OPEN-SOURCE SCRIPT

已更新 Linear Mean Reversion Strategy

📘 Strategy Introduction: Linear Mean Reversion with Fixed Stop

This strategy implements a simple yet powerful mean reversion model that assumes price tends to oscillate around a dynamic average over time. It identifies statistically significant deviations from the moving average using a z-score, and enters trades expecting a return to the mean.

🧠 Core Logic:

A z-score is calculated by comparing the current price to its moving average, normalized by standard deviation, over a user-defined half-life window.

Trades are entered when the z-score crosses a threshold (e.g., ±1), signaling overbought or oversold conditions.

The strategy exits positions either when price reverts back near the mean (z-score close to 0), or if a fixed stop loss of 100 points is hit, whichever comes first.

⚙️ Key Features:

Dynamic mean and volatility estimation using moving average and standard deviation

Configurable z-score thresholds for entry and exit

Position size scaling based on z-score magnitude

Fixed stop loss to control risk and avoid prolonged drawdowns

🧪 Use Case:

Ideal for range-bound markets or assets that exhibit stationary behavior around a mean, this strategy is especially useful on assets with mean-reverting characteristics like currency pairs, ETFs, or large-cap stocks. It is best suited for traders looking for short-term reversions rather than long-term trends.

This strategy implements a simple yet powerful mean reversion model that assumes price tends to oscillate around a dynamic average over time. It identifies statistically significant deviations from the moving average using a z-score, and enters trades expecting a return to the mean.

🧠 Core Logic:

A z-score is calculated by comparing the current price to its moving average, normalized by standard deviation, over a user-defined half-life window.

Trades are entered when the z-score crosses a threshold (e.g., ±1), signaling overbought or oversold conditions.

The strategy exits positions either when price reverts back near the mean (z-score close to 0), or if a fixed stop loss of 100 points is hit, whichever comes first.

⚙️ Key Features:

Dynamic mean and volatility estimation using moving average and standard deviation

Configurable z-score thresholds for entry and exit

Position size scaling based on z-score magnitude

Fixed stop loss to control risk and avoid prolonged drawdowns

🧪 Use Case:

Ideal for range-bound markets or assets that exhibit stationary behavior around a mean, this strategy is especially useful on assets with mean-reverting characteristics like currency pairs, ETFs, or large-cap stocks. It is best suited for traders looking for short-term reversions rather than long-term trends.

發行說明

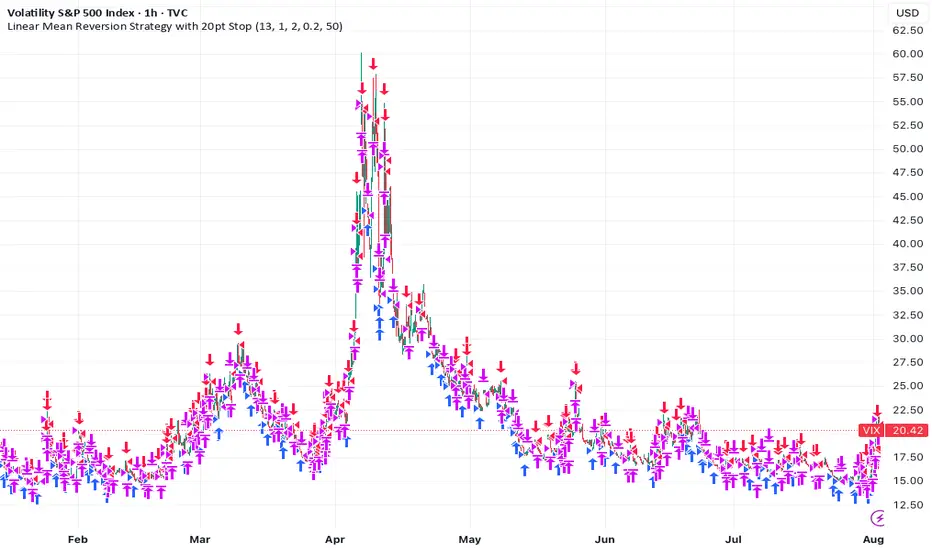

The idea is simple: if an instrument’s price is truly mean-reverting, we can expect it to return to its long-term average. Most assets, however, behave more like random walks and show little tendency to revert. The VIX—an index of S&P 500 volatility—is a notable exception, exhibiting clear mean-reversion.

For this strategy, I’ve assumed a trading cost of 0.1%, which seems reasonable given the typical bid-ask spread on the VIX is about 0.18 points.

A z-score is calculated by comparing the current price to its moving average, normalized by standard deviation, over a user-defined half-life window.

Trades are entered when the z-score crosses a threshold (e.g., ±1), signaling overbought or oversold conditions.

The strategy exits positions either when price reverts back near the mean (z-score close to 0), or if a fixed stop loss is hit, whichever comes first.

Designed for a 1 H window, where the VIX’s mean reversion and assumed costs tend to align well.

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。