Sharpe Ratio Forced Selling StrategyThis study introduces the “Sharpe Ratio Forced Selling Strategy”, a quantitative trading model that dynamically manages positions based on the rolling Sharpe Ratio of an asset’s excess returns relative to the risk-free rate. The Sharpe Ratio, first introduced by Sharpe (1966), remains a cornerstone in risk-adjusted performance measurement, capturing the trade-off between return and volatility. In this strategy, entries are triggered when the Sharpe Ratio falls below a specified low threshold (indicating excessive pessimism), and exits occur either when the Sharpe Ratio surpasses a high threshold (indicating optimism or mean reversion) or when a maximum holding period is reached.

The underlying economic intuition stems from institutional behavior. Institutional investors, such as pension funds and mutual funds, are often subject to risk management mandates and performance benchmarking, requiring them to reduce exposure to assets that exhibit deteriorating risk-adjusted returns over rolling periods (Greenwood and Scharfstein, 2013). When risk-adjusted performance improves, institutions may rebalance or liquidate positions to meet regulatory requirements or internal mandates, a behavior that can be proxied effectively through a rising Sharpe Ratio.

By systematically monitoring the Sharpe Ratio, the strategy anticipates when “forced selling” pressure is likely to abate, allowing for opportunistic entries into assets priced below fundamental value. Exits are equally mechanized, either triggered by Sharpe Ratio improvements or by a strict time-based constraint, acknowledging that institutional rebalancing and window-dressing activities are often time-bound (Coval and Stafford, 2007).

The Sharpe Ratio is particularly suitable for this framework due to its ability to standardize excess returns per unit of risk, ensuring comparability across timeframes and asset classes (Sharpe, 1994). Furthermore, adjusting returns by a dynamically updating short-term risk-free rate (e.g., US 3-Month T-Bills from FRED) ensures that macroeconomic conditions, such as shifting interest rates, are accurately incorporated into the risk assessment.

While the Sharpe Ratio is an efficient and widely recognized measure, the strategy could be enhanced by incorporating alternative or complementary risk metrics:

• Sortino Ratio: Unlike the Sharpe Ratio, the Sortino Ratio penalizes only downside volatility (Sortino and van der Meer, 1991). This would refine entries and exits to distinguish between “good” and “bad” volatility.

• Maximum Drawdown Constraints: Integrating a moving window maximum drawdown filter could prevent entries during persistent downtrends not captured by volatility alone.

• Conditional Value at Risk (CVaR): A measure of expected shortfall beyond the Value at Risk, CVaR could further constrain entry conditions by accounting for tail risk in extreme environments (Rockafellar and Uryasev, 2000).

• Dynamic Thresholds: Instead of static Sharpe thresholds, one could implement dynamic bands based on the historical distribution of the Sharpe Ratio, adjusting for volatility clustering effects (Cont, 2001).

Each of these risk parameters could be incorporated into the current script as additional input controls, further tailoring the model to different market regimes or investor risk appetites.

References

• Cont, R. (2001) ‘Empirical properties of asset returns: stylized facts and statistical issues’, Quantitative Finance, 1(2), pp. 223-236.

• Coval, J.D. and Stafford, E. (2007) ‘Asset Fire Sales (and Purchases) in Equity Markets’, Journal of Financial Economics, 86(2), pp. 479-512.

• Greenwood, R. and Scharfstein, D. (2013) ‘The Growth of Finance’, Journal of Economic Perspectives, 27(2), pp. 3-28.

• Rockafellar, R.T. and Uryasev, S. (2000) ‘Optimization of Conditional Value-at-Risk’, Journal of Risk, 2(3), pp. 21-41.

• Sharpe, W.F. (1966) ‘Mutual Fund Performance’, Journal of Business, 39(1), pp. 119-138.

• Sharpe, W.F. (1994) ‘The Sharpe Ratio’, Journal of Portfolio Management, 21(1), pp. 49-58.

• Sortino, F.A. and van der Meer, R. (1991) ‘Downside Risk’, Journal of Portfolio Management, 17(4), pp. 27-31.

Educational

Gold ORB Strategy (15-min Range, 5-min Entry)The Gold ORB (Opening Range Breakout) Strategy is designed for day traders looking to capitalize on the price action in the early part of the trading day, specifically using a 15-minute range for identifying the opening range and a 5-minute timeframe for breakout entries. The strategy trades the Gold market (XAU/USD) during the New York session.

Opening Range: The strategy defines the Opening Range (ORB) between 9:30 AM EST and 9:45 AM EST using the highest and lowest points during this 15-minute window.

Breakout Entries: The strategy enters trades when the price breaks above the ORB high for a long position or below the ORB low for a short position. It waits for a 5-minute candle close outside the range before entering a trade.

Stop Loss and Take Profit: The stop loss is placed at 50% of the ORB range, and the take profit is set at twice the ORB range (1:2 risk-reward ratio).

Time Window: The strategy only executes trades before 12:00 PM EST, avoiding late-day market fluctuations and consolidations.

Prop Firm Business SimulatorThe prop firm business simulator is exactly what it sounds like. It's a plug and play tool to test out any tradingview strategy and simulate hypothetical performance on CFD Prop Firms.

Now what is a modern day CFD Prop Firm?

These companies sell simulated trading challenges for a challenge fee. If you complete the challenge you get access to simulated capital and you get a portion of the profits you make on those accounts payed out.

I've included some popular firms in the code as presets so it's easy to simulate them. Take into account that this info will likely be out of date soon as these prices and challenge conditions change.

Also, this tool will never be able to 100% simulate prop firm conditions and all their rules. All I aim to do with this tool is provide estimations.

Now why is this tool helpful?

Most traders on here want to turn their passion into their full-time career, prop firms have lately been the buzz in the trading community and market themselves as a faster way to reach that goal.

While this all sounds great on paper, it is sometimes hard to estimate how much money you will have to burn on challenge fees and set realistic monthly payout expectations for yourself and your trading. This is where this tool comes in.

I've specifically developed this for traders that want to treat prop firms as a business. And as a business you want to know your monthly costs and income depending on the trading strategy and prop firm challenge you are using.

How to use this tool

It's quite simple you remove the top part of the script and replace it with your own strategy. Make sure it's written in same version of pinescript before you do that.

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

//--$$$$$--Strategy-- --$$$$$$--// ******************************************************************************************************************************

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

length = input.int(20, minval=1, group="Keltner Channel Breakout")

mult = input(2.0, "Multiplier", group="Keltner Channel Breakout")

src = input(close, title="Source", group="Keltner Channel Breakout")

exp = input(true, "Use Exponential MA", display = display.data_window, group="Keltner Channel Breakout")

BandsStyle = input.string("Average True Range", options = , title="Bands Style", display = display.data_window, group="Keltner Channel Breakout")

atrlength = input(10, "ATR Length", display = display.data_window, group="Keltner Channel Breakout")

esma(source, length)=>

s = ta.sma(source, length)

e = ta.ema(source, length)

exp ? e : s

ma = esma(src, length)

rangema = BandsStyle == "True Range" ? ta.tr(true) : BandsStyle == "Average True Range" ? ta.atr(atrlength) : ta.rma(high - low, length)

upper = ma + rangema * mult

lower = ma - rangema * mult

//--Graphical Display--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

u = plot(upper, color=#2962FF, title="Upper", force_overlay=true)

plot(ma, color=#2962FF, title="Basis", force_overlay=true)

l = plot(lower, color=#2962FF, title="Lower", force_overlay=true)

fill(u, l, color=color.rgb(33, 150, 243, 95), title="Background")

//--Risk Management--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

riskPerTradePerc = input.float(1, title="Risk per trade (%)", group="Keltner Channel Breakout")

le = high>upper ? false : true

se = lowlower

strategy.entry('PivRevLE', strategy.long, comment = 'PivRevLE', stop = upper, qty=riskToLots)

if se and upper>lower

strategy.entry('PivRevSE', strategy.short, comment = 'PivRevSE', stop = lower, qty=riskToLots)

The tool will then use the strategy equity of your own strategy and use this to simulat prop firms. Since these CFD prop firms work with different phases and payouts the indicator will simulate the gains until target or max drawdown / daily drawdown limit gets reached. If it reaches target it will go to the next phase and keep on doing that until it fails a challenge.

If in one of the phases there is a reward for completing, like a payout, refund, extra it will add this to the gains.

If you fail the challenge by reaching max drawdown or daily drawdown limit it will substract the challenge fee from the gains.

These gains are then visualised in the calendar so you can get an idea of yearly / monthly gains of the backtest. Remember, it is just a backtest so no guarantees of future income.

The bottom pane (non-overlay) is visualising the performance of the backtest during the phases. This way u can check if it is realistic. For instance if it only takes 1 bar on chart to reach target you are probably risking more than the firm wants you to risk. Also, it becomes much less clear if daily drawdown got hit in those high risk strategies, the results will be less accurate.

The daily drawdown limit get's reset every time there is a new dayofweek on chart.

If you set your prop firm preset setting to "'custom" the settings below that are applied as your prop firm settings. Otherwise it will use one of the template by default it's FTMO 100K.

The strategy I'm using as an example in this script is a simple Keltner Channel breakout strategy. I'm using a 0.05% commission per trade as that is what I found most common on crypto exchanges and it's close to the commissions+spread you get on a cfd prop firm. I'm targeting a 1% risk per trade in the backtest to try and stay within prop firm boundaries of max 1% risk per trade.

Lastly, the original yearly and monthly performance table was developed by Quantnomad and I've build ontop of that code. Here's a link to the original publication:

That's everything for now, hope this indicator helps people visualise the potential of prop firms better or to understand that they are not a good fit for their current financial situation.

DCA StrategyThis strategy makes it easy for you to backtest and automate the DCA strategy based on 2 triggers:

Day of the week

Every X candles

This way you can set up your DCA strategy the way you like and automate on any exchange or even a DEX, which offers an API.

The strategy is auto selling on the last candle, otherwise you won't see any performance numbers because all positions will still be open (non conclusive).

Settings

Start Date & End Date

Use those dates to help you with your backtest period. It also helps when automating, to start at a specific time to mimic what you have already done on your own portfolio and thus be in sync in TV as well.

Capital to invest per trade

Set how capital to use per DCA buy signal. Hover over the tooltip to understand, which currency is used.

Close All on last candle

When backtesting, you must close open positions, otherwise the Strategy Tester won't show you any numbers. This is why the strategy automatically closes all positions on the last candle for your convenience (ON per default).

BUT, when automating, you cannot have this checked because it would sell all of your asset on every candle open. So turn this OFF when automating.

Use Day of Week Mode

This checkbox switches between the "Day of Week" mode or the "Every X Candles" mode.

Day of Week

Opens a long position at the start of the weekday you have set it to.

Hover over the tooltip to understand, which number to use for the day of the week you need.

Every X Candles

Opens a long position after every x candles. Always at the start of every such candle.

On the daily chart, this number represents "1 day", on the 1h chart, it's "1 hour" and so on.

Properties

Initial Capital

DCA has a special quirk and that is that it invests more and more and more funds the longer it runs. But TradingView takes the Initial Capital number to calculate Net Profit, thus the Initial Capital number has to grow with every additional dollar (money) that is being invested over time, otherwise the Net Profit number will be wrong.

Sadly PineScript does not allow to set the Initial Capital number dynamically. So you have to set it manually.

To that end, this strategy shows a Label on the last candle, which shows the Invested Capital. You must take that number and put it into the Initial Capital input and click Ok .

If you don't do this, your Net Profit Number will be totally wrong!

The label must show green .

If it shows red it means you need to change the Initial Capital number before looking at the performance numbers.

After every timeframe or settings change, you must adapt the Initial Capital, otherwise you will get wrong numbers.

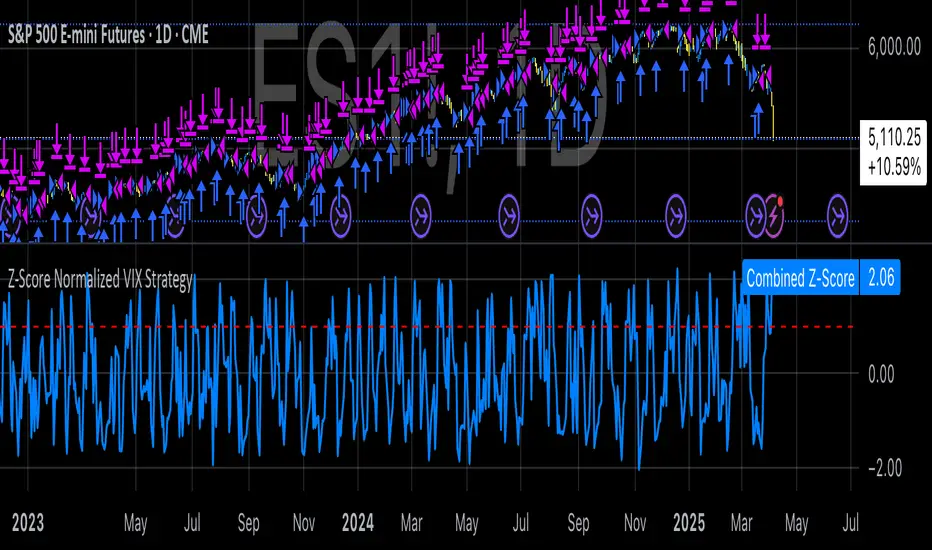

Z-Score Normalized VIX StrategyThis strategy leverages the concept of the Z-score applied to multiple VIX-based volatility indices, specifically designed to capture market reversals based on the normalization of volatility. The strategy takes advantage of VIX-related indicators to measure extreme levels of market fear or greed and adjusts its position accordingly.

1. Overview of the Z-Score Methodology

The Z-score is a statistical measure that describes the position of a value relative to the mean of a distribution in terms of standard deviations. In this strategy, the Z-score is calculated for various volatility indices to assess how far their values are from their historical averages, thus normalizing volatility levels. The Z-score is calculated as follows:

Z = \frac{X - \mu}{\sigma}

Where:

• X is the current value of the volatility index.

• \mu is the mean of the index over a specified period.

• \sigma is the standard deviation of the index over the same period.

This measure tells us how many standard deviations the current value of the index is away from its average, indicating whether the market is experiencing unusually high or low volatility (fear or calm).

2. VIX Indices Used in the Strategy

The strategy utilizes four commonly referenced volatility indices:

• VIX (CBOE Volatility Index): Measures the market’s expectations of 30-day volatility based on S&P 500 options.

• VIX3M (3-Month VIX): Reflects expectations of volatility over the next three months.

• VIX9D (9-Day VIX): Reflects shorter-term volatility expectations.

• VVIX (VIX of VIX): Measures the volatility of the VIX itself, indicating the level of uncertainty in the volatility index.

These indices provide a comprehensive view of the current volatility landscape across different time horizons.

3. Strategy Logic

The strategy follows a long entry condition and an exit condition based on the combined Z-score of the selected volatility indices:

• Long Entry Condition: The strategy enters a long position when the combined Z-score of the selected VIX indices falls below a user-defined threshold, indicating an abnormally low level of volatility (suggesting a potential market bottom and a bullish reversal). The threshold is set as a negative value (e.g., -1), where a more negative Z-score implies greater deviation below the mean.

• Exit Condition: The strategy exits the long position when the combined Z-score exceeds the threshold (i.e., when the market volatility increases above the threshold, indicating a shift in market sentiment and reduced likelihood of continued upward momentum).

4. User Inputs

• Z-Score Lookback Period: The user can adjust the lookback period for calculating the Z-score (e.g., 6 periods).

• Z-Score Threshold: A customizable threshold value to define when the market has reached an extreme volatility level, triggering entries and exits.

The strategy also allows users to select which VIX indices to use, with checkboxes to enable or disable each index in the calculation of the combined Z-score.

5. Trade Execution Parameters

• Initial Capital: The strategy assumes an initial capital of $20,000.

• Pyramiding: The strategy does not allow pyramiding (multiple positions in the same direction).

• Commission and Slippage: The commission is set at $0.05 per contract, and slippage is set at 1 tick.

6. Statistical Basis of the Z-Score Approach

The Z-score methodology is a standard technique in statistics and finance, commonly used in risk management and for identifying outliers or unusual events. According to Dumas, Fleming, and Whaley (1998), volatility indices like the VIX serve as a useful proxy for market sentiment, particularly during periods of high uncertainty. By calculating the Z-score, we normalize volatility and quantify the degree to which the current volatility deviates from historical norms, allowing for systematic entry and exit based on these deviations.

7. Implications of the Strategy

This strategy aims to exploit market conditions where volatility has deviated significantly from its historical mean. When the Z-score falls below the threshold, it suggests that the market has become excessively calm, potentially indicating an overreaction to past market events. Entering long positions under such conditions could capture market reversals as fear subsides and volatility normalizes. Conversely, when the Z-score rises above the threshold, it signals increased volatility, which could be indicative of a bearish shift in the market, prompting an exit from the position.

By applying this Z-score normalized approach, the strategy seeks to achieve more consistent entry and exit points by reducing reliance on subjective interpretation of market conditions.

8. Scientific Sources

• Dumas, B., Fleming, J., & Whaley, R. (1998). “Implied Volatility Functions: Empirical Tests”. The Journal of Finance, 53(6), 2059-2106. This paper discusses the use of volatility indices and their empirical behavior, providing context for volatility-based strategies.

• Black, F., & Scholes, M. (1973). “The Pricing of Options and Corporate Liabilities”. Journal of Political Economy, 81(3), 637-654. The original Black-Scholes model, which forms the basis for many volatility-related strategies.

Cycle Biologique Strategy // (\_/)

// ( •.•)

// (")_(")

//@fr33domz

Experimental Research: Cycle Biologique Strategy

Overview

The "Cycle Biologique Strategy" is an experimental trading algorithm designed to leverage periodic cycles in price movements by utilizing a sinusoidal function. This strategy aims to identify potential buy and sell signals based on the behavior of a custom-defined biological cycle.

Key Parameters

Cycle Length: This parameter defines the duration of the cycle, set by default to 30 periods. The user can adjust this value to optimize the strategy for different asset classes or market conditions.

Amplitude: The amplitude of the cycle influences the scale of the sinusoidal wave, allowing for customization in the sensitivity of buy and sell signals.

Offset: The offset parameter introduces phase shifts to the cycle, adjustable within a range of -360 to 360 degrees. This flexibility allows the strategy to align with various market rhythms.

Methodology

The core of the strategy lies in the calculation of a periodic cycle using a sinusoidal function.

Trading Signals

Buy Signal: A buy signal is generated when the cycle value crosses above zero, indicating a potential upward momentum.

Sell Signal: Conversely, a sell signal is triggered when the cycle value crosses below zero, suggesting a potential downtrend.

Execution

The strategy executes trades based on these signals:

Upon receiving a buy signal, the algorithm enters a long position.

When a sell signal occurs, the strategy closes the long position.

Visualization

To enhance user experience, the periodic cycle is plotted visually on the chart in blue, allowing traders to observe the cyclical nature of the strategy and its alignment with market movements.

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

External Signals Strategy TesterExternal Signals Strategy Tester

This strategy is designed to help you backtest external buy/sell signals coming from another indicator on your chart. It is a flexible and powerful tool that allows you to simulate real trading based on signals generated by any indicator, using input.source connections.

🔧 How It Works

Instead of generating signals internally, this strategy listens to two external input sources:

One for buy signals

One for sell signals

These sources can be connected to the plots from another indicator (for example, custom indicators, signal lines, or logic-based plots).

To use this:

Add your indicator to the chart (it must be visible on the same pane as this strategy).

Open the settings of the strategy.

In the fields Buy Signal and Sell Signal, select the appropriate plot (line, value, etc.) from the indicator that represents the buy/sell logic.

The strategy will open positions when the selected buy signal crosses above 0, and sell signal crosses above 0.

This logic can be easily adapted by modifying the crossover rule inside the script if your signal style is different.

⚙️ Features Included

✅ Configurable trade direction:

You can choose whether to allow long trades, short trades, or both.

✅ Optional close on opposite signal:

When enabled, the strategy will exit the current position if an opposite signal appears.

✅ Optional full position reversal:

When enabled, the strategy will close the current position and immediately open an opposite one on the reverse signal.

✅ Risk Management Tools:

You can define:

Take Profit (TP): Position will be closed once the specified profit (in %) is reached.

Stop Loss (SL): Position will be closed if the price drops to the specified loss level (in %).

BreakEven (BE): Once the specified profit threshold is reached, the strategy will move the stop-loss to the entry price.

📌 If any of these values (TP, SL, BE) are set to 0, the feature is disabled and will not be applied.

🧪 Best Use Cases

Backtesting signals from custom indicators, without rewriting the logic into a strategy.

Comparing the performance of different signal sources.

Testing external indicators with optional position management logic.

Validating strategies using external filters, oscillators, or trend signals.

📌 Final Notes

You can visualize where the strategy detected buy/sell signals using green/red markers on the chart.

All parameters are customizable through the strategy settings panel.

This strategy does not repaint, and it processes signals in real-time only (no lookahead bias).

EMA 10/55/200 - LONG ONLY MTF (4h with 1D & 1W confirmation)Title: EMA 10/55/200 - Long Only Multi-Timeframe Strategy (4h with 1D & 1W confirmation)

Description:

This strategy is designed for trend-following long entries using a combination of exponential moving averages (EMAs) on the 4-hour chart, confirmed by higher timeframe trends from the daily (1D) and weekly (1W) charts.

🔍 How It Works

🔹 Entry Conditions (4h chart):

EMA 10 crosses above EMA 55 and price is above EMA 55

OR

EMA 55 crosses above EMA 200

OR

EMA 10 crosses above EMA 500

These entries indicate short-term momentum aligning with medium/long-term trend strength.

🔹 Confirmation (multi-timeframe alignment):

Daily (1D): EMA 55 is above EMA 200

Weekly (1W): EMA 55 is above EMA 200

This ensures that we only enter long trades when the higher timeframes support an uptrend, reducing false signals during sideways or bearish markets.

🛑 Exit Conditions

Bearish crossover of EMA 10 below EMA 200 or EMA 500

Stop Loss: 5% below entry price

⚙️ Backtest Settings

Capital allocation per trade: 10% of equity

Commission: 0.1%

Slippage: 2 ticks

These are realistic conditions for crypto, forex, and stocks.

📈 Best Used On

Timeframe: 4h

Instruments: Trending markets like BTC/ETH, FX majors, or growth stocks

Works best in volatile or trending environments

⚠️ Disclaimer

This is a backtest tool and educational resource. Always validate on demo accounts before applying to real capital. Do your own due diligence.

Buy on 5% dip strategy with time adjustment

This script is a strategy called "Buy on 5% Dip Strategy with Time Adjustment 📉💡," which detects a 5% drop in price and triggers a buy signal 🔔. It also automatically closes the position once the set profit target is reached 💰, and it has additional logic to close the position if the loss exceeds 14% after holding for 230 days ⏳.

Strategy Explanation

Buy Condition: A buy signal is triggered when the price drops 5% from the highest price reached 🔻.

Take Profit: The position is closed when the price hits a 1.22x target from the average entry price 📈.

Forced Sell Condition: If the position is held for more than 230 days and the loss exceeds 14%, the position is automatically closed 🚫.

Leverage & Capital Allocation: Leverage is adjustable ⚖️, and you can set the percentage of capital allocated to each trade 💸.

Time Limits: The strategy allows you to set a start and end time ⏰ for trading, making the strategy active only within that specific period.

Code Credits and References

Credits: This script utilizes ideas and code from @QuantNomad and jangdokang for the profit table and algorithm concepts 🔧.

Sources:

Monthly Performance Table Script by QuantNomad:

ZenAndTheArtOfTrading's Script:

Strategy Performance

This strategy provides risk management through take profit and forced sell conditions and includes a performance table 📊 to track monthly and yearly results. You can compare backtest results with real-time performance to evaluate the strategy's effectiveness.

The performance numbers shown in the backtest reflect what would have happened if you had used this strategy since the launch date of the SOXL (the Direxion Daily Semiconductor Bull 3x Shares ETF) 📅. These results are not hypothetical but based on actual performance from the day of the ETF’s launch 📈.

Caution ⚠️

No Guarantee of Future Results: The results are based on historical performance from the launch of the SOXL ETF, but past performance does not guarantee future results. It’s important to approach with caution when applying it to live trading 🔍.

Risk Management: Leverage and capital allocation settings are crucial for managing risk ⚠️. Make sure to adjust these according to your risk tolerance ⚖️.

IU Bigger than range strategyDESCRIPTION

IU Bigger Than Range Strategy is designed to capture breakout opportunities by identifying candles that are significantly larger than the previous range. It dynamically calculates the high and low of the last N candles and enters trades when the current candle's range exceeds the previous range. The strategy includes multiple stop-loss methods (Previous High/Low, ATR, Swing High/Low) and automatically manages take-profit and stop-loss levels based on user-defined risk-to-reward ratios. This versatile strategy is optimized for higher timeframes and assets like BTC but can be fine-tuned for different instruments and intervals.

USER INPUTS:

Look back Length: Number of candles to calculate the high-low range. Default is 22.

Risk to Reward: Sets the target reward relative to the stop-loss distance. Default is 3.

Stop Loss Method: Choose between:(Default is "Previous High/Low")

- Previous High/Low

- ATR (Average True Range)

- Swing High/Low

ATR Length: Defines the length for ATR calculation (only applicable when ATR is selected as the stop-loss method) (Default is 14).

ATR Factor: Multiplier applied to the ATR to determine stop-loss distance(Default is 2).

Swing High/Low Length: Specifies the length for identifying swing points (only applicable when Swing High/Low is selected as the stop-loss method).(Default is 2)

LONG CONDITION:

The current candle’s range (absolute difference between open and close) is greater than the previous range.

The closing price is higher than the opening price (bullish candle).

SHORT CONDITIONS:

The current candle’s range exceeds the previous range.

The closing price is lower than the opening price (bearish candle).

LONG EXIT:

Stop-loss:

- Previous Low

- ATR-based trailing stop

- Recent Swing Low

Take-profit:

- Defined by the Risk-to-Reward ratio (default 3x the stop-loss distance).

SHORT EXIT:

Stop-loss:

- Previous High

- ATR-based trailing stop

- Recent Swing High

Take-profit:

- Defined by the Risk-to-Reward ratio (default 3x the stop-loss distance).

ALERTS:

Long Entry Triggered

Short Entry Triggered

WHY IT IS UNIQUE:

This strategy dynamically adapts to different market conditions by identifying candles that exceed the previous range, ensuring that it only enters trades during strong breakout scenarios.

Multiple stop-loss methods provide flexibility for different trading styles and risk profiles.

The visual representation of stop-loss and take-profit levels with color-coded plots improves trade monitoring and decision-making.

HOW USERS CAN BENEFIT FROM IT:

Ideal for breakout traders looking to capitalize on momentum-driven price moves.

Provides flexibility to customize stop-loss methods and fine-tune risk management parameters.

Helps minimize drawdowns with a strong risk-to-reward framework while maximizing profit potential.

Trendline Breaks with Multi Fibonacci Supertrend StrategyTMFS Strategy: Advanced Trendline Breakouts with Multi-Fibonacci Supertrend

Elevate your algorithmic trading with institutional-grade signal confluence

Strategy Genesis & Evolution

This advanced trading system represents the culmination of a personal research journey, evolving from my custom " Multi Fibonacci Supertrend with Signals " indicator into a comprehensive trading strategy. Built upon the exceptional trendline detection methodology pioneered by LuxAlgo in their " Trendlines with Breaks " indicator, I've engineered a systematic framework that integrates multiple technical factors into a cohesive trading system.

Core Fibonacci Principles

At the heart of this strategy lies the Fibonacci sequence application to volatility measurement:

// Fibonacci-based factors for multiple Supertrend calculations

factor1 = input.float(0.618, 'Factor 1 (Weak/Fibonacci)', minval = 0.01, step = 0.01)

factor2 = input.float(1.618, 'Factor 2 (Medium/Golden Ratio)', minval = 0.01, step = 0.01)

factor3 = input.float(2.618, 'Factor 3 (Strong/Extended Fib)', minval = 0.01, step = 0.01)

These precise Fibonacci ratios create a dynamic volatility envelope that adapts to changing market conditions while maintaining mathematical harmony with natural price movements.

Dynamic Trendline Detection

The strategy incorporates LuxAlgo's pioneering approach to trendline detection:

// Pivotal swing detection (inspired by LuxAlgo)

pivot_high = ta.pivothigh(swing_length, swing_length)

pivot_low = ta.pivotlow(swing_length, swing_length)

// Dynamic slope calculation using ATR

slope = atr_value / swing_length * atr_multiplier

// Update trendlines based on pivot detection

if bool(pivot_high)

upper_slope := slope

upper_trendline := pivot_high

else

upper_trendline := nz(upper_trendline) - nz(upper_slope)

This adaptive trendline approach automatically identifies key structural market boundaries, adjusting in real-time to evolving chart patterns.

Breakout State Management

The strategy implements sophisticated state tracking for breakout detection:

// Track breakouts with state variables

var int upper_breakout_state = 0

var int lower_breakout_state = 0

// Update breakout state when price crosses trendlines

upper_breakout_state := bool(pivot_high) ? 0 : close > upper_trendline ? 1 : upper_breakout_state

lower_breakout_state := bool(pivot_low) ? 0 : close < lower_trendline ? 1 : lower_breakout_state

// Detect new breakouts (state transitions)

bool new_upper_breakout = upper_breakout_state > upper_breakout_state

bool new_lower_breakout = lower_breakout_state > lower_breakout_state

This state-based approach enables precise identification of the exact moment when price breaks through a significant trendline.

Multi-Factor Signal Confluence

Entry signals require confirmation from multiple technical factors:

// Define entry conditions with multi-factor confluence

long_entry_condition = enable_long_positions and

upper_breakout_state > upper_breakout_state and // New trendline breakout

di_plus > di_minus and // Bullish DMI confirmation

close > smoothed_trend // Price above Supertrend envelope

// Execute trades only with full confirmation

if long_entry_condition

strategy.entry('L', strategy.long, comment = "LONG")

This strict requirement for confluence significantly reduces false signals and improves the quality of trade entries.

Advanced Risk Management

The strategy includes sophisticated risk controls with multiple methodologies:

// Calculate stop loss based on selected method

get_long_stop_loss_price(base_price) =>

switch stop_loss_method

'PERC' => base_price * (1 - long_stop_loss_percent)

'ATR' => base_price - long_stop_loss_atr_multiplier * entry_atr

'RR' => base_price - (get_long_take_profit_price() - base_price) / long_risk_reward_ratio

=> na

// Implement trailing functionality

strategy.exit(

id = 'Long Take Profit / Stop Loss',

from_entry = 'L',

qty_percent = take_profit_quantity_percent,

limit = trailing_take_profit_enabled ? na : long_take_profit_price,

stop = long_stop_loss_price,

trail_price = trailing_take_profit_enabled ? long_take_profit_price : na,

trail_offset = trailing_take_profit_enabled ? long_trailing_tp_step_ticks : na,

comment = "TP/SL Triggered"

)

This flexible approach adapts to varying market conditions while providing comprehensive downside protection.

Performance Characteristics

Rigorous backtesting demonstrates exceptional capital appreciation potential with impressive risk-adjusted metrics:

Remarkable total return profile (1,517%+)

Strong Sortino ratio (3.691) indicating superior downside risk control

Profit factor of 1.924 across all trades (2.153 for long positions)

Win rate exceeding 35% with balanced distribution across varied market conditions

Institutional Considerations

The strategy architecture addresses execution complexities faced by institutional participants with temporal filtering and date-range capabilities:

// Time Filter settings with flexible timezone support

import jason5480/time_filters/5 as time_filter

src_timezone = input.string(defval = 'Exchange', title = 'Source Timezone')

dst_timezone = input.string(defval = 'Exchange', title = 'Destination Timezone')

// Date range filtering for precise execution windows

use_from_date = input.bool(defval = true, title = 'Enable Start Date')

from_date = input.time(defval = timestamp('01 Jan 2022 00:00'), title = 'Start Date')

// Validate trading permission based on temporal constraints

date_filter_approved = time_filter.is_in_date_range(

use_from_date, from_date, use_to_date, to_date, src_timezone, dst_timezone

)

These capabilities enable precise execution timing and market session optimization critical for larger market participants.

Acknowledgments

Special thanks to LuxAlgo for the pioneering work on trendline detection and breakout identification that inspired elements of this strategy. Their innovative approach to technical analysis provided a valuable foundation upon which I could build my Fibonacci-based methodology.

This strategy is shared under the same Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license as LuxAlgo's original work.

Past performance is not indicative of future results. Conduct thorough analysis before implementing any algorithmic strategy.

BTCUSD with adjustable sl,tpThis strategy is designed for swing traders who want to enter long positions on pullbacks after a short-term trend shift, while also allowing immediate short entries when conditions favor downside movement. It combines SMA crossovers, a fixed-percentage retracement entry, and adjustable risk management parameters for optimal trade execution.

Key Features:

✅ Trend Confirmation with SMA Crossover

The 10-period SMA crossing above the 25-period SMA signals a bullish trend shift.

The 10-period SMA crossing below the 25-period SMA signals a bearish trend shift.

Short trades are only taken if the price is below the 150 EMA, ensuring alignment with the broader trend.

📉 Long Pullback Entry Using Fixed Percentage Retracement

Instead of entering immediately on the SMA crossover, the strategy waits for a retracement before going long.

The pullback entry is defined as a percentage retracement from the recent high, allowing for an optimized entry price.

The retracement percentage is fully adjustable in the settings (default: 1%).

A dynamic support level is plotted on the chart to visualize the pullback entry zone.

📊 Short Entry Rules

If the SMA(10) crosses below the SMA(25) and price is below the 150 EMA, a short trade is immediately entered.

Risk Management & Exit Strategy:

🚀 Take Profit (TP) – Fully customizable profit target in points. (Default: 1000 points)

🛑 Stop Loss (SL) – Adjustable stop loss level in points. (Default: 250 points)

🔄 Break-Even (BE) – When price moves in favor by a set number of points, the stop loss is moved to break-even.

📌 Extra Exit Condition for Longs:

If the SMA(10) crosses below SMA(25) while the price is still below the EMA150, the strategy force-exits the long position to avoid reversals.

How to Use This Strategy:

Enable the strategy on your TradingView chart (recommended for stocks, forex, or indices).

Customize the settings – Adjust TP, SL, BE, and pullback percentage for your risk tolerance.

Observe the plotted retracement levels – When the price touches and bounces off the level, a long trade is triggered.

Let the strategy manage the trade – Break-even protection and take-profit logic will automatically execute.

Ideal Market Conditions:

✅ Trending Markets – The strategy works best when price follows strong trends.

✅ Stocks, Indices, or Forex – Can be applied across multiple asset classes.

✅ Medium-Term Holding Period – Suitable for swing trades lasting days to weeks.

Multi-Timeframe MACD Strategy ver 1.0Multi-Timeframe MACD Strategy: Enhanced Trend Trading with Customizable Entry and Trailing Stop

This strategy utilizes the Moving Average Convergence Divergence (MACD) indicator across multiple timeframes to identify strong trends, generate precise entry and exit signals, and manage risk with an optional trailing stop loss. By combining the insights of both the current chart's timeframe and a user-defined higher timeframe, this strategy aims to improve trade accuracy, reduce exposure to false signals, and capture larger market moves.

Key Features:

Dual Timeframe Analysis: Calculates and analyzes the MACD on both the current chart's timeframe and a user-selected higher timeframe (e.g., Daily MACD on a 1-hour chart). This provides a broader market context, helping to confirm trends and filter out short-term noise.

Configurable MACD: Fine-tune the MACD calculation with adjustable Fast Length, Slow Length, and Signal Length parameters. Optimize the indicator's sensitivity to match your trading style and the volatility of the asset.

Flexible Entry Options: Choose between three distinct entry types:

Crossover: Enters trades when the MACD line crosses above (long) or below (short) the Signal line.

Zero Cross: Enters trades when the MACD line crosses above (long) or below (short) the zero line.

Both: Combines both Crossover and Zero Cross signals, providing more potential entry opportunities.

Independent Timeframe Control: Display and trade based on the current timeframe MACD, the higher timeframe MACD, or both. This allows you to focus on the information most relevant to your analysis.

Optional Trailing Stop Loss: Implements a configurable trailing stop loss to protect profits and limit potential losses. The trailing stop is adjusted dynamically as the price moves in your favor, based on a user-defined percentage.

No Repainting: Employs lookahead=barmerge.lookahead_off in the request.security() function to prevent data leakage and ensure accurate backtesting and real-time signals.

Clear Visual Signals (Optional): Includes optional plotting of the MACD and Signal lines for both timeframes, with distinct colors for easy visual identification. These plots are for visual confirmation and are not required for the strategy's logic.

Suitable for Various Trading Styles: Adaptable to swing trading, day trading, and trend-following strategies across diverse markets (stocks, forex, cryptocurrencies, etc.).

Fully Customizable: All parameters are adjustable, including timeframes, MACD Settings, Entry signal type and trailing stop settings.

How it Works:

MACD Calculation: The strategy calculates the MACD (using the standard formula) for both the current chart's timeframe and the specified higher timeframe.

Trend Identification: The relationship between the MACD line, Signal line, and zero line is used to determine the current trend for each timeframe.

Entry Signals: Buy/sell signals are generated based on the selected "Entry Type":

Crossover: A long signal is generated when the MACD line crosses above the Signal line, and both timeframes are in agreement (if both are enabled). A short signal is generated when the MACD line crosses below the Signal line, and both timeframes are in agreement.

Zero Cross: A long signal is generated when the MACD line crosses above the zero line, and both timeframes agree. A short signal is generated when the MACD line crosses below the zero line and both timeframes agree.

Both: Combines Crossover and Zero Cross signals.

Trailing Stop Loss (Optional): If enabled, a trailing stop loss is set at a specified percentage below (for long positions) or above (for short positions) the entry price. The stop-loss is automatically adjusted as the price moves favorably.

Exit Signals:

Without Trailing Stop: Positions are closed when the MACD signals reverse according to the selected "Entry Type" (e.g., a long position is closed when the MACD line crosses below the Signal line if using "Crossover" entries).

With Trailing Stop: Positions are closed if the price hits the trailing stop loss.

Backtesting and Optimization: The strategy automatically backtests on the chart's historical data, allowing you to assess its performance and optimize parameters for different assets and timeframes.

Example Use Cases:

Confirming Trend Strength: A trader on a 1-hour chart sees a bullish MACD crossover on the current timeframe. They check the MTF MACD strategy and see that the Daily MACD is also bullish, confirming the strength of the uptrend.

Filtering Noise: A trader using a 15-minute chart wants to avoid false signals from short-term volatility. They use the strategy with a 4-hour higher timeframe to filter out noise and only trade in the direction of the dominant trend.

Dynamic Risk Management: A trader enters a long position and enables the trailing stop loss. As the price rises, the trailing stop is automatically adjusted upwards, protecting profits. The trade is exited either when the MACD reverses or when the price hits the trailing stop.

Disclaimer:

The MACD is a lagging indicator and can produce false signals, especially in ranging markets. This strategy is for educational and informational purposes only and should not be considered financial advice. Backtest and optimize the strategy thoroughly, combine it with other technical analysis tools, and always implement sound risk management practices before using it with real capital. Past performance is not indicative of future results. Conduct your own due diligence and consider your risk tolerance before making any trading decisions.

Multi-Timeframe Parabolic SAR Strategy ver 1.0Multi-Timeframe Parabolic SAR Strategy (MTF PSAR) - Enhanced Trend Trading

This strategy leverages the power of the Parabolic SAR (Stop and Reverse) indicator across multiple timeframes to provide robust trend identification, precise entry/exit signals, and dynamic trailing stop management. By combining the insights of both the current chart's timeframe and a user-defined higher timeframe, this strategy aims to improve trading accuracy, reduce risk, and capture more significant market moves.

Key Features:

Dual Timeframe Analysis: Simultaneously analyzes the Parabolic SAR on the current chart and a higher timeframe (e.g., Daily PSAR on a 1-hour chart). This allows you to align your trades with the dominant trend and filter out noise from lower timeframes.

Configurable PSAR: Fine-tune the PSAR calculation with adjustable Start, Increment, and Maximum values to optimize sensitivity for your trading style and the asset's volatility.

Independent Timeframe Control: Choose to display and trade based on either or both the current timeframe PSAR and the higher timeframe PSAR. Focus on the most relevant information for your analysis.

Clear Visual Signals: Distinct colors for the current and higher timeframe PSAR dots provide a clear visual representation of potential entry and exit points.

Multiple Entry Strategies: The strategy offers flexible entry conditions, allowing you to trade based on:

Confirmation: Both current and higher timeframe PSAR signals agree and the current timeframe PSAR has just flipped direction. (Most conservative)

Current Timeframe Only: Trades based solely on the current timeframe PSAR, ideal for when the higher timeframe is less relevant or disabled.

Higher Timeframe Only: Trades based solely on the higher timeframe PSAR.

Dynamic Trailing Stop (PSAR-Based): Implements a trailing stop-loss based on the current timeframe's Parabolic SAR. This helps protect profits by automatically adjusting the stop-loss as the price moves in your favor. Exits are triggered when either the current or HTF PSAR flips.

No Repainting: Uses lookahead=barmerge.lookahead_off in the security() function to ensure that the higher timeframe data is accessed without any data leakage, preventing repainting issues.

Fully Configurable: All parameters (PSAR settings, higher timeframe, visibility, colors) are adjustable through the strategy's settings panel, allowing for extensive customization and optimization.

Suitable for Various Trading Styles: Applicable to swing trading, day trading, and trend-following strategies across various markets (stocks, forex, cryptocurrencies, etc.).

How it Works:

PSAR Calculation: The strategy calculates the standard Parabolic SAR for both the current chart's timeframe and the selected higher timeframe.

Trend Identification: The direction of the PSAR (dots below price = uptrend, dots above price = downtrend) determines the current trend for each timeframe.

Entry Signals: The strategy generates buy/sell signals based on the chosen entry strategy (Confirmation, Current Timeframe Only, or Higher Timeframe Only). The Confirmation strategy offers the highest probability signals by requiring agreement between both timeframes.

Trailing Stop Exit: Once a position is entered, the strategy uses the current timeframe PSAR as a dynamic trailing stop. The stop-loss is automatically adjusted as the PSAR dots move, helping to lock in profits and limit losses. The strategy exits when either the Current or HTF PSAR changes direction.

Backtesting and Optimization: The strategy automatically backtests on the chart's historical data, allowing you to evaluate its performance and optimize the settings for different assets and timeframes.

Example Use Cases:

Trend Confirmation: A trader on a 1-hour chart observes a bullish PSAR flip on the current timeframe. They check the MTF PSAR strategy and see that the Daily PSAR is also bullish, confirming the strength of the uptrend and providing a high-probability long entry signal.

Filtering Noise: A trader on a 5-minute chart wants to avoid whipsaws caused by short-term price fluctuations. They use the strategy with a 1-hour higher timeframe to filter out noise and only trade in the direction of the dominant trend.

Dynamic Risk Management: A trader enters a long position and uses the current timeframe PSAR as a trailing stop. As the price rises, the PSAR dots move upwards, automatically raising the stop-loss and protecting profits. The trade is exited when the current (or HTF) PSAR flips to bearish.

Disclaimer:

The Parabolic SAR is a lagging indicator and can produce false signals, particularly in ranging or choppy markets. This strategy is intended for educational and informational purposes only and should not be considered financial advice. It is essential to backtest and optimize the strategy thoroughly, use it in conjunction with other technical analysis tools, and implement sound risk management practices before using it with real capital. Past performance is not indicative of future results. Always conduct your own due diligence and consider your risk tolerance before making any trading decisions.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

Double Bollinger Bands Strategy with Signals (By Rolwin)Double Bollinger Bands Strategy with Signals 1.0 (By Rolwin)

📌 Overview

The Double Bollinger Bands Strategy is a trend-following system that utilizes two sets of Bollinger Bands (2 standard deviations and 3 standard deviations) to identify high-probability entry and exit points. This strategy helps traders capitalize on strong price movements and potential reversals by detecting overbought and oversold conditions more effectively.

📊 How It Works

• Bollinger Bands Setup:

o Middle Band: 20-period Simple Moving Average (SMA)

o Upper & Lower Bands (2 SD): Standard Bollinger Bands (±2 standard deviations)

o Extreme Bands (3 SD): Additional Bollinger Bands (±3 standard deviations) for extreme price moves

• Entry Signals:

✅ Buy (Long Entry): When the price crosses above the lower 3SD band (oversold zone)

❌ Sell (Short Entry): When the price crosses below the upper 3SD band (overbought zone)

• Exit Signals:

🔼 Exit Long: When the price reaches the upper 2SD band

🔽 Exit Short: When the price reaches the lower 2SD band

• Additional Features:

✅ Buy & Sell Signals plotted directly on the chart

🎨 Candles turn white when price touches the extreme 3SD band

🔥 Why Use This Strategy?

✔️ Clear Entry & Exit Points: Based on strong statistical levels

✔️ Effective in Trending & Reversal Markets: Captures both momentum & mean reversion setups

✔️ Easy-to-Use Visualization: Signals & bands make it beginner-friendly

✔️ Customizable: Adjust Bollinger Band length and multipliers to fit different assets & timeframes

⚠️ Risk Management Tip

While this strategy provides high-probability trade signals, it is essential to use stop-loss orders (e.g., ATR-based) and proper position sizing to manage risk effectively.

📈 Try it out and optimize the settings for your favorite markets! 🚀

Strategy SuperTrend SDI WebhookThis Pine Script™ strategy is designed for automated trading in TradingView. It combines the SuperTrend indicator and Smoothed Directional Indicator (SDI) to generate buy and sell signals, with additional risk management features like stop loss, take profit, and trailing stop. The script also includes settings for leverage trading, equity-based position sizing, and webhook integration.

Key Features

1. Date-based Trade Execution

The strategy is active only between the start and end dates set by the user.

times ensures that trades occur only within this predefined time range.

2. Position Sizing and Leverage

Uses leverage trading to adjust position size dynamically based on initial equity.

The user can set leverage (leverage) and percentage of equity (usdprcnt).

The position size is calculated dynamically (initial_capital) based on account performance.

3. Take Profit, Stop Loss, and Trailing Stop

Take Profit (tp): Defines the target profit percentage.

Stop Loss (sl): Defines the maximum allowable loss per trade.

Trailing Stop (tr): Adjusts dynamically based on trade performance to lock in profits.

4. SuperTrend Indicator

SuperTrend (ta.supertrend) is used to determine the market trend.

If the price is above the SuperTrend line, it indicates an uptrend (bullish).

If the price is below the SuperTrend line, it signals a downtrend (bearish).

Plots visual indicators (green/red lines and circles) to show trend changes.

5. Smoothed Directional Indicator (SDI)

SDI helps to identify trend strength and momentum.

It calculates +DI (bullish strength) and -DI (bearish strength).

If +DI is higher than -DI, the market is considered bullish.

If -DI is higher than +DI, the market is considered bearish.

The background color changes based on the SDI signal.

6. Buy & Sell Conditions

Long Entry (Buy) Conditions:

SDI confirms an uptrend (+DI > -DI).

SuperTrend confirms an uptrend (price crosses above the SuperTrend line).

Short Entry (Sell) Conditions:

SDI confirms a downtrend (+DI < -DI).

SuperTrend confirms a downtrend (price crosses below the SuperTrend line).

Optionally, trades can be filtered using crossovers (occrs option).

7. Trade Execution and Exits

Market entries:

Long (strategy.entry("Long")) when conditions match.

Short (strategy.entry("Short")) when bearish conditions are met.

Trade exits:

Uses predefined take profit, stop loss, and trailing stop levels.

Positions are closed if the strategy is out of the valid time range.

Usage

Automated Trading Strategy:

Can be integrated with webhooks for automated execution on supported trading platforms.

Trend-Following Strategy:

Uses SuperTrend & SDI to identify trend direction and strength.

Risk-Managed Leverage Trading:

Supports position sizing, stop losses, and trailing stops.

Backtesting & Optimization:

Can be used for historical performance analysis before deploying live.

Conclusion

This strategy is suitable for traders who want to automate their trading using SuperTrend and SDI indicators. It incorporates risk management tools like stop loss, take profit, and trailing stop, making it adaptable for leverage trading. Traders can customize settings, conduct backtests, and integrate it with webhooks for real-time trade execution. 🚀

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Supertrend Strategy with Money Ocean TradeStrategy Overview

The Supertrend Strategy with Trend Change Confirmation leverages the Supertrend indicator to identify potential buy and sell signals based on changes in trend direction and subsequent price action. The strategy is designed to work with any financial instrument (symbol) and aims to provide clear entry and exit signals.

Key Components

Supertrend Indicator: The core of this strategy is the Supertrend indicator, calculated using a length of 3 and a factor of 1. The Supertrend line is plotted on the chart to visually represent trend direction.

Direction 1: Indicates an uptrend (bullish).

Direction -1: Indicates a downtrend (bearish).

Trend Change Detection: The strategy monitors changes in the trend direction. When a trend change is detected, it checks if the next candle confirms the trend change by breaking above or below the Supertrend line.

Entry Conditions:

Long Entry (Buy): When the Supertrend direction changes to 1 (uptrend) and the next candle closes above the Supertrend line.

Short Entry (Sell): When the Supertrend direction changes to -1 (downtrend) and the next candle closes below the Supertrend line.

Exit Conditions: The strategy closes the position based on the opposite signal.

Long Exit: When the Supertrend direction changes to -1 (downtrend) and the next candle closes below the Supertrend line.

Short Exit: When the Supertrend direction changes to 1 (uptrend) and the next candle closes above the Supertrend line.

Visual Signals: The strategy plots buy and sell signals on the chart using plotshape:

BUY: A green label below the bar when a long entry is triggered.

SELL: A red label above the bar when a short entry is triggered.

Alerts: Alerts are set up to notify when a buy or sell signal is triggered.

Script Summary

This strategy helps traders identify potential trading opportunities based on trend changes and confirms the trend by checking the next candle's price action. The visual signals and dashboard enhance the user's ability to monitor and manage trades effectively.

Feel free to test and adjust the parameters to suit your trading preferences! If you need further customizations or explanations, let me know.

Boilerplate Configurable Strategy [Yosiet]This is a Boilerplate Code!

Hello! First of all, let me introduce myself a little bit. I don't come from the world of finance, but from the world of information and communication technologies (ICT) where we specialize in data processing with the aim of automating it and eliminating all human factors and actors in the processes. You could say that I am an algotrader.

That said, in my journey through trading in recent years I have understood that this world is often shown to be incomplete. All those who want to learn about trading only end up learning a small part of what it really entails, they only seek to learn how to read candlesticks. Therefore, I want to share with the entire community a fraction of what I have really understood it to be.

As a computer scientist, the most important thing is the data, it is the raw material of our work and without data you simply cannot do anything. Entropy is simple: Data in -> Data is transformed -> Data out.

The quality of the outgoing data will directly depend on the incoming data, there is no greater mystery or magic in the process. In trading it is no different, because at the end of the day it is nothing more than data. As we often say, if garbage comes in, garbage comes out.

Most people focus on the results only, on the outgoing data, because in the end we all want the same thing, to make easy money. Very few pay attention to the input data, much less to the process.

Now, I am not here to delude you, because there is no bigger lie than easy money, but I am here to give you a boilerplate code that will help you create strategies where you only have to concentrate on the quality of the incoming data.

To the Point

The code is a strategy boilerplate that applies the technique that you decide to customize for the criteria for opening a position. It already has the other factors involved in trading programmed and automated.

1. The Entry

This section of the boilerplate is the one that each individual must customize according to their needs and knowledge. The code is offered with two simple, well-known strategies to exemplify how the code can be reused for your own benefits.

For the purposes of this post on tradingview, I am going to use the simplest of the known strategies in trading for entries: SMA Crossing

// SMA Cross Settings

maFast = ta.sma(close, length)

maSlow = ta.sma(open, length)

The Strategy Properties for all cases published here:

For Stock TSLA H1 From 01/01/2025 To 02/15/2025

For Crypto XMR-USDT 30m From 01/01/2025 To 02/15/2025

For Forex EUR-USD 5m From 01/01/2025 To 02/15/2025

But the goal of this post is not to sell you a dream, else to show you that the same Entry decision works very well for some and does not for others and with this boilerplate code you only have to think of entries, not exits.

2. Schedules, Days, Sessions

As you know, there are an infinite number of markets that are susceptible to the sessions of each country and the news that they announce during those sessions, so the code already offers parameters so that you can condition the days and hours of operation, filter the best time parameters for a specific market and time frame.

3. Data Filtering

The data offered in trading are numerical series presented in vectors on a time axis where an endless number of mathematical equations can be applied to process them, with matrix calculation and non-linear regressions being the best, in my humble opinion.

4. Read Fundamental Macroeconomic Events, News

The boilerplate has integration with the tradingview SDK to detect when news will occur and offers parameters so that you can enable an exclusion time margin to not operate anything during that time window.

5. Direction and Sense

In my experience I have found the peculiarity that the same algorithm works very well for a market in a time frame, but for the same market in another time frame it is only a waste of time and money. So now you can easily decide if you only want to open LONG, SHORT or both side positions and know how effective your strategy really is.

6. Reading the money, THE PURPOSE OF EVERYTHING