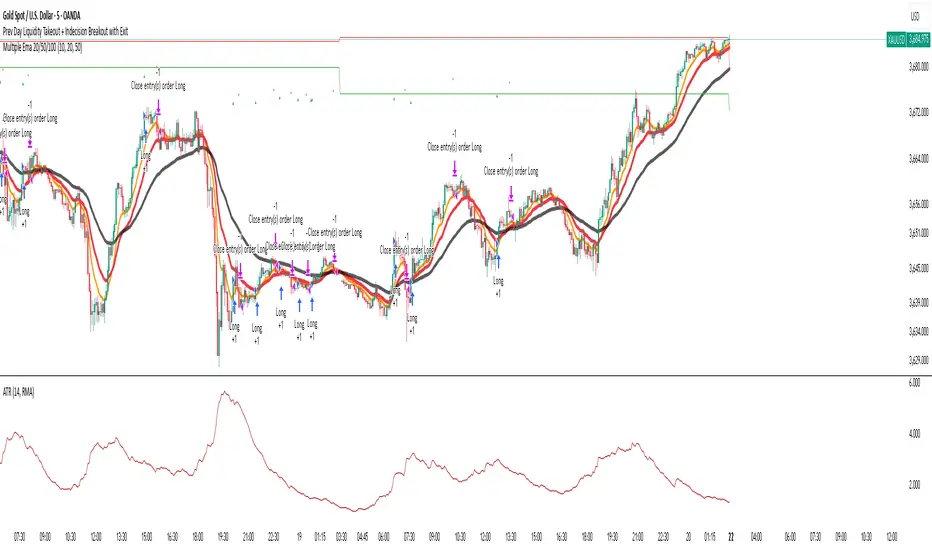

ALMASTO – Pro Trend & Momentum (v1.1)ALMASTO — Pro Trend & Momentum Strategy

Description:

This strategy is designed for precision trading in both Forex (FX) and Crypto markets.

It combines multi-timeframe trend confirmation (EMA200), momentum filters (RSI, MACD, ADX), and ATR-based dynamic risk management.

ALMASTO — Pro Trend & Momentum Strategy automatically manages take-profit levels, stop-loss, and breakeven adjustments once TP1 is reached — providing a structured and emotion-free trading approach.

Optimal Use

Works best on lower timeframes (5m–15m) with strong liquidity sessions.

Optimized for pairs like EURUSD, XAUUSD, and BTCUSDT.

Built for trend-following setups and momentum reversals with high volatility confirmation.

Recommended Settings

🔹 Forex – 5m

EMA Fast = 34, EMA Slow = 200, HTF = 1H

RSI (14): Long ≥ 55 / Short ≤ 45

MACD (8 / 21 / 5), ADX Len 10 / Min 27

ATR Len 7, Stop Loss = ATR × 2.1

TP1 = 1.1 RR, TP2 = 2.3 RR

Session = 07:00–11:00 & 12:30–16:00 (Exchange Time)

Risk = 0.8% per trade

🔹 Forex – 15m

EMA Fast = 50, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 53 / Short ≤ 47

MACD (12 / 26 / 9), ADX Min 24

ATR Len 10, SL = ATR × 1.9

TP1 = 1.2 RR, TP2 = 2.6 RR

Risk = 1.0% per trade

🔹 Crypto – 5m (BTC/USDT)

EMA Fast = 34, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 56 / Short ≤ 44

MACD (8 / 21 / 5), ADX Min 30

ATR Len 7, SL = ATR × 2.2

TP1 = 1.0 RR, TP2 = 2.5 RR

Session = 00:00–06:00 & 12:00–22:00 (UTC)

Risk = 0.5% per trade

Core Features

✅ Auto breakeven after TP1

✅ Dual take-profit system (1:1 & 1:2 RR)

✅ ATR-based stop & trailing logic

✅ Filters for session time, volume, and volatility

✅ Candle-body vs ATR size filter to avoid noise

✅ Optional cooldown between trades

Important Notes

Use bar close confirmation only (barstate.isconfirmed) to avoid repainting on lower timeframes.

Adjust commission (0.01–0.03%) and slippage (1–2 ticks) in Strategy Tester for realistic results.

Avoid low-liquidity hours (after 21:00 UTC for FX / after midnight for crypto).

Backtest using realistic broker data (e.g., BlackBull Markets / Bybit / Binance Futures).

Best results occur during London & New York sessions with moderate volatility.

⚠️ Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice.

Use proper risk management and test thoroughly before using on live accounts.

Developed by KING FX Labs

Built and optimized by Yousef Almasto — combining advanced price-action logic, multi-timeframe EMA structure, and volatility-adaptive ATR management.

Tested across Forex, Gold, and Crypto markets to ensure consistent performance and minimal drawdown.

📈 “Precision Trading. Zero Emotion. Pure Momentum.”

頻帶和通道

Camarilla Pivots + 20 EMA StrategyThis is an intraday volatility and trend-following system for commodities like Natural Gas, combining dynamic pivot levels (Camarilla) with a trend filter (20-period EMA) to improve risk-reward and reduce false breakouts.

Core Components

1. Camarilla Pivots:

These are special support and resistance levels (H3, H4, L3, L4) calculated each day based on the previous day's high, low, and close.

The pivots adapt to daily volatility, giving more relevant breakout and bounce zones than static lines.

H4: Aggressive resistance (used for breakout LONG entry)

H3: Moderate resistance/support (used for bounce or stoploss)

L4: Aggressive support (used for breakout SHORT entry)

L3: Moderate support/resistance (used for bounce or stoploss)

2. 20 EMA (Exponential Moving Average):

Plotted on the 30-minute chart, this acts as a trend filter.

If the price is above 20 EMA: Only look for long trades (bullish bias).

If below 20 EMA: Only look for short trades (bearish bias).

How the Strategy Works

Setup (30-Min Chart):

Camarilla pivots for the day are drawn on the chart.

20 EMA is also plotted.

Trade Filter:

Bullish: Trade ONLY if price is above 20 EMA.

Bearish: Trade ONLY if price is below 20 EMA.

Entry:

LONG: Enter when price breaks and closes above the H4 pivot AND is above 20 EMA.

SHORT: Enter when price breaks and closes below the L4 pivot AND is below 20 EMA.

Stop Loss:

LONG: Place stoploss at H3 (the next lower Camarilla resistance).

SHORT: Place stoploss at L3 (the next higher Camarilla support).

Target:

Always set a profit target at 2x the distance (risk) between entry and stoploss (strict R:R 2).

For example, if your entry is at H4 and stoploss at H3, your target is entry + 2*(entry - stoploss).

Alerts & Visuals:

The strategy plots entry arrows, stoploss and target lines for immediate visual reference.

Alerts trigger on breakout signals so you never miss a trade.

Why This Works Well for Natural Gas

Adapts to volatility: The pivots change daily, handling wide-ranging and choppy price moves better than fixed breakouts.

Trend filter: EMA prevents counter-trend whipsaws, only trades with market momentum.

Risk control: Every trade must meet strict risk-reward criteria, so losses are contained and winners can outweigh losers.

Natural Gas Intraday Strategy [15m] with Partial Profit & TrailBuy when:

1. Close > EMA 100 and EMA 20 > EMA 100

2. MACD (8,21,5) > Signal and histogram rising

3. RSI > 60

4. ATR > threshold (avoid flat market)

Sell when:

1. Close < EMA 100 and EMA 20 < EMA 100

2. MACD (8,21,5) < Signal and histogram falling

3. RSI < 40

4. ATR > threshold

Exit:

• SL = recent swing ± 0.5 ATR

• TP1 = 1 ATR, trail rest with EMA 20

Investorjordann - Script I have developed a script for the BTC pair. I'm currently trialing this...it is using multiple indicators and timeframes to trigger a trade. So far it seems very profitable across many timeframes, but I am still trailing.

Elliott Wave Auto + Fib Targets + Scalper Strategy (Fixed)// Elliott Wave Auto + Fib Targets + Scalper Strategy

//

// Fixed by expert trader:

// - Replaced table with label-based visualization to avoid 'Column 2 is out of table bounds' error.

// - Uses label.new to display buy/sell signal counts in top-right corner, mimicking table layout.

// - Fixed array.sum() error: Replaced invalid range-based array.sum() with custom sum_array_range() function.

// - Removed barstate usage to fix 'Undeclared identifier barstate' error.

// - Replaced barstate.isconfirmed with true (process every bar).

// - Replaced barstate.isfirstconfirmed with bar_index == 0 (first bar).

// - Replaced strategy.alert with label.new for long/short entry signals (buy/sell markers).

// - Fixed array index out-of-bounds: Protected array.get() calls with size checks.

// - Fixed pyramiding: Set constant pyramiding=4 (max 5 entries); use allow_pyramiding to limit entries.

// - Fixed default_qty_value: Set constant default_qty_value=100.0; use entry_size_pct to scale qty.

// - Replaced alertcondition with labels for Elliott Wave patterns.

// - Fixed partial exits: 50% at TP1 with fixed SL, 50% at TP2 with fixed SL or trailing.

// - Fixed Elliott Wave pivot indexing for alternating H/L check.

// - Ensured proper position sizing and exit logic.

BOCS Channel Scalper Strategy - Automated Mean Reversion System# BOCS Channel Scalper Strategy - Automated Mean Reversion System

## WHAT THIS STRATEGY DOES:

This is an automated mean reversion trading strategy that identifies consolidation channels through volatility analysis and executes scalp trades when price enters entry zones near channel boundaries. Unlike breakout strategies, this system assumes price will revert to the channel mean, taking profits as price bounces back from extremes. Position sizing is fully customizable with three methods: fixed contracts, percentage of equity, or fixed dollar amount. Stop losses are placed just outside channel boundaries with take profits calculated either as fixed points or as a percentage of channel range.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This strategy is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Version**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the scalper ideal for active day traders who want continuous opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased trade frequency also means higher commission costs and requires tighter risk management.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The strategy normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The strategy tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The strategy uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. This captures mean reversion opportunities as price reaches channel extremes.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents signal spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long signal will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The strategy includes a multi-timeframe ATR filter to avoid trading during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while trading on 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Trading enabled

- If ATR < threshold: No signals fire

This prevents entries during dead zones where mean reversion is unreliable due to insufficient price movement.

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. Larger percentages aim for opposite channel edge.

### Stop Loss Placement:

Stop losses are placed just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. If price breaks through, the range is no longer valid and position exits.

### Trade Execution Logic:

When entry conditions are met (price in zone, cooldown satisfied, ATR filter passed, no existing position):

1. Calculate entry price at zone boundary

2. Calculate TP and SL based on selected method

3. Execute strategy.entry() with calculated position size

4. Place strategy.exit() with TP limit and SL stop orders

5. Update info table with active trade details

The strategy enforces one position at a time by checking strategy.position_size == 0 before entry.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

### Position Sizing System:

Three methods calculate position size:

**Fixed Contracts**:

- Uses exact contract quantity specified in settings

- Best for futures traders (e.g., "trade 2 NQ contracts")

**Percentage of Equity**:

- position_size = (strategy.equity × equity_pct / 100) / close

- Dynamically scales with account growth

**Cash Amount**:

- position_size = cash_amount / close

- Maintains consistent dollar exposure regardless of price

## INPUT PARAMETERS:

### Position Sizing:

- **Position Size Type**: Choose Fixed Contracts, % of Equity, or Cash Amount

- **Number of Contracts**: Fixed quantity per trade (1-1000)

- **% of Equity**: Percentage of account to allocate (1-100%)

- **Cash Amount**: Dollar value per position ($100+)

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long entries on/off

- **Enable Short Scalps**: Toggle short entries on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between signals (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for trade enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time strategy status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Color Settings**: Customize long/short/TP/SL colors

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short entries

- **Active TP/SL lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing position status, channel state, last signal, entry/TP/SL prices, and ATR status

## HOW TO USE:

### For 1-3 Minute Scalping (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars

- Position Size: 1-2 contracts

### For 5-15 Minute Day Trading:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- Position Size: Fixed contracts or 5-10% equity

### For 30-60 Minute Swing Scalping:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- Position Size: % of equity recommended

## BACKTEST CONSIDERATIONS:

- Strategy performs best in ranging, mean-reverting markets

- Strong trending markets produce more stop losses as price breaks channels

- ATR filter significantly reduces trade count but improves quality during low volatility

- Cooldown period trades signal quantity for signal quality

- Commission and slippage materially impact sub-5-minute timeframe performance

- Shorter timeframes require tighter entry zones (15-20%) to catch quick reversions

- % of Channel TP adapts better to varying channel sizes than fixed points

- Fixed contract sizing recommended for consistent risk per trade in futures

**Backtesting Parameters Used**: This strategy was developed and tested using realistic commission and slippage values to provide accurate performance expectations. Recommended settings: Commission of $1.40 per side (typical for NQ futures through discount brokers), slippage of 2 ticks to account for execution delays on fast-moving scalp entries. These values reflect real-world trading costs that active scalpers will encounter. Backtest results without proper cost simulation will significantly overstate profitability.

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features require data feed with volume information but are optional for core functionality.

## KNOWN LIMITATIONS:

- Immediate touch entry can fire multiple times in choppy zones without adequate cooldown

- Channel deletion at 10-tick breaks may be too aggressive or lenient depending on instrument tick size

- ATR filter from lower timeframes requires higher-tier TradingView subscription (request.security limitation)

- Mean reversion logic fails in strong breakout scenarios leading to stop loss hits

- Position sizing via % of equity or cash amount calculates based on close price, may differ from actual fill price

- No partial closing capability - full position exits at TP or SL only

- Strategy does not account for gap openings or overnight holds

## RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance does not guarantee future results. This strategy is for educational purposes and backtesting only. Mean reversion strategies can experience extended drawdowns during trending markets. Stop losses may not fill at intended levels during extreme volatility or gaps. Thoroughly test on historical data and paper trade before risking real capital. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Automated trading systems can malfunction - monitor all live positions actively.

## ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based signals, multi-timeframe ATR volatility filtering, flexible position sizing (fixed/percentage/cash), cooldown period filtering, dual TP methods (fixed points vs channel percentage), automated strategy execution with exit management, and real-time position monitoring table.

Parthiban Stock Market Buy V2 - Buy onlyFor BUY, condition

continuos 3 down candle

then forms Indecision candle

next candle close above Indecision candle

price above 500 EMA

For sell, condition

continuos 3 up candle

then forms Indecision candle

next candle close below Indecision candle

price below 500 EMA

Parthiban - Stock Market BuyParthiban - Stock Market Buy

For BUY, condition

continuos 3 down candle

then forms Indecision candle

next candle close above Indecision candle

price above 500 EMA

For sell, condition

continuos 3 up candle

then forms Indecision candle

next candle close below Indecision candle

price below 500 EMA

Indecision Candle with 2 Candle Confirmation + 500 EMA - parthibIndecision Candle with 2 Candle Confirmation + 500 EMA

Indecision Candle with 2 Candle Confirmation + 500 EMA

Indecision Candle with 2 Candle Confirmation + 500 EMAIndecision Candle with 2 Candle Confirmation + 500 EMAIndecision Candle with 2 Candle Confirmation + 500 EMA

维加斯双通道策略Vegas Channel Comprehensive Strategy Description

Strategy Overview

A comprehensive trading strategy based on the Vegas Dual Channel indicator, supporting dynamic position sizing and fund management. The strategy employs a multi-signal fusion mechanism including classic price crossover signals, breakout signals, and retest signals, combined with trend filtering, RSI+MACD filtering, and volume filtering to ensure signal reliability.

Core Features

Dynamic Position Sizing: Continue adding positions on same-direction signals, close all positions on opposite signals

Smart Take Profit/Stop Loss: ATR-based dynamic TP/SL, updated with each new signal

Fund Management: Supports dynamic total amount management for compound growth

Time Filtering: Configurable trading time ranges

Risk Control: Maximum order limit to prevent over-leveraging

Leverage Usage Instructions

Important: This strategy does not use TradingView's margin functionality

Setup Method

Total Amount = Actual Funds × Leverage Multiplier

Example: Have 100U actual funds, want to use 10x leverage → Set total amount to 100 × 10 = 1000U

Trading Amount Calculation

Each trade percentage is calculated based on leveraged amount

Example: Set 10% → Actually trade 100U margin × 10x leverage = 1000U trading amount

Maximum Orders Configuration

Must be used in conjunction with leveraged amount

Example: 1000U total amount, 10% per trade, maximum 10 orders = maximum use of 1000U

Note: Do not exceed 100% of total amount to avoid over-leveraging

Parameter Configuration Recommendations

Leverage Configuration Examples

Actual funds 100U, 5x leverage, total amount setting 500U, 10% per trade, 50U per trade, recommended maximum orders 10

Actual funds 100U, 10x leverage, total amount setting 1000U, 10% per trade, 100U per trade, recommended maximum orders 10

Actual funds 100U, 20x leverage, total amount setting 2000U, 5% per trade, 100U per trade, recommended maximum orders 20

Risk Control

Conservative: 5-10x leverage, 10% per trade, maximum 5-8 orders

Aggressive: 10-20x leverage, 5-10% per trade, maximum 10-15 orders

Extreme: 20x+ leverage, 2-5% per trade, maximum 20+ orders

Strategy Advantages

Signal Reliability: Multiple filtering mechanisms reduce false signals

Capital Efficiency: Dynamic fund management for compound growth

Risk Controllable: Maximum order limits prevent liquidation

Flexible Configuration: Supports various leverage and fund allocation schemes

Time Control: Configurable trading hours to avoid high-risk periods

Usage Notes

Ensure total amount is set correctly (actual funds × leverage multiplier)

Maximum orders should not exceed the range allowed by total funds

Recommend starting with conservative configuration and gradually adjusting parameters

Regularly monitor strategy performance and adjust parameters timely

维加斯通道综合策略说明

策略概述

基于维加斯双通道指标的综合交易策略,支持动态加仓和资金管理。策略采用多信号融合机制,包括经典价穿信号、突破信号和回踩信号,结合趋势过滤、RSI+MACD过滤和成交量过滤,确保信号的可靠性。

核心功能

动态加仓:同向信号继续加仓,反向信号全部平仓

智能止盈止损:基于ATR的动态止盈止损,每次新信号更新

资金管理:支持动态总金额管理,实现复利增长

时间过滤:可设置交易时间范围

风险控制:最大订单数限制,防止过度加仓

杠杆使用说明

重要:本策略不使用TradingView的保证金功能

设置方法

总资金 = 实际资金 × 杠杆倍数

示例:实际有100U,想使用10倍杠杆 → 总资金设置为 100 × 10 = 1000U

交易金额计算

每笔交易百分比基于杠杆后的金额计算

示例:设置10% → 实际交易 100U保证金 × 10倍杠杆 = 1000U交易金额

最大订单数配置

必须配合杠杆后的金额使用

示例:1000U总资金,10%单笔,最大10单 = 最多使用1000U

注意:不要超过总资金的100%,避免过度杠杆

参数配置建议

杠杆配置示例

实际资金100U,5倍杠杆,总资金设置500U,单笔百分比10%,单笔金额50U,建议最大订单数10单

实际资金100U,10倍杠杆,总资金设置1000U,单笔百分比10%,单笔金额100U,建议最大订单数10单

实际资金100U,20倍杠杆,总资金设置2000U,单笔百分比5%,单笔金额100U,建议最大订单数20单

风险控制

保守型:5-10倍杠杆,10%单笔,最大5-8单

激进型:10-20倍杠杆,5-10%单笔,最大10-15单

极限型:20倍以上杠杆,2-5%单笔,最大20单以上

策略优势

信号可靠性:多重过滤机制,减少假信号

资金效率:动态资金管理,实现复利增长

风险可控:最大订单数限制,防止爆仓

灵活配置:支持多种杠杆和资金配置方案

时间控制:可设置交易时间,避开高风险时段

使用注意事项

确保总资金设置正确(实际资金×杠杆倍数)

最大订单数不要超过总资金允许的范围

建议从保守配置开始,逐步调整参数

定期监控策略表现,及时调整参数

Nirvana True Duel전략 이름

열반의 진검승부 (영문: Nirvana True Duel)

컨셉과 철학

“열반의 진검승부”는 시장 소음은 무시하고, 확실할 때만 진입하는 전략입니다.

EMA 리본으로 추세 방향을 확인하고, 볼린저 밴드 수축/확장으로 변동성 돌파를 포착하며, OBV로 거래량 확인을 통해 가짜 돌파를 필터링합니다.

전략 로직

매수 조건 (롱)

20EMA > 50EMA (상승 추세)

밴드폭 수축 후 확장 시작

종가가 상단 밴드 돌파

OBV 상승 흐름 유지

매도 조건 (숏)

20EMA < 50EMA (하락 추세)

밴드폭 수축 후 확장 시작

종가가 하단 밴드 이탈

OBV 하락 흐름 유지

진입·청산

손절: ATR × 1.5 배수

익절: 손절폭의 1.5~2배에서 부분 청산

시간 청산: 설정한 최대 보유 봉수 초과 시 강제 청산

장점

✅ 추세·변동성·거래량 3중 필터 → 노이즈 최소화

✅ 백테스트·알람 지원 → 기계적 매매 가능

✅ 5분/15분 차트에 적합 → 단타/스윙 트레이딩 활용 가능

주의점

⚠ 횡보장에서는 신호가 적거나 실패 가능

⚠ 수수료·슬리피지 고려 필요

📜 Nirvana True Duel — Strategy Description (English)

Name:

Nirvana True Duel (a.k.a. Nirvana Cross)

Concept & Philosophy

The “Nirvana True Duel” strategy focuses on trading only meaningful breakouts and avoiding unnecessary noise.

Nirvana: A calm, patient state — waiting for the right opportunity without emotional trading.

True Duel: When the signal appears, enter decisively and let the market reveal the outcome.

In short: “Ignore market noise, trade only high-probability breakouts.”

🧩 Strategy Components

Trend Filter (EMA Ribbon): Stay aligned with the main market trend.

Volatility Squeeze (Bollinger Band): Detect volatility contraction & expansion to catch explosive moves early.

Volume Confirmation (OBV): Filter out false breakouts by confirming with volume flow.

⚔️ Entry & Exit Conditions

Long Setup:

20 EMA > 50 EMA (uptrend)

BB width breaks out from recent squeeze

Close > Upper Bollinger Band

OBV shows positive flow

Short Setup:

20 EMA < 50 EMA (downtrend)

BB width breaks out from recent squeeze

Close < Lower Bollinger Band

OBV shows negative flow

Risk Management:

Stop Loss: ATR × 1.5 below/above entry

Take Profit: 1.5–2× stop distance, partial take-profit allowed

Time Stop: Automatically closes after max bars held (e.g. 8h on 5m chart)

✅ Strengths

Triple Filtering: Trend + Volatility + Volume → fewer false signals

Mechanical & Backtestable: Ideal for objective trading & performance validation

Adaptable: Works well on Bitcoin, Nasdaq futures, and other high-volatility markets (5m/15m)

⚠️ Things to Note

Low signal frequency or higher failure rate in sideways/range markets

Commission & slippage should be factored in, especially on lower timeframes

ATR multiplier and R:R ratio should be optimized per asset

Hilly's 0010110 Reversal Scalping Strategy - 5 Min CandlesKey Features and Rationale:

Timeframe: Restricted to 5-minute candles as requested.

Pattern Integration: Includes single (Hammer, Shooting Star, Doji), two (Engulfing, Harami), and three-plus (Morning Star, Evening Star) candlestick patterns, plus reversal patterns based on RSI extremes.

VWAP Cross: Incorporates bullish (price crosses above VWAP) and bearish (price crosses below VWAP) signals, enhanced by trend context.

Volume Analysis: Uses a volume spike threshold to filter noise, with a simple day-start volume comparison for financial environment context.

Financial Environment: Approximates the day's sentiment using early-hour volume compared to current volume, adjusted by trend.

Aggregation: Scores each condition (e.g., 1 for basic patterns, 2 for strong patterns like Engulfing, 3 for three-candle patterns) and decides based on weighted consensus, with trendStrength as a tunable threshold.

Risky Approach: Minimal filtering and a low trendStrength (default 0.5) allow frequent signals, aligning with your $100-to-$200 goal, but expect higher risk.

Suggested Inputs:

EMA Length: 10 (short enough for 5-minute sensitivity).

VWAP Lookback: 1 (uses current session VWAP).

Volume Threshold Multiplier: 1.2 (moderate spike requirement).

RSI Length: 14 (standard, adjustable to 7 for more sensitivity).

Trend Strength Threshold: 0.5 (balance between signals; lower to 0.4 for more trades, raise to 0.6 for fewer).

QZ Trend (Crypto Edition) v1.1a: Donchian, EMA, ATR, Liquidity/FThe "QZ Trend (Crypto Edition)" is a rules-based trend-following breakout strategy for crypto spot or perpetual contracts, focusing on following trends, prioritizing risk control, seeking small losses and big wins, and trading only when advantageous.

Key mechanisms include:

- Market filters: Screen favorable conditions via ADX (trend strength), dollar volume (liquidity), funding fee windows, session/weekend restrictions, and spot-long-only settings.

- Signals & entries: Based on price position relative to EMA and EMA trends, combined with breaking Donchian channel extremes (with ATR ratio confirmation), plus single-position rules and post-exit cooldowns.

- Position sizing: Calculate positions by fixed risk percentage; initial stop-loss is ATR-based, complying with exchange min/max lot requirements.

- Exits & risk management: Include initial stop-loss, trailing stop (tightens only), break-even rule (stop moves to entry when target floating profit is hit), time-based exit, and post-exit cooldowns.

- Pyramiding: Add positions only when profitable with favorable momentum, requiring ATR-based spacing; add size is a fraction of the base position, with layers sharing stop logic but having unique order IDs.

Charts display EMA, Donchian channels, current stop lines, and highlight low ADX, avoidable funding windows, and low-liquidity periods.

Recommend starting with 4H or 1D timeframes, with typical parameters varying by cycle. Liquidity settings differ by token; perpetuals should enable funding window filters, while spot requires "long-only" and matching fees. The strategy performs well in trends with quick stop-losses but faces whipsaws in ranges (filters mitigate but don’t eliminate noise). Share your symbol and timeframe for tailored parameters.

kaka 谈趋势The Exponential Moving Average (EMA) strategy is a popular technical analysis tool used in trading to smooth price data over a specific time period. The EMA gives more weight to recent prices, making it more responsive to recent price changes compared to the Simple Moving Average (SMA).

TheWave + Supertrend Hybrid w/ Signals• Green triangle below bar → Long entry signal

• Red triangle above bar → Short entry signal

• Small lime cross above/below → Take-profit hit

• Small maroon cross above/below → Stop-loss hit

• SMA5 and Supertrend lines for trend context

This version makes all entries and exits visually obvious while keeping the hybrid TheWave + Supertrend logic intact.

TheWaveStrategy v6 - QQE + ATR (Optional Trailing)New Version Of the wave with QQE and ATR

• Compiles cleanly in Pine v6.

• Optional trailing stop toggle via useTrailingATR.

• Market exit uses strategy.close() properly.

• ATR spike filter uses 5m ATR.

• QQE confluence with 30m timeframe included.

Hilly's Advanced Crypto Scalping Strategy - 5 Min ChartTo determine the "best" input parameters for the Advanced Crypto Scalping Strategy on a 5-minute chart, we need to consider the goals of optimizing for profitability, minimizing false signals, and adapting to the volatile nature of cryptocurrencies. The default parameters in the script are a starting point, but the optimal values depend on the specific cryptocurrency pair, market conditions, and your risk tolerance. Below, I'll provide recommended input values based on common practices in crypto scalping, along with reasoning for each parameter. I’ll also suggest how to fine-tune them using TradingView’s backtesting and optimization tools.

Recommended Input Parameters

These values are tailored for a 5-minute chart for liquid cryptocurrencies like BTC/USD or ETH/USD on exchanges like Binance or Coinbase. They aim to balance signal frequency and accuracy for day trading.

Fast EMA Length (emaFastLen): 9

Reasoning: A 9-period EMA is commonly used in scalping to capture short-term price movements while remaining sensitive to recent price action. It reacts faster than the default 10, aligning with the 5-minute timeframe.

Slow EMA Length (emaSlowLen): 21

Reasoning: A 21-period EMA provides a good balance for identifying the broader trend on a 5-minute chart. It’s slightly longer than the default 20 to reduce noise while confirming the trend direction.

RSI Length (rsiLen): 14

Reasoning: The default 14-period RSI is a standard choice for momentum analysis. It works well for detecting overbought/oversold conditions without being too sensitive on short timeframes.

RSI Overbought (rsiOverbought): 75

Reasoning: Raising the overbought threshold to 75 (from 70) reduces false sell signals in strong bullish trends, which are common in crypto markets.

RSI Oversold (rsiOversold): 25

Reasoning: Lowering the oversold threshold to 25 (from 30) filters out weaker buy signals, ensuring entries occur during stronger reversals.

MACD Fast Length (macdFast): 12

Reasoning: The default 12-period fast EMA for MACD is effective for capturing short-term momentum shifts in crypto, aligning with scalping goals.

MACD Slow Length (macdSlow): 26

Reasoning: The default 26-period slow EMA is a standard setting that works well for confirming momentum trends without lagging too much.

MACD Signal Smoothing (macdSignal): 9

Reasoning: The default 9-period signal line is widely used and provides a good balance for smoothing MACD crossovers on a 5-minute chart.

Bollinger Bands Length (bbLen): 20

Reasoning: The default 20-period Bollinger Bands are effective for identifying volatility breakouts, which are key for scalping in crypto markets.

Bollinger Bands Multiplier (bbMult): 2.0

Reasoning: A 2.0 multiplier is standard and captures most price action within the bands. Increasing it to 2.5 could reduce signals but improve accuracy in highly volatile markets.

Stop Loss % (slPerc): 0.8%

Reasoning: A tighter stop loss of 0.8% (from 1.0%) suits the high volatility of crypto, helping to limit losses on false breakouts while keeping risk manageable.

Take Profit % (tpPerc): 1.5%

Reasoning: A 1.5% take-profit target (from 2.0%) aligns with scalping’s goal of capturing small, frequent gains. Crypto markets often see quick reversals, so a smaller target increases the likelihood of hitting profits.

Use Candlestick Patterns (useCandlePatterns): True

Reasoning: Enabling candlestick patterns (e.g., engulfing, hammer) adds confirmation to signals, reducing false entries in choppy markets.

Use Volume Filter (useVolumeFilter): True

Reasoning: The volume filter ensures signals occur during high-volume breakouts, which are more likely to sustain in crypto markets.

Signal Arrow Size (signalSize): 2.0

Reasoning: Increasing the arrow size to 2.0 (from 1.5) makes buy/sell signals more visible on the chart, especially on smaller screens or volatile price action.

Background Highlight Transparency (bgTransparency): 85

Reasoning: A slightly higher transparency (85 from 80) keeps the background highlights subtle but visible, avoiding chart clutter.

How to Apply These Parameters

Copy the Script: Use the Pine Script provided in the previous response.

Paste in TradingView: Open TradingView, go to the Pine Editor, paste the code, and click "Add to Chart."

Set Parameters: In the strategy settings, manually input the recommended values above or adjust them via the input fields.

Test on a 5-Minute Chart: Apply the strategy to a liquid crypto pair (e.g., BTC/USDT, ETH/USDT) on a 5-minute chart.

Fine-Tuning for Optimal Performance

To find the absolute best parameters for your specific trading pair and market conditions, use TradingView’s Strategy Tester and optimization features:

Backtesting:

Run the strategy on historical data for your chosen pair (e.g., BTC/USDT on Binance).

Check metrics like Net Profit, Profit Factor, Win Rate, and Max Drawdown in the Strategy Tester.

Focus on a sample period of at least 1–3 months to capture various market conditions (bull, bear, sideways).

Parameter Optimization:

In the Strategy Tester, click the settings gear next to the strategy name.

Enable optimization for key inputs like emaFastLen (test range: 7–12), emaSlowLen (15–25), slPerc (0.5–1.5), and tpPerc (1.0–3.0).

Run the optimization to find the combination with the highest net profit or best Sharpe ratio, but avoid over-optimization (curve-fitting) by testing on out-of-sample data.

Market-Specific Adjustments:

Volatile Pairs (e.g., DOGE/USDT): Use tighter stop losses (e.g., 0.5–0.7%) and smaller take-profit targets (e.g., 1.0–1.2%) to account for rapid price swings.

Stable Pairs (e.g., BTC/USDT): Slightly wider stop losses (e.g., 1.0–1.2%) and take-profit targets (e.g., 1.8–2.5%) may work better.

Trending Markets: Increase emaSlowLen (e.g., to 25–30) to follow stronger trends.

Choppy Markets: Tighten bbMult (e.g., to 1.8) and lower rsiOverbought/rsiOversold (e.g., to 70/30) to filter noise.

Forward Testing:

After backtesting, run the strategy in real-time on a demo account for 1–2 weeks to validate performance under current market conditions.

Important Notes

No Universal "Best" Numbers: Optimal parameters vary by crypto pair, exchange, and market conditions (e.g., bull vs. bear market). The suggested values are a starting point based on common scalping practices.

Risk Management: Never risk more than 1–2% of your account per trade. Adjust position sizing in TradingView’s strategy settings to align with your risk tolerance.

Market Volatility: Crypto markets are highly volatile. Test the strategy on your specific pair and adjust parameters if signals are too frequent or too rare.

Not Financial Advice: This is an educational tool. Backtest thoroughly and use a demo account before trading with real funds.

If you want me to generate a chart showing backtest performance for specific parameters or to tweak the script further (e.g., adding more indicators or adjusting signal logic), let me know!can you add clear buy ans sell signs above the candles in this codeTo add clear buy and sell signals above the candles in the provided Pine Script, I'll modify the existing code to include prominent text labels directly above (for sell signals) and below (for buy signals) the candles. These labels will be larger, color-coded, and positioned to avoid clutter, ensuring they are easily visible on the chart. The core strategy logic (EMA, RSI, MACD, Bollinger Bands, candlestick patterns, and volume filter) will remain unchanged, and I'll reuse the same artifact_id since this is an update to the previous script.AdvancedCryptoScalpingStrategy.pinex-pine

Turtle 20-Day Breakout + ATR (v6 Clean)20-bar breakout entries

ATR protective stops

Classic 10-bar opposite breakout exits

Proper plotting of breakout levels and stops

Signals on chart

Alert conditions in global scop

dabilThe strategy is probably to go short or long with the trend depending on the case, but if all time units 1 minute then 3 minutes then 5 minutes then 15 minutes then 1 hour all show the same direction, but first the 1 hour must be bullish in which the 1 hour candle closes above the previous one, for example if the trend is bearish then the market wants to change direction, then a 1 hour bullish close must then be followed by a 1 hour bearish close below the bullish candle, then another bullish candle must shoot above the previous bullish candle, then 15 minutes also shoot above the previous 15 bullish candles, then 1 and 2...3.5. Then I can rise with the market by only covering the last 15 bullish candles with my stop loss, if my SL is 50 pips then I want 100 pips and then I'm out.

EMA MACD - 5-20Based on Crossover and Big timeframe EMA Support and resistance this strategy is developed.

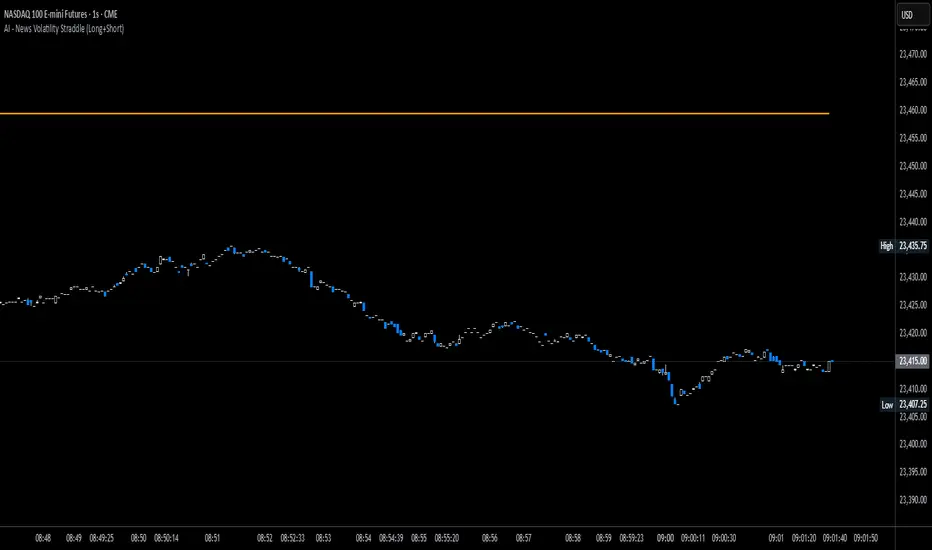

News Volatility Bracketing StrategyThis is a news-volatility bracketing strategy. Five seconds before a scheduled release, the strategy brackets price with a buy-stop above and a sell-stop below (OCO), then converts the untouched side into nothing while the filled side runs with a 1:1 TP/SL set the same distance from entry. Distances are configurable in USD or %, so it scales to the instrument and can run on 1-second data (or higher TF with bar-magnifier). The edge it’s trying to capture is the immediate, one-directional burst and liquidity vacuum that often follows market-moving news—entering on momentum rather than predicting direction. Primary risks are slippage/spread widening and whipsaws right after the print, which can trigger an entry then snap back to the stop.

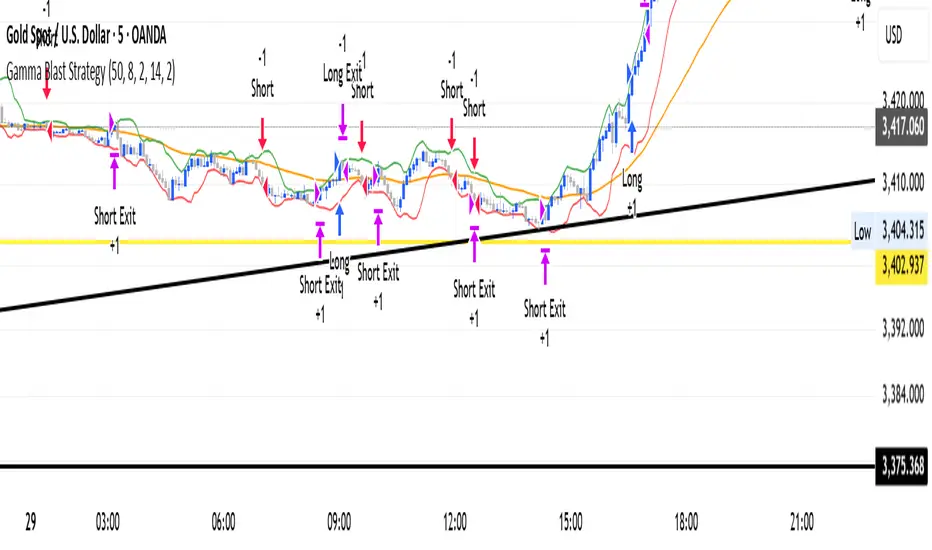

Gamma Blast StrategyGamma Blast Strategy used for quick 2-5 ticks on Buys, but on a sideways market can get up to 15-20 ticks.

Maiko Range Scalper (Sideways BB + RSI) – v4 cleanPurpose

It’s a range scalping strategy for crypto. It tries to take small, repeatable trades inside a sideways market: buy near the bottom of the range, sell near the middle/top (and the reverse for shorts).

Core idea (two timeframes)

Define the trading range on a higher timeframe (HTF)

You choose the HTF (e.g., 15m or 1h).

The script finds the highest high and lowest low over a lookback window (e.g., last 96 HTF candles) → these become HTF Resistance and HTF Support.

It also calculates the midline (average of support/resistance).

Trade signals on your lower timeframe (LTF)

You run the strategy on a fast chart (e.g., 1m or 5m).

Entries are only allowed inside the HTF range.

Entry logic (mean reversion)

Indicators on the LTF:

Bollinger Bands (length & std dev configurable).

RSI (length & thresholds configurable).

Optional VWAP proximity filter (price must be within X% of VWAP).

Long setup:

Price touches/under-cuts the lower Bollinger band AND RSI ≤ threshold (default 30) AND price is inside the HTF range (and passes VWAP filter if enabled).

Short setup:

Price touches/exceeds the upper Bollinger band AND RSI ≥ threshold (default 70) AND price is inside the HTF range (and passes VWAP filter if enabled).

Exits and risk

Stop-loss: placed just outside the HTF range with a configurable buffer %:

Long SL = HTF Support × (1 − buffer).

Short SL = HTF Resistance × (1 + buffer).

Take-profit (selectable):

Mid band (the Bollinger basis) → conservative, faster exits.

Opposite band / HTF boundary → more aggressive, higher RR but more give-backs.

Position sizing

A simple cap: maximum position size = percent of account equity (e.g., 20%).

The script calculates quantity from that cap and current price.

Plots you’ll see on the chart

HTF Resistance (red) and HTF Support (green) via plot().

HTF Midline (gray dashed) drawn with a line.new() object (because plot() cannot do dashed).

Bollinger basis/upper/lower on the LTF.

Optional VWAP line (only shown if you enable the filter).

Signal markers (green triangle up for Long setups, red triangle down for Short setups).

Alerts

Two alertconditions:

“Long Setup” – when a long entry condition appears.

“Short Setup” – when a short entry condition appears.

Create alerts from these to get notified in real time.

How to use it (quick start)

Add to a 1m or 5m chart of a liquid coin (BTC, ETH, SOL).

Set HTF timeframe (start with 1h) and lookback (e.g., 96 = ~4 days on 1h).

Keep default Bollinger/RSI first; tune later.

Choose TP mode:

“Mid band” for quick scalps.

“Opposite band/Range” if the range is very clean and you want bigger targets.

Set SL buffer (0.15–0.30% is common; adjust for volatility).

Set Max position % to control size (e.g., 20%).

(Optional) Enable VWAP filter to skip stretched moves.

When it works best

Clearly sideways markets with visible support/resistance on the HTF.

High-liquidity pairs where spreads/fees are small relative to your scalp target.

Limitations & safety notes

True breakouts will invalidate mean-reversion logic—your SL outside the range is there to cut losses fast.

Fees can eat into small scalps—prefer limit orders, rebates, and liquid pairs.

Backtest results vary by exchange data; always forward-test on small size.

If you want, I can:

Add an ATR-based stop/target option.

Provide a study-only version (signals/alerts, no trading engine).

Pre-set risk to your €5,000 plan (e.g., ~0.5% max loss/trade) with calculated qty.