Multi-Timeframe Stochastic Alert [tradeviZion]# Multi-Timeframe Stochastic Alert : Complete User Guide

## 1. Introduction

### What is the Multi-Timeframe Stochastic Alert?

The Multi-Timeframe Stochastic Alert is an advanced technical analysis tool that helps traders identify potential trading opportunities by analyzing momentum across multiple timeframes. It combines the power of the stochastic oscillator with multi-timeframe analysis to provide more reliable trading signals.

### Key Features and Benefits

- Simultaneous analysis of 6 different timeframes

- Advanced alert system with customizable conditions

- Real-time visual feedback with color-coded signals

- Comprehensive data table with instant market insights

- Motivational trading messages for psychological support

- Flexible theme support for comfortable viewing

### How it Can Help Your Trading

- Identify stronger trends by confirming momentum across multiple timeframes

- Reduce false signals through multi-timeframe confirmation

- Stay informed of market changes with customizable alerts

- Make more informed decisions with comprehensive market data

- Maintain trading discipline with clear visual signals

## 2. Understanding the Display

### The Stochastic Chart

The main chart displays three key components:

1. ** K-Line (Fast) **: The primary stochastic line (default color: green)

2. ** D-Line (Slow) **: The signal line (default color: red)

3. ** Reference Lines **:

- Overbought Level (80): Upper dashed line

- Middle Line (50): Center dashed line

- Oversold Level (20): Lower dashed line

### The Information Table

The table provides a comprehensive view of stochastic readings across all timeframes. Here's what each column means:

#### Column Explanations:

1. ** Timeframe **

- Shows the time period for each row

- Example: "5" = 5 minutes, "15" = 15 minutes, etc.

2. ** K Value **

- The fast stochastic line value (0-100)

- Higher values indicate stronger upward momentum

- Lower values indicate stronger downward momentum

3. ** D Value **

- The slow stochastic line value (0-100)

- Helps confirm momentum direction

- Crossovers with K-line can signal potential trades

4. ** Status **

- Shows current momentum with symbols:

- ▲ = Increasing (bullish)

- ▼ = Decreasing (bearish)

- Color matches the trend direction

5. ** Trend **

- Shows the current market condition:

- "Overbought" (above 80)

- "Bullish" (above 50)

- "Bearish" (below 50)

- "Oversold" (below 20)

#### Row Explanations:

1. ** Title Row **

- Shows "🎯 Multi-Timeframe Stochastic"

- Indicates the indicator is active

2. ** Header Row **

- Contains column titles

- Dark blue background for easy reading

3. ** Timeframe Rows **

- Six rows showing different timeframe analyses

- Each row updates independently

- Color-coded for easy trend identification

4. **Message Row**

- Shows rotating motivational messages

- Updates every 5 bars

- Helps maintain trading discipline

### Visual Indicators and Colors

- ** Green Background **: Indicates bullish conditions

- ** Red Background **: Indicates bearish conditions

- ** Color Intensity **: Shows strength of the signal

- ** Background Highlights **: Appear when alert conditions are met

## 3. Core Settings Groups

### Stochastic Settings

These settings control the core calculation of the stochastic oscillator.

1. ** Length (Default: 14) **

- What it does: Determines the lookback period for calculations

- Higher values (e.g., 21): More stable, fewer signals

- Lower values (e.g., 8): More sensitive, more signals

- Recommended:

* Day Trading: 8-14

* Swing Trading: 14-21

* Position Trading: 21-30

2. ** Smooth K (Default: 3) **

- What it does: Smooths the main stochastic line

- Higher values: Smoother line, fewer false signals

- Lower values: More responsive, but more noise

- Recommended:

* Day Trading: 2-3

* Swing Trading: 3-5

* Position Trading: 5-7

3. ** Smooth D (Default: 3) **

- What it does: Smooths the signal line

- Works in conjunction with Smooth K

- Usually kept equal to or slightly higher than Smooth K

- Recommended: Keep same as Smooth K for consistency

4. ** Source (Default: Close) **

- What it does: Determines price data for calculations

- Options: Close, Open, High, Low, HL2, HLC3, OHLC4

- Recommended: Stick with Close for most reliable signals

### Timeframe Settings

Controls the multiple timeframes analyzed by the indicator.

1. ** Main Timeframes (TF1-TF6) **

- TF1 (Default: 10): Shortest timeframe for quick signals

- TF2 (Default: 15): Short-term trend confirmation

- TF3 (Default: 30): Medium-term trend analysis

- TF4 (Default: 30): Additional medium-term confirmation

- TF5 (Default: 60): Longer-term trend analysis

- TF6 (Default: 240): Major trend confirmation

Recommended Combinations:

* Scalping: 1, 3, 5, 15, 30, 60

* Day Trading: 5, 15, 30, 60, 240, D

* Swing Trading: 15, 60, 240, D, W, M

2. ** Wait for Bar Close (Default: true) **

- What it does: Controls when calculations update

- True: More reliable but slightly delayed signals

- False: Faster signals but may change before bar closes

- Recommended: Keep True for more reliable signals

### Alert Settings

#### Main Alert Settings

1. ** Enable Alerts (Default: true) **

- Master switch for all alert notifications

- Toggle this off when you don't want any alerts

- Useful during testing or when you want to focus on visual signals only

2. ** Alert Condition (Options) **

- "Above Middle": Bullish momentum alerts only

- "Below Middle": Bearish momentum alerts only

- "Both": Alerts for both directions

- Recommended:

* Trending Markets: Choose direction matching the trend

* Ranging Markets: Use "Both" to catch reversals

* New Traders: Start with "Both" until you develop a specific strategy

3. ** Alert Frequency **

- "Once Per Bar": Immediate alerts during the bar

- "Once Per Bar Close": Alerts only after bar closes

- Recommended:

* Day Trading: "Once Per Bar" for quick reactions

* Swing Trading: "Once Per Bar Close" for confirmed signals

* Beginners: "Once Per Bar Close" to reduce false signals

#### Timeframe Check Settings

1. ** First Check (TF1) **

- Purpose: Confirms basic trend direction

- Alert Triggers When:

* For Bullish: Stochastic is above middle line (50)

* For Bearish: Stochastic is below middle line (50)

* For Both: Triggers in either direction based on position relative to middle line

- Settings:

* Enable/Disable: Turn first check on/off

* Timeframe: Default 5 minutes

- Best Used For:

* Quick trend confirmation

* Entry timing

* Scalping setups

2. ** Second Check (TF2) **

- Purpose: Confirms both position and momentum

- Alert Triggers When:

* For Bullish: Stochastic is above middle line AND both K&D lines are increasing

* For Bearish: Stochastic is below middle line AND both K&D lines are decreasing

* For Both: Triggers based on position and direction matching current condition

- Settings:

* Enable/Disable: Turn second check on/off

* Timeframe: Default 15 minutes

- Best Used For:

* Trend strength confirmation

* Avoiding false breakouts

* Day trading setups

3. ** Third Check (TF3) **

- Purpose: Confirms overall momentum direction

- Alert Triggers When:

* For Bullish: Both K&D lines are increasing (momentum confirmation)

* For Bearish: Both K&D lines are decreasing (momentum confirmation)

* For Both: Triggers based on matching momentum direction

- Settings:

* Enable/Disable: Turn third check on/off

* Timeframe: Default 30 minutes

- Best Used For:

* Major trend confirmation

* Swing trading setups

* Avoiding trades against the main trend

Note: All three conditions must be met simultaneously for the alert to trigger. This multi-timeframe confirmation helps reduce false signals and provides stronger trade setups.

#### Alert Combinations Examples

1. ** Conservative Setup **

- Enable all three checks

- Use "Once Per Bar Close"

- Timeframe Selection Example:

* First Check: 15 minutes

* Second Check: 1 hour (60 minutes)

* Third Check: 4 hours (240 minutes)

- Wider gaps between timeframes reduce noise and false signals

- Best for: Swing trading, beginners

2. ** Aggressive Setup **

- Enable first two checks only

- Use "Once Per Bar"

- Timeframe Selection Example:

* First Check: 5 minutes

* Second Check: 15 minutes

- Closer timeframes for quicker signals

- Best for: Day trading, experienced traders

3. ** Balanced Setup **

- Enable all checks

- Use "Once Per Bar"

- Timeframe Selection Example:

* First Check: 5 minutes

* Second Check: 15 minutes

* Third Check: 1 hour (60 minutes)

- Balanced spacing between timeframes

- Best for: All-around trading

### Visual Settings

#### Alert Visual Settings

1. ** Show Background Color (Default: true) **

- What it does: Highlights chart background when alerts trigger

- Benefits:

* Makes signals more visible

* Helps spot opportunities quickly

* Provides visual confirmation of alerts

- When to disable:

* If using multiple indicators

* When preferring a cleaner chart

* During manual backtesting

2. ** Background Transparency (Default: 90) **

- Range: 0 (solid) to 100 (invisible)

- Recommended Settings:

* Clean Charts: 90-95

* Multiple Indicators: 85-90

* Single Indicator: 80-85

- Tip: Adjust based on your chart's overall visibility

3. ** Background Colors **

- Bullish Background:

* Default: Green

* Indicates upward momentum

* Customizable to match your theme

- Bearish Background:

* Default: Red

* Indicates downward momentum

* Customizable to match your theme

#### Level Settings

1. ** Oversold Level (Default: 20) **

- Traditional Setting: 20

- Adjustable Range: 0-100

- Usage:

* Lower values (e.g., 10): More conservative

* Higher values (e.g., 30): More aggressive

- Trading Applications:

* Potential bullish reversal zone

* Support level in uptrends

* Entry point for long positions

2. ** Overbought Level (Default: 80) **

- Traditional Setting: 80

- Adjustable Range: 0-100

- Usage:

* Lower values (e.g., 70): More aggressive

* Higher values (e.g., 90): More conservative

- Trading Applications:

* Potential bearish reversal zone

* Resistance level in downtrends

* Exit point for long positions

3. ** Middle Line (Default: 50) **

- Purpose: Trend direction separator

- Applications:

* Above 50: Bullish territory

* Below 50: Bearish territory

* Crossing 50: Potential trend change

- Trading Uses:

* Trend confirmation

* Entry/exit trigger

* Risk management level

#### Color Settings

1. ** Bullish Color (Default: Green) **

- Used for:

* K-Line (Main stochastic line)

* Status symbols when trending up

* Trend labels for bullish conditions

- Customization:

* Choose colors that stand out

* Match your trading platform theme

* Consider color blindness accessibility

2. ** Bearish Color (Default: Red) **

- Used for:

* D-Line (Signal line)

* Status symbols when trending down

* Trend labels for bearish conditions

- Customization:

* Choose contrasting colors

* Ensure visibility on your chart

* Consider monitor settings

3. ** Neutral Color (Default: Gray) **

- Used for:

* Middle line (50 level)

- Customization:

* Should be less prominent

* Easy on the eyes

* Good background contrast

### Theme Settings

1. **Color Theme Options**

- Dark Theme (Default):

* Dark background with white text

* Optimized for dark chart backgrounds

* Reduces eye strain in low light

- Light Theme:

* Light background with black text

* Better visibility in bright conditions

- Custom Theme:

* Use your own color preferences

2. ** Available Theme Colors **

- Table Background

- Table Text

- Table Headers

Note: The theme affects only the table display colors. The stochastic lines and alert backgrounds use their own color settings.

### Table Settings

#### Position and Size

1. ** Table Position **

- Options:

* Top Right (Default)

* Middle Right

* Bottom Right

* Top Left

* Middle Left

* Bottom Left

- Considerations:

* Chart space utilization

* Personal preference

* Multiple monitor setups

2. ** Text Sizes **

- Title Size Options:

* Tiny: Minimal space usage

* Small: Compact but readable

* Normal (Default): Standard visibility

* Large: Enhanced readability

* Huge: Maximum visibility

- Data Size Options:

* Recommended: One size smaller than title

* Adjust based on screen resolution

* Consider viewing distance

3. ** Empowering Messages **

- Purpose:

* Maintain trading discipline

* Provide psychological support

* Remind of best practices

- Rotation:

* Changes every 5 bars

* Categories include:

- Market Wisdom

- Strategy & Discipline

- Mindset & Growth

- Technical Mastery

- Market Philosophy

## 4. Setting Up for Different Trading Styles

### Day Trading Setup

1. **Timeframes**

- Primary: 5, 15, 30 minutes

- Secondary: 1H, 4H

- Alert Settings: "Once Per Bar"

2. ** Stochastic Settings **

- Length: 8-14

- Smooth K/D: 2-3

- Alert Condition: Match market trend

3. ** Visual Settings **

- Background: Enabled

- Transparency: 85-90

- Theme: Based on trading hours

### Swing Trading Setup

1. ** Timeframes **

- Primary: 1H, 4H, Daily

- Secondary: Weekly

- Alert Settings: "Once Per Bar Close"

2. ** Stochastic Settings **

- Length: 14-21

- Smooth K/D: 3-5

- Alert Condition: "Both"

3. ** Visual Settings **

- Background: Optional

- Transparency: 90-95

- Theme: Personal preference

### Position Trading Setup

1. ** Timeframes **

- Primary: Daily, Weekly

- Secondary: Monthly

- Alert Settings: "Once Per Bar Close"

2. ** Stochastic Settings **

- Length: 21-30

- Smooth K/D: 5-7

- Alert Condition: "Both"

3. ** Visual Settings **

- Background: Disabled

- Focus on table data

- Theme: High contrast

## 5. Troubleshooting Guide

### Common Issues and Solutions

1. ** Too Many Alerts **

- Cause: Settings too sensitive

- Solutions:

* Increase timeframe intervals

* Use "Once Per Bar Close"

* Enable fewer timeframe checks

* Adjust stochastic length higher

2. ** Missed Signals **

- Cause: Settings too conservative

- Solutions:

* Decrease timeframe intervals

* Use "Once Per Bar"

* Enable more timeframe checks

* Adjust stochastic length lower

3. ** False Signals **

- Cause: Insufficient confirmation

- Solutions:

* Enable all three timeframe checks

* Use larger timeframe gaps

* Wait for bar close

* Confirm with price action

4. ** Visual Clarity Issues **

- Cause: Poor contrast or overlap

- Solutions:

* Adjust transparency

* Change theme settings

* Reposition table

* Modify color scheme

### Best Practices

1. ** Getting Started **

- Start with default settings

- Use "Both" alert condition

- Enable all timeframe checks

- Wait for bar close

- Monitor for a few days

2. ** Fine-Tuning **

- Adjust one setting at a time

- Document changes and results

- Test in different market conditions

- Find your optimal timeframe combination

- Balance sensitivity with reliability

3. ** Risk Management **

- Don't trade against major trends

- Confirm signals with price action

- Use appropriate position sizing

- Set clear stop losses

- Follow your trading plan

4. ** Regular Maintenance **

- Review settings weekly

- Adjust for market conditions

- Update color scheme for visibility

- Clean up chart regularly

- Maintain trading journal

## 6. Tips for Success

1. ** Entry Strategies **

- Wait for all timeframes to align

- Confirm with price action

- Use proper position sizing

- Consider market conditions

2. ** Exit Strategies **

- Trail stops using indicator levels

- Take partial profits at targets

- Honor your stop losses

- Don't fight the trend

3. ** Psychology **

- Stay disciplined with settings

- Don't override system signals

- Keep emotions in check

- Learn from each trade

4. ** Continuous Improvement **

- Record your trades

- Review performance regularly

- Adjust settings gradually

- Stay educated on markets

M-oscillator

Kalman Filter Oscillator v4The Kalman Filter Oscillator v4 is an advanced tool designed to help traders and investors identify trends more effectively while reducing the impact of market noise. As the latest iteration in its development, this version integrates improvements that make it more adaptive and precise, catering to the challenges of today’s financial markets.

This indicator operates on the principle of the Kalman filter, a well-regarded mathematical approach used for estimating the state of a dynamic system. By filtering out random fluctuations, it smooths price data to provide clearer insights into underlying trends. Unlike traditional methods such as moving averages, which often lag and can miss rapid shifts, the Kalman Filter Oscillator is reactive in real time, making it particularly suited for dynamic markets.

Version v4 builds on earlier versions by offering a refined combination of short-term and long-term trend analysis. Through adjustable parameters, traders can balance sensitivity to immediate price changes with a broader perspective of the market direction. Additionally, the oscillator incorporates a unique feature that tracks a price’s position relative to its recent highs and lows, which enhances its ability to pinpoint potential turning points or key market conditions.

The indicator’s value lies in its adaptability and practicality. Traders can use it to confirm trends, identify overbought or oversold conditions, or smooth out erratic price movements, reducing the likelihood of false signals. By presenting information in a clear and actionable format, it allows users to make better-informed decisions with greater confidence.

As of late 2024, the Kalman Filter Oscillator v4 represents a sophisticated yet user-friendly advancement in trend analysis. While not a one-size-fits-all solution, it serves as a valuable component in a trader’s toolkit, complementing other strategies and enhancing overall market understanding.

Ensemble Alerts█ OVERVIEW

This indicator creates highly customizable alert conditions and messages by combining several technical conditions into groups , which users can specify directly from the "Settings/Inputs" tab. It offers a flexible framework for building and testing complex alert conditions without requiring code modifications for each adjustment.

█ CONCEPTS

Ensemble analysis

Ensemble analysis is a form of data analysis that combines several "weaker" models to produce a potentially more robust model. In a trading context, one of the most prevalent forms of ensemble analysis is the aggregation (grouping) of several indicators to derive market insights and reinforce trading decisions. With this analysis, traders typically inspect multiple indicators, signaling trade actions when specific conditions or groups of conditions align.

Simplifying ensemble creation

Combining indicators into one or more ensembles can be challenging, especially for users without programming knowledge. It usually involves writing custom scripts to aggregate the indicators and trigger trading alerts based on the confluence of specific conditions. Making such scripts customizable via inputs poses an additional challenge, as it often involves complicated input menus and conditional logic.

This indicator addresses these challenges by providing a simple, flexible input menu where users can easily define alert criteria by listing groups of conditions from various technical indicators in simple text boxes . With this script, you can create complex alert conditions intuitively from the "Settings/Inputs" tab without ever writing or modifying a single line of code. This framework makes advanced alert setups more accessible to non-coders. Additionally, it can help Pine programmers save time and effort when testing various condition combinations.

█ FEATURES

Configurable alert direction

The "Direction" dropdown at the top of the "Settings/Inputs" tab specifies the allowed direction for the alert conditions. There are four possible options:

• Up only : The indicator only evaluates upward conditions.

• Down only : The indicator only evaluates downward conditions.

• Up and down (default): The indicator evaluates upward and downward conditions, creating alert triggers for both.

• Alternating : The indicator prevents alert triggers for consecutive conditions in the same direction. An upward condition must be the first occurrence after a downward condition to trigger an alert, and vice versa for downward conditions.

Flexible condition groups

This script features six text inputs where users can define distinct condition groups (ensembles) for their alerts. An alert trigger occurs if all the conditions in at least one group occur.

Each input accepts a comma-separated list of numbers with optional spaces (e.g., "1, 4, 8"). Each listed number, from 1 to 35, corresponds to a specific individual condition. Below are the conditions that the numbers represent:

1 — RSI above/below threshold

2 — RSI below/above threshold

3 — Stoch above/below threshold

4 — Stoch below/above threshold

5 — Stoch K over/under D

6 — Stoch K under/over D

7 — AO above/below threshold

8 — AO below/above threshold

9 — AO rising/falling

10 — AO falling/rising

11 — Supertrend up/down

12 — Supertrend down/up

13 — Close above/below MA

14 — Close below/above MA

15 — Close above/below open

16 — Close below/above open

17 — Close increase/decrease

18 — Close decrease/increase

19 — Close near Donchian top/bottom (Close > (Mid + HH) / 2)

20 — Close near Donchian bottom/top (Close < (Mid + LL) / 2)

21 — New Donchian high/low

22 — New Donchian low/high

23 — Rising volume

24 — Falling volume

25 — Volume above average (Volume > SMA(Volume, 20))

26 — Volume below average (Volume < SMA(Volume, 20))

27 — High body to range ratio (Abs(Close - Open) / (High - Low) > 0.5)

28 — Low body to range ratio (Abs(Close - Open) / (High - Low) < 0.5)

29 — High relative volatility (ATR(7) > ATR(40))

30 — Low relative volatility (ATR(7) < ATR(40))

31 — External condition 1

32 — External condition 2

33 — External condition 3

34 — External condition 4

35 — External condition 5

These constituent conditions fall into three distinct categories:

• Directional pairs : The numbers 1-22 correspond to pairs of opposing upward and downward conditions. For example, if one of the inputs includes "1" in the comma-separated list, that group uses the "RSI above/below threshold" condition pair. In this case, the RSI must be above a high threshold for the group to trigger an upward alert, and the RSI must be below a defined low threshold to trigger a downward alert.

• Non-directional filters : The numbers 23-30 correspond to conditions that do not represent directional information. These conditions act as filters for both upward and downward alerts. Traders often use non-directional conditions to refine trending or mean reversion signals. For instance, if one of the input lists includes "30", that group uses the "Low relative volatility" condition. The group can trigger an upward or downward alert only if the 7-period Average True Range (ATR) is below the 40-period ATR.

• External conditions : The numbers 31-35 correspond to external conditions based on the plots from other indicators on the chart. To set these conditions, use the source inputs in the "External conditions" section near the bottom of the "Settings/Inputs" tab. The external value can represent an upward, downward, or non-directional condition based on the following logic:

▫ Any value above 0 represents an upward condition.

▫ Any value below 0 represents a downward condition.

▫ If the checkbox next to the source input is selected, the condition becomes non-directional . Any group that uses the condition can trigger upward or downward alerts only if the source value is not 0.

To learn more about using plotted values from other indicators, see this article in our Help Center and the Source input section of our Pine Script™ User Manual.

Group markers

Each comma-separated list represents a distinct group , where all the listed conditions must occur to trigger an alert. This script assigns preset markers (names) to each condition group to make the active ensembles easily identifiable in the generated alert messages and labels. The markers assigned to each group use the format "M", where "M" is short for "Marker" and "x" is the group number. The titles of the inputs at the top of the "Settings/Inputs" tab show these markers for convenience.

For upward conditions, the labels and alert messages show group markers with upward triangles (e.g., "M1▲"). For downward conditions, they show markers with downward triangles (e.g., "M1▼").

NOTE: By default, this script populates the "M1" field with a pre-configured list for a mean reversion group ("2,18,24,28"). The other fields are empty. If any "M*" input does not contain a value, the indicator ignores it in the alert calculations.

Custom alert messages

By default, the indicator's alert message text contains the activated markers and their direction as a comma-separated list. Users can override this message for upward or downward alerts with the two text fields at the bottom of the "Settings/Inputs" tab. When the fields are not empty , the alerts use that text instead of the default marker list.

NOTE: This script generates alert triggers, not the alerts themselves. To set up an alert based on this script's conditions, open the "Create Alert" dialog box, then select the "Ensemble Alerts" and "Any alert() function call" options in the "Condition" tabs. See the Alerts FAQ in our Pine Script™ User Manual for more information.

Condition visualization

This script offers organized visualizations of its conditions, allowing users to inspect the behaviors of each condition alongside the specified groups. The key visual features include:

1) Conditional plots

• The indicator plots the history of each individual condition, excluding the external conditions, as circles at different levels. Opposite conditions appear at positive and negative levels with the same absolute value. The plots for each condition show values only on the bars where they occur.

• Each condition's plot is color-coded based on its type. Aqua and orange plots represent opposing directional conditions, and purple plots represent non-directional conditions. The titles of the plots also contain the condition numbers to which they apply.

• The plots in the separate pane can be turned on or off with the "Show plots in pane" checkbox near the top of the "Settings/Inputs" tab. This input only toggles the color-coded circles, which reduces the graphical load. If you deactivate these visuals, you can still inspect each condition from the script's status line and the Data Window.

• As a bonus, the indicator includes "Up alert" and "Down alert" plots in the Data Window, representing the combined upward and downward ensemble alert conditions. These plots are also usable in additional indicator-on-indicator calculations.

2) Dynamic labels

• The indicator draws a label on the main chart pane displaying the activated group markers (e.g., "M1▲") each time an alert condition occurs.

• The labels for upward alerts appear below chart bars. The labels for downward alerts appear above the bars.

NOTE: This indicator can display up to 500 labels because that is the maximum allowed for a single Pine script.

3) Background highlighting

• The indicator can highlight the main chart's background on bars where upward or downward condition groups activate. Use the "Highlight background" inputs in the "Settings/Inputs" tab to enable these highlights and customize their colors.

• Unlike the dynamic labels, these background highlights are available for all chart bars, irrespective of the number of condition occurrences.

█ NOTES

• This script uses Pine Script™ v6, the latest version of TradingView's programming language. See the Release notes and Migration guide to learn what's new in v6 and how to convert your scripts to this version.

• This script imports our new Alerts library, which features functions that provide high-level simplicity for working with complex compound conditions and alerts. We used the library's `compoundAlertMessage()` function in this indicator. It evaluates items from "bool" arrays in groups specified by an array of strings containing comma-separated index lists , returning a tuple of "string" values containing the marker of each activated group.

• The script imports the latest version of the ta library to calculate several technical indicators not included in the built-in `ta.*` namespace, including Double Exponential Moving Average (DEMA), Triple Exponential Moving Average (TEMA), Fractal Adaptive Moving Average (FRAMA), Tilson T3, Awesome Oscillator (AO), Full Stochastic (%K and %D), SuperTrend, and Donchian Channels.

• The script uses the `force_overlay` parameter in the label.new() and bgcolor() calls to display the drawings and background colors in the main chart pane.

• The plots and hlines use the available `display.*` constants to determine whether the visuals appear in the separate pane.

Look first. Then leap.

Monest Value Indicator (MVI)

Description

The Monest Value Indicator (MVI) is a modern oscillator designed to address common issues in traditional oscillators like RSI or MACD. Unlike classical oscillators, the MVI dynamically adjusts to relative price movements and market volatility, providing a transparent and reliable valuation for short-term trading decisions.

This indicator normalizes price data around a consensus line and accounts for market volatility using the Average True Range (ATR). It highlights overbought and oversold conditions, offering a unique perspective for traders.

Key Features

Dynamic Overbought/Oversold Levels : Highlights significant price extremes for better entry and exit signals. Volatility Normalization : Adapts to market conditions, ensuring consistent readings across various assets. Consensus-Based Valuation : Uses a moving average of the midrange price for baseline calculations. No Lag or Stickiness : Reacts promptly to price movements without getting stuck in extreme zones.

How It Works

Consensus Line :

Calculated as a 5-day moving average of the midrange:

Consensus = SMA((High + Low) / 2, 5) .

Offset OHLC Data :

All prices are adjusted relative to the consensus line:

Offset Price = Price - Consensus .

Volatility Normalization :

Adjusted prices are normalized using a 5-day ATR divided by 5:

Normalized Price = Offset Price / (ATR / 5) .

MVI Calculation :

The normalized closing price is plotted as the MVI.

Overbought/Oversold Levels :

Default levels are set at +8 (overbought) and -8 (oversold).

How to Use

Identifying Overbought/Oversold Conditions :

When the MVI crosses above +8 , the asset is overbought, signaling a potential reversal or pullback.

When the MVI drops below -8 , the asset is oversold, indicating a potential bounce or upward move.

Trend Confirmation :

Use the MVI to confirm trends by observing sustained movements above or below zero.

Combine with other trend indicators (e.g., Moving Averages) for robust analysis.

Alerts :

Set alerts for when the MVI crosses overbought or oversold levels to stay informed about potential trading opportunities.

Inputs

ATR Length : Default is 5. Adjust to modify the sensitivity of volatility normalization. Consensus Length : Default is 5. Change to tweak the baseline calculation.

Example

Overbought Signal : MVI exceeds +8 , indicating the asset may reverse from an overvalued position. Oversold Signal : MVI drops below -8 , suggesting the asset may recover from an undervalued state. Flat Market : MVI hovers near zero, indicating price consolidation.

Global Market Strength IndicatorThe Global Market Strength Indicator is a powerful tool for traders and investors. It helps compare the strength of various global markets and indices. This indicator uses the True Strength Index (TSI) to measure market strength.

The indicator retrieves price data for different markets and calculates their TSI values. These values are then plotted on a chart. Each market is represented by a different colored line, making it easy to distinguish between them.

One of the main benefits of this indicator is its comprehensive global view. It covers major indices and country-specific ETFs, giving users a broad perspective on global market trends. This wide coverage allows for easy comparison between different markets and regions.

The indicator is highly customizable. Users can adjust the TSI smoothing period to suit their preferences. They can also toggle the visibility of individual markets. This feature helps reduce chart clutter and allows for more focused analysis.

To use the indicator, apply it to your chart in TradingView. Adjust the settings as needed, and observe the relative positions and movements of the TSI lines. Lines moving higher indicate increasing strength in that market, while lines moving lower suggest weakening markets.

The chart includes reference lines at 0.5 and -0.5. These help identify potential overbought and oversold conditions. Markets with TSI values above 0.5 may be considered strong or potentially overbought. Those below -0.5 may be weak or potentially oversold.

By comparing the movements of different markets, users can identify which markets are leading or lagging. They can also spot potential divergences between related markets. This information can be valuable for identifying sector rotations or shifts in global market sentiment.

A dynamic legend automatically updates to show only the visible markets. This feature improves chart readability and makes it easier to interpret the data.

The Global Market Strength Indicator is a versatile tool that provides valuable insights into global market performance. It helps traders and investors identify trends, compare market performances, and make more informed decisions. Whether you're looking to spot emerging global trends or identify potential trading opportunities, this indicator offers a comprehensive solution for global market analysis.

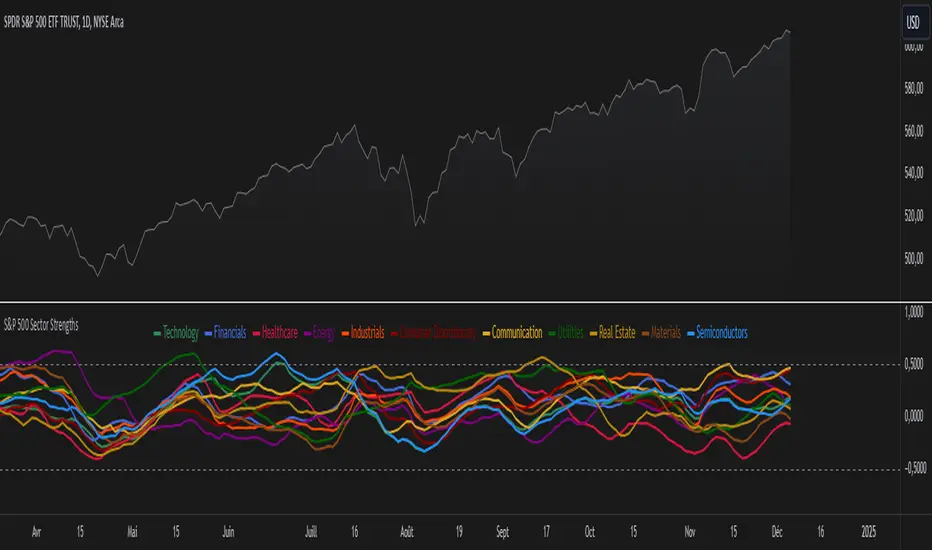

S&P 500 Sector StrengthsThe "S&P 500 Sector Strengths" indicator is a sophisticated tool designed to provide traders and investors with a comprehensive view of the relative performance of various sectors within the S&P 500 index. This indicator utilizes the True Strength Index (TSI) to measure and compare the strength of different sectors, offering valuable insights into market trends and sector rotations.

At its core, the indicator calculates the TSI for each sector using price data obtained through the request.security() function. The TSI, a momentum oscillator, is computed using a user-defined smoothing period, allowing for customization based on individual preferences and trading styles. The resulting TSI values for each sector are then plotted on the chart, creating a visual representation of sector strengths.

To use this indicator effectively, traders should focus on comparing the movements of different sector lines. Sectors with lines moving higher are showing increasing strength, while those with descending lines are exhibiting weakness. This comparative analysis can help identify potential investment opportunities and sector rotations. Additionally, when multiple sector lines move in tandem, it may signal a broader market trend.

The indicator includes dashed lines at 0.5 and -0.5, serving as reference points for overbought and oversold conditions. Sectors with TSI values above 0.5 might be considered overbought, suggesting caution, while those below -0.5 could be viewed as oversold, potentially indicating buying opportunities.

One of the key advantages of this indicator is its flexibility. Users can toggle the visibility of individual sectors and customize their colors, allowing for a tailored analysis experience. This feature is particularly useful when focusing on specific sectors or reducing chart clutter for clearer visualization.

The indicator's ability to provide a comprehensive overview of all major S&P 500 sectors in a single chart is a significant benefit. This consolidated view enables quick comparisons and helps in identifying relative strengths and weaknesses across sectors. Such insights can be invaluable for portfolio allocation decisions and in spotting emerging market trends.

Moreover, the dynamic legend feature enhances the indicator's usability. It automatically updates to display only the visible sectors, improving chart readability and interpretation.

By leveraging this indicator, market participants can gain a deeper understanding of sector dynamics within the S&P 500. This enhanced perspective can lead to more informed decision-making in sector allocation strategies and individual stock selection. The indicator's ability to potentially detect early trends by comparing sector strengths adds another layer of value, allowing users to position themselves ahead of broader market movements.

In conclusion, the "S&P 500 Sector Strengths" indicator is a powerful tool that combines technical analysis with sector comparison. Its user-friendly interface, customizable features, and comprehensive sector coverage make it an valuable asset for traders and investors seeking to navigate the complexities of the S&P 500 market with greater confidence and insight.

SMT Divergence ICT 01 [TradingFinder] Smart Money Technique🔵 Introduction

SMT Divergence (short for Smart Money Technique Divergence) is a trading technique in the ICT Concepts methodology that focuses on identifying divergences between two positively correlated assets in financial markets.

These divergences occur when two assets that should move in the same direction move in opposite directions. Identifying these divergences can help traders spot potential reversal points and trend changes.

Bullish and Bearish divergences are clearly visible when an asset forms a new high or low, and the correlated asset fails to do so. This technique is applicable in markets like Forex, stocks, and cryptocurrencies, and can be used as a valid signal for deciding when to enter or exit trades.

Bullish SMT Divergence : This type of divergence occurs when one asset forms a higher low while the correlated asset forms a lower low. This divergence is typically a sign of weakness in the downtrend and can act as a signal for a trend reversal to the upside.

Bearish SMT Divergence : This type of divergence occurs when one asset forms a higher high while the correlated asset forms a lower high. This divergence usually indicates weakness in the uptrend and can act as a signal for a trend reversal to the downside.

🔵 How to Use

SMT Divergence is an analytical technique that identifies divergences between two correlated assets in financial markets.

This technique is used when two assets that should move in the same direction move in opposite directions.

Identifying these divergences can help you pinpoint reversal points and trend changes in the market.

🟣 Bullish SMT Divergence

This divergence occurs when one asset forms a higher low while the correlated asset forms a lower low. This divergence indicates weakness in the downtrend and can signal a potential price reversal to the upside.

In this case, when the correlated asset is forming a lower low, and the main asset is moving lower but the correlated asset fails to continue the downward trend, there is a high probability of a trend reversal to the upside.

🟣 Bearish SMT Divergence

Bearish divergence occurs when one asset forms a higher high while the correlated asset forms a lower high. This type of divergence indicates weakness in the uptrend and can signal a potential trend reversal to the downside.

When the correlated asset fails to make a new high, this divergence may be a sign of a trend reversal to the downside.

🟣 Confirming Signals with Correlation

To improve the accuracy of the signals, use assets with strong correlation. Forex pairs like OANDA:EURUSD and OANDA:GBPUSD , or cryptocurrencies like COINBASE:BTCUSD and COINBASE:ETHUSD , or commodities such as gold ( FX:XAUUSD ) and silver ( FX:XAGUSD ) typically have significant correlation. Identifying divergences between these assets can provide a strong signal for a trend change.

🔵 Settings

Second Symbol : This setting allows you to select another asset for comparison with the primary asset. By default, "XAUUSD" (Gold) is set as the second symbol, but you can change it to any currency pair, stock, or cryptocurrency. For example, you can choose currency pairs like EUR/USD or GBP/USD to identify divergences between these two assets.

Divergence Fractal Periods : This parameter defines the number of past candles to consider when identifying divergences. The default value is 2, but you can change it to suit your preferences. This setting allows you to detect divergences more accurately by selecting a greater number of candles.

Bullish Divergence Line : Displays a line showing bullish divergence from the lows.

Bearish Divergence Line : Displays a line showing bearish divergence from the highs.

Bullish Divergence Label : Displays the "+SMT" label for bullish divergences.

Bearish Divergence Label : Displays the "-SMT" label for bearish divergences.

🔵 Conclusion

SMT Divergence is an effective tool for identifying trend changes and reversal points in financial markets based on identifying divergences between two correlated assets. This technique helps traders receive more accurate signals for market entry and exit by analyzing bullish and bearish divergences.

Identifying these divergences can provide opportunities to capitalize on trend changes in Forex, stocks, and cryptocurrency markets. Using SMT Divergence along with risk management and confirming signals with other technical analysis tools can improve the accuracy of trading decisions and reduce risks from sudden market changes.

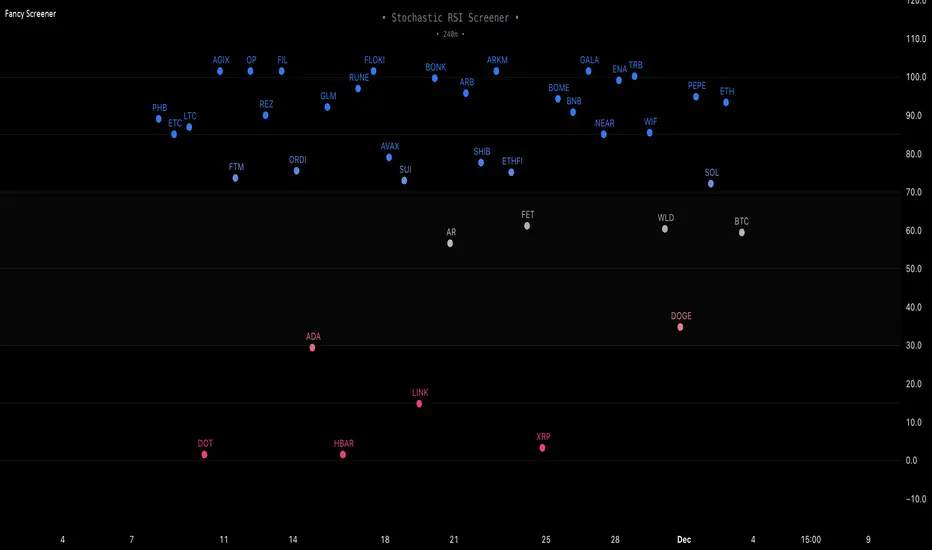

Fancy Oscillator Screener [Daveatt]⬛ OVERVIEW

Building upon LeviathanCapital original RSI Screener (), this enhanced version brings comprehensive technical analysis capabilities to your trading workflow. Through an intuitive grid display, you can monitor multiple trading instruments simultaneously while leveraging powerful indicators to identify market opportunities in real-time.

⬛ FEATURES

This script provides a sophisticated visualization system that supports both cross rates and heat map displays, allowing you to track exchange rates and percentage changes with ease. You can organize up to 40 trading pairs into seven customizable groups, making it simple to focus on specific market segments or trading strategies.

If you overlay on any circle/asset on the chart, you'll see the accurate oscillator value displayed for that asset

⬛ TECHNICAL INDICATORS

The screener supports the following oscillators:

• RSI - the oscillator from the original script version

• Awesome Oscillator

• Chaikin Oscillator

• Stochastic RSI

• Stochastic

• Volume Oscillator

• CCI

• Williams %R

• MFI

• ROC

• ATR Multiple

• ADX

• Fisher Transform

• Historical Volatility

• External : connect your own custom oscillator

⬛ DYNAMIC SCALING

One of the key improvements in this version is the implementation of dynamic chart scaling. Unlike the original script which was optimized for RSI's 0-100 range, this version automatically adjusts its scale based on the selected oscillator.

This adaptation was necessary because different indicators operate on vastly different numerical ranges - for instance, CCI typically ranges from -200 to +200, while Williams %R operates from -100 to 0.

The dynamic scaling ensures that each oscillator's data is properly displayed within its natural range, making the visualization both accurate and meaningful regardless of which indicator you choose to use.

⬛ ALERTS

I've integrated a comprehensive alert system that monitors both overbought and oversold conditions.

Users can now set custom threshold levels for their alerts.

When any asset in your monitored group crosses these thresholds, the system generates an alert, helping you catch potential trading opportunities without constant manual monitoring.

em will help you stay informed of market movements and potential trading opportunities.

I hope you'll find this tool valuable in your trading journey

All the BEST,

Daveatt

Trend Stability Index (TSI)Overview

The Trend Stability Index (TSI) is a technical analysis tool designed to evaluate the stability of a market trend by analyzing both price movements and trading volume. By combining these two crucial elements, the TSI provides traders with insights into the strength and reliability of ongoing trends, assisting in making informed trading decisions.

Key Features

• Dual Analysis: Integrates price changes and volume fluctuations to assess trend stability.

• Customizable Periods: Allows users to set evaluation periods for both trend and volume based on their trading preferences.

• Visual Indicators: Displays the Trend Stability Index as a line chart, highlights neutral zones, and uses background colors to indicate trend stability or instability.

Configuration Settings

1. Trend Length (trendLength)

• Description: Determines the number of periods over which the price stability is evaluated.

• Default Value: 15

• Usage: A longer trend length smooths out short-term volatility, providing a clearer picture of the overarching trend.

2. Volume Length (volumeLength)

• Description: Sets the number of periods over which trading volume changes are assessed.

• Default Value: 15

• Usage: Adjusting the volume length helps in capturing significant volume movements that may influence trend strength.

Calculation Methodology

The Trend Stability Index is calculated through a series of steps that analyze both price and volume changes:

1. Price Change Rate (priceChange)

• Calculation: Utilizes the Rate of Change (ROC) function on the closing prices over the specified trendLength.

• Purpose: Measures the percentage change in price over the trend evaluation period, indicating the direction and momentum of the price movement.

2. Volume Change Rate (volumeChange)

• Calculation: Applies the Rate of Change (ROC) function to the trading volume over the specified volumeLength.

• Purpose: Assesses the percentage change in trading volume, providing insight into the conviction behind price movements.

3. Trend Stability (trendStability)

• Calculation: Multiplies priceChange by volumeChange.

• Purpose: Combines price and volume changes to gauge the overall stability of the trend. A higher positive value suggests a strong and stable trend, while negative values may indicate trend weakness or reversal.

4. Trend Stability Index (TSI)

• Calculation: Applies a Simple Moving Average (SMA) to the trendStability over the trendLength period.

• Purpose: Smooths the trend stability data to create a more consistent and interpretable index.

Trend/Ranging Determination

• Stable Trend (isStable)

• Condition: When the TSI value is greater than 0.

• Interpretation: Indicates that the current trend is stable and likely to continue in its direction.

• Unstable Trend / Range-bound Market

• Condition: When the TSI value is less than or equal to 0.

• Interpretation: Suggests that the trend may be weakening, reversing, or that the market is moving sideways without a clear direction.

Visualization

The TSI indicator employs several visual elements to convey information effectively:

1. TSI Line

• Representation: Plotted as a blue line.

• Purpose: Displays the Trend Stability Index values over time, allowing traders to observe trend stability dynamics.

2. Neutral Horizontal Line

• Representation: A gray horizontal line at the 0 level.

• Purpose: Serves as a reference point to distinguish between stable and unstable trends.

3. Background Color

• Stable Trend: Green background with 80% transparency when isStable is true.

• Unstable Trend: Red background with 80% transparency when isStable is false.

• Purpose: Provides an immediate visual cue about the current trend’s stability, enhancing the interpretability of the indicator.

Usage Guidelines

• Identifying Trend Strength: Utilize the TSI to confirm the strength of existing trends. A consistently positive TSI suggests strong trend momentum, while a negative TSI may signal caution or a potential reversal.

• Volume Confirmation: The integration of volume changes helps in validating price movements. Significant price changes accompanied by corresponding volume shifts can reinforce the reliability of the trend.

• Entry and Exit Signals: Traders can use crossovers of the TSI with the neutral line (0 level) as potential entry or exit points. For instance, a crossover from below to above 0 may indicate a bullish trend initiation, while a crossover from above to below 0 could suggest bearish momentum.

• Combining with Other Indicators: To enhance trading strategies, consider using the TSI in conjunction with other technical indicators such as Moving Averages, RSI, or MACD for comprehensive market analysis.

Example Scenario

Imagine analyzing a stock with the following observations using the TSI:

• The TSI has been consistently above 0 for the past 30 periods, accompanied by increasing trading volume. This scenario indicates a strong and stable uptrend, suggesting that buying opportunities may be favorable.

• Conversely, if the TSI drops below 0 while the price remains relatively flat and volume decreases, it may imply that the current trend is losing momentum, and the market could be entering a consolidation phase or preparing for a trend reversal.

Conclusion

The Trend Stability Index is a valuable tool for traders seeking to assess the reliability and strength of market trends by integrating price and volume dynamics. Its customizable settings and clear visual indicators make it adaptable to various trading styles and market conditions. By incorporating the TSI into your trading analysis, you can enhance your ability to identify and act upon stable and profitable trends.

True Range Trend StrengthThis script is designed to analyze trend strength using True Range calculations alongside Donchian Channels and smoothed moving averages. It provides a dynamic way to interpret market momentum, trend reversals, and anticipate potential entry points for trades.

Key Functionalities:

Trend Strength Oscillator:

Calculates trend strength based on the difference between long and short momentum derived from ATR (Average True Range) adjusted stop levels.

Smooths the trend strength using a simple moving average for better readability.

Donchian Channels on Trend Strength Oscillator:

Plots upper and lower Donchian Channels on the smoothed trend strength oscillator.

Traders can use these levels to anticipate breakout points and determine the strength of a trend.

Zero-Cross Shading:

Highlights bullish and bearish zones with shaded backgrounds:

Green for bullish zones where smoothed trend strength is above zero.

Red for bearish zones where smoothed trend strength is below zero.

Moving Averages for Oscillator:

Overlays fast and slow moving averages on the oscillator to provide crossover signals:

Fast MA Cross Above Slow MA: Indicates bullish momentum.

Fast MA Cross Below Slow MA: Indicates bearish momentum.

Alerts:

Alerts are available for MA crossovers, allowing traders to receive timely notifications about potential trend reversals or continuation signals.

Anticipating Entries with Donchian Channels:

The integration of Donchian Channels offers an edge in anticipating excellent trade entries.

Traders can use the oscillator's position relative to the channels to gauge oversold/overbought conditions or potential breakouts.

Use Case:

This script is particularly useful for traders looking to:

Identify the strength and direction of market trends.

Time entries and exits based on dynamic Donchian Channel levels and trend strength analysis.

Incorporate moving averages and visual cues for better decision-making.

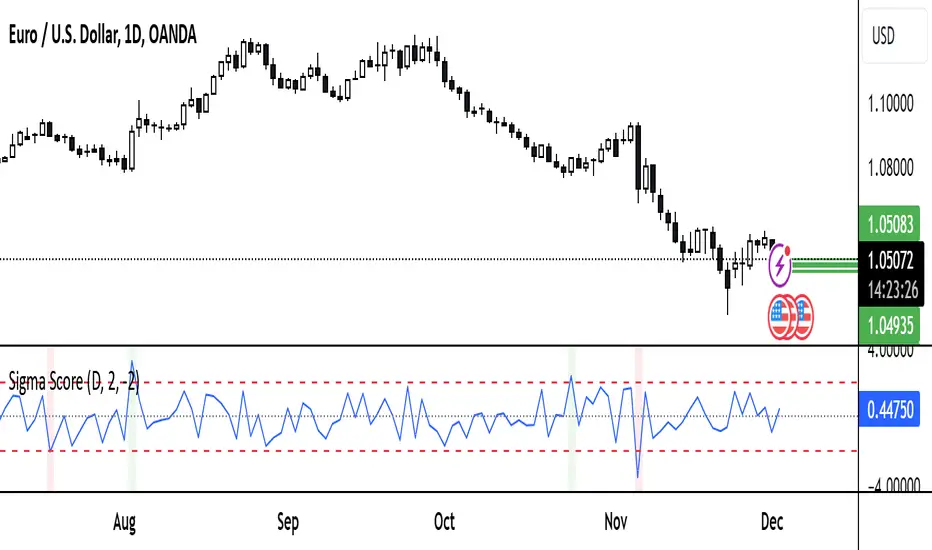

Sigma ScoreFunction and Purpose

The Sigma Score indicator is a tool for analyzing volatility and identifying unusual price movements of a financial instrument over a specified timeframe. It calculates the "Sigma Score," which measures how far the current price change deviates from its historical average in terms of standard deviations. This helps identify potential extremes and unusual market conditions.

Features

Timeframe Control

Users can select the desired timeframe for analysis (e.g., minutes, hours, days). This makes the indicator adaptable to various trading styles:

Supported timeframes: Minutes (M1, M5, M10, M15), Hours (H1, H4, H12), Days (D), Weeks (W), Months (M).

Sigma Score Calculation

The indicator computes the logarithmic return between consecutive price values.

It calculates a simple moving average (SMA) and the standard deviation (StDev) of these returns.

The Sigma Score is derived as the difference between the current return and the average, divided by the standard deviation.

Visual Representation

Sigma Score Plot: The Sigma Score is displayed as a line.

Horizontal Threshold Lines:

A middle line (0) for reference.

Upper and lower threshold lines (default: 2.0 and -2.0) for highlighting extremes.

Background Highlighting:

Green for values above the upper threshold (positive deviations).

Red for values below the lower threshold (negative deviations).

Custom Settings

Timeframe

Select the timeframe for analysis using a dropdown menu (default: D for daily).

Thresholds

Upper Threshold: Default = 2.0 (positive extreme area).

Lower Threshold: Default = -2.0 (negative extreme area).

Both values can be adjusted to modify the indicator's sensitivity.

Use Cases

Identifying Extremes: Values above or below the thresholds can signal unusual market conditions, such as overbought or oversold areas.

Analyzing Market Anomalies: The Sigma Score quantifies how unusual a price movement is based on historical data.

Visual Aid: Threshold lines and background highlighting simplify the interpretation of boundary conditions.

Notes and Limitations

Timeframe Dependency: Results may vary depending on the selected timeframe. Shorter timeframes highlight short-term movements, while longer timeframes capture broader trends.

Volatility Sensitivity: The indicator is sensitive to changes in market volatility. Sudden price swings may produce extreme Sigma values.

Summary

The Sigma Score indicator is a powerful tool for traders and analysts to quickly identify unusual market conditions and make informed decisions. Its flexibility in adjusting timeframes and thresholds makes it a versatile addition to any trading strategy.

USDJPY vanilla indicatorThis Pine Script indicator, USDJPY Strength Index, helps traders evaluate the strength and momentum of the USD/JPY currency pair. It combines the strength of the US Dollar Index (DXY), the inverse of the Japanese Yen Index (JPYX), and the trend of USD/JPY based on moving averages.

Key Features:

1. Strength Measurement: Calculates a score between 0–100 to indicate USD/JPY momentum.

• Above 70: Strong bullish signal (uptrend likely).

• Below 30: Strong bearish signal (downtrend likely).

2. Trend Analysis: Uses 21 EMA and 50 EMA differences to assess trend direction and strength.

3. Visual Indicators:

• Blue line: USDJPY Strength Index.

• Orange line: 50-period EMA of the index for longer-term trends.

• Background colors: Green (bullish) and red (bearish) highlight strong momentum zones.

This indicator provides clear signals to help traders make informed buy or sell decisions for the USD/JPY pair.

tipp: use horizontal line for mark last low and high. when the blue line comes back again you must be ready for open position if the line bounce back. use engulfing pattern for extra confirmation.

Detrended Price Oscillator [NexusSignals]Detrended Price Oscillator (DPO) is a detrended price oscillator, used in technical analysis, strips out price trends in an effort to estimate the length of price cycles from peak to peak or trough to trough.

DPO is not a momentum indicator, instead highlights peaks and troughs in price, which are used to estimate buy and sell points in line with the historical cycle. (cf. to investopedia)

DPO indicator made by NexusSignals components :

a filled area that allow users to see easy the trend of an asset;

a sma moving average on chart (default length is 20)

a 20 sma on oscillator, both ma's are color coded to show uptrend / downtrend

a donchian channel applied to the dpo to show breakouts, breakdowns and resistances/support, reversals

few alerts for price crossing above ma, cross above the 0 dpo line, and for cross above and below the donchian channels top and bottom

How you can use DPO indicator ?

The detrended price oscillator (DPO) can be used for measuring the distance between peaks and troughs in the indicator that may help traders to make future decisions as they can locate the most recent trough and determine when the next one may occur in the meassured distance on oscillator between peaks and troughs.

You can use the indicator to find the potential price reversals, for example when the price of an asset is in a bearish trend and the dpo is bouncing from the donchian channel bottom, that may be a potential swing low for that asset, same thing in a bullish trend when the dpo rejecting at top of donchian channel may be a trend reversal, a pullback or swing high.

When DPO is above the 0 trend is in an uptrend and when dpo is below the zero the asset is possible to move into a downtrend.

Also crosses of DPO above and below the DPO moving average may signalising a trend change.

Smoothed Renko OscillatorSMOOTHED RENKO OSCILLATOR

Technical indicator combining Renko charting with oscillator mechanics for price momentum analysis. Brick size determines sensitivity of price movement detection, with adjustable smoothing for noise reduction.

Parameters include brick size (default 10), smoothing period (5), oscillator period (14), and smoothing type selection (EMA/SMA/WMA). Values above zero indicate bullish momentum, below zero bearish momentum, with ±40-50 marking potential reversal zones. Zero-line crossovers suggest trend changes.

Larger brick settings reduce noise but delay signals, while smaller bricks increase sensitivity. EMA smoothing provides faster response, while SMA/WMA offer more stable readings. The indicator supports trend confirmation, momentum measurement, divergence analysis, and entry/exit timing.

Best used in conjunction with price action and additional indicators for comprehensive market analysis. Particularly effective in trending markets for momentum confirmation and potential reversal identification.

Delta OscillatorAn advanced technical indicator that helps traders identify buying and selling pressure in the market by analyzing volume-based price movements.

Features

Real-time calculation of buying and selling volume

Cumulative delta conversion into oscillator format (-50 to +50 range)

Color-coded visualization (green for buying pressure, red for selling pressure)

Customizable period length for calculations

How It Works

The indicator:

Calculates buying/selling volume based on price direction

Accumulates delta over time

Normalizes values into oscillator format

Displays results as a colored line chart

Trading Applications

Identify potential trend reversals

Measure buying/selling momentum

Confirm price action signals

Spot divergences with price

Installation

Copy the provided Pine Script code

Open TradingView Chart → Pine Editor

Paste the code and click "Add to Chart"

Settings

Period: Adjustable timeframe for calculations (default: 14)

Visualization: Line width and colors can be customized

Market Session Times and Volume [Market Spotter]Market Session Times and Volume

Market Session Times

Inputs

The inputs tab consists of timezone adjustment which would be the chosen timezone for the plotting of the market sessions based on the market timings.

Further it contains settings for each box to show/hide and change box colour and timings for Asian, London and New York Sessions.

How it works

The indicator primarily works by marking the session highs and lows for the chosen time in the inputs, each of the sessions can be input a custom time value which would plot the box. It helps to identify the important price levels and the trading range for each individual session.

The midpoint of each session is marked with a dashed line. The indicator also marks a developing session while it being formed as well to identify potential secondary levels.

Usage

It can be used to trade session breakouts, false breaks and also divide the daily movement into parts and identify possible patterns while trading.

2. Volumes

Inputs

The volume part has 2 inputs - Smoothing and Normalisation. The smoothing period can simply be used to take in charge volumes of last X bars and normalisation can be used for calculating relative volumes based on last Y bars.

How it works

The indicator takes into account the buy and sell volumes of last X bars and then displays that as a relative smoothed volume which helps to identify longer term build or distribution of volume. It plots the positive volume from 0 to 100 and negative volume from 0 to -100 which has been normalised. The colors identify gradual increase or decrease in volumes

Usage

It can also be used to trade volume spikes well and can identify potential market shifts

BTC vs Altcoin CorrelationThis Pine Script indicator calculates and visualizes the rolling correlation between Bitcoin (BTC) and a selected altcoin, while providing insights into the percentage of time the correlation remains above a user-defined threshold. Users can independently configure the correlation calculation period and the lookback period for measuring the percentage of time above the threshold. The correlation is displayed as a color-coded line: green when above the threshold and red otherwise, with a dashed horizontal line marking the threshold level. A dynamic table displays the current correlation value and the percentage of time spent above the threshold within the specified period, enabling quick evaluation of correlation dynamics between BTC and the chosen altcoin.

RSI Difference (Fast and Slow)Introduction

Oscillators like the RSI are fundamental tools for identifying trends in financial markets. Their ability to measure price momentum allows traders to detect overbought, oversold levels, and divergences, anticipating trend changes. Are there ways to improve the use of traditional RSI? How can we obtain more detailed information about current trends? This indicator answers these questions by expanding the functionalities of the traditional RSI and offering an additional tool for analysis.

How does it work?

This indicator provides a framework for trend analysis based on the following setup:

Fast RSI

Slow RSI

SMA of the fast RSI

SMA of the slow RSI

Histogram

Custom Indicator Settings

My preferred configuration is based on the 13 and 55 moving averages. The rest of the setup is as follows:

I typically use the 13 and 55 moving averages to configure both the RSI and short- and long-term moving averages.

Interpretation and Signals: Including a Long-Period RSI

Including a long-period RSI helps identify key patterns in market behavior. Crossovers between the two can be used to establish entry patterns:

If the fast RSI crosses above the slow RSI, this could indicate a long-entry pattern.

If the fast RSI crosses below the slow RSI, this could indicate a short-entry pattern.

Interpretation and Signals: Including Moving Averages

Including moving averages for both the short- and long-period RSI can help identify the base trend of the movement and, consequently:

Avoid false signals.

Trade in favor of the trend.

A simple way to start working with these is to use the crossover of the moving averages to identify the current trend:

If the short-period SMA is above the long-period SMA, the trend is bullish.

If the short-period SMA is below the long-period SMA, the trend is bearish.

Interpretation and Signals: The Histogram

The histogram represents the difference between the moving averages. If the histogram is positive, the short average is above the long average. If the histogram is below zero, the short average is below the long average. Divergences with price provide signals of potential exhaustion in the movement, indicating a possible reversal.

Indicator Details

This indicator builds upon the traditional RSI by integrating additional features that enhance its utility for traders. Here’s how each component is calculated and how they contribute to the originality of the script:

Fast RSI and Slow RSI: The fast RSI is calculated using a shorter lookback period, allowing it to capture rapid changes in momentum. The slow RSI uses a longer period to smooth out fluctuations and provide a broader view of the trend. These two RSIs work together to identify significant momentum shifts.

SMA of RSI values: The simple moving averages (SMA) of the fast and slow RSI help filter out noise and provide clear crossover signals. The SMAs are calculated using standard formulas but applied to the RSI values rather than price data, which adds a layer of insight into momentum trends.

Histogram calculation: The histogram represents the difference between the SMA of the fast RSI and the SMA of the slow RSI. This value gives a visual representation of the convergence or divergence of momentum. When the histogram crosses zero, it signifies a potential shift in the underlying trend.

This indicator combines multiple layers of analysis: fast and slow momentum, trend confirmation through SMAs, and divergence detection via the histogram. This multi-dimensional approach provides traders with a more comprehensive tool for trend analysis and decision-making.

Conclusion

This article has explored how to use this indicator to identify trends, leverage entry patterns, and analyze divergences by combining the fast RSI, slow RSI, their moving averages, and a histogram. Additionally, I’ve detailed how I usually interpret this indicator:

Identifying RSI patterns to anticipate momentum changes.

Using SMAs to confirm base trends.

Leveraging the histogram to detect divergences and potential price reversals.

Cryptocurrency StrengthMulti-Currency Analysis: Monitor up to 19 different currencies simultaneously, including major pairs like USD, EUR, JPY, and GBP, as well as emerging market currencies such as CNY, INR, and BRL.

Customizable Display: Easily toggle the visibility of each currency and personalize their colors to suit your preferences, allowing for a tailored analysis experience.

Real-Time Strength Measurement: The indicator calculates and displays the relative strength of each currency in real-time, helping you identify potential trends and trading opportunities.

Clear Visual Representation: With color-coded lines and a dynamic legend, the indicator presents complex currency relationships in an easy-to-understand format.

Advantages

Comprehensive Market View: Gain insights into the broader forex market dynamics by analyzing multiple currencies at once.

Trend Identification: Quickly spot strong and weak currencies, aiding in the identification of potential trending pairs.

Divergence Detection: Use the indicator to identify divergences between currency strength and price action, potentially signaling reversals or continuation patterns.

Flexible Time Frames: Apply the indicator across various time frames to align with your trading strategy, from intraday to long-term analysis.

Enhanced Decision Making: Make more informed trading decisions by understanding the relative strength of currencies involved in your trades.

Unique Qualities

TSI-Based Calculations: Utilizes the True Strength Index for a more nuanced and responsive measure of currency strength compared to simple price-based indicators.

Adaptive Legend: The indicator features a dynamic legend that updates automatically based on the selected currencies, ensuring a clutter-free and relevant display.

Emerging Market Inclusion: Unlike many standard currency strength indicators, this tool includes a wide range of emerging market currencies, providing a truly global perspective.

Whether you're a seasoned forex trader or just starting out, this Currency Strength Indicator offers valuable insights that can complement your existing strategy and potentially improve your trading outcomes. Its combination of comprehensive analysis, customization options, and clear visualization makes it an essential tool for navigating the complex world of currency trading.

Currency StrengthThis innovative Currency Strength Indicator is a powerful tool for forex traders, offering a comprehensive and visually intuitive way to analyze the relative strength of multiple currencies simultaneously. Here's what makes this indicator stand out:

Extensive Currency Coverage

One of the most striking features of this indicator is its extensive coverage of currencies. While many similar tools focus on just the major currencies, this indicator includes:

Major currencies: USD, EUR, JPY, GBP, CHF, CAD, AUD, NZD

Additional currencies: CNY, HKD, KRW, MXN, INR, RUB, SGD, TRY, BRL, ZAR, THB

This wide range allows traders to gain insights into a broader spectrum of the forex market, including emerging markets and less commonly traded currencies.

Unique Visual Presentation

The indicator boasts a clear and user-friendly interface:

Each currency is represented by a distinct colored line for easy identification

A legend is prominently displayed at the top of the chart, using color-coded labels for quick reference

Users can customize which currencies to display, allowing for a tailored analysis

This clean, organized presentation enables traders to quickly grasp the relative strengths of different currencies at a glance.

Robust Measurement Methodology

The indicator employs the True Strength Index (TSI) to calculate currency strength, which provides several advantages:

TSI is a momentum oscillator that shows both trend direction and overbought/oversold conditions

It uses two smoothing periods (fast and slow), which helps filter out market noise and provides more reliable signals

The indicator calculates TSI for each currency index (e.g., DXY for USD, EXY for EUR), ensuring a comprehensive strength measurement

By using TSI, this indicator offers a more nuanced and accurate representation of currency strength compared to simpler moving average-based indicators.

Customization and Flexibility

Traders can fine-tune the indicator to suit their needs:

Adjustable TSI parameters (fast and slow periods)

Ability to show/hide specific currencies

Customizable color scheme for each currency line

Practical Applications

This Currency Strength Indicator can be used for various trading strategies:

Identifying potential trend reversals when a currency reaches extreme overbought or oversold levels

Spotting divergences between currency pairs

Confirming trends across multiple timeframes

Enhancing multi-pair trading strategies

By providing a clear, comprehensive, and customizable view of currency strength across a wide range of currencies, this indicator equips traders with valuable insights for making informed trading decisions in the complex world of forex.

Adaptive DEMA Momentum Oscillator (ADMO)Overview:

The Adaptive DEMA Momentum Oscillator (ADMO) is an open-source technical analysis tool developed to measure market momentum using a Double Exponential Moving Average (DEMA) and adaptive standard deviation. By dynamically combining price deviation from the moving average with normalized standard deviation, ADMO provides traders with a powerful way to interpret market conditions.

Key Features:

Double Exponential Moving Average (DEMA):

The core calculation of the indicator is based on DEMA, which is known for being more responsive to price changes compared to traditional moving averages. This makes the ADMO capable of capturing trend momentum effectively.

Standard Deviation Integration:

A normalized standard deviation is used to adaptively weight the oscillator. This makes the indicator more sensitive to market volatility, enhancing responsiveness during high volatility and reducing sensitivity during calmer periods.

Oscillator Representation:

The final oscillator value is derived from the combination of the DEMA-based Z-score and the normalized standard deviation. This final value is visualized as a color-coded histogram, reflecting bullish or bearish momentum.

Color-Coded Histogram:

Bullish Momentum: Values above zero are colored using a customizable bullish color (default: light green).

Bearish Momentum: Values below zero are colored using a customizable bearish color (default: red).

How It Works:

Inputs:

DEMA Length: Defines the period used for calculating the Double Exponential Moving Average. It can be adjusted from 1 to 200 to suit different trading styles.

Standard Deviation Length: Sets the lookback period for standard deviation calculations, which influences the responsiveness of the oscillator.

Standard Deviation Weight (StdDev Weight): Controls the weight given to the normalized standard deviation, allowing customization of the oscillator's sensitivity to volatility.

Calculation Steps:

Double Exponential Moving Average Calculation:

The DEMA is calculated using two exponential moving averages, which helps in reducing lag compared to a simple moving average.

Z-score Calculation:

The Z-score is derived by comparing the difference between the DEMA and its smoothed average (LSMA) to the standard deviation. This indicates how far the current value is from the mean in units of standard deviation.

Normalized Standard Deviation:

The standard deviation is normalized by subtracting the mean standard deviation and dividing by the standard deviation of the values. This helps to make the oscillator adaptive to recent changes in volatility.

Final Oscillator Value:

The final value is calculated by multiplying the Z-score with a factor based on the normalized standard deviation, resulting in a momentum indicator that adapts to different market conditions.

Visualization:

Histogram: The oscillator is plotted as a histogram, with color-coded bars showing the strength and direction of market momentum.

Positive (bullish) values are shown in green, indicating upward momentum.

Negative (bearish) values are shown in red, indicating downward momentum.

Zero Line: A zero line is plotted to provide a reference point, helping users quickly determine whether the current momentum is bullish or bearish.

Example Use Cases:

Momentum Identification:

ADMO helps identify the current market momentum by dynamically adapting to changes in market volatility. When the histogram is above zero and green, it indicates bullish conditions, whereas values below zero and red suggest bearish momentum.