INVITE-ONLY SCRIPT

已更新 Moving Average Smoothness Benchmark

Hey there!

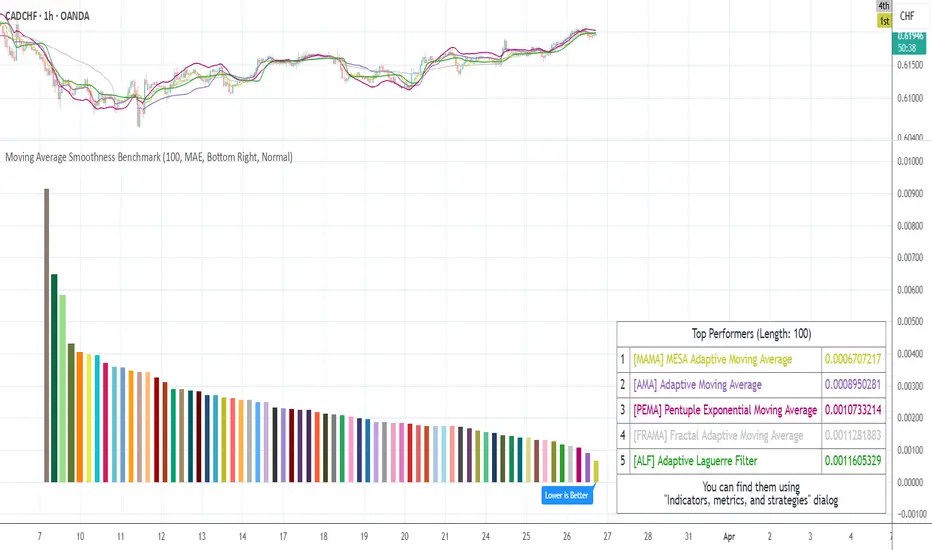

This tool will help you to choose a moving average/filter that has the lowest lag throughout the whole history for the specified period.

What does it do?

It calculates the mean absolute errors for each moving average or filter and shows histogram with results. The lower error the lower lag of the moving average.

So, the best average will be at the end of the list of labels on the chart.

Settings

The main setting is a period for all moving averages.

Additionally, it allows to customize some multi-parametric moving average such as JMA, ALMA, McGinley Dynamic, Tillson's T3, REMA, Adaptive Laguerre Filter, Hampel Filter, Recursive Median Filter and Middle-High-Low MA.

NOTE: The results may vary on the different tickers and timeframes. This tool measures the performances on the current ticker and on the current timeframe.

Supported averages/filters (use short titles to match movings on the chart)

Good luck and Merry Christmas!

This tool will help you to choose a moving average/filter that has the lowest lag throughout the whole history for the specified period.

What does it do?

It calculates the mean absolute errors for each moving average or filter and shows histogram with results. The lower error the lower lag of the moving average.

So, the best average will be at the end of the list of labels on the chart.

Settings

The main setting is a period for all moving averages.

Additionally, it allows to customize some multi-parametric moving average such as JMA, ALMA, McGinley Dynamic, Tillson's T3, REMA, Adaptive Laguerre Filter, Hampel Filter, Recursive Median Filter and Middle-High-Low MA.

NOTE: The results may vary on the different tickers and timeframes. This tool measures the performances on the current ticker and on the current timeframe.

Supported averages/filters (use short titles to match movings on the chart)

- SMA, Simple MA

- EMA, Exponential MA

- WMA, Weighted (Linear) MA

- RMA, Running MA (by J. Welles Wilder)

- VWMA, Volume Weighted MA (by Buff P. Dormeier)

- AHMA, Ahrens MA (by Richard D. Ahrens)

- ALMA, Arnaud Legoux MA (by Arnaud Legoux and Dimitris Kouzis-Loukas)

- ALF, Adaptive Laguerre Filter (by John F. Ehlers)

- ARSI, Adaptive RSI

- DEMA, Double Exponential MA (by Patrick G. Mulloy)

- EDCF, Ehlers Distance Coefficient Filter (by John F. Ehlers)

- EVWMA, Elastic Volume Weighted MA (by Christian P. Fries)

- FRAMA, Fractal Adaptive MA (by John F. Ehlers)

- HFSMA, Hampel Filter on Simple Moving Average

- HFEMA, Hampel Filter on Exponential Moving Average

- HMA, Hull MA (by Alan Hull)

- HWMA, Henderson Weighted MA (by Robert Henderson)

- IIRF, Infinite Impulse Response Filter (by John F. Ehlers)

- JMA1, Jurik MA with power of 1 (by Mark Jurik)

- JMA2, Jurik MA with power of 2 (by Mark Jurik)

- JMA3, Jurik MA with power of 3 (by Mark Jurik)

- JMA4, Jurik MA with power of 4 (by Mark Jurik)

- LF, Laguerre Filter (by John F. Ehlers)

- LMA, Leo MA (by ProRealCode' user Leo)

- LSMA, Least Squares MA (Moving Linear Regression)

- MD, McGinley Dynamic (by John R. McGinley)

- MHLMA, Middle-High-Low MA (by Vitali Apirine)

- REMA, Regularized Exponential MA (by Chris Satchwell)

- RMF, Recursive Median Filter (by John F. Ehlers)

- RMTA, Recursive Moving Trend Average (by Dennis Meyers)

- SHMMA, Sharp Modified MA (by Joe Sharp)

- SWMA, Sine Weighted MA

- TEMA, Triple Exponential MA (by Patrick G. Mulloy)

- TMA, Triangular MA

- T3, (by Tim Tillson)

- VIDYA, Variable Index Dynamic Average (by Tushar S. Chande)

- ZLEMA, Zero Lag Exponential MA (by John F. Ehlers and Ric Way)

- BF2, Butterworth Filter with 2 poles

- BF3, Butterworth Filter with 3 poles

- SSF2, Super Smoother Filter with 2 poles (by John F. Ehlers)

- SSF3, Super Smoother Filter with 3 poles (by John F. Ehlers)

- GF1, Gaussian Filter with 1 pole

- GF2, Gaussian Filter with 2 poles

- GF3, Gaussian Filter with 3 poles

- GF4, Gaussian Filter with 4 poles

Good luck and Merry Christmas!

發行說明

- Added option to reboot indicator

- Added Double Weighted Moving Average (DWMA)

- Added Inverse Distance Weighted Moving Average (IDWMA)

- Added Exponential Hull Moving Average (EHMA)

- Added Parabolic Weighted Moving Average (PWMA)

- Added JMA Phase parameter

發行說明

- Added optimizations

- Added enhanced visualization - now it has more controls

New Moving Averages:

- AEMA, Adaptive Exponential MA (by Vitali Apirine)

- AMA, Adaptive MA (by Vitali Apirine)

- BAMA, Bryant Adaptive MA (by Michael R. Bryant)

- DWMA, Double Weighted MA

- EHMA, Exponential Hull MA

- IDWMA, Inverse Distance Weighted MA

- JMA, Jurik MA (by Mark Jurik https://www.tradingview.com/script/714vYiDe-Jurik-Moving-Average/)

- JAMA, Jurik Adaptive MA (by Mark Jurik)

- KAMA, Kaufman Adaptive MA (by Perry J. Kaufman)

- MNMA, McNicholl MA (by Dennis McNicholl)

- NSMA, Moving Average 3.0 on SMA (by Manfred G. Dürschner)

- NEMA, Moving Average 3.0 on EMA (by Manfred G. Dürschner)

- NWMA, Moving Average 3.0 on WMA (by Manfred G. Dürschner)

- NVWMA, Moving Average 3.0 on VWMA (by Manfred G. Dürschner)

- PEMA, Pentuple Exponential MA (by Bruno Pio)

- PWMA, Parabolic Weighted MA

- QMA, Quick MA (by John McCormick)

- QEMA, Quadruple Exponential MA (by Bruno Pio)

The total number of supported moving averages and filters is 63 now

發行說明

- Update

發行說明

- Bump Pine Script version to 4

發行說明

- Pine Script V5

- Added sorting of results for better UX

- Added comments for better UX

發行說明

- Pine Script V6

- Added table with results

- Refactoring

發行說明

- Added short names of moving averages to the table

發行說明

- Fixed table display when using dark theme

- Added customizable table border and text colors

- Bound metric formatting to the current chart's minimum tick size

僅限邀請腳本

僅作者批准的使用者才能訪問此腳本。您需要申請並獲得使用許可,通常需在付款後才能取得。更多詳情,請依照作者以下的指示操作,或直接聯絡everget。

TradingView不建議在未完全信任作者並了解其運作方式的情況下購買或使用腳本。您也可以在我們的社群腳本中找到免費的開源替代方案。

作者的說明

If you have any questions, feel free to ask them and contact me via private messages on TradingView or via Telegram @alex_everget

👨🏻💻 Coding services -> Telegram: @alex_everget

🆓 List of my FREE indicators: bit.ly/2S7EPuN

💰 List of my PREMIUM indicators: bit.ly/33MA81f

Join Bybit and get up to $6,045 in bonuses!

bybit.com/invite?ref=56ZLQ0Z

🆓 List of my FREE indicators: bit.ly/2S7EPuN

💰 List of my PREMIUM indicators: bit.ly/33MA81f

Join Bybit and get up to $6,045 in bonuses!

bybit.com/invite?ref=56ZLQ0Z

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

僅限邀請腳本

僅作者批准的使用者才能訪問此腳本。您需要申請並獲得使用許可,通常需在付款後才能取得。更多詳情,請依照作者以下的指示操作,或直接聯絡everget。

TradingView不建議在未完全信任作者並了解其運作方式的情況下購買或使用腳本。您也可以在我們的社群腳本中找到免費的開源替代方案。

作者的說明

If you have any questions, feel free to ask them and contact me via private messages on TradingView or via Telegram @alex_everget

👨🏻💻 Coding services -> Telegram: @alex_everget

🆓 List of my FREE indicators: bit.ly/2S7EPuN

💰 List of my PREMIUM indicators: bit.ly/33MA81f

Join Bybit and get up to $6,045 in bonuses!

bybit.com/invite?ref=56ZLQ0Z

🆓 List of my FREE indicators: bit.ly/2S7EPuN

💰 List of my PREMIUM indicators: bit.ly/33MA81f

Join Bybit and get up to $6,045 in bonuses!

bybit.com/invite?ref=56ZLQ0Z

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。