ATR Bands over 50D SMA (% method)Indicator that shows multiples of ATR% above the 50d SMA as bands on a chart, building off of

Jeff Sun 's methodology. You should tinker with the settings to chose your multiples, colors and which multiple lines to show. I don't know if the negative multiple lines have any use, so I turn mine off. Offered as is. I am not a programmer. Note the other indicators shown on the print screen are not mine.

ATR

Average True Range TrackerThis indicator calculates the daily ATR of the past 14 days. The ATR% indicates the range completed for the day. The ATR indicates the average daily range. The 20% ATR indicates the value of 20% of the daily ATR for retracement purposes.

Daily ATR TrackerThis indicator calculates the daily ATR of the past 14 days. The ATR% indicates the range completed for the day. The ATR indicates the average daily range. The 20% ATR indicates the value of 20% of the daily ATR for retracement purposes.

BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

ATR Enhanced [DCAUT]█ ATR Enhanced

📊 OVERVIEW

Standard ATR uses only RMA smoothing, while ATR Enhanced provides 20+ professional smoothing algorithms , offering precise volatility measurement solutions for different trading scenarios and market environments.

💡 CORE VALUE

- 20+ algorithm choices : SMA, EMA, RMA, WMA, HMA, T3, KAMA, FRAMA, Kalman Filter, etc.

📋 PARAMETER SETUP

ATR Length : Calculation period (default: 14)

Moving Average Type : Choose the most suitable smoothing method from 20+ algorithms

🎨 COLOR CODING

Green : Rising volatility

Red : Falling volatility

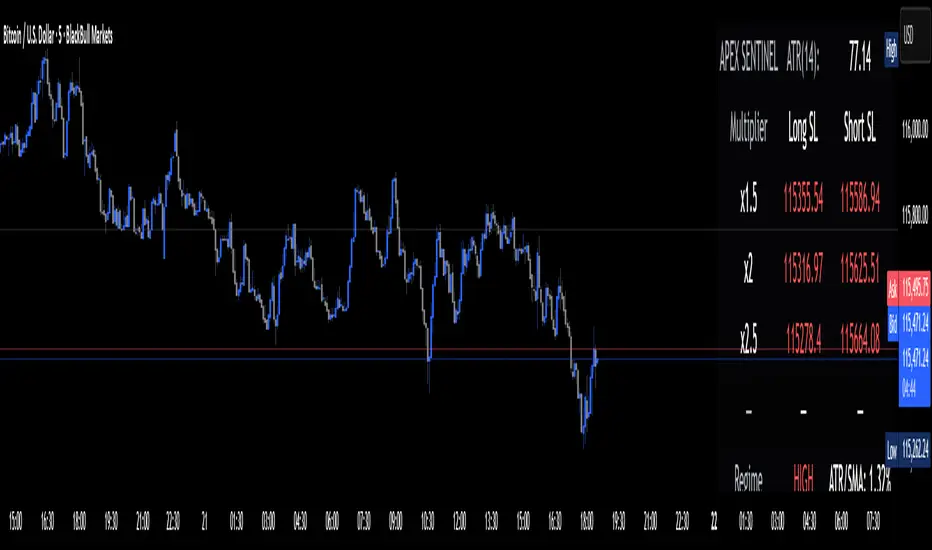

Apex Edge Sentinel - Stop Loss HUDApex Edge – ATR Sentinel Stop Loss HUD

The Apex Edge – ATR Sentinel is a complete stop-loss intelligence system built as a clean, always-on HUD.

It delivers institutional-level risk guidance by calculating and displaying live ATR-based stop levels for both long and short trades at multiple risk tolerances.

Forget cluttered charts and repainting lines — Sentinel gives you a clear stop-loss reference panel that updates dynamically with every bar.

✅ Features

• Triple ATR Multipliers

User-defined (e.g. x1.5 / x2.0 / x2.5). Compare tight, medium, and wide stops instantly.

• Dual-Side SL Levels

Both Long and Short safe stop prices displayed side by side. No more guessing trend

bias.

• ATR Transparency

HUD shows ATR(length) so you always know the calculation basis. Default = 14, adjustable

to your style.

• ATR Regime Meter

Detects volatility conditions (LOW / NORMAL / HIGH) by comparing ATR to its SMA. Helps

you avoid over-tight stops in high-volatility markets.

• Tick-Aware Rounding

Stop levels auto-rounded to the instrument’s tick size (Gold = 0.10, FX = 0.0001, indices =

whole points).

Custom HUD Design

• Location: Top/Bottom, Left/Right

• Sizes: Compact / Medium / Large (desktop or mobile)

• Opacity control (25% default Apex styling)

How to Use

1. Load Sentinel on your chart.

2. Check the HUD:

• ATR(14): 2.6 → base volatility measure.

• x1.5 / x2.0 / x2.5 → instant SL levels for both long & short trades.

3. Before entering a trade → decide which multiplier matches your style (tight scalper vs wider swing).

4. Manually place your SL at the level displayed in the HUD.

Sentinel works as both:

• A pre-trade check (is ATR stop too wide for my RR?).

• A live risk compass (updated stop levels every bar).

Why Apex Sentinel?

Most ATR stop indicators clutter charts with lagging lines or repainting trails. Sentinel strips it back to what matters:

• The numbers.

• The risk levels.

• The context.

It’s a pure stop-loss HUD, designed for serious traders who want clarity, discipline, and instant reference points across any market or timeframe.

Notes

• This is a HUD-only system (no automatic SL line). Traders manually apply the SL level

shown in the panel.

• Defaults: ATR(14), multipliers 1.5 / 2.0 / 2.5. Adjust to your trading style.

• Best used on intraday pairs like XAUUSD, EURUSD, indices, but works universally.

Apex Edge Philosophy: Clean. Smart. Institutional.

No clutter. No gimmicks. Just precision tools for modern markets.

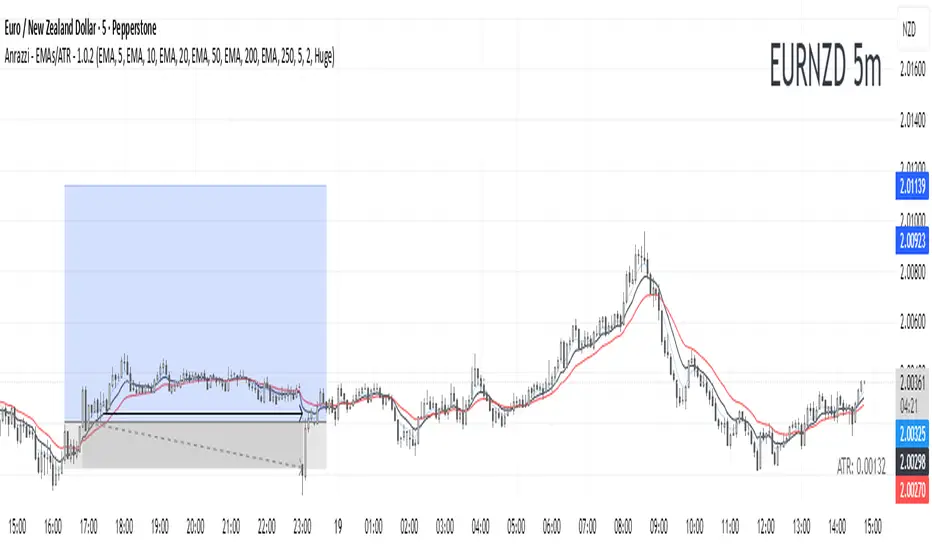

Anrazzi - EMAs/ATR - 1.0.2The Anrazzi – EMAs/ATR indicator is a multi-purpose overlay designed to help traders track trend direction and market volatility in a single clean tool.

It plots up to six customizable moving averages (MAs) and an Average True Range (ATR) value directly on your chart, allowing you to quickly identify market bias, dynamic support/resistance, and volatility levels without switching indicators.

This script is ideal for traders who want a simple, configurable, and efficient way to combine trend-following signals with volatility-based position sizing.

📌 Key Features

Six Moving Averages (MA1 → MA6)

Toggle each MA on/off individually

Choose between EMA or SMA for each

Customize length and color

Perfect for spotting trend direction and pullback zones

ATR Display

Uses Wilder’s ATR formula (ta.rma(ta.tr(true), 14))

Can be calculated on current or higher timeframe

Adjustable multiplier for position sizing (e.g., 1.5× ATR stops)

Displays cleanly in the bottom-right corner

Custom Watermark

Displays symbol + timeframe in top-right

Adjustable color and size for streamers, screenshots, or clear charting

Compact UI

Organized with group and inline inputs for quick configuration

Lightweight and optimized for real-time performance

⚙️ How It Works

MAs: The script uses either ta.ema() or ta.sma() to compute each moving average based on the user-selected type and length.

ATR: The ATR is calculated using ta.rma(ta.tr(true), 14) (Wilder’s smoothing), and optionally scaled by a multiplier for easier use in risk management.

Tables: ATR value and watermark are displayed using table.new() so they stay anchored to the screen regardless of zoom level.

📈 How to Use

Enable the MAs you want to track and adjust their lengths, type, and colors.

Enable ATR if you want to see volatility — optionally select a higher timeframe for broader context.

Use MAs to:

Identify overall trend direction (e.g. price above MA20 = bullish)

Spot pullback zones for entries

See when multiple MAs cluster together as support/resistance zones

Use ATR value to:

Size your stop-loss dynamically (e.g. stop = entry − 1.5×ATR)

Detect volatility breakouts (ATR spikes = market expansion)

🎯 Recommended For

Day traders & swing traders

Trend-following & momentum strategies

Volatility-based risk management

Traders who want a clean, all-in-one dashboard

Anrazzi - EMAs/ATR - 1.0.2Description:

The Anrazzi - EMAs/ATR indicator is a versatile tool for technical traders looking to monitor multiple moving averages alongside the Average True Range (ATR) on any chart. Designed for simplicity and customization, it allows traders to visualize up to six moving averages with configurable type, color, and length, while keeping real-time volatility information via ATR directly on the chart.

This indicator is perfect for spotting trends, identifying support/resistance zones, and gauging market volatility for intraday or swing trading strategies.

Key Features:

Supports up to six independent moving averages (MA1 → MA6)

Each MA is fully customizable:

Enable/disable individually

Type: EMA or SMA

Length

Color

ATR Display:

Custom timeframe

Color and position configurable

Adjustable multiplier

Compact and organized settings for easy configuration

Lightweight and efficient code for smooth chart performance

Watermark

Inputs / Settings:

MA Options: MA1 → MA6 (Enable/Disable, Type, Length, Color)

Additional Settings: ATR (Enable, Timeframe, Color, Multiplier)

How to Use:

Enable the moving averages you want to track

Configure type, length, and color for each MA

Enable ATR if needed and adjust settings

Watch MAs plotted dynamically and ATR in bottom-right corner

Recommended For:

Day traders and swing traders

Trend-following strategies

Volatility analysis and breakout detection

Traders needing a compact multi-MA dashboard

Omega ATR Indicator📖 Introduction

The Ω ATR Indicator was created to provide a more complete and professional framework for volatility analysis than the classic Average True Range (ATR).

While the traditional ATR is a useful tool, it has limitations: it delivers a simple rolling average of volatility, but it does not adapt to market regimes, it does not highlight extreme events, and it often leaves the trader with incomplete information about risk.

The Ω ATR takes the same foundation and elevates it into a multi-dimensional volatility dashboard, adding statistical layers, adaptive calculations, and clear visual references that allow traders to interpret volatility in a way that is immediately actionable.

🔎 What makes it different from a standard ATR?

This indicator introduces several features beyond the classic formula:

True Range Core – plots the raw True Range (TR) for each bar, providing a direct, bar-by-bar view of volatility impulses.

Standard & Adjusted ATR – includes both the conventional ATR (smoothed average) and an Adjusted ATR that automatically corrects for extreme conditions by incorporating percentile rescaling.

Percentile Volatility Levels – dynamically calculated extreme thresholds (99.8%, 75%, 50%, 25%), plotted as dotted levels across the chart. These act as reference lines for “normal” vs. “abnormal” volatility, useful for spotting unusual price expansions or contractions.

Linear Regression Volatility Trend – overlays a regression line of volatility, showing whether the market is moving toward expansion (rising vol), contraction (falling vol), or stability.

Monetary Value Translation – the indicator converts volatility into points, ticks, and dollar values (based on the instrument’s point value). This allows futures traders and high-value instruments users to immediately see how much volatility is “worth” in cash terms.

Interactive Table Display – a real-time statistics table is displayed directly on the chart, showing:

SMA of ATR in $ and points

Percentile-based volatility range (VAR) in $ and points

Tick equivalences, for quick position sizing

⚡ How traders can use it

The Ω ATR Indicator is designed to be versatile, fitting both discretionary traders and systematic strategy developers.

Risk Management: ATR-based stop losses and position sizing are significantly improved by using the adjusted ATR and percentile thresholds. Traders can size their positions according to volatility regimes, not just raw averages.

Breakout & Exhaustion Detection: When TR or ATR values spike above the 99.8% or 95% percentile levels, this often corresponds to breakout conditions or volatility exhaustion — useful for breakout strategies, mean-reversion setups, and volatility fades.

Market Regime Identification: The regression line helps distinguish if volatility is rising (trending environment, larger swings expected) or compressing (range-bound environment, lower risk opportunities).

Multi-Asset Flexibility: Works equally well on equities, futures, crypto, and FX. Its point/tick/dollar conversion makes it especially powerful for futures traders who need to quantify risk precisely.

Scalping to Swing Trading: On lower timeframes, it acts as a micro-volatility detector; on higher timeframes, it functions as a strategic risk gauge for position management.

⚙️ Settings and Customization

Length: The ATR lookback period (default = 34).

Shorter lengths (14–21) for intraday traders who want fast response.

Longer lengths (34–55) for swing/position traders who want smoother readings.

AVG / ADJ AVG: Toggle to display the standard ATR or the adjusted ATR.

Volatility Levels: Enable/disable up to 4 percentile-based levels (1st = 25%, 2nd = 50%, 3rd = 75%, 4th = 99.8%). Recommended: keep 3 levels active for clarity.

Color Controls: All plots and levels are fully customizable to match your chart style.

Table Display: Positioned on the chart (default: middle-right) with key values updated in real time.

🧭 Best Practices for Use

Combine with Trend Tools: Volatility readings are most powerful when combined with trend filters or volume analysis. For example, a breakout with both high volatility and trend confirmation is stronger than either alone.

ATR Stops: Use the Adjusted ATR rather than the standard one when trailing stops in highly volatile instruments like crypto or Nasdaq futures, as it adapts to outlier spikes.

Dollar Risk Translation: Use the dollar-value outputs to predefine maximum acceptable risk per trade (e.g., “I only risk $250 per position”). This bridges volatility to portfolio risk management.

Event Monitoring: Around economic events or earnings, expect volatility spikes above higher percentile levels. The indicator makes these moves instantly visible.

📌 Summary

The Ω ATR Indicator is not just “another ATR.” It is a comprehensive volatility framework that transforms volatility from a simple statistic into an actionable trading signal.

By combining:

the classic ATR,

an adjusted ATR,

percentile extremes,

regression-based volatility trends,

and real-time dollar conversions,

…this tool allows traders to precisely understand, visualize, and act on volatility in ways that a standard ATR simply cannot provide.

Whether you are scalping intraday moves, swing trading equities, or managing futures positions, the Ω ATR equips you with a professional-grade volatility dashboard that clarifies risk, highlights opportunity, and adapts across all markets and timeframes.

👉 Designed and developed by OmegaTools for traders who demand precision, clarity, and adaptability in their volatility analysis.

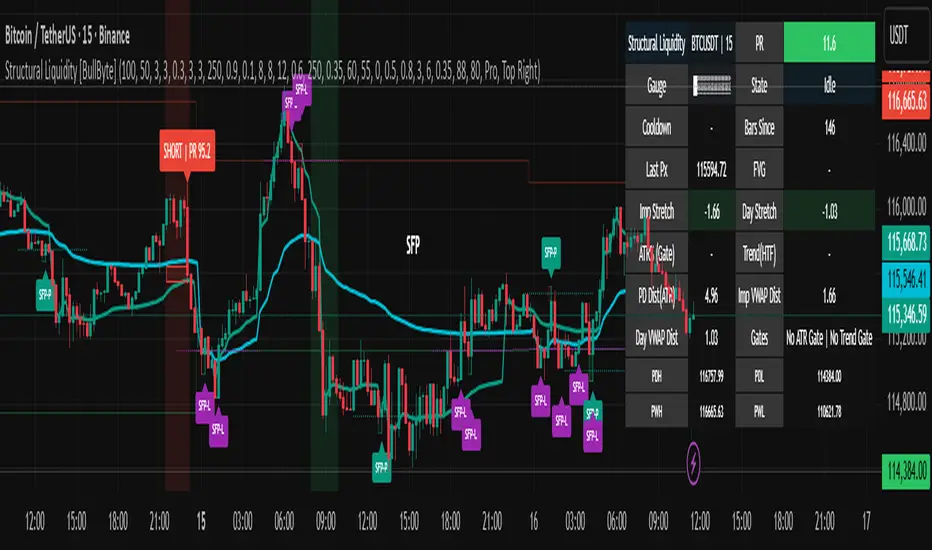

Structural Liquidity Signals [BullByte]Structural Liquidity Signals (SFP, FVG, BOS, AVWAP)

Short description

Detects liquidity sweeps (SFPs) at pivots and PD/W levels, highlights the latest FVG, tracks AVWAP stretch, arms percentile extremes, and triggers after confirmed micro BOS.

Full description

What this tool does

Structural Liquidity Signals shows where price likely tapped liquidity (stop clusters), then waits for structure to actually change before it prints a trigger. It spots:

Liquidity sweeps (SFPs) at recent pivots and at prior day/week highs/lows.

The latest Fair Value Gap (FVG) that often “pulls” price or serves as a reaction zone.

How far price is stretched from two VWAP anchors (one from the latest impulse, one from today’s session), scaled by ATR so it adapts to volatility.

A “percentile” extreme of an internal score. At extremes the script “arms” a setup; it only triggers after a small break of structure (BOS) on a closed bar.

Originality and design rationale, why it’s not “just a mashup”

This is not a mashup for its own sake. It’s a purpose-built flow that links where liquidity is likely to rest with how structure actually changes:

- Liquidity location: We focus on areas where stops commonly cluster—recent pivots and prior day/week highs/lows—then detect sweeps (SFPs) when price wicks beyond and closes back inside.

- Displacement context: We track the last Fair Value Gap (FVG) to account for recent inefficiency that often acts as a magnet or reaction zone.

- Stretch measurement: We anchor VWAP to the latest N-bar impulse and to the Daily session, then normalize stretch by ATR to assess dislocation consistently across assets/timeframes.

- Composite exhaustion: We combine stretch, wick skew, and volume surprise, then bend the result with a tanh transform so extremes are bounded and comparable.

- Dynamic extremes and discipline: Rather than triggering on every sweep, we “arm” at statistical extremes via percent-rank and only fire after a confirmed micro Break of Structure (BOS). This separates “interesting” from “actionable.”

Key concepts

SFP (liquidity sweep): A candle briefly trades beyond a level (where stops sit) and closes back inside. We detect these at:

Pivots (recent swing highs/lows confirmed by “left/right” bars).

Prior Day/Week High/Low (PDH/PDL/PWH/PWL).

FVG (Fair Value Gap): A small 3‑bar gap (bar2 high vs bar1 low, or vice versa). The latest gap often acts like a magnet or reaction zone. We track the most recent Up/Down gap and whether price is inside it.

AVWAP stretch: Distance from an Anchored VWAP divided by ATR (volatility). We use:

Impulse AVWAP: resets on each new N‑bar high/low.

Daily AVWAP: resets each new session.

PR (Percentile Rank): Where the current internal score sits versus its own recent history (0..100). We arm shorts at high PR, longs at low PR.

Micro BOS: A small break of the recent high (for longs) or low (for shorts). This is the “go/no‑go” confirmation.

How the parts work together

Find likely liquidity grabs (SFPs) at pivots and PD/W levels.

Add context from the latest FVG and AVWAP stretch (how far price is from “fair”).

Build a bounded score (so different markets/timeframes are comparable) and compute its percentile (PR).

Arm at extremes (high PR → short candidate; low PR → long candidate).

Only print a trigger after a micro BOS, on a closed bar, with spacing/cooldown rules.

What you see on the chart (legend)

Lines:

Teal line = Impulse AVWAP (resets on new N‑bar extreme).

Aqua line = Daily AVWAP (resets each session).

PDH/PDL/PWH/PWL = prior day/week levels (toggle on/off).

Zones:

Greenish box = latest Up FVG; Reddish box = latest Down FVG.

The shading/border changes after price trades back through it.

SFP labels:

SFP‑P = SFP at Pivot (dotted line marks that pivot’s price).

SFP‑L = SFP at Level (at PDH/PDL/PWH/PWL).

Throttle: To reduce clutter, SFPs are rate‑limited per direction.

Triggers:

Triangle up = long trigger after BOS; triangle down = short trigger after BOS.

Optional badge shows direction and PR at the moment of trigger.

Optional Trigger Zone is an ATR‑sized box around the trigger bar’s close (for visualization only).

Background:

Light green/red shading = a long/short setup is “armed” (not a trigger).

Dashboard (Mini/Pro) — what each item means

PR: Percentile of the internal score (0..100). Near 0 = bullish extreme, near 100 = bearish extreme.

Gauge: Text bar that mirrors PR.

State: Idle, Armed Long (with a countdown), or Armed Short.

Cooldown: Bars remaining before a new setup can arm after a trigger.

Bars Since / Last Px: How long since last trigger and its price.

FVG: Whether price is in the latest Up/Down FVG.

Imp/Day VWAP Dist, PD Dist(ATR): Distance from those references in ATR units.

ATR% (Gate), Trend(HTF): Status of optional regime filters (volatility/trend).

How to use it (step‑by‑step)

Keep the Safety toggles ON (default): triggers/visuals on bar‑close, optional confirmed HTF for trend slope.

Choose timeframe:

Intraday (5m–1h) or Swing (1h–4h). On very fast/thin charts, enable Performance mode and raise spacing/cooldown.

Watch the dashboard:

When PR reaches an extreme and an SFP context is present, the background shades (armed).

Wait for the trigger triangle:

It prints only after a micro BOS on a closed bar and after spacing/cooldown checks.

Use the Trigger Zone box as a visual reference only:

This script never tells you to buy/sell. Apply your own plan for entry, stop, and sizing.

Example:

Bullish: Sweep under PDL (SFP‑L) and reclaim; PR in lower tail arms long; BOS up confirms → long trigger on bar close (ATR-sized trigger zone shown).

Bearish: Sweep above PDH/pivot (SFP‑L/P) and reject; PR in upper tail arms short; BOS down confirms → short trigger on bar close (ATR-sized trigger zone shown).

Settings guide (with “when to adjust”)

Safety & Stability (defaults ON)

Confirm triggers at bar close, Draw visuals at bar close: Keep ON for clean, stable prints.

Use confirmed HTF values: Applies to HTF trend slope only; keeps it from changing until the HTF bar closes.

Performance mode: Turn ON if your chart is busy or laggy.

Core & Context

ATR Length: Bigger = smoother distances; smaller = more reactive.

Impulse AVWAP Anchor: Larger = fewer resets; smaller = resets more often.

Show Daily AVWAP: ON if you want session context.

Use last FVG in logic: ON to include FVG context in arming/score.

Show PDH/PDL/PWH/PWL: ON to see prior day/week levels that often attract sweeps.

Liquidity & Microstructure

Pivot Left/Right: Higher values = stronger/rarer pivots.

Min Wick Ratio (0..1): Higher = only more pronounced SFP wicks qualify.

BOS length: Larger = stricter BOS; smaller = quicker confirmations.

Signal persistence: Keeps SFP context alive for a few bars to avoid flicker.

Signal Gating

Percent‑Rank Lookback: Larger = more stable extremes; smaller = more reactive extremes.

Arm thresholds (qHi/qLo): Move closer to 0.5 to see more arms; move toward 0/1 to see fewer arms.

TTL, Cooldown, Min bars and Min ATR distance: Space out triggers so you’re not reacting to minor noise.

Regime Filters (optional)

ATR percentile gate: Only allow triggers when volatility is at/above a set percentile.

HTF trend gate: Only allow longs when the HTF slope is up (and shorts when it’s down), above a minimum slope.

Visuals & UX

Only show “important” SFPs: Filters pivot SFPs by Volume Z and |Impulse stretch|.

Trigger badges/history and Max badge count: Control label clutter.

Compact labels: Toggle SFP‑P/L vs full names.

Dashboard mode and position; Dark theme.

Reading PR (the built‑in “oscillator”)

PR ~ 0–10: Potential bullish extreme (long side can arm).

PR ~ 90–100: Potential bearish extreme (short side can arm).

Important: “Armed” ≠ “Enter.” A trigger still needs a micro BOS on a closed bar and spacing/cooldown to pass.

Repainting, confirmations, and HTF notes

By default, prints wait for the bar to close; this reduces repaint‑like effects.

Pivot SFPs only appear after the pivot confirms (after the chosen “right” bars).

PD/W levels come from the prior completed candles and do not change intraday.

If you enable confirmed HTF values, the HTF slope will not change until its higher‑timeframe bar completes (safer but slightly delayed).

Performance tips

If labels/zones clutter or the chart lags:

Turn ON Performance mode.

Hide FVG or the Trigger Zone.

Reduce badge history or turn badge history off.

If price scaling looks compressed:

Keep optional “score”/“PR” plots OFF (they overlay price and can affect scaling).

Alerts (neutral)

Structural Liquidity: LONG TRIGGER

Structural Liquidity: SHORT TRIGGER

These fire when a trigger condition is met on a confirmed bar (with defaults).

Limitations and risk

Not every sweep/extreme reverses; false triggers occur, especially on thin markets and low timeframes.

This indicator does not provide entries, exits, or position sizing—use your own plan and risk control.

Educational/informational only; no financial advice.

License and credits

© BullByte - MPL 2.0. Open‑source for learning and research.

Built from repeated observations of how liquidity runs, imbalance (FVG), and distance from “fair” (AVWAPs) combine, and how a small BOS often marks the moment structure actually shifts.

Volume Profile Auto POC📌 Overview

Volume Profile Auto POC is a trend-following strategy that uses the automatically calculated Point of Control (POC) from the volume profile, combined with ATR zones, to capture reversals and breakouts.

By basing decisions on volume concentration, it dynamically visualizes the price levels most watched by market participants.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

Automatically detect the volume concentration area (POC) to improve entry accuracy

Optimize risk management through ATR-based volatility adjustment

Provide early and consistent signals when trends emerge

✨ Key Features

Automatic POC Detection : Updates the volume profile over a defined lookback window in real time

ATR Zone Integration : Defines a POC ± 0.5 ATR zone to clarify potential reversals/breakouts

Visual Support : Plots the POC line and zones on the chart for intuitive decision-making

📊 Trading Rules

Long Entry:

Price breaks above the POC + 0.5 ATR zone

Volume is above average to support the breakout

Short Entry:

Price breaks below the POC - 0.5 ATR zone

Volume is above average to support the downside move

Exit (or Reverse Position):

Price returns to the POC area

Or touches the ATR band

⚙️ Trading Parameters & Considerations

Indicator Name: Volume Profile Auto POC

Parameters:

Lookback Bars: 50

Bins for Volume Profile: 24

ATR Length: 14

ATR Multiplier: 2.0

🖼 Visual Support

POC line plotted in red

POC ± 0.5 ATR zone displayed as a semi-transparent box

ATR bands plotted in blue for confirmation

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by traditional Volume Profile + ATR analysis,

while adding the improvement of a sliding-window mechanism for automatic POC updates.

Compared with conventional trend-following approaches,

its strength lies in combining both price and volume perspectives for decision-making.

✅ Summary

Volume Profile Auto POC automatically extracts key market levels (POC) and combines them with ATR-based zones,

providing a responsive trend-following method.

It balances clarity with practicality, aiming for both usability and reproducibility.

⚠️ This strategy is based on historical data and does not guarantee future profits.

Always use proper risk management when applying it.

Kalman Adjusted Average True Range [BackQuant]Kalman Adjusted Average True Range

A volatility-aware trend baseline that fuses a Kalman price estimate with ATR “rails” to create a smooth, adaptive guide for entries, exits, and trailing risk.

Built on my original Kalman

This indicator is based on my original Kalman Price Filter:

That core smoother is used here to estimate the “true” price path, then blended with ATR to control step size and react proportionally to market noise.

What it plots

Kalman ATR Line the main baseline that turns up/down with the filtered trend.

Optional Moving Average of the Kalman ATR a secondary line for confluence (SMA/Hull/EMA/WMA/DEMA/RMA/LINREG/ALMA).

Candle Coloring (optional) paint bars by the baseline’s current direction.

Why combine Kalman + ATR?

Kalman reduces measurement noise and produces a stable path without the lag of heavy MAs.

ATR rails scale the baseline’s step to current volatility, so it’s calm in chop and more responsive in expansion.

The result is a single, intelligible line you can trade around: slope-up = constructive; slope-down = caution.

How it works (plain English)

Each bar, the Kalman filter updates an internal state (tunable via Process Noise , Measurement Noise , and Filter Order ) to estimate the underlying price.

An ATR band (Period × Factor) defines the allowed per-bar adjustment. The baseline cannot “jump” beyond those rails in one step.

A direction flip is detected when the baseline’s slope changes sign (upturn/downturn), and alerts are provided for both.

Typical uses

Trend confirmation Trade in the baseline’s direction; avoid fading a firmly rising/falling line.

Pullback timing Look for entries when price mean-reverts toward a rising baseline (or exits on tags of a falling one).

Trailing risk Use the baseline as a dynamic guide; many traders set stops a small buffer beyond it (e.g., a fraction of ATR).

Confluence Enable the MA overlay of the Kalman ATR; alignment (baseline above its MA and rising) supports continuation.

Inputs & what they do

Calculation

Kalman Price Source which price the filter tracks (Close by default).

Process Noise how quickly the filter can adapt. Higher = more responsive (but choppier).

Measurement Noise how much you distrust raw price. Higher = smoother (but slower to turn).

Filter Order (N) depth of the internal state array. Higher = slightly steadier behavior.

Kalman ATR

Period ATR lookback. Shorter = snappier; longer = steadier.

Factor scales the allowed step per bar. Larger factors permit faster drift; smaller factors clamp movement.

Confluence (optional)

MA Type & Period compute an MA on the Kalman ATR line , not on price.

Sigma (ALMA) if ALMA is selected, this input controls the curve’s shape. (Ignored for other MA types.)

Visuals

Plot Kalman ATR toggle the main line.

Paint Candles color bars by up/down slope.

Colors choose long/short hues.

Signals & alerts

Trend Up baseline turns upward (slope crosses above 0).

Alert: “Kalman ATR Trend Up”

Trend Down baseline turns downward (slope crosses below 0).

Alert: “Kalman ATR Trend Down”

These are state flips , not “price crossovers,” so you avoid many one-bar head-fakes.

How to start (fast presets)

Swing (daily/4H) ATR Period 7–14, Factor 0.5–0.8, Process Noise 0.02–0.05, Measurement Noise 2–4, N = 3–5.

Intraday (5–15m) ATR Period 5–7, Factor 0.6–1.0, Process Noise 0.05–0.10, Measurement Noise 2–3, N = 3–5.

Slow assets / FX raise Measurement Noise or ATR Period for calmer lines; drop Factor if the baseline feels too jumpy.

Reading the line

Rising & curving upward momentum building; consider long bias until a clear downturn.

Flat & choppy regime uncertainty; many traders stand aside or tighten risk.

Falling & accelerating distribution lower; short bias until a clean upturn.

Practical playbook

Continuation entries After a Trend Up alert, wait for a minor pullback toward the baseline; enter on evidence the line keeps rising.

Exit/reduce If long and the baseline flattens then turns down, trim or exit; reverse logic for shorts.

Filters Add a higher-timeframe check (e.g., only take longs when the daily Kalman ATR is rising).

Stops Place stops just beyond the baseline (e.g., baseline − x% ATR for longs) to avoid “tag & reverse” noise.

Notes

This is a guide to state and momentum, not a guarantee. Combine with your process (structure, volume, time-of-day) for decisions.

Settings are asset/timeframe dependent; start with the presets and nudge Process/Measurement Noise until the baseline “feels right” for your market.

Summary

Kalman ATR takes the noise-reduction of a Kalman price estimate and couples it with volatility-scaled movement to produce a clean, adaptive baseline. If you liked the original Kalman Price Filter (), this is its trend-trading cousin purpose-built for cleaner state flips, intuitive trailing, and confluence with your existing

Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

2ATR / Close %Certainly. Here is the English version of the indicator description you requested.

---

### **2ATR Stop-Loss Ratio**

This indicator provides a straightforward calculation of **what percentage a 2ATR (Average True Range) move represents relative to the current price**. It's a specialized tool designed to help traders set dynamic, volatility-based stop-loss levels.

---

### **Purpose of the Indicator**

Many traders use a **2ATR** as their standard for setting a stop-loss, believing it's a good measure of a stock's typical movement. However, it can be difficult to quickly determine the exact percentage a 2ATR drop represents from the current price. This indicator solves that problem by giving you a clear, single number that shows the **anticipated percentage loss before you even enter a position**.

---

### **How It Works**

The indicator is calculated using a simple formula:

**(2 * ATR(20) / Current Price) * 100**

* `ATR(20)`: The Average True Range over the last 20 periods. This period can be customized in the indicator's settings.

* `Current Price`: The closing price at the time of calculation.

---

### **How to Use It**

* **Assess Risk**: A higher number on the indicator means greater volatility, indicating a wider stop-loss range.

* **Set a Stop-Loss**: If the indicator shows **3%**, it means a 2ATR move is roughly a 3% change from the current price. This gives you a clear understanding of the potential loss.

* **Adjust Position Size**: If the potential percentage loss is larger than you're comfortable with, you can use this information to reduce your position size, effectively managing your risk.

This tool is especially useful for trading highly volatile stocks, as it helps you establish a clear and effective risk management strategy.

NY Anchored VWAP and Auto SMANY Anchored VWAP and Auto SMA

This script is a versatile trading indicator for the TradingView platform that combines two powerful components: a New York-anchored Volume-Weighted Average Price (VWAP) and a dynamic Simple Moving Average (SMA). Designed for traders who utilize VWAP for intraday trend analysis, this tool provides a clear visual representation of average price and volatility-adjusted moving averages, generating automated alerts for key crossover signals.

Indicator Components

1. NY Anchored VWAP

The VWAP is a crucial tool that represents the average price of a security adjusted for volume. This version is "anchored" to the start of the New York trading session, resetting at the beginning of each new session. This provides a clean, session-specific anchor point to gauge market sentiment and trend. The VWAP line changes color to reflect its slope:

Green: When the VWAP is trending upwards, indicating a bullish bias.

Red: When the VWAP is trending downwards, indicating a bearish bias.

2. Auto SMA

The Auto SMA is a moving average with a unique twist: its lookback period is not fixed. Instead, it dynamically adjusts based on market volatility. The script measures volatility using the Average True Range (ATR) and a Z-Score calculation.

When volatility is expanding, the SMA's length shortens, making it more sensitive to recent price changes.

When volatility is contracting, the SMA's length lengthens, smoothing out the price action to filter out noise.

This adaptive approach allows the SMA to react appropriately to different market conditions.

Suggested Trading Strategy

This indicator is particularly effective when used on a one-minute chart for identifying high-probability trade entries. The core of the strategy is to trade the crossover between the VWAP and the Auto SMA, with confirmation from a candle close.

The strategy works best when the entry signal aligns with the overall bias of the higher timeframe market structure. For example, if the daily or 4-hour chart is in an uptrend, you would look for bullish signals on the one-minute chart.

Bullish Entry Signal: A potential entry is signaled when the VWAP crosses above the Auto SMA, and is confirmed when the one-minute candle closes above both the VWAP and the SMA. This indicates a potential continuation of the bullish momentum.

Bearish Entry Signal: A potential entry is signaled when the VWAP crosses below the Auto SMA, and is confirmed when the one-minute candle closes below both the VWAP and the SMA. This indicates a potential continuation of the bearish momentum.

The built-in alerts for these crossovers allow you to receive notifications without having to constantly monitor the charts, ensuring you don't miss a potential setup.

Sentinel 5 — OHL daybreak signals [KedArc Quant]Overview

Sentinel 5 plots the first-bar high/low of each trading session and gives clean, rules-based signals in two ways:

1) OHL Setups at the close of the first bar (Open equals/near High for potential short; Open equals/near Low for potential long).

2) Breakout Signals later in the session when price breaks the first-bar High/Low, with optional body/penetration filters.

Basic workflow

1. Wait for the first session bar to finish.

*If O≈H (optionally by proximity) → short setup. •

*If O≈L → long setup. • If neither happens, optionally allow later breakouts.

2. Optional: Act only on breakouts that penetrate a minimum % of that bar’s range/body.

3. Skip the day automatically if the first bar is abnormally large (marubozu-like / extreme ATR / outsized vs yesterday).

Signals & Markers

Markers on the chart:

▲ O=L (exact) / O near L (proximity) – long setup at first-bar close.

▼ O=H (exact) / O near H (proximity) – short setup at first-bar close.

▲ Breakout Long – later bar breaks above first-bar High meeting your penetration rule.

▼ Breakout Short – later bar breaks below first-bar Low meeting your penetration rule.

Advanced Range Analyzer ProAdvanced Range Analyzer Pro – Adaptive Range Detection & Breakout Forecasting

Overview

Advanced Range Analyzer Pro is a comprehensive trading tool designed to help traders identify consolidations, evaluate their strength, and forecast potential breakout direction. By combining volatility-adjusted thresholds, volume distribution analysis, and historical breakout behavior, the indicator builds an adaptive framework for navigating sideways price action. Instead of treating ranges as noise, this system transforms them into opportunities for mean reversion or breakout trading.

How It Works

The indicator continuously scans price action to identify active range environments. Ranges are defined by volatility compression, repeated boundary interactions, and clustering of volume near equilibrium. Once detected, the indicator assigns a strength score (0–100), which quantifies how well-defined and compressed the consolidation is.

Breakout probabilities are then calculated by factoring in:

Relative time spent near the upper vs. lower range boundaries

Historical breakout tendencies for similar structures

Volume distribution inside the range

Momentum alignment using auxiliary filters (RSI/MACD)

This creates a live probability forecast that updates as price evolves. The tool also supports range memory, allowing traders to analyze the last completed range after a breakout has occurred. A dynamic strength meter is displayed directly above each consolidation range, providing real-time insight into range compression and breakout potential.

Signals and Breakouts

Advanced Range Analyzer Pro includes a structured set of visual tools to highlight actionable conditions:

Range Zones – Gradient-filled boxes highlight active consolidations.

Strength Meter – A live score displayed in the dashboard quantifies compression.

Breakout Labels – Probability percentages show bias toward bullish or bearish continuation.

Breakout Highlights – When a breakout occurs, the range is marked with directional confirmation.

Dashboard Table – Displays current status, strength, live/last range mode, and probabilities.

These elements update in real time, ensuring that traders always see the current state of consolidation and breakout risk.

Interpretation

Range Strength : High scores (70–100) indicate strong consolidations likely to resolve explosively, while low scores suggest weak or choppy ranges prone to false signals.

Breakout Probability : Directional bias greater than 60% suggests meaningful breakout pressure. Equal probabilities indicate balanced compression, favoring mean-reversion strategies.

Market Context : Ranges aligned with higher timeframe trends often resolve in the dominant direction, while counter-trend ranges may lead to reversals or liquidity sweeps.

Volatility Insight : Tight ranges with low ATR imply imminent expansion; wide ranges signal extended consolidation or distribution phases.

Strategy Integration

Advanced Range Analyzer Pro can be applied across multiple trading styles:

Breakout Trading : Enter on probability shifts above 60% with confirmation of volume or momentum.

Mean Reversion : Trade inside ranges with high strength scores by fading boundaries and targeting equilibrium.

Trend Continuation : Focus on ranges that form mid-trend, anticipating continuation after consolidation.

Liquidity Sweeps : Use failed breakouts at boundaries to capture reversals.

Multi-Timeframe : Apply on higher timeframes to frame market context, then execute on lower timeframes.

Advanced Techniques

Combine with volume profiles to identify areas of institutional positioning within ranges.

Track sequences of strong consolidations for trend development or exhaustion signals.

Use breakout probability shifts in conjunction with order flow or momentum indicators to refine entries.

Monitor expanding/contracting range widths to anticipate volatility cycles.

Custom parameters allow fine-tuning sensitivity for different assets (crypto, forex, equities) and trading styles (scalping, intraday, swing).

Inputs and Customization

Range Detection Sensitivity : Controls how strictly ranges are defined.

Strength Score Settings : Adjust weighting of compression, volume, and breakout memory.

Probability Forecasting : Enable/disable directional bias and thresholds.

Gradient & Fill Options : Customize range visualization colors and opacity.

Dashboard Display : Toggle live vs last range, info table size, and position.

Breakout Highlighting : Choose border/zone emphasis on breakout events.

Why Use Advanced Range Analyzer Pro

This indicator provides a data-driven approach to trading consolidation phases, one of the most common yet underutilized market states. By quantifying range strength, mapping probability forecasts, and visually presenting risk zones, it transforms uncertainty into clarity.

Whether you’re trading breakouts, fading ranges, or mapping higher timeframe context, Advanced Range Analyzer Pro delivers a structured, adaptive framework that integrates seamlessly into multiple strategies.

Custom ATR BandsThis indicator provides a customisable, easy to view band around the price, based on the ATR. The ATR length and multiplier can be adjusted.

Average True Ranges with IBD RSAdvanced ATR Analysis with IBD Relative Strength

This comprehensive indicator combines Average True Range (ATR) analysis with IBD (Investor's Business Daily) Relative Strength calculation, providing both volatility measurement and momentum analysis in one powerful tool.

Key Features:

ATR Analysis:

Standard ATR: Customizable period (default 14) with multiple smoothing options

1.5x ATR: Extended range for wider stop-loss and target calculations

Smoothing Options: Choose between RMA, SMA, EMA, or WMA for ATR calculation

Customizable Colors: Distinct colors for easy visual identification

IBD Relative Strength:

Professional RS Formula: Uses the same calculation method as Investor's Business Daily

Multi-Timeframe Analysis: Compares current price to 3, 6, 9, and 12-month performance

Weighted Calculation: 40% weight on 3-month, 20% each on 6, 9, and 12-month performance

Zero-Based Scale: Values above 0 indicate outperformance, below 0 indicate underperformance

Trading Applications:

Volatility-Based Stops: Use ATR and 1.5x ATR for dynamic stop-loss placement

Position Sizing: ATR helps determine appropriate position size based on volatility

Relative Strength Analysis: IBD RS identifies stocks with superior momentum

Market Timing: High RS values often precede strong price moves

Risk Management: Combine volatility (ATR) with momentum (RS) for comprehensive analysis

Technical Details:

ATR Calculation: True Range smoothed over selected period with chosen method

IBD RS Formula: (40% × 3M) + (20% × 6M) + (20% × 9M) + (20% × 12M) - 100

Display: Separate pane indicator with customizable colors for each component

How to Interpret:

High ATR: Increased volatility, wider stops needed

Low ATR: Reduced volatility, tighter stops possible

Positive IBD RS: Stock outperforming market over measured periods

Negative IBD RS: Stock underperforming market over measured periods

Customizable Parameters:

ATR calculation length

Smoothing method for ATR

Individual colors for ATR, 1.5x ATR, and IBD RS lines

Perfect for swing traders and position traders who want to combine volatility analysis with relative strength momentum in their decision-making process. Particularly useful for stock selection and risk management.

Average True Range %The ATR% oscillator measures market volatility as a percentage of the closing price, smooths it using a chosen method (RMA, SMA, EMA, or WMA), and compares it to the threshold levels of 0.95% and 1.20%.

Relative Volatility Mass [SciQua]The ⚖️ Relative Volatility Mass (RVM) is a volatility-based tool inspired by the Relative Volatility Index (RVI) .

While the RVI measures the ratio of upward to downward volatility over a period, RVM takes a different approach:

It sums the standard deviation of price changes over a rolling window, separating upward volatility from downward volatility .

The result is a measure of the total “volatility mass” over a user-defined period, rather than an average or normalized ratio.

This makes RVM particularly useful for identifying sustained high-volatility conditions without being diluted by averaging.

────────────────────────────────────────────────────────────

╭────────────╮

How It Works

╰────────────╯

1. Standard Deviation Calculation

• Computes the standard deviation of the chosen `Source` over a `Standard Deviation Length` (`stdDevLen`).

2. Directional Separation

• Volatility on up bars (`chg > 0`) is treated as upward volatility .

• Volatility on down bars (`chg < 0`) is treated as downward volatility .

3. Rolling Sum

• Over a `Sum Length` (`sumLen`), the upward and downward volatilities are summed separately using `math.sum()`.

4. Relative Volatility Mass

• The two sums are added together to get the total volatility mass for the rolling window.

Formula:

RVM = Σ(σ up) + Σ(σ down)

where σ is the standard deviation over `stdDevLen`.

╭────────────╮

Key Features

╰────────────╯

Directional Volatility Tracking – Differentiates between volatility during price advances vs. declines.

Rolling Volatility Mass – Shows the total standard deviation accumulation over a given period.

Optional Smoothing – Multiple MA types, including SMA, EMA, SMMA (RMA), WMA, VWMA.

Bollinger Band Overlay – Available when SMA is selected, with adjustable standard deviation multiplier.

Configurable Source – Apply RVM to `close`, `open`, `hl2`, or any custom source.

╭─────╮

Usage

╰─────╯

Trend Confirmation: High RVM values can confirm strong trending conditions.

Breakout Detection: Spikes in RVM often precede or accompany price breakouts.

Volatility Cycle Analysis: Compare periods of contraction and expansion.

RVM is not bounded like the RVI, so absolute values depend on market volatility and chosen parameters.

Consider normalizing or using smoothing for easier visual comparison.

╭────────────────╮

Example Settings

╰────────────────╯

Short-term volatility detection: `stdDevLen = 5`, `sumLen = 10`

Medium-term trend volatility: `stdDevLen = 14`, `sumLen = 20`

Enable `SMA + Bollinger Bands` to visualize when volatility is unusually high or low relative to recent history.

╭───────────────────╮

Notes & Limitations

╰───────────────────╯

Not a directional signal by itself — use alongside price structure, volume, or other indicators.

Higher `sumLen` will smooth short-term fluctuations but reduce responsiveness.

Because it sums, not averages, values will scale with both volatility and chosen window size.

╭───────╮

Credits

╰───────╯

Based on the Relative Volatility Index concept by Donald Dorsey (1993).

TradingView

SciQua - Joshua Danford

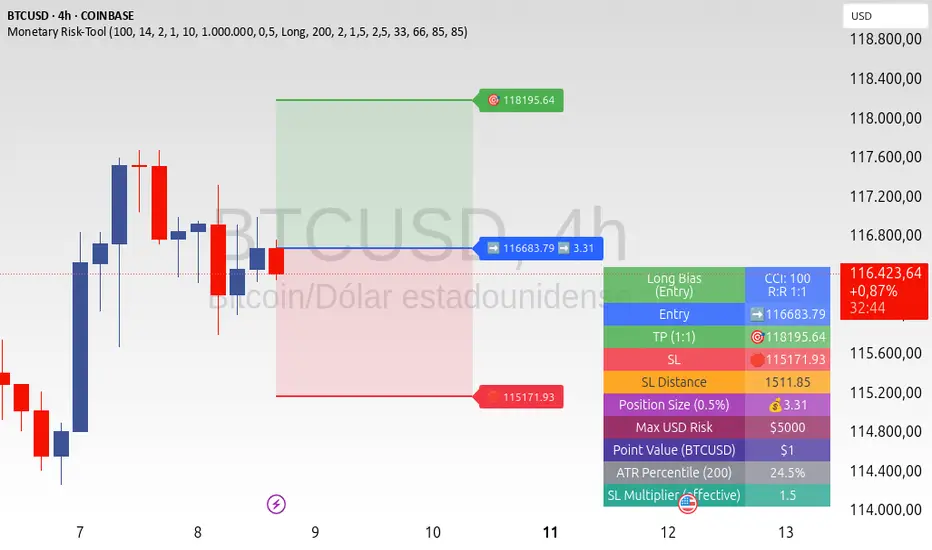

ATR+CCI Monetary Risk Tool - TP/SL⚙️ ATR+CCI Monetary Risk Tool — Volatility-aware TP/SL & Position Sizing

Exact prices (no rounding), ATR-percentile dynamic stops, and risk-budget sizing for consistent execution.

🧠 What this indicator is

A risk-first planning tool. It doesn’t generate orders; it gives you clean, objective levels (Entry, SL, TP) and position size derived from your risk budget. It shows only the latest setup to keep charts readable, and a compact on-chart table summarizing the numbers you actually act on.

✨ What makes it different

Dynamic SL by regime (ATR percentile): Instead of a fixed multiple, the SL multiplier adapts to the current volatility percentile (low / medium / high). That helps avoid tight stops in noisy markets and over-wide stops in quiet markets.

Risk budgeting, not guesswork: Size is computed from Account Balance × Max Risk % divided by SL distance × point value. You risk the same dollars across assets/timeframes.

Precision that matches your instrument: Entry, TP, SL, and SL Distance are displayed as exact prices (no rounding), truncated to syminfo.mintick so they align with broker/exchange precision.

Symbol-aware point value: Uses syminfo.pointvalue so you don’t maintain tick tables.

Non-repaint option: Work from closed bars to keep the plan stable.

🔧 How to use (quick start)

Add to chart and pick your timeframe and symbol.

In settings:

Set Account Balance (USD) and Max Risk per Trade (%).

Choose R:R (1:1 … 1:5).

Pick ATR Period and CCI Period (defaults are sensible).

Keep Dynamic ATR ON to adapt SL by regime.

Keep Use closed-bar values ON to avoid repaint when planning.

Read the labels (Entry/TP/SL) and the table (SL Distance, Position Size, Max USD Risk, ATR Percentile, effective SL Mult).

Combine with your entry trigger (price action, levels, momentum, etc.). This indicator handles risk & targets.

📐 How levels are computed

Bias: CCI ≥ 0 ⇒ long, otherwise short.

ATR Percentile: Percent rank of ATR(atrPeriod) over a lookback window.

Effective SL Mult:

If percentile < Low threshold ⇒ use Low SL Mult (tighter).

If between thresholds ⇒ use Base SL Mult.

If percentile > High threshold ⇒ use High SL Mult (wider).

Stop-Loss: SL = Entry ± ATR × SL_Mult (minus for long, plus for short).

Take-Profit: TP = Entry ± (Entry − SL) × R (R from the R:R dropdown).

Position Size:

USD Risk = Balance × Risk%

Contracts = USD Risk ÷ (|Entry − SL| × PointValue)

For futures, quantity is floored to whole contracts.

Exact prices: Entry/TP/SL and SL Distance are not rounded; they’re truncated to mintick so what you see matches valid price increments.

📊 What you’ll see on chart

Latest Entry (blue), TP (green), SL (red) with labels (optional emojis: ➡️ 🎯 🛑).

Info Table with:

Bias, Entry, TP, SL (exact, truncated to mintick)

SL Distance (exact, truncated)

Position Size (contracts/units)

Max USD Risk

Point Value

ATR Percentile and effective SL Mult

🧪 Practical examples

High-volatility session (e.g., XAUUSD, 1H): ATR percentile is high ⇒ wider SL, smaller size. Reduces churn from normal noise during macro events.

Range-bound market (e.g., EURUSD, 4H): ATR percentile low ⇒ tighter SL, better R:R. Helps you avoid carrying unnecessary risk.

Index swing planning (e.g., ES1!, Daily): Non-repaint levels + risk budgeting = consistent sizing across days/weeks, easier to review and journal.

🧭 Why traders should use it

Consistency: Same dollar risk regardless of instrument or volatility regime.

Clarity: One-trade view forces focus; you see the numbers that matter.

Adaptivity: Stops calibrated to the market’s current behavior, not last month’s.

Discipline: A visible checklist (SL distance, size, USD risk) before you hit buy/sell.

🔧 Input guide (practical defaults)

CCI Period: 100 by default; use as a bias filter, not an entry signal.

ATR Period: 14 by default; raise for smoother, lower for more reactive.

ATR Percentile Lookback: 200 by default (stable regime detection).

Percentile thresholds: 33/66 by default; widen the gap to change how often regimes switch.

SL Mults: Start ~1.5 / 2.0 / 2.5 (low/base/high). Tune by asset.

Risk % per trade: Common pro ranges are 0.25–1.0%; adjust to your risk tolerance.

R:R: Start with 1:2 or 1:3 for balanced skew; adapt to strategy edge.

Closed-bar values: Keep ON for planning/live; turn OFF only for exploration.

💡 Best practices

Combine with your entry logic (structure, momentum, liquidity levels).

Review ATR percentile and effective SL Mult across sessions so you understand regime shifts.

For futures, remember size is floored to whole contracts—safer by design.

Journal trades with the table snapshot to improve risk discipline over time.

⚠️ Notes & limitations

This is not a strategy; it does not place orders or alerts.

No slippage/commissions modeled here; build a strategy() version for backtests that mirror your broker/exchange.

Displayed non-price metrics use two decimals; prices and SL Distance are exact (truncated to mintick).

📎 Disclaimer

For educational purposes only. Not financial advice. Markets involve risk. Test thoroughly before trading live.

ATR%指標概要 / Overview

ATR Percentage (MTF):把 ATR 轉為百分比(ATR%)或保留為絕對值,並在該「波動序列」上套用布林帶。支援多週期(MTF)計算:例如在 5 分圖顯示 4H / D1 的 ATR%。內建白色點狀水平線作為固定門檻(預設 1%)。

ATR Percentage (MTF): Converts ATR to a percentage of price (ATR%) or keeps it as absolute ATR, then applies Bollinger Bands on this volatility series. Supports multi-timeframe (MTF) calculation (e.g., show 4H/D1 ATR% on a 5-min chart). Includes a configurable white dotted horizontal threshold line (default 1%).

⸻

設計目的 / Purpose

• 以 ATR% 衡量相對波動,利於跨品種比較。

Use ATR% for relative volatility to compare across markets.

• 以 布林帶 標示「高/低波動區」,觀察擴張與壓縮。

Use Bollinger Bands on volatility to highlight expansion/squeeze.

• 提供 固定閾值(1%) 作為策略濾網或告警門檻。

Provide a fixed threshold (1%) for filters/alerts.

• 以 MTF 方式,讓低週期策略用高週期波動做濾網。

MTF lets lower-TF strategies filter by higher-TF volatility.

⸻

參數說明 / Inputs

• Use ATR as % of Close:切換 ATR(絕對值)/ ATR%(建議)。

Toggle between absolute ATR and ATR% (recommended).

• ATR Periods:ATR 計算長度(預設 22)。

ATR lookback (default 22).

• Show Bollinger Bands / BB Periods / StdDev:布林帶開關、長度與倍數(預設 20 / 2)。

Bollinger Bands on/off, length, and deviation (default 20 / 2).

• Source Timeframe:計算用週期(如 60、240、D、W;留空/Chart = 跟隨圖表)。

Timeframe used for calculations (e.g., 60, 240, D, W; empty/“Chart” = current).

• Threshold Line (%):白色點線門檻,預設 1.0(即 1%)。

White dotted threshold line, default 1.0 (1%).

提醒:當 非 ATR% 模式時,Threshold 值代表「價格單位」而非百分比。

Note: In non-ATR% mode, the threshold is in price units, not percent.

⸻

訊號解讀 / How to Read

• ATR% > 上軌:波動顯著擴張(趨勢啟動或加速常見)。

ATR% above upper band: significant expansion; often trend ignition/acceleration.

• ATR% < 下軌:波動明顯壓縮(常見於突破前)。

ATR% below lower band: volatility squeeze; often precedes breakouts.

• ATR% 穿越 Threshold(1%):達到固定波動標準,可作策略開關或風控分水嶺。

ATR% crossing the 1% threshold: fixed volatility bar for filters/risk gates.

⸻

內建告警 / Built-in Alerts

• Volatility Breakout (MTF):ATR/ATR% 向上穿越上軌。

Triggers when ATR/ATR% crosses above the upper band.

• Volatility Squeeze (MTF):ATR/ATR% 向下穿越下軌。

Triggers when ATR/ATR% crosses below the lower band.

⸻

使用建議 / Suggested Uses

• 當沖濾網:於 1–5 分圖選擇 4H / D1 作為 Source Timeframe;僅在 ATR% > 1% 且位於中線以上時允許趨勢進場。

Intraday filter: on 1–5m charts, set 4H/D1 as source TF; allow trend entries only when ATR% > 1% and above the midline.

• 突破前偵測:ATR% 長時間貼近下軌 → 留意可能的波動擴張。

Pre-breakout scan: prolonged ATR% near lower band can foreshadow expansion.

• 跨品種比較:用 ATR% 統一指數、外匯、商品的波動刻度。

Cross-asset comparison: ATR% normalizes volatility across indices/FX/commodities.

⸻

已知限制 / Notes

• MTF 對齊:使用 request.security() 對映高週期資料到當前圖表;在歷史回補與即時邊界棒可能略有差異。

MTF alignment: request.security() maps higher-TF data; boundary bars may differ slightly between historical and realtime.

• 百分比分母:ATR% 的分母為同一週期的 close;若需更平滑可改 ATR / SMA(close, N) × 100。

Denominator: ATR% uses same-TF close; for smoother values consider ATR / SMA(close, N) × 100.

• 風險聲明:僅供研究/教育用途,非投資建議,請自行控管風險。

Disclaimer: For research/education only. Not investment advice.

⸻

版本與更新 / Version & Updates

• v1.0:ATR/ATR% + BB(MTF)、1% 白色點線、兩組告警。

v1.0: ATR/ATR% + BB (MTF), 1% white dotted line, two alert conditions.