Trend Pulse Channel StrategyTrend Pulse Channel Strategy

Overview

The Trend Pulse Channel Strategy is a long-only trend-following strategy designed to capture sustained bullish moves by combining trend strength confirmation with price channel structure.

It focuses on participating in strong directional markets while filtering out low-quality signals during ranging conditions.

⸻

Strategy Logic

The strategy is built on three core components:

1. Trend Strength Filter

• Uses the Average Directional Index (ADX) to confirm that the market is trending.

• Trades are allowed only when trend strength exceeds a predefined threshold.

• This helps avoid choppy, sideways markets.

2. Channel-Based Price Structure

• Price action is evaluated within a smoothed channel framework.

• Entries occur when price aligns with bullish channel direction and momentum.

• Channels help define structure, continuation, and exhaustion zones.

3. Long-Only Bias

• The strategy takes long positions only.

• Designed for assets with a natural bullish tendency over time (stocks, indices, major crypto).

⸻

Entry Conditions (Long)

A long trade is triggered when:

• ADX confirms sufficient trend strength.

• Price holds bullish structure within the channel.

• Momentum aligns with the dominant trend direction.

⸻

Exit Conditions

Positions are closed when:

• Trend strength weakens.

• Price loses channel support.

• Momentum shows signs of exhaustion or reversal.

⸻

Risk & Execution Notes

• Percentage-based position sizing.

• Commission and slippage included for realistic backtesting.

• Optimized to reduce over-trading.

⸻

Recommended Usage

Markets:

• Stocks

• Indices

• Cryptocurrencies

Timeframes:

• 15-minute and higher

• Performs best on 1H, 4H, and Daily

⸻

Intended Audience

• Trend followers

• Swing traders

• Position traders

Not suitable for:

• Range-bound scalping

• Counter-trend strategies

⸻

Disclaimer

This strategy is provided for educational and research purposes only.

Always forward-test and apply proper risk management before live trading.

頻帶和通道

Trend Pulse Channel StrategyTrend Pulse Channel Strategy

Overview

The Trend Pulse Channel Strategy is a long-only trend-following strategy designed to capture sustained bullish moves by combining trend strength confirmation with price channel structure.

It focuses on participating in strong directional markets while filtering out low-quality signals during ranging conditions.

⸻

Strategy Logic

The strategy is built on three core components:

1. Trend Strength Filter

• Uses the Average Directional Index (ADX) to confirm that the market is trending.

• Trades are allowed only when trend strength exceeds a predefined threshold.

• This helps avoid choppy, sideways markets.

2. Channel-Based Price Structure

• Price action is evaluated within a smoothed channel framework.

• Entries occur when price aligns with bullish channel direction and momentum.

• Channels help define structure, continuation, and exhaustion zones.

3. Long-Only Bias

• The strategy takes long positions only.

• Designed for assets with a natural bullish tendency over time (stocks, indices, major crypto).

⸻

Entry Conditions (Long)

A long trade is triggered when:

• ADX confirms sufficient trend strength.

• Price holds bullish structure within the channel.

• Momentum aligns with the dominant trend direction.

⸻

Exit Conditions

Positions are closed when:

• Trend strength weakens.

• Price loses channel support.

• Momentum shows signs of exhaustion or reversal.

⸻

Risk & Execution Notes

• Percentage-based position sizing.

• Commission and slippage included for realistic backtesting.

• Optimized to reduce over-trading.

⸻

Recommended Usage

Markets:

• Stocks

• Indices

• Cryptocurrencies

Timeframes:

• 15-minute and higher

• Performs best on 1H, 4H, and Daily

⸻

Intended Audience

• Trend followers

• Swing traders

• Position traders

Not suitable for:

• Range-bound scalping

• Counter-trend strategies

⸻

Disclaimer

This strategy is provided for educational and research purposes only.

Always forward-test and apply proper risk management before live trading.

Pi Strategy Cross Harmonicsstill customizing this one, buy and sell seems to off on alternate time settings.

a work in progress, see if this works for anyone.

thanks again.

225 SMA CrossoverWell-known strategy from Zahlengraf from the Mauerstrassenwetten subreddit for you to test yourself.

You can change the length of the SMA and whether to trade long, short or both directions.

Ribbon Cross Strategy This strategy uses a simple moving-average ribbon crossover system with a customizable entry filter. You can choose whether trades trigger near the fast or slow average, allowing flexibility in capturing early or confirmed trend moves.

It’s best suited for index trading on intraday timeframes , helping identify short-term trend reversals and continuations with clear visual cues and backtestable logic.

Adaptive Alligator - Asymmetric MH (Entry Only)

Adaptive Alligator – Asymmetric Mexican Hat (Entry Only)

This strategy combines adaptive cycle detection (wavelet + autocorrelation), directional entropy, and a Mexican Hat filter to generate highly selective LONG entry signals. Exits are based solely on the Alligator structure. The system is designed to detect asymmetric, strong, and accelerating bullish phases while filtering out market noise.

1. Adaptive Cycle Detection: The strategy analyzes the median price using wavelet decomposition (Haar, Daubechies D4/D6, Symlet 4), wavelet detail energy, and autocorrelation. It also incorporates the ratio of short-term to long-term ATR volatility. Based on these components, it computes a dominant_cycle value, which dynamically controls the lengths of the Alligator lines (Jaw, Teeth, Lips). This adaptive behavior allows the Alligator to speed up during trending phases and slow down during noise or consolidation.

2. Directional Entropy: Entropy is measured separately for upward and downward movements within the selected lookback window. The entropy difference: e_diff = entropy_down - entropy_up represents the directional bias of the market. When e_diff > 0, the market shows an organized bullish pressure; when < 0, bearish dominance.

3. Mexican Hat Filter: The Mexican Hat (Ricker Wavelet) acts as a second-derivative filter, detecting local maxima in the acceleration of directional entropy. The filtered output (mh_out) is compared against an adaptive noise level computed as SMA(|mh_out|). A signal is considered strong only when: – mh_out exceeds the adaptive noise level, – mh_out is rising relative to the previous bar. This step is critical for eliminating false signals produced by random fluctuations.

4. Entry Logic: A LONG entry requires all three layers: (1) Alligator structure: Lips > Teeth > Jaw. (2) Directional entropy bias: e_diff > 0. (3) A strong, accelerating Mexican Hat signal confirmed by a user-defined number of bars. Once all conditions are satisfied, a buy_final entry is triggered.

5. Exit Logic: Exits are intentionally simple and rely solely on the Alligator: crossunder(lips, teeth) This clean separation ensures precise, adaptive entries and stable, consistent exits.

6. Visual Components: – Alligator lines: Jaw (blue), Teeth (red), Lips (green), plotted with their characteristic offsets. – Background coloring reflects signal strength: dark green (STRONG BUY), lime (acceleration), yellow (weak bias), transparent otherwise. – A dedicated panel displays e_diff (entropy difference), mh_out (Mexican Hat output), and the adaptive noise band.

7. Diagnostic Table: A compact diagnostic dashboard shows: – MH Value, – Noise Level, – MH Acceleration (YES/NO), – Signal Status (STRONG BUY / ACCELERATING / WEAK / BEARISH). It updates on the last bar, making it suitable for live monitoring.

8. Use Case: This strategy is highly selective and ideal as an entry module within trend-following systems. By combining wavelets, entropy, and adaptive noise modeling, it effectively filters out consolidation periods and focuses only on statistically significant bullish transitions. It can be integrated with various exit frameworks such as ATR stops, channel-based exits, range boxes, or trailing logic.

Estrategia Trend Following: 52w/26w BreakoutThis is a classic long-term Trend Following strategy, heavily inspired by the Donchian Channel system and the legendary "Turtle Trading" rules. It is designed to capture major market moves (bull runs) while filtering out short-term market noise and volatility.

This script is ideal for investors and swing traders who prefer a "hands-off" approach, looking to catch large trends rather than day-trading small fluctuations.

How it Works:

1. Entry Condition (The Breakout):

52-Week High: The strategy enters a Long position when the price breaks above the highest high of the last 252 trading days (approx. 1 year).

SuperTrend Filter: An additional filter using the SuperTrend indicator ensures that the breakout is supported by positive momentum, helping to reduce false signals during choppy lateral markets.

2. Exit Condition (The Trailing Stop):

26-Week Low: The strategy ignores short-term corrections. It only closes the position if the price closes below the lowest low of the last 126 trading days (approx. 6 months).

This wide stop allows the trade to "breathe" and stay open during significant pullbacks, ensuring you stay in the trend for as long as possible.

Features & Settings:

Customizable Lookback Periods: You can adjust the Entry (default 252 days) and Exit (default 126 days) periods in the settings menu.

Visual Aids:

Blue Line: Represents the 1-Year High (Entry Threshold).

Red Line: Represents the 6-Month Low (Dynamic Stop Loss).

Channel Shading: Visualizes the trading range between the high and low.

Labels: Clearly marks "BUY" and "EXIT" points on the chart.

Recommended Usage:

Timeframe: Daily (1D). This logic is designed for daily candles.

Assets: Works best on assets with strong trending characteristics (e.g., Bitcoin/Crypto, Tech Stocks, Indices like SPX/NDX, and Commodities).

Patience Required: This strategy generates very few signals. It may stay quiet for months and then hold a position for over a year.

Trendline Breaks + Supertrend [Delta BTC-P]Trendline Breaks + Supertrend in same direct Best on 5 min

Mean Reversion — BB + Z-Score + RSI + EMA200 (TP at Opposite Z)This is a systematic mean-reversion framework for index futures and other liquid assets.

This strategy combines Bollinger Bands, Z-Score dislocation, RSI extremes, and a trend-filtering EMA200 to capture short-term mean-reversion inefficiencies in NQ1!. It is designed for high-volatility conditions and uses a precise exit model based on opposite-side Z-Score targets and dynamic mid-band failure detection.

🔍 Entry Logic (Mean Reversion) :

The strategy enters trades only when multiple confluence signals align:

Long Setup

Price at or below the lower Bollinger Band

Z-Score ≤ –Threshold (deep statistical deviation)

RSI ≤ oversold level

Price below the EMA-200 (countertrend mean-reversion only)

Cooldown must be completed

No open position

Short Setup

Price at or above the upper Bollinger Band

Z-Score ≥ Threshold

RSI ≥ overbought level

Price above the EMA-200

Cooldown complete

No open position

This multi-signal gate filters out weak reversions and focuses on mature dislocations.

🎯 Take-Profit Model: Opposite-Side Z-Score Target :

Once in a trade, take-profit is set by solving for the price where the Z-Score reaches the opposite side:

Long TP = Z = +Threshold

Short TP = Z = –Threshold

This creates a symmetric statistical exit based on reverting to equilibrium plus overshoot.

🛡️ Stop-Loss System (Volatility-Aware) :

Stop losses combine:

A fixed base stop (points)

A standard-deviation volatility component

This adapts the SL to regime changes and avoids being shaken out during rare volatility spikes.

⏳ Half-Life Exit :

If a trade has not reverted within a fixed number of bars, it automatically closes.

This prevents “mean-reversion traps” during trending periods.

📉 Advanced Mid-Band Exit Logic (BB Basis Failure) :

This is the unique feature of the system.

After entry:

Wait for price to cross the Bollinger Basis (middle band) in the direction of the mean.

Start a 5-bar delay timer.

After 5 bars, the strategy becomes “armed.”

Once armed:

If price fails back through the mean, exit immediately.

Intrabar exits trigger precisely (with tick-level precision if Bar Magnifier is enabled).

This protects profits and exits trades at the first sign of mean-failure.

⏱️ Cooldown System :

After each closed trade, a cooldown period prevents immediate re-entry.

This avoids clustering and improves statistical independence of trades.

🖥️ What This Strategy Is Best For :

High-volatility intraday NQ conditions

Statistical mean reversion with structured confluence

Traders who want clean, rule-based entries

Avoiding trend-day traps using EMA and half-life logic

📊 Included Visual Elements :

Bollinger Bands (Upper, Basis, Lower)

BUY/SELL markers at signal generation

Optional alerts for automated monitoring

🚀 Summary :

This is a precision mean-reversion system built around volatility bands, statistical dislocation, and price-behavior confirmation. By combining Z-Score, RSI, EMA200 filtering, and a sophisticated mid-band failure exit, this model captures high-probability reversions while avoiding the common pitfalls of naive band-touch systems.

Smart Bottom Catcher @ Le DReversal strategy using recent lowest lows and a fast RSI. Long entries trigger on extreme drops, exits occur when RSI crosses a set threshold. Includes optional SMA55 filter and allows up to 3 pyramids.

Third eye • StrategyThird eye • Strategy – User Guide

1. Idea & Concept

Third eye • Strategy combines three things into one system:

Ichimoku Cloud – to define market regime and support/resistance.

Moving Average (trend filter) – to trade only in the dominant direction.

CCI (Commodity Channel Index) – to generate precise entry signals on momentum breakouts.

The script is a strategy, not an indicator: it can backtest entries, exits, SL, TP and BreakEven logic automatically.

2. Indicators Used

2.1 Ichimoku

Standard Ichimoku settings (by default 9/26/52/26) are used:

Conversion Line (Tenkan-sen)

Base Line (Kijun-sen)

Leading Span A & B (Kumo Cloud)

Lagging Span is calculated but hidden from the chart (for visual simplicity).

From the cloud we derive:

kumoTop – top of the cloud under current price.

kumoBottom – bottom of the cloud under current price.

Flags:

is_above_kumo – price above the cloud.

is_below_kumo – price below the cloud.

is_in_kumo – price inside the cloud.

These conditions are used as trend / regime filters and for stop-loss & trailing stops.

2.2 Moving Average

You can optionally display and use a trend MA:

Types: SMA, EMA, DEMA, WMA

Length: configurable (default 200)

Source: default close

Filter idea:

If MA Direction Filter is ON:

When Close > MA → strategy allows only Long signals.

When Close < MA → strategy allows only Short signals.

The MA is plotted on the chart (if enabled).

2.3 CCI & Panel

The CCI (Commodity Channel Index) is used for entry timing:

CCI length and source are configurable (default length 20, source hlc3).

Two thresholds:

CCI Upper Threshold (Long) – default +100

CCI Lower Threshold (Short) – default –100

Signals:

Long signal:

CCI crosses up through the upper threshold

cci_val < upper_threshold and cci_val > upper_threshold

Short signal:

CCI crosses down through the lower threshold

cci_val > lower_threshold and cci_val < lower_threshold

There is a panel (table) in the bottom-right corner:

Shows current CCI value.

Shows filter status as colored dots:

Green = filter enabled and passed.

Red = filter enabled and blocking trades.

Gray = filter is disabled.

Filters shown in the panel:

Ichimoku Cloud filter (Long/Short)

Ichimoku Lines filter (Conversion/Base vs Cloud)

MA Direction filter

3. Filters & Trade Direction

All filters can be turned ON/OFF independently.

3.1 Ichimoku Cloud Filter

Purpose: trade only when price is clearly above or below the Kumo.

Long Cloud Filter (Use Ichimoku Cloud Filter) – when enabled:

Long trades only if close > cloud top.

Short Cloud Filter – when enabled:

Short trades only if close < cloud bottom.

If the cloud filter is disabled, this condition is ignored.

3.2 Ichimoku Lines Above/Below Cloud

Purpose: stronger trend confirmation: Ichimoku lines should also be on the “correct” side of the cloud.

Long Lines Filter:

Long allowed only if Conversion Line and Base Line are both above the cloud.

Short Lines Filter:

Short allowed only if both lines are below the cloud.

If this filter is OFF, the conditions are not checked.

3.3 MA Direction Filter

As described above:

When ON:

Close > MA → only Longs.

Close < MA → only Shorts.

4. Anti-Re-Entry Logic (Cloud Touch Reset)

The strategy uses internal flags to avoid continuous re-entries in the same direction without a reset.

Two flags:

allowLong

allowShort

After a Long entry, allowLong is set to false, allowShort to true.

After a Short entry, allowShort is set to false, allowLong to true.

Flags are reset when price touches the Kumo:

If Low goes into the cloud → allowLong = true

If High goes into the cloud → allowShort = true

If Close is inside the cloud → both allowLong and allowShort are set to true

There is a key option:

Wait Position Close Before Flag Reset

If ON: cloud touch will reset flags only when there is no open position.

If OFF: flags can be reset even while a trade is open.

This gives a kind of regime-based re-entry control: after a trend leg, you wait for a “cloud interaction” to allow new signals.

5. Risk Management

All risk management is handled inside the strategy.

5.1 Position Sizing

Order Size % of Equity – default 10%

The strategy calculates:

position_value = equity * (Order Size % / 100)

position_qty = position_value / close

So position size automatically adapts to your current equity.

5.2 Take Profit Modes

You can choose one of two TP modes:

Percent

Fibonacci

5.2.1 Percent Mode

Single Take Profit at X% from entry (default 2%).

For Long:

TP = entry_price * (1 + tp_pct / 100)

For Short:

TP = entry_price * (1 - tp_pct / 100)

One strategy.exit per side is used: "Long TP/SL" and "Short TP/SL".

5.2.2 Fibonacci Mode (2 partial TPs)

In this mode, TP levels are based on a virtual Fib-style extension between entry and stop-loss.

Inputs:

Fib TP1 Level (default 1.618)

Fib TP2 Level (default 2.5)

TP1 Share % (Fib) (default 50%)

TP2 share is automatically 100% - TP1 share.

Process for Long:

Compute a reference Stop (see SL section below) → sl_for_fib.

Compute distance: dist = entry_price - sl_for_fib.

TP levels:

TP1 = entry_price + dist * (Fib TP1 Level - 1)

TP2 = entry_price + dist * (Fib TP2 Level - 1)

For Short, the logic is mirrored.

Two exits are used:

TP1 – closes TP1 share % of position.

TP2 – closes remaining TP2 share %.

Same stop is used for both partial exits.

5.3 Stop-Loss Modes

You can choose one of three Stop Loss modes:

Stable – fixed % from entry.

Ichimoku – fixed level derived from the Kumo.

Ichimoku Trailing – dynamic SL following the cloud.

5.3.1 Stable SL

For Long:

SL = entry_price * (1 - Stable SL % / 100)

For Short:

SL = entry_price * (1 + Stable SL % / 100)

Used both for Percent TP mode and as reference for Fib TP if Kumo is not available.

5.3.2 Ichimoku SL (fixed, non-trailing)

At the time of a new trade:

For Long:

Base SL = cloud bottom minus small offset (%)

For Short:

Base SL = cloud top plus small offset (%)

The offset is configurable: Ichimoku SL Offset %.

Once computed, that SL level is fixed for this trade.

5.3.3 Ichimoku Trailing SL

Similar to Ichimoku SL, but recomputed each bar:

For Long:

SL = cloud bottom – offset

For Short:

SL = cloud top + offset

A red trailing SL line is drawn on the chart to visualize current stop level.

This trailing SL is also used as reference for BreakEven and for Fib TP distance.

6. BreakEven Logic (with BE Lines)

BreakEven is optional and supports two modes:

Percent

Fibonacci

Inputs:

Percent mode:

BE Trigger % (from entry) – move SL to BE when price goes this % in profit.

BE Offset % from entry – SL will be set to entry ± this offset.

Fibonacci mode:

BE Fib Level – Fib level at which BE will be activated (default 1.618, same style as TP).

BE Offset % from entry – how far from entry to place BE stop.

The logic:

Before BE is triggered, SL follows its normal mode (Stable/Ichimoku/Ichimoku Trailing).

When BE triggers:

For Long:

New SL = max(current SL, BE SL).

For Short:

New SL = min(current SL, BE SL).

This means BE will never loosen the stop – only tighten it.

When BE is activated, the strategy draws a violet horizontal line at the BreakEven level (once per trade).

BE state is cleared when the position is closed or when a new position is opened.

7. Entry & Exit Logic (Summary)

7.1 Long Entry

Conditions for a Long:

CCI signal:

CCI crosses up through the upper threshold.

Ichimoku Cloud Filter (optional):

If enabled → price must be above the Kumo.

Ichimoku Lines Filter (optional):

If enabled → Conversion Line and Base Line must be above the Kumo.

MA Direction Filter (optional):

If enabled → Close must be above the chosen MA.

Anti-re-entry flag:

allowLong must be true (cloud-based reset).

Position check:

Long entries are allowed when current position size ≤ 0 (so it can also reverse from short to long).

If all these conditions are true, the strategy sends:

strategy.entry("Long", strategy.long, qty = calculated_qty)

After entry:

allowLong = false

allowShort = true

7.2 Short Entry

Same structure, mirrored:

CCI signal:

CCI crosses down through the lower threshold.

Cloud filter: price must be below cloud (if enabled).

Lines filter: conversion & base must be below cloud (if enabled).

MA filter: Close must be below MA (if enabled).

allowShort must be true.

Position check: position size ≥ 0 (allows reversal from long to short).

Then:

strategy.entry("Short", strategy.short, qty = calculated_qty)

Flags update:

allowShort = false

allowLong = true

7.3 Exits

While in a position:

The strategy continuously recalculates SL (depending on chosen mode) and, in Percent mode, TP.

In Fib mode, fixed TP levels are computed at entry.

BreakEven may raise/tighten the SL if its conditions are met.

Exits are executed via strategy.exit:

Percent mode: one TP+SL exit per side.

Fib mode: two partial exits (TP1 and TP2) sharing the same SL.

At position open, the script also draws visual lines:

White line — entry price.

Green line(s) — TP level(s).

Red line — SL (if not using Ichimoku Trailing; with trailing, the red line is updated dynamically).

Maximum of 30 lines are kept to avoid clutter.

8. How to Use the Strategy

Choose market & timeframe

Works well on trending instruments. Try crypto, FX or indices on H1–H4, or intraday if you prefer more trades.

Adjust Ichimoku settings

Keep defaults (9/26/52/26) or adapt to your timeframe.

Configure Moving Average

Typical: EMA 200 as a trend filter.

Turn MA Direction Filter ON if you want to trade only with the main trend.

Set CCI thresholds

Default ±100 is classic.

Lower thresholds → more signals, higher noise.

Higher thresholds → fewer but stronger signals.

Enable/disable filters

Turn on Ichimoku Cloud and Ichimoku Lines if you want only “clean” trend trades.

Use Wait Position Close Before Flag Reset to control how often re-entries are allowed.

Choose TP & SL mode

Percent mode is simpler and easier to understand.

Fibonacci mode is more advanced: it aligns TP levels with the distance to stop, giving asymmetric RR setups (two partial TPs).

Choose Stable SL for fixed-risk trades, or Ichimoku / Ichimoku Trailing to tie stops to the cloud structure.

Set BreakEven

Enable BE if you want to lock in risk-free trades after a certain move.

Percent mode is straightforward; Fib mode keeps BreakEven in harmony with your Fib TP setup.

Run Backtest & Optimize

Press “Add to chart” → go to Strategy Tester.

Adjust parameters to your market and timeframe.

Look at equity curve, PF, drawdown, average trade, etc.

Live / Paper Trading

After you’re satisfied with backtest results, use the strategy to generate signals.

You can mirror entries/exits manually or connect them to alerts (if you build an alert-based execution layer).

ETHUSDT 4H - Keltner Breakout working nice with ETH above EMA200

Using Keltner bands to prevent get rid off unnecessary noices . Works at safe side

Which is fantastic for people who does not want to stick to screen full day , it needs as couple of transactions per month to gain meaningfull profit

Do not forget to use it with 4 hr time frame

Do not recommend to use it with sh*tcoins, however with a small fine tuning its okay to use it with Top altcoins

Long-Term Strategy: 1-Year Breakout + 6-Month ExitDescripción (Description): (Copia y pega todo lo que está dentro del recuadro de abajo)

Description

This is a long-term trend-following strategy designed to capture major market moves while filtering out short-term noise. It is based on the classic principle of "buying strength" (Breakouts) and allowing profits to run, while cutting losses when the medium-term trend reverses.

How it Works (Logic)

1. Entry Condition (Long Only): The strategy looks for a significant display of strength. It enters a Long position only when two conditions are met simultaneously:

Price Breakout: The closing price exceeds the highest high of the last 252 trading days (approximately 1 year). This ensures we are entering during a strong momentum phase.

Trend Filter: The SuperTrend indicator (Settings: ATR 10, Factor 3.0) must be bullish. This acts as a confirmation filter to avoid false breakouts in choppy markets.

2. Exit Condition: The strategy uses a trailing stop based on price action, not a fixed percentage.

It closes the position when the price closes below the lowest low of the last 126 trading days (approximately 6 months).

This wide exit allows the trade to "breathe" during normal market corrections without exiting the position prematurely.

Settings & Risk Management

Capital Usage: The script is configured to use 10% of equity per trade to reflect realistic risk management (compounding).

Commissions: Included at 0.1% to simulate real trading costs.

Slippage: Included (3 ticks) to account for market execution variability.

Best Use: This strategy is intended for higher timeframes (Daily or Weekly) on trending assets like Indices, Crypto, or Commodities.

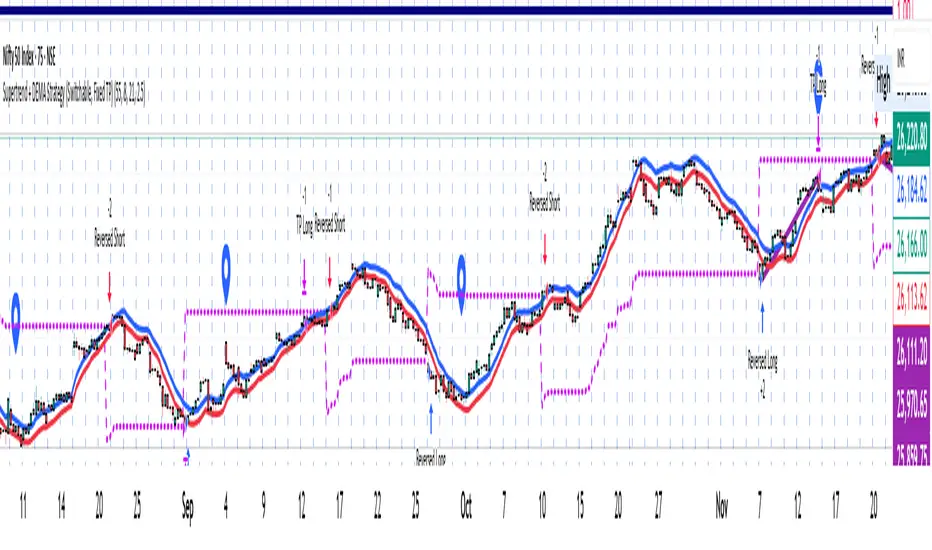

Supertrend + DEMA Strategy ( customised & Switchable, Fixed TP)Supertrend line – a moving line that follows the price and shows whether the market is trending up or down.

If the price goes above this line, it usually means the market is going up.

If the price goes below, it usually means the market is going down.

DEMA (Double Exponential Moving Average) – another line that smooths out price movements to spot trends more clearly.

It calculates an average of prices but reacts faster than a normal moving average.

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

Faraz Perfect Structure XL / XS (Trend-Filtered)Faraz’s Perfect Structure XL/XS identifies premium trend continuation and reversal setups using a three-filter system:

structural breakouts using dynamic swing-based support/resistance,

trend confirmation via 200-EMA slope,

momentum validation through RSI and MACD.

Signals only trigger when all factors align, eliminating noise, chop, and false signals.

Designed for traders who want clean, high-probability long (XL) and short (XS) entries.

RSI BREAKOUT SIGNALSThis BB + RSI Breakout indicator is designed to help traders identify potential buy and sell opportunities based on price movements relative to the Donchian channel (or Bollinger-type channel) and momentum conditions. It calculates the highest high and lowest low over a user-defined length to form a dynamic channel, and then it checks whether the current price breaks above the upper band (for a buy signal) or below the lower band (for a sell signal). To avoid repeated signals in a row, the indicator uses a state system: after a buy signal occurs, it will not generate another buy until a sell occurs, and vice versa. When a buy signal is triggered, it automatically calculates a take-profit price a certain percentage above the buy candle and displays this price below the candle as a “TP” label. Sell signals are displayed above the candle, and any previous TP label is cleared. The indicator updates in real time, so the signals move with the chart, giving a clear and lag-free visualization of entry points and potential profit targets.

Moving Average Band StrategyOverview

The Moving Average Band Strategy is a fully customizable breakout and trend-continuation system designed for traders who need both simplicity and control.

The strategy creates adaptive bands around a user-selected moving average and executes trades when price breaks out of these bands, with advanced risk-management settings including optional Risk:Reward targets.

This script is suitable for intraday, swing, and positional traders across all markets — equities, futures, crypto, and forex.

Key Features

✔ Six Moving Average Types

Choose the MA that best matches your trading style:

SMA

EMA

WMA

HMA

VWMA

RMA

✔ Dynamic Bands

Upper Band built from MA of highs

Lower Band built from MA of lows

Adjustable band offset (%)

Color-coded band fill indicating price position

✔ Configurable Strategy Preferences

Toggle Long and/or Short trades

Toggle Risk:Reward Take-Profit

Adjustable Risk:Reward Ratio

Default position sizing: % of equity (configurable via strategy settings)

Entry Conditions

Long Entry

A long trade triggers when:

Price crosses above the Upper Band

Long trades are enabled

No existing long position is active

Short Entry

A short trade triggers when:

Price crosses below the Lower Band

Short trades are enabled

No existing short position is active

Clear entry markers and price labels appear on the chart.

Risk Management

This strategy includes a complete set of risk-controls:

Stop-Loss (Fixed at Entry)

Long SL: Lower Band

Short SL: Upper Band

These levels remain constant for the entire trade.

Optional Risk:Reward Take-Profit

Enabled/disabled using a toggle switch.

When enabled:

Long TP = Entry + (Risk × Risk:Reward Ratio)

Short TP = Entry – (Risk × Risk:Reward Ratio)

When disabled:

Exits are handled by reverse crossover signals.

Exit Conditions

Long Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Short Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Exit markers and price labels are plotted automatically.

Visual Tools

To improve clarity:

Upper & Lower Band (blue, adjustable width)

Middle Line

Dynamic band fill (green/red/yellow)

SL & TP line plotting when in position

Entry/Exit markers

Price labels for all executed trades

These are built to help users visually follow the strategy logic.

Alerts Included

Every trading event is covered:

Long Entry

Short Entry

Long SL / TP / Cross Exit

Short SL / TP / Cross Exit

Combined Alert for webhook/automation (JSON-formatted)

Perfect for algo trading, Discord bots, or automation platforms.

Best For

This strategy performs best in:

Trending markets

Breakout environments

High-momentum instruments

Clean intraday swings

Works seamlessly on:

Stocks

Index futures

Commodities

Crypto

Forex

⚠️ Important Disclaimer

This script is for educational purposes only.

Trading involves risk. Backtest results are not indicative of future performance.

Always validate settings and use proper position sizing.

Fractional Candlestick Long Only Experimental V10Fractional Candlestick Long-Only Strategy – Technical Description

This document provides a professional English description of the "Fractional Candlestick Long Only Experimental V6" strategy using pure CF/AB fractional kernels and wavelet-based filtering.

1. Fractional Candlesticks (CF / AB)

The strategy computes two fractional representations of price using Caputo–Fabrizio (CF) and Atangana–Baleanu (AB) kernels. These provide long-memory filtering without EMA approximations. Both CF and AB versions are applied to O/H/L/C, producing fractional candlesticks and fractional Heikin-Ashi variants.

2. Trend Stack Logic

Trend confirmation is based on a 4-component stack:

- CF close > AB close

- HA_CF close > HA_AB close

- HA_CF bullish

- HA_AB bullish

The user selects how many components must align (4, 3, or any 2).

3. Wavelet Filtering

A wavelet transform (Haar, Daubechies-4, Mexican Hat) is applied to a chosen source (e.g., HA_CF close). The wavelet response is used as:

- entry filter (4 modes)

- exit filter (4 modes)

Wavelet modes: off, confirm, wavelet-only, block adverse signals.

4. Trailing System

Trailing stop uses fractional AB low × buffer, providing long-memory dynamic trailing behavior. A fractional trend channel (CF/AB lows vs HA highs) is also plotted.

5. Exit Framework

Exit options include: stack flip, CF