

It is important to remember that the script shows the gain relative to SPY (or other selected benchmark), not the asset's gain. Therefore, it may indicate that the asset is profitable, but it still may lose value if SPY is in downtrend.

Therefore, it is crucial to check other indicators before making a decision. In the example above, standard linear regression for one quarter is used to indicate the direction of the trend.

Market DirectionThis script uses the ETF "VTI" to track the trend of the market

It requires 2 consecutive 5 day periods up or down to verify the direction otherwise the trend is neutral

It also uses a BB%B calculation to determine over bought and over sold conditions.

It will display numbers for 10 days ago, 5 days ago, downtrend today and uptrend today and finally the %B

Feel free to use or modify and offer suggestions for improvements

Cumulative RSI StrategyI suppose nothing drives a point home like a 10+ year backtest! A couple of weeks ago I published a custom indicator called the Cumulative RSI. This indicator was straight out of chapter 9 of "Short Term Trading Strategies That Work." Today I am publishing a basic sample strategy in that uses the Cumulative RSI as its only entry and exit signals on a Nasdaq 100 leveraged index ETF (TQQQ). In this example, the indicator is being used as a longer term strategy with just 10% leverage over the account equity and a $25k start balance.

If I had it 10 years ago I would probably be retired! I'm sharing because I've found that it can provide an edge when determining exit/take profit points for trades. Many traders wait for a price reversal / trailing-stop to exit a trade when it starts losing. I've found that, using tools like the Cumulative RSI, you can achieve better exit points over the long term. Disclaimer: Even though this example significantly beats buy and hold, I wouldn't advise using it as a stand-alone strategy without significant additions/modifications to strategy and risk management functions.