Triad Macro Gauge__________________________________________________________________________________

Introduction

__________________________________________________________________________________

The Triad Macro Gauge (TMG) is designed to provide traders with a comprehensive view of the macroeconomic environment impacting financial markets. By synthesizing three critical market signals— VIX (volatility) , Credit Spreads (credit risk) , and the Stocks/Bonds Ratio (SPY/TLT) —this indicator offers a probabilistic assessment of market sentiment, helping traders identify bullish or bearish macro conditions.

Holistic Macro Analysis: Combines three distinct macroeconomic indicators for multi-dimensional insights.

Customization & Flexibility: Adjust weights, thresholds, lookback periods, and visualization styles.

Visual Clarity: Dynamic table, color-coded plots, and anomaly markers for quick interpretation.

Fully Consistent Scores: Identical values across all timeframes (4H, daily, weekly).

Actionable Signals: Clear bull/bear thresholds and volatility spike detection.

Optimized for timeframes ranging from 4 hour to 1 week , the TMG equips swing traders and long-term investors with a robust tool to navigate macroeconomic trends.

__________________________________________________________________________________

Key Indicators

__________________________________________________________________________________

VIX (CBOE:VIX): Measures market volatility (negatively weighted for bearish signals).

Credit Spreads (FRED:BAMLH0A0HYM2EY): Tracks high-yield bond spreads (negatively weighted).

Stocks/Bonds Ratio (SPY/TLT): Evaluates equity sentiment relative to treasuries (positively weighted).

__________________________________________________________________________________

Originality and Purpose

__________________________________________________________________________________

The TMG stands out by combining VIX, Credit Spreads, and SPY/TLT into a single, cohesive indicator. Its unique strength lies in its fully consistent scores across all timeframes, a critical feature for multi-timeframe analysis.

Purpose: To empower traders with a clear, actionable tool to:

Assess macro conditions

Spot market extremes

Anticipate reversals

__________________________________________________________________________________

How It Works

__________________________________________________________________________________

VIX Z-Score: Measures volatility deviations (inverted for bearish signals).

Credit Z-Score: Tracks credit spread deviations (inverted for bearish signals).

Ratio Z-Score: Assesses SPY/TLT strength (positively weighted for bullish signals).

TMG Score: Weighted composite of z-scores (bullish > +0.30, bearish < -0.30).

Anomaly Detection: Identifies extreme volatility spikes (z-score > 3.0).

All calculations are performed using daily data, ensuring that scores remain consistent across all chart timeframes.

__________________________________________________________________________________

Visualization & Interpretation

__________________________________________________________________________________

The script visualizes data through:

A dynamic table displaying TMG Score , VIX Z, Credit Z, Ratio Z, and Anomaly status, with color gradients (green for positive, red for negative, gray for neutral/N/A).

A plotted TMG Score in Area, Histogram, or Line mode , with adaptive opacity for clarity.

Bull/Bear thresholds as horizontal lines (+0.30/-0.30) to signal market conditions.

Anomaly markers (orange circles) for volatility spikes.

Crossover signals (triangles) for bull/bear threshold crossings.

The table provides an immediate snapshot of macro conditions, while the plot offers a visual trend analysis. All values are consistent across timeframes, simplifying multi-timeframe analysis.

__________________________________________________________________________________

Script Parameters

__________________________________________________________________________________

Extensive customization options:

Symbol Selection: Customize VIX, Credit Spreads, SPY, TLT symbols

Core Parameters: Adjust lookback periods, weights, smoothing

Anomaly Detection: Enable/disable with custom thresholds

Visual Style: Choose display modes and colors

__________________________________________________________________________________

Conclusion

__________________________________________________________________________________

The Triad Macro Gauge by Ox_kali is a cutting-edge tool for analyzing macroeconomic trends. By integrating VIX, Credit Spreads, and SPY/TLT, TMG provides traders with a clear, consistent, and actionable gauge of market sentiment.

Recommended for: Swing traders and long-term investors seeking to navigate macro-driven markets.

__________________________________________________________________________________

Credit & Inspiration

__________________________________________________________________________________

Special thanks to Caleb Franzen for his pioneering work on macroeconomic indicator blends – his research directly inspired the core framework of this tool.

__________________________________________________________________________________

Notes & Disclaimer

__________________________________________________________________________________

This is the initial public release (v2.5.9). Future updates may include additional features based on user feedback.

Please note that the Triad Macro Gauge is not a guarantee of future market performance and should be used with proper risk management. Past performance is not indicative of future results.

VIX CBOE Volatility Index

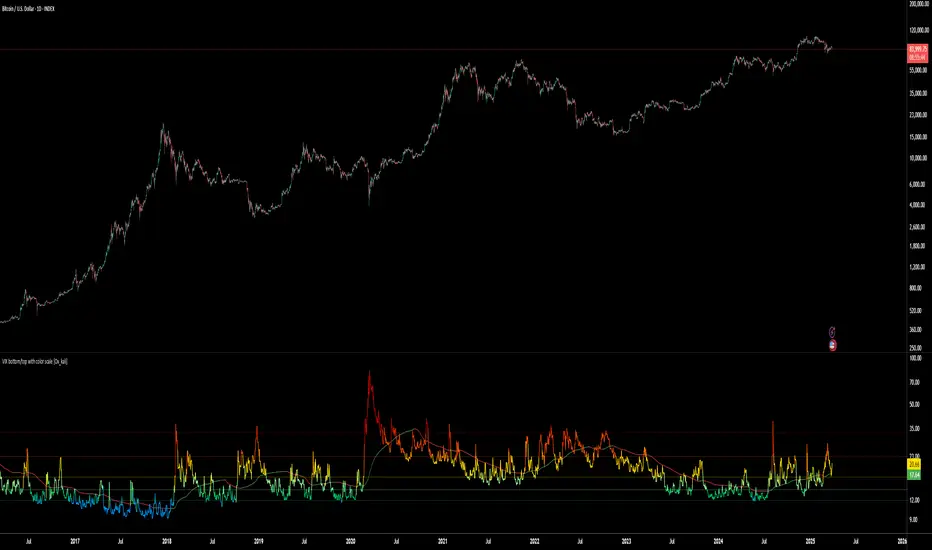

VIX bottom/top with color scale [Ox_kali]📊 Introduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” script is designed to provide an intuitive, color-coded visualization of the VIX (Volatility Index), helping traders interpret market sentiment and volatility extremes in real time.

It segments the VIX into clear threshold zones, each associated with a specific market condition—ranging from fear to calm—using a dynamic color-coded system.

This script offers significant value for the following reasons:

Intuitive Risk Interpretation: Color-coded zones make it easy to interpret market sentiment at a glance.

Dynamic Trend Detection: A 200-period SMA of the VIX is plotted and dynamically colored based on trend direction.

Customization and Flexibility: All colors are editable in the parameters panel, grouped under “## Color parameters ##”.

Visual Clarity: Key thresholds are marked with horizontal lines for quick reference.

Practical Trading Tool: Helps identify high-risk and low-risk environments based on volatility levels.

🔍 Key Indicators

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

VIX (CBOE Volatility Index) : Measures market volatility and investor fear.

SMA 200 : Long-term trendline of the VIX, with color-coded direction (green = uptrend, red = downtrend).

Color-coded VIX Levels:

🔴 33+ → Something bad just happened

🟠 23–33 → Something bad is happening

🟡 17–23 → Something bad might happen

🟢 14–17 → Nothing bad is happening

✅ 12–14 → Nothing bad will ever happen

🔵 <12 → Something bad is going to happen

🧠 Originality and Purpose

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Unlike traditional VIX indicators that only plot a line, this script enhances interpretation through visual segmentation and dynamic trend tracking.

It serves as a risk-awareness tool that transforms the VIX into a simple, emotional market map.

This is the first version of the script, and future updates may include alerts, background fills, and more advanced features.

⚙️ How It Works

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The script maps the current VIX value to a range and applies the corresponding color.

It calculates a SMA 200 and colors it green or red depending on its slope.

It displays horizontal dotted lines at key thresholds (12, 14, 17, 23, 33).

All colors are configurable via input parameters under the group: "## Color parameters ##".

🧭 Indicator Visualization and Interpretation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The VIX line changes color based on market condition zones.

The SMA line shows long-term direction with dynamic color.

Horizontal threshold lines visually mark the transitions between volatility zones.

Ideal for quickly identifying periods of fear, caution, or stability.

🛠️ Script Parameters

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Grouped under “## Color parameters ##”, the following elements are customizable:

🎨 VIX Zone Colors:

33+ → Red

23–33 → Orange

17–23 → Yellow

14–17 → Light Green

12–14 → Dark Green

<12 → Blue

📈 SMA Colors:

Uptrend → Green

Downtrend → Red

These settings allow users to match the script’s visuals to their preferred chart style or theme.

✅ Conclusion

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” is a clean, powerful script designed to simplify how traders view volatility.

By combining long-term trend data with real-time color-coded sentiment analysis, this script becomes a go-to reference for managing risk, timing trades, or simply staying in tune with market mood.

🧪 Notes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This is version 1 of the script. More features such as alert conditions, background fill, and dashboard elements may be added soon. Feedback is welcome!

💡 Color code concept inspired by the original VIX interpretation chart by @nsquaredvalue on Twitter. Big thanks for the visual clarity! 💡

⚠️ Disclaimer

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This script is a visual tool designed to assist in market analysis. It does not guarantee future performance and should be used in conjunction with proper risk management. Past performance is not indicative of future results.

VIX Implied MovesKey Features:

Three Timeframe Bands:

Daily: Blue bands showing ±1σ expected move

Weekly: Green bands showing ±1σ expected move

30-Day: Red bands showing ±1σ expected move

Calculation Methodology:

Uses VIX's annualized volatility converted to specific timeframes using square root of time rule

Trading day convention (252 days/year)

Band width = Price × (VIX/100) ÷ √(number of periods)

Visual Features:

Colored semi-transparent backgrounds between bands

Progressive line thickness (thinner for shorter timeframes)

Real-time updates as VIX and ES prices change

Example Calculation (VIX=20, ES=5000):

Daily move = 5000 × (20/100)/√252 ≈ ±63 points

Weekly move = 5000 × (20/100)/√50 ≈ ±141 points

Monthly move = 5000 × (20/100)/√21 ≈ ±218 points

This indicator helps visualize expected price ranges based on current volatility conditions, with wider bands indicating higher market uncertainty. The probabilistic ranges represent 68% confidence levels (1 standard deviation) derived from options pricing.

Standard Deviation Lines v1.0Overview

The Standard Deviation Lines v1.0 indicator is designed to provide a statistical approach to market volatility by plotting multiple standard deviation levels based on price action. This tool helps traders identify key price levels where the market may experience significant reactions, making it useful for trend analysis, support/resistance identification, and volatility-based trading strategies.

Key Features

✅ Dynamic Standard Deviation Levels: Calculates and plots up to ±3 standard deviation levels, giving traders a clear view of price dispersion and potential overbought/oversold areas.

✅ Quadrant-Based Deviation Zones: Divides standard deviation ranges into smaller, meaningful levels (e.g., 0.214, 0.382, 0.50, 0.618, 0.786) for a granular analysis of price movements.

✅ VIX Integration for Volatility Adjustment: Incorporates CBOE:VIX to dynamically adjust standard deviation levels based on market volatility.

✅ Weekly vs. Daily Mode: Users can toggle between weekly and daily standard deviation calculations to adapt to different trading strategies.

✅ Auto-Updating Levels: The indicator refreshes at market close (17:00), ensuring traders work with the latest price data.

✅ Customizable Display: Uses color-coded lines to differentiate between positive and negative deviations, with dashed lines for mid-levels and key support/resistance areas.

How to Use

📌 Trend & Volatility Analysis – Higher standard deviation levels indicate strong price movements, helping traders assess trend strength and market volatility.

📌 Reversal & Continuation Signals – Prices reaching extreme standard deviation levels (±2 or ±3) may suggest potential reversals or breakouts.

📌 Support & Resistance Zones – The quadrant-based deviation zones help identify hidden support/resistance areas where price may react.

📌 Risk Management – Traders can use standard deviation bands to set stop-loss and take-profit levels based on statistical price dispersion.

Best For

🔹 Day traders & swing traders looking to incorporate volatility-based strategies.

🔹 Mean reversion traders who capitalize on price returning to statistical averages.

🔹 Momentum traders who want to confirm trend strength and continuation.

Try the Standard Deviation Lines v1.0 now and enhance your market analysis with a statistical edge!

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

VIX:VIX3M RatioThe VIX/VIX3M Ratio indicator compares the short-term (1-month) volatility index (VIX) to the medium-term (3-month) volatility index (VIX3M). This ratio provides insights into the market's volatility expectations across different time horizons.

Key Interpretations:

Ratio > 1: Short-term volatility expectations are higher than 3-month expectations

Ratio = 1: Short-term and medium-term volatility expectations are aligned

Ratio < 1: Medium-term volatility expectations are higher than short-term expectations

Potential Trading Insights:

A rising ratio may indicate increasing near-term market uncertainty

Significant deviations from 1.0 can signal potential market stress or changing risk perceptions

Traders use this to gauge the term structure of market volatility

DAILY ATR LEVELS AND EXPECTED MOVE LEVELSThis Pine Script code is designed to visualize ATR (Average True Range) levels and expected move levels on a chart. It provides useful inputs for customizing how these levels are displayed, such as line width, style, and color. The script is divided into several sections, each focused on a different feature:

1. User Inputs for Customization:

- Line Width and Style: Users can customize the line width, style (solid, dotted, or dashed), and color for various levels.

- Offset for Line Placement: The rightOffset input controls how far in the future the lines extend (measured in minutes).

- Show Labels: Labels can be toggled on/off for ATR levels and expected move lines, with customizable text colors.

2. ATR Levels and ATR Settings:

- The ATR length (atrLength) and the multiplier (atrMultiplier) control the calculation of ATR levels.

- The script plots ATR levels based on the daily open price, including key levels like ATR +25%, ATR +50%, etc., for both positive and negative movements.

- Line Drawing: The script dynamically creates lines for each ATR level, and the lines are customized according to the user's inputs. For each level, the line.new function is used to plot a line from the start of the day (daily open) to a point offset in the future.

- Labels: Labels are added near each ATR level to make them more identifiable, such as "ATR +25%" or "Daily Open."

3. Expected Move Calculation and Logic:

- The script calculates the expected move for the next trading session based on the previous close price and the volatility derived from the VIX (Volatility Index).

- The expected move is calculated as a percentage of the previous close and is added and subtracted from the previous close price to generate upper and lower levels.

- Volatility Adjustment: The VIX value is adjusted by the square root of 252 (the number of average trading days in a year) to calculate the daily volatility.

- Upper and Lower Lines: Lines are drawn for the expected move's upper and lower bounds, showing the potential price movement based on volatility.

4. Customizable Expected Move Lines:

- Line Style and Color: The upper and lower expected move lines can be customized in terms of width, style, and color, as specified by the user.

- Labels for Expected Move Levels: Labels are added for the upper and lower expected move lines, such as "Expected Move Upper" and "Expected Move Lower."

5. Logic for Drawing Lines:

- The script continuously evaluates whether the levels should be displayed based on the user's preferences.

- If showATRLevels or showLineEM is enabled, the script will draw the respective lines and labels on the chart.

- It uses line.new to draw the lines and label.new to position the labels at the correct levels on the chart.

6. Handling Time and Line Deletion:

- The script handles the dynamic nature of the chart by deleting previous lines (using line.delete) to avoid cluttering the chart with outdated lines.

- The time for the lines is set dynamically using the startTime and endTime variables, ensuring that lines are drawn within the correct timeframe.

Summary of Key Features:

- ATR Levels: Plots key levels of ATR, such as daily open, ATR +25%, ATR -25%, etc., with customizable colors and line styles.

- Expected Move Levels: Calculates and plots the upper and lower bounds of the expected move based on the VIX and previous close price.

- Customization Options: Users can control the appearance (line width, style, color) and whether to show labels for the ATR and expected move levels.

- Dynamic Updates: The lines and labels update dynamically throughout the trading day, adjusting based on market conditions.

Overall, this script is designed to help traders visualize volatility and potential price movement on a daily chart by providing ATR-based levels and expected move projections. It offers a high degree of customization to suit different charting preferences.

VIX CANDLESThe VIX CANDLES indicator is designed to visualize the Williams VIX Fix, a volatility measure that mimics the VIX index but applies to different financial instruments.

This indicator calculates a custom "VIX-like" value based on the highest close over a specified look-back period and plots the result as candlesticks. It also includes an Exponential Moving Average (EMA) to help identify trends and potential buy/sell signals.

Williams VIX Fix Calculation: Measures volatility by comparing the current low to the highest close over the given period, then expressing the result as a percentage.

Custom Candles: The VIX Fix is displayed as a set of candlesticks where the body is colored based on whether the close is higher (green) or lower (red) than the open.

Exponential Moving Average (EMA): An EMA is applied to the VIX Fix value to smooth the data and identify trend changes. The EMA's length is customizable.

Trade Direction Labels: Labels are plotted when the VIX Fix crosses above or below the EMA, signaling potential buy (▽) or sell (△) opportunities.

Customization: Colors for the candlesticks and EMA, as well as the look-back period and EMA length, can be adjusted to suit your preferences.

This indicator is useful for traders looking to track volatility and identify potential trend shifts in the market. By combining the Williams VIX Fix with an EMA, it provides a more dynamic view of market conditions, helping traders spot extreme volatility and adjust their strategies accordingly.

VIX Bars [CrossTrade]In simple terms, this indicator colors your chart bars based on the VIX levels. We know that high volatility is unstainable and will naturally regress to a calmer market, therefore highlighting the bars where VIX is at extreme highs can sometimes indicate a market turning point. Consider pairing this indicator with my VIX Heatmap indicator for a complete picture of volatility.

Customizable VIX Levels: You can set your own thresholds for when the bars turn green or red. Green bars pop up when the VIX is above your set upper level (default is 30) - kind of like a heads-up that things might get bumpy. Red bars show up when the VIX dips below your lower threshold (default is 15), signaling calmer waters.

Optional Donchian Channel Filter: The Donchian Channel filter looks at the highest highs and lowest lows over your chosen period (default's 52 days) and only colors the bars if they match the filter's criteria. This adds an extra layer of confirmation that the colored bars at at a major high or low.

Visual Simplicity: The indicator keeps things visually straightforward. No cluttered screen, just colored bars telling you a story about market vibes. Alert come standard to signal those potential bottom or top bars based on the VIX being at your preferred extreme levels.

In essence, "VIX Bars" is like having a volatility radar on your chart. It doesn't make predictions, but it sure gives you a neat, color-coded heads-up on market sentiment. Great for adding an extra dimension to your analysis without getting all tangled up in complex indicators!

VIX-Heatmap [CrossTrade]The "VIX-Heatmap" is a sophisticated and informative indicator designed for traders who want to integrate volatility analysis into their trading strategy, especially focusing on the market's fear gauge, the VIX (Volatility Index). This tool is not just about plotting numbers; it's about visualizing market sentiment in a more intuitive and impactful way.

Key Features and Customization Options:

1. Primary Functionality:

At its core, the VIX-Heatmap tracks the daily closing price of the VIX. It provides a clear, line-based visualization, with the line color set to black for stark contrast and easy visibility.

2. Segmented Volatility Levels:

The indicator allows users to set multiple VIX levels: Danger Zone (super low VIX level), and Levels 1 through 5. These levels are represented as horizontal lines on the chart, offering a structured view of different volatility thresholds.

3. Customizable Thresholds:

Traders can input their preferred values for each level, tailoring the indicator to fit their perception of market risk and volatility. This customization makes the tool versatile for different trading styles and market conditions.

4. Heatmap Visualization:

The chart's background color changes based on the VIX level, creating a "heatmap" effect. This visual representation allows traders to quickly gauge the current market sentiment. The color intensity varies from white (for extremely low VIX values) through various shades of red, increasing in intensity with higher VIX levels. This gradient provides an immediate visual cue of rising or falling market anxiety.

5. Interactive Display:

The indicator includes an interactive table display at the bottom center of the chart that shows the current VIX level in large, bold text, ensuring that it catches the trader's eye.

6. Optional Background Coloring:

Users have the option to enable or disable the heatmap feature. When enabled, the chart's background reflects the VIX level with the corresponding color, enhancing the visual impact of the data.

Applications and Benefits:

The VIX-Heatmap is ideal for traders who base their decisions not only on price movements but also on market sentiment and volatility. Its color-coded heatmap approach simplifies the interpretation of the VIX data, making it accessible even to those who may not be deeply familiar with volatility indices. By offering a quick visual summary of current market fear levels, it aids in making informed decisions, especially in times of market uncertainty.

In summary, the VIX-Heatmap transforms the traditional VIX data into an interactive, visually engaging, and easy-to-interpret format.

MTF Williams Vix Market Bottoms [CryptoSea]MTF Williams Vix Fix Indicator is a dynamic tool tailored for traders looking to capture market extremes with high precision. This multi-timeframe indicator leverages the concept of the Williams Vix Fix to spot potential reversals before they occur.

Key Features

Multi-Timeframe Analysis: Provides simultaneous visibility across multiple timeframes, enabling traders to assess market conditions comprehensively from a single chart.

Advanced Volatility Detection: Utilizes a modified Vix Fix formula to highlight extreme price deviations, which often precede significant market reversals.

Customizable Settings: Offers extensive input options to tweak the lookback periods, percentile thresholds, and visibility settings, aligning with various trading strategies.

Visual Band Indicators: Features upper bands and range highs that signal potential overbought and oversold conditions, enhancing trading decision-making.

Below, you can see how the indicator performs across different timeframes, providing valuable insights into market behavior.

How it Works

Vix Fix Calculation: Determines the worst-case 'panic' sell-offs in price as a percentage of the high, capturing the emotional extremes of the market.

Statistical Bands: Employs Bollinger bands over the Vix Fix values to define normal and extreme volatility conditions.

Color-Coded Indicators: Uses color differentiation to instantly highlight when readings surpass critical upper band or range high thresholds, signaling key trading opportunities.

For instance, in the analysis provided below, notice how the indicator flags significant market moves, allowing traders to anticipate potential entry or exit points.

Application

Risk Management: Aids in identifying extreme market conditions where prices may revert, helping in effective position sizing and risk management.

Strategic Planning: Enhances strategic trading plans by identifying not only when but also where market extremes may occur, considering multiple timeframes.

Customization: Adapts seamlessly to different market environments with adjustable settings for volatility thresholds and visual display preferences.

The MTF Williams Vix Fix Indicator by is an essential tool for traders aiming to leverage market volatility for optimal entry and exit, ensuring they are well-equipped to handle market extremes with confidence.

SVMKR_VIX_Based_LevelsThe "SVMKR_VIX_Based_Levels" script is a Pine Script indicator designed to assist intraday traders in identifying dynamic support and resistance levels based on the Volatility Index (VIX). Here's a breakdown of the script and its uses for intraday traders:

### Script Description:

1. **Data Retrieval**:

- The script fetches daily closing prices of the India VIX (volatility index) and a specified security using `request.security()`.

2. **Input Parameters**:

- Intraday traders can customize the indicator using input parameters such as the number of levels above and below the Pivot Day Close (PDC), line offset lengths, line extension options, and color and width settings for plotted lines.

3. **Plotting**:

- The script plots the PDC and VIX as hidden lines (`display=display.none`).

- Support and resistance levels are calculated based on the VIX and PDC, and plotted above and below the PDC with customizable colors and widths.

- Each level can be labeled with its corresponding price.

4. **Customization**:

- Intraday traders can choose to display or hide prices on the plotted lines.

- Colors and widths of plotted lines are customizable.

- Options to show minor and mild support levels provide additional flexibility.

5. **Labels**:

- Labels are added to indicate the PDC and the plotted levels, displaying corresponding prices if enabled.

### Uses for Intraday Traders:

1. **Dynamic Support and Resistance**: Intraday traders can benefit from dynamically adjusted support and resistance levels that respond to changes in market volatility, providing more accurate levels for trade planning.

2. **Market Sentiment Analysis**: By incorporating the VIX, a measure of market volatility and sentiment, the indicator provides insights into market sentiment, helping intraday traders gauge market mood and potential direction.

3. **Confirmation of Price Action**: The plotted support and resistance levels can serve as confirmation signals for intraday traders, helping validate trading decisions and enhance trading confidence.

4. **Adaptability to Changing Market Conditions**: Intraday traders often face rapidly changing market conditions. The indicator's ability to adapt to changes in volatility ensures that plotted levels remain relevant and responsive, aiding traders in adjusting their strategies accordingly.

5. **Trade Planning and Execution**: Intraday traders can use the plotted support and resistance levels to identify potential entry and exit points, set profit targets and stop-loss levels, and plan their trades more effectively.

Overall, the "SVMKR_VIX_Based_Levels" indicator provides intraday traders with a valuable tool for dynamic support and resistance identification, market sentiment analysis, confirmation of price action, and trade planning and execution, ultimately assisting them in making more informed and profitable trading decisions in the intraday timeframe.

VIX Statistical Sentiment Index [Nasan]** THIS IS ONLY FOR US STOCK MARKET**

The indicator analyzes market sentiment by computing the Rate of Change (ROC) for the VIX and S&P 500, visualizing the data as histograms with conditional coloring. It measures the correlation between the VIX, the specific stock, and the S&P 500, displaying the results on the chart. The reliability measure combines these correlations, offering an overall assessment of data robustness. One can use this information to gauge the inverse relationship between VIX and S&P 500, the alignment of the specific stock with the market, and the overall reliability of the correlations for informed decision-making based on the inverse relationship of VIX and price movement.

**WHEN THE VIX ROC IS ABOVE ZERO (RED COLOR) AND RASING ONE CAN EXPECT THE PRICE TO MOVE DOWNWARDS, WHEN THE VIX ROC IS BELOW ZERO (GREEN)AND DECREASING ONE CAN EXPECT THE PRICE TO MOVE UPWARDS"

Understanding the VIX Concept:

The VIX, or Volatility Index, is a widely used indicator in finance that measures the market's expectation of volatility over the next 30 days. Here are key points about the VIX:

Fear Gauge:

Often referred to as the "fear gauge," the VIX tends to rise during periods of market uncertainty or fear and fall during calmer market conditions.

Inverse Relationship with Market:

The VIX typically has an inverse relationship with the stock market. When the stock market experiences a sell-off, the VIX tends to rise, indicating increased expected volatility.

Implied Volatility:

The VIX is derived from the prices of options on the S&P 500. It represents the market's expectations for future volatility and is often referred to as "implied volatility."

Contrarian Indicator:

Extremely high VIX levels may indicate oversold conditions, suggesting a potential market rebound. Conversely, very low VIX levels may signal complacency and a potential reversal.

VIX vs. SPX Correlation:

This correlation measures the strength and direction of the relationship between the VIX (Volatility Index) and the S&P 500 (SPX).

A negative correlation indicates an inverse relationship. When the VIX goes up, the SPX tends to go down, and vice versa.

The correlation value closer to -1 suggests a stronger inverse relationship between VIX and SPX.

Stock vs. SPX Correlation:

This correlation measures the strength and direction of the relationship between the closing price of the stock (retrieved using src1) and the S&P 500 (SPX).

This correlation helps assess how closely the stock's price movements align with the broader market represented by the S&P 500.

A positive correlation suggests that the stock tends to move in the same direction as the S&P 500, while a negative correlation indicates an opposite movement.

Reliability Measure:

Combines the squared values of the VIX vs. SPX and Stock vs. SPX correlations and takes the square root to create a reliability measure.

This measure provides an overall assessment of how reliable the correlation information is in guiding decision-making.

Interpretation:

A higher reliability measure implies that the correlations between VIX and SPX, as well as between the stock and SPX, are more robust and consistent.

One can use this reliability measure to gauge the confidence they can place in the correlations when making decisions about the specific stock based on VIX data and its correlation with the broader market.

VIX based LevelsSupport and resistance levels for the day based on the volatility index.

Major - The Major support line where the day low, high or close can occur at that level

Minor - The second level of the Support/Resistance line , where we can expect some rejections or breakouts/breakdowns

Mild - The mid level between the Major and minor levels. The market may consolidate around that area.

The script will automatically get the previous day close value of the current scrip and the India vix.

India vix is calculated based on the annual percentage and hence the previous day close value of the scrip is divided by 19.1 ( square root of 365 )

The PDC values can be manually overridden for backtesting purposes.

Please note, there will be some slippages involved on the trend lines.

Williams Vix Fix [CC]The Vix Fix indicator was created by Larry Williams and is one of my giant backlog of unpublished scripts which I'm going to start publishing more of. This indicator is a great synthetic version of the classic Volatility Index and can be useful in combination with other indicators to determine when to enter or exit a trade due to the current volatility. The indicator creates this synthetic version of the Volatility Index by a fairly simple formula that subtracts the current low from the highest close over the last 22 days and then divides that result by the same highest close and multiplies by 100 to turn it into a percentage. The 22-day length is used by default since there is a max of 22 trading days in a month but this formula works well for any other timeframe. By itself, this indicator doesn't generate buy or sell signals but generally speaking, you will want to enter or exit a trade when the Vix fix indicator amount spikes and you get an entry or exit signal from another indicator of your choice. Keep in mind that the colors I'm using for this indicator are only a general idea of when volatility is high enough to enter or exit a trade so green colors mean higher volatility and red colors mean low volatility. This is one of the few indicators I have written that don't recommend to buy or sell when the colors change.

This was a custom request from one of my followers so please let me know if you guys have any other script requests you want to see!

VIX Monitor [Zero54]NSE:BANKNIFTY1!

This is a simple but invaluable tool for both day traders and positional traders. VIX is about market expectations of volatility

The VIX is a very good and sound measure of risk in the markets. It gives these stock traders who are in intraday trading and short term traders an idea of whether the volatility is going up or going down in the market. They can calibrate their strategy accordingly. When the volatility is likely to shoot up sharply, the intraday traders run the risk of stop losses getting triggered quickly. Hence they can either reduce their leverage or they can widen their stop losses accordingly.

Also if you notice VIX is a very good and reliable gauge of index movement. If you plot the VIX and the Nifty movement you will see a clear negative correlation in the charts itself. Markets typically tend to peak out when the VIX is bottoming out and the markets tend to bottom out when the VIX is peaking out. This is a useful input for index trades.

You can use this simple indicator to monitor VIX real time. You can use it for short time frame intraday and also multi-hour, multi-day charts. You can also plot a moving average to gauge the VIX trend.

Also is the ability to monitor, Nifty and BankNifty the same way you are able to monitor the VIX (as explained above). The overall market moves in correlation with these main Indexes. So if you are trading a specific counter, you can also keep an eye on the index to get an idea where the counter may be going next.

The source code is open, please feel to modify or re-use as you feel it’s necessary. Any changes, improvements, bugs, please let me know.

Please like/boost this indicator and also add your comments, if you find it useful.

VIX, ATR, and Volatility Indicatorhere what the indictor do !

The "VIX, ATR, and Volatility Indicator" combines the Volatility Index (VIX), Average True Range (ATR), and moving averages to provide insights into market volatility.

VIX (Volatility Index):

The VIX measures the expected volatility in the market over the next 30 days. A higher VIX value indicates increased market volatility, while a lower value suggests lower volatility.

ATR (Average True Range):

The ATR is a technical indicator that measures the average range between high and low prices over a specified period. It provides a sense of the market's volatility by considering price movements. Higher ATR values indicate greater volatility, while lower values indicate lower volatility.

Moving Averages:

The indicator calculates both an Exponential Moving Average (EMA) and Simple Moving Average (SMA) with a specific period (e.g., 50).

Moving averages smooth out price data to identify trends and potential areas of support or resistance.

Volatility Detection:

By comparing the current closing price to the EMA and SMA, the indicator determines if there is high volatility.

If the current closing price is higher than either the EMA or SMA, it indicates potential high volatility.

Visualization:

The VIX and ATR are typically plotted on the chart, providing a visual representation of market volatility and price range.

Additionally, markers or labels may be used to highlight periods of high volatility when the current price exceeds the moving averages.

what are the VIX and ATR

Volatility Index (VIX):

Monitor the VIX value from financial platforms or market data providers. A higher VIX value indicates increased market volatility, suggesting potential trading opportunities. Conversely, a lower VIX value indicates lower volatility, which may influence your trading strategy.

Average True Range (ATR):

Calculate the ATR manually or use charting platforms that provide ATR as an indicator.

Plot the ATR on your trading chart to visualize the range of price movements.

Determine suitable entry and exit points based on ATR values. For example, higher ATR values may indicate larger potential price swings, while lower ATR values may suggest a more stable market.

how it work

Fetching VIX Data:

The request.security function is used to fetch the daily VIX data from the "CBOE:VIX" symbol. It retrieves the closing price of the VIX for each day.

Calculating ATR:

The ta.atr function calculates the Average True Range (ATR) with a period of 14. ATR measures the average range between the high and low prices over the specified period, providing an indication of market volatility.

Calculating Moving Averages:

Two types of moving averages are calculated: Exponential Moving Average (EMA) and Simple Moving Average (SMA). Both moving averages are calculated using a period of 50, but you can adjust the period as needed.

The ta.ema function calculates the Exponential Moving Average, which places greater weight on recent prices.

The ta.sma function calculates the Simple Moving Average, which gives equal weight to all prices in the period.

Identifying High Volatility:

The indicator determines if there is high volatility by comparing the current closing price to both the EMA and SMA.

If the current closing price is higher than either the EMA or SMA, the isHighVolatility variable is set to true, indicating potential high volatility.

Plotting the Indicators:

The VIX and ATR are plotted using the plot function, assigning colors and line widths for visual differentiation.

The plotshape function is used to plot markers below the bars to indicate highly volatile periods. The isHighVolatility variable determines when the markers appear.

TTP VIX SpyTTP VIX Spy is an indicator that uses data from TVC:VIX to better time entries in the market.

The assumption used is that when the VIX is coming down from the top of its range then the risk on assets can move to the upside and when the VIX is is pushing higher there's a high likelihood or risk on assets going down.

This indicator observes the momentum of VIX using MACD. It offers two different signals both for longs and shorts: signal 1 and 2.

Signal 1 is activate when the begging of a new trend for the VIX is confirmed.

Signal 2 is activated when the VIX pulls back from an extreme value.

You can configure the parameters of the internal super trend and the look back for the slope applied to price and RSIs.

The indicator offers the following filter parameters:

- Price RSI slope: it filters signals that have RSI slope pointing in the opposite direction of the signal.

- Counter trend: it filters signals that are not counter trending super trend.

- Wide BBW: it filters signals that happen when there hasn't been high price volatility

- Price slope: it filters signals when the price is not pointing in the direction of the signal (buy: up, sell: down)

- VIX RSI filter: it filters VIX RSI values overextended. MACD can be in the right range, but sometimes RSI contradicts it. By default is OFF since it can cause false negatives.

- Working days only: it filters signals that occur in the weekend.

The colours below the price action show how the VIX momentum is changing. Transitions from red into pink and then green show how the fear is fading which tends to lead to lead to bullish moves, and the opposite when the transitions are from green to red.

Performance and initial thoughts.

I have tried VIX Spy on both BINANCE:BTCUSDT.P and BINANCE:ETHUSDT.P and it seems to offer a decent win ratio. As you can see I had to add many filter to remove bad entries and left toggles available to decide which ones you want to use.

I tried the signal in the 4H, 1H and 15min with mixed results. I tend to incline for the results in the 1H.

VIX signal offers a backtestable stream and alerts both for signals 1 and 2.

VIX HeatmapVIX HeatMap

Instructions:

- To be used with the S&P500 index (ES, SPX, SPY, any S&P ETF) as that's the input from where the CBOE calculates and measures the VIX. Can also be used with the Dow Jones, Nasdaq, & Nasdaq100.

Description:

- Expected Implied Volatility regime simplified & visualized. Know if we are in a high, medium, or low volatility regime, instantly.

- Ranges from Hot to Cold: The hotter the heat-map, the higher the implied volatility and fear & vice versa.

- The VIX HeatMap, color-maps important VIX levels (7 in this case) in measuring volatility for day trading & swing trading.

Using the VIX HeatMap:

- A LOW level volatility environment: Represented by "cooler" colors (Blue & White) depicts that the level of volatility and fear is low. Percentage moves on the index level are going to be tame and less volatile more often than not. Low fear = low perceived risk.

- A MEDIUM level volatility environment: Represented by "warmer" colors (Green & Yellow) depicts that the markets are transitioning from a calmer period or from a more fearful period. Market volatility here will be higher and provide more volatile swings in price.

- A HIGH level volatility environment: Represented by "hotter" colors (Orange, Red, & Purple) depicts that the markets are very fearful at the moment and will have big swings in both directions. Historically, extreme VIX levels tend to coincide with bottoms but are in no way predictive of the exact timing as the volatile moves can continue for an extended period of time.

- Transitioning between the 7 VIX Zones: Each and every one of these specific VIX zone levels is important.

1. Extreme low: <16

2. Low: 16 to 20

3. Normal: 20 to 24

4. Medium: 24 to 28

5. Med-High: 28 to 32

6. High: 32 to 36

7. Extreme high: >36

- These VIX levels in particular measure volatility changes that have a major impact on switching between smaller time frames and measuring depths of a sell move and vice versa. Each level also behaves as its own support & resistance level in terms of taking a bit of effort to switch regimes, and aids in identifying and measuring the potential depth of pullbacks in bull markets and bounces in bear markets to reveal reversal points.

- Examples of VIX level supports depicted on the chart marked with arrows. From left to right:

1. March 10th: Markets jumped 2 volatility levels in 2 days. The fluctuations from blue to yellow to green where a sign that price action would reverse from the selloff.

2. March 28th: As soon as we move from green to the blue VIX level (<20), markets began to rally and only ended when the volatility level moved sub VIX 16 (white).

3. May 4th & 24th: Next we see the 2 dips where volatility levels went from blue to green (VIX > 20), marked bottoms and reversed higher.

4. June 1st: We see a change in VIX regime yet again into lower VIX level and markets rocket higher.

Knowing the current VIX regime is a very important tool and aid in trading, now easily visualized.

BankNifty targets using VIX Version 2Original Idea Credit: Verified Market Waves

Hi,

After watching different videos online on how to get targets of BankNifty & Nifty decided to write this small script using VIX.

Nothing great but I really like the concept of getting high and low targets for the day or weekly or monthly or yearly.

What does the script do

1. We get closing of India Vix & BankNifty and Nifty

2. We get square root of Daily (365 days) | Weekly (52) | Monthly (12) & Yearly (1)

3. We divide India Vix closing with different square root to get a decimal value.

4. We use the derived value from step 3 which is used as % to calculate high and low values on BankNifty close price.

Small explanation via below screen shot to understand how to use it.

As always it comes with source code so you can modify as per your requirement.

Hope it helps 👍

Historical VolatilityThis script calculates the historical volatility of a given market using the standard deviation of its returns over a specified lookback period.

The indicator also includes a volatility Simple Moving Average (SMA), a VIX SMA, and the VIX index as reference market.

The script uses the inputs from the user to adjust the calculation, such as lookback period, volatility SMA period, and reference market.

The Historical Volatility indicator can be a useful tool for traders and investors who want to measure the degree of variation of a market's price over time, which can help them to better understand market trends and potential risks. This script is licensed under the Mozilla Public License 2.0, which means that it can be used, modified, and distributed under the terms of this license.

LNL Simple Hedging ToolLNL Simple Hedging Tool

Simple Hedging Tool was created specifically for swing traders who struggle with hedging. This tool helps to spot the ideal moments to put the hedges on (protection of the portfolio during "high risk" times). Simple Hedging Tool will not help you when day trading. It was designed for the daily charts. It is called simple because it is pretty much self-explanatory indicator. The candles are either blue or yellow. Meaning of the colors depend on the version you are using. This tool consist of two versions:

SPX Version:

This version was designed for indexes & overall market benchmarks. In contrast with the VIX version, the SPX version is little more sophisticated since it is based on key market internals. Blue arrows above the candles? More often than not this is signalizing that the key market internals are now approaching bearish signals which means it is the best time to hedge any bullish positions. On the contrary, the yellow arrows are the good reason to lighten up of the shorts & ease off the gas pedal on any bearish outlooks.

VIX Version:

Apart from the black swan events (big market crashes) Vix usually oscillates between the daily extremes. The VIX version is based on a simple bollinger band technique which is visualized with blue & yellow arrows. Whenever the yellow arrows & candles appear, it is good time to put the hedges on & perhaps lighten up on longs.

IMPORTANT DISCLAIMER:

The signals from this tool WILL NOT TELL YOU where to buy or sell! But rather when is a good time TO NOT buy or TO NOT sell. Once the signals appear it does not necessarily mean that the move is over & reversion willl happen immidiately. These signals can be flashing for days even weeks. They are not flashing for you to change the bias but rather tighten up your exposure in case your portfolio is mostly one sided.

Hope it helps.

Volatility Spike EstimatorPlots the Average True Range (ATR), its historical mean, the upper threshold for a volatility spike, and uses background color to show the likelihood of a volatility spike based on the current ATR value.

Green background indicates an increased likelihood of a volatility spike, while red background means a spike might have already occurred or be in progress.

Update: In this version, we added a short-term ATR calculation with an adjustable input parameter, shortTermATRLength. The likelihood of a volatility spike is now estimated based on the short-term ATR instead of the original ATR. This change makes the indicator more sensitive to recent market conditions and can help detect potential volatility spikes more quickly.