OPEN-SOURCE SCRIPT

CHAN CRYPTO RS

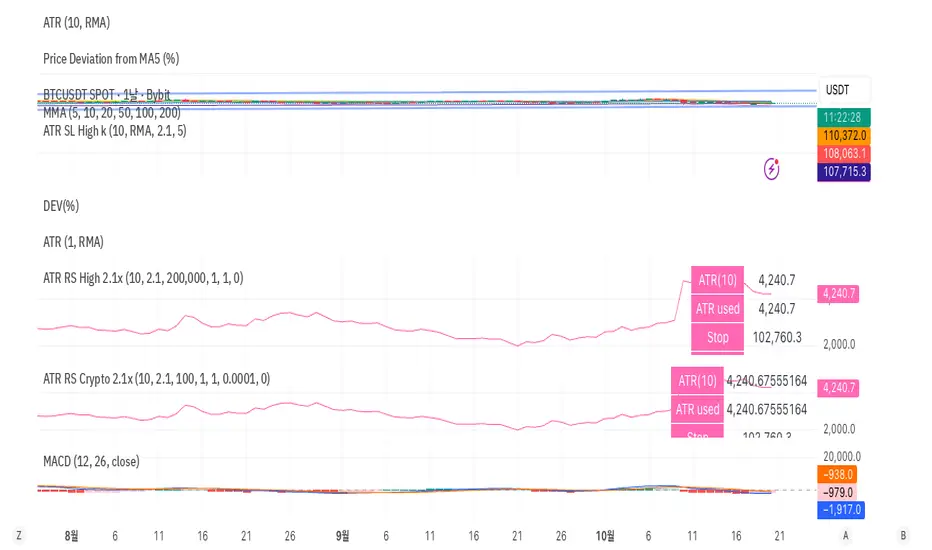

🩷 ATR RS (Crypto / High-based 2.1x, Decimal Safe v2)

This indicator is designed for crypto position sizing and stop calculation using ATR-based risk management. It helps traders automatically determine the stop price, per-unit risk, and optimal position size based on a fixed risk amount in USDT.

🔧 Core Logic

ATR Length (Daily RMA) — calculates the daily Average True Range (ATR) using RMA smoothing.

ATR Multiplier (2.1× default) — defines how far the stop is placed from the daily high.

Stop Price (for Longs) = Daily High − ATR × Multiplier

Per-Unit Risk = (Entry − Stop) × Point Value

Position Size = Risk Amount ÷ Per-Unit Risk

Automatically handles decimal precision for micro-priced crypto assets (e.g., PEPE, SHIB).

Includes safeguards for minimum size and maximum position caps.

💡 Features

Uses Daily ATR without lookahead (no repainting).

Dynamically switches between current and previous ATR for stable results when the daily bar isn’t yet confirmed.

“Snap to tick” ensures stop prices align with the symbol’s tick size.

Table display summarizes ATR, stop price, per-unit risk, total risk, size, and bet amount.

Optional stop label on the chart for visual clarity.

🧮 Output Table

Metric Description

ATR(10) Daily RMA-based ATR

ATR used Chosen ATR (current or previous)

Stop Calculated stop price

Per-unit Risk per coin/unit

Risk Total risk in USDT

Size Optimal position size

Bet Total position value (Entry × Size)

🧠 Ideal For

Crypto traders who use fixed-risk ATR strategies and need precise, decimal-safe position sizing even for ultra-low-priced tokens.

This indicator is designed for crypto position sizing and stop calculation using ATR-based risk management. It helps traders automatically determine the stop price, per-unit risk, and optimal position size based on a fixed risk amount in USDT.

🔧 Core Logic

ATR Length (Daily RMA) — calculates the daily Average True Range (ATR) using RMA smoothing.

ATR Multiplier (2.1× default) — defines how far the stop is placed from the daily high.

Stop Price (for Longs) = Daily High − ATR × Multiplier

Per-Unit Risk = (Entry − Stop) × Point Value

Position Size = Risk Amount ÷ Per-Unit Risk

Automatically handles decimal precision for micro-priced crypto assets (e.g., PEPE, SHIB).

Includes safeguards for minimum size and maximum position caps.

💡 Features

Uses Daily ATR without lookahead (no repainting).

Dynamically switches between current and previous ATR for stable results when the daily bar isn’t yet confirmed.

“Snap to tick” ensures stop prices align with the symbol’s tick size.

Table display summarizes ATR, stop price, per-unit risk, total risk, size, and bet amount.

Optional stop label on the chart for visual clarity.

🧮 Output Table

Metric Description

ATR(10) Daily RMA-based ATR

ATR used Chosen ATR (current or previous)

Stop Calculated stop price

Per-unit Risk per coin/unit

Risk Total risk in USDT

Size Optimal position size

Bet Total position value (Entry × Size)

🧠 Ideal For

Crypto traders who use fixed-risk ATR strategies and need precise, decimal-safe position sizing even for ultra-low-priced tokens.

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。